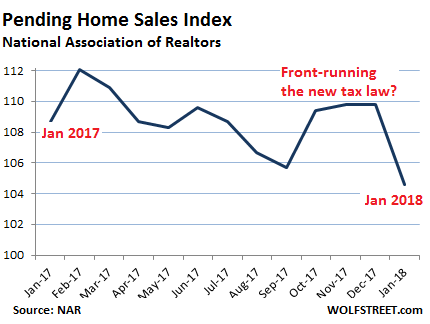

But it just started. Could it be the new tax law and sky-high home prices?

The National Association of Realtors is already blaming rising mortgage rates. Pending home sales – an indicator of future home sales, based on contract signings – in January fell 3.8% from a year ago, to their lowest level since December 2015, NAR reported.

All major regions got hit with year-over-year declines:

- Northeast : -12.1%

- Midwest: -4.1%

- South: -1.1

- West: -2.5

I can see that a harsh-winter scenario in January was in part responsible for the 12% plunge in pending home sales in the Northeast. But year-over-year declines were spread across the nation.

And the trend doesn’t look very hot, outside of the spurt late last year, just before the new tax law took effect, as this 13-month chart of the seasonally adjusted index shows:

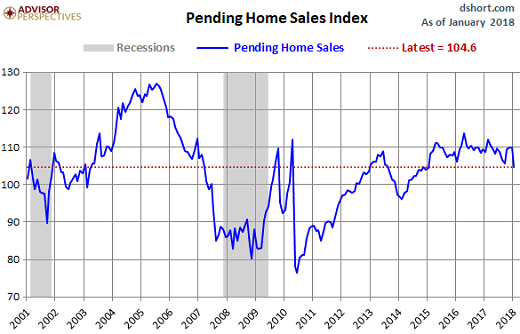

On the long-term chart (via Advisor Perspectives), the magnitude of the decline, while significant, pales compared to the plunges during the housing bust:

What gives? The report names two reasons – mortgage rates and low supply of affordable homes:

The economy is in great shape, most local job markets are very strong and incomes are slowly rising, but there’s little doubt last month’s retreat in contract signings occurred because of woefully low supply levels and the sudden increase in mortgage rates.

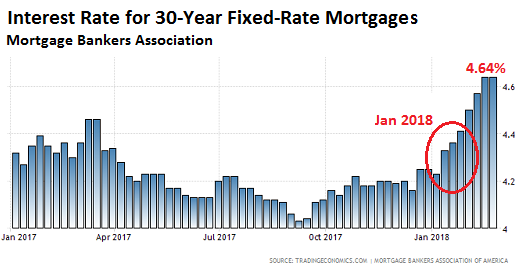

Mortgage rates have been rising sharply since December. According to the Mortgage Bankers Association, the average interest rate of a conforming 30-year fixed-rate mortgage jumped from around 4.0% in November and December to 4.4% by the end of January, and has continued on this trajectory. The MBA reported today that for the week ended February 23, it was 4.64% (via Trading Economics). So the January move in mortgage rates was just the first baby step, there being a good chance mortgage rates will be above 5% and perhaps close to 6% by year-end:

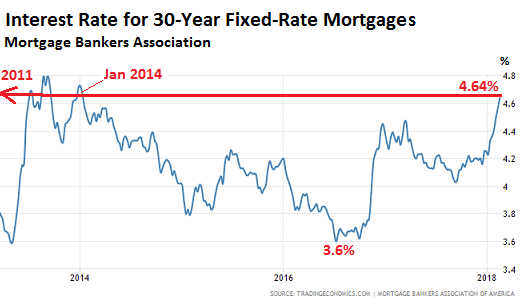

Despite being very low still, the average mortgage rate is now at the highest since the brief peak in 2013, and before then since April 2011:

But home prices have soared 46% since the beginning of 2012, according to the S&P CoreLogic Case-Shiller National Home Price Index:

These far higher home prices with the same mortgage rates as in 2011 produce much higher monthly mortgage payments – hence the affordability crisis for many households. Which the NAR also points out: “The lower end of the market continues to feel the brunt of these supply and affordability impediments.”

