House prices down $265,000 from peak, down $60,000 from year ago. America’s most majestic housing bubble begins to deflate.

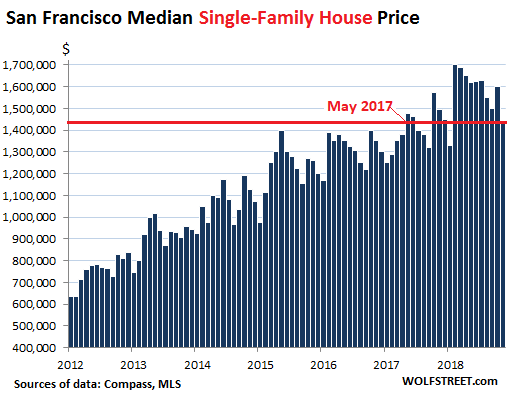

In San Francisco, the median price of single-family house sales that closed in November fell to $1.435 million. This is down a blistering $265,000 or 15.5% from the crazy peak in February of $1.7 million – a time when only the sky was the limit. And down by $60,000 from November 2017. This puts the median house price below where it had first been in May 2017. Note the steep slope from the peak in February:

Median price means half of the homes sold for more, half sold for less. So on the bottom end, people can try to push their luck with an occasional small shack in the $800,000 range. All data via Patrick Carlisle, Chief Market Analyst at Compass.

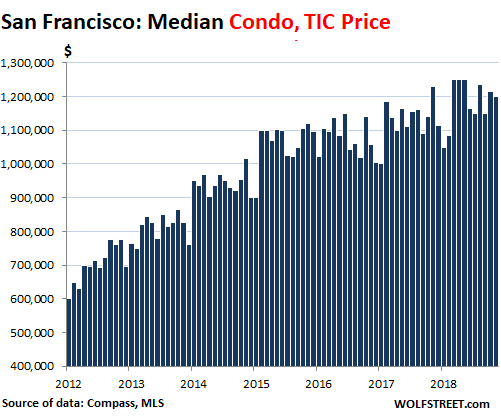

About 53% of total sales in San Francisco were condos; for years, all new housing construction has been condos and apartments, with practically no single-family houses being built, resulting in ever greater population density – and an increasing share of condos in the sales mix.

The median price of condos whose sales closed in November dropped to $1.2 million (also includes the few sales in TIC or Tenancy in Common buildings). While that still sounds like a ludicrously huge amount for a median condo – something like a small-ish two bedroom without anything spectacular – the price is down $50,000 from the peak in March, April, and May, and down $30,000 from November 2017:

Data for condo sales represent actual sales that closed and were reported to the MLS (Multiple Listing Services) where brokers list properties. However, these sales do not include the sales of new-built condos that developers sell through their own sales offices. A lot of condos have been built recently, and a lot more are in the pipeline. But developers don’t list them with the MLS and don’t report sales and prices to the MLS.

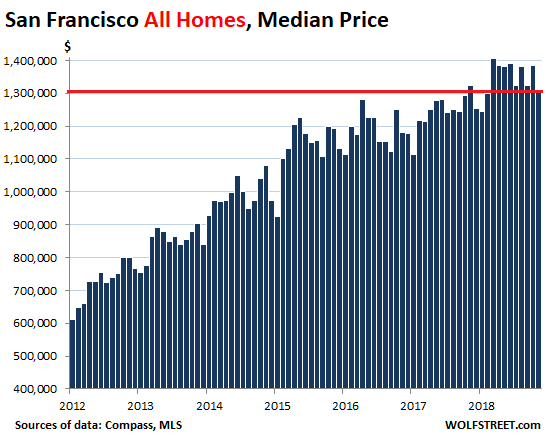

The median price of all types of dwellings combined dropped to $1.31 million, down about $95,000 or 7% from the peak of $1.41 million in March, and down $14,000 from November last year:

Clearly, the sky is not the limit for home prices in San Francisco, but the sky is not yet falling either. These are just relatively minor price declines in volatile data of one of the biggest real estate bubbles the US has ever seen.

Sales volume for all types of dwellings combined fell 14% in November, compared to a year ago, to 444 homes.

In San Francisco as well as the counties of San Mateo and Santa Clara, which make up Silicon Valley, the underlying dynamics of the housing market changed last summer and have since taken a more serious turn for the worse. These median selling prices show that the underlying dynamics have come to the surface.

