PE firms are all over this, but investors are still chasing yield.

Since the Federal Reserve started warning about the risks of “leveraged loans” in 2014, the amount of US leveraged loans outstanding has surged with delicious irony from $700 billion to $1.3 trillion. These things are hot. And now the Fed is even more worried.

The latest warning came from Todd Vermilyea, who leads the Risk, Surveillance, and Data sections at the Fed Board of Governors’ Division of Banking Supervision and Regulation. His responsibilities include, as he says, the Shared National Credit program, “a key interagency program that reviews and assesses risk in the largest and most complex credits shared by multiple financial institutions.”

Leveraged loans are issued by highly leveraged companies with below-investment grade credit ratings (“junk”) to fund primarily:

- Leveraged buyouts (LBOs) where a private-equity firm buys a company that then has to borrow the money to fund its own acquisition.

- Special dividends by the acquired company back to its PE firm owners. The euphemism for this form of asset stripping is “recapitalization.”

- Refinancing existing debt to give the company a leg up with creditors.

Regulators consider leveraged loans too risky for banks to keep on their balance sheet, so banks rearrange them, structure them, collect hefty fees, and sell them to loan mutual funds, pension funds, and other institutional investors, domestic or foreign.

Investors have the hots for leveraged loans because they pay a higher yield, and because the yield is based on a floating rate that rises as interest rates rise. But this is also one of the reasons these loans are even riskier in a rising-interest-rate environment.

In his remarks at the Loan Syndications and Trading Association Conference in New York, Vermilyea warned that “there may be material loosening of terms and weaknesses in risk management of the leveraged loan market,” and that “some institutions could be taking on risk without the appropriate mitigating controls.”

Then he went into the specifics of the surge in risks and abuses that bank supervisors are finding:

“Cov-lite” leveraged loans

“Covenant-lite” refers to loans that do not contain financial performance safeguards for the lender, such as specific commitments to maintain financial ratios related to debt service. These types of loans used to be reserved for the highest quality borrowers. Today, “cov-lite” structures are widespread.

How cov-lite loans would perform in a downturn is not well understood because data are not available.

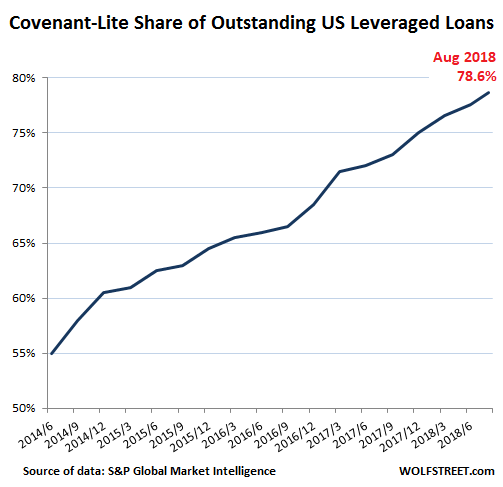

The chart below shows how cov-lite loans have taken over leveraged lending in recent years. Their share surged from an already high 55% of outstanding leveraged loans in 2014 to 78.6% at the end of August.

In terms of dollars, cov-lite leveraged loans outstanding ballooned from $385 billion in 2014 (55% of $700 billion) to $1.02 trillion (78.6% of $1.3 trillion). So, suddenly, there are over $1 trillion in “cov-lite” leveraged loans, and no one knows how they will perform during a downturn.

“Incremental Facilities”

This is the ability of borrowers to add further debt onto an existing loan to the disadvantage of existing creditors, and without their consent. Vermilyea:

Similarly, incremental facilities (IFs), which allow additional borrowing that is pari passu, or of equal seniority, with their existing bank loan, often without the consent of the lender, have grown in the marketplace and are now both more widespread and with looser restrictions than in the past. While IFs can provide an economic benefit to borrowers, IFs rarely limit the use of IF-provided proceeds and can be used for non-earnings purposes.

In other words, PE-firm owned companies can use “incremental facilities” to borrow even more, at equal seniority in the capital structure to the existing loan, and use these funds not to invest in something productive that can help pay off the loan, but for “non-earnings purposes,” such as a special dividend back to the PE firm, which adds risk for existing lenders.

