With Seattle’s economy still strong, the downturn isn’t caused by layoffs & defaulting mortgages. The fabulous bubble has run out of steam on its own.

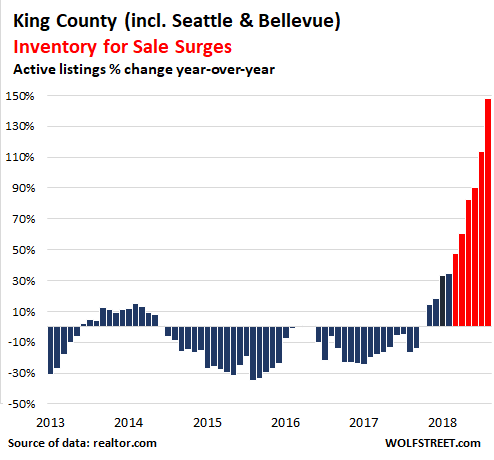

Inventory of houses and condos for sale in King County – which includes Seattle and Bellevue but does not include Tacoma – surged 148% in December, compared to December last year, to 4,017 active listings, according to data by the National Association of Realtors.

Active listings started piling up in the spring 2018 when levels were still very low. By July, when active listings reached the highest level since October 2014, the underlying dynamics of the housing market in King County had clearly changed direction. Since then, active listings exploded higher. This chart shows the year-over-year percentage changes, with the red bars denoting the new era of bubble trouble (all data via the National Association of Realtors at realtor.com):

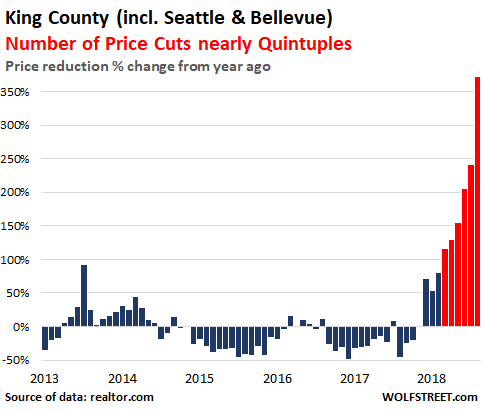

Surging inventories mean that sellers have to actually compete for buyers, rather than just trying to fend off jostling buyers during crazy bidding wars, which are now a quaint memory of the past. And motivated sellers compete by trying to get the price to where the buyers are. When the price is right, the property will sell quickly. But when the price is based on some aspirations from yesteryear, the property will sit. So the game of cutting listing prices has commenced.

The listing price is the advertised price of the property. And in December, price cuts exploded, skyrocketing by 372% from December 2017. This chart shows the year-over-year percentage change for each month. Bubble trouble in red:

December can be a squirrely month for real estate, with the two holiday weeks mucking up the normal process of business. Sellers pull properties off the market. Buyers are scarce because they have other things to do, etc. So it’s important to compare December to December. And we do.

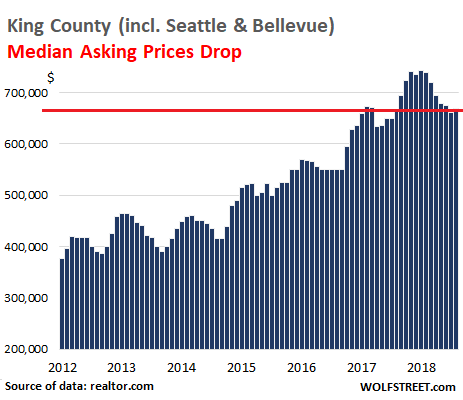

And these price reductions impact the median listing price – the dividing line, where half the properties are advertised for more, and half for less. It differs from the median selling price which is determined by closed home sales.

In King County, the median listing price peaked in May at $742,000. It then dropped six months in a row and ticked up one notch in December, to $668,550, just above where it had first been in May 2017. It is down $73,450 or 9.9% from the peak:

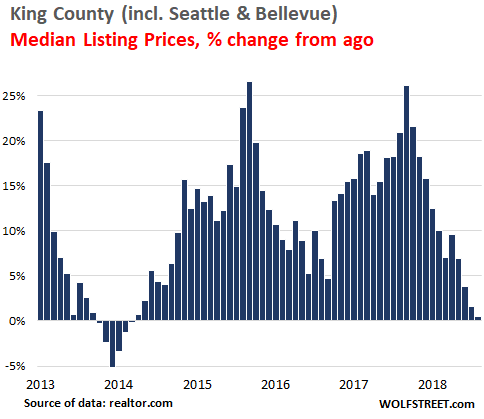

The double-digit year-over-year increases in asking prices during the heyday of the bubble were whittled down months after month. By December 2018, the year-over-year increase was down to almost nothing (0.5%):