Inventory of homes listed for sale has been low and trending lower. According to the NAR report: “The number of available listings at the end of January was at an all-time low for the month and a startling 9.5% below a year ago.”

Why are homeowners not putting their homes on the market? Here are some reasons:

- In 2017, sellers “typically stayed in their home for 10 years before selling” – an all-time high, according to NAR. And “higher mortgage rates will likely discourage some homeowners from wanting a new home with a higher rate….”

- Homeowners who sell now and buy another home would lose some or all of the tax benefits they still enjoy with the old mortgage.

- The combination of higher rates on a new mortgage and the loss of tax benefits might lock homeowners into their current homes because they cannot afford the payments on a similar home at current prices, and thus cannot afford to sell.

- The new tax law also removes some or all of the tax benefits of homeownership for first-time buyers, as the near-doubling of the standard deduction puts renting and owning on the same tax level in most markets, and there’s one less reason to buy.

January was the first month when higher mortgage rates, the elimination of many of the tax benefits of homeownership, and soaring home prices came together in one package. If pending home sales are any indication, the confluence of these three factors might turn out to be more quickly disruptive than I’d figured just a few weeks ago.

But the proof is not in declining volume but in declining prices – and this is not happening yet. Instead we get a story of price spikes and some new flat spots. Read… Update on the Splendid Housing Bubbles in US Cities

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just local news:

I was walking yesterday in Everett, a commuting suburb of Seattle, and saw a local broker’s sign claiming their top salesman had sold 50 homes in just one month. I don’t think 2005/06 was that wild.

Harsh winter? I live in the Northeast and it has been 50-70 degrees for half of February. It’s the mildest February I have ever seen. I haven’t worn a jacket for a week. I love it how they blame the poor results on winter. These numbers are all adjusted for the fact that winter exists in the first place.

I believe those are January numbers, and living in Boston, I can tell you that January was brutally cold. It had the longest extended cold snap that I can recall.

The figures were for January, not February.

The personal savings rate is at an all-time low.

Real price inflation is well north of what is purported by the “official” rate.

Retail sales are substantially down, with the trend heading lower.

Consumer debt has surpassed its previous high set in 2008 and is now over $13 trillion, with revolving credit card debt soaring.

Real wages have been in a steady decline since 1999 .

Is it any wonder that existing and new home sales have collapsed?

This make believe “recovery” since 2008 is already long in the tooth and most people are finally able to see the fantasy.

Wolf –

What’s the matter?

Did you forget to vet this comment?

I am in San Diego and although inventory is low, the bigger problem is lack of affordable home. If you have a million dollar, you can buy a small 2K sq feet house with heavy mella-roos ( additional tax ) and HOA in a super small lot in a good neighborhood.

My guess is. one day buyers would wisen up and stop paying outrageous price for these over priced homes.

Well, that one day does not seem to be coming after almost 10 years just the last housing bust. As long as the prices bounce back up to new highs pretty quickly, it does not seem to affect most buyers. Today might be the top of the market and prices might fall 40% tomorrow. Does it really matter if you know that CBs and other powers that be will do anything and everything to pump up the prices again within just a short 5 years to new highs and beyond?

There is no way to know when the top is reached. Today might be it. It might be this summer or 2020 or 2025. Many people thought early 2016 was the top and look where we are. And before it was 2011 and 2013. Who know where this will run up to before it ultimately comes down.

If there is no way to know for sure when the top is reached, given CB policies, buying at any given time is as risky and sure as any other time. Who can say that $1 Million little house you are mentioning will not run up to $2.5 Million before it “crashes” down to only $1.8? Who gained or lost at that point?

It is hard to see who is the white bearded wise man and who is the village idiot in this market.

It is hard to see who is the white-bearded wise man and who is the village idiot in this market.”

Amen!

To your example, the home’s price doesn’t go up by itself. It requires a willing and able buyer (sometimes in a speculative market it’s a greater fool). In any case, wages would have to nearly double for that million dollar shack to sell for two million OR interest rates would have to decrease to maybe 2%. There aren’t many folks whose incomes qualify for 1.6 million dollar mortgages.

