Their “Everything Bubble” is being pricked “gradually,” and they don’t like it.

Wall Street has been moaning, groaning, and crying out loud about the Fed’s current monetary policies – raising rates and unwinding QE. They fear that these policies will undo the Fed’s handiwork since the onset of QE and zero-interest-rate policy in 2008, now called the “Everything Bubble” (stocks, bonds, “leveraged loans,” housing, commercial real estate, classic cars, art…). In an effort to pressure the Fed to back off, they’re accusing the Fed of making a “policy mistake” and creating “scarcity” of bank reserves.

Here is Bloomberg News this morning. It’s really cute how this works. This is how the article starts out: “Fixed-income traders are telling the Federal Reserve that it might end up making a big policy mistake.”

These folks cannot say that the Fed’s QE unwind and higher rates might unwind some of the wealth of asset holders that resulted from the Fed’s desired “wealth effect.” That would be too clear. So they have to come up with hoary theories to back their “policy mistake” theme. This time it’s the theory of a “scarcity of bank reserves.”

When these folks talk about “scarcity,” what they mean is that they have to pay a little more. In this case, banks are having to pay more interest to attract deposits.

For the crybabies on Wall Street, that’s “scarcity.” For savers, money-market investors, and short-term Treasury investors, however, it means the era of brutal interest rate repression has ended, and that they’re earning once again more than inflation on their money (savers might have to shop around).

But that the money from depositors is suddenly not free anymore is anathema on Wall Street. So here we go – this time specifically targeting the QE unwind. Bloomberg:

The most vocal critics contend that if the Fed doesn’t slow or stop its unwind, it could end up draining too much money from the banking system, cause market volatility to surge and undermine its ability to control its rate-setting policy.

“The Fed is in denial,” said Priya Misra, the head of global interest-rate strategy at TD Securities. “If the Fed continues to let its balance-sheet runoff continue, then reserves will begin to become scarce.”

I receive these doom-and-gloom pronouncements about a “policy mistake” and “scarcity” of reserves all the time in my inbox, sent by economists working for Wall Street firms. They want me to cover this stuff, just like Bloomberg is covering it. It’s a ludicrous charade. But they’re out there trying to pressure the Fed with a publicity campaign to back off because Wall Street is at risk of giving up some of what it gained during the era of interest-rate repression and QE.

The Fed’s QE unwind got started in October last year and finally reached cruising speed. “Gradual” is the operative term. The Fed has shed $195 billion in Treasury securities, which are now down to $2.27 trillion; and it has shed $102 billion in mortgage-backed securities, which are now down to $1.67 trillion. Total assets on its balance sheet have dropped by $321 billion over those 13 months, to $4.14 trillion.

And every step along the way, the crybabies on Wall Street were out there whining about it.

These are the same folks who said during QE that the Fed could never stop QE, and they baptized QE-3 “QE Infinity.” And when QE Infinity ended, they said that the Fed had “painted itself into a corner” and could never shed any of these assets. And when the Fed started shedding these assets late last year, they said that the Fed would back off, and when the Fed accelerated as planned the QE unwind to cruising speed, they called it a “policy mistake” that is creating “scarcity” of whatever.

These economists are a transparent PR and lobbying joke.

Bloomberg lays out their theories that the effects of the QE unwind are “creating the scarcity of reserves that has banks – mainly the smaller ones at this point – scrambling for short-term dollar funding.”

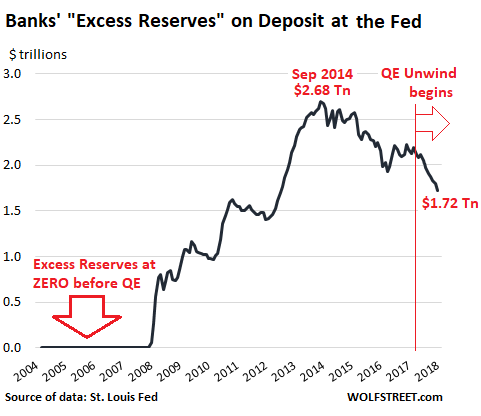

So what are these “reserves?” These are the “excess reserves” – cash obtained from bank deposits that banks in turn place on deposit at the Fed to earn the easy and risk-free “Interest on Excess Reserves” (IOER), currently 2.20%, that the Fed currently pays. This is a great deal for banks: They pay customers next to nothing for their money and then deposit the excess cash at the Fed for an easy 2.2% return.

Or at least it was a great deal. But now banks have to raise interest rates to retain deposits, and to rope in new customers, they’re offering higher rates on “brokered CDs.” They’re having to pay 2.5% and even 3% for a one-year CD to do so. And giving up 2.2% income from excess reserves and bringing that cash back to the bank to lend out, is cheaper than having to pay customers 2.5% or 3%.

Excess reserves have been shrinking since September 2014, when they peaked at $2.74 trillion. As of October 25, 2018, they dropped to $1.72 trillion, down $1 trillion over the span of four years. But they’re far from having “normalized,” which would be zero, as before QE started:

“Banks are in a decent position right now, but over time this will begin to weigh,” Jonathan Cohn, the head of interest-rate trading strategy at Credit Suisse, told Bloomberg, with reference to that $1.72 trillion of still nearly free money that banks got from their deposit customers and have in turn placed on deposit at the Fed earning currently 2.2% risk free. These “excess reserves” provide $38 billion a year in pure profit for banks, handed to them by the Fed. Thank you for the free gift. And now the crybabies don’t want to give that up.

Bloomberg cites another Wall Street crybaby:

Michael Cloherty, the head of U.S. interest rate strategy at RBC Capital Markets, is worried. He says the biggest risk is the Fed turns a blind eye to the pressures on bank reserves and triggers huge swings in short-term rates with its balance-sheet runoff.

There haven’t been any “huge swings in short-term rates,” but they have increased steadily to the highest levels since before the era of interest rate repression as they begin to “normalize.” Normalcy, after a decade of being coddled, is a painful thing for these crybabies.

“At some point, all of the reserves outstanding will be locked up by all the people who need it” to meet all the regulatory mandates, which may lead to a “scramble” for short-term cash, he said. “If the Fed keeps shrinking its balance sheet until it sees signs of stress, the question will be, ‘How ugly is that stress?’ I think it will be quite ugly.”

This “‘scramble’ for short-term cash” is of course the market force that pushes banks to offer higher interest rates on their deposits to attract more deposits, a sign that the Fed’s interest-rate-repression decade has come to an end.

And yes, it might get “quite ugly” for asset holders because asset prices are heading south, after a decade of Fed-engineered “wealth effect.” That’s the fear, and that’s why the crybabies on Wall Street are making such a racket.

Some of the asset classes in the Everything Bubble, such as “leveraged loans,” are specifically being targeted by the Fed. Most recently, it warns about the widespread practices of ‘collateral stripping,’ ‘incremental facilities,’ ‘cov-lite,’ and ‘EBITDA add-backs.’ Read… The Fed Broadsides $1.3-Trillion “Leveraged Loan” Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

All the money Wall St. expects to make in the future has already been spent trying to make even more money. Therefore it needs still more, just to keep going.

It is always a mistake to feed the ultrarich. It only makes them hungrier. Right now Wall St. is seriously bloated, and therefore madly ravenous. If you try to put it on a diet, like the Fed is doing, it will not lose weight. It will starve.

It will crash the moment there is nothing left to feed it. Since you ultimately cannot save it even if you sacrifice everything it is worse than useless to try.

In related news, Stock Markets Do Not Create Value. You can google up the article yourself, and this is what it says:

Since 1977 the median new shares issued on the stock exchange has delivered a negative rate of return, even with dividends reinvested. On average, a quoted security has a life expectancy of just 7.5 years over the 90 year period studied. No wonder short-termism is rife.

Just five companies out of the universe of 25,967 in the study account for 10 per cent of the total wealth creation over the 90 years, and just over 4 per cent of the companies account for all of the wealth created.

So, what is to be learned? First, the stock exchange is not a business funding mechanism: it is a business exit strategy for most companies. Second, most people are fools to take part in this game.