“EBITDA add-backs”

“EBITDA (earnings before interest, tax, depreciation and amortization) is a well-defined measure of cash flow that is used to show how well a company is able to deal with its debts. “EBITDA add-backs” inflate that measure by adding back expenses and cost savings. And this “could inflate the projected capacity of the borrowers to repay their loans.”

“Collateral Stripping”

This is a special strategy that PE firms use to strip assets away from the first-lien creditors who thought they had rights to those assets as collateral. This operation has been successfully implemented by the PE firms behind J. Crew, PetSmart, and Neiman Marcus. When these companies go into default, first-lien holders end up holding the bag because their collateral has been stripped out. Vermilyea:

Supervisors have noted transactions where borrowers were able to transfer secured collateral beyond the reach of their senior creditor banks that issued the original leveraged loans, a practice known as “collateral stripping.”

And Vermilyea concludes ever so gently that “the presence of these practices, especially without the appropriate controls, may lead to safety and soundness concerns.”

But in these crazy times, after 10 years of interest-rate repression by the Fed, investors don’t really care, and they keep buying these leveraged-loan products despite years of warnings from the Fed.

So the next question is: Will this scheduled bloodbath in risky corporate debt, such as leveraged loans, deter the Fed on its rate-hike path? Read… THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Will this scheduled bloodbath in risky corporate debt, such as leveraged loans, deter the Fed on its rate-hike path?”

Looks like the Fed needs BALLS if it wants to make sure that the market listen. That is something sorely lacking since end of QE1. So you can expect “Vermilyea to conclude ever so gently” and “the Fed to raise rates ever so gradually”.

Heard of tail wagging the dog?

Anything to keep construction workers working. What would YOU do with them otherwise????

The “financial Salami” is getting sliced thinner and thinner and pretty soon…..”Poof!” it’s all GONE!!!!

PPPs should made illegal. They slowly destroy taxpayers

Meanwhile the administration keeps chipping away at Dodd-Frank and the Volcker Rule ‘cos you know regulations are BAAAAD.

https://www.bloomberg.com/news/articles/2017-10-12/frothy-leveraged-loans-may-get-whipped-up-by-regulatory-rollback

This is the role of the Congress and The regulatory relief recently passed had many Dem Senator voting yes/for and many neck deep in negotiating it. There was unanimous support for doing something because it was bad.

Federal Register: Over 83,500 Pages in 2010

Gary North

Printer-Friendly Format

March 15, 2012

https://www.garynorth.com/public/9227.cfm

there is picture of it 3 columns thick.

where good job for millions of layers.

who can afford that layers big corporations and rich.

Market regulators are still asleep at the switch, enabling a bottomless credit issuance that will further destroy any remaining confidence in the dollar. There will be plenty of dollars, but they won’t buy much.

Meanwhile the Fed continues on it’s merry way, oblivious to the fact that this course of action it has decided upon, will come to an ignominious end.

The only 100% predictable outcome to any given strategy, is that when implemented, things will not go 100% according to plan.

The lenders (investors, funds) are just as responsible as the borrowers and regulators for this situation. The banks and borrowers wouldn’t be in the game if they didn’t have willing customers. But the regulators do keep these kinds of loans out of banks and normal investment-grade bond funds, so investors have to make an effort to put money into them.

Without the covenants, these loans are less like home loans and more like unsecured personal credit card loans. The high rates are needed to make the loans attractive to people willing to bet that taking the spread will cover them against losses from defaults etc.

Now, if it were shown that fraud was taking place (as it did rampantly in Subprime and Alt-A mortgage lending in 2005-2008), that would be a different story. Wolf’s news about collateral stripping and incremental facilities sounds almost like legalized fraud, if the lenders didn’t realize the implications of what they had signed off on.

I’d love to see Wolf (or others) identify more specifically who is at risk from these toxic securities, both the borrowers and the lenders. Which specific funds are holding the bonds, and who holds the funds? Which specific issuers are most highly indebted and most vulnerable to the Fed’s rate squeeze? Right now “Leveraged Loans” is sort of abstract; having some poster children would make this a lot more tangible to people.

