A story of spikes and new flat spots.

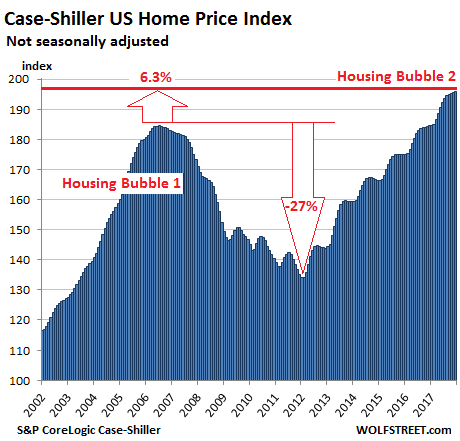

Home prices on a nationwide basis rose 6.3% from a year earlier (not seasonally-adjusted), according to the S&P CoreLogic Case-Shiller National Home Price Index for December, released this morning. The index has now surpassed by 6.3% the crazy peak of Housing Bubble 1 in July 2006, at which point it began to implode in spectacular fashion. Thanks to the radical and experimental monetary policies, prices were reflated by 46% since the bottom of Housing Bust 1:

Local real estate prices, in addition to being impacted by national and global factors — such as monetary policies and offshore investors looking at US homes as an asset class — are impacted by local factors, which cause local housing bubbles, operating on their own schedules. When enough of them coincide, they form a national housing bubble. See chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release was for October, November, and December data. The index uses “home price sales pairs,” for instance, for a house that sold in 2008 and then again in December 2017. Other factors and algorithms are used to obtain a price movement. The index was set at 100 for January 2000. An index value of 200 means prices as figured by the index have doubled since then.

Here are the most splendid among the housing bubbles in major metro areas:

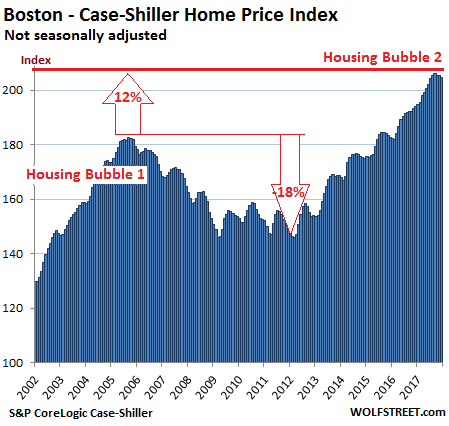

Boston:

The Case-Shiller home price index for the Boston metro edged down again on a monthly basis, the third decline in a row after 22 months of increases. It is now from six months ago, but due to the surge earlier in the year is still up 5.5% year-over-year. The monthly declines could still be within the typical seasonal variations. However, there were no seasonal variations during the relentless ascend in 2015 and 2016. During Housing Bubble 1, from January 2000 to October 2005, the index soared 82% before dropping. It now exceeds the peak of Housing Bubble 1 by 12.2%:

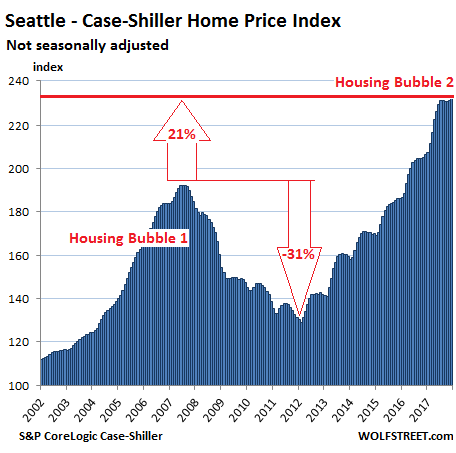

Seattle:

The Seattle metro index rose by 0.6% on a month-to-month basis to a new record, after the first two back-to-back declines in the fall since the end of 2014! The December rise tentatively ended the flat or down-trend that had started to develop. The index is up 12.7% year-over-year, 21% from the peak of Housing Bubble 1 (July 2007), and 80% from the bottom of Housing Bust 1 in February 2011:

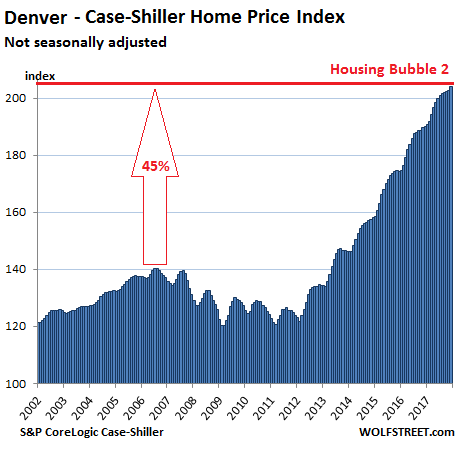

Denver:

The Case-Shiller home price index for the Denver metro rose 0.5% on a monthly basis, the 26th increase in a row. The index is up 7.4% year-over-year and 45% from the peak in July 2006. Denver’s Housing Bubble 2 is a sight to behold:

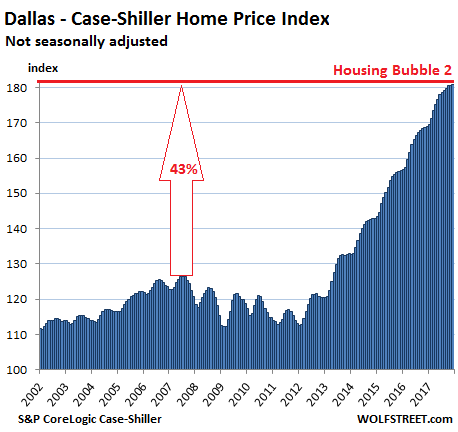

Dallas-Fort Worth:

The Dallas-Fort Worth metro index edged up on a monthly basis for the 47th month in a row. It is up 6.9% year-over-year and has skyrocketed 43% from the prior peak in June 2007. The metro’s price surge since 2012 has been stunning and relentless:

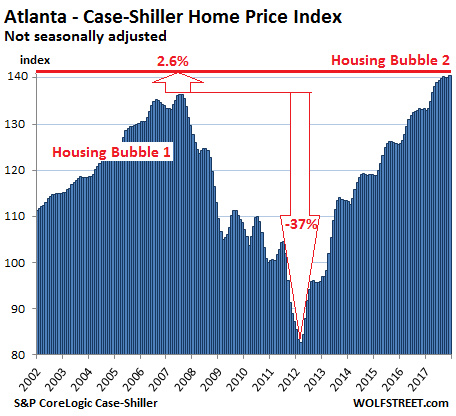

Atlanta:

The December index for the Atlanta metro has been about flat for four months in a row, in line with prior seasonal patterns, but is still up 5.4% from a year ago and is now 3% above the peak of Housing Bubble 1 in July 2007. Note that the index surged 70% since February 2012:

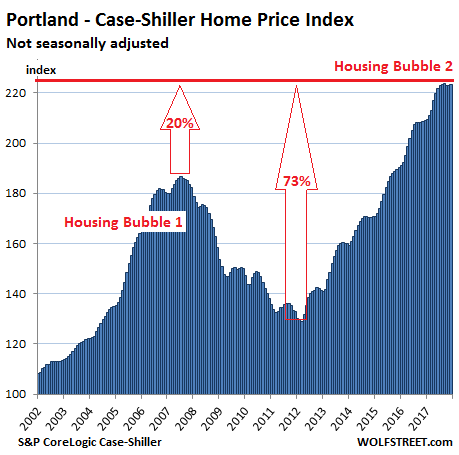

Portland:

Portland’s home price index has now remained essentially flat for five months. This is still within range of normal seasonal flat spots at this time of the year – during times when there were any flat spots at all. The index is up 6.8% year-over-year, has skyrocketed 73% since 2012, and is 20% above the peak of Housing Bubble 1. The index has ballooned 123% since 2000:

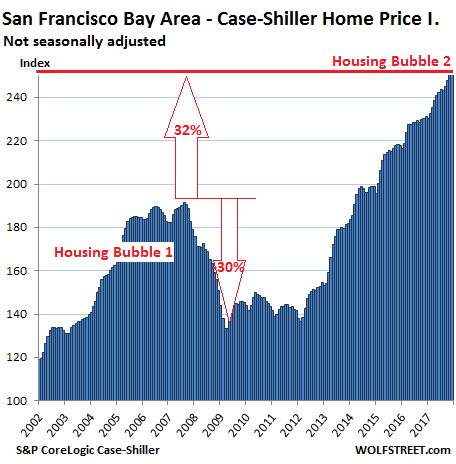

San Francisco Bay Area:

