Something’s not right: Banks are heavily exposed to record business debt, as credit quality deteriorates.

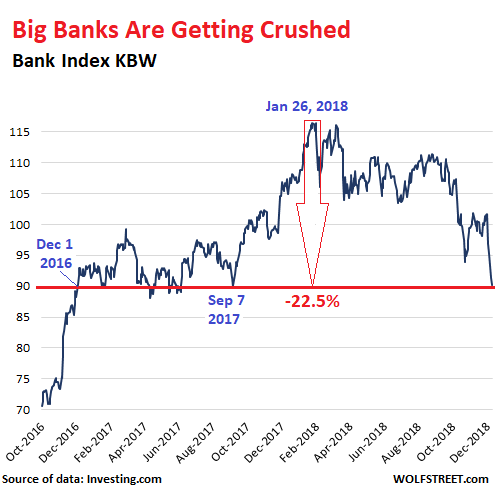

On Tuesday, the US KBW Bank index, which tracks the largest 24 US banks and serves as a benchmark for the banking sector, dropped 1.2%, the fifth day in a row of declines, to the lowest close since September 7, 2017.The index is now back where it had been on December 1, 2016. Two years of big gains gone up in smoke. The past five trading days looked like this:

- Dec 11: -1.2%

- Dec-10: -2.1%

- Dec 07: -2.0%

- Dec 06: -1.6%

- Dec 05: -4.9%

But no, the index doesn’t include Goldman Sachs – which is big in other ways but not as a bank, and which has skidded 35% from its all-time peak in February. The index has now dropped 22.5% since the post-financial crisis peak on January 26:

So far in Q4, the index has dropped 14%. Unless a miraculous banking-Santa-Claus rally pulls banks out of their dive by the end of the quarter, a 14% decline would make it the worst quarterly decline since Q3 2011. If tax selling kicks in, given the losses bank-stock investors have taken so far this year, it could get worse in the coming days.

Not even in Q3 2015, during the oil bust, when investors were fearing that banks would take steep losses on their loans to the oil industry, did shares drop this much.

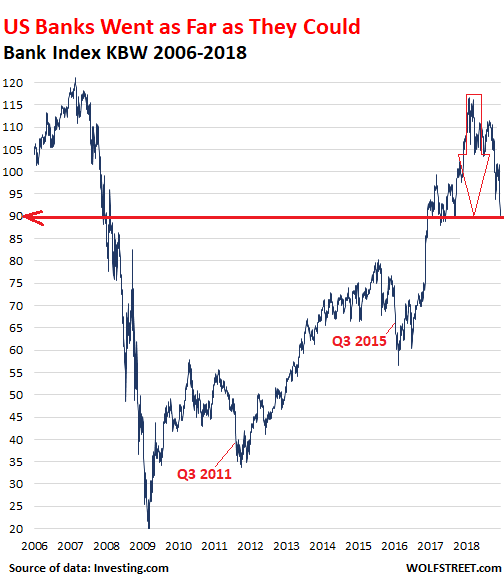

The index is now back where it had first been a couple of years before its crazy peak in February 2007. Said peak occurred about a year before Bear Stearns toppled. During the subsequent collapse of banks stocks, it looked like the index would hit zero.

After the bottom in March 2009, the Fed’s strategies to benefit the banks and those that owned them took hold, at the expense of depositors and other classes of US stake holders, such as renters or future home buyers. And it worked. But that era is now over. And the tax cut too has been baked in, and banks are left to fend for themselves:

Big banks are heavily exposed to business debt, and business debt, which includes commercial real estate debt, has ballooned to record levels, while credit quality has deteriorated. The Fed, in its recent Financial Stability Report, pointed out this issue as a major risk to financial stability.

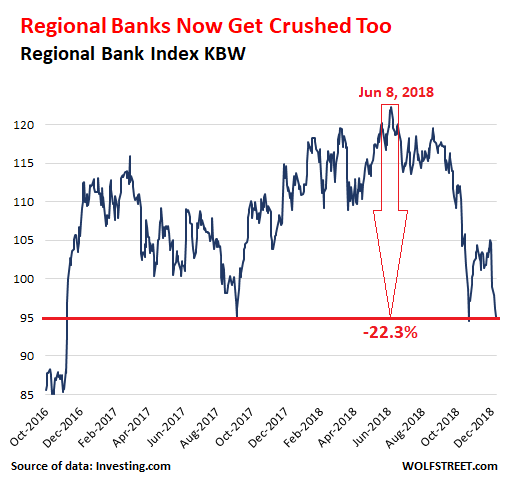

But those are the biggest 24 banks in the US. What bout the regional banks?

Since the big-bank sell-off started in January, the regionalbanks actually performed quite well, and the KBW US Regional Bank Index climbedto new post-Financial Crisis highs the summer.