IMO the banks’ balance sheets are in much better shape this time through. A big chunk of these loans are being underwritten and held by the large unregulated pools of capital (look to the larger BDC names) that have come in without a glance from any regulators. They can offer terms that banks can’t (or couldn’t until recently) without any scrutiny, so they have taken a lot of market share in the lev fin space.

The healthiest outcome is to have some of these CLOs and BDCs crumble under their own weight; you’ll get some sob story from pensions and mutual funds but caveat emptor. The fact that there are ETFs for mom and pop investors to put money into leveraged loans (without covenants) should be the first warning sign. But a repeat of significant depositor money being at risk probably won’t happen.

Comes down to credit quality; once it starts sneezing, it will deteriorate fast and these CLOs will have to start rerouting cash flows. Then the bag-holders will be uncovered.

Wisdom Seeker ,

To get some of the candidates for who is at risk, google: loan mutual fund … or … loan etf

You can also check what pension funds hold in their portfolio.

Banks are also at risk if they retain portions of those loans or are caught with them before they can off-load them during a downturn, which is what happened during the Financial Crisis.

There will be runs on open-end loan funds, and since the underlying loans are illiquid (takes days or even weeks to sell one), while redemptions must be met on the spot, some of these funds will collapse.

Thanks. Did some legwork. There’s basically 4 major ETFs: BKLN, SRLN, FTSL and SNLN, which total about 12-15 $B in assets. There are maybe 10 closed-end funds in the Morningstar database that fall into this group; total assets are maybe a few $B more. This is clearly not where most of the bagholders will be. Also, interestingly the holdings for the ETFs contain a large “cash component”, 30-50%, presumably to cope with that liquidity issue.

There are far more players in the mutual fund space. Morningstar has a listing:

http://news.morningstar.com/fund-category-returns/bank-loan/$FOCA$BL.aspx

Drilling down into the holdings for a few of these shows a lot of companies on the borrowing end. But I can’t find a summary of the total asset value for these funds.

BTW, calling these things “Bank Loan” funds is hopelessly misleading. If the bank sells the loan to the fund then it’s a Fund Loan, no longer a bank loan! In effect the fund is acting as a bank (lending money) with the bank merely being an intermediary for a fee, right? Unless the bank has skin in the game, the loan isn’t really a bank loan.

Wisdom Seeker,

Yes, and thanks for the legwork. I’m a lot less worried about closed-end funds, in terms of the liquidity issues (that includes bond funds, btw). Closed-end funds are much safer because there is little risk of a run on the fund. You’re still exposed to the risks of the loans, but that’s a risk you’re getting paid to take via the yield, and it’s not catastrophic. But no one ever is getting paid for the risk of a run-on-the-fund (open-end fund). That’s a risk people take unknowingly.

Banks also sell mutual funds to their customers, so would these be in-house or off-loaded? I believe, this is a grey area, where the bank might be forced to preserve it’s reputation or risk a run on the bank.

I suppose that since asset values have been inflated they now have more collateral to borrow against…

“Now, if it were shown that fraud was taking place (as it did rampantly in Subprime and Alt-A mortgage lending in 2005-2008), that would be a different story. Wolf’s news about collateral stripping and incremental facilities sounds almost like legalized fraud”

PE asset stripping *is* a form of legalized fraud, but it’s made a lot of the looters immensely rich, and said looters have been very effective at putting some small portion of their ill-gotten gains to use by way of bribing lawmakers to let them continue and expand the racket.

“I’d love to see Wolf (or others) identify more specifically who is at risk from these toxic securities”

Taking a broader view than “who holds the securities” — Given the manifest toxicity to the real economy and the working class folks of this country of PE asset stripping, *all* of society (except for the tiny sliver of it profiting disproportionately from said racket) is at risk from the profound economic harms caused by this crap, just as all of society was gravely harmed by the past 40 years of neoliberal offshoring of jobs that allowed a person to make a decent living by producing things of real economic value.