Unamused, I generally share your perspective, but without hard data I cannot follow your conclusions in this comment. The equal-weight index research doesn’t seem to deliver the same conclusions as this study.

It’s well known that most new companies fail. That doesn’t make it pointless to start new ones. Every venture capitalist knows this.

If 4% of 26,000 companies are successful, that is 1000 survivors, which is about the size of the market. So what’s the problem?

Finally, when you write “most people are fools to take part in this game”, what game specifically are you talking about? Individual investors blindly buying IPOs? Venture capital? Entrepreneurs starting new companies? Buying and holding equity index funds? There are many games in the market, and many of the companies that fail, fail precisely because investors don’t want to play their game.

P.S. The original study that you refused to link to appears to be hiding behind a paywall at Financial Times. It looks to me like you quoted from a blog post that looked at the article, not the original article, so I’m guessing you don’t have the hard data yourself either?

P.P.S. The original study, upon which the FT article was apparently based, is at the link below. It actually says that 4% of stocks explain the outperformance of Stocks relative to Treasuries, with the other 96% collectively matching Treasuries. It doesn’t say that only 4% of stocks make money. It does say that many stocks end up total losses, but these are more than compensated for by the long-term success of others.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2900447

->It does say that many stocks end up total losses, but these are more than compensated for by the long-term success of others.

But not for everybody. And certainly not for most retail investors. I am persuaded that the conclusions are valid: on average, new shares do deliver a negative return. In the long run you couldn’t select a portfolio from IPOs selected at random because you’d go bankrupt.

The article I referenced, plagiarized actually, is at nakedcapitalism dot com.

Conventional approaches to investment research typically have a strong tendency to find what they want to find, rather than what is true. Quite aside from methodological errors, logical fallacies by themselves are not always so easy to avoid: the Gambler’s Fallacy, for one, seems to have been popular forever, but there are several others. Further, studies are often traps set by marketing guys for the unwary.

For example, Black-Scholes-Merton, on which all options markets are traded, has long been one of my pet peeves, insofar as it is easily provable that it is a tautology resulting in a zero-sum game, so that the sum of all transactions in a specified set must necessarily be negative because of transaction costs. Papers exposing the theory are routinely suppressed and ignored.

->If 4% of 26,000 companies are successful, that is 1000 survivors, which is about the size of the market. So what’s the problem?

25,000 failures is likely to deep-six rather a lot of opportunity cost.

I am truly sorry to present such unsatisfactory discussions. Given my restrictions, very often the best I can do is to make certain points using oblique literary devices. I do have hard data on numerous issues, nearly all of which can never be cited anywhere.

Put another way the rise in stock prices occurs because it takes more dollars to purchase a share of the same S&P future earnings. Now was it always that way? Probably not.

Unamused, thanks for the follow up. This statement of yours is a misinterpretation of the research:

“I am persuaded that the conclusions are valid: on average, new shares do deliver a negative return. In the long run you couldn’t select a portfolio from IPOs selected at random because you’d go bankrupt.”

The research in the article doesn’t say that. First, the “negative return” for the median company is relative to treasuries. The average total return for all companies is very positive, but only because a small fraction of companies do very well. It’s like having a coin that is biased to show tails 80% of the time, and you lose $1 when it does that, but the 20% of the time when it comes up heads, you make $100. The median result is a loss but the overall average is a gain.

Stock investors do make money overall. They lose more often than they win, but when they win, they tend to do very well. This is one reason why all the trading literature emphasizes the need to cut losing positions while holding onto the winners. The goal of successful investing is to build (or find) and own the companies in the “winning tail” of the distribution.

->The goal of successful investing is to build (or find) and own the companies in the “winning tail” of the distribution.

And most people are unable to do that. It should be easy to see why: it’s a competition, and most people are hopelessly outclassed as it becomes increasingly institutionalised. Successful traders are those with the best resources. Most people can’t spend $24,000/year on a Bloomberg terminal, and even a bare-bones Eikon costs $4,000/year. Most people who have money in equities have it through institutions, but that is not retail trading. Most people have to have a job. In 1950, retail investors owned over 90% of the stock of U.S. corporations. Today, retail investors own less than 30%, and falling. Individual investors represent less than 2% of trading volume, and falling, and almost none of us can do HFT.

Like the article says, most people are fools to take part in this game. You can believe what you like, but mind what I’ve told you about fallacies.

As you’ve said, Wall Street and the banking industry have declared a full on PR war against current Fed policy. I’m curious why you believe Wall Street will lose this war. Cramer has demanded the Fed reverse course – he generally gets what he demands on behalf of CEOs. Bernanke set us up for an eventual catastrophe and Wall Street has aimed their massive PR arsenal at Powell with the explicit threat that he will be blamed for all of the terrible things that occur due to short sighted Bernanke policies. Powell will not want to be blamed for Bernanke blunders and he will resume the can kicking catastrophe we (middle class savers) have endured for 10 years.

Why will we soon experience QE4? Because 4 is the number that follows 3.

Powell is just trying to work back to typical business cycles. In a typical cycle, rates go up while GDP climbs and rates go down after the GDP slows and drops, then it repeats.

Wall Street has always fought for lower rates and Powell is used to that. He’ll wait until GDP slows or reverses just like in a normal cycle, shrugging them off like it’s 1999.

The difference here is mainly that the mal-investment from the everything bubble was allowed to get so high. That is why Powell is tightening so slowly and why wall Street fears the correction more than usual.

Rates will continue rising until there is either a 20% market correction or government measured GDP growth drops too low.

I tend to doubt Powell will launch QE4 – I think it’s more likely that he’ll respond to the data by pausing the increases or droping rates back down as a normal response, or he’ll be replaced as Fed Chair by another wall Street cheerleader if there’s a big enough drop to cause political waves.

It’s funny saying this, but I actually think Powell is a good person for the Fed chair – definitely better than Greenspan, Bernanke and Yellen.

There’s a phrase by Mao Zedong I like quoting ad nauseam “All reactionaries are paper tigers. In appearance the reactionaries are terrifying, but in reality they are not so powerful.”

Wall Street is one of the reactionaries likened by Mao to paper tigers because what they have but their carefully cultivated image? Sure, they can swamp the media they own or control (through ad money) with whatever propaganda they want but they have long overplayed their hand.

Remember, these are the same people who assured us with a straight face back in 2008 oil would hit $120 “by Christmas” and $150 “by the end of 2009”. Remember GoPro? Remember their 2016 IPO at $24? “Can only go higher!” said the Wall Street propaganda machine. Now GPRO struggles to avoid becoming yet another penny stock as defined by the SEC. Remember all the scandals FaceBook has been involved over the last couple of years? Also remember how quickly the Wall Street-friendly media buried them to avoid FB from hitting the all-important FANGMAN too hard.

Powell is a lawyer by trade, and lawyers deal with paper tigers such as the Wall Street windbags pretty much every day. It’s sadly part of their job. He won’t be fazed by them.

Cramer has demanded the Fed reverse course – he generally gets what he demands on behalf of CEOs.

Ugh! Cramer’s show is American Wresting with Live-betting!

Jim Cramer is simply the investment-version of a WWE-match reporter: Ugly, noisy, stupid, and never informed which way the “match” he is spectating is rigged, because Management don’t trust him to not spoil the show!

*) He is probably an OK man in person. I can’t stand his TV character, however. Another WWE-like feature, I guess.

In the 90s his fund underperformed in a raging bull market. He was accused or using Maria B on CNBC to pump Mister Softy in the AM and dump his shares in the PM. He did create the BEST stock traders website ever. They had the best, you could make money reading their columns. I learned a great deal reading those columns. (and his wife, he calls the Trading Goddess)

As you say he earns his edge by being able to pick up the phone and call CEOs. They know its him and they are ready. He’s a trend follower and generally he knows what other traders are going to do. Story goes he roomed with Andy Beyer in college, put himself through college betting horses at Aqueduct, sold Rockport shoes. Interesting guy.

