Forced selling by loan funds in the once red-hot $1.3-trillion “leveraged loan” market.

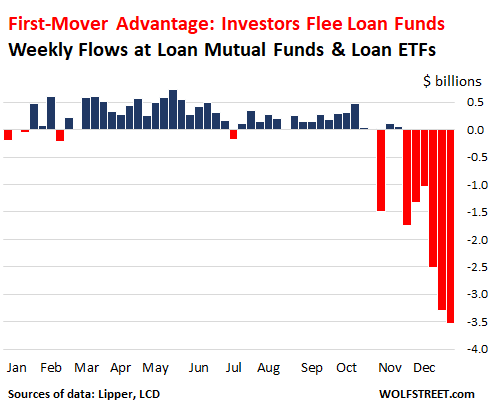

Part of the $1.3 trillion in “leveraged loans” — loans issued by junk-rated overleveraged companies — end up in loan mutual funds and loan ETFs. These funds saw another record outflow in the week ended December 26: $3.53 billion, according to Lipper. It was the sixth outflow in a row, another record. Over the past nine weeks, $14.8 billion had been yanked out, another record. These outflows are, as LCD, a unit of S&P Global Market Intelligence, put it, “punctuating a staggering turnaround for the asset class” that until October was red-hot:

Despite $10 billion of net inflows during 2018 through early October, the record outflows at the end of the year caused a net outflow for the entire year of $3.1 billion. What a sudden turnaround!

The net outflow of $3.53 billion during the final week of the year consisted of $2.9 billion that was yanked out of loan mutual funds and $626 million that was yanked out of loan ETFs.

In addition, during the week, prices of these loans dropped. Lipper reported that the balances at loan funds fell by another $746 million “due to market value.” The total amount in leveraged loans that loan funds now hold has dropped to $91 billion. So the $746 million drop due to “market value” during the week amounted to a price drop of 0.8%.

The rest of the $1.3 trillion in leveraged loans are held by institutional investors, hedge funds, pension funds, etc., or have been packaged into collateralized loan obligations (CLOs) that were sold to institutional investors globally.

It can take a long time to sell a leveraged loan. Each is a unique contract, and finding a buyer and agreeing on a price and completing the sale takes time. So loan funds hold considerable amounts of cash so that they can meet redemptions. But now, loan funds faced with this onslaught of redemptions have to dump loans in order to stay ahead of the redemptions and maintain a cash cushion. This forced selling by loan funds has caused prices to drop – which is further motivating investors to yank even more out of those loan funds.

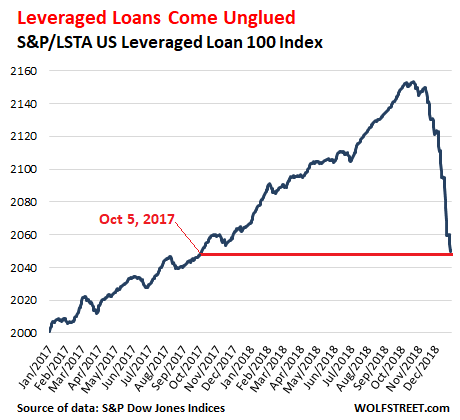

Since October 22, the S&P/LSTA US Leveraged Loan 100 Index, which tracks the prices of the largest leveraged loans, has dropped 4.8%. This price decline put the index back where it had been on October 5, 2017. But note, while there have been some defaults recently, the big wave of defaults that many expect in an environment where credit is tightening for risky corporate borrowers, hasn’t even started yet. These are still the good times:

Leveraged loans carry a floating interest rate, usually pegged to Libor. Libor has been rising in parallel with one-month and three-month US Treasury yields. And the interest that these loans pay has been rising too. Bonds that pay a fixed coupon rate lose value in a rising interest rate environment. But unlike bonds, leveraged loan generally protect investors from a price decline due to rising interest rates – which is why they were such a hot asset class over the past three years, with investors swarming all over them, and with companies issuing them in record amounts.

The risk of these floating rates is that struggling companies, faced with higher interest payments on existing loans, will be pushed into default sooner. That hasn’t happened yet in a large wave, but it’s on the horizon for the next few years.

