Fears that the bull market died sent people and algos scrambling out of the way.

There were company-specific debacles that sank some of the gorillas, such as Goldman Sachs, Apple, and – oh gosh, not again – GE; and there was the general issue of fears circulating that the bull market has died, with people and algos trying to scramble out of the way:

- The Dow dropped 602 points, or 2.3%, to 25,387.

- The S&P 500 dropped nearly 2% to 2,726.

- And the Nasdaq dropped 2.8% to 7,201.

Goldman Sachs got re-embroiled in corruption allegations

Goldman Sachs shares [GS] plunged 7.5% to $206.05 today. They’re down 24% from their 52-week high in March.

The company came under renewed scrutiny for its role in the 1MDB corruption scandal when it emerged late Friday that then-CEO Lloyd Blankfein was the unidentified Goldman executive who attended a 2009 meeting with Malaysian Prime Minister Najib Razak, Malaysian financier Low Taek Jho, and about a dozen other people, referenced in the US indictment unsealed on Friday.

Goldman Sachs arranged $6.5 billion in bond deals in 2012 and 2013 to fund 1MDB. The DOJ alleged Low Taek Jho paid bribes to officials and attempted to launder billions of dollars stolen from the fund. According to prosecutors, about $4 billion of those funds were stolen by numerous people, including friends and family of Malaysia’s prime minister at the time.

Former Goldman top banker for Asia, Tim Leissner, pleaded guilty. In the heavily redacted guilty plea, released on Friday, he said: “I conspired with other employees and agents of Goldman Sachs very much in line of its culture of Goldman Sachs to conceal facts from certain compliance and legal employees of Goldman Sachs.”

General Electric struggles with a “sense of urgency.”

Though shares [GE] have already plunged so much, they nevertheless plunged another 6.9% today to $7.99 a share, after its brand-spanking new outsider CEO, Larry Culp, on the job for only six weeks, got on CNBC and declared boldly and with refreshing straightforwardness what everyone has known for a long time, that after $40 billion of share buybacks since 2012, GE has too much debt.

To avoid a debt restructuring and stay out of bankruptcy court, GE has to sell whatever it can to try to whittle down its debts. This has been the theme for a while. Now the company is doing it with “a sense of urgency,” he said. And he emphasized: “We have options.”

There’s GE’s healthcare business for which GE is considering an IPO, he said. And there’s Baker Hughes, which GE acquired at the worst possible time and needs to sell — on the principle of buy-high-sell-low — to “generate real cash to bring leverage down,” as he said.

But selling cash-flow-producing business units to pay down an overwhelming pile of debt cuts down on cash-flow producing business units the company still has to service the remaining debts. Dismantling an overindebted financialized industrial conglomerate is always ugly.

“It’s tough to play offense with the balance sheet in the shape that it is in,” Culp said. Shares are down 58% from a year ago because investors have figured that out a while ago.

Apple suppliers unravel

Apple shares [AAPL] dropped 5.0% to $194.17, after its main supplier for its Face ID technology, Lumentum Holdings, chopped its own revenue and profit forecasts, blaming reduced orders from “one of our largest” customers “for laser diodes for 3D sensing” — which can only be Apple. Lumentum shares [LITE] plunged 33% to $37.50.

This came on top of a warning today from another Apple supplier, screen maker Japan Display Inc, which had come on top of warnings by Foxconn and Pegatron a week ago that they would halt plans for additional iPhone XR production lines.

Then JP Morgan analysts had the temerity to cut their price target for Apple by $4 to $270, based on weak orders for the new iPhone XR. Alas, this is still nearly 40% above today’s reality.

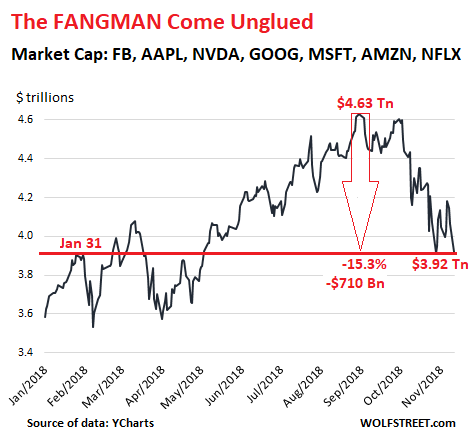

Apple is the biggest gorilla in the FANGMAN stocks – Facebook, Amazon, Netflix, Google’s parent Alphabet, Microsoft, Apple, and NVIDIA. And the other six FANGMAN stocks also got hit today:

- Facebook [FB] dropped 2.4% today, to $141.55 and is down 35% from its peak in July.