The story on Wall Street was that regional banks would be immune to the downdraft, and that investors needed to rotate from big banks into regional banks, etc. With immaculate timing, the KBW Regional Bank Index [KRX] peaked on June 8, wavered for a month, and in September started to spiral down. It too has plunged 22.3% by now, but in a much shorter time period than the large bank index:

This is a new era for banks – the era the Fed arm-twisted them into preparing for: Building their loss-absorption capacity by building their capital buffer to have it nice and fat and ready to be eaten up by business loan losses over the next few years. But these are still the good times, loan losses are still low, and money is still flowing relatively cheaply and plentifully. The actual pain won’t start for a while.

Instead of “bubble” or “collapse,” the Fed uses “valuation pressures” and “broad adjustment in prices.” Business debt, not consumer debt, is the bogeyman this time. Read... The Fed Explains the Rate Hikes: To Prevent Financial Crisis 2

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

Sometimes I wonder when we will see the Capital Countercyclical Buffer CCyB ? I’m sure the banks will love that.

Unless FedGov is willing to prosecute bankers for fraud, I don’t see why anyone would use profits to build up capital reserves when the could just pay themselves special dividends or stock buyback, and let the companies run themselves into the ground. Did the principals at Lehman or Bear care that they ran those companies into the ground?

FedGov prosecuting bankers for fraud?!! BWAHAHHAAHAAAA!

The banksters own our so-called regulators and enforcers.

Amen. The little issue of derivatives exposure is now usually ignored in discussions of bank finances. They amount to reportedly over a hundred trillion dollars and banks have at most capital of 1.5-5% of the value of their investments.

Financial times and zero hedge report the banks’ exposure is massive. I am surprised that the banks’ stocks are as high as they are. It is because they make profits from risky transactions effectively guaranteed by the U.S. government if they lose (through FED and TARP type bailouts) and by dividends and stock buy backs if their bets come back as winners.

We should give the privilege of fractional reserve banking, (effective) government guarantee of against losses, access to ultra low interest rate loans from the FED (even when the entities are insolvent), FED protection, to America’s biggest employers and companies which are important to our nation, not to the most crooked and incompetently run by banksters. Let Intel or GM create banks and get the FED loans, if they agree to increase numbers of U.S. employees.

But they are not on their own….

They have the full faith and credit of the US Government and the Federal Reserve backstopping them.

A Roman historian once wrote that at some point the secret of Empire was out: that emperors could be made not in Rome, but in the provinces if they had enough legions backing the claim. Well, the secret of economics is out: money does not have to be made through trade, industry, and extraction. It can be summoned up via computer at will. We may not like it, or agree with it, but the bankers know it and they are basing their actions accordingly.

Hence bitcoin.

Bitcoin = scam. 82% of its price disappeared in just 11 months. This is one of the reasons it’s useless as a currency.

True about bitcoin. But to save the banks, it cost US depositors trillions of interest in the past 10 years. In essence, the bank stock price went up, via the ‘gift’ that the feral reserve gave to these banks. A transfer of wealth to the banking elites. Middle class america got gutted in the process. A more ethical and legal outcome, would have let these banks figured out on their own, how to stay solvent, and the bad ones disappeared, while protecting the depositors to the tune of $250,000 per account. Yes, that would have been costly, and been beyond what the authorities had on reserve for insurance, but they could have conjured that money up, just as easily as the trillions in debt on the Fed’s balance sheet, that was taken off the bank’s balance sheet. Accounting trickery, screwed every single bank depositor. More-over, we’d very likely have a much healthier banking system by now, with the rot of those immoral people who ran this thing into the ground, out of their positions. And there would not likely be only 5 or 6 big banks, that control 80% of the money. So here we are again, except this time its much worse, with far higher levels of debt across businesses, states, and our own federal government. Same wicked and immoral people are still there, so expecting their actions to be any different this time, is literally the definition of insane. It’s really incredible that so many people let their government screw them royally, and steal so much wealth from them, due to the terrible wretchedness of these banking institutions. No rage, no riots, no pitchforks. Just passive aggressive verbal vitriol, increased mass mental depression, increased suicides, and continuing delusion. People actually believe we escaped the horror of the 1930’s style depression. their denial, is the statement this could have been worse. Well the ‘worse’ merely got kicked down the road, and will be exponentially ‘worse’ than the correct course of action taken back in 2009, with many more trillions in debt spread across every sector, and across the globe. Bail that one out ‘geniuses’ at the Fed and other cental banks !!!

I call it bit-con.

Agreed, dropping 82% in 11 months is not good if it wants to be a currency but don’t agree it’s a scam[1]. If it fails to settle down it will fail as a currency, but it’s still early days.

