Seattle house prices drop 4.4% in four months, biggest drop since Housing Bust 1; Prices deflate in San Francisco Bay Area, San Diego, Denver, and Portland.

Some of the markets in this select group of the most spending housing bubbles in America have turned the corner, according to the S&P CoreLogic Case-Shiller Home Price Index, released this morning for October, confirming other more immediate data. This includes the Seattle metro, the five-county San Francisco Bay Area, the San Diego metro, the Denver metro, and the Portland metro. In these metros, house prices have skidded the fastest, and in some cases for the first time, since the Housing Bust. In other markets, house prices have been flat for months. And in a few markets on this list, prices rose. More on those markets in a moment.

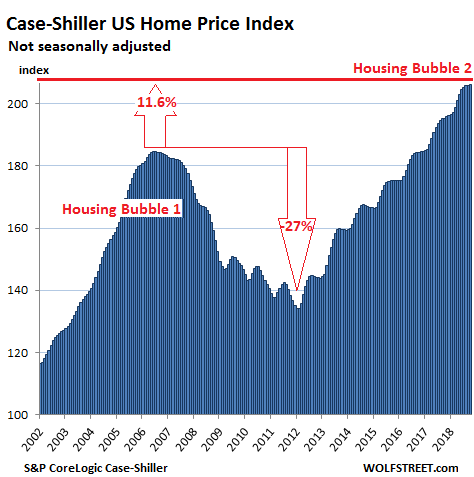

On a national basis, these dynamics get washed out. Single-family house prices in the US, according to the S&P CoreLogic Case-Shiller National Home Price Index, ticked up a smidgen on a month-to-month basis in October, and rose 5.5% compared to a year ago (not seasonally-adjusted). This year-over-year growth rate has been slowing from the 6%-plus range that reigned from September last year to July this year. The index is now 11.6% above the July 2006 peak of “Housing Bubble 1” (the first housing bubble in this millennium), which came to be called “bubble” and “unsustainable” only after it had begun to implode during “Housing Bust 1”:

The index is a measure of inflation — not of consumer price inflation but of house-price inflation, where the same house requires more dollars over the years to be purchased. In other words, the index shows to what extent the dollar is losing purchasing power with regards to buying the same house over time.

The Case-Shiller Home Price Index is a rolling three-month average; today’s release is for August, September, and October data. Based on “sales pairs,” it compares the sales price of a house in the current month to the prior transaction of the same house years earlier. The index incorporates other factors and formulas to arrive at each data point.

The index tracks single-family houses. In some large markets, Case-Shiller provides a separate index for condos. Unlike median-price indices, the Case-Shiller index does not indicate dollar-price levels. It was set at 100 for January 2000; hence, an index value of over 200 means prices as tracked by the index have more than doubled since the year 2000. This is the case for the National Home Price Index (above) and for every metro tracked on this list of the most splendid housing bubbles in America, except Dallas and Atlanta.

Seattle:

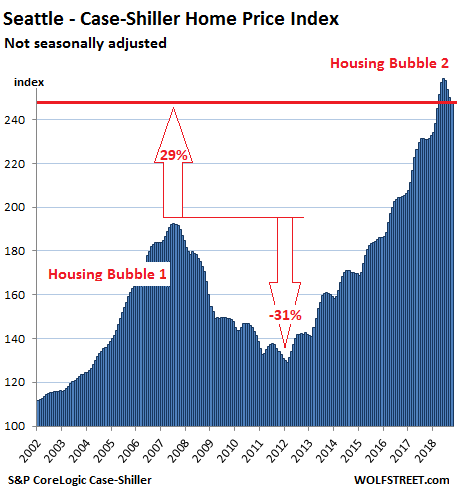

House prices in the Seattle metro dropped 1.1% in October from prior month, according to the Case-Shiller Home Price Index. The index has now dropped 4.4% in four months, the biggest four-month drop since Housing Bust 1 (December 2011). The historic spike that had peaked in June is now getting unwound at a rapid pace. If this pace continues for a 12-month period, the annual decline would be around 13%. The index is now at the lowest level since March.

