Sales decline to steepen, no respite in sight.

The reasons for the housing-market downturn are in the eye of the beholder, as we will see in a moment. But whatever the reasons for it may be, the data on the housing market is getting uglier by the month.

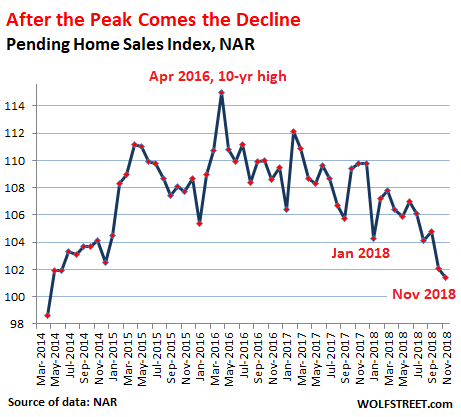

Pending home sales is a forward-looking measure. It counts how many contracts were signed, rather than how many sales actually closed that month. There can be a lag of about a month or two between signing the contract and closing the sale. This morning, the National Association of Realtors (NAR) released its Pending Home Sales Index for November, an indication of the direction of actual sales to be reported for December and January. This index for November fell to the lowest level since May 2014:

“There is no reason to be concerned,” the report said, reassuringly. And it predicted “solid growth potential for the long-term.”

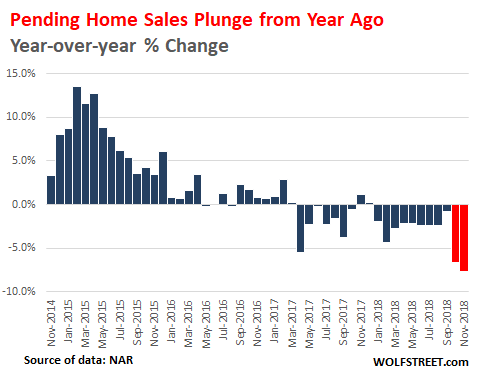

And the index plunged 7.7% compared to November last year, the biggest year-over-year percentage drop since June 2014. The drops in October and November are indicated in red:

All four regions got whacked by year-over-year declines:

- Northeast : -3.5%

- Midwest: -7.0%

- South: -7.4%

- West: -12.2%

The plunge in pending home sales in the West, a vast and diverse region, will prolong the plunge in closed sales for the region. Particularly on the West Coast, the largest and very expensive markets — Seattle metro, Portland metro, Bay Area, and Los Angeles area — have been experiencing sharp sales declines, a surge in inventory for sale, and starting this summer, declining prices.

Today’s pending home sales data confirms that these trends are intact and will likely continue.

The NAR report blames the sales decline in the expensive markets in the West on “affordability challenges” – because prices “have risen too much, too fast,” it said.

And this is a true and huge problem: Home prices have shot up for years, even while wages ticked up at much slower rates. At some point, the market is going to run out of people with median incomes who are willing to stretch to the limit to buy a starter shack; and the market is going to run out of people with high incomes who are willing to stretch to the limit to buy a median house.

For example, at the peak, the median house price in San Francisco was over $1.7 million. That median house is nothing fancy. And the market has run out of high-income people blowing so much money on a modest house. Hence prices have come down sharply over the past six months.

“Local officials should consider ways to boost local supply,” the report says. Alas, there is all kinds of supply suddenly coming on the market. It’s not that there isn’t anything to buy; the problem is that everything is too expensive, and that sellers and buyers no longer see eye-to-eye.

But the decline in sales on a national basis, according to the report, is a “short-term pullback” that “does not yet capture the impact of recent favorable conditions of mortgage rates.”

Sure, lower mortgage rates are a relief for buyers. But wait… According to the Mortgage Bankers Association, the average rate of conforming 30-year fixed-rate mortgages with a 20% down payment has dropped to 4.94% during the latest reporting week. This is 23 basis points off the high of 5.17% in early November.

But here is the thing: In January 2018, when the Pending Home Sales index plunged to the lowest level since December 2015 (indicated in the first chart above), the NAR blamed low supply of homes and surging mortgage rates.

Since then, supply has sharply increased, and mortgage rates?

Currently, the average 30-year fixed rate, at 4.94%, is still 54 basis points higher than it had been in January. And if an average mortgage rate of 4.4% was blamed for plunging home sales in January, then an average rate of 4.94% isn’t going to suddenly boost sales.

There is a lot more at play here than just wobbling mortgage rates. At the top of the list are woefully inflated prices that potential buyers now see as such.