The Case-Shiller home price index for “San Francisco” — actually for the counties of San Francisco, Alameda, Contra Costa, Marin, and San Mateo, which forms the northern part of Silicon Valley — rose 0.5% in December, after jumping 1.4% in November, and 1.2% in October. It’s up 9.2% year-over-year, up 32% from the insane peak of Housing Bubble 1, and up 86% from the end of Housing Bust 1. The index has surged 153% since 2000:

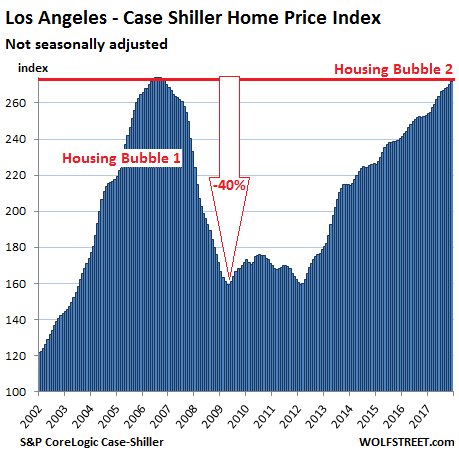

Los Angeles:

The Los Angeles metro index rose again for the month and 7.5% year-over-year. Housing Bubble 1 in Los Angeles was in a special category in terms of its height (up 174% from January 2000 to July 2006) and its steepness on both sides. The index is now less than 1% from where it had been during the peak of the housing insanity in 2006:

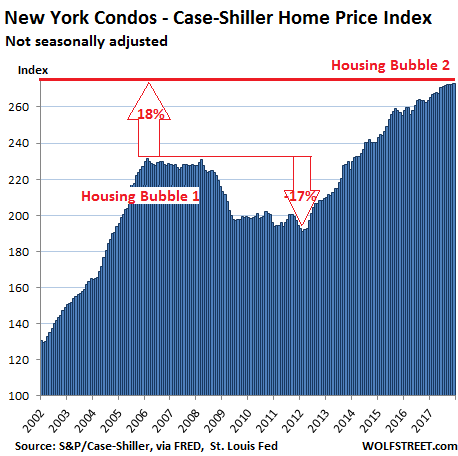

New York City Condos:

Because the New York City condo market is so large, Case-Shiller has a special index just for condos. It inched up in December and is up 3.6% year-over-year. During Housing Bubble 1, from 2000 to February 2006, the index skyrocketed 131%. The onset of QE unleashed money for Wall Street and global investors, and this kept the condo market from plunging. The index is now 17.5% above the prior peak, having surged 173% in 17 years:

This is the handiwork of asset-price inflation — when the dollar loses its purchasing power with regards to assets, such as homes. It was a specific goal the Fed has set out to accomplish in 2008 and onward, and it has succeeded splendidly. Since there has been little wage inflation over the same period, labor has been devalued with regards to assets. Many people who rely on their income from work to fund their housing needs are having to grapple with what is now called the “affordability crisis” or “housing crisis” in those cities, when it’s really just a result of the Fed’s asset price inflation and devaluation of labor with regards to assets.

Surging home prices have primed the housing market for this. Read… What will Spiking Mortgage Rates, High Home Prices, & the New Tax Law Do to the Housing Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Message boards are ringing with stories about how the Fed monetized the deficits and caused this housing boom. So my question is, how did the fed monetize 10 trillion in new government debt by buying 1.8 trillion in treasuries.

The majority of what the Fed monetized was fannie and freddie debt held by foreign central banks. Monetizing old debt doesn’t create new miney, it just keeps the old money from disappearing.

Bernanke said in testamony 8 years ago that without US governmet deficits, free trade would not be possible. Treasury bills are what we call reserve currency.

The world thinks this bubble is a grand mistake by inept politiciant was the plan and has been since Timothy Geithner and Henry Paulson hatched it in 1997. Much of it has been shrouded in (IMO antisemetic) rhetoric by the intellectually confused Ron Paul and his tackling dummy son Rand.

The USA has power today that more than rivals the power the British bankers amd mercantists had in the 19th century. It’s really sad so few people see this. (Spoiler alert – Ambrose Evans Pritchard has been talking about it for years.)

From 2 months ago….