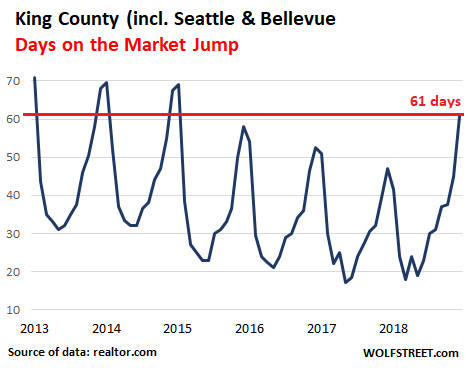

And the time it takes to sell a property has spiked to 61 days in December, up 30% from 47 days in December 2017, and the longest period for any month since January 2015. Note the strong seasonality with December generally being the slowest month:

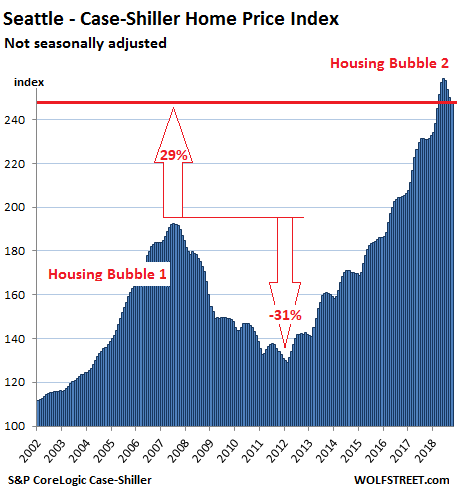

These dynamics have made an impact on selling prices – the prices at which properties are actually sold and the sales are closed. Even the Case-Shiller Home Price Index, which is a rolling three-month average and lags about three months, is showing that impact. The most recent reading, released on December 26, covers August, September, and October. After spiking for months into June, prices turned around and dropped 4.4% in four months, the biggest four-month drop since December 2011 during Housing Bust 1:

But in Seattle, as in the Bay Area, the economy is still strong, and this housing downturn has not been caused by people losing their jobs and defaulting on their mortgages. Instead, this fabulous housing bubble is just running out of steam on its own, after having outrun household incomes for years. It’s weighed down too by higher mortgage rates – though, ironically, given the deterioration in the housing market, mortgage rates have been inching down for two months.

In Silicon Valley and San Francisco, the housing downturn commenced over the summer, but this time it’s not a result of a tech bust. That tech bust hasn’t happened yet. Read… Housing Bubble Trouble in Silicon Valley & San Francisco

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Can you do a graph of total inventory month over month for the past decade? Although inventory has surged, it’s still pretty low historically.

Hey, this is not the depth of the housing bust of 2011. This is just the turning point at the peak of the bubble. Think 2006-07.

Check out seattlebubble.com – historical inventory is actually front page. Here is a link to the plot: https://seattlebubble.com/blog/wp-content/uploads/2019/01/KingCoSFHInventory_2018-12.png

I appreciate this site, but unfortunately many data series presented don’t cover the last recession. The more data the better!

Yikes, that’s a bad graph.

That’s definitely an interesting graph. I notice that even during the 2000-2006 boom period, inventories were higher than anything after 2012.

My gut says this has a lot to do with fundamental market changes … 2006 and prior you had ordinary people using ever more aggressive loans to chase these properties. Post 2012 the government gave up on ordinary buyers and turned to hedge funds, as well as allowing the banks to hide vacant homes in inventory much easier.

If I’m right, then data should show a much larger number of home sales pre-2006 than we saw in the post 2012 run-up.

Different sales volumes and different buyers means you can’t compare the old inventory levels to the new ones because sales and inventories won’t come up that high again – we’re simply in a world of smaller inventories and less buyers. To get back to prior sales volumes, we would have to allow prices to fall enough so that median income people can buy property again.

The trends that Wolf points out certainly matter, and the correction in housing will likely be significant, but there will be a floor built by hedge funds and stretching double-median-income earners that will suck up any remaining inventory. Median income earners with steady jobs might be able to afford homes with 50+ mile commutes at the low point though.

Why would double-median income earners commit in a falling market? They didnt last time. Eschewing wishful thinking is the first step to wealth accumulation.

I live near Bellevue. I don’t see as many Chinese Communists buying homes in King County compared to a year ago. Are they going elsewhere to launder their money???

