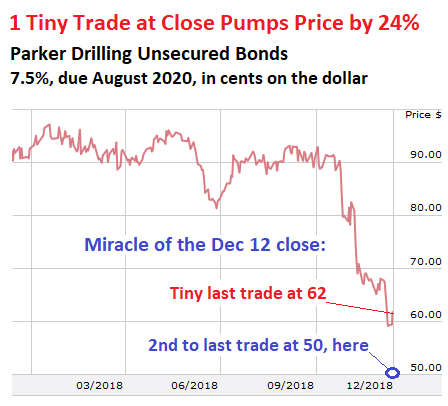

But look how the bonds got manipulated up 24% in one minute at the close.

Parker Drilling announced Wednesday morning that it had filed for a “pre-arranged” chapter 11 bankruptcy. The storied drilling contractor has been in business since 1934. It has been involved in oil fields from Alaska’s Prudhoe Bay and the Siberian Arctic to the Caspian Sea and China, in addition to its work in the US. The company had somehow survived the first Oil Bust this decade (now called “Oil Bust 1,” 2015-2016), but was so weakened that it became one of the first casualties of Oil Bust 2.

The bankruptcy filing was under an agreement with a group of creditors, the company said, with the idea to allow the company to restructure quickly. This is a classic “debt restructuring” under the supervision of a court.

The company listed $691 million in assets. This is down from$869 million in assets in its 10-Q filing with the SEC in November. And it listed $937 million in debts. This includes about $585 million that it owes to unsecured bondholders.

But top executives will be just fine.

We’ll get into more detail in a moment, but to summarize the eternally long agreement with creditors: Existing common shareholders will be almost wiped out. Creditors will get much of the new company along with some new debt. The company will reduce its debt by two-thirds and will get $95 million in new equity capital through a rights offering, which will leave it in better shape than before. And management, instead of being tarred and feathered and driven out of town for having ridden the company to ruin, will be richly reward going forward.

The deal and the filing, though long expected, must have nevertheless come as a surprise to penny-stock chasers because shares today plunged 61% from nearly nothing to even less, closing at 43 cents.

On November 22, Parker Drilling was at the top of my list of 438 stocks traded on the New York Stock Exchange that had plunged between 40% and 94% from their 52-week highs. At the time, shares closed at $1.39. Penny-stock dip chaser seeing a buying opportunity in this “cheap” stock have since been crushed. The shares went from $21 to 43 cents in less than a year.

The largest shareholders, according to the filing, include Saba Capital Management, Brigade Capital Management, Dimension Fund Advisors, and Whitebox Advisors.

A similar fate is befalling quite a few oil-and-gas stocks that have survived Oil Bust 1. Oil Bust 2 may turn out to be merciless because the Fed is now raising rates, and financial conditions are tightening for all companies, and the ensuing shakeout is tripping up weakened survivors of Oil Bust 1 first.

Bondholders started smelling a rat on October 22. For example, the 7.5% senior unsecured notes due in August 2020 traded at around 90 cents on the dollar until October 22, then they began plunging. In November, Parker Drilling warned it might not be able to repay or refinance some of its debts. Bonds plunged further. Over the last couple of days, they traded at below 60 cents on the dollar, according to FINRA/Morningstar data.

1 Tiny Trade pumps bonds 24% at the close today.

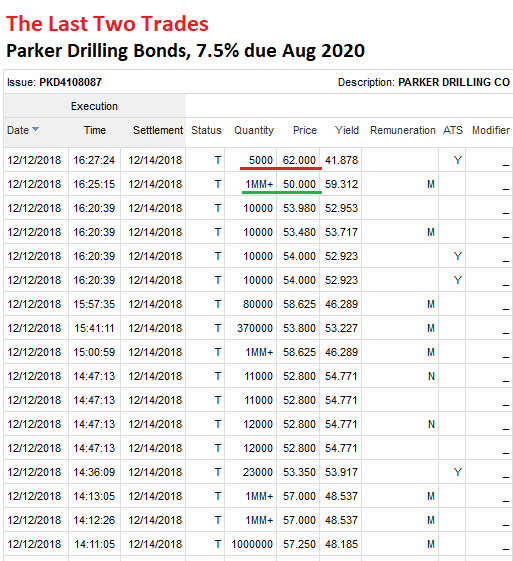

Today, after the bankruptcy filings, trades gyrated wildly allover the place, ranging from 45 cents to 62 cents on the dollar. When you look at the transaction history, you can see how crazy this is – and how profoundly manipulated.

The last tiny trade (underlined in red, below) was at 62 cents on the dollar, executed at 4:27 PM, to be the trade that would show the daily closing price.

