But this time it’s not a result of a tech bust. That hasn’t happened yet.

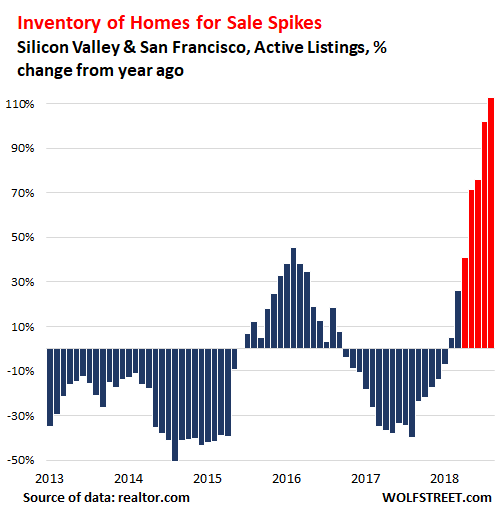

Housing inventory listed for sale in the two counties that make up Silicon Valley – San Mateo County and Santa Clara County – and in the county of San Francisco, surged by 113% in December compared to December last year, to 2,691 active listings, the most for any December since 2013, when the area emerged from Housing Bust 1. December is usually near the annual low point in terms of listings, but not in 2018, when listings in December were higher than in each of the first five months that year.

The chart below shows the year-over-year percentage change in active listings. The bars in red denote when the underlying dynamics of the housing market changed direction (all data via the National Association of Realtors at realtor.com):

The shift is now becoming more obvious in Silicon Valley and San Francisco, among the most expensive housing markets in the US with median prices for single-family houses ranging from about $1.2 million in Santa Clara to about $1.5 million in San Mateo.

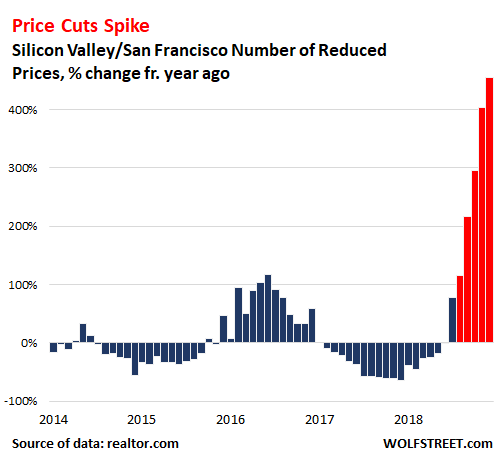

With inventories for sale rising, as sales are slowing, a whiff of competition is settling in among sellers, who have to determine where the market is today, not where it was last year, and if they want to sell their property, they have to price it where the buyers are. But buyers aren’t where they were a year ago, and the bidding wars have receded into history, and mortgage rates have jumped from a year ago. The right property, priced right will sell. But if it’s priced off the market, it will likely sit. This is starting to sink in. And sellers are cutting their asking prices.

In December, the number of properties on the market with price cuts in Silicon Valley and San Francisco combined skyrocketed by 455% from a year earlier to 444. This chart shows the year-over-year percentage change for each month, with the red bars denoting when bubble trouble began:

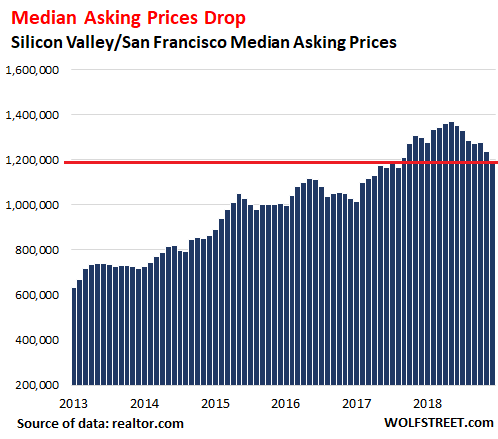

The median asking price for the three counties had peaked in May 2018 at $1.37 million but has since plunged by $170,300 or by 12% from the peak, to $1.2 million. Median asking price means half the properties are listed for more and half are listed for less. It differs from the median selling price at which homes are actually sold. This was the lowest median asking price since August 2017:

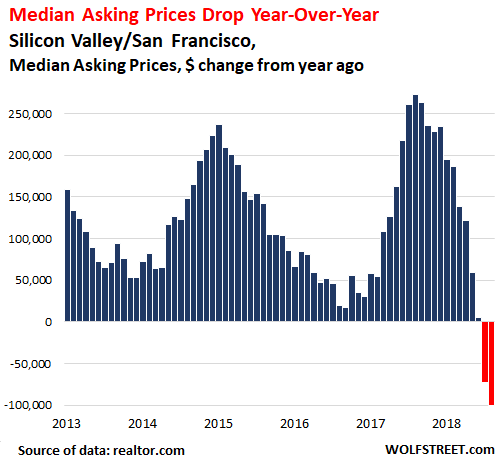

Compared to December last year, the median asking price dropped by $100,000 or by 7.7%. The chart below of year-over-year dollar changes in median asking prices shows to what extent a new sense of reality about the direction of the market has crept into asking prices over the past two months:

And these are still the boom times in Silicon Valley and San Francisco. There is some anecdotal evidence that some of the tech companies are slowing down some moonshots or expansion projects or are cancelling later phases, and some startups have trouble getting funding.

But a slew of massive IPOs are being hyped for 2019 – Uber, Palantir, Lyft, Airbnb, and the like – before the Nasdaq craters, thereby shutting the IPO window. And this tsunami of mega-IPOs was hoped to flood the land with cash, as investors and employees start selling their shares. These hopes still exist, and at least some of those IPOs will happen this year. While the water is a little ruffled, these are still the boom times in the Bay Area.

And that the underlying dynamics of the housing market have changed direction is – this time – not a result of the tech bust. That hasn’t happened yet. Is just the housing market turning on its own.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf your point is well made. Despite a “strong” economy, housing is slumping. Perhaps its quite different this time.