- Amazon [AMZN] dropped 4.4% to $1,636.85 a share and is down nearly 20%, from the peak on September 5, when shares nearly kissed for the briefest moment $1 trillion.

- Alphabet [GOOG] dropped 2.6%. At $1,038.63, shares are down 18% from the peak in July.

- NVIDIA [NVDA] plunged 7.8% today to $189.54 and is down 34.5% over the past six weeks and down 11% from a year ago.

- Netflix [NFLX] dropped 3.1% today to $294.07 and has plunged 30% from its high in early July.

- Microsoft [MSFT] fell 2.4% today to $106.87 and is down 7.5% from its peak at the beginning of October.

In terms of dollars, the FANGMAN stocks have lost $710 billion from their combined market cap peak on August 31, having plunged 15.3% from $4.63 trillion to $3.92 trillion (data via YCharts).

But in terms of the longer view, the FANGMAN stocks have just barely begun to unwind the ludicrous skyward spiral over the past few years. The current sell-off just takes them back to the end of January.

At the other end of the spectrum from these seven more-or-less-tech gorillas are a couple of thousand smaller companies tracked by the Russell 2000 small-cap index. It fell 1.8% today to 1,549 and is down 11% from its peak at the end of August. It’s back where it first had been in December last year.

Neither the FANGMAN nor the Russell 2000 took a big hit during the January-April sell-off. But now they both are back where they’d been before that sell-off. That both the largest gorillas and the smallest featherweights are caught in the downdraft show just how widespread the sell-off is.

Retail investors were lured to GE by the siren song of a “buying opportunity” and a fat yield throughout the sell-off. Read… This is What Retail Investors Did with GE This Year as it Plunged

[Correction: The share buyback data on GE has been corrected; it previously reflected an error on my part]

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“I conspired with other employees and agents of Goldman Sachs very much in line of its culture of Goldman Sachs to conceal facts from certain compliance and legal employees of Goldman Sachs.”

I think I speak for all cephalopods – both small and giant – in that they find it insulting to be compared to Goldman Sachs.

And on the subject of marine fauna, a fish rots from the head, Mr Blankfein.

When I think of the term “marine”, it reminds me of why we celebrate all our military folk, retired and active. I would consider Blankfiend as more of a parasite–always feeding off a host and only offering feces in return. I’m PRAYING one of these sealed indictments has his slimy, scuzbucket, cesspool-loving name on it….

WHY SO BITTER?

He was only doing “Gods Work”.

“WHY SO BITTER?

He was only doing “Gods Work”.”

Methinks that Monsewer Blankfein misidentified the entity upon whose behalf he actually toils so diligently: SATAN.

But, I can certainly understand his desire to obfuscate that entity’s true name.

When Ge Bottomed out at $6.66 while the SP500 also bottomed at 666 in early 2009, I figured it was time to head north and get some of that old time religion!!!

“It’s tough to play offense with the balance sheet in the shape that it is in,”

and, could one call the floating of 1MDB and IPO?

With a high percentage of Apple sales in China, which appears to be a slowing market, a higher US dollar that may hurt earnings, and given the stock was $120 only a couple years ago, below $150 could be interesting. Hopefully they don’t do anything stupid like build electric cars..

Quite a bet, given that massive wealth disparity, insecure employment the and high cost of putting a roof over one’s head means that, once the cheap credit stops flowing, vast swathes of the world will have no money whatsoever for shiny electronic gadgets.

Your money though. Feel free.

That would be interesting, an electric car shaped like an iPhone. :)

Yes an I-car That navigates hill and dale through the use of “brainless waves”.

Fundamentals don’t matter…

Until they do.

I bought AAPL at $95 a couple of years ago, when everyone was selling. At that price it looked like a solid value. I dumped it a few months later, at $130, but find it humorous that brokers had been recommending it over $200. Buy low, sell high – I will get back in if it goes back to 100.

As for the others, they are like trading bitcoin. Trading well above intrinsic value, they can get cut in half and still not be a good value

So what is “intrinsic value” of a bitcoin anyways?