As I keep saying, trying to gauge the value of bitcoin using traditional metrics isn’t going to work. Even poor Tom Lee has come unstuck. It’s like measuring the first automobiles using your hand. Yes, you get a number that you can compare with the height of a horse, but it tells you naff all about the automobile’s cubic capacity. But of course, the true innovation of the automobile was not the infernal combustion engine, it was the pneumatic tyres, right? Blockchain any one? Now there’s a scam[2]

So it’s best to ignore bitcoin’s price at present. It, in fact the whole crypto-space, is undergoing massive development. True innovation, unrestricted by regulators and their sand boxes. The species are evolving, literally. Most activity related to bitcoin is the Lightning Network (LN). Other, more technical stuff’s going on too, but LN’s more than enough for me to keep up with.

[1] But that’s an argument for another day.

[2] Actually, blockchain is just technology and, like any other technology, it’s non-sense to call it a scam. It can be used in a scam, sure, but then so can any technology. Blockchain has legit uses, e.g. as an immutable, extend only, ledger, such as bitcoin’s.

medialAxis,

Blockchain is not a scam. But the term has been USED for stock scams. It’s a legit technology that may have been over-hyped. Lot’s of companies are spending a lot of money trying to figure out how blockchain might solve some of their problems. Maybe someday, something big will come of it, but it hasn’t yet.

Bitcoin has counterparty risk. Gold has NO counterparty risk. There are no similarities between them.

and the value of those IOU’s known as FRN’s are what $0.02?? (the cost to issue)

Issuing Bitcoin broke the monopoly on money issuance. The question now is, how much are you willing to pay for a viable truly anonymous cryptocurrency? Or how much do you really trust your government?

Bitcoin has as much intrinsic value as fiat, but its ultimate supply is limited, so it has that advantage in terms of a competing ‘scam’.

As to bitcoin, I suspect that the creator figured out a way to make vast sums of money with little effort. Reportedly a reserve remains in the creator’s name, so by creating this “currency” he can periodically sell large portions of his reserve for huge profits.

On another subject, I completely agree with Mike R’s analysis below: we and our children and grandchildren will pay for the de facto bailouts (e.g., QE) for dozens of years or more. However, the shock to the financial system of the banks’ collapse could have been averted in other ways.

The banksters stampeded the U.S. congress into bailing them out WITHOUT conditions or banksters’ loss of bank ownership like you scare cattle. Usually, the management and shareholders of bankrupt corporations lose everything and if the entities continue, the banks’ new shareholders are their former creditors: that is the bankruptcy process.

The U.S. congress could just have passed emergency laws and taken over the banks, guaranteed their debts to avoid collateral damage to others, and left the banksters holding nothing, without any more control of the banks. Due to the constitution, the U.S. would just have had to pay the banksters whatever their banks were worth at the moment when they collapsed (or had to be taken over) and needed U.S government aid, even if most concealed that fact.

Whatever the banks were worth when they were insolvent and taken over by the government could have been paid over to the banksters: zero or close to it. The banksters used (and will soon use again) fear of financial collapse to demand an enormous bail out (and get huge amounts of FED ultra-low interest rate loans), which let them keep control of our financial system despite their massive frauds against pensioners and others in selling worthless RE mortgage-backed securities, which they knew would fail.

Unfortunately, the banksters’ demands for bailouts will soon resume: it is just a matter of time given the derivatives and other risks that they are taking. They cannot be called casinos, because professionally run casinos do not really run the risks that major banks are running now.

The only positive is that they will soon need such huge bailouts that the IMF or EU will have to participate. Let us hope that they at least are a little less corrupt and controlled by the banksters, so they impose conditions on the banksters’ bailouts: such as new bank owners and new officers.

European authorities and national governments have been backing Euro banks for years now and look how far it got them. The STOXX® Europe 600 Banks is down 26% year to date and has never got remotely close to its 2015 peak even during the recent stock market euphoria.

The Bank of Japan has been doing everything to back national banks, including directly intervening on stock markets to buttress their equities, yet Mitsubishi UFJ is down a cool 33% since its January peak and hasn’t gone close to 1,000 yen since 2008.

On paper this wasn’t supposed to happen: if it’s State-backed it cannot go burst, right?

The reality is these banks are not your honest State-owned enterprises like Qatargas, Codelco or Aramco, whose main scope of existance is to be profitable to provide a steady revenue stream for the government.

These are companies which cannot walk on their own legs, at least not without sweeping reforms, and hence need to be constantly protected, whether by providing them nearly unlimited liquidity or by sheltering them from potentially crippling lawsuits and prosecution.

But government support is a fickle thing. It can be withdrawn as easily as it is bestowed.