Crackdown from China and new treasury dept rules requiring real names for all cash purchases instead of hiding them through LLCs

Looks like Chinese are buying all over USA

https://www.cnbc.com/2019/01/08/chinese-middle-class-buying-up-american-residential-real-estate.html

Sad to see locals being prices out and becoming renter in their own country locality..

..and yet USA nationals would have/would have had absolutely no qualms about buying a holiday home abroad somewhere cheap and sunny, forcing up the prices for THOSE locals. ie. not your ‘tribe’ so it doesn’t matter and HEY you’re helping out the local economy, right?

Just like those Chinese are spending in yours…

What goes around, comes around…can’t have one type of wealth imbalance good (the ones that suits me) and one bad (the one that doesn’t).

With the Chinese, we are talking about the rich laundering thier money, business money, borrowed money into the US. That’s what is crating this market distortions in housing. In Canada, provincial goverments are at least doing something about it after years of looking the other way.

Exactly. In the US, not only do we have a history of buying up the beachfront property of less prosperous (but beautiful) countries, but we also have TV shows that turn the whole process into entertainment. Ooooohhh honey, which Central American villa shall we buy? I bet some of the locals would love to enjoy their native shores.

There are hundreds of websites dedicated to “expats” buying property in Costa Rica and Ecuador (a favored destination for young American retirees in the FIRE movement) or Brits buying properties in Spain.

But Chinese, Indians or Mexicans are never called “expats”. They are called “immigrants”.

The flaw with that argument is that you’re comparing nationalities rather than incomes.

Most people in the US were never buying second homes and vacation properties. In fact, they were plagued by price increases driven by the same group of wealthy Americans who were buying abroad.

Don’t confuse nationalism with wealth disparity issues, its a tactic too often used to deflect political focus.

You are right. Our crooks are the same as theirs

According to article in CNBC online, today, the Chinese are still in the market in a big way. They’ve gone down to cheaper properties and have moved to other states such as Texas and Florida.

There are 1 billion chinese who wants to move to US,,,,millions of chinese will make babies in the US and become citizens….

I’m connected to one quite extended Chinese family – and their friends – living in HK & mainland. Not one of them wants to go to the US – doing OK where they are, thanks very much.

But even if they did, is that such a bad thing? From my observation, most Chinese who migrate work hard and are successful and their kids over-achieve in education, becoming top professional or do well in business.

It could even move the overall IQ up a notch or two..

Get over it, Roger. There are now more illegals leaving the US than entering and the illegal population is at its lowest since 2007. I know it may cause your head to explode but most people think the US is what your president would call a s***hole. I have lived here 40 years and it’s worse every year – a lot of Third World countries have a better quality of life. If my grandchildren weren’t here I would live in Uruguay.

It would be interesting to see all graphs go back to the last bubble pop to 2006…

Goodness that’s one heck of a surge in inventory. That’s gonna leave a mark.

Is it possible for you to differentiate between new vs. existing? I’d be curious to know if that is builders getting inventory on market or home owners. Or a little of both.

This data is based on Multiple Listing Services (MLS) data, which is what brokers list and sell. Builders have their own sales offices with their own advertising, etc., and unless they’re in deep trouble, they don’t list their units with brokers, and so these units don’t show up in the MLS, and therefore are not included in this data.

In other words, the thousands of new-built units that are for sale in the Seattle metro are in addition to what you’re seeing in the charts.

That’s good to know, thanks wolf. In my MLS (Charlotte area), there is a field for new construction. More builders here seem to be putting some (not all) their inventory into MLS.

They might develop the land (pads,elect,sewer,roads etc) but typically they won’t build until someone has signed the dotted line… Drive through one of these big project one day, you’ll see “Sold” on most lots…. the house itself in theory never really hits the market anyways…

Clearly, all the negative press on the housing market temporarily suppressed housing demand. The lul will not last.

Yes.. I agree with you

This time is different

?

There will be a day when people have houses and debt want buyer’s cash more than the buyer want the houses.

They say the bull market climb in a wall of worry and the bear market sell you down the river of “hope”. Let’s hope the “lull” will be over soon.

Read JZ’s comment a couple of times and you may grasp exactly what he is saying…..a real ‘pearl of wisdom’.

“Never a truer word spoken in jest”.

Because my financial bubble is different to all those in recorded human history. It HAS to be…

At what point does the hype of a housing bust become a self-fulfilling prophecy? Would-be buyers reading about the housing slowdown will sit by and postpone buying, thus accelerating the decline in sales and increasing inventory. As more and more buyers take a “wait and see” posture, prices will fall regardless of the economy. I believe someone once said that perception drives the economy.

The flood of hype during the uptrend of housing bubbles 1 & 2 was certainly part of what induced large numbers of people to do very crazy things, which is what it takes to create a bubble.