And these potential buyers are now also confronting the fear that prices will decline, or further decline, after they buy. This is a scary thought, given the amount of leverage and the large dollar figures involved in a home purchase. Potential buyers now see that after the purchase, those fears could translate into some real and long-lasting headaches.

n Seattle, house prices dropped 4.4% in four months, the biggest four-month drop since Housing Bust 1, according to the Case-Shiller Home Price Index. Prices also deflated in the San Francisco Bay Area, San Diego, Denver, and Portland. Read… The Most Splendid Housing Bubbles in America Decline

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So far the pullback in the housing market is not keeping pace with the stock market, and I believe that if history is any indication, that the solution will be more people moving to California who can afford that housing, and people who cannot afford it will be moving away. Those in the middle will rent, with more emphasis on affordable housing policies. Isn’t that how the state came to have one of the largest global economies?

>”Isn’t that how the state came to have one of the largest global economies?”

No.

> No.

Flugelhorn.

Why would people who can afford would move into CA unless and until they have good jobs ?

Bottom-line is: CA housing has to go down. Housing market is like a titanic unlike stock market which can change on a dime. You’d need to wait for a year or two atleast for the prices to come down big time. Just think: Housing slowing down amidst strong economy.. How would it fare when the economy is bad

Everything financial got addicted to the crack cocaine of low, near zero interest rates.

Now they all gotta go through rehab.

In a debt based economy, people are basically gambling whenever they make a major purchase. Unfortunately, their decisions are often based on emotion rather than logic, which is why you have bubbles. When their income becomes overwhelmed by the payments on past purchases, their present spending has to stop. Overoptimism becomes over=pessimism and their gamble, for many, goes bad.

This ridiculous market is not sustainable without money laundering, foreign money and ballooning tech stocks and each of these are going away.

Only the most favorable places seem to be selling. I’ve noticed quite a few houses slash prices and then remove their house from the market. Guess bidding wars are not working anymore, but 20k in property taxes will start to hurt sooner or later.

https://www.zillow.com/homedetails/1460-Davis-St-San-Jose-CA-95126/19581697_zpid/

https://www.zillow.com/homedetails/1556-Foxworthy-Ave-San-Jose-CA-95118/19693557_zpid/

“Isn’t that how the state came to have one of the largest global economies”

In other words, CA’s GDP per capita is 7th highest in the US and 6th highest in the world.

https://en.wikipedia.org/wiki/List_of_U.S._states_by_GDP_per_capita

The democrats in CA always brings this stat up around election time and dimwitted CA voters always lap it up. Ignoring all the other metrics where this state has lagged behind.

By this measure, China, you know, the second biggest economy in the world ranks between 76th and 83rd place depending on who is counting.

GDP per capita is not a very relevant measure of standard of living. It uses US dollars to measure the cost of goods and services in America. In almost any country, a US dollar buys a lot more than it does in America. Also, the financial status of the consumer is important. If the average person is saddled with overwhelming debt and financial obligations just to maintain a certain lifestyle, a comparison with a nearly debt free citizen in another country is not valid.

A US dollar buys 5X the lifestyle in China as it does in the States. A citizen in flyover country with a $60,000 income is doing OK, while in LA or SF he is struggling.

California has prospered with a “country club” economy since the aerospace industry was big in the 50’s. The premise of opening the state to manufacturing jobs (something the GOP always tries to do) has been opposed on mostly environmental grounds. The air in LA is actually better. A service economy grows around the media/ entertainment (Hollywood, Google, FB) industry. Those with the capital gentrify the most desirable property. (SF?) Middle income people are leaving, while the homeless in the midwest are given bus tickets to the promised land. The rich are way ahead of them and RE values should remain solid. (IMO)

During the last 5 years I have known or met many younger people who stretched their borrowing capacity to the limit, and tapped mom, dad and any other available relatives to get in to a crummy starter house in a mediocre neighborhood because they were desperate to get on to the “property ladder”. The houses they bought were often bad values in terms of living space per dollar, require tons of remodeling, and are in up and coming areas with horrible schools. I think they were only willing to take this risk because they assumed that real estate will only go up and they could soon take their equity gains and move to a better place. Once they “property ladder” gives the appearance of being a greased slide to purgatory most other young folks will wisely decide to wait until house prices have completed a long steep slide to rationality before climbing aboard.

It takes about a million Bagholders to grow one billionnaire. I’m sure your finds aren’t alone.

“It takes about a million Bagholders to grow one billionnaire.”

~Bobber

HAHA! Do I attribute that quote to you?

