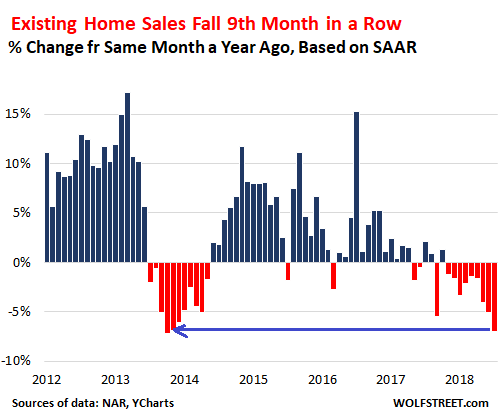

Existing home sales across the US drop 7% from a year ago, plunge 15.4% in the West.

Sales of existing homes — including single-family houses, townhouses, condos, and co-ops — in November, dropped 7.0% from November last year, to a seasonally adjusted annual rate (SAAR) of 5.32 million homes, according to the National Association of Realtors this morning. This was the ninth month in a row of year-over-year sales declines, and the biggest such drop since February 2014 (year-over-year comparisons eliminate the effects of seasonal fluctuations; data via YCharts):

Sales of single-family houses fell 6.7% from November last year, according to the NAR report, and sales of condos and co-ops plunged 9.0%. Sales by Region — note the plunge in the West:

- Northeast: -2.6%, to an annual rate of 740,000.

- Midwest:-4.3%, to an annual rate of 1.34 million.

- South:-5.6%, to an annual rate of 2.20 million.

- West: -15.4%, to an annual rate of 1.04 million.

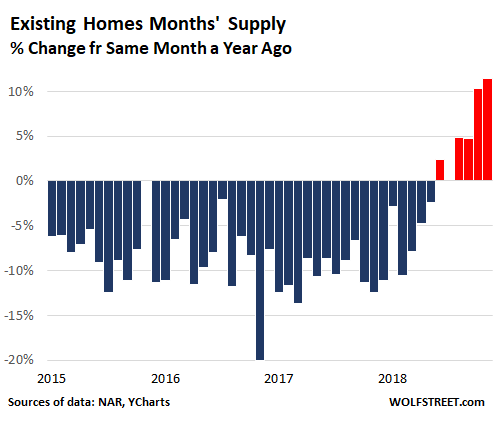

Total housing inventory at the end of November rose 4.2% from November last year, to 1.74 million homes.

Suddenly inventory is “plentiful,” as the NAR report puts it, after years of blaming a shortage of inventory for the rampant price increases. But it’s the wrong kind of inventory, after years of precisely these rampant price increases, and everything is too darn expensive – or as the NAR put it in more appropriate economic terms: a “mismatch between supply and demand exists at affordable price points.”

Given the dropping home sales, the number of months it takes to sell this inventory (months’ supply) jumped 11.4% year-over-year to 3.9 months. This measure of supply has been increasing for six months. The chart below shows the percent change in months’ supply compared to the same month a year earlier:

“Rising inventory is clearly taming home price appreciation,” said the NAR report.

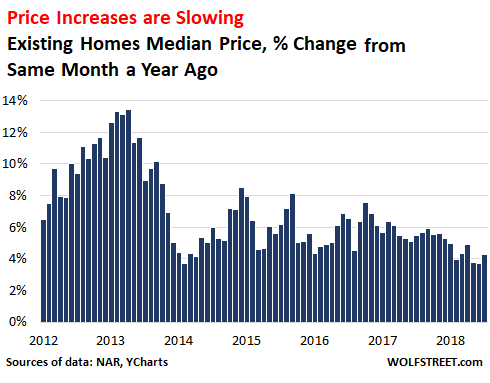

The median sales price – meaning that half of the homes sold for more and half sold for less — across the US rose 4.2% from November last year, to $257,700. Changes in the median price, year-over-year by home type:

- Single-family houses: +5.0%

- Condo and co-ops -1.3%.

Overall, the rate of year-over-year price increases over the past six months, ranging between 3.8% and 4.9%, is down sharply from the price increases over the past few years. And looking at the trend, it seems the hot air is gradually coming out of the national average:

However, housing is local. As already depicted in the regional sales volume data above, at one end of the spectrum, home sales in the West plunged 15.4% year-over-year; at the other end of the spectrum, home sales in the Northeast dropped “only” 2.6%.

