One after the other, individual stocks are getting crushed.

It was an ugly Monday and Tuesday followed by a Wednesday that at first look like a real bounce but ended with the indices giving up their gains. This was followed, mercifully, by Thursday when markets were closed, which was followed unmercifully by Friday, during which the whole schmear came unglued again.

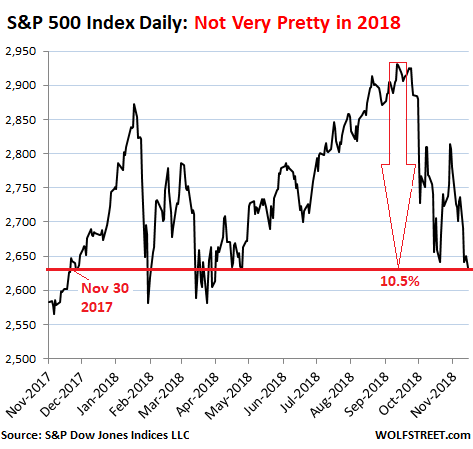

The S&P 500 index dropped 0.7% on Friday to 2,632 and 3.8% for Thanksgiving week, though this week is usually – by calendar black-magic – a good week, according to the Wall Street Journal: During Thanksgiving weeks going back a decade, the S&P 500 rose on average 1.3%.

This leaves the S&P 500 index 1.5% in the hole year-to-date. It’s now back where it had first been on November 30, 2017:

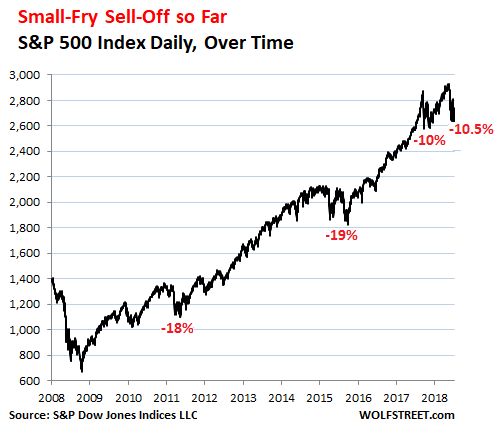

Clearly, when seen over the longer term, the sell-off for now still belongs to the small-fry among sell-offs, with S&P 500 down just 10.5% from its peak:

The Dow dropped 0.7% on Friday and 4.4% during Thanksgiving week, to 24,286. It’s 1.75% in the hole for the year. Technically speaking, it’s not even in a correction, being down only 9.9% from its peak.

And the Nasdaq, dropped 0.5% on Friday and 4.3% during Thanksgiving week. According to the Wall Street Journal, during Thanksgiving week over the past 20 years, the Nasdaq rose on average 1.3%. So this is no good for calendar-black-magic aficionados. Where’s the free-wheeling holiday spirit?

The Nasdaq is now down 14.7% from its peak at the end of August but remains up 0.5% year-to-date.

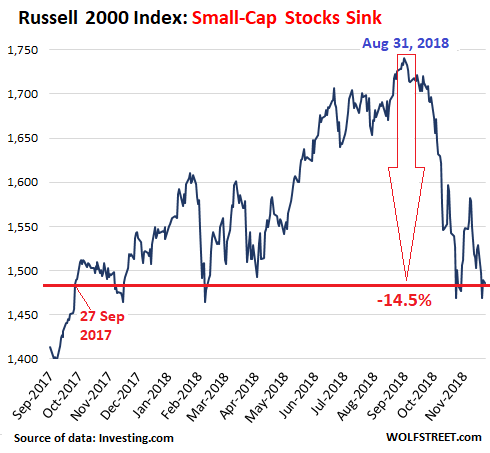

The Russell 2000 small-caps index edged down today and is down 14.5% from its peak on August 31. It’s 3% in the hole year-to-date and right back where it had first been on September 27, 2017:

These indices are unwinding little-by-little. And the fact that they’re barely in the red for the year, or in Nasdaq’s case still up a tiny bit, is a gruesome sight in November the likes of which a whole generation of stock market jockeys has never seen before and finds utterly outrageous.

They and their TV-personality allies – along with the professional crybabies on Wall Street – are already wailing and gnashing their teeth, and are clamoring for the Fed to reverse the rate hikes and stop the QE unwind to end this shocking and appalling phenomenon.

But there is considerable destruction going on beneath the surface, and investors who were overweighed these stocks are finding themselves with stiff losses – and if they were leveraged, may have already faced margin calls. Yesterday I covered the 438 stocks on the NYSE that have already plunged 40%-94% from their 52-week highs, including some very big names. Today, I’ll take a look at the biggest names on the Nasdaq.

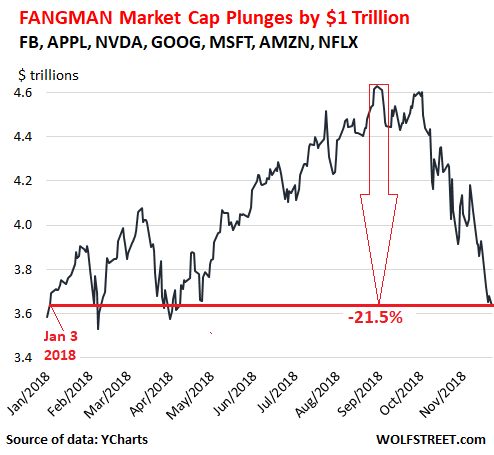

The seven FANGMAN stocks – Facebook, Amazon, Netflix, Google’s parent Alphabet, Microsoft, Apple, and NVIDIA – fell 1.3% on Friday in combined market cap. Over Thanksgiving week, they have now plunged 6.7%, or by $259 billion. Those are real dollars gone in four trading days with just seven stocks.

Since their combined market-cap peak of $4.63 trillion at the end of August, nearly $1 trillion — $994 billion to be precise – has dissolved into ambient air, as their combined market cap has plunged 21.5% in ca. 12 weeks (data via YCharts):

But if you look at them as individual stocks, it’s even worse. The saving grace for the group as a whole was Microsoft, the second largest stock by market cap, which is threatening to become the largest stock shortly if Apple continues to fall at this pace. Three of the seven have already plunged by 38% to nearly 50%. Two more have plunged by 26% to 27%. Only two have dropped by less than 20%.

These are the market cap and percentage losses for each of the FANGMAN stocks from their respective peaks:

- Facebook [FB]: -$250 billion (-39.8%)

- Amazon [AMZN]: -$255.3 billion (-25.7%)

- Netflix [NFLX]: -$69.5 billion (-38.2%)

- Google [GOOG]: -$170.2 billion (-19.3%)

- Microsoft [MSFT]: -$92.5 billion (-10.5%)

- Apple [AAPL]: -$304 billion (-27.1%)

- NVIDIA [NVDA]: -$87.4 billion (-49.7%).

Added together, these price drops of each FANGMAN stock from its individual peak balloon to $1.23 trillion.

But even at these prices, the FANGMAN stocks are still vastly over-inflated. This is what you get after a huge run-up that lasted for so many years: There is a lot of air beneath them before prices make sense on a fundamental basis.

The pain is in some of the details beneath the surface. Overall nothing serious has happened yet. The S&P 500 has not yet unwound several years of gains. It’s working on unwinding one year of gains, and that’s as far has it has gotten at this point.

There is a large amount of money waiting in special funds to jump into the fray when the sell-off of particular shares or the market overall reaches certain levels. Get in, make a buck, get out. Dip buying is a huge thing, and will continue to be. It’s driven by humans and algos – and by companies buying back their own shares at strategic moments to push their prices back up. These dynamics will continue, sell-offs followed by dip-buying, followed by sell-offs that will “gradually” – as the Fed would likely say – wring the excesses out of the market, possibly for years to come, even as individual stocks, one after the other, get destroyed.