Over the past 12 months, given the phenomenal spike into June, the index is still up 7.3% year-over-year. The index is up 29% from the peak of Seattle’s Housing Bubble 1 (July 2007), but that is down from the 35% increase in the July reading:

San Francisco Bay Area:

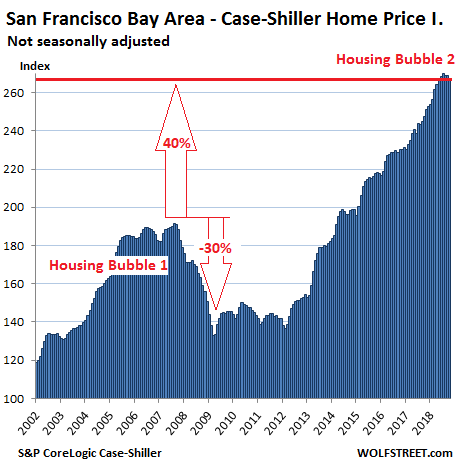

The Case-Shiller index for “San Francisco” includes five counties: San Francisco, the northern part of Silicon Valley (San Mateo County), part of the East Bay (Alameda and Contra Costa), and part of the North Bay (Marin). In October, the index for single-family houses fell 0.7% from September, to the lowest level since May. Over the past three months, the index is down 1.0%, the biggest three-month drop since March 2012.

The index was still up 7.9% from a year ago, after the surge in prices earlier this year, and remains nearly 40% above the peak of Housing Bubble 1:

Also in the five-county San Francisco Bay Area, the Case-Shiller index for condo prices edged down in October to the lowest level since April, and is down nearly 1% from the peak in June.

San Diego:

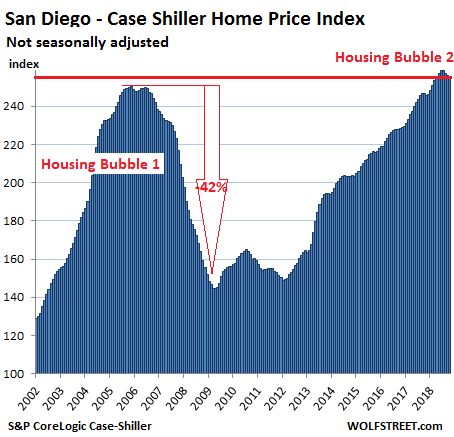

House prices in the San Diego metro edged down again in October and are now down 1.1% from their peak in June, the biggest four-month drop since Housing Bust 1 (March 2012). The Case-Shiller Index for the metro is now at the lowest level since April:

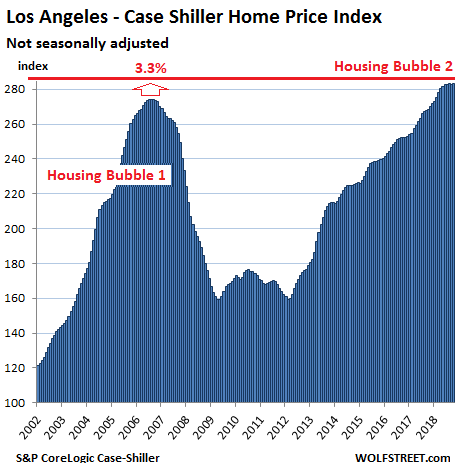

Los Angeles:

House prices in Los Angeles, after relentless increases through the spring, were flat in October for the fifth month in a row, when compared to the prior month, and were about at the same level as in June. The index is still up 5.5% from a year earlier and exceeds the crazy peak of Housing Bubble 1 by 3.3%:

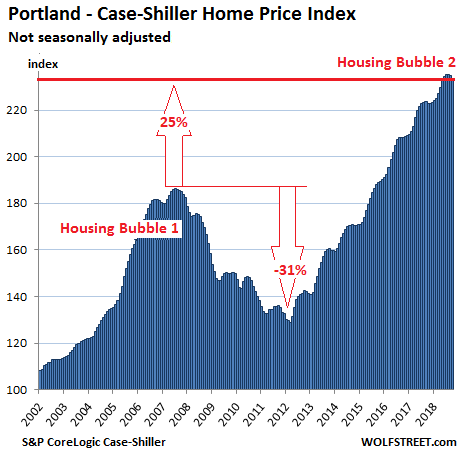

Portland:

The Case-Shiller index for the Portland metro in October dropped for the third month in a row, booking the biggest three-month drop since January 2013. The year-over-year gain has been whittled down to 4.9%. The index is now at the lowest level since April:

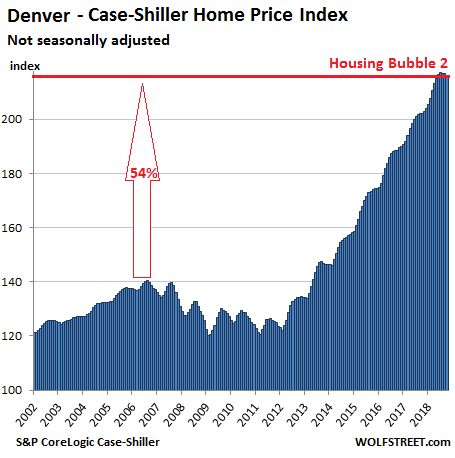

Denver:

Prices in the Denver metro fell in October for the third month in a row, compared to the prior month, after a perfect run of 33 monthly increases in a row. The index is now at the lowest level since May. The three-month drop was the first three-month drop since January 2014, and the largest since December 2013. The index is up 6.9% from a year ago:

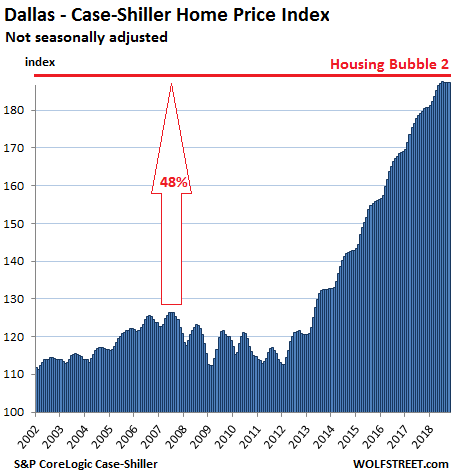

Dallas-Fort Worth:

House prices in the Dallas-Fort Worth metro in October were flat for the fourth month in a row, after a perfect run of 54 monthly increases in a row. The annual gain has been whittled down to 3.9% — from the 5.0% year-over-year gain in July. Since its peak during Housing Bubble 1 in June 2007, the index has surged 48%:

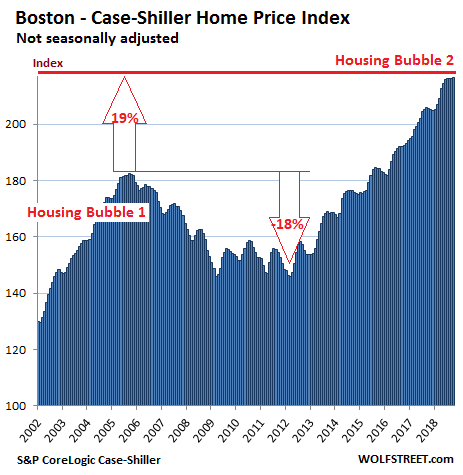

Boston:

The Case-Shiller Index for the Boston metro eked out a new all-time high in October, after having been essentially flat for three months. The index is up 5.4% from a year ago and exceeds the crazy peak of Housing Bubble 1 by 18.7%:

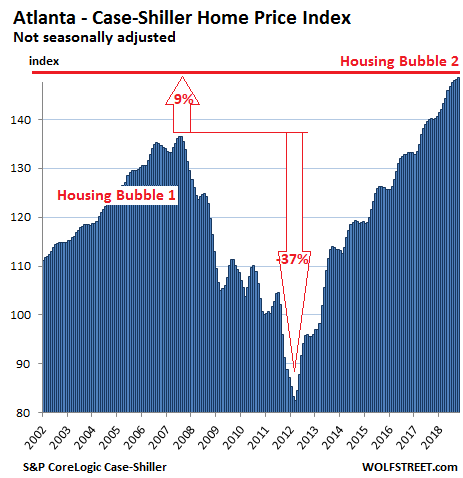

Atlanta:

House prices in Atlanta inched up to a new record in October and were up 6.0% from a year ago. So Atlanta’s housing bubble remains on track. The Case-Shiller index is now nearly 9% above the peak of Atlanta’s crazy Housing Bubble 1 in July 2007:

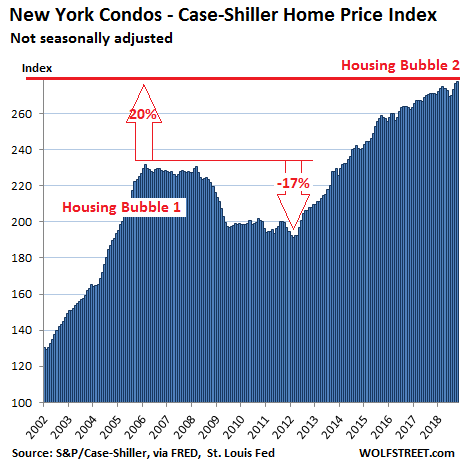

New York City Condos:

The Case-Shiller index for condo prices in the New York City metro, after ticking down several months in a row, has now jumped for the third month in a row. With the recent gains, it is now up 2.4% compared to October last year.