“A marked shift is occurring in the West region, with much lower sales and very soft price growth,” the NAR report said. “It is also the West region where consumers have expressed the weakest sentiment about home buying, largely due to lack of affordable housing inventory.”

Yup, after years of ludicrous price increases, leading to ludicrous prices, suddenly and surprisingly for the industry, everything is too darn expensive, and potential buyers are losing their appetite for stretching beyond what the can reach.

Median home prices by region:

- Northeast, rose 6.5% from November 2017, to $291,400.

- Midwest, rose 2.6% from November 2017, to $199,100.

- South: rose 3.2% from November 2017, to $223,600.

- West: inched up 1.8% from November 2017, to $380,600.

But the West is a huge very diverse region with enormous differences in local housing markets. In the western-most strip of this region, the West Coast, two of the three biggest housing markets are already seriously and rapidly deteriorating – the Seattle metro area and the Bay Area, including San Francisco and Silicon Valley. And the process is starting in Southern California.

There are still many housing markets in the US where prices are surging. The national and regional averages that the NAR reported today are comprised of markets that are variously booming, stable, or deteriorating, each at its own pace. As the deterioration has spread more deeply to more markets, the national averages are now beginning to reflect it.

Homebuilder Toll Brothers just said it out loud. Read... Why California’s Housing Market is in for Serious Trouble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Averages”?

If the Canadian housing market could be so lucky!

The real estate pricing and sales stats are nightmarish.

The forward looking, entire real estate picture is very grim.

The Canadian market, as in the Australian real estate market, are diving into the doldrums with no end in sight. Far from being the the end of the beginning, we are seeing the beginning of the end. (apologies to Winston Churchill)

We are now seeing the downward real estate market move, taking place in the UK as London’s high end market expires, along with the remainder, as is what is now occurring in China. This is a global trend taking place. Starts on the periphery and works to the core. The US.

http://www.betterdwelling.com

RE is local and averages, even divided into regions, can still be misleading.

For example, sales are down in Vancouver BC and prices are dropping, yet ground is breaking on a 1500 home development in Union Bay and a projected 1,000 home development in Ladysmith (both on Vancouver Island). I have relatives in both locations.

This doesn’t seem like much, but for these two locations the impacts will be drastic and life changing. Previously closed schools will have to be replaced, there are traffic concerns, and many many locals are not happy about the development. Campbell River and Courtenay/Comox are still rapidly growing.

I certainly noticed the disclaimer Wolf provided about the snapshot portrayed, but grouping the US into 4 regions is probably not very accurate. And no, I don’t have a better suggestion and I am not being critical of the article. I suppose the shared trend is what is most important. And we just saw another Fed increase so the inverse relationship of home prices to interest rates will most likely continue.

I expect we’ll see more forestry layoffs where I live as a result of the slowdown.

Great article and thanks for the info.

A 1500 house development? That’s more like a town!

Who are these people? Where are they moving from? What are their expectations with regards to the changes to their source of income and lifestyle? Do they care about the reaction from the local community, as well as what their arrival will do to the local micro-culture?

Do I ask too many questions?

Jerry, you do ask many questions. But they don’t. And they are the ones purchasing these home (apologies to Seinfeld).

Guido, I am bewildered about what is going on in peoples’ heads these days. I am feeling as if most everyone is on a Secret and I have been excluded.

– Jerry

‘ground is breaking’ and ‘projected development’

On the ‘ground is breaking’ they must have closed on the land a minimum of a year ago, i.e., at the peak.

‘Projected’ can mean anything. If they haven’t bought the land they will be rethinking the project.

I was a young realtor in the early 80’s just before the crash

and saw Nanaimo’s Oakridge development go back to First National Bank. It was beautifully but very expensively done with roads cut through rock, underground services. It was far more classy those newer (strata?) houses near Ladysmith that all look the same and have a highway view and noise as well as an ocean view.

Today there are million dollar houses there but the crash then wiped out the long- time developer of North Nanaimo, including Sherwood Forest.

Land development is VERY risky. At the end of the project you still don’t have income, but you are still carrying expensive financing and now you have taxes on each lot.

if ground is breaking and they are just putting these developments up, doesn’t that just add inventory to a potentially weakening market? I have no idea re: the markets in the locations u mention, but was curious why you consider the increased building equivalent to the finished properties being purchased and filled?

We have a problem with “Averages”!!