A similar scenario played out in most other Bay Area counties, with only three still showing year-over-year increases in median prices, if modest ones; the other counties showing year-over-year declines (data via email from Patrick Carlisle at Compass):

- Santa Clara County (Silicon Valley): -1.6%

- San Mateo (Silicon Valley): +1.0%

- Marin County (north of the Golden Gate Bridge): -6.0%

- Sonoma County (north of Marin): -5.3%

- Alameda County (includes Berkley, Oakland, and a big part of the East Bay down to Santa Clara County): +2.3%

- Contra Costa Central (Lamorinda and Diablo Valley): -3.8%

- Napa County: +1.8%

But the Bay Area economy is still hopping, and companies are still hiring. The classic and inevitable tech bust that everyone who has been around here long enough is expecting hasn’t arrived yet. And this downturn in housing is taking off in a very strong local economy.

Homebuilder Toll Brothers just said it out loud. Read… Why California’s Housing Market is in for Serious Trouble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

> It’s Happening

ronpaul.jpeg

https://media.giphy.com/media/vv41HlvfogHAY/giphy.gif

Ron Paul was our last best hope to fight back against the Wall Street-Federal Reserve Looting Syndicate and head off the coming financial crisis caused by ten years of radical Keynesian monetary experiments by Bernanke & Yellen.

Anyone who thinks pro-cyclical stimulus is “Keynesian” completely and absolutely misunderstands Keynes.

The 1% surely thank you for your error.

Keynes believed in balanced budgets and no trade deficits.

Balanced budget in constant value money or money that inflates away?

It’s not “happening”.

Looking at these graphs, there was a fair dip in the first graph in January 2018.

I’d bet the year-over-year figures for January 2019 show an increase in price. “San Francisco Median Single-Family House Price”.

Not until February figures (released in March) might we start seeing a sustained downward trend.

As for the “San Francisco All Homes Median Price”, as you say it peaked in March 2018 so there won’t likely be a consistent downward trend in the year-over-year result until the March figures are released in April.

Looks like we’ve got at least 4 more months of this “shadow-boxing” with prices up/down compared to a year ago almost at random.

Yeah it always disheartens me on this site when I see sensationalized results. Anyone that looks at a chart sees how this looks like the random up and down levels in a clear uptrend that hasn’t broken. I agree with the sentiment but this isn’t really evidence and claiming it is makes me lose confidence in the source, it’s reaching too much.

Yeah, you may not like declining house prices, and so you don’t like the data and call it “sensationalized.” That sure is one way to stick your head into the sand and hope the data is meaningless.

House prices fell 5% or $60,000 year-over-year. That’s not up, but down, and it’s not random, but year-over-year.

By contrast, when the market was still hot in February 2018, house prices shot up $400k year-over-year. So this is a huge change in direction, even if you don’t like it.

The cratering is just getting started. When Tech Bubble 2.0 implodes, it’s going to take down all these superheated housing bubble markets with it.

Got popcorn?

Futures are tumbling tonight following the arrest of the CFO of China’s biggest telecom in Canada on a US warrant. Anyone who thought Chinese investors were going to keep paying outlandish prices for West Coast real estate is in for a rude awakening as the trade war reignites.

And what does it say when the futures tank on the arrest of one corrupt executive, among hundreds if not thousands? One could get the impression that the “system” (narrative) doesn’t function unless those pulling the strings continue to turn a blind eye to the fraud, the bubbles, and the predatory nature of the financial system in general.

She is not arrested for corruption.

ps. I wonder how long it will take for a Canadian executive to be arrested in Cambodia for trading with Taiwan.

She wasn’t arrested for corruption. She was arrested in Canada on a US warrant for Huawei’s dealings with Iran, evidently, in violation of sanctions. China is going to view this as a serious affront and provocation, and retaliation of some sort is almost certain. Any thought Trump might’ve had that China will open their markets to US goods probably just went up in smoke. In addition, the globalists who exported our manufacturing base to China might belatedly realize that China never ceased being our adversary.