Existing home sales across the US dropped 7% from a year ago, but plunged 15.4% in the West. Read… Downturn in Local Housing Markets Hit National Averages

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wake me up when a number of markets post Year over Year price declines. Monthly declines may not mean much because prices tend to drift lower into the holidays.

By the time you wake up and hear about YOY prices dropping, the MOM prices have been dropping for several months already. It is not advisable to focus on YOY in dropping markets, look at MOM to see what is really going on. In fact, one should always look at MOM first to be safe and catch trends early.

I agree with this… and further, that at about 6mo into a trend is about the time the YOY change turns negative… and whereas then, that negative number becomes the headline and starts scarrying the shit out of Home Owners thinking of Selling.

See the bottomof the trough? Thats what houses are really worth without government manipulation. End the Fed.

+1

#end the fed

We work for currency they create from thin air, then we compete for assets with them. Wake up people

Very informative video-Mike Maloney hidden secrets of money episode 4

bitcoin

Nope – it’s what houses are worth without the naked greed and usurious lending practices of the private financial sector, whose wealthy executives spend lots of money into right-wing ‘think tanks; whose job it is to convince you the problem is one of governance, so they can in future pay less tax and enjoy even greater returns from even bigger bubbles and crashes.

Failure to acknowledge this is failure to appreciate the true root cause of the problem.

Md

Obviously you didn’t watch episode 4, it explains the fed is the private finance sector you wrongly call right wing.

A country divided…

Educate yourself

It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.

Henry Ford

Love that Ford quote and I use it all the time.

For revolution to happen, two necessary conditions need to be met.

1st people are mad at status quo

2nd, the existing tools of the ruling class no longer works.

This is Vladimir Lenin.

Even if people are extremely mad at the FED, only the first condition is met.

I trust Lenin more than Ford on revolution because Lenin did one.

I can’t imagine that there will be a national housing “collapse” on the magnitude of 2008 because there won’t be the rate refinancing issue that caused so many to simply walk away from their homes. Instead, in most areas, it seems like this will be a steady deflation, as sellers slowly reduce prices to match buyer expectations and ability to pay. And as long as people keep flowing to these superstar cities, downward pressure on prices will be mitigated.

Of course, I expect cities Seattle and San Fran to see accelerated declines from Tech Deflation. And in Miami and other areas that require retiree churn to increase prices.

Rowen I agree that the collapse in prices and sales will not be as fast as it was in 2008, but I believe that it will be much deeper. In 2008 the fed in conjunction with the big banks and investment firms ( Blackrock Etc.) went on a buying spree of mid level houses and turned them in to institutionally owned rentals. This put a floor under prices that would have fallen further. In addition the Chinese economy was humming and in a giant binge of credit creation that flowed in to the West Coast Housing markets, and further the Fed managed to reflate the Tech bubble in time to reflate the housing bubble. They also still had room to drop interest rates. This time there has been a huge boom in rental apartments along the west coast flooding the rental market , any many of the apartment investors from 2008 are ready to dump their units and cash out. The Chinese money is flowing out, and the Tech stocks are in the middle of a massive crash that will begin to such liquidity out of the housing market as it progresses. I think our real estate price curve for the next 30 years will look more like Japan’s than many people think.

“( Blackrock Etc.) went on a buying spree of mid level houses and turned them in to institutionally owned rentals”

And what does one think these same companies will be doing when they see the value of their “stock” dropping like a stone? first one to the exit wins.

Blackrock and others didn’t start buying homes until 2010-2011 and prices didn’t stop declining until 2011. Most purchases were made by investors owning less than 100 homes. Even today small investors own 90+% of SFR rentals. Prices were so low and have now increased to Pre recession levels. We’re sitting pretty with lots of income. No need for us to unload now.

and to add to that, we’d take a big capital gains hit if we sell. Instead we are barely taxed on income thanks to the overly friendly deductions. Being a small residential landlord is a great job (trust me you passive idiots, it’s a job) but one that is really hard to get out of without dying (provided you have a good accountant)

I think Case-Shiller is understating it. I’ve been watching my house value on Zillow very closely for the past five years and it was going up steadily the whole time. I live in the N.Silicon Valley area. But almost exactly one month ago the price stopped rising and began dropping. Now my house is down 2.3% from where it was a month ago.