The Fed has been warning about the risks of leveraged loans since 2014. Most recently, on October 24 – about the time the leveraged-loan sell-off started – and on December 2, in its first-ever Financial Stability Report. Perhaps investors have finally taken note.

Investors are now fleeing from open-end loan mutual funds because they know what the risks are: There is little liquidity in the leveraged-loan market even in good times, but investors can sell the mutual fund instantly. When these investors start yanking their money out of these funds in large numbers, they can create a run-on-the-fund. If the fund doesn’t have enough cash on hand to meet the redemptions and isn’t able to sell the loans fast enough into the illiquid market, the fund is then forced to sell loans for cents on the dollar to some distressed-credit hedge fund or PE firm waiting for this opportunity. And the net asset value of the mutual fund gets crushed.

Investors that grab the “first-mover advantage” in an illiquid market and are among the first out the door before they get caught in a run-on-the-fund come out unscathed. The late movers, or non-movers, in the worst-case scenario, can get caught up in the collapse of the fund. This “liquidity mismatch” makes open-end loan mutual funds riskier than the actual leveraged loans – and they’re risky enough — and investors are not getting paid for taking this risk.

“It now appears bike sharing is the stupidest business, but the smartest brains of China all tried to get in,” said Wu Shenghua, founder of one of the collapsed bike-share companies. “It really now seems ridiculous.” Read… China’s Startup Bubble Runs Aground

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I feel bad for the millions of people who will have their retirements adversely affected by this. Pension funds as a whole have been extremely negligent in their duty to their clients to safely invest their money.

Hi, Jdog I’m a little puzzled by what you are trying to say while its true that pension funds have invested in these financial products they also hold enormous amounts of “safer” investments such as blue-chip company stock and of course lots of bonds. I put safer in quotes because in this everything bubble all asset classes are inflated and pension funds’ fund managers were buying anything that promised any yield. As for who to blame well I suppose its the powers at be, that kept interest rates at effectively negative rates.

In my opinion, “Junk” rated investments are not suitable for peoples hard earnded, and much needed pension money. It is irresponsible for a pension fund manager to gamble with the futures of the people investing in his fund. Chasing yield by ignoring risk is irresponsible, but to do it for the small yields they have been getting is plain stupid.

Unfortunatly, being as most fund managers are not held to the standards of being fuduciaries, the investments they choose are not always in the best interest of their clients. The only standard they must meet is that they can be defended as appropriate given the situation.

I would hazard a guess that the obscenely high compensation of all these “money managers” has more than a bit to do with their chase for yield; even when inappropriate. They can always rationalize that they disclosed the risk.

Your gripe is valid but goes to the larger issue of how financialized the economy has become and all the negatives associated with such for the “little guy”.

What kind of pension funds will put money in “lower” than investment grade bonds? They are mostly in Treasuries, MBS, Agency and blue chip company bonds.

On average, pension funds are holding about 60% stocks, 30% bonds, and 10% alternatives (PE, hedge funds. VC). And of the bonds, much (perhaps most) would not have bee considered appropriate for pensions 30 years ago.

These are not safe investments. But in order to make the 7.5% annually they require to avoid falling further behind, they must reach for yield. When it blows up, they will just say it was unforseeable.

Jdog

Hindsight is a wonderful thing, and your current-date statements are undoubtedly accurate.

However, 12 months ago, investing in what is now crap looked like the smart move (hi-yield and all that).

Back then, everybody on the planet knew this manure pile was going to implode; the only question was “exactly when & who do the “smart guys” dump this stuff on?”.

Interestingly enough, today’s technology vastly accelerates the speed of communication, eliminating the time available to hunt down the “greater fool”. For once, the “greater fool” doesn’t get 100% buried in the manure pile.

Not negligent, only move with the stream. As financial advisors would say, you can behave like a bank, and bet that the system will save your behind. Moral hazard has been shot multiple times.

Index Funds/ETF’s

Wells Fargo pension funds managing over a half trillion dollars, sold its indexing operation in 1996 to Barclays Bank of London, which operated under the name of Barclays Global Investors. (BGI)

Blackrock acquired BGI in 2009 which included both its institutional funds and its iShares ETF, along with its management.

Investors globally directed about $2 trillion of new money in 2017 into the investment industry, which pushed worldwide assets under management to a record $88.5 trillion.

