The vengeance of share buybacks: buyback queen Apple plunges.

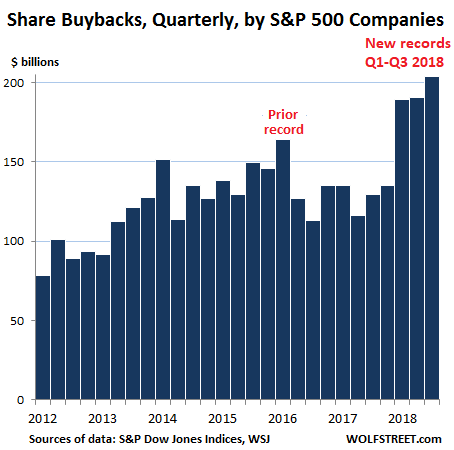

In the third quarter, share buybacks by S&P 500 companies totaled $203.8 billion, according to S&P Dow Jones Indices today. These are actual buybacks, not hyperventilated announcements of possible future share buybacks:

- Share buybacks in Q3 jumped 57.7% from a year earlier.

- This was the third quarter in a row of record share buybacks.

- For the first three quarters this year, buybacks totaled a mind-bending $583 billion.

- This $583 billion was up 34% from the same period in 2017.

- This $583 billion was within a hair of beating the full-year all-time record of $589 billion set in 2007 before it all collapsed.

- Since Q1 2012 — in less than seven years — all share buybacks combined totaled an even more mind-bending $3.54 trillion.

These share buybacks were funded by debt issuance and by cash, including cash that had been registered “overseas” for tax-avoidance purposes, where it was invested in US Treasuries, US corporate bonds, and other bonds. The new tax law allowed companies to “repatriate” this moolah under tax-advantaged terms.

And companies are doing this. For example, we have been seeing for over a year that US Treasuries held in tax havens for Corporate America, such as Ireland and the Cayman Islands, have plunged. So, companies are selling these securities registered in accounts overseas and are using the proceeds to buy back their own shares.

The effect on the economy is nil, but it was hoped that it would pump up share prices, and it did for a little while, but now the opposite is happening.

The report by S&P Dow Jones Indices explained that the buying “continued to be top heavy,” where the top 20 companies playing this game accounted for 54.3% of all S&P 500 buybacks.”

Alas, since the end of August, it seems, as companies have been buying back their own shares, just about everyone else has been selling them.

The fourth quarter is still not finished, and shares still have a few trading days left to get creamed further, and Q4 share buyback totals won’t be known until March. But given the 34% surge in share buybacks so far this year, Q4 share buybacks are likely to be another doozie. At the same time, so far in Q4, the S&P 500 index has dropped 12.6%.

To put a positive spin on skidding stock prices, the S&P report explained that the lower stock prices “would increase the number of shares a company can buy with the same expenditure and further increase the EPS [earnings per share] tailwind.”

So, following that logic to its conclusion: Let the shares plunge all the way; it’ll save our buyback queens some serious money. If it were just that simple.

The number one share-buyback queen in Q3 was Qualcomm [QCOM], which blew $21 billion on buying back its own shares, the third highest amount for any company in any quarter in history, according to S&P, behind only Apple’s share buybacks in Q1 and Q2 2018. Qualcomm’s stock price has dropped 23% since September 14.

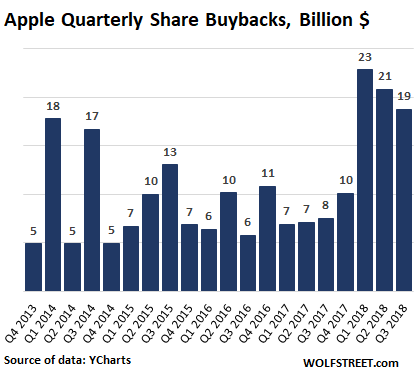

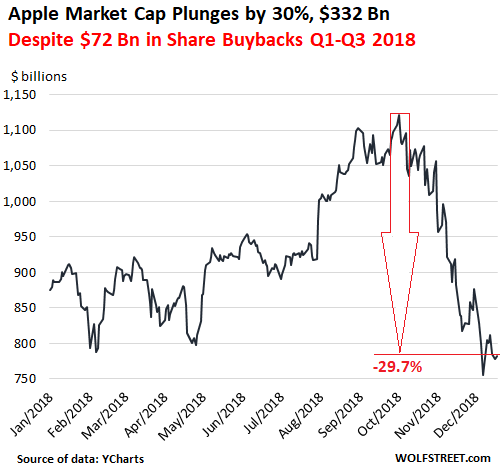

The number two share-buyback queen in Q3 was Apple [AAPL], which blew $19 billion on share buybacks. This brings its share buybacks for Q1 through Q3 to $72 billion. Apple’s stock price has plunged 28.4% since October 3 (data via YCharts).

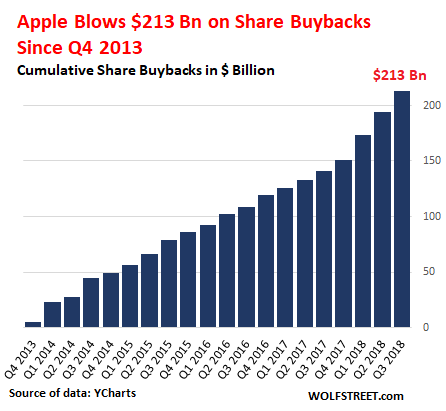

Just how immense are Apple’s share buybacks? Let’s say, they add up after a while. Since Q1 2013, Apple has wasted $213 billion on buying back its own shares (data via YCharts):

Since Apple is continuing to buy back its own shares in Q4, and is thereby reducing the number of shares outstanding, it is also reducing its market capitalization (number of shares outstanding times share price), even if the share price remains steady. But with the share price down 28.4%, and fewer shares outstanding, Apple’s market cap has plunged 29.7% since October 3:

This is the vengeance of share buybacks. They accomplish absolutely nothing productive. But they waste huge amounts of money – likely over $700 billion just in the full year of 2018 and $3.5 trillion since 2012 – that could have been used for productive purposes, such as inventing new things, building new plants in the US, and the like.