There are about 4000 pension funds in the U.S:

https://ballotpedia.org/Public_pensions_in_the_United_States

How many hundreds of thousands of private 401K accounts, etc., etc.?

Substantially all of these continue to chase yields and all are at risk

The Triumph of Conservatism by Gabriel Kook

economic historian Gabriel Kolko show that the leaders of big business and not the reformers sought to regulate business to counteract the effects of competition and economic decentralization and to achieve concentration and monopoly.

the role of such business leaders and the corporations in the furthering of their interests through the power of the state.

https://www.amazon.com/Triumph-Conservatism-Reinterpretation-American-1900-1916/dp/0029166500

big business doing its best to be in bed with big government in order to exclude or squeeze out the smaller competitors

The Fed/Treasury is an “incremental” facility

“Since the Federal Reserve started warning about the risks of “leveraged loans” in 2014, the amount of US leveraged loans outstanding has surged with delicious irony from $700 billion to $1.3 trillion. These things are hot. And now the Fed is even more worried.”

Well maybe the Fed could actually do something about that…like blowing the roof off the market by raising the FF rate a whole…drum role…0.25%! And maybe excelerate QE unwind another whole $10/month!

That’ll show’m who’s boss.

In truth, why should anybody believe the Fed about anything? At some point, their tattered credibility will be totally non-existent.

When their “creation” of any “economy” is such a fraud as this is- they should be eliminated as a tool of only the very rich. Private banking.

(The problem is – we’re a totalitarian oligarchy. The jack-boot of the Fed exists for a reason).

Jeeeez; some people’s kids…

Wolf – I see bad things in the future for investors who buy these leveraged loans. One point you made in this extremely informative post stood out to me:

“This is a special strategy that PE firms use to strip assets away from the first-lien creditors who thought they had rights to those assets as collateral.”

These ‘creative’ PE firms, I think, may have found a way to strip assets while also becoming first-lien creditors. If asset stripping is performed using sale leasebacks, where a PE firm buys discounted real estate from distressed companies because they agree to lease or rent it back for a similar discount, then the PE firm can strip assets at discounted prices while also becoming a major unsecured creditor due to the future lease payments it is owed. They strip valuable assets at deeply discounted prices before bankruptcy, then are owed an additional share of asset liquidations as an unsecured creditor after bankruptcy.

A+ for superior analysis. Great comment.

The old saying goes: “don’t hate the player hate the game” what we’re seeing is the results of decades of players changing the rules of the game. As another old saying goes “what goes up must come down.” Preferably we’ll see these leveraged loan products reduce in a proportion of the economy and as interest rates begin to rise slowly deflate as the real economy shines through. I guess more remains to be seen.

You CAN hate the players, when they’re the ones who pushed for the laws to be changed to ruin the game for everyone else.

Wisdom seeking

That’s what I was getting at I suppose I wasn’t clear enough?

To imagine how worse cov lite is:

Moody said in July its “Loan Covenant Quality Indicator, a measure of the level of protections for investors embedded in junk-rated leveraged loans issued in the U.S. and Canada, ended the second quarter at 4.09, up from 4.05 at the end of the first quarter. The LCQI rates quality on a five-point scale where 1.0 is strongest and 5.0 is weakest. ”

and

“Covenant protections are “dramatically weaker” today than before the last recession. ”

nothing to worry about. leave all the problems to fed.

“In terms of dollars, cov-lite leveraged loans outstanding ballooned from $385 billion in 2014 (55% of $700 billion) to $1.02 trillion (78.6% of $1.3 trillion). So, suddenly, there are over $1 trillion in “cov-lite” leveraged loans, and no one knows how they will perform during a downturn.”

The FED has been dragging their feet for 5 years. 25 bps rate hikes. QT slower than molasses. The problem is that everyone ends up paying the price for these bad loans in the form of subsequent cyclical rate suppression, after everything crashes.

Why don’t they raise rates rapidly enough to change actual debt and leverage behavior? Clean out the garbage before it becomes an even a greater menace. This includes the zombie corporations.

Oh wait, there’s that equity bubble thingy that they are concerned about…….