The “Everything Bubble” is about to burst……

By: Ambrose Evans-Pritchard

https://www.telegraph.co.uk/business/2017/12/13/2018-spells-reckoning-us-china-economic-axis/

Based on what? This bubble has been supposedly bursting for 3 years. It’s clear we were in a recession in 2016, which was papered over for the election.

I’m not saying their won’y be, but the trade deficit skyrocketed last month. All those freshly minted trade deficit dollars have to land somewhere.

Everything (stocks, bonds, housing, etc…) has been about to burst or crash for the past 3-4 yrs; but, on we go……

Spoiler Alert: He’s changed his mind.

The bubble goes on but volume and liquidity continue to slowly dry up, as with other overpriced assets.

The FED increased its budget fivefolded…wih superlow interest. ECB and many other coutries has done the same but worser

Let me just rephrase your question. “Who can stop US as a nation that consumes more than it produces for ever given it has the biggest power AKA (carriers, intelligence, nuke) ? The world should just take T bills and let US consume goods”.

A few responses.

1) The Fed did not monetize 10T in debt. It did monetize whatever is on it’s balance sheet. The 10T probably comes from those that extrapolate new money because of fractional reserve system.

2) I believe the majority of what is on the Fed’s balance sheet is US Treasuries. That said, there is 1.75 T in Fannie/Freddie stuff. It doesn’t matter who/where the Fed buys this stuff. If it’s on their balance sheet they are monetizing it. Existing debt was funded with “new money”. When the Fed buys it, they create new money again.

3) Bernanke and others have stated that US deficits have to occur if the reserve currency is the US dollar AND the US runs a trade deficit. If the US did NOT run a trade deficit, then US government would not have to run a fiscal deficit.

4) You are correct to believe that this is not a grand mistake by inept politicians. The US’s fincancial condition and predicament is very much a planned affair with both plus’s and minus’s. The bottom line though is to maintain US supremacy (finacially and militarily).

he may not have actually said it but i’m reminded of the famous 1971 john connolly quote, “the dollar is our currency but your problem.”

Without government deficits free trade could not exist…….please explain.

Let me try. First, US use it’s military power in middle east and tell Saudi and others that you only accept $ for oil. Sadat said NO, so he was taken outs. Now in order to buy oil, you have to first get $ first. In order to get $, you have to sell more foods to US than you buy from US. Therefore, US trade deficit is essential to inject $ into the world for trading oil. Then Saudi gets lots of $, and where would Saudi save it? They buy safe US treasury. Other countries who exports goods will follow the oil model, basically, only take $ and invest back to US treasury.

The more trade the world want to do, the more $ they need and if US does NOT run deficit, the world trade will stop.

No data for San Diego but I suppose it is much the same as LA. Is it any wonder that we now have the city setting up large tent shelters for the homeless, all on our dime of course. As I have stated on this board before, California continues to be a prime example of the line in Kiplings Gods of the Copy Book Heading;

In the Carboniferous Epoch we were promised abundance for all,

By robbing selected Peter to pay for collective Paul;

Not a week goes by that I don’t hear about some new plan coming out of Sacramento to tax the Peters of this place to help build communal style homes for the ‘less advantaged” ( that means those who for the most part refuse to work!). My heart doesn’t go out them, but it does go out to those young folks who have prepared themselves, gotten good jobs in todays economy and yet still are priced out of housing for what ever reason. There seems to be no end to it…………….

Here’s San Diego. Your suspicions are right: the chart is very close to the LA chart.

If you are taking requests Wolf, I’m interested in soon to be Bankrupt Chicago, and the languishing/slowly recovering from Bankruptcy Detroit.

OK, maybe next month.

But Chicago isn’t anywhere near the prior bubble highs, so it doesn’t really fit in.

Detroit’s chart looks like a beautiful double-bubble, though December was still 7% below the prior peak. In terms the median home price, Detroit is among the more affordable big cities in the US. But its downtown area has been booming for years (friend of mine moved there in 2009), and prices have skyrocketed in that area. But that’s a small-ish area of the city. So I don’t know if it makes sense to include it here.

This graph of San Diego should be shown to everyone thinking about buying a house in Denver right now.

Why?

-Both metros are similar in size

-Both have geographic constraints

-Both are trendy places to live

-While San Diego’s weather is truly the best, people in Denver also rave about its milder winters and summers

Funny thing is, people in Denver mention some of the bullet points above as to why “real estate prices aren’t going to go down.” If San Diego is any indicator, those factors aren’t protection against a real estate bust.