In 1973 Norton-Villiers-Triumph (NVT), formed from the remains of Britain’s once glorious motorcycle industry, formed grandiose plans to take on the Japanese and the Germans, which however wholly depended on the continuation of the loans, to the tune of £4 million (in 1970’s money), extended by the Heath Cabinet.

However in October 1974 the Tories were heavily defeated and the newly appointed Minister of Industry, Eric Varley, started waging an all-out war against “Wardens of the State” which were a drag on the exchequer such as NVT. The government loans were recalled in July 1975 and that’s about it. NVT entered receivership right away and was liquidated in 1978.

I honestly doubt NVT would have been able to impress BMW or Honda: their present models were basically early 50’s vintage and what they had in the pipeline was a technological dead-end. On top of this their factories, logistic chain and QC were ridiculously outdated.

But they were backed by HM Government so nobody really cared because they would have been bailed out no matter what, right?

The artist Monet lived off an allowance from his solid bourgeois father, and with some sales he lived very well indeed: when the allowance was withdrawn, and the art market hit a low in a general financial crisis, he and his wife and children almost starved – even having to beg money to bury his wife with decency.

Ever thus: the rules are different, until they are not…..

How could modern corporate capitalism survive if the banking system went down? Everything is run on credit. Again, I’m not saying any of this is good, but government and central bank support for the too big to fail financial institutions is now baked into the cake. I can imagine no government pulling the plug unless the entire system is in collapse from an exogenous source (plague, asteroid, climate catastrophe) and they are in “every man for himself” mode.

Or, possibly….”…..pitchforks at the ramparts!”

You aren’t serious? Banking services are everywhere, the problem with banks isn’t shadow banking, the problem is shadow banking is real competition to traditional services. Banks are where Autos were a few decades ago, under siege by new technology, and foreign competition. Argentina issues bonds in US dollars and sells them to US pension funds (and the IMF bails them out!) The web of interdependence is locked in, the FED made US banks buy DBs derivative book. When you bailout out the banking system you are bailing out foreign banks. The banks blew up in 2008 and they never got better but a lot of people drank the KoolAid.

Nobody disagrees with that.

However, the question is how much banking is needed, maybe 10-25% of GDP is overdone?

Also, why bail out failing banks without any consequences?

I am in favour of nationalising them, firing the failed leadership, blowing the bond- and stockholders out of the water and then sell the remains of the business in the market to one of the banks that works.

For capitalism to work, there has to be real losses and personal consequences imposed upon poor business decisions.

Government and CB support for “all” existing institutions is NOT baked into the cake – just ask Wells Fargo.

Also, the millions of people who were robbed blind by the bailout of the crime-banks in 2008-2009 are now on alert. If the government attempts to bail out the big banks at taxpayer expense yet again, that will be so unpopular that genuine financial reform could easily become inevitable.

Split banks into commercial and investment banking. Regulate commercial banking like utilities and limit geographically. No implicit backing for investment casinos.

“But government support is a fickle thing. It can be withdrawn as easily as it is bestowed”

exactly. we now have a generation of financiers who grew up in the era of “moral hazard.” goldman was allowed to become a bank overnight so that the government had an excuse to bail them out in 2008. jp morgan was made whole by msglobal by “rehypothicating” retail investors accounts. i could go on and on.

this is why populism terrifies bankers and their gov’t cronies. it’s a reminder that the government requires the consent of the governed. people are waking up. the yellow vests in paris are just the beginning.

Had a BSA 441 Victor in the 60’s. A really cool bike (in my opinion). Sad to see the British bikes go away.

Cycle magazine had full page ads showing the 441 caressed by a lithe and lovely beauty wearing the shortest short shorts. This was probably April 1968. I promptly pinned the ad on my bedroom wall. My old man promptly tore the ad off the wall. Alas, I acquired a wife and three daughters, but no BSA. Thanks for for the pleasant memory jog, Lion.

Lion,

I also had a Beezer, a Triumph, and once a Norton…Sad to see my youth go away….

British bikes…not so much.

I used to think the same until the gearbox on my brand new Triumph disintegrated on Christmas Eve. And it took three months getting it back together because the first time around Triumph actually dispatched a defective gearbox as a spare. I will spare the long lithany of assorted mechanical and electrical horror stories topped with amazingly poor quality control.

Needless to say when I bought my first Honda I kept on asking myself why I hadn’t bought one straight away. Same thing with BMW.

Man I thought no one today would remember them. I had my first bike crash on one. It was great off road. Problem was the Lucas electrics. God help you if was wet. The motor was bulletproof single cylinder, kick start on a freezing morning.

MC01, I’ve owned six motorbikes since my 18th birthday – all Japanese made. In spring 2002, I bought a new Kawasaki ZRX 1200, and I’ll drive it until I’m too old to ride! It’s a great machine in terms of design, engineering and build quality.