Share buybacks are a product of financial engineers. They’re designed to tweak earnings per share (by reducing the share count), create market hype and buying pressure to drive up the share price, fatten executive compensation packages, and overcome the dilutive effects of stock-based compensation and M&A. And since a good portion of them have been funded with debt, leading to record indebtedness and deteriorating credit quality of Corporate America, they will also contribute to real existential problems, such as those that GE is struggling right now.

Peak “Everything Bubble?” The data is piling up. A deep dive in my latest podcast, THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Share buybacks seems to be about as smart as someone borrowing money from one institution to make their savings account look fat in another.

One more reason not to buy manipulated stocks.

It is more like borrowing on your credit cards to pay off your mortgage. Which is even dumber.

No, it’s the contractor you hired to landscape your yard, deciding to use your credit cards to pay himself $40K to paint your house, but then saying “hey, it’s all cool, because according to HGTV, the new paint job increased your house price by $100K.”

The lemonade stand equivalent is borrowing forty dollars to turn your coins into notes.

And then shredding and setting fire to the forty dollars.

You have a forty dollar debt and high denominations with which to measure your net wealth.

Then you get your home value reassessed take out a line on your HELOC pay off the contractor and pocket the difference.

Actually it is taking out a third mortgage in order to pay back the credit card debt that is outstanding from Christmas 1996.

Paulo, agreed …but only to the extent of any manipulation component of the underlying equities valuation. Otherwise, we should be free to spend our cash or choose to borrow to buy whatever we want to buy. If that means buying a larger % of a company I already have ownership in, then so be it.

Let me put it another way. You like your VW van which you rely on to create income and/or simply like owning it, but assume so far you own only X% of it. You want to own a higher % of it and you have some cash and/or some ability to borrow. And furthermore, you think owning more of it is the best use of your cash and/or that it is actually undervalued to an extent that borrowing makes sense (especially if money has been virtually free for years!) Should you be allowed to buy a larger %????

Unless your intent is to manipulate the price of the VW van thus harming others, why the heck not? And consider that intent is a very hard thing to discern even if we are brave enough to try to honestly analyze our own behavior and intentions.

Like most things, buy backs can be smart or dumb, good or evil. Wringing the evil out while leaving the good alone requires assessing someone else’s intent. When we are able to regulate ourselves effectively, we might be able to do a better job of trying to regulate everybody else.

Perhaps they should just make stock buybacks illegal in companies that use stock and options in their executive compensation packages. Simple conflict of interest argument.

I still subscribe to the theory that we hit Peak 401(k) in 2017/2018. Going forward, the required distributions >> inflows. Even worse, is that because of how fast the job market is getting Flexed/uBer-fied, the inflows will be much less than projected.

The runup this year was almost all stock buybacks. And Wolf, you forgot another huge reason for buybacks. It allows insiders to sell huge chunks of stock in private transactions that wouldn’t cause the liquidation that would occur if regular shareholders sold. It’s almost as if they have their own lifeboats.

Wolf’s site is clearly worthy of contributions (and ad clicking) and comments such as yours keep me coming back as well.

What is the buyer thinking in the private transactions you mentioned? The insiders are the last people I would want to trade with!

I am obviously missing something as these buyers have much more capital that I do!

https://corpgov.law.harvard.edu/2013/03/14/questions-surrounding-share-repurchases/

“There are four principal ways a company can repurchase its shares, all of which are discussed below:

(1) open market purchases;

(2) issuer tender offers;

(3) privately-negotiated repurchases; and

(4) structural programs, including accelerated share repurchase programs.”

So if you’re a major shareholder (e.g. Sheryl Sandberg), how do you sell your 100M shares to get CASH without liquidating the market? Private-negotiated repurchases… Since the “buyer” and “insider” are practically the same, it’s really self-dealing.

If he holds rates tomorrow and drops the $50b’s, then stocks will take off again. Problem solved.

The cry babies want their last minute stocking stuffer.

Wolf,

You know what I see. You need to invest a few minutes into a couple of new acronyms.

One for companies doing the largest stock buybacks over the last 12 months. Then may be another that’s a combination of the largest buy back with biggest market cap loss.

I would guess that Apple probably fits into both categories. I bet you’d have quite a few interesting acronyms that comes up a la FANGMAN.

But fortunately, companies like these have figured out that investing in America is a huge waste of time, while leader Tim and his fellow captains of industry constantly decries the lack of manufacturing know how and capability, he has done almost nothing to help the situation. The same would be true for most of these folks. But then, you can’t argue with finding the lowest cost manufacturing sites.

Although it is just the height of hypocrisy to keep arguing for things like pay equality on the one hand, while on the other actively looking to outsource manufacturing to the cheapest possible locations. Thank goodness we have someone the media can actively bash without shining light on this little bit of duplicity.

– How much were the (commercial) banks involved in share buy backs ? Is there any data on that ? If they have done it then it’s more than scandalous. First they buy their own shares back and then the tax payer has to bail them out again.

After the financial crisis, the Fed prohibited commercial banks from buying back their shares or paying dividends. It’s only when they built up enough capital to survive the stress tests that the Fed allowed them to pay dividends and buy back their shares. I can’t remember when the first banks got to this point — maybe 2015. These “capital plans” are contingent on banks surviving the stress tests with certain capital levels intact. My understanding is that the process is currently under review to give banks more flexibility… the White House wants it so.

It seems to me, from a capitalistic perspective, that these companies are basically zombie companies. With little investment in innovation they are dependent on socialist intervention by the Fed (virtually zero interest rates) and share buybacks to have any value as a company whatsoever. And with the Fed working at letting interest rates rise and share buybacks not working as well, it seems the zombies are running out of food.