Less than $0 based on the electricity it takes to create one.

Same with all non-fixed income assets that I own: it’s just another “precious” that I hope attracts more buyers than sellers.

Back in the bad old days of when men peed in men’s bathrooms and the US could still run a semi-competent elections…

A stock’s price was significantly determined by the NPV of future dividend distributions. With a little taken off for risk.

2banana

Money launderers & criminal enterprises (read: drugs & sex traffickers) love cryptos. Crooks who hack in & steal hundreds of millions in tokens probably think highly of them as well.

Oh, and millennials think this is the way to sudden (work-free) wealth.

Hi Javert,

My millenial friends and I steered well clear of that mess for the most part – the stories of people mortgaging houses to speculate on bitcoin couldn’t have been us since we’re supposedly “killing the housing industry” for avocado toast. That was boomers going long on that insanity.

depends on what premium you attach to making anonymous transactions

Bitcoins are the opposite of anonymous as all transactions become a permanent part of the ledger that anyone can download.

I assume that there is a group at a three letter organization tasked with assigning names to Bitcoin transactions.

If you insist on treating it as an asset, the Old Lady of Threadneedle Street can help with valuing it[1]. Hope they leave that page up for posterity.

[1] https://bankunderground.co.uk/2018/11/13/the-seven-deadly-paradoxes-of-cryptocurrency/

I would note that Philip went the opposite direction to GE – its healthcare unit became so successful that Philips spun off most of its other businesses to concentrate on its healthcare unit.

Buying GE Healthcare in an IPO would be like buying a former champion racehorse that just broke 3 of its 4 legs and the vets are discussing whether to shoot it or try to save its life for the stud farm (of course a real life modern alternative would be to harvest cells for cloning and then shoot it).

A quarter century of mismanagement and lack of product R&D has left GE Medical with so many products that are just DOA or grossly inferior to its competitors that it would take a massive infusion of R&D money to make better stuff to get GE customers to come back. The only thing I still like that’s made by GE are their Ultrasound machines. Everything else sucks.

Sad, because in the late 1980s and early 1990s, GE had great CT and MRI scanners and mammo units and dominated the US Radiology market.

And oh, in my last rant about GE and Jeffrey Immelt, I left out the debacle with GE’s acquisition of Amersham. The big product GE got was Omniscan, a me-too and not very good copycat gadolinium MRI contrast agent that was found a few years later to be one of the absolute WORST chelates of all the ones approved by the FDA at keeping the gadolinium from flying free and causing nephrogenic systemic fibrosis in patients.

Look closely to see if this lawsuit magnet gets included in the IPO or gets deep sixed somewhere else

At today’s closing price of $7.99, GE’s previous 5-years of $152 Billion in stock buy-backs has destroyed a cool $100 Billion (that’s $100,000,000,000).

If I were Imlet, I might try negotiating a lump-sum retirement settlement.

Makes you wonder.

If GE had invested $100 Billion in R&D, developing new products, training their workers, building new/modernizing factories, stayed away from obama and stayed even father away from becoming a “financial company that happened to make a few things…”

How much better off would they be now?

There is a lesson in there somewhere…

GE had been investing a whole lot of money in new product lines.

The big problems is many of these new products were not exactly met by crowds jumping up and down with excitement (see the Catalyst turboprop) and they have been having a lot of problems holding on to their R&D people, kinda understandable when the company has a maxi R&D center in Bangalore, which Jeff Immelt allegedly planned to use as a leverage against the US Government and which many employees saw as a one way ticket to the unemployment office.

If history has a constant is that when a company is on a downward slope it seemingly cannot do anything right reagrdless of real product quality.

The Catalyst turboprop is the first breath of fresh air in a market that despite its growth over the past two decades is still completely dominated by early 60’s designs, the Garrett (now Honeywell) TPE331 and especially the Pratt & Whitney PT6. Yes, these engines have been improved several times over the past five decades, but they cannot compete with a clean sheet design incorporating all the latest advances in design, manufacturing and materials.

One would expect companies to be very interested, but so far only Textron has bitten, and cautiously so. The Denali is not exactly a high priority development, coming in a world saturated by very similar aircraft.

The lesson is that neoliberal economics – the nub of which is that companies should be run only for the benefit of stockholders, not employees, and that businesses have no moral obligation to anyone apart from those stockholders (wholly mistaken thinking) – kills businesses and ultimately societies (yes, that too) with its race-to-the-bottom monomaniacal search for short-term stock price and dividend gains.