Usually in my neighborhood houses go for mind melting prices within just a few days of listing. Now it’s taking weeks. I should add: there is still very little inventory. I guess that indicates the job situation is still good in the area. For now.

Yes, there are many RE observers that think the Case-Shiller understates price changes, in both directions, on the way up and on the way down. But it’s the only measure we have that uses “sales pairs” – comparing transactions of the same home over time. This eliminates the issues that median prices cause, but it creates new issues.

It is also about three months behind. We just got “October” which was the rolling three-month average of August, September, and October, with the midpoint in September. In a few days, MLS will come out with median prices for December.

But the Case-Shiller captures the trends very well and is a lot less volatile than median prices, which jump up and down maniacally from month to month.

Wow, I was just looking at the chart for L.A. I do not remember L.A. house prices being up that high back in 2007. What was going on with that?

While we in the bay area have seen enormous gains in bubble 2 L.A. is basically just back to where they were 11 years ago. That seems pretty crazy. Either way, though L.A. sucks. I wouldn’t live there if you paid me!

Lisa Murphy, actually, since Case Shiller started tracking prices in 2000, the LA metro area has appreciated significantly more than the Bay area. That is why LA metro has a higher value than the Bay area. But, that is a fact. This is common knowledge.

Would appreciate if you could un-confuse me:

Based on your post, ‘LA metro area has appreciated significantly more than the Bay area”

2002: LAX @ 120 & SFO @ 120 (2002 earliest in Wolf’s chart)

2018: LAX @280 & SFO @ 270

I’m not seeing a “significant” difference (unless 10 points out of 280, or 3%, is significant). I suspect (but don’t know) SFO started from a higher base (price) in 2002.

LA = 283, SF = 267. Difference is 16 points. January 2000 = 100 for both cities. LA’s index increased 183 points since Jan 2000. SF’s index increased 168 points since Jan 2000. Therefore, LA’s index increased 10% more than SF’s index since Jan 2000. Therefore, the average home in LA appreciated 10% more than the average SF home since Jan 2000.

Javert Chip,

I think SocalJim is trying to address the differences between the two areas in terms of timing — how and when they got to their bubble peaks.

The CS index was set at 100 for the year 2000. So let’s start with 2000.

— SF Bay Area: 2000 to 2007 (peak) gain: 90%.

— LA metro: 2000 to 2006 (peak) gain: 170% or nearly twice the gain of the SF Bay Area.

— Housing Bubble 2: SF Bay Area blew past prior peak now at 267, or up 167% from the 2000 level, essentially catching up with the wild gains of 2000-2006 bubble in LA.

— Housing Bubble 2: LA barely passed its 2006 peak (now at 283, thus up 183% from 2000)

Note however, that through 2000 (dotcom), the SF Bay Area was in a HUGE bubble, and values didn’t really drop after the bubble, but % gains to the next bubble (peaked 2007) were smaller from that high base.

In terms of median price, San Francisco and Silicon Valley are much more expensive than LA.

If 2000 homes prices in each city start at $100, and by 2018 LAX is $283 and SFO is $267, the LAX house is 5.7% (not 10%) more expensive than the SFO house.

Using relative change in the index is a false reading: if LAX house increased from $100 to $101, and SFO stayed at $100, the LAX house is 1% more expensive, but the LAX index change (+1) is an infinite increase over the SFO house’s index change (0).

Here is an interesting link. Looking at appreciation over the last five years, SF cities have been higher.

However, if you look further into the report, the most expensive cities list shows LA cities dominate the most expensive.

In my opinion, this appears correct.

http://www.visualcapitalist.com/map-where-real-estate-prices-are-rising-fastest/

SocalJim,

You’re citing per-square-foot prices, from Zillows.

I was referring to median sold prices. So here are median sold prices in November, from the California Association of Realtors, of single-family houses, by county. As you can see the most expensive counties in SoCal are not even in the same ballpark as the most expensive counties in the Bay Area:

Los Angeles: $553,940

Orange: $795,000

Ventura: $643,740

San Francisco: $1,442,000

San Mateo (northern Silicon Valley): $1,500,000

Santa Clara (southern Silicon Valley): $1,250,000

Marin (North Bay): $1,172,940

https://www.car.org/en/marketdata/data/countysalesactivity

Also note that San Francisco and Santa Clara already booked year-over-year declines in their median prices.

Something that is not being factored-in is the general population of SF vs. Los Angeles. L.A. has over 4 times the people as that of San Fran. That figure includes housing that is in “marginal” areas which are no longer particularly cheap but there’s almost nothing equivalent, in terms of undesirability, in San Francisco. So, the average or median price in L.A. is diminished by those areas.