It gets serious. Margin calls? Read… Stock-Market Margin Debt Plunges Most Since Lehman Moment

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What’s the old saying about how you go bankrupt….it starts slowly but then goes really really quickly?

“Gradually, then suddenly.” It’s in ‘The Sun also Rises’ by Ernest Hemingway.

My favorite so far is: “In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” -Kenneth Rogoff

Like

Prices on things go up when there are more buyers than sellers. They go down when there’s more sellers than buyers.

My investment thesis is that the runup during Q2-Q3 was fueled by stock buybacks using leveraged funds and repatriated earnings. That fuel is loooooog gone. QE is unwinding everywhere. Global slowdown.

Yeah, the Bank of America analyst who predicted SP 3000 this morning was smoking some quality stuff.

Finding a bank analyst to give a ridiculously bullish forecast is not exactly difficult.

I would agree with him. The Feds tightening is nothing compared with global monetary accommodation in the aggregate. Should business conditions in the US deteriorate, (no signs of that) that still has to weighed against global conditions, and the various carry trades, (SNB buying stocks). The US has been a hot money destination and hot money is notoriously fickle. However as Wolf points out many of those stocks are ADRs, the NYSE is a pass through for foreign investment. The Trump plan can only work if those $10 hour jobs returning to the US are backstopped by universal healthcare, and various other government subsidies. (so lets attack immigration) With a crude US political consensus, global money printing, and global economic expansion, the markets could manage new highs. They outlaw FB in China. There are solutions to problems that would lift the market. There are plenty of near term obstacles too.

debts and deficits dont matter, we’ve seen this since 9/11 and especially in Iraq War 2 and then the 08 Bush crash 09 Obama stimulus and most recently in the 2017 Trump Tax Cut; a government issuing a fiat currency in a floating rate environment need never incur any public debt.

meaning, dick cheney was right, it can print whatever it wants; in theory; in practice, that government needs to back that float with something, like say oil backed by a war machine.

There is still massive demand for the old dollar. In fact, I’d say we’re on the knife’s edge of a dollar shortage. eurodollar market is broken, the more debtors unwind the more the dollar shortage.

my point is, they have no qualms about restarting QE; like Lucas Joyner, NYFED just wants some room. I can easily see SPX3k by end of 2019.

One cannot sell if there’s no buyer. A seller becomes a seller if the sale’s done. Ergo…. (You’re wrong).

Actually’ on the NYE there is always a buyer. They are called “specialists.” Each stock has one. Each specialist gets a seat on the exchange. His job is to manage the buy and sell orders smoothly. He sets the price for any given stocks at any point in time. Specialists themselves can either blow-up and be out of business, or become fabulously wealthy. As part of their priviliged position they are required to buy any orders themselves when there are no buyers. But they do set the price. And raise or lower prices to suit themselves, and market conditions.

Thanks for sharing. But I doubt it’s as neat as you describe: They couldnt set the price if they’re to blow themselves up.

I think the “specialist” went the way of the dodo bird some time ago. They used to man the posts on the floor of the NYSE. But now, the trading is mostly done by computers, and I doubt whether they are programmed to ensure “orderly markets” when things get difficult. In fact, I suspect the algos will simply back away completely.

Dollar still screaming higher….

The Euro is STILL going lower.

Currencies may all be bad… but the USD is the least bad of the lot.

As Wolf noted in another comment happened to him, I also lost a lot of money expecting a dramatic price decline. However, I agree.

Given the high PE ratios, except for stocks that may have some future potential to expand in select markets internationally to sell in other countries like Amazon might in allies like the Philippines, I cannot see US stock prices maintaining the regular increases they enjoyed for years. Stock buybacks will become harder to finance due to the QE unwind.

Inflation will cause modest price increases. International wars may make investors in that area flee to our stock markets. However, I do not think that will last.

Global climate instability and net warming, which a certain ill informed leader of the rich does not realize can actually result in massive cooling off of parts of North America and northern Europe, will hurt us massively. The latest climate report describes what will happen.

Like other aspects of our lives, unless there is some unexpected, beneficial invention, like Fusion or true (safe) AI or a battery or solar energy breakthrough, the damage from climate and poor K through 12 education system in US will bring our economy down. I do not predict a collapse but something like what Greece and the old Soviet Union suffered.

The furher of the rich is right to retaliate against China but does not know what he is doing as to most, important issues. A border wall will only bar people that might have picked our fruit or cleaned our homes or watched our children. It is a stupid, racist, pretend solution to our problems, like a bully safely picking on the skinny kid with glasses or who is different somehow

It’s lazy to dismiss concerns about immigration to the U.S. as “racist”. There are legitimate questions about downward pressure on wages, increased competition for housing (low end) and external costs to the public (education, healthcare, etc). When the local chambers of commerce and major home builders are the loudest cheerleaders for “immigration reform”, it should be a red flag to us all.

Yes, the wall is a silly political sop to Trump’s base, but a thoughtful debate about ‘who’ and ‘how many’ we admit to this country is only sensible.

Chain immigration is a problem. I know of older people from Vietnam who married off their 23 year old daughter to a ugly, 47 year old to come here and live off the government, like their uncle. Chain immgration allows that.

However, the people being targeted by the wall and Trump’s tirades are those who perform humble services that Americans do not want to perform. I saw some of them living in tents in the fields and often cheated of their earnngs.

Without them our fruit growers are in BIG trouble. As to housing for low income persons and schools, we already have huge problems which the furher of the rich will not address.

There is little low income housing and too many incentives enacted are tax scams for RE developers. Schools in rich areas get more funding than necessary and schools in poor areas suffer with little funding… Kids must still share textbooks in some.

Those will be tomorrow’s wage earners, if they can overcome some of the world’s worst schools. Norwegians do not want to come here en masse as the furher urges.

Even low income workers are useful to the economy. Watch Japan suffer now and in future years the economic effects of racism due to its excluding immigrants and thus preventing economic growth due to the economic pressure the rich banksters and other crooks put on our and their population, so they must have fewer children to survive.

The problems in the US are caused by crooked, tax evading people at the top not some poor immigrants at the bottom

What the Soviet Union suffered was most definitely a collapse.

If you want to delve into the gory details you should google Dimitry Orlov.

I agree as to the Soviets. I just did not want to be seen as trying to spook people. What we should realize is that much of our workers now work low wage jobs.

Another sector works even lower wage jobs: which is all that they can get without papers. We should keep in mind that these people are coming here, because farmers and other hired their neighbors or relatives and they know that they can find humble jobs here.

If those undesirable employers with jobs in gardening or picking fruit, etc., were not seeking workers without papers to pay them the minimum possible, those people would not come here no matter what the conditions back home.

As to what is going on with the people on the border, there is a good source for information: https://www.yahoo.com/entertainment/bear-responsibility-conditions-honduras-causing-204500302.html

It is sad that politicians are distracting us from our real economic problems, the free money to the banksters in the form of Fed. (now maybe paid only for treasury rolling over) commissions, ultra low interest rate loans to banks with risky investments, and fractional reserve banking, by picking on the helpless, who are in hopeless conditions and are only coming here to do the humblest possible jobs. Most do not apply for benefits, government because they are scared of immigration authorities.

I have met some, because I handled a few cases dealing with people cheated of their overtime and a small portion of the security guard employees were illegal. Their job conditions were pitiful.

Before we resent these people for “taking away jobs,” we should bear in mind that the jobs that they perform here are jobs that none of us would want. They are not “taking away” desirable jobs.