Re: “the property ladder”, it’s been skyrocketing so long that I have to remind myself that Portland was a run-down dump even in the 90’s because economy & crime reasons.

That said, a lot of the people who bought in CA about 5 years ago actually bought at the bottom. Prices unreasonably more than doubled in many places, especially around Bay Area. As much as I think it was, and still is, unreasonable to leverage to your eyeballs to buy a mediocre house in a bad neighborhood, those who took that gamble, won. If they paid 50 K down payment on a 500K house, they are now proud owners of a million dollar house. Looking back, was that a bad decision? Not so sure. Will the prices go down? Absolutely. Will it crash, crash? Say, half of what it is today? Highly unlikely. Given where we are, if prices go down by half, we will be in deep trouble collectively, and powers that be will do everything to save those brothers in trouble. You and I will pay to save them. So, heads they win, tails you lose.

I hear this every time especially from people associated with real estate that prices may soften a bit or go down a bit but would never crash as this is California.

But we all know how things turned up

AS Engineer, let’s NOT claim victory or defeat at half time. Assuming there is a cycle which has been true in history, you have just seen half the cycle. The other point is that those who put downpay of 50K is at risk of losing 50K if house prices did NOT rise this much. Although the ZIRP and QE did increase the chance of asset inflation, you still have to consider what would happen to them if the alternative outcome happened to be true. My general strategy is save half, work 30 years and retire 30 years on savings. Consume within my means and buy stuff when cheap. This is laughed at. Your savings will be inflated away and things will never be cheap in California. When discipline is punished and immediate reward on the table, people forget about any discipline. You think the reckless debtors that front run savers on assets have put themselves in a head-they-way-tail-others-lose position? Wait till the cycle complete. Try NOT to draw conclusions at half time. If you think you can predict that the FED will bail everybody out “LIKE LAST TIME”, let me tell you this. In wealth transfer games, you can NOT do what you did last round. If you do, you get killed by your competitors. FED knows this and if they repeat their policies, FEF itself may go extinct. Do NOT believe? It is one bailout away from Yellow Vest to occupy the FED and guillotine some bankers.

There are a lot more reasons to be a home owner than to be on the “property ladder”!

One very obvious one is a place to have the *stuff* people feel is necessary to be a member of our society.. Stuff like jet skies and other yard art that people use once in a while and really can’t rent.

One of the things that makes America Great is that we have stuff, lots of stuff.. We are consumers and we need a place to keep all our consumer stuff.

Uh, hello… understand the rent to price ratio first before considering the purchase of a house. Yes, house, not a home. “Home” is a warm and fuzzy term used to get you emotionally attached to a real estate purchase by real estate agents who want your commission. Home is what that house will become after you purchase it.

Financial prudence first, please.

Rent to Price ratio:

https://20somethingfinance.com/price-to-rent-ratio/

The price to rent ratio failed to identify some of the greatest real estate buying opportunities of all time. Feel sorry for people that relied on that ratio during the mid 90s to early 00s. They lost their shirt renting.

Tell that to the folks who bought during the ’06 to ’08 time frame. Just saying it’s a tool to use when looking at houses.

Still kicking myself.

-SF bay area renter

Make sure you let us know when the price to rent ratio is again at a point when we can be certain of all appreciation. I’m not interested in advice from people who tell me what I should have done 30 years ago. What about all those folks who lost their shirts buying in the late 2000s when the expected appreciation to continue indefinitely? Your comment was not well thought out.

Unlikely to happen soon. Rents, as measured by total rental income divided by total number of rental units, has appreciated by 200% in the last 10 years.

Thus proponents of high real estate prices, higher than the value achieved during the last bubble, declare that this must not be a bubble. But, in reality, there is a bubble in both house prices and rental costs.

Crushing the middle class with both housing / rents and healthcare. We’ll see where that leads.

There is another interesting dynamic with condos and seniors or those who bought intending to move in in their later years being hit with large special assessments and fee hikes (in Ontario new legislation has mandated reserve funds have three years to play catch up after a major draw down such as replacement of aging elevators (even though the next replacement cycle will be a couple of decades off) so the intention to avoid special assessments with this new mandate on reserve funds has had unintended consequences.

So even if the reserve fund appears healthy this may be before major upgrades that are cyclical.

And of course there are a chunk of seniors who never owned and even with so called rent controlled building are being hit with special assessments. (In the context of fading indexed defined benefit company pension plans.