Hello Javert Chip always enjoy your informative posts but think on this one, a small misunderstanding is causing confusion.

Each region started year 2000 at 100 value (NOT $). One region may have seen increases leading up to 2000, others may have been flat or seen declines prior, but they would all start at year 2000 with 100 value.

Therefore the index value is useful to visualize trends since 2000 within its own regional chart. Beyond that, comparing index values or percent changes in one region vs another is problematic because every region’s 2000 value may represent a different point in a different market cycle.

In the Bay Area you can get a decent 3 / 1.5 1400 Sq Ft in a good area for the media price.

In LA, you take your life in your hands when you purchase a home at the median price. In LA, you need to spend at least 2X the median to get something safe to live in.

In the Bay Area, the counties are small where LA county is massive.

This is comedy. Take it from someone who grew up in LA and has lived in SF for the past 7 + years. SF is WAY more expensive than LA to rent or own in comparable neighborhoods. In LA you get an entire nice house with a yard in mid city for less than you get a good two bedroom condo in the Mission. If you don’t think SF or Oakland has its share of shitty neighborhoods, you don’t k ow the area. I wish my budget could go as far in SF as it would in LA.

Trojan Man, perhaps we have a different perspective, but I would not consider living in LAs mid city. On the southern border of mid city is some of the toughest gangs in the country. In my opinion, the Mission is comparable to the west side and the west side is much more expensive than mid city.

Socaljim – Midcity in the Wilshire coordinator in the doorstep of West Hollywood is not the ghetto. There are gangs in every big city. I grew up in game land and Mid City is not it. The Mission is not comparable to the West Side. If you want to compare the West Side, then look at Pacific Heights or the Marina where people often pay $1500 per square foot. . Any way you slice it, SF is way more expensive than LA. It is not even comparable. I think you are the only person I have seen try to argue it’s not. It’s like arguing water isn’t wet.

So Lisa,

Do you think your bay area will see a significant downturn with the Trump trade war affecting Chinese demand, and big tech potentially blowing up?

The city may no longer be able to afford the all day sh*t patrol.

Only 15% of China’s exports are to the US. A lot of that 15% are American companies that are exempt from the tariffs. The Trump Trade War is a tempest in a teapot.

Broker Dan,

I think we are in a giant RE bubble here in the bay area and especially the mid-peninsula. Houses in my neighborhood in n.silicon valley have gone up not 40% – the average of the bay area – but a whopping 100% since 2007. But apparently median incomes here have only increased about 20%.

I think Trump’s trade war just boils down to a new tax on the people and will pose a drag on our economy in the 2 or 6 years remaining in his term. I expect a recession (or maybe depression) coming in mid to late 2019 — with a huge RE collapse in my area.

That said, I tend to be a pessimist!

LA County, Orange, and San Diego counties are the largest counties in the state … much larger than the bay area counties … they contain large areas of impoverished zip codes. The bay area counties do not have that demographic balance. That is the difference of the medians. In the Bay area, you can get a decent home in a safe area for the median price. In LA county, you are looking at hard core ghetto areas for the median price. In LA county, you need to spend at 2.5X the LA median to get a home comparable to what you get in the Bay area at the bay median price.

Lmfao. Wish this were true. We can start posting comps feom Trulia is you’d like.

Unless all these houses were purchased on very sketchy financing, I don’t see a huge drop in prices…EXCEPT when the economy starts shedding jobs big time. Then, even properly financed houses (albeit at nose bleed prices) will start coming on the market and exerting downward pressure on prices.

However, just as in 2009, the government has a plan for this. It’s called QE and would involve the buying up of many/strategic mortgages to prevent fire sale liquidation and large drops in housing prices.

Unless Fed Chair Powell is philisohpically opposed to reflating the economy to avoid the mother of all depressions, I doubt we’ll see a repeat of house price crash as before. They will come down off the highs and of course as this occurs, interested buyers will step in an buy to help offset that drop. Again, should lot’s of houses start to become deliquent, I would look to see some form of government prop-up.

Don’t get me wrong on this prediction. I don’t like it. But I don’t see how it can go any other way, given the alternative.

What is your definition of “sketchy financing”? Could it include artificially low manipulated interest rates? Or unrealistic income to debt ratios?

The problem with housing bubbles is that they induce people to take on more debt than they can afford under periods of stress. What people can afford under the best of economic times is much different than what they can afford when things go south.