Since M. Milken there is big money in this kind of “garbage”! And, always some schmucks breathlessly waiting to buy.

Does Fed see a systemic risk due to this? If not, things should be left alone.

Companies go private to avoid the extra scrutiny. Isn’t it the responsibility of individual investor to know the risks?

The problem is interest rate whores (stupid people, pension funds, people playing with other people’s money) will buy the bonds and some goofy bank from Arkansas will make condo construction loans to anybody in Miami beach.

re individual investors knowing the risk, yea, that’s how it’s supposed to work, but as I frequently point out, 95%+ of “investors” can’t read a financial statement. They buy the risky stuff because Uncle Ralph, their broker or some drunk at a bar told them about this “great deal” that nobody knows about yet…

I’m not kidding.

Correct. But exactly whose responsibility would that be to stop investors from taking blind risks?

I see so many cities around the country mismanaging their pension funds (example: https://www.seattletimes.com/seattle-news/seattles-retirement-fund-was-mismanaged-now-taxpayers-are-paying-the-price/).

Whoever’s in charge of fixing stupid, may perhaps start there.

There are people who have taken out mortgages to purchase crypto currencies. I really doubt anyone can fix all stupidity.

I don’t think many pension beneficiaries know about these risks, and when the loans blow up, I doubt the board members and fund managers who made the bad disicions will lose any money.

Exactly like folks taking zero down mortgages for large homes and blaming the banks, the Fed, their neighbor’s cat.

Right now the dividend chasers are pursuing the same Arkansas bank with questionable loans in Miami beach and other debt-laden companies that keep buying back their stocks.

We’re now at the point where the Ouroboros begins to eat its own tail.

Nobody who matters was prosecuted for causing the GFC. So what’s the incentive to behave this time? There is none.

The only difference now is that most of the sheep were slaughtered and eaten last time, with zero support given to growing the herd back. Now the wolves must start eating each other.

I’d celebrate but asset-strippers and their prey (bankers and institutional investors) are all known for their scorched-earth tactics. The rest of us are reduced to crossing our fingers and hoping we’re not in the path of any flame throwers.

How much is the banking industry involved with this?

These loans are going to go nuclear all at once!

The problem is that becuase there are no covenants if issues start popping up with the collateral the lenders are pretty much in the dark. Then the bonds default all of a sudden in a waterfall fashion.

In “normal” loans recourse actions get triggered by broken covenants. Here there are no covenants. Oops.

I lay the biggest fault for this at the Fed… by forcing investors waay up in the interest rate risk curve.

The Fed & its collateral activities definitely set up the environment.

However, if you’re blaming the Fed for self destructive investor activity from interest rate whores, and you’re expecting “regulators” to clean up your life, well your momma & daddy just didn’t get the point across about personal responsibility.

There’s an old saying: “If it looks too good to be true, it probably isn’t”. A huge number of investors are too stupid or greedy to give it a second thought…until it blows us and they want to blame the regulators or (fill in the blank).

Whoever said “there’s a sucker born every minute” knew whet he was talking about.

I don’t have the time to get into all of the dynamics of this debate, but you don’t hear much on this site about the leveraged loans creating liquidity for founders and optionholders, validating their efforts to get a new company off the ground, or even advance a developed middle market company into something more. Those are real dollars entering the economy in the hands of value creators. You also don’t hear much about the PE funds that flip their leveraged buyouts for many multiples of what they paid (including leverage) with blockbuster returns for those pension funds etc. Let’s not forget, the goal of PE fund managers is to get a return on invested capital. The leveraged recap is usually a secondary option if the liquidity event does not happen on schedule (and by the way, if a leveraged recap is on the table that means the business has been able to service its debt and generate excess value for equityholders). Banks are also not in the business of losing their shirts if it can be helped, and while they may not be able to treat these loans the same as other loans for accounting purposes, that does not mean there is not underwriting on these loans (there is actually a ton of underwriting that goes into these loans). It’s ironic that the Fed is now calling out the risks of leveraged loans while it’s the Fed’s interest rate policy that has allowed the principal balance of these loans to balloon.