Bernanke was the original “rig artist” of Wall street when he coined the phrase “backstop the market” way back in 2012. Put another way Wall Street is nothing but a total fraud today.

Not just Wall Street – everywhere that adhered to the auspices of ‘Chicago School’ is the same way.

Once politicians become convinced the most important members of society are mega-wealthy financial speculators, and that their ‘trickle down’ will provide for all (don’t tax ’em or they’ll leave…), you know you’re in trouble.

They’re happy to de-industrialize, for a start, because that increases short-term stock prices due to lower wage bills, which keeps the speculators happy – and if your only measure of a successful economy is a stockmarket index, then that’s a successful policy all round…just ignore the destruction of your middle class, and all is well.

Cramer is a court jester. Serious Wall Street people don’t pay much attention to him. Many of them are warning that the Fed is serious and interest rates are going higher than people think.

Cramer has been all over the place, reverses himself like a weather vane. Example: Last week after sell- offs he switched to liking defensive stocks, telling us ‘where to hide’. Now he’s back to tech, spec. whatever.

I’m a bit surprised CNBC thinks they can pass him off forever as an expert on everything: oil, metals. tech, etc. etc. You name it the Mad Man will tell you about it. Serious investment firms don’t have a guy covering oil and Facebook.

As for Powell paying the slightest attention to Cramer’s ‘demands’ ….

There is only one revered figure in the Fed: Paul Volcker, who took the Fed rate well into double digits. When Powell says ‘we are no where near normal rates’ he is not kidding. He is also stating the obvious.

Of course nothing is certain. Maybe populist politicos will force the Fed to ‘just print money’ and the US will become Venezuela.

Cramer – why listen to him unless you need entertainment of WWE type. If he is the hotshot why is he still working at his age? Must have buku debt to pay off.

After 10 years of being awash in Excess Reserves, the banks will have lost most of their institutional knowledge of how to operate profitably in any other environment. But they have another 2 years of Excess Reserves left to figure out the “scarce reserves” world. And by then they will have another couple trillion in Treasuries fortifying their balance sheets, paying risk-free interest, and not needing to be marked-to-market.

The banks have basically only one strategy to compensate for the loss of free money. That’s to rapidly shrink their physical footprint (branches) in the new world of virtual banking. IOW, when free “raw material” ends, they’re going to need to cut costs super-aggressively, and the only way to do that is to become virtual overnight. Which is OK, and doable, because young people can’t understand what a bank branch is anyway. Fintech is the future. Some will adapt. Some won’t.

How dare you take away the punch bowl.

Thanks for this, Wolf – yes, how great would it have been for us mopes to have the option of earning 2.2% risk-free via our own deposits at the Fed (or at a retail-level Postal Savings Bank as many progressives have argued for) over the past decade?

One potential quibble, however:

“They’re having to pay 2.5% and even 3% for a one-year CD to do so. And giving up 2.2% income from excess reserves and bringing that cash back to the bank to lend out, is cheaper than having to pay customers 2.5% or 3%.”

Isn’t this what is often referred to as the Loanable Funds Fallacy? I.e. that banks need an actual reserve cushion from which to lend in accordance to the leverage limits set by the applicable fractional reserve banking schema? When in fact the way modern bank lending actually works is “loans create deposits”, i.e. customer requests loan, bank creates ex nihilo “credit money’ to fund loan and deposits same into customer’s account, et voilà! There’s your reserve cushion in form of a deposit. (I like to call this scheme “fictional reserve banking”.) In other words, the only constraint on lending is the supply of creditworthy borrowers, which is why the Fed giving the banks free money “to lend out” never has the allegedly-intended effect as said cash instead simply gets redeposited at the Fed to earn that free 2.2%, or gets funneled into speculative asset-price bubbles.

ewmayer,

Banks have “required reserves” — 10% of deposits in the US, if I remember right. “Excess reserves” are on top of that, and they can go to zero, and were at zero before QE. So banks can live just fine without depositing extra cash at the Fed, beyond the “required reserves.”

An individual bank MUST fund its loans in some way. Its own deposits are the primary way. You need to understand the basic principles of modern double-entry accounting to understand how banks fund their loans. I’m going to write an article on this someday because there is so much confusion about this, because people have no clue about accounting, but here is the short version:

To ALL READERS: if you think a bank just creates money out of nothing when it makes loans, or that it doesn’t need deposits to make loans, please read this:

Accounting 101, day one, minute two: On a company’s books, every transaction is recorded with at least one debit entry and one credit entry. For this transaction, the sum of all debits must equal the sum of all credits.

When you “deposit” a $1,000 check into your checking account, the bank (boiled down to the most basic form) books this transaction with two entries:

1. It “credits” $1,000 to a liability account (money it owes you) called “deposit” (thereby increasing its liabilities.

2. It “debits” $1,000 to an asset account called “cash” (thereby increasing the asset balance).

These two entries make sure that liabilities and assets rise by $1,000 each so that the balance sheet stays in “balance.”

Then the bank takes this $1,000 cash in its “cash” asset account and lends it out. This is booked with two entries, a credit and a debit:

1. It credits its cash account $1,000 (thus lowering the account by $1,000).

2. It debits a loan account $1,000 (thus raising it by $1,000). This could be a loan to me to buy an AC, or a loan to the Fed in form of “excess reserves.” The bank would receive interest from either one of them.

3. But the liability account “deposit” remains the same.

So the bank retains the liability called “deposit” but lends out the “cash” from that deposit and turns it into a “loan.” Both cash and loans are assets on the bank’s books.

When people say that banks don’t lend out “deposits,” they’re technically correct in the debit-and-credit sense of the word. But a bank lends out the CASH from those deposits.

In normal language, a “deposit” confusingly means both the bank’s liability account and the cash that comes with it (the bank’s asset). This normal use of “deposit” is where much of the confusion comes from.

It all boils down to this: A bank retains the liability called “deposits,” but lends out the “cash” from those deposits; and a bank MUST fund the loans it makes, and the cash from deposits is the primary source of funding.

Then banks borrow from other banks, and lend to other banks through fractional reserve lending. I could post this farther down but I think the quality of their collateral is being called into question.

Yes, banks can borrow from each other if they need to in order to fund loans, but each of those transactions is recorded with a debit and a credit by each side of the transaction. See above. No money is created.

BTW, interbank lending has shriveled since the Financial Crisis to almost nothing. And that’s a good thing because it reduces the risk of contagion.

https://fred.stlouisfed.org/series/IBLACBW027NBOG

You also have the difference between time and demand deposits.

If I take out a 12-month CD from a bank, I don’t have access to those funds for a year, but in return get my money back with interest at the end. During the year the bank has my money, they can use it for whatever they want (hookers and blow?) That is a form of full reserve banking.

On the other hand, if I deposit $1,000 in cash (10 Ben Franklins) in a checking account, I get a $1,000 deposit in return but with no interest. If the bank then takes $900 of my cash and lends it out (keeping 10% in reserve as required) while my checking account still shows a $1,000 balance, well, now they’re playing a little “okey doke,” if you know what I’m saying. The financial system now has $1,900 in ‘money,’ my $1,000 checking deposit and the 9 Ben Franklins that my bank lent out. Take this to the limit, and the initial $1,000 would eventually create $10,000 in checking deposits, but all of it is really only backed by $1,000 in real money.

The system only works because we treat checking deposits as equivalent to cold, hard cash. In the old days, banks would issue their own bank notes with the bank’s name and denomination on them. They often weren’t treated as equal to real government money very far from the home town of the bank that issued them. Some of us may even be old enough to remember when you had to buy traveler’s checks and withdraw a fat stack of cash before going out of town.

No, that’s not how it works:

“…. while my checking account still shows a $1,000 balance, well, now they’re playing a little “okey doke,”

And no, the bank cannot lend out the $1,000 you deposited 10 times and generate $10,000 in loans from it.

You still don’t understand debits and credits — that YOUR $1,000 for the bank is TWO entries: a liability of $1,000 that doesn’t change (which is what you see when you look at your account) and cash (asset) of $1,000 that it lends out.