QE was instituted to save the banks, not the citizens. The big difference between today and 2008 is that the banks today are better capitalized due to the fact they are not holding the liar loans they write. They are sold into a hungry bond market that has been chasing yield at any risk.

If you think the Fed is going to step in and re-inflate its balance sheet to bail out citizens and pension funds then you do not understand the purpose of the Fed.

This time the banks are secure, and the Fed will stand aside and let the imprudent investors reap the consequences of their foolishness.

My definition of sketchy financing is what occurred leading up to 2008. Liar loans, interest only, crap securitization,etc. I do believe the last round of housing financing has been done closer to what is proper and sound. But I’m open to being wrong on that.

QE was not just done to save the banks. It served multiple purposes, the most obvious being saving the banks. QE took a ton of bad housing loans off the hands of duped investors and ‘managed’ those to prevent a complete collapse of housing.

I just don’t agree with your premise that the Fed will “save the banks” and let the US economy go into deep depression. How would that “save the banks”? The banks need an economy to survive as well.

In my opinion, our financial system is “in too deep” to allow for a deflationary spiral. It would be a catastrophe. That said….it will happen someday. Just the powers to be in power will delay it as long as they can and keep it off their watch.

Banks make money in both inflationary and deflationary cycles.

They got themselves in trouble in 2008 by being too greedy and owning too much sub prime debt. Most would not have survived without the Gov/Fed bail out which would have been preferable.

Instead, the government and the Fed enguaged in rewarding unethical behavour, and created another bubble. The large banks are well capitalized this time, and will profit from the foreclosure resale cycle. In addition, every cycle serves to steal assets from the working class, and to concentrate wealth among the upper classes.

There was a time when it was common for an average American to have 160 acres of land. That ended in the great depression.

Today we exchange our labor for debt, instead of for assets.

Slavery did not end, it was just prefected…

Then you don’t know much about the secondary mortgage market like Quicken and Rocket Loans and the exposure the banks have to those entities. I believe SoFi is the largest jumbo lender in CA with average of 10% down. Much of the income in the Bay Area is equity comp from tech companies, and guess what’s happening to those valuations? Traditional lenders won’t accept equity as income to support a jumbo loan, but not sure about secondary lenderz.

TrojanMan,

Yes, good point on stock-based compensation being used for backing multi-million-dollar home purchases. I know a guy who does this for a living. He works for a special department at a good-sized bank. None of these mortgages can be sold to the GSEs. Even employees at startups that have not yet gone public can use their stock options to back mortgages. But these options may be illiquid now and perhaps worthless in the future. So these lenders will take big losses if the market turns on them.

I don’t know anyone at Silicon Valley Bank. So, just anecdotally, this bank is specialized in startups and their employees. And it is very exposed to a change in fortunes in the Bay Area. Its shares have plunged 41% since August.

But all this is too limited to cause a national banking problem.

Mike, there is news for you. The FED is in trouble itself. Never thought about this? You think Powell raised rates at the risk of losing his job because he likes it that way? You think FED can save everybody else like they did in 09? They need to save themselves first, sorry.

I am in lending, and the quality of loans now versus 2003-07 is night and day. Everything is income based. I mainly write conventional, FHA, VA and some non-QM.

That being said, I don’t like some of the loans I have seen written by these bay area specialized lenders. I have seen 0 down to 1mil for employees with limited work histories.

Those are all portfolio and the banks handing those out are taking large risk without too much reward.

Should be interesting to see what happens

True price discovery, long deferred by Ben & Janet’s deranged money printing, is now stalking the Fed’s Everything Bubble and will lay waste to the fake “wealth” created by trillions in conjured-out-of-thin-air FedBux lavished on the Fed’s investment banker cohorts so they could speculate with wild abandon. This is not going to end well for the fools who rushed in to buy insanely overpriced housing due to greed, recklessness, Fear of Missing Out (FOMO) and realtor snake oil.

Ah, THAT’s why Warren Buffett loved ice cream so much! He “shopped” at Ben & Janet’s !!

Housing is a commodity, that due to credit cycles becomes investable.

It is the investment aspect of housing that causes the wild price swings.

In times of easy credit, investors push home prices up, and people feel secure taking on more debt than they can actually afford due to price apreciation.

When credit tightens, that security dissapears as loans become delinquent and begin to default causing prices to decline.

What always amazes me during these deflationary cycles is the denial from the RE industry of what they know is happening. A RE broker in Boise recently told me that “local experts” consider Boise to be immune from the price declines happening in places like Washington, California, Texas, and Florida…

Housing is a commodity, that due to credit cycles becomes investable.