As for seniors who bought condos during the first blush of this type of housing…say thirty forty decades ago who have lived on fixed incomes…there really is no place to run no place to hide when a condo suddenly hikes fees well above inflation over the short timespan of three years…..and of course the higher fees are also a deterent to new buyers who can absorb the cost but not the fees. Many of these elderly residents could absorb the fees at a reasonable pace but could not afford to upgrade their internal units.

This runs along with a dwindling stock of affordable housing for rent that in the gta (Toronto) are being closed at a rate of a unit a day due to unsafe conditions due to poor maintenance over the years.

And the size of the units is on a share footage growing smaller while ceilings grow higher to disguise lack of living space and storage

Thus the popularity of the instant pot for younger generations. We hear about lack of affordable accomodation for families but for aging boomers this is going to become a major issue as well.

My wife and I recently looked at a condo in such a place. The complex was built in the early 90’s as investment and retirement property for folks from Japan. It consists of 5 towers scattered throughout a gated property landscaped by a famous Japanese landscape architect with underground parking and elevators for each tower, an indoor pool, rec center, tennis courts etc. It was built to look like a resort in hawaii, but is only 10 minutes from downtown portland. The HOA that maintains the place is very well run and has all financials for multiple years online. But after a quick inspection of the books we could see the place was in a financial death spiral. HOA fees had already climbed to a fairly high level compared to the selling price of the units, and you could see that the large and elaborate infrastructure was needing more and more maintenance as it aged., but their list of needs was even higher, and the size of the uncollected HOA pot was increasing year after year. Most of the occupants looked to be the original buyers from the 90’s ( not wealthy japanese as that market crashed before the place was finished) and were probably on fixed incomes or declining investment portfolios. In such a situation there seems to be no way out as raising the fees to cover growing costs would drive existing tennants bankrupt, or force them to sell in to a market that is discounting condo values due to high hoa fees. A bad situation, and we ran away though my wife still loves the view, the landscaping and the beautifully remodeled unit we toured.

Interesting story, can you drop a hint about where these conds are? Zip code, at least?

Zip is 97210 in the west Hills of Portland Oregon.

Probably the Quintet.

http://www.thequintet.org/

South Waterfront was a mess last time around and probably will be again. The interesting thing was how long the banks sat on empty, unsold, and foreclosed inventory.

Being a barely Millennial.

Most of my friends in LA have recently bought not because it was a “great” deal, but because a few years ago, the lending standards where easier to meet when buying vs. renting.

Landlords were doing a lot more due diligence on credit scores when renting then the secondary lenders attitude toward their borrowers. Add the innocence of not predicting interest rate hikes and you got a lot of gullible youngsters in the housing market. A hand full of friends have definitely dipped into their folks pocket for the down-payment.

To be fair, if they bought prior to 2016, most of my friends are still up on house appreciation, so can’t feel sorry for them yet.

With markets down, and treasuries down, i wonder if the lower rates now might last and give housing a second wind?

Oh, these lower rates will be here a while; I suspect we’ll see 4.25% by next summer. The issue is whether the LTVs will be the same.

Conv is at 4.5% and FHA hit 4% today.

Rates are at 6 month lows.

Inventory is up and price reductions are prevalent. That being said I dont know if this is the beginning of a “crash” or jsut a normal pull back.

Properties priced right go FAST. Sellers with a mindset of 6 months ago where they hold the leverage are in for a surprise, they aren’t and need to accomodate buyers and adjust their expectations.

What I’m seeing in Sonoma County pretty much agrees with what Broker Dan has written.

Hmmm… “FHA at 4%”…

Talking to various folks in the industry the sense I get is that the FHA has become the lynchpin of the latest housing bubble.

It is patently obvious to anyone with half a brain that Ginnie Mae is going to go belly up in the next recession, at a huge expense to the taxpayer (although the general consensus in the MSM will be that “nobody saw it coming”).

If there are lower rates, its because the stock market crashes even further. Everyone who screams sell, sell, sell to their broker moves the money to something safe, like a CD or UST. Thus, the sellers can lower their rates and still have business coming in the door.

On the other hand, if the stock market goes past this little speed bump of a pull back and then goes back to climb, climb, climb, then the Fed will be raising rates both to try to keep the bubble from getting too big and to get the rates back up to what they consider normal before the Great Not A Depression.

I guess the ideal for low rates is if someone is a person who’s wealth and income are not effected by a plummeting stock market who can take advantage of the resulting lower rates and real estate prices that are dropping fast as well.

So, I’m a big fan of Wolf Street. Read it all the time. I also happen to agree with most of it.

That being said, it feels like some of this is hyperbole and there isn’t a single bullish article. Is the entire blog about the economy “plunging”?