I don’t see anything different than past cycles. In a debt based economy, the economy appears strong until debt reaches the point where it stifles new purchases. This usually appears first in big ticket items such as housing and autos, it then trickles down. As the prices of assets begin to stagnate or decline, the speculators will begin scrambling for the doors. The only difference I see this time is up to now there has been no major event to panic people up to now. It is hard to tell what will panic the heard, but when that event happens, I believe you will see debt default on a scale at least as bad as 2008.

There is nothing fundamentally different. I have lived through all the 3 bubbles in the Bay Area – the dotcom bubble of the late 90s, the housing bubble of the 2000s and the “everything bubble” of the present day. In the dotcom bubble, stocks fell first; housing followed about a year later. In the housing bubble, they both fell together in a heap quite fast. In the current one, the housing bubble seems to have burst first. Stocks are likely to follow later this year.

In the Bay Area, housing can certainly lead the stock market instead of vice-versa. The housing-bubble peak for the Bay Area was late summer of 2005, ahead of the national curve. But the stock market didn’t peak until late 2007, a full 2 years later.

In both dot-com and housing bubbles, the speculative silliness was concentrated and obviously foolish to anyone willing to take a close look with a historically informed perspective. In the current Everything Bubble, the silliness is more insidious and consequently more pervasive.

Rising debts will adversely affect asset values and interest rates. This is the perfect time to unload homes whose mortgages costs exceed rent values.

The answer is simple.

Median prices compared to incomes were/ are unsustainable levels. All cash buyers (Chinese)have been a primary cause of this problem.If they have disappeared then prices will move down towards more realistic levels. Now when the boom in Silicon Valley stocks stop,then housing will really tube.

A similar thing is happening in Australia.

Cash buyers have been a tremendous force in California, accounting for about a quarter of the transactions in 2017-8. A decade ago they were just 10% of the total.

But it would be wrong to assume cash buyers equal Chinese nationals: only 3% of total residential real estate in California were to foreign nationals, and this total include people from all over the world. Granted, this doesn’t include US registered LLC nor front men (if they are still used) but even doubling that 3% doesn’t translate into such a massive influx of foreign capital as Melbourne and Vancouver experienced.

EB-5 visa do overwhelmingly go to Chinese nationals (84% of the total), but only about 10,000 EB-5 are issued yearly and as they are a political hot potato the FBI keeps a close eye on them and has shut down several “cash-for-residency” schemes over the past five years.

The reason why Chinese buyers are so talked about is the Chinese diaspora tends to concentrate in certain geographical areas and how most of them are wont to pay full prices to close real estate deals quickly. While these purchases are largely in cash, this doesn’t mean every single penny comes from the Celestial Kingdom via overinvoicing or other forms of capital flight: many overseas Chinese communities have access to various forms of shadow banking, not unlike what goes on in China proper.

While generally speaking these Chinese communities are considered good neighbors and amazingly hard workers, the way they tend to keep to themselves (nothing wrong with it, in fact I prefer my neighbors that way) and the excesses of some upstarts in places like Canada are making them easy targets as the search for scapegoats for two decades of economic lunacy begins in the earnest.

In Boise, Idaho, those paying all cash and messing up the local market are the “refugees” from California, Washington and other states.

Idaho has completely lost its “wow factor”. Prices are way over-inflated for what wages in the area will support. In addition, the feeder areas like California are beginning to see stagnation in their markets which will put pressure on prices in Idaho. Add to that the fact that a large percentage of Idaho’s employment is now construction based, and you have the ingredients for a major meltdown in the real estate market when it does turn.

3% for all of CA is a meaningless number. Show me the breakdown per city.

Exactly, there are a couple of empty homes on my street owned by Chinese investors.

Vancouver, anyone? I realize it’s a different market and country and, subsequently, “rules” per se but foreign buyers have influenced the market significantly. Besides, 3% (anywhere) is a small number but when we’re talking housing, the 3 over-inflated cash purchases in a neighborhood start a trend into higher median housing prices.

I doubt buyers are the key. Likely there are 20x as many potential sellers as there are buyers at the current price level. I think the issue is, those potential sellers have been holding out while the going was good. But when their time comes or when they get spooked and start turning to the market in some numbers we’ll see more price cuts, because there aren’t any more buyers to be found at these prices. Probably 20-25-30% lower. The “investor types” would have been a factor in as much as they were buying for the sole pleasure of owning a piece of SV, but folks who want a home to live in have different standards: they won’t trade a high-flier income for a crap shack entry, only “investors” used to do that. But those “investors” are gone now it seems they’ve come to their senses. Perhaps the fed had something to do with that or other macro conditions.

There is a sales slowdown, but not any kind of a price slump. In the LA area, a 50s original in a decent location where you feel safe starts at 1.5M. Same in the bay area … starts at 1.5M. While that is expensive, it is doable with a professional married couple. No problem here at all, especially with the stellar jobs report released last Friday.

In reality, LA should hold up a little better than SF since LA has a more diversified economy. SF is too tech heavy … not the best economic situation. The central banks have tightened monetary policy and that is triggering the start of a tech “mini bust”. Going forward, LA housing will fare a little better than SF housing. However, in either case, inflation has taken root, and if a Y over Y price decline ever emerges, it will be tiny. Don’t fear housing. Fear renting.

Jt, Median household income in LA is much lower than in the Bay Area. As I recall median house prices are much lower as well. Can you come sources for your data?

Really poor argument, jt

The assumption you make is that the professional couple continues to make the same compensation over 30 years and won’t age out of their jobs.

Not everyone works as Senior Staff Engineer at Google or Netflix or Uber.

I am in SV and work as high end engineer (undisclosed) and know typical 2 salary incomes don’t exceed 350K ; some get to 500K but are very rare.