Don’t forget that all houses are owned by someone at any point in time and the over all prices in a market are set on the flow of new sales, not the stock of all existing homes.

So, as the flow sets the price for the stock, the owners of said stock see their assets appreciate – and this enables them to “trade” into a new house. This is probably a fat chunk of the activity going on right now, because, as you correctly observed, new entrants to this market are just plain priced out (unless they take on obscene mortgages).

The only reasonably (i.e. not borrowing an ridiculous amount of money) entrance opportunity for new participants in these markets given wages is to inherit a property or move some place that isn’t out of control.

Regards,

Cooter

Back when the housing market crashed last time and people were left scratching their heads, one the few things I read that made sense to me (while still struggling to understand all the other causes of the crash) was that housing prices cannot continue up forever if wages are not going up at a similar pace. Wages ultimately dictate affordability (but of course interest rates play the next big role) and at some point housing on a monthly cost basis cannot be more than what people can afford. That is the price ceiling. Interest rates are going up so monthly mortgage payments will increase as well. In areas where people are already stretching their budgets the most to afford housing I do believe it will be impossible not to see at least mild price declines in line with interest rate increases.

There with always be a greater fool , a sucker is born every minute.

Most assets today won’t make any sense if you considered how much income they generate. Especially real estate. Cap rates in California apartment building are sub 3%. 10 year treasury bond is almost yielding 3%.

Why would anyone invest money in apartment building for a meager 3% return and deal with a lot of hassles instead of buying the peace of mind risk free treasury bond?

The answer is simple. Because a sucker is born every minute and will show up and pay 30% more for your moldy real estate next year, you can be sure about it.

Just a few short years ago, I thought wages would have to double for that half a million dollar shack to sell at 1 million dollars. Guess what, that shack is selling at 2 million right now where I live, the Bay Area.

There is always someone who has more money than you and I do. Call it the techies making gazillions on their company stock, call it the Chinese investors or the not so smart folks who are taking on debt up to their eyeballs. It really does not matter. From where I look, there are still quite a few of them out there. Yes, the inventory has diminished even in the Bay Area. Sales are not as fast as it used to be. However, most houses sell within days of coming to market and almost always above asking price. This alone tells me that we are not at the top yet. Chances are, the prices will go up some more before they come down.

Do I think the current prices are ridiculous? Heaven, yes. Does my very strong opinion matter to the folks who buy those shacks at millions of dollars? Heaven, no!

Wages don’t need to double and interest rates do not need to go down for prices to keep going UP. There is a steady stream of asian buyers in my town overbidding for existing homes and paying cash. This could continue for a LONG time.

Amen Brother

Here in Palm Beach county in a middle income 55+ older-condo area, realtors are telling me inventory is “tight” if priced at the market. Condos sell rapidly and often for cash (below 100k). Demand appears to exceed supply at present.

However, recently even full cash buyers are becoming very picky about inspection issues as prices here have doubled from 2010-2012 levels.

Cash deals in the recent past always closed, now buyers want everything fixed or no closing. This change points to a possible shift to more of a “buyers” market.

Financed deals seem to fall out left and right with difficulty closing due to credit scores below 680, or debt to income ratios too high, or insufficient income level. Perhaps higher lending rates simply push more buyers out of the market.

Weirdly, in a so-called tight market closing a deal in 2018 seems fraught with problems and insecurities for sellers.

I agree but at some point in time affordability is what is gonna matter the most.

At this time, there is fear in the market for FOMO ( fear of missing out ).

But at some point in time, it is affordability which is going to dictate the housing prices.

If CBs are going to pump in the money in the market, making assets expensive, at the end of the day you need people to be able to afford the prices.

May not be true for stocks but definitely true for real estate.

I’ve a real estate broker for over 30 years – all markets are local, many are currently declining , it depends on where you are in the Country – Connecticut is a mess. With that said , don’t be so sure that QE will be a viable option in the next down turn – Gundluch said last week -” will the next recession be bond friendly ?” He sees massive issuance and refinancing of all debt , as potential risk – simple supply and demand will keep upward pressure on rates – don’t be mistaken there is a difference between monetary policy and money

Adam smith E, all you are saying is simply CB making house prices detach from fundamentals, and given that, there is NO price anchor, so it becomes gambling/lottery/speculation. Agreed. So let’s speculate and see what are the participants doing and out smart them.