Look, I totally agree that we are in for stormy weather but perhaps include some positive articles?

Seems to me that you have not even read this site even one bit, otherwise you would not say that “the entire blog about the economy “plunging” …. hahahaha… I have said numerous times that the overall economy is STRONG, and HOT, and employment is STRONG, and that the Fed thinks it’s STRONG. So clearly, you haven’t read a thing on this site.

However, asset prices are something else. Turns out the Everything Bubble has turned the corner, so get ready for a lot of non-bullish data on inflated asset prices now deflating and risks being repriced, because that’s what is happening right now, like it or not.

Btw, I covered the housing bubble on the way up – that was “bullish” because prices rose to ludicrous levels. Now I cover it on the way down. Just happens to be the phase we’re in.

If you want to read unadulterated hype, there are plenty of publications that specialize it. They even proudly regurgitate corporate propaganda. That will make you feel better.

Here you go, Ron — the NAR has all the good news you need:

https://www.youtube.com/watch?v=oPtJ28j6TP4

For years I have assumed the NAR folks are one and the same as the folks who publish China’s economics statistics.

Saying the economy is strong and employment is strong is complete bull. Companies can’t find workers because every kid thinks they are going to be college rich someday and we are herding young people into college at record rates and record debt levels. They aren’t going to waste time entering the workforce after high school when they can spend a decade in college earning the degree and coming out making $100k. But they have been lied to and made debt slaves, unableto grasp that only around 7% of employed people make that kind of salary.

And the economy is strong? Come on! The US economy alone cannot function or “grow” without cheap money and debt. But hey Dick Cheney said don’t worry about it. Meanhile corporate America is churning out record CEO salaries, golden parachutes, and billionaires! Yay MAGA!

“we are herding young people into college at record rates and record debt levels.”

No to part 1 and yes to part 2: College enrollment has been in decline since 2010. But yes, student loan debt is at record levels.

Seems to me that not only are asset prices inflated but so are degrees. (I just read a book on this, called The Case Against Education, on the signalling theory of education; and I can’t think of an argument against it).

Is it just me, or does anyone else get the sense that the root of all this is that everything in our economy and society has become zero-sum? It keeps reminding me of Carter’s speech:

https://youtu.be/kakFDUeoJKM?t=459

There is a part of me that agrees with your College statement…. Not enough kids are learning a trade and getting there hands dirty anymore. Not sure when it started, but I guarantee it wasn’t in the last 2 years…It’s been going on for at least a generation. This generation will feel the pain..Just like any product, flood the market and prices/wages will go down.. not sure what the fix is though.. manufacturing has dried up and construction is as unpredictable as the weather.

As far as corporations go, I’ve seen fat being cut at the top and the bottom …My guess is they finally have to show growth without borrowing money for capital project and finance them with real profits.. I think there finding its a lot harder then anticipated..

I find Wolf generally contemplative and informative with a defensive approach. Actually I would say he is too generous on the state of the economy except that he does not openly push that viewpoint, nor one of doom, i.e. he understands the definition of a zero sum game and the good position to observe it from.

Hi Ron , Wolf and Readers, season’s greetings to all.

Ron, if you ever need ( God forbid) going to an MD for consultation you’d definitely want him/ her to be diagnosing the problems you might have with the transparency you’d expect from a professional.

Wolf in his analytical views here is NOT trying to sooth the pain of the “ self deluded folks “ !

I presume this is precisely the reason that a level headed person would be seeking.

… and Wolf if possible please remove those “ Tinder” app ads on here , they’re Not “ Wolf Street worthy “ !!! :)

I promise to click on all the worthy ads , Happy new year to you all.

Jack

Jack,

I don’t see Tinder app ads. I see that guy from Fisher Financial all the time, and occasionally — too rarely, I admit — I see Asian girls in more or less revealing outfits lusting for older men. And for some reason, I see a fancy Japanese crapper a lot.

Everyone sees something different. That’s part of the fun :-]

I like comparing the Wolfstreet ads on my laptop vs my phone. Judging by the quality of offerings, my laptop thinks i’m broke and stupid while my phone thinks i’m wealthy and sophisticated.

My laptop has known me longer…

Jack you think you’ve got it bad? I’m getting lectured at by WolfStreet’s advertisers about the fact that I clearly need a

“POWER WASH FOR MY BOWELS”

I shit you not.