Those security guards were a good example. They were not allowed to sleep and paid below minimum wage, without overtime. They were so poor and humble that many were just happy to have a roof over their heads: in that case, an unheated shack in which they might sleep a few hours a night, when their bosses were not watching.

Most dogs are treated better here. Without papers, we could not even help them in the class action lawsuit, even though they had been cheated for years. They were too afraid.

US treasury borrowings have been ramping up in Q4. The stock market has been tracking the ebb and flows in US treasury supply for nearly a year and the gradually diminishing flow of QE from Europe and Japan. The two big rallies were kicked off in December 2017 and April 2018 from large pay-downs in treasury debt due to tax collections.

The stock market is wholly overvalued as part of the “everything bubble” Wolfe has written about, the overvalued asset classes need to continue rotting away and correcting itself. The real issue is that of the savings of regular individuals which are dissolving into ambient air as Wolfe says.

” It’s now back where it had first been on November 30, 2018:”,..small typo in a sea of numbers,..to be expected with the vast crunching that Wolf presents.

Keep up the great work!

Thanks. Fixed.

Small typo in the third paragraph…

“It’s now back where it had first been on November 30, 2018”

Should be:

“It’s now back where it had first been on November 30, 2017”

Thanks. Fixed.

The article makes more sense now…

“But even at these prices, the FANGMAN stocks are still vastly over-inflated. This is what you get after a huge run-up that lasted for so many years: There is a lot of air beneath them before prices make sense on a fundamental basis.”

The entire “Trump bump” in all of the equity indices (Dec 2016-Aug 2018) looks very artificial and odd from a statistical perspective. It’s an incredible real life example of a bubble within a bubble. Greed has no limits……

The logic 101 solution goes that the Trump “Dump” will be an inverse stock market reaction. Assuming the “Bump” was real in the first place. Jim Rickards told his clients to sell stocks when he got the clue that Trump would be elected. He was half right. Everyone misses the benign nature of the global backdrop and the ease with which money moves around the globe. I always assume greed is a personal matter, Exploitation and profits are a matter of corporate efficiency at the macroeconomic level. The markets have gotten so large that the individual (and greed) has been crowded out.

After 10 years of saving 401Ks in all kinds of funds, people walked into the stawks very orderly. Every year, they put their 17.5K 401K and 5K IRA, year after year like clock work. Then Wolf says “Fire! pleas exit orderly!” So John politely says to Dave, “so sell first, after you sell and price drop 5%, I will sell in an orderly matter, everybody is in a line and the lady guy sells when price drop by half. Pre determined, orderly.

Don’t get me started on what a swindle 401ks are. You’ll never hear the end of it.

How about starting… Aside from the fees that are charged every-which-way, are there other swindles??

How about the 10% ripoff penalty if you should ever need your own money in an emergency?

I think the 401k/IRA by itself isn’t fraudulent, since a participant could just invest in cash or government fixed income. I think combining the 401k, mutual funds, and the population demographics post 1950 turned the stock market into a literal pyramid scheme.

Part of this unwind is that 2017 was Peak 401k, with outflows > inflows going forward. I think future projections of the delta will undershoot, given how fast uBerfication of employment is occurring.

Rowen, “uBerfication”, good term. It’s the next iteration of moving human labor further into the hands of management. It’s another step beyond Taylor’s “Time Motion Studies” that effectively automated human work.

How far behind will human reproduction be? You know, it’s not as efficient as it could be…

I agree. Profits are negative if we fully consider the costs. Economists should intervene asap to deal with such waste.

Tangential, at least, to this discussion:

https://www.commonwealthclub.org/events/2018-10-16/reid-hoffman-secrets-blitzscaling

(or google ‘blitzscaling;’ you’ll probably be hearing this term a lot in the near future)

TLDR: Whoever builds the biggest monopoly first, wins.

I had a hazy plan about retiring in my mid-to-late 50’s, this was around 2006-2007 before the GFC. In doing research one of the topics was the retirement of the Baby Boom generation in the coming years and how that might have a devastating effect on the stock market as boomers started to cash in their 401k stocks, “en masse”. It seemed like a reasonable concern at the time. Now, over a decade later, what can we say about Baby Boomers cashing in on 401k assets. I haven’t run across many articles on this post-GFC. Maybe it was a big nothing-burger ala legitimate concerns regarding Y2k. Or maybe this has dropped below the radar and could re-surface and catch people by “surprise”. Mr. Wolf Richter, did you ever look into this concern at that time and how might it look now. Are Baby Boomers still at risk in their 401k stock investments or did they get washed away in the GFC?

I’m a boomer. I’m young and active. I hate the idea of retirement. I just started this business in 2011, from nothing. It’s doing great. I’m not the only boomer out there who is still professionally active. Boomers retiring at 60 is overhyped. Sure, some do, and good for them, but many don’t. And many cannot afford to. Eventually, we will all die, and millennials will get our stuff, but as a group, we’re not checking out just yet.

I very clearly remember the market pundits bringing up the regular 401k contributions during the 2000 bubble. They said there was no limit to how far the market would rise because new 401k money needed to find a home every two weeks.

I guess they were wrong. The precious internet stocks lost more than 80% of their value.

Warren Buffett owns more than 250 million shares of Apple (as reported in Berkshire’s latest holdings filing at the SEC). Depending on Apple’s stock price, he lost between $4 billion and $3.7 billion on paper. Pocket change for him but a blow to his ego. Double blow as he had been saying for decades that he’d rather stay away from technology companies. Had he listened to his own advice he’d be better off today. First it was IBM. Now Apple.

Having said that, most of Berkshire’s traditional investments are still doing quite well. And considering that Berkshire’s cash pile is higher than Scrooge McDuck’s, it’s fair to predict that in 2019 he will be buying Berkshire shares by the truckload.

I remember a few years looking class A Berkshire shares just for fun when they were selling for about 250K per share, recently they’ve increased to 300K per share, talk about absurdity.

BRK is the highest percent of cash it has ever been. Buffett et all are the all time market timers of non-market timers. The media makes sure we only pay attention to the equity portion of BRK. Traditionally, when BRK spend that cash load, it takes them years, not just a few months out.

The financial advisor says”Nobody can time the market.” I say “Buffet has a lot of cash”. Advisor replies “nobody is Warren Buffet and nobody should invest like Buffet especially YOU!” I then was humbled and told myself probability I should just save everything in Stawks and pray and 40 years later I will be fine. Although this all in and hold and hold and hold makes sense, my speculator blood is still telling me that is NOT the right thing to do. There is still an instinct drive to taste the blood of the market, and I know this may very likely make me taste my own blood in the end. But hey, you only live once, got to taste some. And for that dose of emotions, I will likely be Buffet’s victim. I long for the world turning into a jungle where I can run and hunt better than Buffet. But today, the world is a market and a casino. Survival of the fittest.

Not a casino; it’s rigged…

Actually, the “market” seems to be in its last stage of openly importing the traditional government ploy to socialize losses and privatize profits…

Look back at BRK 15 years ago with dividends reinvested, and you will see BRK beat the SP500 by 1% per annum over that period. The media hypes Buffett well beyond that reality because that reality doesn’t make the confirmation bias article that Buffett is a genius. His genius ended decades ago. He is no longer the “dangerous hunter” to fear. Your greatest competition in investing is yourself.

The Oracle of Omaha likely invested in Apple as a favour to juice their backing due to low growth. He bought those shares recently too.

Everyone calls him when they can’t find a backer.

MOU

It is quite possible that investments more closely aligned with what one would call “Main Street” will do significantly better than those more closely aligned with “Wall Street,” which now do not reflect the U.S. economic situation, being, rather, aligned with “international” interests.