Also missed is that this whole crazy era is one big hype, starting with the ‘economy is strong’. Last month’s employment numbers have been touted so many times people are still flocking to the cheering section, yet we all know there is a different reality out there, (even in Seattle). The employment numbers will be quietly revised just about any day, now. It still takes two incomes to get by compared to 40 years ago when I started my family. Vehicles are being paid for these days with 7-8 year loans, or even worse, leased. People cannot afford education and must take on soul crushing debt to train for a career. Health care coverage? Forgetaboutit.

Hype.

It is getting harder and harder to work into upward mobility. Yet hype and marketing keeps convincing people to follow a certain path, which coincidentally enough enriches others.

Two quick definition searches:

Hype…. “Promotion or propaganda; especially exaggerated claims. After all the hype for the diet plan, only the results ended up slim.”

Gullible…… “easily persuaded to believe something; credulous.”

Paulo your posts are always a breath of fresh air.

I could still be on the hook for student loans if I hadn’t gotten an inheritance that allowed me to pay the 2nd half of ’em off and buy my first car, at age 29 or so. Health care is becoming less available not more, and this Mark Zuckerberg character, whatever it is he did to get rich and put his name on a hospital around here, is profiteering like crazy on anyone unfortunate enough to have to go to said hospital.

In my area it wasn’t “perception”. People, including myself went to the banks and the banks flat out wouldn’t sell mortgages for over priced houses. When the banks pull away the free credit people are left to rent. No media hype is being used, just reporting facts. Debt is too high to sustain, the correction hasn’t even begun.

Although it’s a minority view, it seems pretty obvious to me that housing prices are being driven down in large part by the huge amount of new construction that’s taken place in the last 2 years. In part stimulated by government initiative, Seattle built ~12,000 new residential units in 2017 and 2018, twice the average since 2013. Most of those units are rental, and vacancies have crept up while rent for the last several months have trended down.

As that inventory is absorbed, it’s made renting more attractive, i.e. reduced demand for purchased homes by providing attractively priced alternatives. I find the extreme resistance to idea that new construction can substantially reduce housing costs, if there’s enough of it, quite curious, since it’s a orthodox rather conservative economics notion (econ 101, supply & demand, stupid, etc.) Wishful thinking of real-estate investors? Cranky residents who feel their city’s become full just after the moment they moved into them? Cranky resentment against millennials who put a premium on dense, walkable urban cores where renting predominantly prevails? *shrugs*

In any case it’s taken a substantial amount of cash out of the pockets of rent seekers and placed it into the pockets of productive residents. Which, as long as it doesn’t precipitate larger economic contagion, can only be a net win for most Seattle residents.

As long as you accept the idea of “dense, walkable urban cores” as being nice. Which is dramatically different than how people in this country have lived up until the last 20 years or so. So removed from nature and natural systems. No wonder the earth is undergoing the largest and fastest die off of species in its history.

Lots of competition for food and shelter, big incomes, lots of inequity and income disparity. Lots of homelessness.. Pretty soon the walls of the Hunger Games will be erected to keep out all the riffraff.

This is what happened in France. The walkable cities are for the better-off and the suburbs are for the riffraff.

I grew up poor on a small family dairy farm, the last generation to do so — I have a tremendous appreciation of nature.

But, the word civilization is derived from the Latin word for city, and with good reason cities virtually synonymous with human progress. Writing, law making, nation-hood, international trade, technological development were all practically coincident with the rise of the world’s first cities in lower Mesopotamia. The collapse of civilization in the Dark Ages was starkly contemporaneous with deurbanization on a massive scale in Europe and its gradual recovery emerged from those cities that had managed to survive most intact, e.g. Venice for much of the early middle ages remained a possession of the still flourishing Byzantine empire.

Even the US which thinks of itself as a nation of the great outdoors, was home to the largest city in the world, New York, which held that title for much of the 20th century.

Aside from being closely correlated to national economic productivity, social and cultural development, technological innovation, dense urban centers have a far smaller environmental footprint than the equivalent population spread across suburban sprawl, this is well substantiated by numerous studies, but should be obvious: if you want pristine wilderness then of course you don’t want suburban sprawl and strip malls running through those lands.

Conservative antipathy toward America’s great cities (not accusing you specifically of being at any particular place on the political spectrum) is incoherent and ahistorical, as is liberal (in some quarters) hostility toward commercial and residential development.

Money moves to stability and growth.That has been real estate

for a long time.When that is no longer true it will move again’

Those who can solve that puzzle profit.

But ‘gold is just..gold’?