The bank can lend your cash ONLY ONCE. When it’s lent out, it’s gone until it’s paid back.

What the bank shows in your checking account is the liability (deposit) — the amount it owes you, not the cash (asset). The bank’s liability is all you see. You don’t see what happens to your cash (asset).

When you look at the amount in your deposit account it is an asset to you (a lone to the bank), but it’s a liability for the bank (what it owes you).

You guys need to get off these crazy theories — “now they’re playing a little okey doke” — and study basic accounting, chapter 1.

Hi Wolf – Can you expand on this? I think something is being lost in translation – he is talking about banks in aggregate and you are talking about lending by a single bank where a deposit is placed.

Specifically, when the bank loans out money, that money gets deposited elsewhere, and that bank can loan it out again, etc. I think that’s what he is getting at – the idea that it is a lending chain and the original $1k deposit can become $10k in loans by banks in aggregate. Whether that is how it works is another issue.

ZeroBrain,

I’ve already expanded on this in this comment section. Yes, the banking system as a whole creates money as you described. But an individual bank MUST fund the loans it makes (via deposits and other funding sources).

I think the idea of fractional reserve lending is the point of confusion here.

The rough idea is that the banks require only a fraction of the cash as reserves from a deposit and they lend out the rest.

If $1000 is deposited and the reserve required is 10% in order to cover potential withdrawals, then the bank lends out $900 and holds the rest in bills.

The depositer often uses checks to transfer the balance of the account to pay for things. The $900 loaned out is spent, so the idea is that the $1900 is acting in the system based on the $1000 deposit. This idea can get confusing.

The person is not talking about the original bank. The poster is describing the process of fractional reserve banking involving the entire banking system.

The original bank – call it bank A – can only lend out the funds once.

The person taking the loan goes to Mr Plumber and has some work done and pays him $900.

Mr Plumber goes to Bank B and deposits the funds into his account there. Bank B now has $900 on its books.

Bank B takes out the required 10% and lends out $810 to Mr Baker who buys a new oven.

The store selling the oven takes the $810 to Bank C and it now has $810 on its books. It takes out the required 10% and lends out the remainder.

And so on.

That is how money circulates in the banking system. So yes, that original $1000 multiplies itself though the system by means purchases and loans.

Wolf

Best wishes trying to explain this to the uninitiated.

I have frequently commented that 95%+ of US “retail investors” cannot read a financial statement and literally have no business investing in anything other than mutual (Index?) funds.

People who cannot understand the basics are not investing, they are gambling; they are sheep being led to the slaughter. When their investments fail (HIGHLY likely) they immediately blame various criminal conspiracies, the ultra-rich, corrupt capitalists, and/or the crooked FED.

These sad-sack investors NEVER realize their lack of experience and inability to understand and track an investment is a HUGE disadvantage.

I guess they feel they “deserve” to make some money. Unfortunately, there are exactly zero participation medals given out to investors.

Reserve Requirements and Money Creation Reserve requirements affect the potential of the banking system to create transaction deposits. If the reserve requirement is 10%, for example, a bank that receives a $100 deposit may lend out $90 of that deposit. If the borrower then writes a check to someone who deposits the $90, the bank receiving that deposit can lend out $81. As the process continues, the banking system can expand the initial deposit of $100 into a maximum of $1,000 of money ($100+$90+81+$72.90+…=$1,000). In contrast, with a 20% reserve requirement, the banking system would be able to expand the initial $100 deposit into a maximum of $500 ($100+$80+$64+$51.20+…=$500). Thus, higher reserve requirements should result in reduced money creation and, in turn, in reduced economic activity.

In practice, the connection between reserve requirements and money creation is not nearly as strong as the exercise above would suggest. Reserve requirements apply only to transaction accounts, which are components of M1, a narrowly defined measure of money. Deposits that are components of M2 and M3 (but not M1), such as savings accounts and time deposits, have no reserve requirements and therefore can expand without regard to reserve levels. Furthermore, the Federal Reserve operates in a way that permits banks to acquire the reserves they need to meet their requirements from the money market, so long as they are willing to pay the prevailing price (the federal funds rate) for borrowed reserves. Consequently, reserve requirements currently play a relatively limited role in money creation in the United States.

https://web.archive.org/web/20040203023009/http://www.newyorkfed.org/aboutthefed/fedpoint/fed45.html

Exactly. How does Wolf not see this? Once bank loans the money, these money can be redepositted by someone else in some other bank – they are put into checking account and process repeats. This literally creates new money in the system (that has to be repaid with interest, let’s not forget that).

Mario,

You need to read what max is saying. Max describes how the BANKING SYSTEM as a whole creates money as deposits and loans flow through the banking system. I have said many times that the BANKING SYSTEM as a whole creates money. We agree on this.

max is also saying that an INDIVIDUAL BANK must fund its loans via deposits (or other sources of funding) and that an INDIVIDUAL BANK does not create money when it makes a loan.

This is really key to understand:

– No individual commercial bank creates money to make a loan; it must fund the loans it makes via deposits or other sources;

– The banking system as a whole creates money.

Suffice it to say that a deposit of base money or reserves allows lending, and then that lending creates checking deposits. If we let r=required reserve ratio, then we get a maximum of 1/r times base money in checking deposits so $1,000 in base money would allow for $10,000 in deposits with a 10% reserve requirement. The fraud is in people believing that there is enough cash to cover all checking deposits at all times, and in getting 0% in return (or paying fees!) on their checking deposits. Every bank will always have way more in deposit liabilities than it has in vault cash and reserves. But they usually have a lot of liquid assets like U.S. treasuries that they can sell for cash if necessary. Bankers would much prefer you to lock up your money in a CD for a paltry rate of interest because it means that you agree not to withdraw the funds in cash, write checks on it, or move your account to a competitor for a period of time. They are only trying to cover their rear ends.

Todd H,

“The fraud is in people believing that there is enough cash to cover all checking deposits at all times,…” I don’t know anyone who believes that. I think most people understand that the bank puts most of their deposits to work.

It’s like car insurance. If all cars got into an accident on the same day, all insurance companies would go bankrupt and payouts would be next to nothing. And everyone knows that, and we still give our money to insurance companies. Why? Because that event is very unlikely.

Banking has the additional wrinkle that a panic can set in, in which case you can get a run on the bank. So you need an insurance program to prevent those fears (FDIC), and you need a lender of last resort as a backstop (central bank). Problem solved.

I would at least like the option of a full reserve checking account where the bank just acts as a warehouse for my cash and doesn’t lend it out, in return for me paying a monthly fee. Are there any options for a full reserve checking account? To my knowledge, the system only provides 2 options: cash under a mattress or a deposit in a fractional reserve bank.

Wolf, If you will write an article about this topic could you address Richard Werner’s article “Can Banks Individually Create Money Out of Nothing? – The Theories and the Empirical Evidence,” International Review of Financial Analysis 36 (2014) 1–19

It found out that lending did not take away funds from any internal or external accounts.

“Instead, it was found that the bank newly ‘invented’ the funds by crediting the borrower’s account with a deposit, although no such deposit had taken place. This is in line with the claims of the credit creation theory”

Tomi,

I already addressed this in this comment section. I haven’t read Werner’s stuff, and judging from the nonsense headline you cited, I’m not going to read his stuff. I stick to reality.

The paper I cited deals with empirical evidence. The researcher looked at bank’s internal accounts while he took out a loan. He had first account for taking the loan and second account in another bank where the money was transferred after he got the loan.

After loan was made and paid to the second account, first account had 200k liability and second had 200k asset. So the sum of the assets and liabilities is 0.

And as I said before the money for the loan did not come from any other account. What Werner described in his paper is completely in line what the central banks have been admitting in last few years. For example Bank of England said:

“Commercial banks create money, in the form of bank deposits, by making new loans. When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created. For this reason, some economists have referred to bank deposits as ‘fountain pen money’, created at the stroke of bankers’ pens when they approve loans.”, Money creation in the modern economy(2014)

easy way to explain is :

only central bank can write check out of nothing, let say 10 million. they can do that because by law they have machine which makes money.