DANGER WILL ROBINSON!! DANGER!!! All other countries on planet EARTH, take heed. You are now under FOREIGN DICTATE of the United States of America, which means you are NOW unilaterally subject to the laws of the United States of America. We mean to rule the world. You are now our disloyal subjects. Violation of our laws will mean your extradition and incarceration in a foreign prison system. Yes! We mean to rule the world. Sovereignty of your country means absolutely nothing to us as we control the skies above your country with our unmanned military drones, and will soon with our new US Space Force will rule the space over your countries in their entirety as well. Welcome to the new PAX AMERICANA of the 21st Century. There is no escape! Resistance is FUTILE! Assimilation is INEVITABLE! Surrender to absolute US HEGEMONY or be ELIMINATED forthwith!!! (And make no mistake, we mean BUSINESS!) [;-)

It’s about time.

Thank you Sweet Jesus!

Its about time! “We got the power!”

and a good part of that rude awakening is coming to…. er…

Chinese investors.

Once the decline is obvious to the public, people will stand by and wait to see further drops before even thinking of buying. The decline will then accelerate and become even more pronounced. There’ll be a lot of condos for rent that people can rent while the situation plays out.

“Look out below”.

When my rural valley was in a big decline about 10 years ago, there were houses for sale for years. People just took them off the market. Now, there’s hardly anything to buy as city folks recently cashed out, retired, and relocated here. Few stay, though. They miss the conveniences (which is a euphemsim for mindless habitual shopping). Most move away to another urban center.

I suspect people will just leave California for a lower cost environment, as mentioned in the previous housing article. It is my observation that most folks seldom do anything outside anymore. Does it matter where their subdivision or condo is located? It could be in Iceland for all the difference it would make.

I don’t know about a “lower cost environment” but the ones I know are leaving because of the flat out insanity from California government to education and all points in between. Won’t even mention the social justice police.

Sure… can you give a specific example of this ‘insanity’?

California is not any more insane than any of the other 49 states.

1. Sanctuary state.

Samurai: I think he is talking about stuff like the Crazy Train, also known as High Speed Rail.

And many will regret doing so – climate, lifestyle, and often the cost of living where they’re headed will differ little from CA. Then when they want to return, prices will have moved up again – rent or purchase – and they won’t be able to do so.

Yes, there are many stupid ideas in CA politics. But they exist in every part of IOUSA. Bottom line, be careful what you wish for when leaving CA.

> Then when they want to return, prices will have moved up again – rent or purchase – and they won’t be able to do so.

Did you read the lede? “House prices down $265,000 from peak, down $60,000 from year ago…”

Stagnation and decreases in rents are also already happening, which Wolf has written about in other posts.

I’m a renter in the Bay Area and based on what I’m seeing, it wouldn’t take much for me to shave a few hundred dollars off my rent, especially when factoring in incentives that aren’t reflected in the rent itself.

Past performance is not an indicator of future outcomes. Just because prices have increased dramatically over the past decade doesn’t mean the next decade will see the same trend.

The idea that you can’t leave the Bay Area without taking a hit if you decide to return later might be true for some, but it’s not a universal truth forever.

Agreed. After spending about 20 years of my young adult life in SoCal, Dana Point to Long Beach, stationed at the closed down MCAS Tustin for 5 of those early years, I moved to Wisconsin in 2014.

Big mistake.

The condo I bought in Aliso Viejo in 2011 and sold in 2014 is up an additional ~100K in price from when I sold it. Now I’m trying to engineer a move back to that area. Not easy.

Paulo, you are missing something here.

If the economy hits a recession, then prices and rents will tumble. That is a fact.

But, if what we have is a buyers strike without a recession, then rents will not tumble, and the high rents will support the high prices because people will just decide to park a property as a rental and wait it out.

In my opinion, we are not headed for a recession, and we will see slower and slower sales without much price movement because rents stay high. That is my base case. But, recessions do happen when least expected.

The possibility of a recession in 2019 is stronger than you’d think. Here are some possible trends that could push that way:

1. The tightening of China’s easy money policies, reflected in the dropping price of real estate there, leading to a slowdown that has already been spreading through many emerging markets

2. The ending of corporate stockpiling to front-run US tariffs, and the chance that trade agreements reached will be seen as a reason to reduce inventory back to previous levels

3. The continued reduction in prices of oil causing a slowdown in our shale oil regions, spreading from there. The US is an oil exporter now.

4. The sales slowdown in housing leading to a slowdown in new construction plans.

With the rich valuations in the markets today I’d certainly recommend caution.