Parts of East Bay can be had for <900k ; cities like Dublin, Pleasant Hill, Fremont are safe and the latte provides easy access to South Bay Armand core SV.

1.5 M is still mid high end and just see Redfin on how long it takes to sell houses now.

U r smoking something..

Actually, an income of 300K and a down payment of 300K will do it. That means each spouse makes 150K … not that unreasonable. I know quite a few couples in LA that hit those numbers without much problem.

Did you fully read what I wrote?

I don’t dispute > 300k income; just it being guaranteed for 30 years. SALT limit is a major impediment.

I am not going to argue with you on sample sizes etc. The next few months will show whether you or I are right.

Houses in my neighborhood in Mountain View range from 2.2-2.5M. The people buying them presumably can afford them but it’s getting harder with the new tax laws. It was nice to be able to deduct that 30k property tax payment but no longer. Well see in April how this works out. Also, limit on mortgage interest and state income taxes. Could be painfull!

PJ, here is a reasonable Mountain View home.

1.7M and it has been on the market for a long time, so perhaps closer to 1.6 … 774 SE Burgoyne St.

No different than the bottom end of good LA beach cities. You can grab a low end small home in a marginal location in good LA area cities for about the same.

In either area, you can find areas where small homes start well in the mid 2M or even 3M, but there are options in the mid 1Ms in either place.

Truth Always,

Over time, inflation will fix the 30 year payment problem. Big payments today are small payments in 15 years, and minimal payments in 25 years because of inflation. Inflation digs you out if you can make it for 10 or 15 years.

You also need to get to that income under 35 to have a 30y runway, ie. we’re down to a hypothetical couple of young well paid professionals with speedy careers as candidates for your starter home! Meanwhile retired highschool library assistants and former special-needs preschool teachers are selling their houses for >2M. To whom? 30-sething hedge-fund partners with 27yo best selling cookbook author wife’s?

“Over time, inflation will fix the 30 year payment problem. Big payments today are small payments in 15 years, and minimal payments in 25 years because of inflation. Inflation digs you out if you can make it for 10 or 15 years”

This has never ever worked that way for me. My shop rate hasn’t changed in 25 years. I’ve never meet anyone who’s income keeps up with inflation (unless you wanna talk about min. wage which has been climbing big time which may have kept up). When I had a real job my first 3 raises in my career were huge, and then after that never matched inflation….ever, not once….usually about 1/2.

There’s no suck thing is COLA in my line of work.

Honestly LA would fall as bad as other ca metros if the median income goes not support the median home prices

“That means each spouse makes 150K … not that unreasonable.”

The median HOUSEHOLD income in the Bay Area is around $118,000.

http://fortune.com/2018/06/27/bay-area-six-figures-housing-hud/

Teachers and nurses either have to commute from 3 hours away or go live under the Bay Bridge. Or maybe they will have apps for teaching and nursing. No personnel required.

Okay. 300K combined income can justify 1.5 million, assuming 1. The couple will have to both working and neither lose their jobs. Don’t think about raising some children. 2. Their income will keep up with inflation.

The thing is, both 1 and 2 are “future” estimate without any room for error. What if any of the above two assumptions turned out to be wrong? Banks will take your home and you lose your down pay and all the later payments. The way to take about future is to take about safety margins.

I think today’s safety margin for W2 buyers is low.

It may very well be that inflation will support all asset prices and those who rent will be squeezed like lemons until all juice come out of it. But you still have to think about the other outcome, and that is the couple lost one of the jobs, the RSUs promised got cut in half and then some. Can you sustain like 5 years to keep up the payment before things turn better or they will never turn?

“Inflation digs you out if you can make it for 10 or 15 years.”

Only if wages/salaries increase at least as much as inflation. Doesn’t sound like that’s happening.

Let’s not forget that many of these $300 include RSUs that vest monthly in their total comp calculation. So let’s supposed they don’t lose their jobs but somehow the value of those RSUs dropped by 20% (unfathanable, I know). Then what?? Uh, oh….already happened.

So I guess amateur married couples have to live in trailer parks in L.A. and San Francisco?

David Horowitz,

“Amateur” married couples can either buy a home in a rough tough area for 750K, or they can get a 2BD condo in a nice area. They have options that are workable.

jt,

The people on this website don’t really understand how much money a lot of young people are making (especially in tandem), nor do they grasp how many of them there are.

There is pretty wide gap between those that are able to buy right now and those that are not… and the gap is widening.

J Bank, and the wider that gap gets, the fewer there will be in the “able to buy” category. And that is not at all positive for house prices.

Let me know where I can find one in SF. I’m interested. Better than the $3000 I’m paying for a 1/1.

If you go to redfin, you will see San Francisco has 98 properties available that are priced below 800K. Many are condos and even a few fringe single families. But, there is stuff available for under 800K. You might not like what you see, but stuff is there.

I remember hearing about people living in conversion vans, box trucks and RVs parked on side streets in the S.F. metro area. Some would have gym memberships just to shower and dress to go to work. Is that still the case?

I tend to agree. I contend (repeating myself a bit) that CA’s house crisis is principally caused by NIMBY induced scarcity both directly, through zoning ordinances prohibiting dense new construction, and indirectly through onerous approval processes and a ridiculous amount of bureaucratic red tape and fees which increases costs of those units that finally are allowed to be built.

Factors that would ordinarily mitigate price such as interest rates, reduce the supply of new construction along with demand, dampening their downward effect on price.

Really the only things that could reduce housing costs significantly is a full scale financial crisis, a la 2008, which made financing for more expensive homes virtually non-existent for a while. Or an outbreak of good governance that revamped and streamlined CA’s housing production.

So far, thankfully, there’s no sign of the former — though Wolf has dutifully kept us appraised of all the vector from which that could come. As for the later, you would never have gone broke betting against CA’s ability to govern itself effectively.