Wolf, your last paragraph in this article is a masterpiece. It summarizes what passes for capitalism among many companies in the US these days and with no reference to providing useful/innovate products and/or services shows why they are doomed, sooner rather than later.

Old Engineer,

If you have a “capitalist perspective” you will note the following problems:

1) financial engineering IS capitalistic

2) off-shoring, where you get the absolutely cheapest labor, is capitalistic; using Asian manufacturing to make goods, then sell them to the munchkins in the U S is near-perfect capitalism

3) allowing CEOs and boards of directors enrich themselves by having consulting companies explain to them why increasing both C-suite compensation and salaries of board members should be increased is capitalistic (gee, the same consulting firms are invited annually to do this research and consultation)

4) “manipulating” stock prices is capitalistic

5) the mythical “level playing field” is the last thing a company wants – they want moats and monopolies. Why? Because they’re capitalistic.

6) Lobbying (buying your political representation) is capitalistic

7) Zombie companies are perfectly okay in a capitalist economy, provided they’re enriching the board, the executives, the shareholders, if they’re lucky. Why demonize Zombies? You may want to include vampires. Sucking someone else’s blood is capitalistic, no?

8) When corporations are on the hook for bad executive behavior, their corporate charter includes the defense of their CEO, board, and other top executives, and all assets can be utilized for that defense. What’s not capitalistic about that? Corporations are people; they don’t want to lose their brains.

So what part of the capitalist system were you elevating? Regarding the “socialism” of the Fed: Did the average bumpkin get bailed out recently or was it primarily the financial industry? Who controls the financial industry – Walmart employees or the bankers? Most people consider bankers to be capitalists, at least the people I know do.

Time to take the fantasyland-Ayn Rand-colored glasses off. Socialism doesn’t work, but the “free market” b.s. isn’t the answer either. What we need and do not have is capitalism with some moral component that keeps the profit motive restrained in terms of helping the average American, not stripping them of their diminishing assets. There was a time when companies had social responsibility and accountability.

HowNow:

Correct!! I have nothing against “capitalism” itself. What I do oppose is “…..unbridled capitalism!” “Capitalism” is a life game. Like all games it needs rules. Those rules (read: regulation) that have been shaped to try to control uncontrolled capitalism have been stripped away and we have what we have today: A criminal/political/economic enterprise system. For a truly progressive society to survive, that “unbridled capitalism” needs to be restrained; a “firewall” must be structured to protect ordinary people from the destructive, distorted reign of (too) “free flows of capital.” We need rules. We need to jail those who break the rules. Without that we have modern, “Kings and Queens”…….until the rabble get enough and revolt.

The cheapest and most effective way to enforce a moral component is to enact severe penalty provisions that are high-level and conceptual in nature, so that they can’t be gamed. Companies and persons would then choose to stay away from harmful interpretations of laws. They will abide by the spirit of the law.

A sturdy penalty regime eliminates the need for large regulatory bodies.

Penalties work, and that’s why we don’t see them today. The crony capitalist world sees no need for them.

Yup! That is why fraud has become the business model. Imagine the damage to society.

You mean like before 1982 when it was illegal to perform stock buybacks except for very narrow set of reasons?

“What we need and do not have is capitalism with some moral component.”

Totally agree HowNow. UK is the same. Been swapping Tory and Labour for 300 years and still the same old ideas. France tried taxing the rich 75% and they all left. Need to reward the risk takers and job creators.

Government wasting billions and trillions on bond interest also goes under the radar.

HowNow,

Socialism is still socialism, whether it benefits the 90% or the 10%. And American companies appear to be almost totally dependent on government subsidies and protections at the expense of the U.S. treasury.

However, the real problem is when an attempt is made to justify the piracies that are capitalism morally. I think you are probably right in your assessment that capitalism has no moral foundations. But that doesn’t make it good for the 100% or for the country. And disguising what is an existential dependence on government policy as “free market” capitalism is just hypocrisy and self delusion.

And, by the way, it appears that you are right. The failure of the socialistically dependent U.S. companies gives evidence that socialism is not the panacea for incompetent and failing companies.

Capitalism is when Sears employees get no severance, but the top execs walk off with $25mn for running the company to the ground.

When these same ex-employees line up for unemployment benefits and expect “entitlements” like Social Security that they paid into, they are socialist moochers.

HowNow, an impressive list, but what you have largely described is crony-capitalism. There has been a steady march to it in the US. Crony-capitalism is almost always conflated nowadays with capitalism – the degree of this conflation indicates a broad-based intent. We should ask why we don’t have honest assessments of capitalism anymore.

True Capitalism is certainly brutal and survival of the fittest is also unattractive to many/even most UNTIL they consider the alternatives objectively. Rand did that analysis and to a depth that few have bothered. What we have today is very far along the path that she was warning about …more than half a century ago. To think that what you listed above is what she was advocating is mistaken.

If Rand was missing something important ( and I think she did), it was not related to economics, it was related to morality. She took a shortcut on that and concluded that her version of morality existed within materialism. This is a gross oversimplification. Said another way, she admired Aristotle and she discounted Plato. We do owe all of economic success to Aristotle, but a lack of understanding Plato is why we have many of the problems that we do.

Despite her mistake, she at least placed morality at the correct level – the individual. Companies, governments and other groups have invented their own versions of morality, but most have been found sorely lacking.

Thanks, Sedarcos, for the clarification and erudition. Can you elaborate a bit more on the differences btwn the philosphers? I don’t think of Plato or Aristotle in economic terms, but it may be there.

But your comment about “crony-capitalism” being something other than capitalism is, imo, a distinction that shouldn’t be made. Here’s a working def. of capitalism: “an economic and political system in which a country’s trade and industry are controlled by private owners for profit, rather than by the state.” Why isn’t “cronyism” an inevitable outcome of capitalism? We may sniff at the obscene behavior of financial engineers who over-leverage companies to the point of destroying them for their personal gain, but, hey, isn’t that capitalism at work?