Bank of America, Wells Fargo, JPMorgan Chase, … by law can not do that

banks by way of fractional reserve and central bank together create additional money/credit.

meaning if you have savings in the bank which is not covered by government insurance — you can lose that money — like in cyprus

That’s the static picture. Dynamically, the bank’s mission is to make sure every day that the daily deposits plus the reserves at least equal the daily withdrawals (caused by loans.) That way the bank stays liquid,and stays in business until the next day.

If they fall short by accident, there’s very short term credit from the FED to keep them going while things sort themselves out.

If they really have over-loaned, and will persistently fail to get the daily deposits to cover the day’s withdrawals, then they need to do something. They can borrow money from banks that *are* getting the deposits, they can borrow less-short, or even long, term from the FED. Maybe sell some loans to outfits that can fund them. And have a look at their lending practices.

Wolf, have the BOE lost their marbles? A genuine question I’m trying to understand!

“This article explains how the majority of money in the modern economy is created by commercial banks making loans.”

Paul,

Read the original BOE article you refer to, and not just the headline. You will learn that the BOE says that the banking system AS A WHOLE creates money via deposits, but that an INDIVIDUAL BANK MUST fund the loans it makes in some way, most of it from cash it receives from depositors.

This is key to understanding the banking system – and that a bank MUST fund its loans in some way (most of it from deposits).

Wolf, even though you may be growing tired of the repeated questions about money creation, this back and forth has been extremely valuable to me. Seeing the flawed arguments being presented and then reading the methodical debunking of those arguments is instructive in a way that straight up explanations are not. For example, if you simply explained the way that the banking system creates money on a whole (and that individual banks cannot do this), then I would easily understand. But if I then went to another site and read some of these convoluted theories on money creation, I may see the flaws, but likely I would not. People can make very convincing arguments by using dense language and circular logic. So, in short, thanks for being so active in the discussions.

On a similar note, I face this kind of thing all the time as a scientist. Pseudoscience is everywhere and when I read the things people say, it’s so obviously false that it almost seems funny (or I assume that the purveyors have mental health issues of paranoia and whatnot). But then people believe it. Hook line and sinker. And when I sit down with someone to explain the flaws in this or that pseudoscience, it becomes apparent how the believers were not dumb or lazy per se. Usually, they were busy – as in got a million things going in their already busy overworked lives with stress and kids and illnesses and financial problems and politics and on and on. So, when someone offered a simple explanation for something… an easy answer among all the hard problems in life… well, it’s just kind of like a relief. Just my two cents – which by the way is a hypothetical two scents that does not add to the money supply… unless of course a bank take my two cents and loans it out as four cents to another bank ;)

“For example, if you simply explained the way that the banking system creates money on a whole (and that individual banks cannot do this), then I would easily understand.”

it is made this way on purpose ( too complicated and not easy to understand )

easy way to explain is :

only central bank can write check out of nothing, let say 10 million. they can do that because by law they have machine which makes money.

Bank of America, Wells Fargo, JPMorgan Chase, … by law can not do that

banks by way of fractional reserve and central bank together create additional money/credit.

meaning if you have savings in the bank which is not covered by government insurance — you can lose that money — like in cyprus

Marcus,

Thank you! I also want to thank the other commenters here who contributed to the debate.

I’m grateful for all the commenters who challenge me and others here on this topic — because it makes us think through things we don’t normally think through since we just take them for granted – or last thought through them decades ago and forgot. And it’s really good from time to time to sit down think stuff through.

But it does get exhausting occasionally ;-]

Canada and Australia have zero minimum reserve requirements, and even in the US it only really applies to chequing accounts. The Bank of England debunks the money multiplier myth in “Money Creation in the Modern Economy” (pdf warning):

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-in-the-modern-economy-an-introduction.pdf

@Adrian

That’s a good article. Thanks for posting.

Wolf, with all due respect, that’s not how it works. The loans come first and banks are not constrained by the deposits to make loans:

Very few people understand how the modern banking system really works.

They have in their heads a model they learned from text books in which banks take deposits from customers, then lend out those deposits as loans. In reality, banks fund their loans by borrowing in the interbank market.

How the Banking System Really Works https://www.cnbc.com/id/44931200

THE MAN,

The article you linked is complete hogwash. It was written in 2011 by a guy who used to work for Business Insider before being at CNBC. He was never a banker, or a central banker, or an economics prof, but just a kid with some crazy theories. So here is why this article is just nuts:

It says that banks fund their loans almost exclusively by borrowing from each other in the interbank lending market. This would mean that interbank lending would be in the many TRILLIONS of dollars in the US alone. It was never big to begin with – peaked at $500 billion in 2008. And it has since shriveled to just $68 Billion… minuscule considering that the biggest banks in the US have EACH over $2 Trillion with a T in assets (mostly loans), and that all US commercial banks combined have $17 Trillion in assets on their books (commercial loans, credit card loans, auto loans, mortgages, etc.).

So the first few paragraphs about the article are just NUTS.

The rest of the article is about government finance, and it gets even nuttier. It’s promoting Modern Monetary Theory (MMT), which is a hogwash monetary religion about how governments should fund their spending.

I ban MMT promos from this site. And I block MMT trolls, of which there are many. If they want to spread this hogwash economic religion, they need to find some other place. Or they can pay me to buy a banner ad on this site.

Please don’t post this crap here – or else I’ll have to consider you an MMT troll :-]

“The truth, however, is that the reserve requirement does not act as a binding constraint on banks’ ability to lend and consequently their ability to create money. The reality is that banks first extend loans and then look for the required reserves later.”

Read more: Why Banks Don’t Need Your Money

https://www.investopedia.com/articles/investing/022416/why-banks-dont-need-your-money-make-loans.asp

Read the article and not just the headline. This piece if about the banking system as a whole, how it creates money. And it’s confusing all kinds of stuff in the process. Why don’t you read an article about this by people who know, such as the New York Fed, and not some hacks…

https://web.archive.org/web/20040203023009/http://www.newyorkfed.org/aboutthefed/fedpoint/fed45.html

You guys just don’t give up, do you? You have this believe that a bank doesn’t need deposits, and you cling to this believe no matter what the facts or the data, and you try to pick articles whose headlines seem to support your point of view. You can believe that the earth is flat or whatever, as far as I’m concerned, but you cannot post this crap here.

THE MAN,

Also “required reserves” are not how a loan is funded. Required reserves are deposited at the Fed, figured as percent (10%) of overall deposits. They have nothing to do with loans, and everything to do with deposits.

Loans are funded from deposits (and other funding sources such as securitization of loans, bonds, etc.)

I did not see john Paulson crying in 2008…he just played the fall through his cronies at Goldman Sachs when they bet against the same toxic mortgages they were selling…trust me…there is enough smart money out there positioned for the fall…but smart money usually stays quiet.

What’s wrong with the FED ending risk-free interest money? Banks will just have to work harder to loan money out to people and businesses who need it. Just hire some people and compete and do it?

I personally think this is a good thing for the economy. People will be encouraged to save more, earn interest instead of gambling on wall street, which survives on such money being present in that market.

It’s ok for hedge funds and speculators to earn 3% of one trillion instead of 3% of four trillion.

Great article Wolf! I watch way too much CNBC and I constantly hear the WS economists saying the Fed is going to fast. Give me a break! And don’t get me started on Cramer, who said to load up on Bear Stearns on their way to collapse. Cramer also said no one will quit Facebook a few months back. I happily deleted the FB app and so did millions of others.

The only way for true price discovery with stocks is to have alternative investments. With the Fed holding rates at zero for 8 years, most investors had no alternative but to invest in the FANG names and other “high growth” stocks. That game is slowly ending.

I fall victim to watching/listening to CNBC as well – thinking it is best viewed as a contrarian indicator. I deleted FB (and NFL) and things are now so bright I have to wear shades.

What do you use instead of Facebook?? Axin for a friend.