California’s housing crisis is due to massive overpopulation. When I grew up in San Diego County, the population was about 1M now it is about 4M. Add to that a government cabal that practices extortion like mafia gangsters and there is no hope of anything close to affordable housing coming in the future.

Jdog, San Diego county’s current population is 3.2 million. It’s population in 1990 was 2.5 million, an increase of 28%

Houston’s population in 1990 was 1. 6 million and it’s current population is 2.3 million, an increase of 44%. Yet Houston’s housing costs are 1/3 those of San Diego, largely because Houston is a ‘right to build’ city, while San Diego has the usual CA impediments to residential construction.

“… largely because Houston is a ‘right to build’ city …”

‘Right to build’ on all the flood plains and marshlands. How’d that work out?

Commentors have referenced Vancouver and its Chinese population. Plus, a comment theme seems to be the insane cost of living in California, rising costs not reflecting real wages, and asks what is driving the everything bubble into unaffordability at this very moment; also producing a decrease in property values?

California’s population is larger than Canada’s. Canada’s housing prices range from absolutely unaffordable (Vancouver and TO) to middling, and finally dirt cheap. I assume California is similar.

With the drought and fire problems looming, plus the high cost of living and large taxation issues including Calpers, leaving California is probably a wise thing to do (10 years ago?). Leaving Vancouver is a wise thing to do, now..and was for sure 10 years ago. Leaving Toronto is a no brainer thing to do (and always has been). :-)

This is what I have noticed over the years. There are beautiful and stunning places in both Canada and California that people laugh at while at the same time infer the local population is deficient. That opportunites are non-existent, is a given. I established myself in one of those places 16 years ago, bought land, + riverfront, and built a home. Last year my ‘hell hole’ was regarded to have the largest percentage increase in land assesment values in British Columbia. What happened? Did anything really change here? Nope…it just got noticed and people started looking around instead of blindly judging. When folks bail from California they shouldn’t go for the trendy alternatives like Oregon or Idaho, instead they might look on the computer and research a road trip to somewhere appealing. Visit a beautiful hell hole that people look down on and then beat the rush into relocation. I’m thinking Appalachia and perhaps a few more southern states. Northern Minnesota? Wisconsin?

Where I live I sense a rising pressure from transplants. There are city refugees buying up whatever they can. There is nothing to rent. I know what this looks like because 52 years ago my parents fled Walnut Creek for Vancouver Island. Because we have an agricultural land reserve in BC (think a ‘no development’ freeze), and the forest land is owned by the Crown and is designated as ‘working forest’, we will be safe from the golf course and sub-divisons that chased my parents out of CA way back when. But moving on has to be considered and planned for as an option for all of us. Watching it all unwind is not a very good thing to do, imho. Of course any reader might be in the catbird seat and then reality doesn’t apply, does it?

But, you ask, how can I do this because I work in SV practicing a high tech career? The answer is that you used to work in SV. Instead, you prepped and trained for a different job somewhere else. Lifelong learning and Darwinian adaptation in action. :-)

Regards and best of luck as the wind down continues. It is a wind down. Nothing goes up forever.

I grew up in the 60’s not the 90’s…

Very roughly, prices in Hawaii are 1/2 what they are in California here. Yep, I’ve decided I’m buggering off back home to Hawaii when I turn 65, in about 8 years. Good, bad, ugly, at least I won’t be in the battle to make a living and that changes everything.

But also, you’ll have a hard go there if you want to live like the Brady Bunch. Living like a local, it’s fine. But that requires a very different diet, dress, way of living, I dunno if it’s possible to change your way of life that much if you weren’t raised in the local culture.

Welcome back, Alex. Hadn’t seen you post in a while, was getting worried ;)

Ehh … registered on Reddit instead of being read-only, finally had had enough and un-registered again.

Basically got two plans: Move back to Da Rock or find some way to afford to stay here.

San Jose’s #1 among Hawaii transplants anyway.

Lol, just heard 300sq ft condoz starting at 500K on Oahu. You gonna sleep on the beach? Getting pretty crowded there too.

Oahu, by far the most populated island, has vast, vast areas that have no people on them at all. It amazes me. There’s more area that had people on it 200 years ago but not now, than I imagine the vast state of California having.

Also, there are condoz down as far as $30k, you have to know the difference between fee simple and leasehold, it might be a 30-year lease which is where you get out the actuarial tables …

Alex!

yeah, i was worried about you, too. this internet thing is weird because i can’t ask your neighbors if they’ve seen you. you’ll have to come up here whenever we all get around to kickin’ it together up here.

Happy New Years, homeskillet.

p.s. and Alex, regarding staying here vs hawaii.. i feel a weird kinda renaissance coming on with the downturn…arts and such. gotta go breakfast ready but i’m FEELING it…hang in there… we’re MADE for chaos…

unusual biz systems underground…gotta start new parties… the KIDS don’t know how to do anything in real life… us middle aged folks have to have things so they can learn to MEET each other again and be embarrassed and shy and not swipe anymore…swiping is creeeeeepy…

James yelling at me!

(smile)

x

“While that is expensive, it is doable with a professional married couple.”

JT, you’re describing people falling for the Two Income Trap. It’s a huge risk for a couple to buy the largest possible house under the assumption that neither of them will never lose a job or face a pay cut. Sometimes it works out but often it’s a disaster.

I don’t often agree with Elizabeth Warren (and perhaps her daughter-as-coauthor did the real work for the book), but their book with this title describes a legitimate financial risk. One which destroyed a lot of families in 2006-2009.

To make such a purchase in the 10th year of an economic expansion, with inventory rising, the Fed tightening credit, and the stock market acting squirrelly, is probably much riskier than usual.

Hear yourself JT: “starter” home is “doable” for a well-paid professional couple. You are grasping for straws here. Such a feeble equilibrium is obviously not sustainable, not even in a thought experiment. As I suggested above: once sellers start coming out in even mildly increasing numbers they’ll find no matching buyers. And my guess is, there are an order of magnitude more potential sellers than potential buyers at these prices. (None of those sellers ever earned anything near the figures they’re hoping to reek from their lowish-quality homes). I think the sick transaction figures prove that. It’s not like buyers were taking a tactical pause before storming the market with offers. More like the other way around.