We all want a moral compass working in business for the general benefit of humankind. But, it was there and no longer is. It needs correction and labeling it “socialism” and advocating “free markets” is simplistic.

The problem with every “ism” is people. And every government, corporation and business is made up of people. We are never actually going to solve the problem because we are the problem.

How Now:

Why can’t we offshore CEO’s too? I mean we can surely go to India and find bright English speaking MBA’s (ala Jack Welch) to supplant the top five corporate heads. Look at all the money and perks the Corp. would save. This would be capitalism working its finest.

Thank you, HowNow.

Bailing out private, for-profit entities, at the expense of millions of ordinary people, is the antithesis of what socialism aspires to.

There is nothing wrong per se with share buy-backs. It’s essentially the reverse of a public offering, whereas public offerings are often done by young firm to raise cash in order to accelerate their growth. For large firms sitting on a pile of cash it allows them to increase the ownership stake by taking share off the market. In that sense it’s not just a sugar injection, but a lasting boost to the underlying value of the stock. As far as I can see Apple’s buybacks were prudent long-term focused actions and even with the spill that’s wiped out all the gains the company’s stock made this year, long term share-holders are still better off then they would have been otherwise

Where stock buy-backs have become poisonous is when they are financed with debt. What’s particularly onerous is the justification that a company’s own stock can represent the best investment of a companies capital. That puts the company in the business of share manipulation rather than in producing some tangible good or service, which is exactly where executive management shouldn’t be holding their short term attention.

There is plenty wrong with it because it is used to manipulate share prices to enrich the few at the expense of the many.

That seem simplistic. If you own the stock, no one is forcing you to sell or to hold for that matter.

Wolf’s point is that buybacks are wasteful and value destroying. Look at Amazon, I don’t think it has bought back much of its own stock, it has reinvested its profits to expand on the business. Hence not wasteful.

The idea of buybacks enriching only a few when it is done on open market is a bit far fetched. It isn’t as if the buyback was not open to the public. Value destroying, yes, enriching a specifically select group, no.

Just because it’s done in the open market doesn’t mean it’s not manipulative. There are plenty of open market practices that are bad and have caused regulations to be put in place. Stock buybacks were illegal for decades because of their inherent shadiness. The execs and BoD set a price to shrink shares, which drives up share prices usually allowing them to hit targets to enrich themselves.

@Matt

Your point was originally “manipulate share prices to enrich the few at the expense of the many”

So, are you changing your tune now to just that it’s manipulative? Cause, yeah, no kidding, it is.

And seriously. Have you even read Wolf’s article. His point is that all this manipulation hasn’t helped the share prices at all. And let’s be honest, if Leader Tim need to manipulate stock prices to enrich himself like backdating Steve did, then he deserves to go to jail. But so far, all of his buybacks hasn’t done squat for the execs or the BOD. And hasn’t done much for most of the other execs either, they could’ve done just as well dousing the money with gasoline and lighting it on fire.

Just because wolf points out the stock prices are dropping even in the face of record buybacks, doesnt not mean that the premise that stock buybacks are meant to goose share prices is not true.

The implication is that stocks are in worshape than they appear given that companies are buy shit loads and still managing to be out run by stock sales by the public.

Yes. It benefits anyone who is selling, which can be the executives who temporarily goose the stock value but may know they are not investing in the company’s long term future.

(In other words, not everyone benefits, but selling executives certainly do.)

Hmm, going in to a recession or whatever they come up with to call this next downswing of the cycle, seems like a company would want a lot of cash.

Which means if this economy swings downwards, Wolf will be doing a story in the future about the company that wasted its cash during the good times, and how much the executives walked away with big bonuses, but now how the company is going under as revenues fell and money got tight and expensive.

Of course, to the people now making these decisions, the important question is how much did they grab for themselves before the bottom falls out. Ooops, there goes another company. Ooops, there goes thousands of jobs. It must suck not to be a billionaire.

Kind of like neighborhood NIMBYs blocking all development/up-zoning/transportation and infrastructure projects to artificially boost their home’s value, whilst driving up cost of living and driving down quality of life for everyone else?

Same difference.

Earl D – ‘That puts the company in the business of share manipulation rather than in producing some tangible good or service’. I understand that in some countries it is illegal for companies to buy their own shares, for that very reason. Why is it not illegal in the US, whether with cash or borrowed money ? (Rhetorical question of course.) If I were a shareholder I would be asking hard questions, except of course if I had also benefited from the same buyback scheme. Let’s see how this pans out as the market keeps dropping – will companies who made large share buybacks get hammered harder than those that didn’t? Serves them right if they do IMO.

re: “… I understand that in some countries it is illegal for companies to buy their own shares, for that very reason. Why is it not illegal in the US, whether with cash or borrowed money ? ”

“Buybacks were illegal throughout most of the 20th century because they were considered a form of stock market manipulation. But in 1982, the Securities and Exchange Commission passed rule 10b-18, which created a legal process for buybacks and opened the floodgates for companies to start repurchasing their stock en masse.”

https://www.vox.com/policy-and-politics/2018/3/22/17144870/stock-buybacks-republican-tax-cuts

The funny thing about share buybacks is it shows up as earnings at the end of the quarter. Analysts estimate earnings and then the company will make sure to beat earnings estimates with share buybacks at the end of the quarter. Rinse, repeat.

It’s not a “lasting boost” The bump in the stock price is almost always temporary. I worked for JC Penney. Back in 2011, they were having troubles, and elected to blow almost a billion on a stock buyback. The stock price jumped for a few months, then proceeded to makes its trip toward the bottom. They could have retired 25% of their debt, or made long overdue upgrades to their fossil of a supply chain, but they took the Pump and Dump route. My wife and I had a lot of company stock in our 401K’s back when it was climbing. There was absolutely no reason for it’s rise–the two big problems they had/have–debt and an expensive, antiquated supply chain, were never fixed. We sold at $82 a share when the stock topped out. It is now $1.20, almost a Penny stock (rimshot).