Um….Apple has almost $300 billion cash reserves. They’re no IBM.

Had almost $300B cash. Between stock buy backs and special divvies, that number is 60ish. Meanwhile, its debt (albeit long-term) is 110ish.

It’s worth remembering that good ole grandpa Warren is also a primary shareholder of WellsFraudco. Looking back on his investing success, a cynical person might conclude he’s simply a highly successful con man with a well-scripted PR department.

Buffet is either manipulating the market (lots of insider info is spinning around, but I am not familiar with them…) or this was the way he lost the lowest amount.

I now work at a savings bank (after retirement from the auto business) and we specialize in “high yield” CDs with a very conservative (lower risk-higher yield) loan portfolio. We have customers turning over portions of their equity portfolio to purchasde CDs. We have a 2.75% yield on a 12 month with minimum $500 to open. The majority of our clientele is 70+ years old. Quite a number of them have sizable assets. They like safety of principal Liquidity (fees may apply), and a decent yield. Stocks have fees, variable liquidity, and uncertain gain after the fees and taxes.

I must admit that, other than some shares earned or awarded years ago, I am out of the market completely since August. I know I lost some, but I am earning a safe return and I am 68+.

“I am more concerned with the return of my money than the return on my money.”— Will Rogers.

Stocks have dropped so much, but it has had zero impact on the real economy. This tells me the only ones getting hurt are on Wall Street or are savers with too much wealth. Why else would anyone own stocks now. They have money to gamble. I don’t feel sorry for any of them. They knew the risks.

Stock declines, even steep ones, alone are not enough to cause a crisis; those declines have to coincide with cascading losses in the credit markets.

Highly leveraged funds, banks, commercial/industrial companies and retail investors have to be simultaneously over-indebted as prices fall, in order to have a real financial crisis.

Which is what’s going to happen, especially with companies that borrowed billions, which will have to be re-financed at higher rates – to goose their now-declining stock prices.

Correct. The difference between 2008 is that equities aren’t packaged into securities (i.e. MBS) that counted towards a capital requirements.

That is, unless the bleed-off in equities starts affecting the real economy.

Why waste time yammering about QE, Fed balance sheets & interest rates? What’s the point? The Plunge Protection Team just needs a new algo – Stocks can only go up never down. Problem solved.

I guess they are on a coffee break, at least as far as the 500 stocks that have already fallen more than 50%.

The global economy is slowing and the fall of oil prices signals this fact. Sure maybe the Saudis’ cut production but this is the same as buying back stocks, as prices rise, but this is an illusion, built on what fundamental. But if the Saudis’ cut production they may find they will sell less oil.

Wolf is correct the stock market will slowly fall as QE is reversed.

And yes the die hard Wall Street boys will try to come up with some story to keep the suckers in stocks. Inflation did not follow QE to Main Street as much as it did to within the canyons of Wall Street.

When the products of trade are used to trade paper built on this trading by 4 fold, one can see Wall Street’s focus is no longer supporting capitalism but their own greedy trading of paper assets.

Bingo, LE.

“They and their TV-personality allies – along with the professional crybabies on Wall Street – are already wailing and gnashing their teeth, and are clamoring for the Fed to reverse the rate hikes and stop the QE unwind to end this shocking and appalling phenomenon.”

Nothing much of substance has happened yet and the wailing is already reaching a crescendo. It would appear that for these scoundrels their friend and benefactor, the Fed, is their to ONLY ensure their profiteering.

And the Fed is not immune to these cry-babies’ wailing. Couple of them have come out of the woodwork. Clarida and Evans.

Let the selling really get going then we will see if the Fed has the BALLS to stand up to the cry-babies. IMO, the Fed will fold up as is their wont.

KPL said:

“And the Fed is not immune to these cry-babies’ wailing. Couple of them have come out of the woodwork. Clarida and Evans.”

I agree. The Fed will buckle and return to it’s long established policy of crushing working people and transferring working people’s income to provide super massive Welfare for the Ultra Rich.

The Fed will stop it’s interest rate hikes.

Wolf is wrong. The Fed will side with the Ultra Rich and against working people. Always.

Timbers,

“Wolf is wrong. The Fed will side with the Ultra Rich and against working people. Always.”

Hahahahaha… that’s the funniest accusation I’ve heard all day, and I’ve been on the internet for already two hours. When did I EVER say that the Fed would side with “working people?”

Quite the contrary. I’ve always said that the Fed doesn’t give a hoot about you or me or other working people — and that Warren Buffett was the single biggest beneficiary of the Fed’s bailouts, QE, and ZIRP. I don’t say it every day because it’s old hat and I’d sound like a broken record.

But now the Fed is going in the opposite direction, not to help the working people, oh no!

The folks at the Fed have their priorities, and you and me, we are not their priorities. But I do try to figure out what those priorities are and what the Fed will do because it has huge consequences.

One of the priorities of the Fed is maintaining the supply of cheap labor – by keeping wage inflation below consumer price inflation – thus tamping down real wage increases of the lower 60% on the income scale. That’s why the Fed pays so much attention to wage increases. It’s in all their communications.

Another priority is consumer price inflation. The Fed doesn’t want inflation to get out of control because it would wipe out the financial wealth (purchasing power) of the richest, and because a high rate of inflation has very negative effects on the economy as well.

And the Fed doesn’t want the financial system (banks) to collapse again. So it’s tamping down on asset price inflation, because these assets are collateral for the banks, and inflated collateral prices put the banks at risk. So now the Fed is targeting inflated asset prices for that reason. This is a key thing to understand. I’ve been saying it for over two years, and it’s coming to pass.

It has other priorities too. And some of those priorities shift as the people at the Fed change. Close your eyes to the Fed at your own risk.

Here is some insight from Fed insiders (Greenspan, Lindsey, Fisher) as to what Powell is trying to do –namely, forestall a much greater crisis than a correction or even a bear market — and why Wolf is probably right that the Fed won’t change course soon.

The link:

https://www.bloomberg.com/news/videos/2015-05-19/greenspan-fisher-lindsey-on-interest-rates-economy

Excellent synopsis of their behaviour. What I see as prime motive is rate normalization which would help Joe Mainstreet save at the bank if the fundamentals of banking were normalized once again.

The unfortunate aspect is that the USA has morphed into Japan with respect to deficit & GDP. Rate normalization is only a dream now that assets are deflating within merely a short timeframe of the introduction of QT.

We all know that the naked swimmers are going to be corporate this leg down. And as soon as they topple we are looking at the knock-on of increased unemployment for the let go employees and we are looking at increased listings with no corresponding buyers because assets are priced out-of-the-market more than they were before QE even manifested.

Everyone will run to one side of the Titanic to list the global economic ship of greater fools as they all consolidate all at the same time.

Bottom line is that liquidity is going to completely dry up once again and just as everyone piled out of securities in 08 they are doing it again.

As the ship lists & starts sinking we will see ever increasing volatility and VIX will skyrocket.

War will follow soon, methinks. Oil is going to continue to plummet which will necessitate a response all across the Western world of manufacturing & banking due to expected loss of livelihood across the board.

Soon we will have to design our macroeconomic reset so we had better start thinking about what we want in the new banking system because the old one is going down very soon due to the oil trend towards a death spiral.

Oil is the most serious conundrum right now.

MOU

“So it’s tamping down on asset price inflation, because these assets are collateral for the banks” – Wolf

While it’s not important to the Fed that ordinary savers are benefited, in fact, they are.

For people with high credit scores, Capita One (for example) has offered a checking account paying a little less than the some Fed bonds rate (I’ve forgotten which one) on balances up to 15K and also offers a linked savings account paying a little less on balances up to another15K.