But the trade before it, executed at 4:25 PM, was a much larger transaction, at 50 cents on the dollar (underlined in green). Data, table, and chart via FINRA/Morningstar:

Had 50 cents on the dollar been the price of the closing transaction, the chart would have shown the bonds to have plunged nearly 20% today to 50 cents on the dollar. But thanks to the tiny last-moment trade at 62 cents, which pushed up the price for everyone by 24% in a single stroke, the chart shows a gain. I have marked the last trade at 62 and the second to last trade at 50. Go figure!

Ironically, Moody’s still rates these bonds Caa2; Standard& Poor’s rates them even higher, B-, both in deep junk but well above “default” (my cheat sheet on credit ratings)

Who gets what? The #1 Issue in Bankruptcy Court.

Existing common shares and existing preferred shares will be cancelled. Their holders will get some crumbs and can participate in the rights offering by buying rights to the New Common Shares to be issued. Here is what the company said the Capital Stock of New Company will be, post-closing, on a fully-diluted basis (rounded). I highlighted the common stock:

New Company Capital Stock:

- Rights Offering (see below): 41.9%;

- Put Option Equity Premium: 3.4%;

- Converted 2020 Notes: 18.8%;

- Converted 2022 Notes: 34.4%;

- Existing Preferred Stock: 0.6%;

- Existing Common Stock: 0.9%.

Of the New Common Stock offered in the Rights Offering:

- Holders of unsecured notes can purchase up to 63.2%;

- Holders of existing common stock can purchase up to 22.1%;

- Holders of existing preferred stock can purchase up to 14.7%.

Holders of existing common stock will also receive 60% of the new warrants, and holders of existing preferred will receive 40% of the new warrants. At this point, no one knows if these warrants will ever have any value.

But you gotta take care of your own.

The executives, having ridden the company into bankruptcy, will be retained and richly compensated going forward. For example, Chairman and CEO Gary Rich: He became CEO in October 2012 and Chairman in May 2014. He negotiated for himself an annual base salary of $745,000 with an annual bonus of $1.49 million, plus a target bonus, plus 49.8% of the Incentive Equity Pool exclusively set up for a handful of executives.

This Equity Incentive Pool will get “no less than” 9% of the New Common Stock. Up to 40% of this pool will be issued to the participating executives as restricted stock of the new company and up to 60% will be issued as non-qualified stock options in the new company.

The company expects to emerge from bankruptcy protection in early 2019. The restructuring plan is subject to court approval and stakeholder approval.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

->But look how the bonds got manipulated up 24% in one minute at the close.

I don’t suppose any fraud investigation will be forthcoming.

Nah!

->The executives, having ridden the company into bankruptcy, will be retained and richly compensated going forward.

Because it’s so much easier to ruin a company for fun and profit than to manage it successfully.

Rewarding failure clearly means the incentives are backwards. I don’t suppose any fraud investigation will be forthcoming.

Nah!

People who are avariciously stupid enough to speculate on this sort of thing deserve to live in a cardboard box. Presumably these companies exist to provide tax write-offs against their profitable ‘investments’.

Is there any part of the US economy or global economy that is operated ethically? Or is that a bad question?

Of course not. It is a giant Ponzi, and when it goes we will all go with it.

” …when it goes we will all go with it.”

I guess that depends who is included as “we”.

There are those who have arranged their lives to be quite independent of financial markets, providing for themselves with privately held capital, such as productive land. Everybody will be hurt, sure, but some will not have to “go with it”.

Reminds me of Major Major’s father from CATCH-22. At least I think it was Major Major’s father. The one who was employed by company owners to run companies into the ground for profit.

And I thought it was fiction!

“Major Major’s father was a sober God-fearing man whose idea of a good joke was to lie about his age. He was a long-limbed farmer, a God-fearing, freedom-loving, law-abiding rugged individualist who held that federal aid to anyone but farmers was creeping socialism. He advocated thrift and hard work and disapproved of loose women who turned him down.”

If I recall correctly during Oil Bust One (i.e. the frackers) the Fed asked some banks to put off foreclosing and go as easy as possible.

I guess this was part of a QE- type approach. At least with Parker this help was not available or did not need to be repeated. No doubt the pre-packaged 13 was nice and tidy and the company will keep operating.

Also the overall economy is supposedly stronger than in 2015.

If these low prices get worse ( one large outfit is saying $20 is possible in 2019) it remains to be seen whether some suasion by the Fed will be applied again. (Assuming I’m recalling correctly and this ever happened)

Your recollection is correct. Did you think helicopter money meant throwing money off a helicopter? Besides, being a net oil exporter raises the morale of the people. /s

Good thing it’s extremely lightly held:

https://www.etf.com/stock/PKD

Waiting for the big one.

Thanks for the tip. This is a great shortcut to finding ETF ownership.

Well it’s nice to know that one of the largest shareholders is Saba Capital Management which, according to their website, “Is An Alternative Investment Firm Focused On Credit And Equity Relative Value Investing” – whatever the hell that means.