If a company has healthy financial basics it do a stock buyback. It may not be a waste of money. In most cases, it just allows the insiders and Wall Street gamblers to make a quick buck. It isz of no long term benefit to the company or its stockholders.

Share buy backs used to not be permitted. It really should be illegal. The ONLY possible beneficiary, is the CEO, and top company insiders. How much of the $3.2 trillion in buy backs, has been funded by debt issuance ? That’s even worse than the repatriating of cash. So their stocks will crater during the inevitable crash, and their debt will still be looming like a boat anchor with rope attached to their necks. Imagine Warren Buffet buying all those shares of Apple, right when they are doing buybacks. Too much money sure makes a lot of formerly ‘smart’ people do some really dumb things. They should have sent their $3.2 trillion to Uncle Sam, to pay off a chunk of the national debt.

Another Mike R. I’ll have to change to Mike Are; have posted here quite awhile. No problem.

Regarding buybacks, my theory is that this was all orchestrated during the Obama administration to keep stocks up. The deal was that if needed, the Fed would monetize the corporate debt in another QE.

I still believe this is going to happen. Of course there will be some big winners and many losers as there are too many companies for this shrinking economy.

There were buybacks before Obama. The last time repatriation from overseas happened in 2004, companies used that free dough for buybacks and compensation

Countrywide CEO used 180 million In buybacks to support shares for some 18 months while he liquidated. Mozillo or whatever the crooks name was.

Aapl and BA and QCOM are the buyback leaders now. All close to or at 20 billion in buybacks. Booyah

“This $583 billion was within a hair of beating the full-year all-time record of $589 billion set in 2007 before it all collapsed.”

This was happening before Obama.

The market is way overpriced partly because of buy backs, government stimulation, low interest rates, ECT ECT. Buy high sell low. Companies that are buying back their shares want those shares to short them. After 2008 they won’t get away with doing the naked short tactic again.

The logic puzzles me, why would a company want its own shares in order to short them? I could see why they would want to control the float so other investors could not borrow their shares, and deny the shorts what they need. The exchange can ban short sales and it won’t matter because many of these shorts are synthetic using swaps and derivatives. If you are wondering what happens when the counterparty yells uncle, I suspect they simply find another counterparty to underwrite their short, since there is no central market, on the downside it becomes a daisy chain. We are getting near that place where the stock market is exposed for what it is, a money printing machine for government economists, and stock trading is hereafter conducted on a futures exchange.

Agreed….thank you Earl D for your assessment that seems to be missing in both content and replies of this article.

That’s because it’s an assessment we don’t agree with…hence why would it be in the content of our replies created to rebut? Daft comment.

Isn’t there..?

In the days before we had mass financial deregulation and unfettered greed was encouraged resulting in the enormous continual booms and busts which have resulted, it was illegal, as quite obviously it’s stock price manipulation.

It encourages laziness amongst senior execs, who rightly see it as an easy way to run a ‘succesful’ company which in reality of course is gradually withering on the vine due to malinvestment. It stifles development (hence job creation) as resources are channelled into stock purchase.

Nothing wrong with it ‘per se’..? Delusional to say that IMO.

Share buybacks are fraud. And buybacks were illegal until the early 1980s. Just because legalistic language says it is okay does not mean it is not fraudulent.

I actually don’t understand why a legitimate listed company would do a share buy back unless it sees no future expansion and has excessive surplus cash.

Why would a listed company borrow money from a bank to buy shares back?

Apple in particular is in a strange place. I don’t think the problem with recent products have been lack of spending, so simply spending more on it probably isn’t the best idea. Many of the acquisitions (Netflix) that journalists have mentioned in articles don’t make much sense. The best option probably would be to have blue sky development or actually invest in its own manufacturing, but even those wouldn’t move the needle on its huge cash pile.

But the worst option probably was borrowing cash to buy back stock for reasons we’re all familiar with.

Apple’s problem is that they don’t have a Steve Jobs to tell them what to do. Leader Tim has all this cash, and he has no clue what to do with it outside of dividends and buybacks. Sure, they spend a lot on R&D, but they don’t know what to do with the results of that R&D. Just like you said.

Heaven forbid that Apple would do manufacturing. It would be too inefficient given the existence of companies like Foxconn. (I am not being sarcastic here)

Agreed. The only reason Apple should invest in its own manufacturing would be if they think the supply chain might be broken by on-going politics.

Right now Apple gets the overwhelming share of profits from its products’ supply chains.

Steve Jobs once commented that Tim Cook is a financial genius, but not worth much when it comes to product development.

Cook committed his first sin when he greenlighted the iPhone 6S Plus, not so much because it was a bad product, but because it started the trend of cannibalizing one of Apple’s most profitable product lines: the iPad.

From then on Cook’s tenure has been one of financial brilliance but of continuous small mistakes when it came to product development and placement, which resulted in Apple having effectively devolved in a one-product-line company.

There isn’t a whole lot left outside the iPhone, especially since Asus has been eating sales of the MacBook Pro by aiming their high end laptops squarely at Apple customers. It was a smart strategy which is paying dividends for the Taiwan company.

I am saying this as an Apple customer, and I would have already dropped the iPhone as well if I weren’t genetically adverse to Android. Those new Chinese smartphones from Huawei, Honor and Xiaomi are really slick and well made products.

Regarding manufacturing… companies are starting to move out of China, not so much because they fear disruption, but because wages in China are growing too much for their liking and finally executives are waking up to the stupidity of handing their own expensive patents and manufacturing processes to future Chinese rivals in return for saving some money. Robert Bosch (automtive electronics) and Zama (fuel delivery system) are moving part of their manufacturing capacity from China to The Philippines, Samsung has shifted part of their smartphone assembly lines to Vietnam and Sony is firmly committed to Malaysia.

It won’t be long before Apple follows suit.

China knows the cure for its own dependence on cheap labor, given the demographic time bomb that’s rapidly wiping out base consumers, Chinese factories have already started the shift to robotics at least four or five years ago.