There are requirements re use of the checking account each month, but they are not onerous – easy to conform in the ordinary course of personal financial transactions each month.

The interest paid on these accounts is up nearly 1% since the fed began unwinding QE.

Also, asset price deflation makes desired purchases more affordable for those who have savings to pay for them.

Remember: Not everything bought and sold is paper.

The present Fed will not buckle. I had my doubts earlier this year but now I am pretty sure that unless a catastrophic event happens they’ll stay the course. In fact I am convinced inflation, and in particular wage inflation, ranks far higher on the Fed’s priority list than propping up asset bubbles. Nobody likes wage inflation bar those who get paid more for their hard work. ;-)

Remember: this will take years to unwind, and we’ll have all the time in the world to enjoy the Wall Street PR machine hitting new peaks of absurdity. Considering the main US newspapers are owned by people with huge equity positions (The New York Times by Carlos Slim, The Washington Post by Jeff Bezos etc) I expect the clamor to become simply deafening and to be relayed across the whole media spectrum.

Luckily I have just bought a package of Honeywell earplugs. ;-)

Hello Wolf,

Good article! Though, your believe in a “Methodical Unwind of Stock Prices” begs the questions who is the mighty controller that can deflate this bubble in an orderly fashion, if you believe its the CBs, then why could they not do it last time and how many of the last 4 stock market crashes did you predict?

The last two. But I was early. More detail here…

https://wolfstreet.com/2018/11/21/stock-market-margin-debt-plunges-most-since-lehman-moment/#comment-161721

The 1987 crash hit me out of the blue. I was just starting out and was clueless. Those are the only three crashes I lived through as an adult.

The banking system isn’t going to collapse this time around. This time around, corporate debt will be in trouble. But much of it will mature in future years (2-7 years), which is when these companies may not be able to refinance this debt, and instead they’ll have to default. So this will drag out for a very long time. Everyone hopes that this will be a sharp, fast, and tradable crash. But I think they’ll be disappointed. It’s instead going to be a long-drawn-out downward zigzag and a miserable and frustrating time for investors.

And remember, 20% down over a few weeks or months is not a crash, but just a regular common ordinary sell-off. In the 2000-2002 crash, the Nasdaq lost 78%. That was a crash.

We have had 10 Year’s of CB pumping, some are still at it covertly, full steam.

The FED’S Unwind pace is considerably slower, than its stimulate pace was.

Hence this ” balancing ” of asset prices, should take at least 15 Year’s, unless there are some serious defaults that turn it into a ” Crash ” scenario.

The US banks appear to have adequate capital to handle some pain, but I get worried looking at European banks.

For kicks I aggregated the data of the six largest European banks (excluding HSBC), which include DB, CS, BCS, CRARY, SCGLY, and BNPQY using 2017 balance sheet data from Marketwatch. The aggregate book value of equity is only 3.5% of the assets. Assets were $8.1T and equity BV was only $290B. These banks are teetering now. If there is any trouble ahead, some major bailouts will be required. It makes me wonder if the US can avoid a banking crisis if European banks are needing bailouts.

I excluded HSBC because it is the one bank that appears to be somewhat stronger than the rest of them, at least on its face.

What peaked my interest in this exercise was a fascination that a bank as large as Deutschesbank (DB) could have a market cap less than $20B while managing $1.5T of assets. To my surprise, most of the European banks are priced this way. Credit Swiss, Barclays, Credit Agricole, Societe Generale each have market cap around $30B or less.

This also leads me to believe these dying banks are purposely being dressed for show. I assume they are using “optimistic” loan values in order to show a sliver of positive equity book value.

This may not be a surprise to anyone, but it was an eye opener for me as to how fragile the banking system has become as a direct result of central bank efforts. The central banks have let the banking system speculate and deteriorate.

Yes, many European banks are a mess and are vulnerable.

Yes, I totally agree with your crash definition. I had bought a couple of out of the money put options in 2000, when Barrons published the available cash to burn of those internet stocks. One dropped from $160 to to 16.

It was your own description re. the effect of leverage, i.e. margin calls, which suggest to me a crash is very likely:

“Now they have to dump stocks to pay down margin debt. This begets further selling pressure, which begets more margin calls, which begets more forced selling…. In this manner, a high level of margin debt turns into the great accelerator on the way down.

But this money from those stock sales doesn’t go into other stocks or another asset class, and it doesn’t sit at the “sidelines” waiting to jump in again at the next dip. Nope, it is used to pay down margin debt. And thus, this liquidity just evaporates without a trace.”

Concur :)

Many European banks are probably bankrupt. I have no idea how this will affect US banks, but it certainly does.

As long as the amount of money in circulation keeps shrinking (or not growing fast enough to keep up with the economy), assets will have to fall one by one, it’s like a game of musical chairs at this point.

It’s funny, it seems like Canada and the U.S. have switched places since 2007. Back then, the U.S. housing market was out of control while Canada’s was merely inflated, but the Canadian stock market was very high while the U.S. market was merely inflated.

Now it is Canada with the out of control housing market and milder stock market (tsx at same level now as May 2008) while the U.S. has the out of control stock market and a housing market that is merely inflated.

Of course last time around showed that a housing bust is far more painful than a stock market bust – I wonder who our Trump equivalent will be …

“I wonder who our Trump equivalent will be “…

Ford? :-)

With our Parliamentary system, French/English divide, the more welcoming attitude towards diversity, only 10 provinces and western alienation looming large, + some dependent territories, I honestly don’t think one of two parties could be taken over by a Trumpian like figure. Yes, the Wynne backlash created a Ford result….. I just hope not for the Country as a whole. Think of herding cats.

More dire changes will be made in mayorships and provincial leaders if there…..WHEN there is a housing bust in Canada. However, we just had a new regime put in place. With the NDP (federal) plunging to new lows it looks like Trudeau benefits and will return with another mandate in one year. Scheer is not Harper. Who knows? Maybe Trudeau will lose his short pants and man-up as time goes by? Anything is possible.

Vancouver and Toronto will be interesting. It is going to be Uggggly. Exodus would be my bet until population and demographics balance out with opportunity. You can’t eat hype, myth, and BS. I would bet that across the Country a lot of kids will be returning home (that have somewhere to return to) and we might get back to sanity and more sustainable values.

There’s a guy in Canada, who joked about creating a MTATA hat, red cap with the same typeface as he who must not be named on WS. MTATA stands for “Make Trudeau a Teacher Again,” too funny.

You can name him, but you can’t call him (or anyone else) names ;-]

And God forbid Canadian companies, the government and people don’t simultaneously get up one day and simultaneously panic at the realization that the oil sands are a thermodynamic and economic sinkhole of epic proportions.

Negative energy return on investment (EROI) for the low-quality fuel that’s produced, to say nothing of the immensely negative environmental/climatic externalities… when the histories are written, it will be more clearly seen as the madness it is…

If the energy and major Canadian urban real estate markets plunge simultaneously, then look out below !!

Goldy has just started referring to cash as an ‘asset’.

How about that? Instead of ‘putting cash to work’ (the stock broker’s mantra) you sell stocks and invest in cash.

After 10 years of ‘cash is trash’ it’s kind of ‘though the looking glass’.

Typo: ‘through the looking glass’

If one goes back to before the Fed began hiking rates, selling MBS/UST and pre-Trump Tariffs, markets were making new all time highs. If both of those headwinds were removed tomorrow why would anyone believe markets & real estate wouldn’t go on to make new highs? Especially given that stocks & bonds weren’t the least bit detoured by individual retail bankruptcies before?

Point being is bears have been playing the part of Chicken Little since 2012 yet somehow it’s supposedly Now…due to nothing more than ‘external’ Fed tightening and import taxes…that they’re claiming victory. Pardon me but until markets run out of steam all on their own with easy money STILL in place…it ain’t over yet.