If you stick your head in the oven and your feet in the fridge, on average, you’re okay. -Stephen Kotkin

Lmao…that one made me spit my coffee out…

APRA just gave the go ahead to relax lending, our market is not yet bloated enough (their own report findings, recommended tightening) but their is pressure from HIA and government, and the banks are crying poor!

So the facade continues until it all hits the wall, please don’t worry about the DUTY OF CARE to Australians, in fact they have giving us the middle-finger! But Australians are blind because MSM and government have put a bag over the tops of most of our gullible stupid population, and like a wolf in sheep’s clothing lured the ignorant and blind public to the cliff’s edge, where, soon, they will ALL be pushed off! It is going to be a hell of long way to the bottom, I reckon!

Well said, on the money,or should that be on the loan.

Wolf,

Thanks for your dedicated reporting on this. It looks ugly but I suspect it’s not going to be happy 2019 for realtors.

One of my friends is a real estate agent. The year 2018 has been a real bust for her. I’ve heard that she’s now looking for a full-time job.

Realtors make money when house price go up. Realtors make money when house price go down. They suffer when there is NO activity, which is now. Affordability prices out W2 and the property owners can NOT fleece shelter buyers by offloading at higher prices. In stead, theyare raising rent to squeeze the renters to justify their investment in a rising interest rate. Come on, two year treasury yield close to 3% and price to rent is over 30? No activity kills realtors. When price really moves and activity increases in 2019, they will have a better until …… I heard on radio that Zillow will become real estate “dealers”. No more brokers! People will buy houses like they go to a car dealership. Their days are numbered and they will all wind up being Zillow’s employees like all cab drivers are working for Uber now.

Higher priced homes in many Chicago suburbs, just haven’t been moving. We are talking the existing stock of $700,000 plus. So a number of people have simply moved out of them, and are renting them out. This after trying to put them on the market over a year.

Now neighborhood pockets exist, where $1 to $2 million priced NEW homes, are going up like crazy.

So its very spurious, and very local, which to me sounds like a major long term housing ‘top’ is occurring, and prices will resume their downward slide again, like post 2006 peak.

This time though there are a lot more people already renting. A LOT of midwest homes never recovered their price peaks from the 2006 levels. This is as if the great depression is being spread out over decades, where the reflationary practices of the Fed, just keeps taking out larger and larger chunks of wealth from all but the upper 1%.

Previously they took out a chunk who were upside down on their mortgages. Now they are going to take out the folks who have paid off their mortages, and permanently evaporate the home ‘wealth’, to where prices now will be cut by 50% or even a lot more, before this is all over. So if they are ‘retired’ they will either die in their homes, and not move, or be pushed out with substantial losses by ever increasing property taxes. If I didnt have a teen in high school, I’d sell now, and move out of our very high property tax state. the worst in the midwest by far, and the most indebted, which is easy for anyone to guess.

Wolf – does the chart go back past the GFC? That would be interesting to see.

Some housing charts with monthly year-over-year percent-change data reflecting sort of normal times become unreadable when on the same chart with the chaos of the financial crisis, when numbers jumped in huge leaps in all directions. Those were chaotic times, when the world seemed to be collapsing, followed by an equally chaotic recovery, and we’re not anywhere near that.

Wolf, but like in photography, what one decides to leave outside the frame is often as important as what’s in the picture.

Leaving a major disruption out creates a different baseline, along with a different scale. Or do you believe the Housing Bust was a six-sigma event?

I’ve seen a housing bust like this only on a very local basis, due to a very specific reason: In Tulsa, OK, in the late 1980s, all the oil companies headquartered in Tulsa (at the time the “Oil Capital of the World”) moved to Houston during the oil bust. It was terrible locally. I lived there at the time. Over the years, people left, restaurants closed, construction stopped entirely, young people bailed out, and Tulsa’s workforce dropped by 15%. But it was a unique situation, rarely duplicated on a larger scale… until 2007-2011. So the national scale of the housing bust was, to use your phrase, a six sigma event.

Maybe I wouldn’t quite call is a “six-sigma event,” but something of that magnitude across the nation is highly unlikely.

That same housing bust happened in and around Houston in the early 80’s. Folks just walked away from homes, and entire sub divisions were abandoned. Again, oil bust. A colleague of mine, who lived right in it, left and moved to ‘dirt cheap’ western Kentucky. Whatever ‘equity’ he had, simply went kapoof. divorce ensued, and his wife took every other penny beyond that.