1. Central bankers are selling assets.

2. W2 shelter buyers are close to max out, they will NOT sell unless they can not keep up payments. So they do NOT buy and they do NOT sell.

3. Rent seekers. The pool other people’s money, take control of houses and squeeze W2 earner’s income. Their funding channel is getting expensive due to rate rise. Price/Rent is high and Wolf keeps publishing data saying rent is dropping.

4. Price insensitive buyers. These guys do NOT care how much they pay as long as they can park their cash and get their cash out of it when they need. They can keep buying as long as they believe house is better than cash or because they can NOT put cash in banks due to money luandering. To turn them off, you need FinCen and you need to make the area undesirable like a tank in job market, homeless on the street, crime rate rise. Essentially this is toughest group to fold on high house prices. I think to let them sell, we need financial crisis. Slow down in economy or rates move will NOT discourage them.

still, comparing to previous years where W2 and rent seekers were strong, the buyer base is weak today. There is NO forced selling yet since people are NOTblosong jobs and rate rise is slow and there is NO financial crisis. But to convince me price will keep rising, we have to have stronger W2, higher rent and stability in financial markets.

What I see is lower rent, rising rates, increased volitility in financial markets. Trump will make W2 stronger, but that’s minor.

Most of your post is irrelevant to anywhere outside of a bubble city.

The vast majority of home prices have NOT recovered from previous highs.

As of March 2017, only 1/3 homes nationwide have recovered or surpassed previous highs (Trulia). As of December 2017, 1.4 million homeowners are still underwater (MarketWatch).

“Does it really matter if you know that CBs and other powers that be will do anything and everything to pump up the prices again within just a short 5 years to new highs and beyond?”

San Francisco peaked in March 2006. It took until November 2015 for prices to recover, and that was in one of the absolute fastest / probably bubbliest recoveries in the country. Most people haven’t been so lucky– and there’s a lot more to it than just CB activity.

“Just a few short years ago, I thought wages would have to double for that half a million dollar shack to sell at 1 million dollars. Guess what, that shack is selling at 2 million right now where I live, the Bay Area.”

According to the Fed, SF home prices are 16% above previous peak (March 2006). Meanwhile, per capita incomes are 37% higher.

People are extrapolating 2007 – present as what will happen forever more in the future. That markets will crash, and CBs will prop them up immediately, and markets will immediately recover to new highs. To me, that is an idiotic and massively myopic viewpoint with no basis. It’s “this time it’s different” syndrome taken to an extreme.

Not sure where you’re getting your numbers on SF. But here’s a dose of reality on SF.

The median home price in the City of San Francisco (this is not the 5-county Case-Shiller number) peaked in April 2008 at $828,000, a crazy bubble peak that was totally unsustainable, and everyone knew it at the time. It then plunged 26% to $610,000 by January 2012, and has since risen to $1.3 million.

In other words, the median price has soared by 57% from its prior totally crazy unsustainable peak.

According to the Census, median household income in SF was $73,100 in 2008. In June 2017, it was $90,529, an increase of 23%.

Housing was totally unaffordable at the crazy peak in 2007. And it has since gotten worse. This is called the “housing crisis” in SF. And for a good reason. No household with the median income of $90K can buy a median home for $1.3 million. They cannot even save up a 20% down payment (= $260,000). If they save 10% a year, it would take them 29 YEARS to get there, by which time the home price has galloped out of range again.

Jon, Totally agree, but I wonder how many sales in SD are offshore buyers looking for a place to stash their cash. SD is nice but it seems to be getting awfully crowded on the freeways as well. Still looking for 2008-09 to be revisited.

San Diego has very low inventory, insane prices and lots of buyer demand.

Last month I saw three tear down properties sell for cash over asking at prices that didn’t make any sense no matter how you looked at it.