So here’s my call. This time is different in that world markets have been well trained to ignore the real economy and instead move in lock step with monetary and fiscal policy. And since both of those policies are currently transient, so too is this market rout. The Fed doesn’t seem at all worried about inflation so my guess is their current rate hikes are solely for stocking up on dry powder. As soon as the Fed feels markets need a breather they’ll pause rate hikes and/or balance sheet unwind – and markets will rally BIG. So ‘if’ markets go on to make new all time highs despite a cratering economy (on nothing more than the Fed pausing/easing or the end of tariffs), will bears yet again return to whining and complaining about how it only ‘interrupted’ the crash? Hint: Once markets truly are ready to crash, they’ll do it With or Without monetary and fiscal intervention.

My opinion differs on with one part of that. If the Fed pauses and stocks head quickly upward again, we should expect rate hikes to continue at the next meeting. The upward spasm would be temporary at best. The Fed may see no purpose served by pausing rates and enabling this little blip. It simply would create more uncertainty.

But I agree there may be a point soon when the Fed has no control over the market. There are many factors in play here, not just interest rates. There are many structural factors that have headed the wrong way for a long time – wealth concentration, asset prices, productivity, industry consolidation, etc. You can’t solve these problems by playing with interest rate levels.

Phizer just announced a 5% price hike on its drugs. Incredibly, prescription drugs are 12% of TOTAL wholesale. (I queried this stat on first reading it on WS but WR says its for real. )

‘Total health spending is projected to increase by 5.3 percent to about $3.7 trillion in 2018, according to the CMS report, and the growth will average 5.5 percent per year over the next decade. While that’s still faster than the overall rate of economic growth, it’s an improvement from past decades.’ Feb 15, 2018

All the developed world is facing the growing cost of health care but in the US it’s devouring the economy, in return for the worst results.

So there is some inflation.

But moving to the crux of opposition to the Fed’s ‘tightening’…why is the massive, historic, unprecedented, emergency injection of liquidity by the Fed now perceived as ‘normal’ and its attempt to return to actual normal as a ‘head wind’?

The removal of a tail wind is not a head wind.

Why would the lowest real interest rates, even after the hikes, in perhaps 500 years be considered normal? Why would the Fed putting 4 trillion on its own balance sheet be considered normal, and the gradual reduction be considered Fed interference in what would otherwise be a normal healthy stock market?

Drugs (overall, including over-the-counter and prescription drugs but not including illegal drugs) was 11% of total wholesale in Sept.

You can get it from the horse’s mouth. In the table on page 4, go down to “Drugs” (= $53.3 billion) and divide by total wholesales (= $511.2 billion).

Due to strong wholesales in other sectors, and big inventory build-ups on those sectors, the share of drug sales might have edged down a little since the point in time you mention (2015?).

stocks aren’t the problem. sovereign debt is the problem.

Personal, corporate and sovereign debt are all symptoms of the same problem:

Bank usury.

Financial institutions foisting massive amounts of debt onto all levels of society from the national to the personal, in order that their stockholders may enjoy the privileges they demand.

They’ve inserted their representatives into civil service positions across the globe in order that his happens – with the double benefit of then being able to point the finger at ‘the interfering government’ in order to deflect attention from the real problem – which is the unlimited greed of the private financial sector, and its socio/psychoptahic behavior which has already been evidenced in the events of 2008.

Politicians, blinded by the promises of the glittering prize of cushy board positions, have been all too complicit.

So here we are. A mountain of unpayable debt – numbers so huge that a human being can’t even conceive of them. Interesting times ahead.

Wolf .are you sure it disloved into ambient air,because wealth is never lost it is always transfered but never really lost the Fangman stocks fell because some people were smart enough sell.so I presume that trillion dollars is sitting in someone’s pockets Am I missing something about wealth evaporating into thin air . Sure the fed can do roll offs they create thin air money there sorry about my dumb question

Revolution, war, chaos….that tends to destroy wealth. It happened in many countries part of the Arab Spring….it can happen, but probably not on a global scale.

Tony bolongy,

Yes, I’m sure. It’s a basic principle. I didn’t make it up. It’s called asset price inflation and asset price deflation. The wealth among all participants combined dissolves during a sell-off in the same manner in which it was created during the rally.

If the stock market loses $5 trillion in market cap, that $5 trillion has evaporated. In sum-total, it was not “transferred” to anyone. It just disappeared, just like it had appeared out of nowhere during the rally. Same with the sum-total of home prices and other assets.

On an individual basis, between each of the participants, the question is who holds the assets when prices rise and who holds the assets when prices fall.

For example, person A owns Facebook. One day, when trading starts in the morning, FB gaps down $20 to $160. Person A and everyone holding FB overnight is down $20 a share. That wealth just evaporated. It was not transferred to anyone. Now person A sells FB to person B. Person A thus locks in the $20 overnight loss. And person B is a dip buyer. So over the next three days, FB rises $5 to $165. Everyone holding FB during these three days increased their wealth by $5 a share. This wealth came from nowhere. It’s just asset price inflation. Now person B then sells FB at $165, thus locking in the $5 wealth that was created. And person C who bought from person B at $165 is hoping for more asset price inflation.

Some individuals can also benefit from a sell-off: they can trade the dips or short some stocks or the market. But in sum-total, when asset prices decline, the wealth evaporates in the same manner in which it is created when asset prices increase.

The Fed tracks household wealth (“net worth” = assets minus debts). This is a huge number ($107 trillion as of Q2 2018) and includes homes minus mortgages, retirement accounts, stock portfolios, bond holdings, etc. less debt. This number fluctuates with asset prices. During the Financial Crisis, when home prices and stocks plunged, this number dropped by 17%. In dollars, $12 trillion evaporated in sum-total. It has since almost doubled as asset prices have been inflating.

https://fred.stlouisfed.org/series/TNWBSHNO

Doug Noland makes the case that assets cannot vanish, or deleverage, (as they always have) in the current system, It’s complicated, in the global daisy chain each investor in an international trade firewalls off from the other. It’s Bernanke’s sterilization argument on steroids. This explains why recessions do not cancel bad debt and why only market (systemic) events can do that, which are promptly reflated by the central banks (hence more asset inflation). At some point we enter (global) recession, and you add a HYPER to the inflation. Deflation is something different than deleveraging.

Funny, I read Doug Noland and thought he says the exact opposite. He talks about it in his Market Dislocation Watch.

It certainly had the appearance of incipient fear of tightening financial conditions – contagion having made important headway from the “Periphery” to the “Core.” If, as it appears, global “Risk Off” is attaining some momentum, my thoughts return to Contemporary Finance’s Defect: it doesn’t function in reverse.

Contemporary Finances Defect 10/05

In all of his work the word “deflation” seldom comes up.

Termites are good at dissolving real wealth, as are various forms of oxidation. Military industrial complexes excel at wealth destruction – witness Libya, Iraq, Ukraine, Syria, N. Korea, Afghanistan etc. We need a sound banking system to manage this ongoing destruction and reconstruction of global societal wealth.

I agree with You 100%. Someone got that ‘vaporized’ cash.

According to this lunacy (unlike the host I don’t have to be polite) after the 1929 crash there should have been a whole bunch of happy people who now had the all money lost by the sad people.

Net economic result: zero.

There were a few short pools (Banker Wiggins was part of a short pool while supposedly part of ‘organized support’ for the market)

But these were few. Overall the society at large saw a massive overall reduction in its perceived paper wealth.

Key words are ‘perceived’ and ‘paper’.

If a number of gold bars are in a vault, they are actual. If they go missing, someone has them. This is not true of a stock.