I’m hailing from the “Oil Capital of Canada”, which was also a home of the Jingle Mail back in the 80s, during the same bust.

We have been in an economic state technically known as “the deep doo-doo” for a few years now, with no respite in sight.

Not yet, but many of the same underlying fundamentals are similar.

The bottom line is that much of the RE boom we have seen recently has been driven by debt fueled speculation which always ends the same way, especially when the bond market begins to exert pressure on the system which it has created.

Hard to believe it’s been 11 years, give or take, since “housing bubble 1”…. seems like just yesterday I was picking up 3 bed 2 bath “as is” homes for 60k…. (central valley) I can’t see that happening again with this economy, but as soon as the residential framers, Sheetrock, plumbers, etc etc get layed off…..Watch out! Question is, how much more can the big builders absorb before they send everyone home and leave a bunch of empty streets and house pads vacant for another 10 years…

After the tornado in Seattle you wonder what the insurance companies are thinking? Climate change isn’t real but the economic consequences are? One suspects consumers will be more inclined to rent, landlords will feel compelled to raise the rent, and local government will continue to try and pass rent control measures?

The insurers don’t really think, they are investors in the negative skew business. In a sense they don’t care what is real or not, they only track “the numbers”.

They will update their models, maybe take a look at what the 2’nd derivatives on the “loss model” parameters are doing. Tweak the odds a bit forward.

> Tweak the odds a bit forward.

How the fark do I short these assclowns?

Difficult. Usually it is easier to wait for some ‘100 year storm’ which happens every 10 years and then buy the stock low on the losses.

Over 3-5 years that is a likely 2- 300% profit.

Insurance is a pretty solid business. Because they run it on the numbers, like the bookies do.

Just to put the “Seattle tornado” into context. The tornado happened in Port Orchard across the Puget Sound from Seattle. I am not sure if a tornado could actually sustain itself long in Seattle given the building structures / pavement / etc. in Seattle itself. It’s been a while since I read up on weather, but I think they need specific hot / cold conditions which are rare here. I think they categorized it as a F2 in strength. These larger tornadoes have happened before – with the last larger tornado that actually killed people happening in 1972 I think and a large one in 1986. But Washington state has a few tornadoes every year with plenty of smaller twister / dust devils likely not being recorded as tornadoes. People new to the area and residents with short memories might think they never happen so they are increasing here but that doesn’t appear to be the case. What is likely a higher risk to Seattle area is an Earthquake or Mt. Rainier exploding – both events that are just a matter of when not if.

https://komonews.com/news/local/storm-survey-team-heads-to-gauge-damage-from-port-orchard-tornado

https://www.google.com/maps/dir/Seattle,+Washington/Port+Orchard,+Washington/@47.4625328,-122.4913328,10.53z/data=!4m14!4m13!1m5!1m1!1s0x5490102c93e83355:0x102565466944d59a!2m2!1d-122.3320708!2d47.6062095!1m5!1m1!1s0x5490362b813efd01:0x7b3b46c5baa649cc!2m2!1d-122.6362492!2d47.5403732!3e0

http://mynorthwest.com/category/earthquake_tracker/?

If I was an actuary I would be a climate change believer. There is also a school of thought that climate change affects earthquakes and volcanoes. FYI they have had tornadoes in LA as well. I know here in SoCa we have a hurricane season, which means bigger surf, but it could be a real storm season if the water off the coast stays as warm as it has been. Right now the insurance companies are losing money rapidly (stocks) and will need to raise rates to cover their losses. SoCa could not handle a FLA type storm.

Of course the lack of Chinese money was gonna have an effect on the whole country, I am surprised it took this long.

Wolf, do you share my suspicion that despite the huge YoY drop in sales in the West region prices there are still inching up only because increased giveaways to buyers are masking what would otherwise be a price drop? Perhaps our Santa-Rosa-area market maven Tom Stone could weigh in on that as well.

The West includes Colorado, Nevada, Arizona, Montana, etc… Many of those markets are still doing OK. That evens out the numbers.

– I don’t think Montana has a housing bubble ……….

Powell at least maintained the nominal illusion of independence for one more meeting in raising rates. Props to Wolf who of course said he’d go through with it.

With that happening it’s hard to see the downward trend in housing doing anything but being strengthed.