For most of human history, housing has been shelter and is a basic human need. It only become a “commodity” thanks to the financializaiton of everything in our “new economy” wherein our rapacious financial elites systematically loot and asset-strip the 99%, while its Fed accomplices create engineered boom-bust cycles so the wealth and property of the middle and working classes can be transferred to the Fed’s Wall Street grifter cronies. Wash, rinse, repeat.

“For most of human history” is a very dangerous framing.

“Housing is shelter and a basic human need” is not what the London slumlords of the Victorian age thought, except insofar as they could monetize it. New York tenements of the Gilded Age also come to mind.

And the Romans and Greeks, being slaveholders, didn’t think too highly of basic human needs, except their own.

In between, wasn’t housing mostly a source of rents paid by the serfs to the feudal lords?

I’m not disputing that housing = shelter and is a basic human need, but it’s also always been a commodity, a financial asset, and a tool by which the wealthy extract economic rents from the poor.

I’d also say it’s a mistake to think that the current financial elites are more rapacious than their historical predecessors. They’re just as rapacious as ever, but have been enabled by everyone’s addiction to debt to prey more than normal.

To the extent that there was a golden age, it was because most people were so horrified by the Great Depression that they refused to take out large mortgages and put themselves in hock to lenders generally. And they took over the political system to protect themselves. Very little of either of those things going on today, at the opposite end of the long credit cycle. But the social mood is slowly turning.

Correct, debt slavery is as old as written history. And yes, the country as a whole learned some very important lessons from the great depression, and those lessons created the greatest accumulation of wealth among working people in history.

The problem is those lessons are not able to be instilled in the decendants of the people who learned them. The wealth accumulated by the greatest generation was for most part squanderd by their children and grandchildren.

I keep a close eye on the residential job sites and supply houses… when we start seeing equipment sitting in yards, and tumble weeds in the developed land, the pendulum has swung…

Wolf, I’ve looked for a break down in construction trades vs % of economy… curious how much of the pie is “residential “ construction in terms of over all economy/ jobs?

IMHO, there’s a big difference between an industrial electrician, pipe fitter etc. etc. compared to residential electrician, plumbers etc.etc.

I’m in the “industrial/heavy commercial “ side of construction and our down times usually don’t run lock step with “residential “…

I have to believe that residential is a lot bigger than folks think.

Jason,

I had a long conversation with an architect friend of mine yesterday. The large firm she works for (she is in her firm’s San Francisco office) has among its clients some of the big names in Tech. They don’t do industrial. They do offices, and some of this is very specialized. So a little different from what you’re looking at. She told me that numerous projects are being slowed down by their clients and that additional phases have been cancelled. I have no data on this yet, but this is front-line Bay Area gossip pointing at a slowdown in the office sector.

From what I hear, industrial (fulfillment centers, warehouses, etc. often to build out retailers’ e-commerce infrastructure) are still hot.

I do a lot of work for Constellation Brands and I smell something fishy…New equipment sitting without being installed (jobs cancelled after p.o. is issued)no big capital project (so far) being talked about etc etc….. this will be an interesting year for sure.. Maybe the big boys are in the wait and see mentality or maybe there digging there heals in and will just sit for a spell and wait for interest rates to fall again….

Seems to be a lot of astute business people and financial wizards on this site, makes for some very interesting reading. What escapes me is the amount of doom and gloom everyone seems to be fixated on. The only time you lose money in a down market is if you are forced to sell. In fact, I would argue to the contrary as property taxes also plummet when values drop. More importantly, if you have positioned yourself right, you are poised to cash in on the housing bust buy adding bargain-priced real estate to your portfolio, riding the wave to the next crest. RE only differs from stocks in that it is tangible, with the end game being the same, to separate the naive from their money.

What if there is not a next crest? Japan, an advanced industrial nation with a positive balance of trade and a money printing central bank as seen real estate values fall for 30 years now, it is entirely possible we could entire such a cycle here. We are at the end of a 40 year debt supercycle where interest rates decreased steadily over time. Since we nearly touched bottom the story for the next few decades will probably be one of increasing interest rates leading to declining home selling prices. Plus the overbuilding of rentals ( on the west coast anyway) could lead to lower rents keeping RE speculators from covering their costs of properties and forcing them to sell in to a declining market.

Big difference is we allow immigration and Japan does not. Yes, Immigration properly handled is very good for our country. cf Japan