Blackrock and Vanguard the worlds two largest managers both attracted record inflows, helped by the major shift of investors into low cost index tracking funds. A major portion of those “institutional investors” are pensions.

Did people suddenly figure out that these are “riskier” now? Why are they wanting a higher risk premium now when the longer term Treasuries have dropped considerably? Why the change of temperament? Why are the ICE BofAML BBB and CCC indexes spiking? I hate to be the person to ask – aren’t these the industries the country needs the most now since they actually employ a lot of people? Where exactly are we gonna invest?

Yes, this is exactly what happens. Investors suddenly see the risks that they were blind to before, or were too greedy to see and didn’t want to see. ZIRP and QE did a real job on the brains of investors. Now that drug is fading and investors are coming out from under it. The technical term for this process is that “risk is being repriced.” We’re now seeing this process almost everywhere.

If this “repricing of risk” happens gradually, it’s a good thing because it makes the financial system less vulnerable — something the Fed is trying to accomplish. If it happens gradually, it means that investors will keep losing money, but gradually, and it doesn’t hurt that much. But if it happens all at once, it can get very nasty.

I appreciate this explanation. I was wondering the same thing.

True price discovery is inevitable. Maybe some assets will reprice quickly and others will be gradual but it will happen and it’s happening now.

Throughout the modern era (post WWII) this appears to happen about every 10-20 years. I’m 72; I’ve seen this movie 4-5 times.

Ten-twenty years is just enough time for a new generation to jump in and play ball. Cryptos are the current period’s point of the spear, but a lot of people who have seen it all before and should know better get desperate, and are sucked along.

I had a contrary view of 2008, they should have raised rates to accurately price risk. I think this Fed may agree with that.

Good write up. 2 other important points that can be added 1) LIBOR has stopped its incessant rise and actually has come down a few bps in past several days. That rising rate protection may cease, now you just own the credit risk. 2) Most of these loans are priced by model, when an actual trade goes off and they get marked to market there tend to be gaps lower in a formerly modeled price. When you are a leveraged entity that owns these (CEF, BDC, & the massive CLOs) the risk of margin calls grow with each repricing. It’s already ugly but can get really ugly quickly. Vulture buyers are way below current market prices so very few smart money buyers right now.

1 month LIBOR is up 15% since October,

There are numerous ominous signs. It may be helpful if you would post a list. I won’t have the opportunity.

Ambrose

You are assuming LIBOR is not being manipulated, right?

Not being snarky, just asking a legitimate question.

You mean compared to a committee of political bureaucrats who meet four times a year. Even they want LIBOR.

When reading throughout the day, it is rare that I get even one sentence that helps me, but this article did. We don’t own any floating-rate bonds and sold our floating-rate preferreds just before the 2018 mess, but still interesting reading. Thanks. Clear and concise.

BKLN is up double digits relative to the S&P since Oct. I think you make the point Wolf that floating rate interest on these loans offers more protection than fixed rate coupons. If rates rise and the economy is strong the factors balance. In the event of a credit “crisis” these loan funds are toast, right now the markets aren’t seeing that.

BKLN got crushed starting early October and the economy is slowing so nothing will balance. The market is seeing this clearly now

Ambrose Bierce,

“BKLN is up double digits relative to the S&P since Oct.”

OK, yes, that is one way of looking at it, comparing these loan funds to the riskiest assets out there, namely stocks (that got hammered).

I’m not sure how fair this comparison is, though.

A stock can go to zero, no problem. But a leveraged loan is secured by collateral. In case of bankruptcy or other debt restructuring, there is some recovery. This recovery could be 40% to 60% of the face value of the loan — while the company’s shares would go to zero.

At the same time, the upside of a loan is much more limited. A stock can double or triple within a year. Loans can only tick up a few percentage points a year, under the best-case scenario. Their main draw is that they pay a higher yield than Treasury securities or dividends.

Plus, if the company survives over the term of the loan, investors get paid face value. This is also very different from stocks. With stocks, you get paid when you sell, and the market decides how much that is.