It’s not about wising up, it’s about supply and demand. As interest rates/inflation creep upwards and mortgage affordability declines, house prices will fall. The bottom 20% of the market are up to their eyebrows in debt shouldn’t be buying houses anyways, much less flipping them. BTW, home flipping or speculation also greatly affects the supply of houses on the market. Higher interest rates should remedy that somewhat.

I wonder how much of San Diego is driven by attempts of foreigners to escape capital controls. Cash buyers? Also, don’t forget that NAR is one of the AML loopholes. This should be factored into any analysis.

Buyers never wisen up until they either lose their job or lose access to credit

Wolf I love your articles about housing. As a millennial with a great job who who is still priced out of housing I know this insanity will come to an end soon but it seems like nobody else highlights the magnitude or the underlying cause of the bubble. Keep up the great work

Usually, asset markets can’t sustain rising interest rates and rising asset prices simultaneously or falling interest rates and falling asset prices simultaneously. These metrics usually move in the inverse of each other. As interest rates rise, asset prices should fall.

Harsh winter Uhh Don’t think so More like high property taxes

Whiners are relentless. Bloody murder is coming when the punch bowl goes away. Oh, the horror.

People will go homeless unless rates stay at the lowest levels in history. Or, even more horrific, they won’t be able to upgrade from a hovel to a mansion, as they deserve. Values once considered sacred may even look a little high … just saying.

As everyone knows, adjusting building codes to reflect technical innovations, and resulting lower costs, are an insult to the working class and a massive safety hazard. People will sicken and/or die, horribly, if homes are built that are affordable but different from the ones your grandparents considered safe. I suspect California and the great Northwest are at the vanguard of this consumer safety movement. My neighborhood will not allow seat of the pants building like this, either. Neither will yours, I suspect.

All the Founding Fathers pooped in a hole in the ground. Only becomes a prob if you add 3 gallons of water each time.

you live, you learn… oh, wait.

Missing from this discussion is the actual hard costs of building a home and developing the land. When a $500,000 house sells for

$1 million a few years later, it is an excess of money sloshing around that is the reason. Costs have not gone up.

Foreigners, rent seekers, asset purchasers, borrowers hanging on by the skin of their eyelids, are all financed directly or indirectly by Central Bankers. That is the fundamental factor in the rise or fall of housing prices. Excess money/credit with its first cousin, low interest rates are the only thing that has pushed the price of a home into the atmosphere.

I can tell you from real people, the rising rates are pushing sellers/buyers to move quickly to lock in rates ASAP. Problem is everything is overpriced so they are sitting. My issue is our county is going berserk with the taxes and driving people out which might speed up any adjustments on the horizon.

Sales volume is down but the market is still pretty hot. I know bidding without visiting a house has a lot to with being comfortable with technology, but it may indicate a certain urgency.

https://www.bloomberg.com/news/articles/2018-02-26/housing-frenzy-sees-a-third-of-u-s-buyers-bidding-sight-unseen

The knee jerk reaction is “that’s insane”, but think about the process. The most ridiculous aspect of real estate (besides the $40 charged to overnight an envelope) is the inspection and appraisal AFTER the contract is signed. Just another way to extract cash from buyer/sellers. There are so many ways to get out of a deal because of this and the risk to buying sight unseen is probably low, especially if you have a lot of time on your hands.

Portland, Maine is out of control. New condos everywhere.

New Yorker’s are selling their houses at crazy prices and moving here to live the simple life and are replacing what they had for 1/2 the price-or less.

The Designer coffee/Microbrew/social media economy will crash eventually and the obnoxious New Yorkers will go back to where they came from with their tails between their legs

“The Designer coffee/Microbrew/social media economy“ Great desription, although I do like microbrews. This part of the economy bugs me, mainly because they have such hipsterish attitudes about their jobs. Yeah, we get it, you are sooo creative and witty with those thick rimmed glasses.

When the economy crashes again all these freelance and advertising jobs will be the first to vanish. First part of budget companies cut in recessions is advertising. Many won’t be able to afford their high rent apartments.

There seem to be redundancies going on in publishing for some time now: sure sign of a major advertising downturn, or that one is anticipated -these people are very quick to sack staff.

It was a VERY severe winter (up until Februay) in the Midwest, Northeast and Southeast. I would think this would have had some impact on sales.