Good luck and happy trails to all the WS readers who’re motorcyclists out there.

P.S. Wolf, do you ever get the itch to ride a motorbike one more time?

Dan Romig,

Occasionally, a brief unpleasant itch :-]

I’m like so done with these things. Thank God I survived them.

I’d like to further qualify my statement. The 441 was a cool bike to ride around, but not a comfortable one ! Vibrated a lot, especially at speed, weight centered high, but when you’re young you overlook comfort to be cool. I owned 3 bikes with my brother-in-law before I went off to college, my part was providing half the money. The other two were a Triumph 650 that we put electronic ignition on, and in 1970 we bought a Honda 750. Way ahead of the British bikes in ride-ability. And that Honda was fast.

Mike R – You have summed up the situation nicely. They can’t keep this artificial system going indefinitely, though, and the pain will unfortunately be felt by all.

I.m.o. one should hedge against fiat currencies by owning some physical precious metals, kept outside of the crooked banks.

“Something is not right” – Indeed!

They have a leadership challenge in the UK over Brexit, the Tory’s are eating each other like rats in a sack, and, yet they run up the indexes!

I’d have thought that the big money, the people dealing with writing and buying futures and derivatives would about now begin to consider: “Will this clear? and “When / Where will this clear?”.

But, no worries, obviously.

Funny how banks really work. My nephew worked for a US bank right after Uni. (BOA) It was a nightmare sweat shot, a real crap job with nice slacks and a tie. He remarked to me that one day wanted to make it into the “regional” upper echelon for the sake of his children. It took about 5 years for him to understand there was no room and he would never make it into the ‘club’. What drove him nuts about the job was the club and the closed membership, thereof; the disparity in wages and benefits/bonuses, and lack of accountability for the manager.

He quit.

So, just after “uni” (about 21-22 years old) he started at BOA. Five years later (about 26-27 years old), he was upset he wasn’t in the “regional upper echelon” and quit.

Amazing.

To be fair, you are either on track or you are a wage cuck. It is predetermined and you know within couple of years where you stand. If you ain’t getting regular promotions and bonuses in excess of 10-15 percent, you are a cuck and should look else where. They will never respect you, no matter what you do. Working extra unpaid OT, is not how you get ahead despite what any Boomer would say. It’s like this in all semi preffftigious companies. Sticking around is just asking to waste your career and to be layed off once they start paying you too much bc you stayed there 10 years.

After working at large organizations for 30 years. I think truly talented people get promoted to top positions, but they are talented in certain ways. They are abnormally energetic, articulate, and great executors, to the point of being heartless when needed. They usually have tremendous ego (sometimes well hidden) and they have high expectations. The downside is they usually have no creativity or patience to think outside the box. This is why most large corporations ultimately fail. They can’t change their ways. They can’t think of new ways of doing things.

If you are a thinker and like to ask the question “why?”, it is best to get out on your own at some point or work for a small organization. You will get bounced out of a large corporation fairly quickly unless you agree to sit back, shut up, and be happy with your current pay and responsibility. If you want more, you’ll have to sell your soul and not ask why.

Working extra hard as a means of getting ahead is like peeing yourself in a dark woolen suit. You get a warm feeling, but nobody notices.

Yes. My experience is that it usually takes about 3 to 5 years to figure out the political lay of the land in a bigger company. Merit has almost no bearing on where you fall

If you’re not in the in-group, then you’d be better off leaving.

Great article and spot on comments. Regards Steve

” This is why most large corporations ultimately fail.

Bobber,

I would offer that Corporations eventually fail due to the requirement to exceed quarterly expectations…quarter after quarter. They start cutting fat, then muscle, then come the board members with a friend from Bain Capital or some other cancer from Wall Street.

If you do not move up or are earning significantly more after 2-3 years, then they don’t really like you and you will never get more than the bare minimum. It doesn’t matter how well you perform and how happy you look.

Once in that place, you’re better off rolling that dice again in another job.

The next step is that they move some of their favourites into positions of influence on your project / budget code so they can take their sponsors cost overruns out of your budgets and it will look like you are doing a lousy job since you will be responsible for all the bullshit.

Better quit early.

Happens in software industry all the time. If you don’t make it into some management position by thirtiish , you might just as well look for another profession. By software industry I mean a software house, not a layby semi-government shop.

If Americans worked hard enough we could have an entire economy of ceo’s and executives all hanging off the top of a very tall ladder!

“How’s the weather in your office Johnny?”

“Great! How’s productivity?”

“I don’t know! What’s productivity!?”

Coming soon to a fully automated idiocracy near you!

I just heard one of the largest US banks will be freezing their pension plan and adding the pension contribution to employee’s 401K. For now they are promising to keep the contribution amount the same, let’s see how long that lasts.