It means all your money gets transferred to them, it does state “An Alternative Investment Firm….”

Weatherford may be next. Currently trading at $.46 cents with $8B debt and negative book value.

Goodfellas Inc. does the same thing to restaurants after they sell all the stock too. By now it’s a classic tried & true method repeated all over North America every time a small business venture spirals out of control financially.

Interesting how the oil drillers can go bankrupt but students with Student Loans cannot. Better to be a driller than a scholar too. The ROI is much better too.

MOU

This should have happened over a year ago, the shale oil scam really has been making oil a losing business save in places were shale oil is not easily available or were protectionism does work.

Wolf, how about a recap report about how shale oil sank the oil business?

Shale oil is a national security strategic plan. It will continue even if fails to make money. Anyone note the recent run up in natural gas price?. Totally inexplicable except from a standpoint of helping out the frackers; particularly as oil pricing cratered.

There may be more of these bankruptcy filings but rest assured that fracking will continue, including the forthcoming new round of QE.

What does this mean for the group? Technically the XES broke down last week, with no objective bottom. The recessionary dominoes are lining up. There is a correlation between banks and energy companies? When the Fed caused Oil bust one by holding rates too low too long, they set up OB2, but in normalization the Fed was really too accommodative after all? They couldn’t tighten up the junk market enough to put a bid under energy, and now they are going to lower rates into the maelstrom? So far the markets have been right about interest rates and have called the Feds bluff at every turn. The only caveat is LIBOR which is signalling a credit crisis. That should be the end of this group one fears.

Wolf, what service or broker do you use to get the intraday bond trade data? I mean the intraday price graph and the “Time and Sales” tables?

The bond market is notoriously opaque — any tips on the best way to get these kind of data is very useful for the small investor.

FINRA (in conjunction with Morningstar) publishes this data now. This is new, part of the effort to bring more transparency to the bond market. Kudos.

@Wolf, thank you, very good info. I have also been digging around for a site that will generate a list of bond “issue names” and/or CUSIPs from a stock symbol. Looking up bonds by company name is cumbersome and also often seems to produce matches for multiple companies at the same time. There must be a better way?

My contribution: Vanguard accounts can look up bonds using the underlying common stock symbols. Then copy/paste the CUSIP into the FINRA/Morningstar site for intraday prices.

If you know anything about the oil business then you know that the cycle of boom and bust has been going on in this industry for well over a hundred years. I believe that market share for EV’s in the US is around 2% and I seriously doubt that that this cycle will abate anytime soon. This is an unfortunate event for Parker and the the workers in the oil fields in our country and I agree with Wolf that this may be the beginning of something bigger. Interesting times for sure.

“The restructuring plan is subject to court approval and stakeholder approval.”

Are the stockholders “stakeholders”? If so, have they any leverage at all to improve their treatment?

Yes, stockholders have the right to turn down the offer. If they do, they don’t get anything (zero), and the remaining stakeholders will get their share. It’s that simple. The document is very explicit about it.

In a bankruptcy, stockholders have no rights. Bankruptcy is the legal process of transferring ownership from stockholders to creditors. It’s the legal process by which stockholders are being expropriated, and creditors get the company or the assets.

Dumb questions:

Do drillers such as PD buy oil leases to drill?

Are these valued based on per barrel oil prices?

Do they borrow using leaseholds as collateral?

If so, had oil been at $75 or more, would they still be in bankruptcy?

Just asking.

“at the top of my list of 438 stocks”

Mr Richter, thank you for the extensive compilation, of

which I reviewed each and every stock as a possible investment

going forward. I culled about some 50 stocks and placed

them on my further review and watch list.

Parker Drilling one them?

But-t-t-t didn’t I just read that the USA was now truly energy independent? That fracking has been so successful that we are now a net exporter? That the reserve estimates for the Permian have been more than doubled?

I recently had an instructive conversation with a retired oil fracker executive from Houston. When I raised issues like 1 year half life depreciation rates and capital intensive and interest rate drilling dependency his final rejoinder was “it’s a big world.” Evidently it no longer matters where you drill for tight oil — as long as you have enough aircraft carriers to enforce your right to drill.

Unfortunately there is still a real world out there. That is the one where a single glacier in Antarctica containing enough ice to raise the sea level 12 feet has started racing at a gallop toward the sea. One in which the Glacier Park I recently hiked through has virtually no glaciers left. One in which the Arctic permafrost is melting rapidly and releasing methane which is 20 times more effective than Co2 as a greenhouse gas. One in which the fire ecology in California has shifted toward the extreme fire side of the dial. One in which vertebrate species loss and extinction is proceeding at the fastest rate since the last giant meteor impact.

“Let them eat fracking” said the Texas Queen