Have you ever been to San Diego? I don’t think the Fed’s money is the prime reason for San Diego’s growth. (although I’m sure it helps with building).

San Diego is overwhelmed by Asian and Indian buyers, so it’s a foreign money town now. They’re widening the roads and building housing complexes on every spare patch of land to accomodate the foreign rentirer class. It’s similar to Toronto.

San Diego not too long ago was a quaint beach city south of LA. Now it’s becoming LA, and in ten years there will be no reason to go there for a vacation. The city is absolutely determined to destroy its tourist business.

But I see no jobs boom to accomodate the new population. The rents go up like clockwork evey year and the ‘locals’ are fleeing the city. It’s becoming a satellite city of Beijing.

I’m not sure any of these city charts make sense in comparison to one another. Take Dallas and San Diego. The cost of home ownership and dollar per square foot are vastly different.

Dallas values have exploded and locals trying to buy are in some cases unhappy. But for transplants from California home prices for 3-4 bedroom homes in nice areas are still very affordable. Especially given many professional jobs are willing to pay the same in Dallas as in San Diego. A 4 bedroom starter home, 2-3k sqft in a top suburb has a carrying cost at a median of maybe $2000-$2500 a month after a 2-3% property tax and triple the home insurance in SD. Meanwhile a nice 2 bedroom condo in SD in a top school district runs $2500-$2800 to carry.

Plus Dallas is acctually building new homes people can afford to start in at a really fast clip. Their growth seems to be tied to coorporate job growth.

San Diegos prices are jumping even while are job market is flat and companies like Qualcomm are in termoil. Simply because there are no new starter homes anywhere close to job centers and resales are weak.

All I am really saying is that as crazy as Dallas prices may seem compared to recent history, it is easy to justify their prices even on one solid corporate income. And save a good 30% of take home pay or more.

In SD you get nearly the same income and almost zero chance of affording adequate housing unless you are willing to save nothing or manage to aquire an oversized downpayment.

I suspect markets like Denver may be more similar to Dallas more than SD. I wouldn’t be surprised if anyone of them has prices come down in the near future, but it will be for different reasons in each.

AC in SD – I really hope you mess up your back, lose your house in the next dip, etc and find yourself out on the street in your 50s or older so you can have people tell you you “refuse to work”.

Better still, since a large proportion of the homeless are children (something AC in SD presumably is ignorant of) we can put the little buggers to work in Amazon warehouses. It’s win-win, a glorious public private partnership, the free market at work, and a lesson in “responsibility” these people need.

Life is about “choices,” and why should decent taxpayers like AC in SD have to pay for these children’s choice of poor parents?

Not directly related, but an epiphany I had a year or so ago…

If NYC/Chicago subways, trains, bridges, etc. etc. are in desperate need of maintenance & repair, are there not unfilled jobs to do this work?

How can basic infrastructure jobs go left wanting IF there are millions sitting at home collecting welfare?

Supposedly we can’t afford to pay people to fix our infrastructure but we can afford to pay them to do nothing?

Can someone please explain this dichotomy?

Powerful unions prevent using low wage labor. Municipal jobs are among the best paid in the cities.

@Petunia Thanks. Makes sense.

Yes, it makes perfect sense, except that it’s completely wrong.

First, those jobs rebuilding roads and bridges are not “municipal jobs,” they are performed by private sector contractors employing engineers, skilled tradespeople and laborers.

Second, in a country where far less than 10% of private sector employees are unionized, and where median incomes have been stagnant for over forty years, where are these mythic “powerful unions?” If unions are so powerful (a Big Lie promoted by the US Chamber of Commerce and other representatives of Money) why haven’t wages increased across the board? Unions increase wages for all workers in their industry, even the non-unionized, since union wage scales have a trickle-down effect.

It’s no accident that wage stagnation, and wage declines for those without a college degree, has accompanied the decline of union density. Yeah, “powerful unions,” indeed.

Finally, I assume you’d prefer that your medical care not be provided by “low wage workers:” why should you feel any different about repairing the bridges you and your family drive across?

Do you you really want “low wage labor” (as if that’s a good thing) repairing the infrastructure you rely on? Sure, your taxes will be lower (except they won’t, since the same politicians who blather about “powerful unions” are also hot to provide corporate welfare with our tax money: NFL stadiums, anyone?), but driving to work might be playing Russian roulette.