Add to this the public expenses that will now have to be paid for that were promised on the expectation of continually rising tax bases. My city has seen annual appraisals on property exceeding 10% a year for about a decade. It will be interesting to see if those appraisals decrease with a downturn in housing. (I’m not holding my breath.) Folks on fixed incomes are having trouble making payments on their taxes as they rise faster than they can adjust for. Likewise I seriously doubt the politicians are going to run and cut the extravagant services, pensions, and civil projects they promised to get into office. That money will have to come from somewhere.

KGC said:

“Folks on fixed incomes are having trouble making payments on their taxes as they rise faster than they can adjust for. Likewise I seriously doubt the politicians are going to run and cut the extravagant services, pensions, and civil projects they promised to get into office.”

Please name a recent federal public office holder who promised to increase government pay and benefits for working folks.

You can’t, because that hasn’t happened on a long time.

In fact, both Dems & Repubs and been mercilessly cutting pay and benefits to working folks will enacting massive tax cuts for the rich and starting illegal wars of aggression requiring massive increases in war spending.

And Dems are at least as good as Repubs at doing this.

You are saying public services and benefits are “extravagant” as opposed to frugal Wars Of Aggression, frugal Massive Tax Cuts For The Ultra Rich, frugal Trillions In Subsidies for Rich Gigantic Insurance Companies for ACA?

Dick Nixon started Federal subsidies for local governments. Those have been steadily eroded and transferred to the Ultra Rich.

It is the unraveling of Federal subsidies to local governments that is the reason your local taxes are going up faster than the did in the past.

They don’t promise it, they just do it or just avoid changing it. Check out the prison guards in California for a real taxpayer butch haircut. Or just look at Illinois.

Pension spiking, COLAS and best one year of FAE to compute pension payout leads to extravagant pensions and underfunding. Full blown pig out.

The funny part is the pinwheeling eyeballs when you try to explain what a ripoff that is to the taxpayer.

They think they deserve it while no one in the private sector gets that deal.

Is there any nexus between new, used housing

sales declines and a recession?? Schiller said no.

Thank you for any replies.

Reversion to the mean can be a bitch. Things are way out of whack now.T he national mean ratio of house price to household income for over 50 years is 2.2. Of course, all all real estate is local. Pick an area, look up the numbers, and see. The Bay Area and Park Avenue will have different ratios than flyover country.

Reversion to the mean is as sure as gravity.

http://www.mybudget360.com/the-magical-2-housing-ratio-between-median-nationwide-home-prices-and-household-income/

My housing experience has been so much less angst-ridden than that discussed here that I wonder if there’s anybody out there who might find it worth looking at for themselves?

https://lenpenzo.com/blog/id43684-grandfather-says-the-benefits-of-diy-housing.html

Yun is delusional thinking this is a short-term pull-back, as are most economists who continue to drink the Kool-Aid. I had a good chuckle reading the suggestion that the decline in pending sales had not captured the impact of “recent favorable conditions of mortgage rates.” What Yun, and most of the real estate industry pundits are ignoring is the complete financialization of the U.S. housing market. When the bear market officially arrives, this reality will eventually sink in with all of these willfully ignorant “economists” who are really just overpaid carnival barkers with fabulously flawed models.

If you work for the real estate industry you can not tell the truth. That would be bad for your employer. Besides, as Churchill once wisely said, “Few men are prepared to accept the truth.”

I may still have a few of those NAR bumper stickers somewhere–“It’s a good time to buy a house”, left over from 1986.

Everybody who bought a house from me in 1986-1988 ended upside down in their mortgage, just like me. House prices in CT dropped up to 50% and took a decade to recover. Ten years!

I felt like they all chipped in for a hitman. Do I still have that target on my back?

Great article w/ good explanations/supporting data! Thank you. Based on comments, I think many haven’t (yet) tied housing bubble 2.0 with declining house sales and prices as well as rising inventory. Sort of “deer in the headlights” response (for now). I’ll reference your most recent article on the subject:

The Most Splendid Housing Bubbles in America Decline

by Wolf Richter • Dec 26, 2018

There’s definitely a relationship here, that will become more apparent as we move further to the downside. Some, such as myself, would say cause and effect. Ref.: housing bubble 1.0.

I’m looking for a reversion to the mean such that house price to income gets back close to historical 3:1 ratio, or in that neighborhood, for shelter-buyers. Any MSA higher than this has some serious revertin’ to do, and there are many. The justification for this, IMHO, is that the speculators, like Elvis, have “left the building”, with shelter-buyers becoming the market again.

My 2 cents here.