An intelligent man knows when the odds are against him, and bails.

Kudos to him.

Would you care hazard a guess, Wolf, as to roughly when the pain might start for the banks, as business loans turn bad?

This will happen when the defaults start rising in a significant way. In the current environment, cash-flow negative companies with deep-junk credit ratings can still issue bonds and leveraged loans without problems, and they can use the proceeds to pay off their bank loans (and borrow more from banks after that). As long as this continues, default rates should stay low.

But the deep-junk credit market has finally started to tighten a tiny bit (I’ll cover that in a little while), and as it tightens, it will make it harder for companies to service bank loans. This will take on momentum next year. This is what the Fed wants to accomplish, and it’s just now getting started. So we should see defaults ticking up next year.

This process is long and drawn out and will likely last several years, with rising loan loss reserves hitting bank earnings quarter after quarter. If it happens “gradually” enough, the Fed will encourage it. If it happens all at once and credit freezes up across the economy, the Fed will try to stop it.

Will you be reporting it when some shadow banking shops start closing shops?

Yes I will. I already covered three small specialized subprime lenders (all of them “shadow banks”) that shut down earlier this year:

https://wolfstreet.com/2018/04/11/how-much-are-banks-exposed-to-subprime-more-than-we-think/

https://wolfstreet.com/2018/04/08/subprime-carmageddon-specialized-lenders-begin-to-collapse/

Wolf,

Might leveraged loans tip the cart over?

These loans are nearly all floating rate tied to 3-month LIBOR. Since LIBOR has gone vertical again (up over 45 basis points in four months) might not be too much longer before leveraged loans begin imploding. If these are mostly cov-light then good luck to investors with recovery efforts.

Last we heard, leveraged loans outstanding at $1.3T which far surpasses the size of the traditional U.S. junk bond market.

Leveraged loans are near the top of Fed’s worry list. Yellen started talking about them in 2014. Since then, the outstanding amount has about doubled. So talking alone doesn’t help. But recently, the appetite for them has been waning.

Leveraged loans, when they go bad, hit the banks only marginally. Most of them are investor owned (as CLOs, in funds, etc). I fully expect some open-end leveraged loan mutual funds to experience a run on the fund and blow up.

Dividend Yields are spiking on the bank loan mutual funds. Take a look at BKLN and LFRAX. I’m not sure if it’s the floating rate coupon or the rise in the real yield causing this, or a combination of both (flat float with rising real yield) but it’s quite dramatic.

Like covenants, addbacks, and the other bells and whistles, the “old way” to do lev lending included mandating the borrower hedge their interest rate exposure (or at least 50% of it) at close, to take the ‘spiking LIBOR’ risk off the table. But that requirement is not in most agreements anymore, it’s up to the borrower.

With covi-lite so prevalent, I think the default rate will stay lower this time through, but by the time a default happens, you’re talking about payment defaults and/or insolvency, so the recovery rates will be much lower, even for senior lenders.

Thanks Wolf, makes sense – alas….

Wolf, have you looked into which large banks are the most exposed to this type of risk or are we looking at the whole industry here? Would be nice to avoid having to rely on a potentially insolvent FDIC too if it all goes south too quickly…

I know it’s not large corporate level, but I’ve been watching some businesses deteriorate here in FL. There has been such a boom in new retail and service companies.

One anecdote: a local restaurant owner has been running two rock solid eateries for several years. Nothing fancy, but always busy and the kind of local fare that becomes an institution. In the past two years he took out loans to build two high end restaurants. During the new site prep, he ran out of funds and took an additional loan with his existing business assets as collateral. Now he’s losing it all. Going from two good businesses to zero.

This is one of a handful of stories that have hit the news lately, after years of nowhere to go but up, up, up. But going down, down, down will be the construction jobs and retail jobs that were part of the credit expansion.

Related to that, one of the new restaurants was to go into this huge new retail development. Construction on that has frozen mid-way with some stores opening and others backing out. There is a large portion of the site that has unfinished concrete structures and the porta-johns have been hauled away. Equipment gone too. Just like 2008-09

Florida will a very interesting study in overbuilding in about 5-15 years. I don’t see how a bunch of these retirement towns exist once these asset-rich boomers have to sell their 5000 sq ft, $1-2M golf course homes. Towns like Naples, Windermere, etc.

So many demographic changes strangle the number of eligible buyers. Smaller sized families, distaste for golf, no discernible sources of gainful employment for younger people, etc. I can easily see these dropping below 50% of peak really quickly.

Thanks to the crapification of private-sector retirement benefits in the last few decades, towns relying on retirees for their economic future are likely to have a bad time.