I killed my entire FB account. I’m trying out “Minds” as a less annoying (and invasive) alternative. I’m also trying out weird things like calling people, seeing them in person, writing on scraps of paper called letters and postcards, NOT hearing every dumb thought my friends and family think, not POSTING every dumb thought I think, not having my life be a commodity… Nothing you could reasonably short FB with. ;)

excellent choices!!!

Phone calls…coffee chats…real news…real friends. :-)

Never had it never will. I saw on the news last night they are using the platform for a dating site in Canada…your profile and inclinations sorted by the all-knowing FB algos.

So many of the youth nowadays don’t know of the days before these criminally low-interest rates back when being a saver meant something, I wonder if our collective lack of thrift is a result of this. After all, what’s the point of saving if inflation eats away at all your hard work. Just something to think about.

Ha. So much wrong in the comments, including fictional reserve spew.

Please take some basic courses in money and banking. The banks literally got a risk free parking place for 1.7 trillion dollars, so they took it. The cost of the funds was simply being a bank with static deposits.

Now, the cost of the funds is increasing, slightly. Meh. Yes, competitive banks now pay above the Fed reserve rate. Back to the 3-6-3 world. 3 percent on deposits, lend at 6 percent, go golfing by 3pm to get to happy hour.

Remember, these are EXCESS reserves, not required. So, literally $1.7 trillion in lending capacity sitting there dormant. The Fed just functioned like a big bank, taking in cheap deposits and lending long into the housing market for 10 bloody years. And they made the difference, LoL.

So, until excess reserves flatline, we don’t even have a normal money policy, and higher rates are going to be very difficult to maintain. So, if QE4 shows up, we are still in the Japanese restaurant.

Now, back to the regular whining.

BTW, this is also why the huge increase in the Fed assets was not really printing $4 trillion and spending it. Which is why this is happening, but doesn’t matter to a real money supply analysis.

Think about it.

yep. No velocity. Never lent out…just parked. So the $4 Trill never hit the economy.

Yepper again…why velocity is just barely beginning to pick its head up now too…

As a result of ZIRP, a dozen or so online banks emerged, offering high interest saving accounts (insured, but…). It is a foregone conclusion where these deposits ended up invested (RE). I wouldn’t be surprised if a few went belly up even with ever so gentle tightening. The depositors are not greedy investors, only interest rate repression refugees.

The only question is, when do we start seeing a few bombs going off?

Until then, it is half steam ahead.

At a normal interest rate I would have had enough savings to never have to touch my principle and live comfortably.

After March 2000, and Oct. 2008 I wasn’t thrilled with putting it in the stock market. At a .003 interest rate I had to draw down my principle. Now that it’s gone they are starting to pay interest again.

Wonder if there are many like me. I never expected the Fed to go this crazy for this long. At least their banking friends were saved… for awhile.

I don’t think there were any flaws in your logic. The Fed acted with extreme irresponsibility. Nobody expected the Fed would go out and double down on moral hazard, immediately after the last debacle.

The Fed has created a huge bubble and ruined the future for many years to come. We will either have austerity, or hyperinflation followed by extreme austerity. Plus, there’s a good chance for civil unrest, given how angry people are with the arbitrary wealth transfers caused by the Fed’s interventions.

@xear

None of us had any idea it would be taken to a QE3 level of insanity. I am very sorry that your principle has eroded so far down. This is the stealth transfer of wealth from the fixed income investors to the equity investors. Many of us hadn’t realized how nefarious a plot it was as it occurred. We only came to our senses in 2015 when the Fed backed down yet again for the sake of the market. At that point i realized that the greed had no limits.

Bernanke and Yellen knew what they were doing every step of the way and I hope they can enjoy their bloated retirements without guilt. I am sure they will. It takes a special kind of person to knowingly do what they did for 10 years.

My only concern is that Wall Street will win again and that these meager crumbs that we have now will be once again taken away.

I think many of the ultra rich do realize how precarious the equity market has become, and a lot of the ultra rich have always parked vast sums of money in CDs and treasuries for safety and pre- recession. The 10 year UST last had some life in 2007, and so all of those notes have matured. Perhaps they too are getting a bit irritated at this point ;) ? A taste of their own medicine…….

Many have been using up their seed corn. What makes people angry is their arbitrary brainchild of “wealth effect” for some selected groups, contrary to their mandate(s).

I am a little slow on the uptake. As interest rates rise I see bond investors which include pension and other retirement vehicles possibly negatively impacting an already gravely unprepared boomer generation as they sail off into retirement. I also see rising interest rates affecting Dollar strength which is crushing emerging market debt. Then of course we have extreme government debt levels at all levels. Rising rates on Trillions of debt is not something to take lightly. Then again there is the housing market probably already in bubble territory. I’m one of those concerned people that believe the system as we know it is very fragile and any distortion could create an overly outsized domino effect across the economic landscape.

I agree: recent readings indicate lots of boomers are unprepared for retirement. However, I suspect this has, more-or-less, always been so: not everybody has the discipline & diligence to manage their financial affairs.

If you think that’s bad (and it is), wait until it dawns on millennials (born 1982-2000) that at age 40, they have saved squat, zippo, nada, zilch. Kinda makes you want to run right down to Starbucks for another $8 grande cafe mocha cappuccino latte dusted with Sumatran nutmeg (250 of those a year = $4,000).

One proposed solutions is socialism: the majority simply votes to take money from others who have worked to earn it. The problem here is the market value of MOST asset classes literally evaporates under socialism (how much would Apple stock be worth under socialism – 66-75-90% less?).

Ooops – 250 (one every business day) $8 Starbucks = $2,000.

I just turned 72 3 days ago, I’m old.

Not surprising really. Awful people do awful things.

This Fed has one mission prepare the bond market for massive new supply.

Sorry Wolf, I have to disagree with you about the Fed creating money, but that is the purpose for which they were created in 1913. They are suppose to create money in a liquidity crisis. This “money” can take many forms, a line of credit, or negotiable instruments, but it lands up being money.

They bailed out Bear Stearns and AIG with a line of credit, money out of nowhere. They also bailed out the European banks with a currency swap, dollars for Euros, a TRILLION Dollars of money they also didn’t have, until they did.

Wolf, just to follow up on your correction of tom freeman above;

what if Bob deposits $1,000 and the bank lends the cash to Ted. But then Ted (or whoever he gave the money to) also deposits that cash with the same bank. I know that isn’t creating cash, but it is kind of like creating money because now the bank has two $1,000.00 liabilities but only $1000.00 in cash was ever involved. This was a problem under a gold standard and the reason a central bank was created was to protect the system when Bob and Ted both showed up for their money at the same time. The created money is “synthetic”. Or no?

This discusses the same question. Bill Gross: Show Me The Money.

https://seekingalpha.com/article/4053707-bill-gross-show-money

Thanks for the link. Stocks too. I mean, a stock’s price is implied from the last sale. The owners own shares. Not dollars. But they never measure their wealth in shares, always dollars. The dollars are synthetic. There’s no money sitting there and people who “save” in the stock markets are always surprised when it disappears and act like they’ve been robbed or something. Time for another gold article hahaha

bungee,

Every time someone deposits $1,000 at the bank, it creates a liability for the bank, and it creates an asset in equal amount. This was same under the gold standard. Accounting rules didn’t change.

In your example, the bank ends up with $2,000 in liabilities: the $1,000 it owes Bob (his deposit) and the $1,000 it owes Ted (when he deposits the proceeds from his loan at the bank).

And it has $2,000 in assets, the $1,000 it loaned to Ted and the $1,000 cash from Ted’s deposit in his account.

But half of this cancels each other out: the amount that the bank owes Ted = the amount Ted owes the bank. The net = 0

If Ted wanted to use the $1,000, he’d have to withdraw it, and then the bank would have only $1,000 in liabilities (the deposit it owes Bob) and $1,000 in assets (the loan to Ted).

Debits and credits balance. No money was created. Liabilities and assets rose by equal amounts. The gold standard has nothing to do with this. Bank accounting has not changed since then.

Money creation and money destruction takes place in the overall banking system, as loans and cash from deposits flow through the banking system overall. But an individual bank cannot create money, it MUST fund its loans.