When Singer Sewing Machine went from 48 dollars to one dollar,

very few people had any of the missing 47 dollars.

And the 29 crash did not spare the rich. Far from it.

Faith and credit… when the former disappears, the latter collapses…

And, yes, while shorts (and carrion-eaters like bankruptcy lawyers, etc.) who’ve timed things right/been lucky make huge amounts of money, that’s minscule compared to the fictitious/derivative/faith-based capital that vaporizes in a panic.

Finances are different. They are not economics. Finances are as you say perceived paper (nice one), as it is cash, altough it feels real.

They shift the ownership around while skimming the incumbents.

I mean this as you said economic result: zero. It was financial result: zero – ownership shifted, mission accomplished.

Pardon my stubborness, but sales are made at the top, and they (sales) are passed around in the plunge like a Hot potato. If theres no buyer one cant sell. The buyer gets crushed and her cash ‘vaporices’ through …. to the seller.

By the way: if YOUR gold bars are missing you wont feel any relief thinking like that…

When a company goes bankrupt you should know they previously spent the money to someone else: it didnt vanish in smoke…

I think there’s confusion between “value” and money. Value can vaporize, money in circulation probably doesn’t although banks will remove it once it’s too worn.

But the value of money is an “illusion”. What it’s worth one day is likely more today than a day in the future. We think of it as having a fixed value – it doesn’t.

And if a stock cert., or classic car, or work of art has no buyers, when times are tough, it’s value drops. I understand that there were some depression-era auctions that W R Hearst attended, buying great art and sculptures. He was the only buyer.

No you got it all wrong. Value stays, price changes, imaginary wealth goes up in smoke as price drops.

Can I use the “money is an illusion” defense to get my a** out of jail after leaving the gas station convenience store without paying for my egg, cheese and ham burrito?

The ‘shocking and appalling’ phenomena of not having cheap credit to buy back your own shares, speculators not having cheap credit to recklessly speculate, and subsequent price discovery!

Quelle horreur!

Coming to houses (sorry ‘ properties’), classic cars, classic motorcycles and just about every other thing bought with cheap credit soon!

Hopefully. People need to learn the lessons of the results decadence…as if they ever will!

The Fed just reduced (as of Nov 22) its QE Treasury Holdings by about $17.4 Billion (not including MBS), and the market sold off by MORE than that. This is probably proof that excess liquidity (multiplied by the banks) really came from the Fed’s QE and moved to other (mis-priced) assets.

Wolf,

I don’t see how the psychology of the market would allow for a slow unwind from a bubble. Under what situation do heavy traders not stampede out of the market if they think they are going to lose money? I tend to think the market always has to be a slow, nervous climb up, followed by a shark-fin plummet. Just because of human psychology.

This is a testing phase. Nobody wants to lose money. So the big players are going to see if they can find a footing for the market, and take off for new highs. Or if not, they will bail off the cliff.

It’s hard to see it as being dependent on human psychology when more than half the trades and at times 80 to 90 percent are made by algorithms.

If and when EPS growth goes negative then you can bet’cha there will be a stampede out of the market.

If EPS growth starts slowing moderately then a more orderly unwind may be a possible outcome.

Basically it depends on how the economy as a whole behaves and its subsequent effect on corporate profitability.

Kent,

Scared traders don’t run the show entirely.

Retail investors have been told by the entire financial-advice industry to stick it out and not sell. They own $18 trillion in stocks directly or indirectly in their retirement accounts and in their investment accounts. And they’ll hold. In addition, they’re regular buyers, no matter what, through their 401k and other retirement accounts.

Corporations are buying back their own shares at every dip. They will spend hundreds of billions of dollars a year doing this (until they won’t).

There are hedge funds that have raised very large amounts of money to buy the sell-offs or the crashes.

A lot of people (hedge fund managers, etc.) know something is coming, and they want to profit from it, and they’ve prepared for it, and they’ll jump in with individual stocks as well as the market overall.

Note the 40% single-day surge of PG&E after a lonesome regulator said at a teleconference with analysts that the company shouldn’t go bankrupt. This happened after the market had closed. Hedge funds – perhaps driven by algos – jumped into it afterhours, and the next day the shares gapped higher at the open by a huge amount. This will happen time after time, for years to come. A lot of money will pounce on every opportunity they see, thus causing these bounces in individual stocks as well as the market overall, but on a downward curve.

also, if investors exit bonds, they have to park their money somewhere. some of that will go to stocks. if the euro collapses, that money is coming this way fast.

Sum-total, investors cannot “exit bonds.” If I sell my bonds, there must be a buyer paying exactly the same amount that I’m receiving for these bonds. I cannot sell the bonds without a buyer on the other side. It’s just a trade. It doesn’t create any cash. Cash and bonds just change hands at the negotiated price.

You can park money in a bank, in your wallet, under the mattress, in a register in grocery store. I dont think you can park money in stocks or bonds.

I would have to disagree with that. Retail investors who bought for the ‘long term’, on the advice of ‘financial advisors’ – they will sell when they feel enough pain. This will be towards the bottom of the market, so not for a while yet.

This is why the market does what it does. When there is a bear market, the smartest and swiftest get out first, followed by those receiving margin calls, followed by those ‘rebalancing their portfolio’. Naive retail investors won’t even hear about what is going on for weeks, maybe until they get a 401K statement.

Retail investors cannot stand the prospect of losing all their hard-earned gains, and don’t know enough about corporate finance to be able to calculate the fair value of their holdings. So they sell after the market has gone down, accelerating the decline.

Agree, at some point they scream Sell, a well known phenomenon called PANIC.

Regarding rate hikes – it seems to me the Fed is loading it’s gun to be ready for the next ugly recession. Hear me out – in 2008 the Fed created a lot of new money to supposedly save the economy from a major crash. We still haven’t paid that off yet. The Fed won’t be able to create that much money again with the next recession (maybe some new money) because we can’t afford it. So the only main thing the Fed would be able to do in the next recession is to lower rates. I think that’s why they are forcing the economy now to absorb rate hikes as a way to load their gun to get ready. Yes the rate hikes rattle everyone but the Fed doesn’t care about that.

Does this also mean the Fed knows we’ll have another recession in 12 to 18 months and it may be another ugly one so they are getting ready?

“Does this also mean the Fed knows we’ll have another recession in 12 to 18 months and it may be another ugly one so they are getting ready?”

Just about everyone knows that there will be another recession some day. There always are recessions. They’re part of the cycle. So the likelihood that there will be a recession in 2020 is not minimal. Run-of-the-mill recessions have a cleansing effect on the economy. So that’s nothing to be afraid of (unless your job is threatened). But if something causes credit to freeze up, as it did last time, all heck tends to break loose.

What are some good indicators, red flags to watch, if there is another credit freeze approaching? I understand, you are not expecting this, but i would love to have some in my tool box.

They will declare recession when we’re 6-12 months into it. Then lagging indocators like employment will catch up by the time the recession is close to over. First warnings credit spreads widen, stocks sell off, I think.

When interest rate spreads blow out that is the official red flag. But by that time, it’s fairly late in the game. You’ll see nervous exes of banks that are bogged down in bad loans; banks collapsing or being bailed out (Bear Stearns during the Financial Crisis was a huge red flag); healthy companies that suddenly are having trouble borrowing; and the like.

The BoJ Gov. bond holdings exceed Japanese GDP, so far no inflation. Doesnt surprise me since the low cost of credit does lower the cost of goods and thus keep inflation at bay. (For some uncanny reason CBankers believe its the other way round.) Hence, I dont understand why the FED should not be able to do it again?