The biggest problem that China has now is a perception one. This might very well stunt China’s growth. Comrade Xi screwed up by deviating from Deng Xiaoping’s path, which was to be as quiet and humble as possible so as not to attract negative attention while growing China.

Xi’s China 2025 plan has put a big bullseye on China, and now you see the world pushing back much harder. People are wary of Chinese control on infrastructure, western countries no longer want Chinese capital to buy up their companies and the real estate, Chinese companies aren’t as welcomed into western markets. All because fat Pooh couldn’t keep his pride in check, in China, at least a few years ago, people were really proud of Xi’s declarations. But now, China gets to pay for it, I think this is largely done at the behest of the US, but other countries were already not happy about it.

I disagree however about eg iPhone 6S, I think that product was in then planning stages when Jobs died, but more than that it was probably a smart business move. Apple saw that Phablets were stating to eat into iPad market share, and they probably realized the iPad was going to get cannibalized. So, they figured that they might as well do the cannibalization themselves. I think it was a sound decision.

However, what has happened since then is that Apple keeps iterating the phone, sometimes in needless ways. You can tell that they don’t have any real actionable ideas in terms of a product, and leader Tim has done nothing on cloud for consumers. You could easily imaging something like Google photos as a product at Apple, but that hasn’t happened. In terms of software, the execution has been really poor. Leader Tim isn’t flexible that way, I agree, may be a financial genius, but he is essentially like Ballmer running Microsoft, tons of profits. But getting left behind as they keep trying to protect the phone business.

Unless they pull out of it, it will be the end of Apple. They are fast on their way to becoming the next Kodak without Jobs.

Hey, Apple coins, anyone?

Here here! Apple went ex-growth when SJ died and took his vision of the future to pastures new. Since then TC has merely capitalised on what was in development but has come up with nothing new and exciting. The gravy train is running out of steam. Pity really because I am an Apple customer partly because the hardware and software is brill but also because the alternative is too awful to contemplate.

Wow! How do they legally get away with this? Give a good indication how corrupt the bloody system is. I’m feeling it’s systemic throughout the whole internal structure, built, and implemented since WW2, though by design, even prior to Frances Civil war? planned and executed by the Rothschild Cabal

How do you dismantle something so large, so integrated and corrupt, not in weeks or months but possibly even decades, if at all! There is an answer!

By the use of Force! (Their own tactic)

Are the populists, UP FOR IT?

France and some other nations are leading the way, the wick has been lit, but will the populists rise up to ignite a flame, underneath the movement, as momentum, weight, endurance, strength and spirit, will be needed to be called upon, by the people and for the people! Are you, up to the task?

When Congress passed this tax bill they should have specifically outlined that the 21% corporate rate would be contingent on specific US capex investments which would have stimulated US economic activity. One little known part of this tax law is an 8% corporate tax rate for investing in US commercial real estate capex. Amazon is actually using this tax break and Apple also (think Trump). Sometimes I think our Congress has the IQ of a cucumber…

On December 13, Wolf wrote, “But not even Congress is that stupid.” in an article, ‘US Banks Disclose Biggest Unrealized Losses on Security Investments since Q1: FDIC”

My comment was, “Never underestimate your opponent.” But Sadie, you’re spot on with the IQ of a cucumber line. To be fair, Congress does, for the most part, what its handlers (lobbyists, money suppliers, Dem or Rep party lines, etc.) instruct it to do.

Apple has been sitting on cash in a time when the central banks have kept interest rates artificially low, so I understand Mr. Cook’s dilemma about what to do with that cash. However, IMO share buybacks should not have been his choice. As Wolf so accurately states, “Since Q1 2013, Apple has wasted $213 billion on buying back its own shares …”

Instead, Apple could/should have used that cash to increase the annual dividend to 7% of its stock price. Currently, Apple’s dividend yield is 1.76%.

Dan Romig,

Don’t forget: Apple now has $114 billion in debt that it didn’t have before it started the buybacks. In other words, some of the buybacks were funded with borrowed money.

Apple’s debt is not a worry at the moment. Unlike many of the corporate borrowers, it has the cash flow to pay off its debt.

The bigger problem for Apple is what’s next. They don’t have a visionary guiding them any more, so they are meandering. May be they will come up with something. But it’s a long time coming.

Dan, Amazon has been buying/leasing warehouse space all over the US. They are creating investments and jobs and wisely using the corporate 8% tax rate rule for profitable commercial real estate investment/job creation. If I had to guess, Trump probably had a hand in this little known tax rule since he is a real estate business man.

Indeed. None of us are as dumb as all of us ….and that is what Govt/congress represents.

Well put, Setarcos!

When the tide goes out, you find out who’s been Swimming naked. Looks like the tide is going out.

*This $583 billion was within a hair of beating the full-year all-time record of $589 billion set in 2007 before it all collapsed.*

I am the only one that finds that worrysome? I mean even adjusted by inflation is still close.

“could have been used for productive purposes, such as inventing new things, building new plants in the US”

Which would warrant stock price increases. As soon as a company begins buying back its own stocks, it’s a certain sign of long-term decline. But in the short term – party like it’s 1999.

“As soon as a company begins buying back its own stocks, it’s a certain sing of long-term decline”

The other possibility is that the company is minting so much money (perhaps due to a monopoly or pseudo-monopoly) that it just cannot put that money into R&D. You can only grow so fast without wrecking your company’s culture and screwing up future products. I am not sure this is still true of Apple but it used to be true of them.

Does buying back stock reduce the float so a company can be less easily taken over? I don’t know. Other than that, one would think excess cash if not invested in the business (not through buybacks) would have to be distributed to shareholders. At least that way the shareholders can vote with their dollars to buy more shares if they feel the company’s future prospects look rosy. Otherwise, they are free to sell their shares if not. A company buying their own shares may be a strong sell signal.