And yet apparently there is – still – no alternative to this model.

Apparently, your “neoliberal economics” model DESTROYED stockholders. It DESTROYED the dividend. It does not work.

I wish GE has rewarded stockholders with LONG TERM thinking.

Such as what I mentioned before. R/D investments, new product investments, worker investments, factory investments…etc.

++++

“The lesson is that neoliberal economics – the nub of which is that companies should be run only for the benefit of stockholders, not employees, and that businesses have no moral obligation to anyone apart from those stockholders (wholly mistaken thinking) – kills businesses and ultimately societies (yes, that too) with its race-to-the-bottom monomaniacal search for short-term stock price and dividend gains.”

“Investing” in stock buy backs instead of in R&D is what happens when companies are run (ruined) by accountants instead of engineers.

Who would have guessed that sadistic numbers-game BS like Sick Smegma and routinely culling a tenth of your workforce every year for intimidation purposes would cause problems with morale, initiative and recruiting?

It always seems to be the corporations with such arrogant certainty that its management techniques are so superior, and everyone else’s are stupid, who end up falling hardest on their faces.

Wow, thanks for the “nephrogenic systemic fibrosis” info! I am wondering just how many other imaging contrast agents will be found to be contraindicated for any human use. Angiograms can cause strokes and/or kidney damage days or weeks afterwards, so even this widely used diagnostic is dangerous. And even if they say (which they always do) that “only a small percentage” are affected, you can rest assured that *you* will be in that “small” subset. Doing an internet word search on all this stuff is just depressing!

The lawyer ads on late night TV are thick with Gd contrast MRI issues.

Yes, it’s now known that all gadolinium agents deposit some amount of gadolinium in brain and bone and other tissues regardless of whether the patient is in renal failure or not.

The linear class of agents are much worse than the macrocyclics, perhaps a hundred to a thousand times worse, and Omniscan is the worst of the linear class. Over a year ago the linear class- Omniscan, Optimark, and Magnevist, were flat out banned in Europe and South Korea. The FDA continues to allow sales with warning labels in the USA.

The info about generalized deposition of gadolinium spread, leading people with all sorts of the usual aches and pains and neurologic/psychiatric symptoms to blame the gadolinium contrast they got. A radiologist, Richard Semelka, compiled this list from a rather unscientific survey of these “I blame everything on gadolinium” support groups and labeled it “gadolinium deposition disease”- GDD. Right.

Chuck Norris’s wife was one of them and sued. So that got GDD lots more publicity, even though there isn’t any causal relationship proven yet (unlike nephrogenic systemic fibrosis for which there is a ton of proof)

But the handwriting is on the wall. I have no idea why GE continues to sell Omniscan – it’s just a dog of a product and will give whoever owns it a backlog of lawsuits

I just wanted to thank you for your excellent posts.

And I am honestly surprised ambulance chasers took so long to get on the case.

Since you obviously know your stuff, what do you suggest as a better option to MRI? CT and it’s potential for inducing cancer? I know they say it’s negligible, unless you become the statistical error.

Maximus,

MR scans don’t use ionizing Xray radiation, although they do radiate you with VHF TV/radio frequency waves. Much less risk. Pregnant women and kids get MR scans now for r/o appendicitis cases instead of CT ( everybody else gets CT because it’s easier and faster)

Most MR scans don’t use gadolinium contrast. In general, CT is better for seeing bone and capturing the fine details of areas of the body that move, like the chest, neck, and abdomen, but MR has superior tissue discrimination.

Contrast agents in both CT and MR help sort normal from abnormal, sometimes it is really necessary, often it is not needed

The macrocyclic gadolinium agents are much better, several orders of magnitude more stable than the linears. Dotarem appears to be the most stable of them all. The place I work at now uses Dotarem, but had used Omniscan up to a couple years ago.

The main reason the linear agents are still being used anywhere at all in the US is because the FDA hasn’t banned them and because of pricing and profit. Medicare and other payers pay the same for giving contrast regardless of what is used. And guess what? The linears banned in Europe have plunged in price, maximizing profits for MR scanner sites in areas where the patients don’t know better. The linear gadolinium agents are super cheap to make, so companies still make lots of money seling these linears

$$$

I’ve owned Phillips electronics in the past tv’s and vcrs, all good quality equipment and affordable. Owned some GE appliances too, they broke down every year or two like clockwork, super expensive to repair.