Wolf, I love your coverage and don’t necessarily dispute the risks from these loans as you have identified them, but I do want to caution against the notion that “PE is evil” and similar sentiments. At the end of the day PE managers are first and foremost driving value for their investors and themselves, and in my experience they take their fiduciary obligations very seriously.

I should caveat that most of my impressions come from the middle market, where you see enterprise values anywhere from $50 million through $500 million. I will admit there are different dynamics in the bulge bracket, but the core principal of driving equityholder value remains the same.

TrojanMan

Point taken.

However, PE firms that knowing load up failed companies with loans that cannot reasonably be repaid & are sold to stupid individuals and greedy third parties (eg: pension funds managers) playing with other people’s money are, indeed, evil.

Institutions (banks & otherwise) who originate & sell this sewage to the public should be required to keep 30-40% of the debt on their balance sheet.

Yea, I can think of a couple ways that might be used to work around this, but any regulator (government employee, by definition) who works more that 3 hours a day should be able to think of a way to contain this.

The object isn’t to 100% stop stupid debt, it’s to stop stupid debt from EASILY being passed on.

“At the end of the day PE managers are first and foremost driving value for their investors and themselves, and in my experience they take their fiduciary obligations very seriously.”

Yes, they do. But risks of leveraged loans are not with the PE firms and their funds — the risks are with investors at the other end of the transaction.

I didn’t say PE firms are “evil.” I don’t think this term applies here. They do what investors and markets allow or encourage them to do. But I’m warning investors to not end up on the other side of a transaction with a PE firm without understanding all the details and risks.

I call it the Connecticut rule.

“Of course, I am going to try and screw you in this deal. If you let me screw you over, that’s your fault.”

A large portion of this country does not think or operate this way but I find it’s a good rule of thumb to apply when dealing with the finance industry.

I see a lot of pension funds failing and more Orange County type bankruptcies coming up

\\\

If my perception of leveraged loan principle is correct, you use this financial tool when you are short of cash, or have a bad credit, or as Wolf put it: “junk”. We just had a zero interest rate bonanza like 8 years in a row, and I don’t care how bad your credit was, you could have gotten cheap loans (given you are not already exposed to significantly more then you can carry) …who was using these tools? Did companies try to emulate the government and spend their way to the top? How bad did you need a loan that you took a leveraged loan, and how badly are you exposed to the new fed hikes?

\\\

Wolf, I tried to nominate you for the Nobel prize in economics, but then found out I am not important enough to do so.

\\\

LouisDeLaSmart,

If you succeed in nominating me, and if I succeed in winning the prize, I’ll split it with you :-]

Whenever I read PE firms and loan risks, my first thought is that someone’s pension fund is about to get looted.

It would be of interest to have readers / Wolf comment on where the opportunity lies with this canary in the coalmine.

Is it similar to ’06-’07 subprime but with mid-market businesses? Will there be opportunities to pull a Mnuchin-i.e. Indymac -> OneWest? and buy the debt of non asset-stripped companies on the cheap (debt to own) or simply pull a move similar to how john grey bought hundreds of thousands of foreclosed homes- but this oppt. Wont be homes, it will be operating companies.

Thoughts? PIK Toggle loans etc. from 2016 will get hammered as fed continues bumping rates, so the question becomes – how do u turn this danger and chaos into opportunity?

Great article on a very serious problem! These types of loans are most likely a disaster waiting to happen! Wolf, could you please explain why the lenders allow these “special dividends” back to the VC owners…it seems so crazy to me they are not strictly verboten as a condition of the loan. The lenders are just asking for it. What am I missing? Thank you.

Visions of Bain Capital and dancing horses come to mind.

If there’s a way, there’s a will to steal from society and the FED sits right in the middle, as an enabler.

The floating rate on leveraged loans is 125 basis points over LIBOR. That is to say, it insulates it from FED funds rate increases.

Leveraged loans are popular because they are syndicated, they aren’t regulated by the SEC (as junk bonds are) thus aren’t subject to legal financial disclosures like maintenance covenant contracts.

problems arise when there is a price decline as it can take time to sell these debt products- as opposed to junk bonds.