If China’s economy continues to deteriorate, these numbers can only get worse.

Wolf,

During the last housing bubble…

I was told by a realtor that the banks wouldn’t take a reasonable offer due to the bail out? In other words, if I make and offer say 100k the banks would deny it…Then a couple months later, the new listing would be for 75k…. I was confused by this until someone explained that if the banks waited for a certain amount of time, they could get more money from the bailout…..Hence the reason they would refuse a decent offer at first…. I had my suspicions about this theory, but after watching several listing do just that, I think maybe so….

Is this true? If so, (if or when it happens again)would it be the same old same old this time around?

We’re at the very beginning of this as the effects seep into the greater economy. RE agents and mortgage brokers have a mortgage nut to maintain just like everyone else. As sales and refi’s decline, they will be the first to be distressed. I would imagine banks are scrutinizing their loan requirements more than they were 6 months ago. Construction is probably already slowing down around Seattle (as Wolf has noted in the past) – so those in construction should be feeling the heat. Then you have all of the ancillary businesses which thrive off of a heated housing market when people spend luxuriously because they ‘feel’ rich. The moment homeowners stop spending lavishly those businesses will suffer. Any slowdowns in other industries will exasperate the problem.

Housing is a slow-moving train. The real pain will come whenever the overall economy sinks into recession – as it always does.

As long as the population (Legal and/or Illegal) continues to increase, there will be demand for housing. These dips do not negate the overall long term trend up. They resemble market corrections, more than anything. Two steps forward, one step back, as always.

Wolf,

A somewhat related question or possibly subject of a later article.

I seen an article today about mortgage apps being up %23 over last week. My question is this…

Is there any good way of determining how many of those applications went through, how many were a Refi and lastly how many resulted in the purchase of a home?

This is not something I keep up with regularly but I feel the the %23 number isn’t telling the whole story.

Shizz,

You’re correct with your suspicions that the “23% number isn’t telling the whole story.” I’ll start here:

1. Ignore week-to-week comparisons of the type you mentioned, especially holiday weeks, and weeks following holidays. They’re completely meaningless. Year-over-year is somewhat more reliable but not perfect.

2. There are two types of applications:

— purchase mortgages (used to finance the purchase of a home);

— refinance mortgages (use to refinance an existing mortgage).

The number you cited – 23% week-to-week increase, according to the Mortgage Bankers Association – was for both mortgage types combined.

3. Refinance mortgages have no impact on the housing market. But they’re a huge profit center for lenders. This business has withered after mortgage rates began to rise a couple of years ago. The somewhat lower mortgage rates in recent weeks have caused the purchase mortgage index to tick up.

4. The purchase mortgage index for the reporting week was up only 4% from the same week a year earlier. So this year-over-year comparison is somewhat more useful than the week-to-week number for all mortgages combined. But it too is very volatile data, being up one week and down the next.

5. This are mortgage applications only. The purpose is to gauge how much demand there is for mortgages of both types. The purpose is not to see how many actually went through. And the data set from the MBA does not include data on approvals.

Portland is like a younger sibling to the Bay area and Seattle when it comes to the RE market. A month ago my wife and I went to an RE open house in a newly trendy part of town and got to talking to the listing real estate agent. At some point she exhuberantly proclaimed. ” Portland employment is no longer driven by tech or industry but is now primarily the driven by construction and tourism.” My response was ” god help us.” I don’t really agree, but the amount of employment that is currently related to construction, real estate, interior design, furniture, and property development is very large and as the RE boom deflates the deflation of this employment will supercharge the collapse of the bubble.

Wolf, thoughts on how motivated the sellers are? By that I mean, wasn’t a large part of housing bubble 1 because of resetting mortgages and owners inability to keep up with new payments? Those are very motivated sellers. Not saying this is true here, but if these are sellers who don’t have to sell, but rather are trying to cash out, they could de-list or be patient and not accelerate the price deflation like that last time. Not sure there is any way to know that from this data, but given where rates are and how fewer ARMs were used post-crash, this seems worth considering.

Rory Boyle,

Please don’t compare the depth of Housing Bust 1 with this bubble that is just now at a turning point. These two points are years and 10 million job losses apart.

Agreed. Seems as if though some of the commenters are conflating the two and hope that investment decisions are not being made expecting similar results.

Itd be interesting to see a comparison of median home prices to median income adjusted for mortgage rates or some other valuation to compare housing bubbles other than price change. Basically something akin to cap rates but for owner occupied single fam RE.

Wolf,

Mortgage rates had moderated late last year. No more. Up 38 basis points this week. Back above 5%, per Bankrate (01-09-19).