The FED holds 20% of US GDP, so the US has still a long way to go, if interest rates stay at the present low levels. The more Treasuries the FED is holding, the smaller the burden for the US tax payer. The FED must pay the collected interest back to the US Gov.

I think why there’s no inflation in Japan despite ZIRP is its population decline (started 2004). Basically, fewer people chasing goods. it’s never happened naturally in the industrialized world for an extended period.

Only one thing scares me at the moment, the falling price of energy in an overheated economy. It portends that should the Fed stop raising rates it will add fuel to the selloff in crude oil. That might set off a deflationary crash. When those jobs are brought back from overseas consumers will need the safety net more than they do now. Low paying jobs put pressure on the red hot employment sector, and the modest wage gains the last few years. More deflationary tinder. Many HELOCs and PLOCs are structured in ways that they cannot be marked to market. A failed policy of the Depression was price controls, and interest rates are the penultimate price control policy, should the Fed take that path. The alternative is to allow deflation to run its course, or to keep raising rates no matter what.

when i was growing up, we used to camp on my friend’s 1000 acre farm in litchfield, connecticut. his grandfather told us that he bought it for back taxes with his winnings from poker in the 1930s.

“one man gathers what another man spills.”

Only possible because the land went for pennies of what the original buyer lost.

In this case one man gathered a fraction of what another man spilled.

The effect of the Great Depression was not net zero.

There was a famous case I read somewhere of a Connecticut estate that sold for over a million in the 1920s that went for $75,000 at the bottom of the Great Depression.

The wealth among all participants combined dissolves during a sell-off in the same manner in which it was created during the rally.

Oh I see now there never really was wealth anyway lol what’s the point of the stock markets all joking aside thanks for a basic explanation for some of us less knowledgeable ones

that’s why it’s called “notional value.”

And “wealth effect.”

But still some did the sell off as you say ,if I sell all my fang stocks I get my money deposited into my bank .

For all you know I could have been the one who sold all last week You never know and I got the suckered that stayed in money …no?

It would be interesting to have the line indicating the FANGMAN market cap with the amount these companies have actually grown in the same graph.

Good idea. Working on trailing 12-months income vs stock price. But there is a structural problem putting this data into the same chart in that income data is quarterly and is reported with a lag, whereas stock prices are daily. So I have to make some compromises and arm-wrestle Excel into doing this the hard way :-]

Also in terms of income, Apple is huge even among the FANGMAN, so I might have to do it with and without Apple to see if it changes the dynamics.

Fact is, we haven’t even come close to coming back down to normal historic valuations in the last 25 years. Financial markets have simply accepted twice the normal valuation since 1995. That, and Tens of TRILLIONS in buybacks, is the only way we’ve kept the stock market in its upward climb. The DJIA could lose 30% from here and still be overvalued historically speaking. But that will never happen in the completely subsidized “market” we have today.

The NASDAQ lost more than double that in the Dot,com crash.

Isn’t it odd that all the FAANGS are internet related.

That’s why they are called FAANG for a reason they will devour the entire stock market like a cobra they will be the entire stock market one day .

They are almost there

The holding of many quality stocks did not work in the last crash.

Perhaps this whole move is orchestrated Trump, Big banks wall street, huge players,Huge funds in collusion to fight the FED. Trump has not held back with criticism of the fed and is a type of person who wants to win after comments. Interesting who wins or who buckles. Not moving rates higher allows a market to change direction. Seems it was very low interest rates after 2008 ( QE ) that exploded it into artificial pricing after the big correction. If the fed buckles is it another feast for the top few. Wash, rinse, repeat. It again narrows the competition for elite players as they become even more monopolized. Big fish eating smaller fish. What does the winning fish eat after all is devoured. My view is this has been the game historically.

What worries me is shale gas. The entire shale industry has been sustained by low interest rates. If the market crashes, it could take drillers and shale companies with it.

This would have big effects on US energy. The shale industry consumes capital and is basically non-profit. Oil prices are set internationally, but natural gas prices are set locally. About 50% of natural gas used in the US comes from shale. If shale blows up, expect the following:

Natural gas shortages followed by a large increase in price. This will start some profits in the energy industry, and cause some manufacturers to start moving offshore.

A big increase in coal usage. Coal has been competing in the electric generation market with gas. As the lowest priced fuel, it will eventually win out. This will take time.

A general economic decline. When societies spend more on energy, they spend less on everything else. Skyrocketing utility bills will force families to pare back on non-essentials, such as dining out or entertainment, rather than food or housing.

Obviously, this will not help the stock market.

“A big increase in coal usage. Coal has been competing in the electric generation market with gas. As the lowest priced fuel, it will eventually win out. This will take time.”

What you typed across your typer and into the comment box on this site is total paranoid pseudo-jargonic debunked olduvai sputum.

Richard, in 2018, multiple governments, including the USGOV, international institutions such as the European bank for reconstruction and the World bank and Wall street trading houses – i.e. spot market and futures prices – all issued reports stating that:

On an unsubsidized basis, natgas, syngas, utility scale solar and wind are all cheaper in producing 1 megawatt hour of electricity than coal going forward out to 2040 and beyond, and have been cheaper than coal for at least the past 3 years and biomass, enhanced geothermal and roof top solar are also at, below and/or trending lower in price than any type of coal used for energy production.

AND THAT “the introduction of competitive auctions will lead both to a steep drop in electricity prices” – this was just last month in OCTOBER 2018.

It feels good to spew nonsense, this is the cybernetic essence and the dopamine-hit-core of the internet where any fool can for a fleeting fraction of a moment, see himself in a hyper-reality version of reality.

…[xyz]

…[XYZ] denotes that I deleted some text that was purely a personal attack on another commenter (Richard), which is inappropriate here and against the guidelines.

Trump wins round one as per previous post. Fed buckled as per remarks for now or so it was intercepted. Many rounds to go. Kind of too bad the posts get aged (days) and any follow up disappears that fast. All want the latest.

For what it worth there is a team directed who can move the market up and down. Look at the chart, some players are surely tipped off ahead of moves/remarks and will result in the big moves. All a big game. How many billions on the way down then today up as directed. No collusion ???

will JPMorgan introduce a silver crypto. With interest of the idea a lot of fees would look nice for them in the future. The downside is probably not a problem. Wonder if a silver crypto token could appreciate with a silver upwards move. A crypto backed by silver, hmmmm. Big success if played right. Maybe even stable.

“They and their TV-personality allies – along with the professional crybabies on Wall Street – are already wailing and gnashing their teeth, and are clamoring for the Fed to reverse the rate hikes and stop the QE unwind to end this shocking and appalling phenomenon.”

Yes wolf you called this in that paragraph. I am always happy to read your thoughts. Good wisdom and learned wisdom from reading you. Proof that education never ends. One item from myself is Trump has a team which can make the markets go either way. The fund must be incredibly enormous as each market point is beyond thought. To make 100 point moves instantly has to include others in the know before hand. You may think all is fair or perhaps not. I suppose a card player never shows a real hand or would be dangerous personally to a depth of your discussions. I believe you have seen all for yourself actually.

“If everyone’s thinking alike, then no one is thinking”

All but 1 or 2 commenters agree with your perception of the “markets”.

As I have gotten older, when I’m feeling confident of my perspective, I pause and consider what would make me change or adapt. (do you?)

So many variables affecting and creating the “market”.

In the end, “they” will use the markets to create wealth, not destroy it, imho.

I’ll follow along closely and jump back in sometime

next year, for the next big up-swing.

Great website, Happy Holidays to you and yours.

You got it terribly wrong: between 80% to 100% of the people in the market think like you. Why else would they still be in the market at these crazy prices? They, including you, are thinking alike. This site goes against the tide, if you haven’t noticed.