February turned the opposite in most parts of the country and now record highs.

Look, the housing market is going to be affected by rising mortgage rates, no question. But I don’t think the sky is falling, just yet. Sellers will adjust if they want to sell. But again, I don’t think housing is going to collapse like 07/08. The underwriting has been much tougher.

Regarding apartment construction, slightly higher rates and lower house sales will only help keep that housing occupied. That said, I see an epic bubble on that front and as I’ve said before, it was well planned by Obama and Watt and the result will be when the time comes that the US government (you me, taxpayer, inflation payer) will become the proud owners. To be directed for use as subsidized and elderly housing. This will occur in the next big slide in the economy when those developers/owners will not be able to service their debts.

Lots of people won’t be selling because they are sitting on an appreciated property with a low interest rate loan, but the price of their homes will drop whether they sell or not. The market prices will be set by forced sellers – those that bought recently and got over their head, people getting divorces, investors that fear prices are dropping, etc.

A huge RE price drop could occur if only 5% of the homes turn over in the next few years.

I am not planning to sell anytime soon because of my large unrealized capital gain and the tax that I would owe if I sold it. In the meantime, my property taxes are low in comparison to what a new buyer would pay, thanks to California’s Proposition 13. I never expected it to last this long but nearly 40 years after it passed, it is still in effect.

If you are a California homeowner and approaching age 65, learn how to read your property tax bill and check for parcel taxes that you might be exempt from once you become age 65. Not all parcel taxes have a senior exemption and some only offer an exemption to seniors below a certain for income level (e.g. $40,000 income per year). Parcel tax exemptions are limited to owner occupants, not investors.

“I am not planning to sell anytime soon because of my large unrealized capital gain and the tax that I would owe if I sold it. In the meantime, my property taxes are low in comparison to what a new buyer would pay, thanks to California’s Proposition 13.” – THIS!

As a result of Prop. 13 in CA, a lot of us Boomers are not following the script and moving on. Wife and I live in a highly-desirable part of So. Cal. – great schools, access to freeways, the list goes on, and have no intention of going anywhere! We own the place outright and have more than enough income to live the life you see in pharmaceutical commercials. Back a dump-truck full of money up and say “it’s yours, just give us the keys” and we’d laugh. We’ll leave it to the kid, he can sell it when we kick the bucket or rent it or whatever. In the meantime, as the LG folks say – “Life’s Good!”

Under certain circumstances, it is possible for a child to acquire the family home in California and keep the parent’s property tax basis. Read here: http://articles.latimes.com/2005/sep/25/realestate/re-inheritside25

I wish I can be a fly on the wall on the following US casino: https://www.bloomberg.com/news/features/2018-02-15/a-chinese-company-has-conquered-a-piece-of-america

Should give a fair idea on Chinese money flowing to Murica. If it drops by half, watch out.

Watching the price of Home Depot. A stock that traded in a range of 40 to 50 dollars all during the last housing boom. Now it’s been up over 200 a share. Obviously free money for buy backs. But it essentially a commodity stock As it serves the housing and building industry. I learned back in 2005 that when the love is gone housing stocks drop and they dont bounce on the way down. Watching HD in the coming weeks as the canary. TOL Was a gap and crap on its report this week

Just watching to see what breaks first

Saw an article in SF Gate yesterday that said none of “those slick new condo’s and apartments that have been popping up all over SF are all priced under $3,000/month” Even “rich” folks in the Tech industry can’t afford that kind of rent and I suspect that sooner than later the market will catch on to this nonsense.

The thing about these supply numbers is that they’re limited to existing homes that homeowners are putting on the market. New units, when the developer puts them up for sale, are not listed in the MLS and are therefore not part of the “supply.” SF’s high-end (almost everything) new-built market is suffocating under unsold units, and no one knows how many there are.

If a border wall is built and immigrations severly limited; as the baby boomers die off…they will be bulldozing apartment houses and homes for lack of occupancy.

Baby boomers aren’t ready to “die off” just yet (just ask them). So you have to be patient. Many of us feel like we’ve got 3 decades left in us. And by then, the millennials — the largest generation ever — will be middle-aged or looking at retirement.