Some people will leave, but there is something to be said for an employed young family staying put when it has a 30 year fixed rate mortgage at an attractive rate with 28 years to go. My boon-doogle is my very low property tax bill with a basis that dates back to the late 1970’s and a house that is within walking distance of the BART rapid transit line. The mortgage was paid off long ago.

30 year fixed rate mortgages are practically extinct in Canada (unless Mom and Dad provide the loan). So the real estate problem may be a lot worse in Toronto and Vancouver if a lot of recent home buyers find that they no longer qualify for refinancing at the end of their first fixed rate period (typically five years?).

And don’t forget about Prop 13, whose taxpayer protections are frequently overlooked when discussing income taxes.

My co-workers in NJ and NY pay 2-3 times as much in property taxes as I do in Orange Co. on a similarly price home. The longer one resides in their home, the bigger the Prop 13 advantage.

May God forever bless Howard Jarvis and Paul Gann!!

If fact, I was thinking of Prop. 13, which went into effect for the 1978-79 tax year. My tax saving from Prop. 13 covers a lot of sins committed by big spending Democrats in the State Legislature.

Well, in the north silicon valley area where I’m at we had significant upward movement in prices from January till just a few weeks ago. I noticed this morning on Zillow my house had lost 1% on the 30 day average from where it was yesterday. After reading this article I just checked again. Now it’s down another half a percent! Just from this morning!

So if my bad math skills are correct at this rate my house will be worth zero in about a hundred days. Gosh– I hope I can get my taxes reassessed!

Property tax reassessment is a two-decade lagging indicator. /

About 53% of total sales in San Francisco were condos; for years, all new housing construction has been condos and apartments. . . ,

Why don’t they just say it: Storage units for humans.

Some people, us included, don’t need 5,000 square feet for two people. 1,450 square feet and many miles of gorgeous ever-changing Bay views are enough space for us :-]

Exactly! My 99 year-old 1,400 sq ft Craftsman bungalow (with large detached garage for toys & a basement for workshop and tools) feels like a mansion to me. As an extra bonus, I have great neighbors too.

It comes down to being happy with what you have already. Wolf, you and your wife are obviously happy, as am I, and that’s what life should be about.

I raised four kids in a house that was 1080 square feet, though this was in Hawai’i where the kids were outside most of the time! The bedrooms were small and only used for sleeping and making more kids!! :) But we made it work. Don’t know why people think they need such large houses. I watch house shows sometimes with one of my daughters and we both marvel at the space “requirements” of some of the people!

Wife and I had this exact conversation last evening. Our house, also in the 1500 foot range is in a great location, beautiful yard and relatively easy upkeep. We spend 95% of our time in 20% of the space. We also paid 25% of what neighbors are paying now and that was only 15 years ago. The house across the street has had 4 different owners during that same time

Great response, Mr. R. If I had my druthers, ever since it’s build the “Golden Gateway” hi rise (in the Marina) would have been my choice of living quarters……but, alas decades later and many children raised it is/was always out of my reach. Born and raised in SF (Outer Mission) moved away in the late 1950’s to points south…..sailed the Bay for many years….the views from top of Market St. on a cold, clear winter day; from the North side of the GG bridge…….the vistas are incredible. In my youth the fog was so wet in early morning hours the streets/sidewalks looked as it large silver dollars were raining down. When did “homes” becoming “assets”? That’s when we got into trouble.

A bay view would be great but where I live in the urban ghetto there is no sunshine until around 11:00am when sun appears in the front of my 1100 sq ft townhouse. My back yard is all green moss from a lack of sunshine and not even a tomato plant can survive the summer. Winter is especially tough to deal with due to a lack of sun or views.

Never move to a townhouse in an urban ghetto as it is a lesson in noise whereby every two days someone is running a chop saw or chainsaw. Noise is not worth the move to these storage units for human beings.

I am a victim of human warehousing in CANADA. Optimism is a lottery ticket.

P.S. Don’t ever get poor in North America as governments en masse further deindividuate into the in-group of asset strippers in opposition to the human beings that are challenged with respect to wealth. In brief, when one gets warehoused in an urban ghetto there is not much left in life to fell optimistic about.

MOU

When I get much older I think I would prefer a condo. The only downside for me is possibly noise and HOA fees. But noise can be mitigated by a good design and build.

But condos generally get close to the city, nice views, a manageable space and I don’t have mess with too much maintenance or yard work which I hate anyway.