So tired of hearing from most mainstream media sources that it’s a simple lack of supply that has lead to high housing prices. There’s a shit ton of houses in my neck of the woods for sale but everyone’s asking too much and now houses are sitting and asking prices are dropping. It’s encouraging to see that even the more appropriately priced houses are not selling quickly, probably because everyone knows prices are flatlining or coming down. How far they go I guess we’ll see. I’m very eager to see what happens in the spring. We’ll see if the insanity ensues. Course with the way this white house runs things… Serenity now!

Homes in my area have gone up 50-60% in the last 2-3 years and the number of active flips going on right now is definitely reminiscent of the last bubble.

“At some point, the market is going to run out of people with median incomes who are willing to stretch to the limit to buy a starter shack”

“Starter shack,” love it. And ‘shack’ is an appropriate term for a lot of what has been bought at hideous prices the last several years.

Could the immigration crackdown be a factor in decreased demand?

How about China?

To the best of my knowledge EB5 visa are immune from any crackdown, real or presumed. Exactly the same when Switzerland finally capped permits: investors, their spouses and children (if minor) were exempted.

EB5 has long been favored by Mainland Chinese nationals: since 2011 the yearly percentage of EB5 visa obtained by them has skyrocketed to well over 80%.

While the number of EB5 is rather small compared to those of, say, H-1B visa, these are usually very wealthy people who can afford to put down the $500,000 or more investment in a TEA (Target Employment Area) to get their visa, plus all sundry fees.

2018 data are still not available, but it seems EB5 issuance was unaffected by economic and political turmoil, so we cannot really blame these very rich Chinese investors.

There has been a lot confusion about foreign buyers, with headlines such as “Chinese cash buyers may account for 20% of sales in XYZ” but the reality is we don’t really know: if a property in Denver is bought by a LLC registered in Boulder we should do some digging to find who’s really behind this LLC. Imagine doing that for every single real estate purchase in the US.

– Ask yourself: do have all those immigrants have hundreds/thousends of USDs/money “in their backpocket” ?

What about the drop in fertility rates in the US and elsewhere? There are only two ways to grow the economy, increase in population or increase in productivity.

http://time.com/5485023/census-us-population-growth-2018/

Get ready for a slowdown with inflation. No real estate problems in most parts of the country with the exception of the Bay Area.

The Bay Area has a special problem in that many of those startup companies operate in the red and only exist because of central bank monetary printing. Now that the printing has slowed, you will see heavy job losses while those companies fold because they just burn money.

Boston may also have a problem because of the biotech business … also full of firms that just burn money.

– Nonsense !!!!! Those startup companies don’t borrow from either the FED or the banks. They get their money from socalled “Venture Capitalists”. These are the persons that provide the start capital. After that those companies have to find other ways to borrow money. E.g. by issueing bonds.

The vcs work for firms that have what are known as principals. It is their money that the VC is paid to invest. The Principal himself/herself has a lot of assets, a lot of which are in the stock market. So when the stock market drops, their valuations drop too. In October 2008, the principals started withdrawing the lines of credit and a lot of start ups folded in a span of 3 days.

The fed’s QE is responsible for the stock market inflation, which in turn inflates the principals’ valuation. Now that QE is heading out, one would think the stock market will drop.

Also, why would one lend money to a startup and be a bond holder rather than be an owner by directly investing? Aren’t the returns higher, especially if the company gets bought out or does an ipo, by being an investor rather than get back the principal with a measly return? From what I’ve read, the vcs are all investing in each other’s companies into round F and Gs. So I suspect they’re not borrowing as much as bringing in newer investors.

Search for how Soft Bank is funding anybody who’s asking — there was a profile done on the founder and how he’s upending the startup market with sovereign money, which as you point out is now exactly fed money.

There is another component to monthly payments and that is interest rates. As rates go up typically real estate prices go down. Yet, if prices drop 30 percent and interest rates go way up, the monthly payment may be about the same. I got a great deal on my first home as it had lost 40 percent of it’s value, but I had to pay 12.5 percent interest.

Central-Florida resident here; 120 acres across the street from me are being developed. Over the last two years I’ve watched them clear the forest, lay out streets and sewage, and begin building homes.

At first, they were promoted as ‘in the low $200s’ but they have inflated. The next round of signs promoting them said, ‘beginning in the mid 200s’ then ‘from high-$200s’ to where they are right now, ‘in the low $300s’. Thing is, these are the exact same type of houses!

While that’s good for the builder (Toll Brothers), I’ve noticed a decline in the pace of construction. At first they were going up fairly quickly so that 5-6 homes were being roofed (easy to see) at any one time. At present, there’s 1 house ready to roof and looking out my window I see one other home going up. Slower, a significantly slower pace.