Duky,

In a place like NYC, where public transportation probably has the widest use of any place in the country, the construction unions rule. The Brotherhood of Electrical Workers is not a bunch to be fooled with, nor are the plumbers, cement workers, etc. In the 1980’s a master electrician I knew made $250K.

@Duke I get the sense you haven’t been on Chicago or NYC public transport much. In some sense I’m simply talking about cleaning up the grime/urine/graffiti, new paint, etc. Minimum wage, no/low skill stuff. Some subway trains/stations in NYC look as bad today as they did in the 1970s. They look like no one has done anything for 40 years. Yet, people have been getting paid decade after decade for sitting on their butts.

Neither of you have any idea what you’re talking about.

I happen to live in NYC, and take public transportation to work every day, and can confidently say you’re both wrong: the subways are crumbling because a succession of governors and mayors have failed to maintain funding to keep the system up and running.

Your Fox News talking points have nothing to do with the reality in NYC, also typified by your false claim that Local 3 of the IBEW has anything to do with the subways. Subway workers are represented by Local 100 of the Transport Workers Union.

And I call BS on your deceptive claim about your “Master Electrician” friend. The term denotes a licensed employer, not a journeyman electrician working for a union contractor.

I’d recommend that you educate yourselves about the history and role of unions, and how they were the single biggest factor in the emergence of a broad middle class after WWII, but you seem too engrossed in your Glibertarian fantasies.

It is like pissing in your trousers,,warm and nice in beginning,,,cold and terrible later. O r like party and later hangover

In the broad scheme of things if you compare genuine money against all other assets you can see that the pm manipulators are handing us all a gift. Just put 2 pm /month away then wait until the rest of the world wakes from their slumber/comer.Sit back relax and watch the show unfold. Enjoy.

Sorry for my ignorance, but what does “pm” mean Tom?

Typically, “pm” refers to “precious metals” as in gold, silver etc. If someone talks about “stockpiling pm’s” they mean stockpiling gold, silver non-collectible coins etc.

Cheers

Question:

Why can’t the Fed just keep doing low interest rates and QE forever…or for a least a very long time more? Based on Wolf’s prior articles, the U.S. if far behind Japan in debt and QE. After all, asset inflation and wage degradation fits in with the establishment’s neo-liberal agenda quite nicely.

So why can’t the Fed keep the party going and going and going?

Why can’t it work here, it it has “worked” in Japan?

I think this is a good question. If you ask the MMTers, they will say that it definitely can. The currency will lose value, but they’ll argue that’s been happening anyways.

In Japan’s case though, they continue to defy expectations i.e. the currency still retains quite a bit of value in spite of rocketing debt.

Maybe we’ve been wrong all along?

The MMT might/should also point out that QE targets the wrong thing and just creates assets inflation. This actually has some pretty negative demographic (and thus long term) consequences. You can essentially use the same program to fund a jobs guarantee to create employment directly instead of relying on trickle down wealth effects.

“The MMT might/should also point out that QE targets the wrong thing and just creates assets inflation.”

If you’re a neo-liberal (Hillary, Obama, Democrats, Republicans, the entire establishment) that is the RIGHT thing to target. That is exactly what the neo-liberals want to accomplish and they have and are succeeding brilliantly.

Timbers.

I don’t doubt that.

The short answer is that the US wants to maintain dominance with the dollar around the world. Therefore, loans in dollars need to be worth something; i.e., pay reasonable interest.

That is the world view. Back at home, there are plenty of investors that have been given the shaft with ZIRP. Insurance companies and others depending on low risk and reasonable interest. Joe six pack at 62 comes to mind as well.

I would like to hear Wolf’s response too.

I don’t get this. Japan was no.2, and they leveraged themselves into no.3 and two lost decades. Leveraged debt consumption and wealth transfer will lead to Japan’s result and some how people are thinking Japan is a good example.

Good question. I have been thinking about this as well.

I think a race to the bottom is the new normal for developed economies. Countries such as China and India are the Walmart or Amazon of planet and have been chipping away at the developed economies. The latter are basically high-end brick and mortar retailers, unable to compete. So they have to cut cost. Enter concurrency devaluation, thus making their products (assets and labor force) cheaper, more attractive.