“Debits and credits balance”

of course they do. But there is a reason it’s called fractional reserve banking. There’s a reason the fed was created. It’s to be the reserve in a pinch. If deposits were never lent out, there’d be no need for any of this. If Ted bought a $1000.00 car and the dealer puts the money in the bank, then yes, the bank has an asset of $1000.00 that Ted owes and a $1000.00 liability to the car dealer. They cancel and equal zero on the books which means they only have a $1000.00 liability to bob which is fully covered by bob’s $1000.00 deposit. I get that it’s zero. Balanced. But in practice both bob and the car dealer think they have $1000.00. These “assets” circulate just as good as dollars! There are $2000.00 being traded out there but it started as only $1000.00. And the banks books still balance. It’s whats meant by “synthetic.” These synthetic dollars are debts and are hoarded and saved which can cause a liquidity crisis when depositors want cash. A bank’s accounting is no doubt impeccable. But what does it mean in real life?

Look, we don’t need a bank to do this. I have $1,000 in cash, and I lend it to you, and you give it back to me, but instead of paying off the loan, we agree that you lend me this $1,000. And then I lend it back to you, back and forth, until I owe you $99,000, and you owe me $100,000. None of this is money. It’s just entries that cancel each other out. No one can use these numbers to buy anything. These are not dollars that are “circulating,” as you said. The only money is the $1,000. And no money was created.

People who want to believe that a bank can just create money out of nothing to lend it out come up with the silliest example to support their believes.

A bank MUST fund its loans. No commercial bank creates money (but central banks can).

That said, as I said many times before, the banking system overall creates (and destroys) money by a very different process. And I think this is what you’re alluding to… Just have Ted borrow from Bank A and deposit this money in Bank B, and Bank B can then lend out this money (minus reserve requirement) to Paula, who deposits it in Bank C, etc. In this process no bank creates money, and each bank has to fund its loans, but the process between banks creates money.

Can’t attach this reply to WR’s reply to your post, so I’m attaching this to your post.

From WR’s last para…

“Just have Ted borrow from Bank A and deposit this money in Bank B, and Bank B can then lend out this money (minus reserve requirement) to Paula, who deposits it in Bank C, etc. In this process no bank creates money, and each bank has to fund its loans, but the process between banks creates money. ”

So you’re (WR) saying banks A, B and C between them can create money, right? But not A, B or C on their own, right? If so, what’s stopping A, B and C, in the above argument, being the same bank, and so a single bank has created money? Or am I misinterpreting what you’re trying to say?

Or perhaps we’re all arguing past each other, using the same words but with different meanings. Which I think is likely the case, as there are some pretty bright people who do think banks can create money out of thin air[1]. The most common way a bank does it is to lend £100k, say, against an asset such as a house. The house[2] goes in the assets column which is balanced by a £100k deposit in the liabilities’ column. That £100k is £100k that wasn’t in the economy prior to the loan being taken out[3].

[1] But within capital requirement restraints.

[2] Actually, first charge on the house.

[3] To keep it simple, let’s assume the house builder banks with the same bank, as does everyone else that gets to touch any of the money generated by the £100k loan (which slowly disappears as it is repaid).

“Money creation and money destruction takes place in the overall banking system, as loans and cash from deposits flow through the banking system overall. But an individual bank cannot create money, it MUST fund its loans.”

Yeah. That is the key to it, isn’t it? But the banks don’t have to collude one time to do this. They can bootstrap each other to gradually build to any amount of money (in total) at all in the system. As long as each bank plays within the system’s (community of banks’) rules. Cameron Murray wrote a post once about “Game of Mates” (also the title of his book) describing this, also apparently muck-raking about the uses for the money they create.

The actual title of the Cameron Murray article I was thinking of is “The Bank Competition Myth” (https://gameofmates.com/2017/05/17/the-bank-competition-myth/) The point is that no bank can generate extra money excessively beyond its share of the business overall. But if they all do their little bit every day, it can build up to a lot.

As of now nothing has happened to the stock market, meaning to say the gyrations have not impacted the index much. Thus when these cry babies at Wall street are crying the Fed is able to brush it off.

The BIG question is what happens to this nonchalance when the market really takes a hit. If one goes by past history at the Fed, it will be on its knees asking for forgiveness of Wall street for having raised rates and drained liquidity (basically acting beyond their brief, which is to provide free money to these scamsters) and oblige their masters soon thereafter.

Bungee

Allen deposits $1000 into Bank X, which now has a $1000 liability (Allen’s deposit) and a $1000 asset (Allen’s cash). Bank X loans $1000 to Bob, debiting (reducing) cash asset and booking a $1000 asset (loan to Bob). Bank X now has a $1000 liability (for Allen’s deposit) and a $1000 asset (loan to Bob). At this moment, Bank X cannot make anymore loans (no loanable assets).

Bob pays $1000 to Chuck, who deposits the cash in Bank X, which now has 2 $1000 liabilities: 1 for Allen’s deposit & 1 for Chuck’s deposit. Banks X has a $1000 asset (Chuck’s cash) and a $1000 loan asset (loan to Bob).

There may be an infinite chain of deposits turned into loans, however, AT ANY GIVEN POINT IN TIME in this simple example, there is never more than $1000 available for lending: a deposit must occur BEFORE the next loan can be made.

I see what you’re saying.

See my above response to wolf and let me know If it doesn’t make sense.

Wolf is a black-belt finance guy who has a knack of decomposing & explaining complex topics like yours.

My reading of your hypothetical is it’s composed of a number of highly complex topics, some of which are unrelated and somewhat misstated (fractional reserves, gold standard, synthetic money, cash liquidity plus a couple others).

One hypotheticals you seem to be struggling with is even in a very healthy bank (with 100% performing loans), almost all depositor’s physical cash (a bank asset) is gone (it’s been loaned out, also a bank asset); however, the bank retains the obligation (a bank liability) to repay depositors. If the tiny statistical possibility that 100% of depositors demand their cash actually came to pass, the Fed is chartered to provide the bank with the required physical cash.

This Fed cash comes from other routine Fed activities (aggregating other bank reserve deposits), and would have to be paid back. Loans could either be called in early or sold approximately at par (we’re assuming 100% performing loans).

Hi Javert Chip,

Thanks for the response.

“Wolf is a black-belt finance guy who has a knack of decomposing & explaining complex topics like yours”.

Totally why I sharpen my worldview here.

“If the tiny statistical possibility that 100% of depositors demand their cash actually came to pass, the Fed is chartered to provide the bank with the required physical cash.”

This gets to the root of the problem that laypeople on this site (like me!) and experts are having, and that is with the idea of clearing. In Wolf’s hypothetical to me he describes a situation that NEVER clears. The tiny, statistical possibility of everyone cashing-in is the system trying to clear. But laypeople (like me again!) are suspicious of a system that cannot clear. The analogy often used is musical chairs – the fed supplying new chairs is of little comfort. It’s why some advocate for a return to a gold standard (def NOT me) because the system theoretically clears perfectly.

but a question: if banks make loans, say mortgages, and then these assets are bundled and traded and saved, haven’t we created money in somone’s mind, regardless of accounts balancing? That value is how I think of “synthetic” money. The value of your bundle is based on the sale of another just like it. I know I’m going in circles here and I think you hit the nail on the head in one of your earlier comments:

“People who cannot understand the basics are not investing, they are gambling”

and rest assured that when I’m in the markets I am totally gambling and I know it. hahaha. Physical gold please.

one last subtle point as food for thought: the bank in my simple example essentially has a short position on money, no? They borrow it and invest it with a promise to return it at full value. So banks in general will always be pro inflation so that they can repay in easier dollars. And that seems to be the point of the article; they’re crying about money that’s getting more expensive.

“and that they’re earning once again more than inflation on their money “…I would say they might earn more than reported price inflation but they are not earning more than the monetary inflation.

If the Government is running a 6% fiscal deficit, then that is 6% monetary inflation. The saver is not keeping up with the monetary inflation created by Government deficit spending. Federal debt trades just like money so it is money and contributes to the total supply of money equivalents.