Phil’s comment resonates with a comment I made some weeks ago. I asked if anyone knew the bookkeeping method that Companies use to account for buy backs. Do they “dissolve ” the shares and contra against their cash or the fresh borrowed cash? Or do they create a separate asset item on the balance sheet ? In one case the shares held by shareholders are reduced but the bought back shares still exist. In the other case they completely disappear.

The ongoing difference is that in one case the shares can go up in value and lead to an increase in profit which is just financial engineering. In the other they just lead to an increase in EPS.

Either way it is just financial engineering enabling unjustified share price increases which are linked to senior employee and Director bonuses and a route for the beneficiaries to disposes of the bonus shares without the downward price pressure that would normally result from those shares being sold.

Overall except when clearly explained to all shareholders giving them a greater opportunity to assess for themselves the extent to which buy backs are taking place and the extent of the buybacks and bought back shares held for subsequent controlled selling on an underlying bull market, they should be illegal.

method that Companies used

Furthermore, not only do these buy backs benefit management by levitating EPS in order to trigger remuneration clauses, they can also help recycle management’s shares and share options. They can convert their shares and share options into cash at a higher price, and restock treasury with the newly bought back shares that they at a later date can award themselves shares from and options on.

It would be interesting to see some statistics over a longer time frame showing how large a portion of the companies engaged in buy backs actually persistently maintain a lower number of shares outstanding.

I’ve read more than once that Foxcon’s advantage in building Apple products is no longer one of cheaper labor, but rather one of superior manufacturing organization. Something that has become as lost in the USA as superior skills as a mule driver. Meanwhile Apple has become just another advertising and fashion company. One facing accelerating margin compression and a stock price moving toward realistic valuation of it’s actual contribution.

The horizon for business decision making in corporate USA is at most quarterly (or whatever the time frame for determining executive bonuses). However dysfunctional the Chinese system for capital allocation is, I can guarantee that they think further ahead than that!

The Chinese IT goal for the immediate future is to acquire next generation chip making processes that leapfrog current Western practice. The goal is twofold: cut themselves off from dependency on the US and be able to produce superior home-grown advanced weaponry, and perfect population surveillance and control technology to keep the lower classes under control.

At least they will find a ready buyer in the USA for the latter.

After reading APPL’s $213 B in stock buybacks over the last 5 years, I had to compile a brief list of things that cost that amount of money or less:

(All amounts in $2015 $)

1. Apollo Space Program: $105 B.

2. Three Gorges Dam: $48.1 B

3. Manhattan Project: $30.6 B.

4. Boston’s Big Dig: $24 B.

5. Colorado River Aqueduct: $3.2 B.

Doubtless, to be realistic there should be some “hedonistic” adjustments made to the older projects. Would SpaceX really let paying astronauts fly in the conditions the Apollo astronauts did? Also the Three Gorges Dam amount is Chinese state sourced numbers and possibly suspect, but the real number is probably not over $213 B.

When Facebook bought WhatsApp, somebody made a Tumblr site called Things That Are Cheaper Than WhatsApp: http://thingsthatarecheaperthanwhatsapp.tumblr.com/

um, perhaps supporting a rising stock price is not as effective an investment as supporting a declining stock price.

does take courage, though.

“but everybody’s having such a good time.”

$213 billion in buybacks works out to almost $200 per iPhone sold. Yay!

Looks like a giant misallocation of capital.

I bet these are the same folks whining about the rise of the Fed funds rate.

The very same folks. Thus the editorial in the Wall Street Journal imploring Powell to take a “rate pause”. Those same folks are also whining directly to the President and Whitehouse officials, begging them not only to rein in the Fed rate hikes, but to stop the $50 billion per month balance sheet normalization as well. Thus Trump’s angry tweets over the past few days demanding no further rate hikes and “Stop with the 50 B’s.”.

So Wolf how important is this thing they call “Market Capitalization”?

Instead of “investing” in buy backs they ought be investing in blockchain.

Share buybacks for 2018 will be $1 trillion.

https://www.cnn.com/2018/12/17/investing/stock-buybacks-trillion-dollars/index.html

If this isn’t all the proof needed for Powell to continue to raise rates, I don’t know what is. The fact that companies think it pays more to buy back shares than to invest in productive capital or to pay down debt, or failing that, to park the cash in treasuries in order to invest in productive capital at some opportune future date, then they are still responding to some perverse incentive. That perverse incentive is an interest rate that is still too low.

Poor Fed.

When too may revelers are getting drunk at the party, the host should end it, but that’s mighty unpopular with the drunks.

You wrote “The effect on the economy is nil, but it was hoped that it would pump up share prices, and it did for a little while, but now the opposite is happening.”

This statement implies that stock buy backs are at least in part causing the decline in equity prices. This is misleading. The rise in equity prices was caused by FED which tried to create the wealth effect with easy money policy. The rise in equity prices was thus artificial. The decline is mainly caused by the ending of the FED’s easy money policy. Cause and effect is a chain and we must go all the way back to the 1st cause.

This also ingores what equity prices would be if there were no buy backs! If the FEDs desire to create the wealth effect is okay, then how the heck is it wrong to try to react to that policy?

Let me clarify, getting to a 1st cause is difficult, but we are best served by tracing problems as closely to the root as possible. Buy backs are not even close to the root cause in the case of equity prices overall.

When stock buybacks are funded with debt (even Apple took on $110 billion in debt to fund them), they can cause the company to get credit downgrades (happening all the time) and can eventually cause the company to go bankrupt because it has too much debt (this includes Sears and might include GE). Stock buybacks, even when they’re funded with cash, destroy the equity of a company and make it more leveraged. At some point, stock investors get a whiff of the credit risk involved.

Credit risk correlates to interest rates, so even if a company (or government) loses grade, if interest rates go lower, the credit environment lifts all boats. The point of this exercise is will Powell bail out Apple’s share buyback program by pausing rates? At issue is their mispricing of risk (2008 redux) as well as corporate HY, whose collapse is a yawn. CRUDE took another leg down, confirming cheap money translates to cheap oil.