Meanwhile, reports are of new car sales declining, repossessions are rising, and while employment still looks OK, I’m thinking both the car and housing market are going TU once again. Or am I alone in noticing the return of television commercials touting 0% financing and ‘large’ manufacturer’s rebates and ’employee pricing’ on new cars?

Anyway, while our sales have been crackerjack the last few months, I’ve been uneasy and just last week informed the sales rep for the sole national magazine in which we advertise that we’re switching from a yearly contract to month-by-month. Why? It’s because I was hung out to dry beginning in mid-2007 with 1-year commitments to three magazines for full-page 4-color adverts. Those nearly sunk us!

Anyway, refraining from signing long-term advertising contracts is the first step (we manufacture hobby products, which are 100% discretionary spending). First step? Yes, basically, I am positioning us for hard times because if big ticket item sales go south, the whole US economy goes, which means us also.

Add in the turmoil with China and pulling in my horns a little bit seems the wiser course of action. Sad thing is, while I understand my Mr.Powell is raising rates, I didn’t see the need and feel this downturn is/has been manufactured by one single human being. I’ve been in business since 1992 and experienced downturns in 1993, 1998, 2003, 2007-2010, and a blip in 2015 but this time it won’t be pretty. Then again, it never is.

You didn’t see the need to raise rates?

Maybe you don’t see the need in the private economy, but the low rates are doing much damage to government and pension financing. At current rates, the US federal government will be running $2T annual deficits in the near future. Pensions and social security will be going going belly up.

O think you provided a good, concise description of how recessions begin in the real economy. One decision at a time until it becomes a deluge.

I do take exception to laying the issue of the markets at the feet of Powell though. While he leads the Fed, he is only one vote on the FOMC. And you could make the argument that their conduct is prudent, despite Trump’s whining.

I flip single family houses in Massachusetts. Statewide we are seeing median prices rising, inventory falling, months supply falling, and new listings falling. All of this tells me there is strong demand but we are following national trends too.

The Boston chart of the CaseShiller data confirms what you’re saying… On my list of “the most splendid housing bubbles in America,” Boston is one of only a few that eked out a new all-time high in the last data release. The CaseShiller index (which lags about three months) has recently turned south for a bunch of the others.

https://wolfstreet.com/2018/12/26/most-splendid-housing-bubbles-in-america-decline-seattle-san-francisco-bay-area-san-diego-denver-portland/

Short of climate change making California undesirable decades in the future, prices will never stay down long in California.

They will come down and then shoot back up again. Whether a particualr home can ride the wave depends on the particular neighborhood not going to shit.

But major cities and Cali seem to be stuck in a bubbly up and down housing market. At least unless we drastically alter the number of new homes being made. And the build cost.

Maybe a tech revolution in 3d printed homes will change the game one day.

As I’ve argued in my articles for years, Case-Shiller is useless for telling us what is really going on in the real world. Sales volume is much more important. For the best figures on actual price trends for the northeast, go to raveis.com.

The housing recovery has always been an illusion facilitated by the regulators and the FASB in 2009. Don’t believe me? Check out some of my in-depth articles at my website

My new article — out shortly on MarketWatch — will show “The Shocking Truth about Mortgage Deadbeats.” That should dispel the myth that the mortgage crisis ended years ago.

Great research, Keith. Your long term analysis of housing in the Northeastern quadrant of USA is refreshingly “hard-nosed” and granular. The Boston metropolitan area has kept the “illusion” from popping. We will see what the demographics of the next decade reveal.

I appreciate the kind words. My next two articles on MarketWatch will be really important in exploding the myths about “nothing to worry about.” There is plenty to be concerned about, but I am the only analyst willing to dig deep to find the ugly truth.

reading all this makes me feel smug being a long term renter. i wish i could say it was due to my brilliance but actually, i was never able to afford anything that i wanted to live in. my brother on the other hand bought. he’s made a couple million or so in paper profits but his taxes are more than my rent. i guess were both happy with our situations.

dumb question….need some advise with a bit of background ( I own land and want to build). In my area the prices per sq ft have gone from $125 to 170 in about a year or so. With all of the above detail from Wolf…. can I expect a normalization of prices to occur (decline). I am hopeful to leverage all of these builders as housing starts drop off. Building a 1600 sq ft house with basement. thanks

I have been watching the sales of new and used homes start to decline between $10k to 15k in the past six month. People are taking less in the $200k and up…. where smaller starter homes are still getting more than asking price (up to $165k).