My Credit Union provides a very easy to understand financial statement every year. They have a simple ‘front page’ and a more detailed ledger/balance sheet. They also provide a statement of other assets including land, buildings they own, etc. The Union has 7-8 branches and the Board of Directors are local residents who we elected based on their expertise. The employees are union and we know their salaries. Management are excluded but they do NOT receive bonus payouts of extra shares for doing their job.

I don’t think I could/would believe the statements produced by a Wells Fargo regardless of who provides the oversight. I always think of Enron, or the movie Too Big to Fail where they ‘portrayed’ Dick Fuld and the sunglass-wearing bandit running Countrywide.

When I used to deal with RBC about 40 years ago I would read their statements and get pissed off they made so much money…on my deposits! :-)

You guys need to look at how real world large banks actually operate.

Assume a 10% fractional reserve requirement. (Actually it’s lower, but 10% makes the math easy.)

During the regular course of business one day, MegaBank decides to loan money to X-Corp. MegaBank creates an account for X-Corp with $1,000,000 in it; this is now an asset for X-Corp and a liability for MegaBank. MegaBank also books a $1,000,000 loan to X-Corp (asset for MegaBank) and X-Corp’s CFO marks down the $1,000,000 debt to MegaBank (liability on X-Corp’s books). Everything matches up, so far so good. Note also that MegaBank has $1,000,000 in deposits on hand from this transaction, so the reserve balance is healthy. In fact, MegaBank’s liabilities here are $1,000,000, so at 10% reserve it only needs to keep $100,000 on hand. Therefore, at the end of the day it deposits the extra $900,000 as a reserve balance with the Fed, and collects interest on the excess reserves for a little while. MegaBank’s books close the day with a new $1,000,000 asset (the loan to X-Corp), plus a liability of $1,000,000 (X-corp’s account) consisting of a balance on-hand of $100,000 and $900,000 in reserve credit with the Fed. Everyone goes home happy AND no prior reserves were needed AT MegaBank to create the loan.

A few days later, X-Corp pays its supplier, Y-Corp, $1,000,000 for a shipment of widgets. The credit moves through ACH out of its account with MegaBank and over to GigaBank where Y-Corp has its account. GigaBank finds itself with $1,000,000 in excess reserves and deposits them with the Fed, while MegaBank marks down its $900,000 reserve balance and its internal $100,000 reserve (this is how ACH works!!). At the end of the day, the accounting computer at MegaBank tallies up the numbers and says they need a $1,000,000 reserve liability to balance their $1,000,000 loan asset (because they’re a bank, it has to balance!), so MegaBank looks to the overnight money market to borrow, and if that fails then it borrows the $1,000,000 from the Fed…

At this point: X-Corp owes MegaBank $1,000,000 (an asset for MegaBank), and has $1,000,000 in widgets from Y-Corp. Y-Corp has a $1,000,000 deposit with GigaBank – a liability for GigaBank, which they have kindly shifted to the Fed in order to collect a few dollars in interest. GigaBank’s $1,000,000 liability to Y-Corp is balanced by the $1,000,000 asset at the Fed. MegaBank’s $1,000,000 asset owed by X-Corp is balanced by their $1,000,000 liability to the Fed.

None of this credit was ever printed on paper, but with the Fed tying everything together behind the scenes, $1,000,000 in new credit was created WITHOUT pre-existing reserves (those are borrowed when and as needed). In this simplified example the banks in need of reserves borrowed them from the Fed, which is possible, but historically they draw upon the overnight money markets where whoever has extra deposits lends them out.

Now, here is where the rubber meets the road. Wolf is generally right that the reserves to be lent had to be in the system somewhere, for MegaBank to draw upon the money market at close of business. But everyone on the other side is ALSO right, because the reserves did NOT already need to be at MegaBank for them to issue the loan.

Normally the system has adequate reserves, because the Fed has created plenty of Reserve Bank Credit for everyone. The banks don’t worry about getting the reserves they need, they are out there and the system balances itself every night. This is the direct effect of all the Treasuries sitting on the Fed balance sheet – the money that the Fed created by buying those Treasuries IS the banking system’s reserves. And right now there are excess reserves so no worries.

The interesting situation happens when the Fed unwinds its balance sheet, the Excess Reserves go away, and credit gets a bit tight. Now if MegaBank issues a loan and finds itself short on reserves in the ordinary course of business, it needs to borrow from the money market, but No One Will Lend. This is what happened in 2008. The classic role of the central bank is to be the Lender of Last Resort – the Fed DOES have the power to create credit from nothing without needing to find reserves – so MegaBank gets the money. But the Fed charges a punitive rate for this service, and MegaBank gets the message that it can’t create more loans than the Fed cares to support! This transaction also shows up on the Fed’s reports and everyone paying attention – which includes GigaBank – knows that someone got in trouble and thus that the system is approaching its credit limit. GigaBank now knows that MegaBank is short on reserves and might look to tighten the screws on MegaBank if they wish…

This is how the overall supply of credit is constrained by the Fed. Wolf is right that reserves are needed to create credit, but he’s wrong that they have to be in the bank before the loan is made. So long as the bank believes they can readily get the required reserves from the money market, before the books are balanced at the end of the day, it can loan as much as it likes.

“Scarcity” simply means “capitalism”. You know, the best, most favourable projects and endeavours proceed and those deemed to risky or offering poor returns do not. That monetary scarcity then gives a signal for real world resources like manpower, land etc. to follow in its wake on the accountant’s discounted cash flow spreadsheet.

Scarcity should mean de-zombification of the economy. Who doesn’t like ‘scarce’?

What’s not surprising is that the FED caved

In this cycle, the Fed has not caved yet. On the contrary.

That’s not to say that it won’t cave in the future.

Maybe you should have said, “What’s surprising is that the Fed has not caved yet.”

That said, in terms of bank regulations, the Fed is caving.

It already has done so in a few areas, and today it was reported that it is going to water down the stress tests and make them easier to pass.

Perhaps that’s the comprise with the White House: we’ll soften bank regulations (a big agenda item for Republicans) but we’ll stick to our interest rate course.

The campaign has kicked up in Canada too. Benjamin Tal – chief economist at CIBC – warned last week that further BoC rate hikes would be a policy mistake and that every recession we ever had was caused by central bank tightening. Apparently central banks are only supposed to loosen, never tighten. How that works when you get to the zero bound is something Benny never explained.

Wolf, great article. I get so pissed off every time the stock market falls 500 points and its the “end of the world” on Wall Street while if it rises 500 points in a day like it did this week, well that’s “just the way it should be”, and tomorrow it should go up by a thousand. These Wall Street firms spend all their time creating these “forward” earnings 10 years out telling everyone how rich they will be if you listened to them and buy whatever they are peddling. They don’t care one iota about the future except their own, and that is focused on winning the next 30 seconds, by producing nothing more than yadda, yadda, ya. Talkers, whiners, wailers, cheer leaders, carnival barkers, but almost no doers, makers or producers, and the rest of us are just suckers to be fleeced. In this they are assisted by the various bureaucrats who assigned to protect, have become like scavengers following and living off a defeated army, bayonetting the wounded of savers and producers, dreaming of joining the ever Victorious Army Of Wall Street. I like Powell, he is trying to do what no one, to my knowledge, has done, that is deflate rather than pop the bubble(s). Strangely, he is actually trying to save this Wall Street rabble, but no it’s full speed ahead, and don’t mind the icebergs…

There’s a reason US indexes reverse intraday losses 75% of the time within 48 hrs. And why a 500 point gain is never reversed within 48 hrs. The US stock market (and it’s wealth effect) has never been so integral to the economy as it is now. As a trader for over 25 years, I have never made more money. The market has never been so manipulated. It’s always been controlled to some degree. But you can set your watch (literally) to these pre-programmed trading patterns. Valuations are double historic norms. Trillions in buybacks contine. And every FA in the US will tell you how things are UNDERVALUED and that it’s a great time to buy. The illusion is real.