“Stock buybacks, even when they’re funded with cash, destroy the equity of a company and make it more leveraged.”

Didn’t that used to be called “watering the stock”?

When you write that “…buybacks, even when funded with cash, “destroy the equity of a company…” , I am reminded that I used my cash to “destroy” my mortgage. A perfectly reasonable even prudent thing to do suddenly sounds almost sinister. You do your readers a great service, but that choice of words simply serves to lump all buybacks together as being bad. The issue is not so one-sided.

Setarcos,

Paying down your mortgage with cash is the opposite of what borrowing money to buy back shares is.

In basic accounting terms (modern double-entry accounting): assets = liabilities + equity.

So turn the equation around: equity = assets – liabilities.

When a company borrows $100, it triggers two entries: Assets (cash) increase by $100; and liabilities increase by $100. Equity remains the same.

When this company buys back its shares with this $100, those shares get canceled and disappear, but the cash is gone too, and the liability remains. If this company buys back shares with $100, it triggers two entries: assets (cash) drop by $100 and equity drops by $100 because the shares have no value after the company buys them since they get cancelled.

After it’s all said and done, this company ends up with $100 more in liabilities and $100 less in equity. This is how equity gets “destroyed.” The company is now MORE leveraged.

When you pay down your mortgage by $100, it triggers two entries on your personal balance sheet:

Assets (cash) drop by $100; and liabilities (mortgage) drop by $100. Equity on your balance sheet remains unchanged — the equity in one of your assets (house) increases by $100, as another one of your assets (cash) decreases by $100.

But now you’re LESS leveraged because you reduced your debt, and this is prudent.

As usual, I was not clear …my issue was using the word “destroy”. I understand the accounting. To call cancelling shares and concentrating ownership destruction seems over the top to me. No matter how many shares a company has outstanding, ownership always totals 100%.

I am not defending price manipulation. But washing a car is unlike rolling back an odometer.

Setarcos,

“Equity” on the balance sheet has nothing to do with “100% ownership.” On the balance sheet, equity = “stockholder equity” = “net worth” = “book value” of the company: assets minus liabilities. Like equity in your house = value of your house (asset) minus the outstanding mortgage (liability): asset – liability = equity.

A $100 share buyback destroys $100 in “equity” or “book value” or “stockholder equity” or “net worth.” It’s just that simple. That’s how it works. The company is paying $100 for something that has zero value for the company because the shares get canceled. “Destroys equity” is a very precise term for this procedure.

In the trade war between China and the USA, APPLE is the trench line where the battle might well be fought. APPLE has invested huge values in plant and equipment and property throughout China, therefore it is reasonable to assume that China knows how much activity is happening within APPLE’s entities based in China.

APPLE is therefore very vulnerable in US/SINO trade war.

Share buybacks? Companies, and their agents, should not be permitted to purchase their own shares/stocks. These purchases create the false impression that there is a level of demand for these shares. Also these purchases nominally have nothing whatsoever to do with the commercial/operational performance of these entities.

In many cases in fact these buyback purchases are done to try to disguise the weakness of the commercial/operational performances of those companies.

Paul Morphy, perhaps we should not allow them to decide how many shares to offer initially to the public either. For that matter, why even allow them to sell us shares at all? If more than 1 person is involved in any trade, someone can easily be deceived. Heck, most people make a habit of deceiving themselves on a continuous basis and then blame anyone but themselves for their results.

Take a look around. How much of what you see could have been invented, produced and distributed simply by using the capital of 1 person?

Share Buy-Backs tell me these companies know the global economy is moving downward as the supply of stuff has outpaced demand. That is why they are not investing in more production. As for the buy-backs, I agree they should be illegal.

As for Apple, I have an iPhone 8, a iPad mini, and the new iPad Pro 12+ inch screen for my old eyes as I can blow up the small print. I also got their keyboard for it. Wow, what a difference in typing speed.

I bought an iPhone finally after all my family members were using text to communitcate instead of calling. My son said if you want to comnmunicate with the younger members of the family you need to text. I had a flip phone until August 2018. But being the oldest and sometimes stubborn, I changed my atittude to stay in touch. I can say I now like to text over calling. Allows one not to stop doing what you were doing, as you can answer a text hours later.

I have used Apple for customer service three times and I can say they have the best customer service by far of any company I have dealt with. Every time the problem was solved and you talk to someone who can speak English.

A few questions re: the article / comments section

1) What is the role of a CEO? Managing / setting direction for the operating business? Determining optimal capital allocation?

2) What role are institutional investors playing in the buyback mania? There’s been a push to passive whole-market ownership in the past decade. Hence, there’s growing influence from the likes of Vanguard, Fidelity, Blackrock, etc on company managements. If the excess cash is to be returned to shareholders, might the institutional managers be another culprit for the increased use of buybacks? Share repurchases are the more tax efficient means of returning money to shareholders.

3) To what degree do poorly conceived management incentive structures (i.e. incentives don’t align with those of shareholders) contribute to the buyback mania? Do large institutional money managers not have the spine to have a voice in setting how managements are compensated? If not, is this a breach of fiduciary duty on their part?

And a couple of comments:

Ben Graham, at least in the second edition of Security Analysis, spoke strongly against open market share repurchases (prior to the SEC). From what I recall, he believed share repurchases to be taking advantage of existing shareholders from an information asymmetry perspective. Additionally, there is discussion on an average management’s poor capital allocation abilities, and that in most cases, shareholders would be better suited to receive dividends rather than share repurchases. It is interesting that nothing seems to have been learned from history!

This all being said, there are some examples where share repurchases have been the most logical use of excess cash (Thorndike’s Outliers; also read: excess cash, not debt-funded): when the future return on growth CapEx is, relatively speaking, low and when shares are deeply underpriced relative to their intrinsic value. In this case, perhaps a tender offer, and not an open market repurchase, would be both amenable to Graham and the optimal mechanism for existing shareholders. Note that these instances would likely be rare.