Ok, they haven’t even lost a trillion in value yet. When they go down a whole Apple or two, then let me know.

OMG, Goldman is evil? That’s crazy, next you will tell me that Google is evil too. Mind blown, didn’t their motto use to be: don’t be evil. Those bastards.

When the going gets tough, the tough BUY!!!

This is only the beginning. A banana republic political system deserves a banana republic financial market.

– I think Goldman Sachs now got what it deserved.

Goldman Sachs will get what it deserves when it will get back at being just another investment bank and not some mythical creature possessing supernatural powers.

For me it’s absolutely inexplicable how their alumni have been picked by governments as “economy doctors” time and time again despite their track record in the field: it’s kinda like people keep on buying Brand X razor blades despite the fact they are basically blunt pieces of steel. But they have a catchy advertisement jiggle and “everybody” uses them. ;-)

Given that DJIA & S&P have fallen less than 8% from its peak, nothing has happened as yet. That too in an extremely overvalued market meaning to say the market has just got from extremely overvalued to less extremely overvalued.

Probably the reason that there was nary a squeak from the Fed. The movie will begin when the pain begins. Let us see what comes out of the bag of tricks at the Fed then.

I totally agree KPL. The end of the FED PUT is just beginning. Wait until these unicorns have to actually pay a fair rate of interest on their debt. The VC cash will start drying up pretty quickly. My guess is the FANG stocks will move lower, but they are cash generating machines. The real blood bath will be in the smaller “tech” stocks like Snap, Aprn, W, Z, etc that do not have a business model to earn profits.

The S&P 500 today still sits above the peak valuation from 1929. The market gained over 300% since 2009. Losing 8% is a rounding error, not a correction or a crash.

They are (were) all doing, “God’s work!!”

Just wondering why a Goldman Alumni is now in charge of the worlds largest gold mining company?

The guy must be a masochist. His mining company’s stock is probably in the toilet and will be for the next several years.

Cuz he loves GOOOOOOLLLLD? (Insert possibly forbidden link to Austin Powers clip of Goldmember.) Sorry, but it was earl D who brought up Dr Evil.

Really though, Goldman Alumni in charge of ____ is never surprising. Are you saying he’s slumming it? Goldman Borg is just diversifying. Maybe they’re shorting the $.

All the loot withdrawn from

f

All the loot withdrawn from FANGMAN visible equities, may now be reassigned to their classified Secret Ops – off books divisions working under cover of “national security”. The $ credit might pool temporarily in bonds at negative real interest, otherwise it must find a constructive destination that at least breaks even. Spaceships ? Immortality research & treatment clinics ? It might (less likely) be used to rebuild infrastructure lost in the recent weather – fire disasters, pleasantly being provided to us by upper division corporate MIC global management. The toughest decisions are made at the top of the food chain.

Tyson – It doesn’t work like that. If AAPL opens, say, 5% down, ALL shareholders are worth 5% less. Even though no shares traded. No one gets to “withdraw” loot, because stocks are not bank accounts. This isn’t a case of taking wealth from one pocket and hiding it in another.

When a stock is topping out on the charts, during the trading day, a small handful of prior shareholders may unload a small fraction of a company’s shares upon soon-to-be-poorer future shareholders. Trading volume is much smaller than total shares outstanding, though, so only a few people get to be fortunate. But as the price declines ALL shareholders see their valuation decline. Only the few who sell early enough are able to convert paper share-wealth into cash, and even that part is zero-sum at the expense of the new shareholders.

When stocks go up, everyone feels wealthier, but when stocks go down, everyone discovers they are poorer. There is no secret stash of hidden wealth here.

You mean it’s… A PONZI SCHEME!!! :O

A specific example to approach the question from a slightly different angle:- Beginning in July 2018, The Swiss National Bank chooses to sell $50 billion in FANGMAN. Since the SNB is a bank of issue, it may also choose to buy 50 billion Swiss Francs with the $ credit in which the FANGMAN are denominated. These francs are effectively retired from from any collateral wealth assignment as long as the SNB “holds them” in bank. Since these 50 billion fr. no longer exist as circulating credit, the value of the franc appreciates relative to the U$D. The loss of $4.6 trillion in FANGMAN valuation would be a major deflationary event for the U$D, taken by itself; but most of the valuation change results in reassignment of $ credit to other ventures. Am I making sense ?