Not if the opioids have their say. It’s now supposedly a “crisis”. Imagine when the economy goes to hell.

Heck pensions, etc may not be an issue if pensioners are opioid-ed off. See what the private sector can do for you?

A true Public Private Partnership that works!!!

Absolutely correct. I have at least another 30 years to go….

Another variable to throw in the mix is the fact that upwards of 10,000 Baby Boomers retire EVERY day. It started in 2011 when the first of that 70+ million cohort turned 65, and will continue for another dozen or so years until the last of that cohort retires. This has huge consequences for a lot of aspects of the economy, but one in particular is housing, e.g. selling/downsizing. A significant proportion of those retirees are ill-equipped financially to survive the duration of their retirement. I predict a sizeable number of millennials & Gen Xers will need to become very good friends with a local architect who specializes in designing mother-in-law suites.

It just seems to me that higher housing prices simply reflect the greater Central bank supply of fiat money. When real interest rates are zero then basically money is free and asset prices start approaching infinity. The value of housing hasn’t gone up! The value of paper money to buy the house has simply gone down!

Shhhh. That’s supposed to be kept secret.

LOL

The last housing bust was incubated by subprime adjustable rate mortgages, NINJA loans, skyrocketing prices (supply and demand) and then nurtured by a full blown recession. Notwithstanding the exponential price increases, I do not see the same dynamics at play with the current real estate market. Without a recession, subprime and NINJA loans and the reset of adjustable mortgages, the bubble may not be as disasterous as before.

There has been many housing busts in us history.. happens every 15 years or so…

The reasons are always different but the impact is same.. pice bust..

This is true esp for California

DD,

But none were the equivalent of 2009 to 2012 the Great Recession where values dropped 50 to 60% in some areas

Agreed

Perhaps some of those loan anomalies like subprime and ninja will not be as much of a factor this time around, but the rate at which debt has been increasing –

from the consumer to businesses to the federal government – will drawf those anomalies in terms of adverse consequences. The question is not if, but when.

Mvrk,

Those were not loan anomalies; that was the majority of the mortgage market back then. That was wiped out with Dodd-Frank and 95+% of loans written over the past 10 yrs have been done so with income verification.

Income verification was the #1 variable attributed to loan default and the basis for Dodd-Frank. Of course there can be a pull back but I dont think it will be anything close to the housing collapse 10 yrs ago.

Sorry Broker Dan, but the no doc mortgages were like turds tossed in the punch bowl of documented mortgages. They contaminated the entire bowl, especially when the wizards on Wall Street poured the contaminated bowl into buckets with fancy derivative names like CDOs. These buckets looked attractive to global buyers, until the buyers realized they were toxic. The rest is history. Yes, Dodd-Frank was designed in part to eliminate/limit the no doc turds, but interestingly, the current Administration is trying to systematically dismantle Dodd-Frank. So time will tell as to whether the turds make a come-back. Meanwhile, notwithstanding turds, the levels of debt across all facets of the economy are increasing at alarming rates. I doubt it will end well.

Wolf, any stories on foreign investors popping up like they are in Canada? China is starting to get better at finding some leaks.

http://www.huffingtonpost.ca/2018/02/26/real-estate-canada-anbang_a_23371224/

As long as jobs stay strong housing wont go down much

Jobs won’t stay strong, see the Car, Housing and Blockchain bubbles. Plus you know, government jobs being slashed to pay for tax cuts.

Not to mention zombie companies and zombie unicorns money problems.

2018 might combine a stronger dollar with a lot of people losing their jobs.

People need to look at a chart of Home Depot for what the smart money is doing. Their stock is cratering. A lot of big cash knows something is coming and it ain’t good for the housing industry. I think the canary in the coal mine just bought it.

I don’t agree that Home Depot is a good bell-weather. They are getting competition from Amazon on appliances, from places like Harbor Freight on tools, and Home Depot is not very competitive on materials pricing for DIY types, nor for professional builders. The thing that Home Depot has been best at is harvesting TIF funds from local governments – but that gravy train can only last so long.