As to rents, some anecdotal account: here in SV friends of mine were about to have their rent raised from 3.6k to 4.1k but the landlord reconsidered after some tenants cancelled their lease and retreated to 3.8k. Still outrageous. Another friend in Sunnyvale even had their rent lower a notch from around 2.9k. So rents are slowly finding some resistance too. Should be said that normal families can’t pay these rents anymore, often it is 3-4 young engineers colocating who pay them. But there is a limit to how many FAANG engineers are willing to move in a minimally maintained apt, so we’re reaching some top here on rents too.

The rent side of this whole area is interesting; you are talking about SV, but I know no shortage of people (myself included) that live in rent-controlled SF apts, which adds even more leverage to the buyers side. 70% of the housing stock in SF is rent-controlled.

The drawback has always been “what if they raise your rent, you could get squeezed?” Well, they really can’t, so I think a lot of potential buyers are more than willing to watch this play out with the added incentive that their rent isn’t going up. If you keep that money invested (even in CDs), you’re not getting behind in the game, especially where prices are now. If asset values rebound for some reason, you’ll catch those gains through your investment holdings. If they fall, you have the cash to sit back and get a good deal in RE.

Saw a price drop on Macondray Lane last week (rather famous street in Russian Hill); first price drop I have seen in Russian Hill in 7 years. But prices are still way too high (not even RH, you’re still looking at overpriced shacks out in the Avenues that shouldn’t be worth 60% of their ask).

Something will have to give. Will be an interesting year.

We just negotiated our rent down for a 3 bed 2 bath house in North San Jose area in November. Rents are absolutely starting to come down. Now almost everyone offers 1 month free.

The family thing is very true. A lot of families have left Silicon Valley. The low end houses are coming to the same level as the fancy 1 beds about 3k a month.

That’s because families make the same income as 1 tech worker. Small houses, it’s just not easy to have roommates. Thin walls, rooms very close together, large backyard. They are made for a 1950s style family with three kids. One large room for a bunk bed, a small master and a small nursery room. Does not work well for tech workers and thus are cheap ( $2800-$3200 a month).

The market is correcting itself.

Amen!

How much of a price drop will it take for wannabe property investors to start having second thoughts?

Interesting what the highly paid are saying

https://www.teamblind.com/article/Buy-or-Rent-SpeViWLD

REQUIRED to buy a house:

-Double $150k incomes

-$300k cash

Easy! If someone can’t do this, they need to work harder!

Or find a more hyped up named company as an employer. After all, a lot of compensation is not just cash but options, even if they are in a car company that delivers pizzas. Then they take a loan against those options.

Yes, they need to work much, much harder, and in many cases should have shown greater responsibility and judgement in choosing their parents…

The red ink coincides almost perfectly with the slump in FANG+ stocks.

Gee whiz, I hope nobody stretched to buy a shack or cashed out shack equity in the last few years.

I had a good conversation with a rwaltor friend today working in South Bay. He also confirmed that many people are holding off, even though they migh have money in the bank. He says many customers are spooked by the volatility in the stock market and they hesitate to sign the papers, because their incomes depend on the stock market. 5-10% daily moves up or down in Trillion dollar company stocks is not an easy thing to swallow.

What goes up inevitably comes down…

The Wolf-Man has got this right. We’re witnessing the repricing of assets eg Homes, Stocks after a huge run since 2008.

Real Estate agents throw around $400K and $500K a year salary numbers around as if every teenage in McDonald in silicon valley is guaranteed to make $200K a year. Let’s see some numbers:

MSA/CSA Name Total Population,

2016 Total Households, 2016 Median Household Income, 2016

Napa, CA Metro Area 142,166 49,561 $75,077

San Francisco-Oakland-Hayward, CA Metro Area 4,679,166 1,691,781 $96,677

San Jose-Sunnyvale-Santa Clara, CA Metro Area 1,978,816 653,296 $110,040

Santa Cruz-Watsonville, CA Metro Area 274,673 96,257 $77,613

Santa Rosa, CA Metro Area 503,070 187,504 $73,929

Stockton-Lodi, CA Metro Area 733,709 227,186 $59,518

Vallejo-Fairfield, CA Metro Area 440,207 149,172 $73,900

San Jose-San Francisco-Oakland, CA CSA 8,751,807 3,054,757 $91,234

I like the statistics- but the reality is the ones who are buying houses are NOT the median.

They are newly minted paper or actual millionaires- not sure how true anonymous figures but please see teamblind.com on how much the top companies in SV pay – 300K total comp. for senior staff is bare minimum).

Now teamblind.com also has a housing section where these highly paid (unverified) engineers are advising (mostly) NOT to buy RE in the SF Bay Area.

So I can predict another 20% down at least in East Bay.

I was looking for houses in Fremont and 1200sq ft houses listed at 880k were easily going for 1 M in fall of 2017 in 2 weeks post listing. Now I see 1700-1800 sq ft listed at 1 M and moving in 2-3 months. I think the market in Fremont has dropped at least 10% already.

Personally I am rooting for further fall.

You know it is fairly easy to checkout out census figures, household income, and see how many top earners their are by county. Cross that with housing data. Hmm maybe I’ll do that. My guess there are not enough W2 earners to sustain the bay area housing market at this price.

I hate to tell JT but your wrong about prices holding in LA. I’m a real broker and the last 4 homes I have been involved in required price cuts of 10% or more to get one buyer qualified to close escrow. Mark Cuban just closed escrow on a Laguna Beach house for $19Mil than had been listed Jan 2018 for over $25Mil. Huge price cuts in the very high end($10Mil plus) are very common now.