Condos have perks for those who dont like some of the normal shit that comes with single family home ownership.

Most condos built during Housing Bubbles 1.0 and 2.0 are shoddily constructed testaments to maximum profits and cutting corners. Residents foolish enough to buy into these money pits are going to be eaten alive by the assessments required to fix or remediate the shoddy work done by cowboy crews of illegals who slapped these complexes together.

Residential properties in CA are only reassessed at market value for property tax purposes when they’re sold, or on the value of unattached improvements done to a home (which is why many older homes in the OC and elsewhere leave a couple of 2x4s present to avoid having the entire property reassessed).

The only reassessment that occurs annually is up to a 2.0% increase allowed under Prop 13 and any bond indebtedness or parcel taxes levied by the municipality. There is a famous case know as “2 percent MEANS 2 percent” that was decided in OC Superior Court in 2010 wherein the Assessor tried to increase a homeowner’s assessment by 4.0% in one year because it had been missed the previous year. The judge ruled in favor of the taxpayer and informed the Assessor that under Prop 13, “2 percent MEANS 2 percent”.

May God forever bless Howard Jarvis and Paul Gann!!

Our cost basis is a lot lower here on the Gulf coast, but at one point in ’10 my house was assessed at a lower value than my car. Once values began to climb again, the new homestead protection kicked in and increases are limited by law — I just paid my $950 tax bill for ’19…not even enough to deduct.

“And this downturn in housing is taking off in a very strong local economy.”

Fascinating could it be that external factors namely the shattering of the “false economy” eg massive cheap debt-fueled buying activity is beginning to give way to the real economy?

Real estate prices and sales are declining, the stock market is getting volatile with regular 500+ point drops, car makers are announcing mass layoffs and the 2-10 spread is close to inverting. Someone convince me we’re not entering a recession or something much worse.

We are sailing in unchartered waters here: what we have seen in Q3 wasn’t supposed to happen, for the simple reason monetary stimulus is still in full swing in both Europe and Japan and credit conditions remain extraordinarily loose in the US as well: for all the wailing and gnashing of teeth getting a mortgage in the US right now remains very cheap by historical standards and commercial real estate is still one of those asset bubbles the Fed is most concerned about.

When a real estate market overextends itself or simply reaches its limits it becomes completely dependent on stimulus, fiscal, legislative and monetary, just to avoid a correction. That’s what Italy and Spain have been doing for almost a decade now to avoid a massive correction of their obscenely bloated construction and real estate sectors.

But as we are seeing it works until it doesn’t: Spain has already reintroduced 100+% and no money down mortgages, yet mortgage approvals have been steadily slipping since July. Italy is in the same boat.

All the endless attempts to reinflate the bubble managed to do is generate epic distortions that will have to be corrected, like it or not: a lot of people will have to eat a whole lot of losses.

It doesn’t need to be a recession: the Fed has proven this can be done in orderly fashion. The free punch bowl is being taken away while party-goers are still inhebriated, meaning they aren’t feeling a thing. The problems will start once they’ll find drinks have increased four-fold in prices while they were lying blind drunk on the couch.

Spain’s population has plateaued for several years. Italy/Greece/Japan’s have been decreasing for several years.

Because the only way CB’s know how to stimulate aggregate demand is through credit, after a while, the system literally runs out of qualified buyers to match those selling. 100% mortgages just kicked the can down the road. Eventually, the system burns through those borrowers as well.

The FED (and central banks) have created a MONSTER, and it is coming for all of us. They knew exactly what they were doing, being gods, they can do no wrong. Don’t think for one second the “friends’ didn’t have advance notice of the next move.

After 10 years you get a significant price reduction through inflation so Spain has seen a correction. Spain had a bloated construction sector 10 years ago. Not now.

This is literally the funniest thing I’ve read or heard today… because I’ve been reading and hearing the same since I care to remember.

Real estate is always undervalued, the construction industry is always going through a “tight spot” and always needs “fiscal stimulus”, lending practices are always “too tight”, regulation and zoning laws “too oppressive” and real estate is always a good deal because “prices have come down a long way, if you factor inflation in”.

In a way real estate and construction have stolen a trick from agriculture, as farmers are always on the local newspaper lamenting their misfortune, no matter how large their bank account and the subsidies they already recieve. Trust me: my grandfather owned a large farm and I’ve seen these things up close before turning eight.