As Wolf says ‘ some things not right”

Most people I know seem to be in good shape

their money right now.With banks though you do not

know . Their derivative trades and many other situations

that are off book make it impossible to assess risk.

“After the bottom in March 2009, the Fed’s strategies to benefit the banks and those that owned them took hold, at the expense of depositors and other classes of US stake holders, such as renters or future home buyers. And it worked.”

Wolf, could you please explain how this affected renters and future home buyers?

I have learned so much from you. Thank you for sharing your knowledge and insight with the rest of us.

Wolf has written quite a bit about where real estate prices and rents have gone since 2009.

Tip: the answer is not “a recovery followed by a healthy market”. Click on the “Housing Bubble 2” category at the top left to learn more.

Thank you. Putting the details together in the Big Picture is always where I struggle.

CP, the big picture is basically this, and I’ll give you a quick history of everything that happened for us to get to this point.

1907: The bankers engineer a stock market crash and later suggest a central bank as the solution to America’s problems.

December 1913: The Fed is signed into law right before Christmas after being passed by a few members of Congress because everybody else went home. President Woodrow Wilson later regrets signing the bill.

1933: Because of the Great Depression, President Franklin Roosevelt bans gold from being owned by Americans. People are jailed because they will not give up the gold.

1941: The President takes a lead role in getting Japan to attack Pearl Harbor. The ironic thing is that World War II will result in America regaining a relatively healthy economy primarily because Americas are forced to save due to rationing.

1962: Walmart is founded. The company would prove to be a big bully by putting Mom & Pops out of business as well as killing off other regional and nationwide stores. In addition, when Richard Nixon opens China for Business in 1972, Walmart forces companies to close US factories and move production to China and Asia.

November 22, 1963: President Kennedy is killed. Theories as to why he was killed was because he wanted to smash the CIA into a thousand pieces, signed an executive order calling for debt free greenbacks, or he just didn’t want to go to war in Vietnam.

1965: A new law is passed allowing for unlimited immigration into the United States. This along with the rest of LBJ’s great society would prove to be a burden to the country and help kill the middle class. Welfare, Social Security, Medicare, and Medicaid aren’t long term answers.

1971: Richard Nixon takes the country off the Gold Standard which means that the US Dollar will no longer be backed by Gold.

July 1980: The soon to be 40th President Ronald Reagan makes a bad choice in selecting George H. W. Bush as Vice President. The first amnesty is passed in 1986. For the most part, the borders have been opened until recently.

1989-1993: Despite his faults, President Reagan made changes that helped the US economy, but those changes are derailed by President Bush 41 to the point that there is a recession in 1990. In addition, the President ends up signing the jobs killing NAFTA and getting us involved with war in Somalia. Bush 41 ultimately lost reelection because Americans read his lips but discovered new taxes.

1994: President Clinton manages to choke NAFTA through congress to the point it becomes law in the US, Canada, and Mexico. Also, war leads to refugees from Somalia entering the United States.

2001-2009: President Bush 43 presides over the managed decline of the economy while stealing elections though the 2002 midterm was self-inflicted by the Democrats who turned a memorial for Paul Wellstone into a political rally right before the election. The managed decline included the 2008-9 Financial crisis that led to Barack Obama being elected.

2009-2017: The “recovery” engineered under Obama wasn’t a recovery at all. How can it be a recovery when the middle class is dying. Now the bottom is starting to fall out.

Jessy S, I would add two more things to your “history of everything that happened to get us to this point.”

1999: The GLB Act is passed in November essentially repealing the Glass-Steagall Act of 1933. Commercial and investment banking merge together along with securities and insurance companies.

2004: The Securities and Exchange Commission under President George W. Bush, deregulate the debt to equity ratio of five, and only five Wall Street investment banks from 12 to 1 up to 40 to 1. These five are Goldman Sachs, Merrill Lynch, Lehman Brothers, Bear Stearns and Morgan Stanley. The leading, and most influential proponent of this deregulation is Henry M. Paulson, CEO of Goldman Sachs who then succeeded John Snow to be Treasury Secretary in 2006.

It inflated home prices, which requires that future buyers pay more dollars (fruits of their labor) for the same home. In many cases, home prices have moved out of reach for potential first-time buyers. Inflated asset prices have also put upward pressure on rents (though the relationship is not linear).

Yes, people always seem to think lower interest rates benefit the buyers. In reality, they benefit the sellers. Buyers get future consumption strangled for 30 years… Sellers walk away with more money than the home should have commanded under a normal interest rate regime.

Agreed! I would much rather homes be $70k at 12% (financed for 10yr) interest vs $200k at 5% interest (for 30!) First scenario you pay about 58% over list vs 75% in the second scenario (both 20% down).

Expensive money (high rates) means your dollar is valuable.

But… most people don’t look at total cost of ownership vs “how much a month,” which is why places like Rent-A-Center and Aaron’s exist.