I think JR is thinking to take positions and give those 300K double income families two choices. 1. Take out 30 year mortgage and make sure the couple work 30 years without one losing a job for more than 1 year and never think about raising children. and retire 2. Don’t buy and we will inflation squeeze you rent lemons until all juice come out.

This is what 300K can afford means and this is what 300K holding off means.

I think JT is probably right in this gamble because the FED has their back. Asset and rent (house,tuition,insurance) will keep squeezing the W2

working class. Give the McDonald workers minimum wage or even universal income. Squeeze the 300K incomes and let them code robots to replace themselves and in the end they will be universal income too. Yellow vest occupy Washington and Federal reserve? Pitchforks? No, we have universal incomes.

Does the initial sking price even matter?

Trend in final sale prices would be more helpful. A low initial ask is really more to drum up interest. The price that’s finally paid could be well over 12% above the initial listing.

This is doom porn, plain and simple. Maybe SV real estate prices are stable for a couple years. Or rather, increase only 2-3% rather than more than 15% per year.

Raj Laroia,

You’re hilarious. You said: “This is doom porn, plain and simple.”

No, it’s just some basic numbers.

But I do understand that you would much rather have hype-porn, because it makes you feel so much better. Sorry, for your dose of hype-porn, you need to go somewhere else. There’s plenty of it out there.

I would suggest Zerohedge…they got more of the hyper doom porn over there, otherwise mainstream media will provide hyper porn on the opposite spectrum.

Wolf, with all due respect you’ve been calling for this teal estate collapse for several years. I truly believe in everything you’re saying and the numbers support it, but it’s not unreasonable for Raj to make that statement, especially if he’s been following you as long as I have. Keep up the great work!!

Slursurp,

Don’t confuse this site with Zero Hedge (happens a lot). I have talked about a “bubble” for years, because it has been a bubble for years, and all bubbles eventually deflate, and I might have pointed out some of those reasons why bubbles deflate, but I don’t remember ever calling for a “collapse” of this or any real estate market.

A bubble is the opposite of a collapse. Once a bubble is over, it “deflates” — which is a term I use.

I recently cited an OECD report that used the phrase “severe collapse” regarding as a risk for Australia’s banks. But I put that in quotes because it was a citation.

I’m a big fan of Wolf’s, don’t like being pedantic, and think it’s probably just a problem with terminology and metaphor, but it’s not unreasonable to assume that a bubble’s end equals its collapse.

Think about it: balloons may deflate, but bubbles ALWAYS pop/collapse suddenly.

Perhaps better to go back to the old “Boom and Bust?”

Or my persoanl preference, “Manias and Panics,” since they correspond better to the mass psychology of these episodes…

The great value of this site is that it provides useful information and measured, heterodox analysis, but no doom porn.

Touché Wolf. My interpretion was a collapse (biases of course by my personal interests). Thanks for responding. I truly enjoy your highly informative website.

No one doubts the validity of the statistics above. Those are facts.

Question is the relevance. Yes, initial listing prices are down 12% year on year. What is the price finally paid?

It’s a bit like tracking MSRP’s on new autos. Nobody actually pays that price. Or tracking, for arguments sake, number of toaster ovens in the average home. It may very well be 0.487, not 0.445, as I assert. All the same, there are more useful indicators out there, such as actual transaction prices. If those confirm these findings, maybe the sky is in fact falling.

Raj Laroia

The article discusses the underlying dynamics. Prices paid follow with a lag because at first, the deals where buyers and sellers are too far apart don’t happen. So volume slows. Then when more sellers cut prices, more deals happen, and eventually, the median price comes down, and eventually even the Case-Shiller sees the price declines. This is already happening. I write about selling prices often enough (median and Case-Shiller). This was about the underlying dynamics.

For example, the median selling price for houses in San Francisco in December has already dropped $200K from the peak in February. I covered median selling prices in San Francisco for the month of November:

https://wolfstreet.com/2018/12/05/san-francisco-house-condo-bubble-prices-fall/

Oh yes! Enormous asset bubbles detached from all fundamentals for 99% of a populace always ‘stabilize’, then continue to go. History’s full of examples of this happening.

But it’s YOUR bubble – and those are always different, as we know.

If you have enough data, the difference between bid/ask spread is negligible. The trends will still be the exact same, with -maybe- a slight delay in the ask price trend.

LOL, looks like someone didn’t save their commission checks during the bubble years.

I loved the CAR and NAR terms like slowdown, shift, deaccelerate, etc. If Raj actually read the article, prices are down like a turd flushing in the toilet and he still thinks its “increase only 2-3%”.

I remember there was a long-haired RE guy on CNBC who came on TV at the start of 2008 and declared that it would be a “normal” market for real-estate with price increases limited to just the rate of inflation.

Of course, as things turned out, it was anything but a normal year!

I’m seeing more and more real estate pumpers showing up to comment here and elsewhere, trying to counter any arguments that RE might be headed for a slump. The theme is always the same: dissing “doomers”, feigning pity for renters, stressing how a home purchase always works out over the (very) long term. The message is nothing new. It’s just a little more intense and frequent recently. Could be nerves, or perhaps they just aren’t as busy as they were a year ago.

These are the same people who troll the other housing website (Doctor).

Also seen repeat handles/writing style in the socketsite comments.

Methinks they’re suffering from denial … as one might expect … and will get over it soon.

I should add that another common theme is just how much money people are making these days. Made-up sample quote:

“I just closed a deal for a couple of young professionals making $XXXX and they are quite typical for that home-buying demographic.”

The reason realtors think salaries are so high is because those are the only ones who can afford to buy houses now, so those are the only people they see. It creates the illusion that the pool of high income home buyers is inexhaustible. But that pool of high earners only needs to shrink a tiny bit, and suddenly realtors have a very, very big problem.

Good point!

Remember before the last crash when they were saying things like: “People will always want to move to Las Vegas, because of the sunshine. So prices will continue to rise.”