I have no opinion if the housing market in Spain is still over-valued but if you keep prices constant nominal and have inflation than if you wait long enough the house prices wont be overpriced.

If the Fed stops raising rates at 2.5 – 3% the possibility of the large crash can still occur (and will, in my opinion) because they will not have taken the air out of the balloon enough and they also won’t have enough ammo to combat a decline. What they do past the presumed December hike into 2019 is going to be very telling. I hope they press on with hikes until at least 5%, or ideally 6%, and we have a steady asset decline from here until we get to those normalized rates. But based on the weakness the economy is already showing, I have concerns they will stop raising. Maybe a pause into early 2019 is warranted, but the amount of speculation in the markets right now is still rampant and wildly out of control, so if the Fed wants to get a true handle on things they will press on and let the weakest links start to falter.

Almost forgot to mention: crude oil prices are collapsing.

The 93 million people “not in the work force” but not counted as unemployed, oh heavens no! don’t seem to be doing much driving.

MC01 –

“We are sailing in uncharted waters here”

Totally agree.

While there has been an astounding increase in the money supply in the last 17 years, almost all of the increase has been in the form of debt. I an unable to predict how it will play out, and I doubt that anybody else knows, either.

I have seen reports that China was the leading foreign funding supplier for public debt in the US(not huge for over all debt but noticeable). I am sure with the current trade war that has changed. Now with them cutting back on funding US debt the markets and the housing have all tapered off. I don’t think that is a coincidence.

Not uncharted waters. Just very murky waters, still no light at the end of the tunnel either.

Exactly my thoughts David

In San Mateo, rents are still “too-damn-high”. Yet, three realtors told me last weekend that renters are toughing it out and staying put. Lots of open houses but the traffic of would-be-buyers has slowed down to a trickle. This observation is statistically worthless but it matches the general trend in the Bay Area.

Maybe buyers are either afraid of buying at the top or maybe they are unable to qualify for a mortgage. Or maybe they have no plans to stick around for the long term. Maybe those who really wanted to buy a house already did it when interest rates were lower. Either way, the slowing down points to a down market for 2019.

Well that and buying doesn’t look as good to people when they consider they may be trapped in that starter home for 10 years instead of 2… there were possibly a lot of people banking on trading up in as short as 2-5 years. But that wont be possible if price are flat/falling.

Priced for foreigners. The only explanation.

In the capital they are, prices peaked in 2014. Taxi drivers, useful conduit of public sentiment, now state the falling of house prices as a fact whereas a year or two ago, they’d typically state it as something that ought to and will happen.

This week I saw a house in Ukiah drop in price $100k on Zillow. For a while there, even the most remote podunk in California had absurdly inflated prices.

Interesting you mention Ukiah. Have relative in not too distant HOA that has residence and a rental. 3 months ago the renters were asked to pay about $200 month more. They refused. Back and forth. Long story short, good long term renters moved and got a place in same HOA for less money. So “things” are not what they are perceived to be now. Turning homes into “assets” instead of treating as a place to live has ruined our housing situation. But, it’s all about “profits”, no? “What Fools These Mortals Be!” (Puck)

Indeed. I live in Santa Rosa, my rent has gone up $600. a month over the past four years. $1480. plus utilities for a 400 square foot apartment.

The fraud of our “recovery” based on a massive expansion of debt, the Fed’s tsunami of FedBux “stimulus” since 2009, and corporate buybacks of their own overpriced stock with borrowed money, is about to be laid bare.

No matter how hard I stare at those graphs, I still don’t see evidence of a massive decline. Maybe we are in the early innings. Certainly demographics will come into play as 10K baby boomers continue to retire daily, and vote with their feet as they migrate out of high tax states.

It would be nice if real estate could drop 30-40% to allow first time buyers a chance, but trying to predict an event like this with a reasonably strong economy, and a persistent headwind of 3% (real) inflation, is a fools errand–but fools errands can be fun to toss up for discussion, hence I will stand aside and let the comments section debate rage on, brimming with breathless anecdotal evidence, full of sound and fury.

Keep in mind recent posts have opined on the 10yr treasury rate, once past 3% would continue upward like a train leaving a station for good. Well, it looks like the train has now stopped and is backing up to the station– something all the experts did not contemplate, but have plenty of new narratives to describe why this has happened–all, mind you, after the fact.