The real question is whether Powell and company will continue with the 2 rate hikes they plan for 2019.

Unrelated, I wonder how loud the sound of Trump’s head is right now as it explodes given how he’s made his presidential approval meter the down Jones…

I’ve been tracking mid-range (1-2M) Florida communities for about a year now. Eyeballing the data, houses are cut below pre-GCF prices, and still not moving. I’m guessing they’re looking at 75% cuts before they clear, IF they clear.

Entire communities were built upon a generation of pensioners who retired at 65 and would receive a paycheck for life. Some many demographic headwinds…

Zillow doesn’t think so. It has a data mining guru and his/her algorithm thinks the prices will rise 11% at least next year. So there.

If your iphone’s algorithm says it is raining outside and you don’t feel any rain when you stand out, whom do you believe? If you said the algorithm, congratulations, you must be a very highly educated person.

Do you have a link to this? Genuinely curious about the methodology of this insight.

Genuinely genuine. Literally. Millennial?

What I wrote above was based on what I saw on Zillow yesterday, a few hours before this posting. The home I was looking at was based in San Mateo, CA. The home sold originally for 560k in 2010 and is now valued at 1.5 million. The market in Bay Area is slowing down (I know this because the same homes now have open houses week after week unlike 2014/15 when they would go from ‘for sale’ to ‘sold’ signs in a few hours) yet Zillow told me that this home would rise in price by 10% in the next year.

After your question, I went back and tried to get it to show me the same message for the same home. This time, however, I saw no messages that gave me their expectations or forecasts for the next year. So I am guessing this being their website they are showing different types of messages to different viewers. They’ll have to show these kinds of messages again and I will post a link should I spot one.

Is Zillow, nowadays it has become famous for how accurate is not. And by nowadays I meant since at least 2015.

Now since this is the season of giving, anyone here at Wolf Street donates to charities or something during the holidays? I tend to donate money to churches sometimes during this season. I also like those things were they collect toys to give to poor children if is local.

And I better stop here before I go on a rant about computers and robots taking our jobs.

I like to stick tens and twenties in every Salvation Army bucket I pass during December. It’s a verified 95%-to-the-cause charity, and I can stay semi-anonymous. You send somebody a check for a few hundred bucks, and you spend the next five years throwing away daily solicitations from every known and unknown charity that buys a list.

Here in Sonoma County Inventory is up 77% YoY as of November, sales are down 30% YoY and the median price has dropped 9% since June 1st.

We’re a bit of a special case due to both the loss of 5K houses in the fires and the short term flood on Insurance money.

The influence of that Insurance money mostly affected rents and rental properties, the majority of home owners were substantially underinsured.

And yet the prices in Sonoma are still ridiculous

Yes, and they will stay that way for a long time. Even a 50% decline leaves the median above the national median, assuming national remains unchanged.

Can you share how you got these insights? Would like to look at my city (Nashville).

Thanks

Don’t see a problem in Socal Beach cities. Sales are slower, but decent deals are still being snapped up.

We are still very early in this cycle. Some people were in denial during the last housing crash until after 2010. There is always a gap between reality and perception….

Back in 2010, we were in the midst of a deflationary recession so houses took a hit. I doubt the central banks will ever let deflation take hold again. They learned their deflationary lesson and will front run any deflationary threat.

Also, that deflationary experience caused regulators to overreact with tight mortgage underwriting guidelines. The result will be far far fewer foreclosures in the next recession which drastically reduces potential real estate deflation.

This is true for big name banks and homeowners, but the downturn that will cause the next recession will be caused by the commercial crash.

Commercial RE is a nightmare right now, and when sales sputter in the states as the tax money dries up e-commerce will sputter. Look back on history and see the previous recessions, you will find different causes for all of them. The hard part is ignoring the last one to recognize the next one.

The last recession was based on the housing , this recession is much more broadly based, with bubbles in various areas, housing only being one. In addition, in the 2008 recession, at least there was some assets backing the debt, although they were overvalued. In this coming recession, much of the debt is based in large part on non assets such as education and stock buy backs which cannot be tendered even at reduced prices to satisfy debt.

If you think we are in a better position now than in 2008, you do not fully understand the entire situation.

Why do I feel like everyone on this blog tries to be like the guys in “The Big Short”?

No, you’re not Michael Burry.

Years I’ve heard of this bubble and nothing’s happened lol

Peace.