Wolf,

Indeed looking quite bleak for RE in the Bay area. Sure can’t help matters when the local utility (PG&E) just got downgraded to junk status by S&P this morning.

Yeah, very belatedly. The company has been discussing internally a bankruptcy filing, as Reuters reported Friday after hours. How can a company that is considering a bankruptcy filing be “investment grade”? Well, we know how….

A few weeks ago, ABC in Bay Area ran an ad on a Sunday afternoon from Caldwell bankers, iirc. They showcased homes on TV! I watch football games all day Sunday and I have never seen these ads in the last few years.

The fact that they are pitching those places to me means that they are out of suckers.

I also noticed that the homes shown were in outskirts of Bay Area such as Pleasanton and Petaluma. I have heard from people how the once hot San Ramon area and the neighborhood have a market that is now frozen. The ad seemed to confirm.

I see the problems in the cities as a population issue. To many people wanting or needing to live in close proximity to each other with little alternative.. The cities were built when the population was much less and there weren’t such large corporate entities such as Google.

The quality of life, no matter what the pay or income, has to be diminished by the sheer affect of the numbers. If there is a scarcity of housing do to demand driven by the immensity of the size of the employers, if everyone made a million$ a year doesn’t affect the supply and demand curve except to make a one bedroom house cost million$.

There is no benefit in making a million$ per year if your quality of life sucks. And if your quality of life sucks, then making 2 million$ per year doesn’t make you happy or productive..

Answer = give up all your freedom, live in a dormitory supplied by your employer and live under their rules completely. 1984 has arrived!

Interesting data but I question how relevant the “purchase” housing market in the Bay Area is as an indicator of economic activity.

Between Prop. 13 and the high cost – turnover seems to be very low to me. This is based on this background info:

The Bay Area has around 7 million people – which implies roughly 3 million housing units. In comparison, the US overall has around 140 million housing units for 330 million people.

The US Census shows 613K new homes sold in 2017; NAR shows 5.5M existing homes sold in 2017 for a total of 6.13M homes sold in 2017 = 4.3% turnover rate.

2000 or so listed properties per monthx12 divided by 3 million = 0.8% turnover rate, or less than 1/5th of national average. Obviously I am assuming listings = sales which may not be at all true. Also, the Bay Area numbers are obviously approximate, but would have to be nearly an order of magnitude off for the ratio vs national to be invalidated.

My point being that housing in the Bay Area may likely be largely a 1% affair – thus not necessarily indicative of overall economic activity.

The household with $300K income is largely irrelevant – the low turnover rate shows that people just aren’t selling or buying houses.

It would be a really interesting study to see just how diverse the population is of families who buy and sell houses in the Bay Area; I strongly suspect it is the same group of people (1% trading up/around) as opposed to a broad base of demographic/generational turnover.

So true. It’s just a painful housing situation when you live here in deleterious housing conditions caused by greed and poor housing policy. Lots of people who write blogs live here.

Whatever diversity you’d see would probably be provided by working/middle class old-timers and legacy homeowners cashing out.

Once that demographic is gone, it’s not returning, and the cities become playgrounds and playthings for the rich.

For the time being, that seems to be the dynamic: hyper-gentrification/asset inflation in cities connected to the global economic circuitry (with a Colors of Benetton overlay of corporate faux diversity), and social/economic blight everywhere else.

Manhattan, or Detroit…

I personally think the “cashing out” is more anecdote than reality. My view is that those selling out are ones who bought 10 or even 20 years ago – still have a significant mortgage but not enough Prop. 13 subsidies to be worth keeping. A small percentage/absolute number.

Anyone selling a house bought for $35K or $70K in the 1970s, with a $2K/year property tax, even for $2M, is stupid.

Instead, they could rent it out for $5K/month, likely much more…forever.

Go check out Pacific Heights using Zillow to see just how low those property taxes are. To put the $2K/year property tax in perspective: the same house, sold for $2M (and Pac Heights houses would be much more) would pay $30K/year in property taxes alone.

Throw in the intergenerational transfers that are possible…

Yes, this absolutely happens. Right now there are too many houses for rent and little demand. We were able to negotiate our rent down by $300 on a house in Silicon Valley because it had been sitting 3 months already.

It will only get worse if a recession comes, rent prices will fall and it will become hard to find renters that can pay the rent. Silicon Valley is bifurcating into the haves and the have nots. The have nots can only barely afford the rent. In a recession, this is not sustainable.

Health care and nursing home costs will eventually force a lot of boomers to sell.

Perhaps, but keeping the house and renting it for $5,000.00 + a month has the same effect on neighborhood demographics as selling, with the economic diversity of areas becoming less and less common.

My point was just an elaboration on c1ue’s comment, and about the stark polarization (hyper-gentrification or blight) between cities in the US.

Interest rate cuts are could well be in the cards for 2019 or at least 2020, an election year.

And since the Fed failed spectacularly for a great many years to raise rates sufficiently and doesn’t have much bang on that front, my guess is political pressure for QE will grow.

One wild card: the elites and establishment folk in D.C. may decided to go with higher rates, in the calculation another corporatist Dem (Biden?)

is better for their agenda than Trump, who wanders off the acceptable establishment policy menu when he talks about ending eternal wars and occupations…way too much gravy and corporate profits in those to be allowed to end.

Teaser loans are back again.

More folks moving out of CA, they arriving as taxes, traffic, and crime are major factor.s

What’s the typical cost structure of a home purchase? For instance, how much of a sale price is from construction costs (and how much profit does the builder take?) How much is from real estate agents? How much is from listing fees, etc.? Curious to know if these margins have increased since 2008.

One thing I’m wondering is, if their margins are slim all around, then wouldn’t the builders/RE agents simply clamor for a stifling of supply to increase profits, rather than the construction of affordable homes with slim margins? Or if their profits are huge, will they once again re-enter the “mass market, low margin” space?