Leveraged loans are legit products for long-term investors who understand the risks and read and understand the loan covenant. But loan mutual funds are riskier than the underlying loans because of the risk of a devastating run-on-the-fund. And this risk is never priced into a mutual fund, and mutual fund investors never get paid for this risk. They’re just saddled with this risk without compensation.

At any rate, BKLN is down 6% since October. So yes, this is less than the S&P 500 is down. But these funds should really not be down at all unless some of its loans approach and go into default. And that hasn’t really happened yet.

It’s a good thing the US now has the Greatest Economy Ever*, otherwise investors would be in even worse trouble.

*According to the World’s Foremost Authority (a title held previously by Dr. Irwin Corey).

/s

Name a better economy in a country with a population of more than 20 million.

Note: I’m not claiming the US economy is in robust health; I’m just saying name a better economy.

That’s Professor Irwin Corey.

Still laugh when I think of his wacky hair and double-talk explanations.

A regular on The Merv Griffin Show.

I read somewhere recently that there are only two large us corporations with AAA rated bonds. Msft and jnj. Shocking.

“The risk of these floating rates is that struggling companies, faced with higher interest payments on existing loans, will be pushed into default sooner. That hasn’t happened yet in a large wave, but it’s on the horizon for the next few years.”

And yet, how easily a wave turns into a tsunami. And how easily any company can become a struggling one.

The US Federal Reserve can raise interest rates in the attempt to deflate the omnibubble without bursting it, and it can unwind its own assets, but it cannot unwind the vast overhang of personal, corporate, and government debt. Very simply, there is no way to do it. Careful examination of the data and a little thought should be enough to persuade anybody that this is true. Huis clos: there is no way out. There never was, short of radical economic reorganization after bouncing off the bottom.

Unfortunately, simply maintaining the US economy in its present state requires that debt must increase and must be dirt-cheap, a condition which is absolutely unsustainable, making collapse and catastrophe inevitable. The Fed knows all this and its member banks are just hoping they will be able to exploit it.

Chaos creates opportunity. The coming crisis can be expected to be so severe that it will enable resort to drastic action, in particular, drastic political action. Properly timed, a gratuitous government shutdown helps the process along.

These are ‘the good old days’. Enjoy them which you can – if you can – because they won’t last much longer, and they aren’t coming back.

Walter –

Will history repeat? Or just rhyme?

16 of the last 19 times the Fed started raising rates, the stock markets have tanked. Thats 84% of the time.

@walter

“but it cannot unwind the vast overhang of personal, corporate, and government debt. Very simply, there is no way to do it. ”

Higher rates will force all of those sectors to start deleveraging (except perhaps the govt), but the problem is as you’ve stated. Global economies are so buried in debt, that to deleverage to any significant degree would be painful beyond belief. The equity markets would tumble and the POTUS would call for a national emergency. He’s practically calling for one now,and the process has just started……We are experiencing a correction but if one reads the news one would think the sky is falling.

If FFR rates were completely normalized to reflect true market price discovery, we would be looking at a 5% FFR. This is obviously unsustainable. At 5% FFR those sectors would be forced to deleverage but it would be at the expense of the economy (massive deflation ). Our POTUS deems 2.50% FFR as completely “insane”. This is how very distorted things have become. And it’s all being done to perpetuate financial asset bubbles, namely the equity asset bubble. We’ve sacrificed everything for a bunch of paper gains that can never be fully realized……

Excellent. You get it.

I wonder what will happen to asset prices if the market figures out that those gains are unrealisable… :-)

The moral hazard of pension funds investing in junk rated investments is a double edge sword. On one hand they are being neglegent with their investors money, and on the other they are financing the means of the next colapse. By pouring mass quantities of liquidity into sub prime debt they are insuring a much larger implosion when the easy almost free money is cut off. Corporate America is obsessed with short term profits at the expense of long term growth and health.

Think of stuff like this the next time you might think state funded pensions are evil. The number of scams I have seen in private funded pensions are more than enough for a few books. And no, the scams and or crashes of pensions are nor limited to third world countries.

Our great great great great grandparents had it right, work until you drop dead. Granted they did that so their children would have a better future. Post Gen Xs are gonna have and are having a worse future. Worse jobs, worse pays, and losing their jobs to machines or AI way faster that it has happened ever before.

On that bright note, happy new year!