Not to worry, knowing the FED board is well paid for all their hard work and although considerably less now, surely there’s still remaining wealth to steal from some target groups?

Excellent article and very interesting comments bringing further material to the discussion.

My sense is that history will repeat

I just don’t think this is correct. The largest banks have been very conservative in the loan policies, and their major customers are the Fortune 100 companies. These companies are not going to fail to pay their bank loans or default on their commercial paper. They may have to suspend share buybacks and cut Capex, but they have the financial strength to stick around.

Large banks learn a lot about how to structure loans when oil prices fell under $30 and a lot of drillers with bank loans got into trouble. Even so, it wasn’t as bad for the banks as everyone feared. Now, they take the riskiest loans and sell them to hedge funds and HY CEFs.

So your thesis suggests that the banks lent loans “responsibly”.

Didn’t the Fed just warn us about the opposite in their Nov. vulnerability report? Other than a flattened yield curve (short term borrowing costs higher) then, why are bank stocks getting hammered? What are we missing?

Vinyl1 is missing the fact that there are so many corporations issuing stock buybacks that the total greed of executives is going to kill the economy. That is before we consider the fact that there is too much debt in circulation.

Wolf, you talk abut banks, but how vulnerable are insurance companies “that have been around over 100 years” with their fixed and variable indexed annuity products?

All you guys who want to trash Bitcoin are going to own it if you live long enough. Well….maybe not the BTC coin itself, but digital assets that use blockchain technology.

The light at the end of that tunnel is a train. You think the money is funny now… Just wait. We’re not at the end. We’re at the beginning.

Let’s look back in a few years. About 30% of HNWI’s surveyed are very interested in owning cryptocurrency, last year’s bubble notwithstanding. Right now it’s the Wild Wild West, and full of scammers. It won’t always be so.

Right now cryptos are in the toilet. Time to learn how they work and where the real opportunities are, as opposed to the bs and hype. They won’t always be in the toilet. But hey, don’t listen. No skin off my nose.

Eddie- I believe crytos or any digital currency still will have the same problems as any paper fiat currency as in they will lose value over time as long as we have central banks controlling the currency.

Changing from paper to digital is less costly as banks can avoid all the counting of the paper going in and out of banks and that is why a move to digital will occur.

Well, they still haven’t reinstated FASB 157-8, that is the real tell

Why would they ?

There was NO outrage, even now with earnings stated in 2 ways – GAAP & Non-GAAP!

No concern any where – regulators, investors or the lawmakers!? B/c they all get benefited with ‘fantasy’ accounting!

Has any, one lawmaker worried about deficit or debt, other than in passing, here and there?

Wolf,

Glad to see this piece.

This observer has been watching $BKX most of the year. The index was conspicuous in being one of the few which failed to surpass its January high (another notable exception being $NYA).

We hear repeated ad infinitum in the MSM that the big banks are in such remarkably better shape than they were in 2008/2009 due to having far less exposure to subprime credit of all forms. All nonsense because the banks simply outsourced this risk to “non-bank entities”. The banks are still on the hook since they’ve funded these non-banks.

Keep in mind that $BKX is not only well below its 200-day MA, the index has been below its 400-day MA for nearly two months. Support is in the 87 to 88 range. If 87 gives way, look out below.

My XLF puts are just doing fine!

Every time there is hopium headlines the puts get cheaper. When the reality descends sell them! rinse & Repeat!

NOT surprised that many are getting the message NOW, about what Fed/CBers have done to the Joe/Jane of the main street favoring wall st all these years!

How will they rescue this 3rd largest ‘everything’ bubble, Wolf?

QEs 4&5 and NRP to infinity?

“How will they rescue this 3rd largest ‘everything’ bubble, Wolf?”

They can’t. But I think they’ll be more inclined to rescue the dollar than hyperinflate it.

Since 2008, millions of former sheeple have become awake and aware of the pernicious role of the Fed and its “No Billionaire Left Behind” monetary policies. I suspect the TBTF banks and their Congressional hirelings will have a much tougher time pushing through the next Wall Street bailout and QE4 given the growing antipathy much of the populace of flyover country has developed for our political and financial elites and their never-ending swindles against the 99%.

Meanwhile, the leveraged loan market is grinding to a halt

https://www.zerohedge.com/news/2018-12-13/wheels-come-leveraged-loan-market-banks-unable-offload-loans-amid-record-outflows

Sadie

Dec 13, 2018 at 3:15 pm

Bitcoin has counterparty risk. Gold has NO counterparty risk. There are no similarities between them.

Bitcoin has counterparty risk? How so. Sadie?

https://www.investopedia.com/articles/optioninvestor/11/understanding-counterparty-risk.asp