House buyers traditionally paid 6% to agents, which was split evenly between buyers’ and sellers’ agents. Five percent is typical now; I sold my house and paid 3% to an agent who handled both sides.

I’d be interested to know what you pay if you buy directly from a builder/developer?

The real reason you have booms and busts is that people tend to think in lineal terms instead of cyclical. In good times, they think good times are going to last forever, and in bad times they tend to think just the opposite.

For some reason they cannot grasp the concept that one creates the other.

I sold my late-fifties tract home in San Jose last March for $1.305M. Zillow–FWIW–now has it valued at $1,270,604.

So we are that dual-income high-earning professional couple living in SV. Kids. It makes no sense to buy right now, and purchasing anything in a good school district – a lot of the school districts on the Peninsula are not that good, by the way – is also pretty much out of our budget, unless we are Ok with a several million $ mortgage on a 1600 sq ft 1950s teardown. But, you can rent a house that sold for $4 million for $8-9k a month and lots of houses priced at $2-3 million are in the $6k/month rent range even in prime areas such as Palo Alto.

If you live in the south or east bay, you can get a nice house for about $3k.

It’s much cheaper to rent.

This might knock a hole in Bay Area house prices. At least at the margin,,,,

https://www.wsj.com/articles/u-s-expands-coverage-of-real-estate-anti-money-laundering-program-1542322224

I look forward to your analysis of Seattle soon. This place is crazy but it seems like everyone stopped buying.

Coming in a few hours :-]

“But a slew of massive IPOs are being hyped for 2019 – Uber, Palantir, Lyft, Airbnb, and the like – before the Nasdaq craters, thereby shutting the IPO window.”

Rats trying to get out while the getting is good.

Don’t worry. Powell pit is comming I a few quarters. Money printing will make today’s prices look like lunch money. Just like the 70s prices look ridiculously cheap to us now..

My guess is the avg Bay Area home price in 2030 will be around $2.5m and the avg household income will be around $300k. Tech workers will be bringing in closer to $400k/year – DINKs (dual income no kids)will be around $800-1m/year

And of course the govt will reassure us that there’s little to no inflation. Thanks China and Mexico for your cheap goods and produce to keep our general lifestyles afloat!

If you think I’m nuts just research what incomes where in the 70s,80s,90s,00s. $15/hr min wage in a Cali. Used to be $5

What makes you think this? Are the owners of all this debt the weak hands in government to see all their investments eaten away by inflation? Politics says the other side of the loans will be protected. Inflation hurts the rich, whereas deflation means they consolidate more power by buying assets cheap as the weak (leveraged) hands are forced to liquidate. My money’s on deflation and my powder is dry. Is yours?

Hey Wolf,

You should start discussing the pension crisis that 10 years of the lowest interest rates in history created. I don’t expect the fed will ever be able to drop interest rates back down to the ground without completely bankrupting the retirement of millions.

If you ask me, everything from mass inequality to the election of Trump was a byproduct of prolonged artificially low interest rates.

I’m blown away by how many that read this blog still believe that housing prices only go up.

NIMBYism is strong in Silicon Valley.

Property owners who vote disproportionately don’t want more properties (go figure!)

Cities are financially incentivized to build anything other than housing due to Prop 13 passed by voters in 1978.

The result: the county that Facebook is in has a 16:1 new jobs to new homes ratio.

Meanwhile – property owners flip out when housing for teachers (who are fleeing) is proposed: https://abc7news.com/education/opposition-to-teacher-housing-mounts-in-san-joses-almaden-valley/4404364/

And long time residents are coaching parents to tell their children to leave Silicon Valley because they don’t want to add more housing – https://twitter.com/nextdoorsv/status/999364778907914245

I guess its all understandable when you consider 3 story apartments to be tall, monstrous, blight and would rather have an abandoned gas station… https://twitter.com/nextdoorsv/status/1071132825317982213

“And that the underlying dynamics of the housing market have changed direction is – this time – not a result of the tech bust. That hasn’t happened yet. Is just the housing market turning on its own.”

In this regard, I think it might be illustrative to add a plot of the Nasdaq on top of that asking-price chart.

Listen to your realtor price your home based on sales in the last 15 to 30 days if you want it sold. If you want last year prices you might find a realtor who just wants a listing but they will be back looking for a price reduction on your home. Loan appraisers are only looking at the most recent comps….

Clearly, real estate in most major markets is over inflated. Every article I’ve read for the past 6 months keeps blaming slowing in the housing market on rising interest rates, which is BS, since rates are still incredibly low. Living in AZ, our housing prices are still relatively affordable compared to places like CA, which would explain why AZ is being overrun with people flooding in from CA lately. I can’t drive 2 seconds in any direction without seeing CA license plates. Having said that, the flood of people moving to AZ from CA is artificially keeping our real estate market overinflated, as the people from CA come in and are willing to overpay for a dumpy $400K house, which is actually only worth $200K, with no yard in the middle of the desert. It’s all a sign of desperation, as the ridiculous prices in CA are creating a flood of desperate people moving out to cash in their chips, while they still have them from unrealistic house appreciation. Most of it is the result of investors, who own much of the properties, and I’m guessing the only ones with the capital to buy these houses that CA residents are selling, so the real estate investors are driving this whole over inflated market. It’s also why rents keep going up, as the investors know that most people can no longer afford to own a home, so rent just keeps surging higher and higher, as most people have nowhere else to turn. The only way it’s going to stop it’s ridiculous course is for people to stop buying the overinflated properties. Millennials are going to have a big influence on this, as I’m sure most Millennials can’t afford to own homes and will likely live out their lives by taking over the tenancies at their parents’ homes, once they pass away. Basically, the real estate market is a dumpster fire and only going to get worse before it gets better. Oh, and for anyone from CA reading this thinking about moving to AZ, please just stay in CA…or go to Canada….the desert sucks…you’ll hate it.