Developed (racing downward) and developing (racing upward) economies will eventually meet somewhere in the middle. But the party is over for younger generations in developed economies.

timbers,

I can see two questions in your comment. These are big questions, and kind of hard to address in just a few words, but I’ll try:

1. “Why can’t the Fed just keep doing low interest rates and QE forever…or for a least a very long time more?”

The reason why the Fed doesn’t keep QE and ZIRP forever is that it doesn’t want to crash the system. Asset price inflation is very destructive, as we have seen every time. Assets are used as collateral. The whole system is tied together. Once asset prices deflate, which they invariably do after a bubble, the whole financial system is at risk.

Japan went through this type of asset bubble in the 1980s. And it blew up. It tore up its financial system, including the banks. Today, the Nikkei is still down 45% from where it was in 1989! This is the future of the US unless the Fed figures out how to unwind its asset bubble scheme before it’s too late.

2. “Why can’t it work here, it has ‘worked’ in Japan?”

No it hasn’t worked in Japan. See above.

Best I can tell, there is now a social contract of sorts in Japan to work out the fiscal mess via the currency and inflation, rather than a debt crisis or austerity. They’re trying to do this in a controlled manner over many years. And Japan has some tools the US doesn’t have, including a large trade surplus and a shrinking working-age population: when jobs are getting scarcer due to automation, those fewer working-age people are still going to have jobs!

The hope is that the process will be “contained” and slow-moving, and that it spread equally among all Japanese, which will be fairer and more bearable than the harsh austerity a debt crisis would entail, which affects the poorest parts of society the most (see Greece). Each Japanese is expected to do their part and bear their burden.

I’ve just been to Tokyo last year. And the 2 lost decade thing is a bit of an exaggeration. Tokyo didn’t look squalid whatsoever, and I am sure many of the big cities are like that as well.

I’ve definitely heard of smaller areas looking like poverty zones, but comparing US and Japan side by side I think the Japanese are faring better.

I agree that the lost-decades thing that is being propagated in the media here is nonsense. I’ve been going to Japan since 1996 (just over 2 decades), and there’s nothing of that sort going on.

Their huge government deficits are paying for a lot of good stuff, some of which you see when you go there. You cannot see the fiscal mess. In a debt crisis (Greece, austerity), you could see it because government services would be cut. But Japan has decided not to go that route. They’re continuing to run huge deficits, knowing that at some point they’ll have to accept that this will be paid for (hopefully under someone else’s watch) by the currency. This can go on for a long time.

Thanks for the response!…(One wonders if the Fed thinks/knows this)

“The reason why the Fed doesn’t keep QE and ZIRP forever is that it doesn’t want to crash the system. Asset price inflation is very destructive, as we have seen every time. Assets are used as collateral. The whole system is tied together. ”

The chance to increase interest rates has long past. Hence your answer actually suggests the fed will keep interest rates low forever because assets have been used as collateral for new assets and those assets have been used as collateral and so on.

Any weakness in the market is temporary, pending new fed cuts (after their pathetic raises) or even new QE. The whole economy would implode if rates got too high.

There is no way back. Interest rates are still essentially negative, I can’t see them rising much more.

…labor has been devalued with regards to assets…

This is the greatest comment ever made, thank you for your saying that Wolf.

I wish our media will say the same thing and expose how Fed has screwed the working man to save the financial engineers of speculation on Wall Street.

Fed should not be immune of the ballot box, it’s the most powerful gang in the country and we should at the very least be able to vote them out, I know it a small consolation, but still better than nothing.

they do acknowledge this concept but only in code. the media was buzzing about “wage inflation” causing the stock market dip.

“…labor has been devalued with regards to assets.”

In the not-so-distant past, this had a less euphemistic description: class warfare, as Warren Buffet himself indiscreetly admitted a dozen years ago.

Who gets hurt when the real estate bubble bursts? Those with little or no equity, those forced to sell when the market is down and perhaps taxpayers if there is another bailout. Who benefits? Those of us sitting on the sideline with cash ready to scoop up more properties, politicians who funnel REO’s to their cronies and landlords who now have a plethora of renters to choose from. Like the stock market, it is merely a cyclical transfer of wealth since money does no evaporate, it simply changes hands. If you are on the “right” side of this exchange, it’s all good.

You know, the rule of wealth transfer game is simply 95% will lose and 5% will win. It is a gambler’s game. As Buffet said, MOST people are bad at this game and majority will lose. Hence this is NOT “ all good”. When you have enough inequality and enough homeless, you will have social unrest.