Well put Wendy. There are a handful of doom porn posters on this site that have been prattling on for the last five years about how we are just a moment away from crashing. Then another year goes by. Had I listened to the Stockman’s out there I’d be 300k lighter.

So they got the timing wrong. It doesn’t mean that a crash WON’T happen. It’s like the proverbial “Big One” that will strike CA along the San Andreas – we don’t know WHEN it will happen, but do know that based on past history, it WILL happen.

Would you rather live in an unreinforced masonry structure sited on compacted fill when the “Big One” hits, or a single story wood frame structure bolted to a concrete slab poured on rock? The same analogy extends to the coming crash, which will be of the same magnitude in financial markets as the “Big One”.

Thanks for posting the retirement number. If i remember my demographics study from a decade ago, USA birth rate took a dive during the Korean war, but bounced smartly after the 1953 truce, and took off 9 months after Elvis appeared on Sullivan, spring of 1956. So retirees are piling up, and they’re going to want friends and helpers around to commiserate…

Real estate would drop for sure

No one knows when and and how much

I think the beginning of the decline has started and it would take few years to play it out

The prices are out of whack for sure

Do you have any control over your advertisers, Wolf? “Noah and his family still alive. See striking photos “

Please.

@Bill Shortell-

The “ad-sense” is based on your browsing history, e.g., the “click bait” that you follow. Try a VPN service.

No, I don’t control the advertisers. I don’t even know them. I deal with ad agencies and automatic bot-driven ad exchanges (mostly Google) with behind-the-scenes bidding for my ad space. Just look at this with a sense of humor. That helps.

Unrelated to topic.

\\\

Wolf, am I wrong or did we just have a partially inverted yield curve on Tuesday with a a convergence with the spread almost being non existing. Yes, the yield increased in general YtY, and we had a previous “splash” in Q2 (all yields dipped and recovered) but this is different.

Y1=2.71

Y2=2.80

Y3=2.81

Y5=2.79

Y7=2.84

\\\

Yes the 3-5 yr yield started inverting a few days ago

It’s just a correction. Tesla construction bots assemble oriented hemp strand board (ohsb, a byproduct of the thc/cbd industry) into mini/micro homes at practically no cost. So it’s merely a transition to the ‘sharing economy’. SF is a loving city.

In the 2008 recession, I suffered a 15% pay cut and gutted benefits. My retirement funds took a 40% hit, as did the market price of my home. Those were big losses – but I was one of the lucky ones, able to keep going. A lot of my co-workers suffered 100% cuts.

I am out of the workforce now, have no debt and have my finances configured as best I can to weather the coming recession ok. We’ll see.

Zillow says the market value of my (East Bay) house took a 4.4% hit over the last 30 days. It’s paid off and it’s a place to live, not an investment, so at this point I claim I don’t care. But I sure do watch it…

I think those that continued to work, save, and invest during the 2002 and 2009 downturns are still in great shape. The key was to keep adding money to “losing” investments while the general public was running screaming for the exits. We may now be in a similar period, but “this time is different” in that a lot of baby boomers are now retired, so they don’t have an income to invest each month, even though they know what to do this time around, they will not have the revenue stream to participate. I know that some of my best investments were made when clicking the buy icon, I had the feeling that I was going to throw up.

Don’t look at Zillow, it will drive you nuts. For fun, compare Zillow prices to Redfin, and you will realize that these estimates are very rough at best, and are pure fiction at worst. On Zillow my home has “appreciated” $500K in the last 6 months, only to fall $100K in the last two weeks. It is what it is, and the only price that matters is what the market is when you decide to sell, and if you have a good agent that can sucker the money out of a person (preferably from out of town) by convincing them they are getting a good deal. All cash buyers, and a lack of understanding of the local market, is a killer combo–for the buyer, that is.

Zillow and redfin would give you a general idea and direction

Don’t take these estimates too close to heart

SF and Hongcouver don’t matter as the real estate was artificially inflated by people with money. The places (like Toronto) where real working slaves have been priced out of the market will be the winners if the prices fall (at least 30% or more). When the average Joe can’t afford a home then something doesn’t compute.

Toward the end of 2015 we were keeping an eye on SF real estate and thought prices were astronomical. Bidding wars were in full effect. Now I see sales on Trulia in the past few months where people bought in 2015 and recently sold for $300K – $400K gains. The recent price drop is just eroding the insane appreciation in the last three years, but what about the run up through the end of 2015? That should be another 20% that comes off of prices assuming normal interest rates. The recent price drops are a move in the right direction but prices need to come down a LONG way in SF before they make sense. The run up in tech stocks has been so insane that a lot of rank and file at places like Google ended up making WAY more than they ever expected or knew how to manage. Most of those folks are professional couples, and they plowed a ton of that money into housing. I know so many of those people personally and have seen it happen over and over. I recall discussing real estate with a buddy in such a relationship, and he doubted that interest rates would ever rise again.

The bubble in tech stocks is going to hammer this real estate market.

You would need to wait couple of years at least for the prices to come down substantially

Real estate market is a sentiment driven and is like a titanic.. takes time to change

Once again, hope everyone is doing well and I hope you can enjoy the Fed gradual draining of historic liquidity.

But, my house is my retirement! Only if you liquidate it. Otherwise, it is subject to change.

The boomers in general are delusional in their expectations.

Now comes a winter long delayed in asset prices. Inflation needs to be at 10% for a decade or so to even begin to approach where asset prices are now. And it ain’t gonna happen.

Welcome to a party that nobody anticipated, asset deflating fed actions in a low growth environment.

The biggest rump of boomers is now going to be turning 65, 1954-1963, and it will be special.

AllenM. That the scenario that I’m seeing. So much of current home equity and stock market capitalization were “time locked” as retirement funds. Once these funds have to be liquidated into cash or cash-equivalents, there’s going to be a severe disconnect between the number of sellers and the availability of buyers.

Typically, inflation cures the mismatch, but I’m not sure inflation is possible given how levered the private sector is. Lord knows, Japan has tried for decades.

Of course, FedGov could solve the problem with 90% tax rates on billionaires to force income downstream. But it’s more likely they do something stupid like “privatize” social security.

BTW, I just looked at the Dow 5year chart, Tanta is here still, for I see pig ears….

Da Mortgage Pig lives?

Viva Tanya !

I still have my mortgage pig t shirt somewhere.

Tanta. Stupid spell check

The interesting question of course is how far beyond the housing markets does this extend.

In the 2006-8 crisis, the cyclical drop in real estate values spread to banks and insurance companies and before people knew it Lehman Bros and AIG and others were failing and demanding billions in bailouts.

So, assuming that the cyclical real estate market will indeed follow its cycles and won’t rise into the stratosphere endlessly, how far does this spread and hurt this time around?

The spread of contagion is a function of NYSE stocks that are valued disproportionately to actual worth. Corporate defaults are the new subprime meltdown but their demise has not really hit yet because QE spigots were only turned off after they all got plastered & three sheets to the wind with share buybacks. Now the naked swimmers are starting to wake up to the fact that everyone is just about to see a few too many naked swimmers even for Warren Buffett’s liking.

Corporate America is about to evidence the insolvency of GE which is going to be the kind of body blow that takes down a few companies with them. When the dust settles from GE it will be re-set time.

USD is getting old as currencies go too, eh. What is the statistical probability of USD being around in 25 years if the average currency is around 100?

MOU

I lived through home ownership in the Bay Area in ’08. What was a bit odd where we lived was that a main price driver was the banks being unwilling to loan what people were willing to pay. In the aftermath, a buyer and seller could get together at 500K for a condo, and then the appraisers would come in and declare it 450K usually by digging up an a beat up foreclosure to drag the price down. So buy had to come up with cash for the difference or seller needed to drop the price.

What happened is that literally nothing was for sale. People stayed where they were or left and rented the place out.

The people who really won? The tech workers from Google, Facebook, Apple, etc. who moved to California around ’08-’09. Those companies weren’t really hit by the recession and workers started accruing stock. Additionally some rents were comparatively affordable, particularly from those people who rented their place out because it wouldn’t sell or they were underwater. A 4-5 years later their stock provides a down payment when prices are still near the bottom. Then 5 years after that, their home/condo is worth 2x the purchase price and 10x what they put down.

The people who lost? Those that bought a home in ’05-’07, lost their job and moved away. Even some of these people might not have been that much of a loss. People were taking 5/15/80 loans and I know of people that stopped paying their mortgage for several months waiting for eviction. I mean 5% down on a condo is 25K, stop paying mortgage for 8 months is probably in the neighborhood of 16-20k.