As a nation, the policy should encourage wealth creation rather than wealth transfer. Forcing people to play the wealth transfer game which they are NOT good at will lead to bad social environment. All the depression drug use, school shooting, etc.

i have my doubts the people that are calling the shots care whatsoever about any of this, as it will certainly never affect them. if roving masses of angry, armed homeless people ever become so much as a remote threat to them, it’s always a quick helicopter ride to the private plane or yacht, and off to new zealand they will go to live happily ever after.

Yep that’s how our system works. You get paid money for having money.

It’s truly amazing to see how the prices have vaulted past the old highs. I’ve been selling my rental houses since early 2017. My last one goes on the market in about a month. Probably a year or two early, but I’m ok with it. This is crazy.

Curious, what were the selling prices vs rents?

Here in the Dallas area rents are up a lot, but costs and values are up even more. Thus, reducing Return On Equity. Plus, local city governments are going REGULATION CRAZY. Since there is no income tax in Texas, our property taxes are HUGE and increasing faster than prices. Labor and materials are up 50-100% and in some cases 150% in 3 years!

Add once-in-a-lifetime price appreciation (at least for Dallas), and so, like DK, we are selling.

But stategically and definitely not everything. About 5% of our houses per year. Getting out of “challenging” areas and “culling” the herd.

We are essentially fixing and flipping our own rental houses. Since we have owned them for 10+ years our basis and mortgages are low. We can thus put in a Premium Sale Rehab, which is far superior to true flippers that have to buy at today’s overpriced wholesale costs.

We price them fairly for Owner Occupants and are getting 8-22 offers per house, almost all ABOVE asking price.

Interestingly, it seems everyone here is BUSY BUSY. Too busy to want to do any repairs. Or too busy shopping (mall and store parking lots are as full as if this is the weekend before Christmas).

So houses that are in basic good shape but need “some” work are sitting for months. As are ones that had low-end flipping rehabs. They are too much work for retail buyers, and too expensive for flippers.

Of course houses that need LOTS of work are snapped up by investors and flippers. Margins for these are very tight and most of these people will be bankrupt when the music stops.

Just a note about the titling I’ve seen here (and other places). “Bubble 2” as shown on the charts, implies that prior to 2007, everything was wonderful and we’ve never had asset bubbles before.

Asset bubbles are NOTHING NEW. History is filled with them and 2007 was just one of MANY. There will be more. Just like human history, it repeats.

2007 was only relevant to those who happened to have “lost” then. There are lots of people who don’t remember the 2000 bubble and believe it or not, don’t even know about the 2007 bubble.

Erik, asset bubbles are nothing new but today, we are saddled with an nsurpassed amount of debt, entitlement & pension liabilities, an aging population and out of control healthcare costs. Job & wage growth are weak as is GDP growth so these factors combine to make it different this time. Maybe the roll offs and rate hikes slow in the second half of the year if equities start to suffer but with all of the above, the piper will be paid. If not this year, then within the next couple of years. None of this is sustainable.

More than a crisis is brewing. For decades regular folks built wealth through home equity, and the forced saving a mortgage applies to a family. Home ownership is a pillar America’s social contract. Seeing the concept being undermined by huge financial players 10 years ago was a serious blow the the legitimacy of nation. Another meltdown in home prices is another nail in the coffin of the Americain dream.

As much as I’d like to believe this is a bubble, I can also see current conditions as a permanent shift of individual assets to corporate assets. The giant investment bank housing purchase since 2009 was an attempt to generate rent revenue and not build equity, so even if home prices decline significantly, there’s no incentive for the corporate owners to unload properties if they can still collect rent.

The corporate entities are there to make money.

If they see a scenario where they can unload for a given price and buy it later for much less, why won’t they sell it ?

ON top of that, if interest rates rise,corporate would have even lesser incentives to keep rental homes .

I wonder how a stronger dollar will affect this.

I am curious what it looks like in more of a median market that isn’t has large as the cities you provided, say Charlotte, NC., do you have data that can show the same increase happening there

Working on it. It won’t be Case-Shiller data but median home prices. I’ve reached out to these folks but haven’t heard back yet. Once I have the data, I’ll post it :-]

Anybody hazard a guess how much longer the second bubble in specifically San Diego will continue to inflate?