No. “Valuation Change” does not result in “Reassignment of $ Credit to other ventures”.

Valuation Change can occur in the middle of the night without anyone having a chance to reassign anything. If the price buyers are willing to pay in the morning is lower than the price they were willing to pay the afternoon before, all holders have their valuation changed and none of them get to reassign anything.

Or, taking your example and looking at it the other way, if the SNB sell $50B in FANGMAN over 4 months “starting in July”, the market wouldn’t even notice. First of all, for every $ the SNB takes out, there’s a $ on the other side that someone else puts in, so absolutely no credit is “reassigned” anywhere. In a trade, all that happens is ownership of the $ and the stock is swapped between two parties. But second, the SNB’s hypothetical trading is only about $7B per stock, spread over 60-70 trading days, or $100M/day, which works out to 0.5-1% of the daily trading volume in stocks like these (AAPL volume is about $20B/day). That’s not enough trading to pressure the price relative to where the market is moving it already.

Now, if the SNB wants to swap $$ for CHF and then retire the CHF in order to swing the exchange rate, that’s entirely separate from FANGMAN. The SNB can move the CHF with effort – since it has credibility which, say, the Argentine or Venezuelan banks lack – but it can’t move the $$.

P.S. The SNB don’t worry about the $$. The SNB’s job for the past 7 years has been to stabilize the CHF against the Euro. In the 2011 Euro crisis, and again in 2015, people who placed faith in the CHF found out the hard way that the 8 million Swiss can’t really allow their currency to deviate too far from that of the 330 million Euro-users surrounding them, or their economy blows up.

P.S. I suspect the SNB is only able to invest CHF abroad because the EUR folks have done such a poor job preserving their currency; the SNB has had to print an enormous amount of CHF to avoid it appreciating too far. Owning a highly respected currency has been a good deal for the people of Switzerland though!

Tim Leissner of Goldman Sachs, conspired with Goldman Sachs, because of Goldman Sachs, to defraud Goldman Sachs. Got it. Can it get more convoluted? Really, can this entire debt-based, fraud-based, bubble-based, centrally-planned-mishap/unmishap/remishap-based, leveraged, financed economy get more convoluted? Good thing there are blogs like this to help sort it out for normal people.

I’ve taken a strong personal dislike to Culp as GE CEO, so it’s hard for me to separate the personal from the objective, but taken together Culp is way into: what-was-the-board-thinking territory.

On the personal dislike side:

– Management by sports analogy (“ripping the cover of the ball” & “it’s tough to play offense”) is one of least favorite executive tics and seems doubly inappropriate given the awfulness of the GE “dumpster fire”.

– Culp’s engineered press release of buying $2 *voice of Dr. Evil* million of GE shares, given the outrageous compensation package he negotiated as a sitting board member if he manages to sustain a very modest (at the time) increase in share price and sustain it for a couple of months.

On the more objective side:

– I’m pretty sure sure that the negotiation courses that are a required part of most MBA programs don’t recommend that you enter into talks about the sale of multi-billion dollar divisions by announcing your heightened sense of urgency to sell. And that your desire for an all-cash transaction is to temporarily staunch the bleeding of your balance-sheet.

What to levy a tariff on to save GE?

How many pension funds go under with a GE bankruptcy?

Don’t think it will be allowed.

Keep in mind that GE is just the canary in the coal mine.

There are numerous big cap stocks that either are already or soon will be in big trouble due to high debt loads and falling cash flow.

Our government always chooses the least painful solution for anything and continues to do so until it can’t. One of ZIRP’s intended benficiaries was corporate America to keep stock valuations up.

When it comes crashing down, the Fed will be forced to buy stocks and/or bad debt from these American stalwarts. They know that.

But another round of QE that is coming will have major impacts on faith in the dollar. They know that too.

Thanks for the opportunity to post.

Or FedGov via Social Security Reform/Privatization…

There’s only a couple of trillion to loot (yes, I’m aware the money’s already spent, but there’s still engineering the cash flow).

“When it comes crashing down, the Fed will be forced to buy stocks and/or bad debt from these American stalwarts. They know that.”

Is there an assumption here of who the FED works for?

Keep in mind that for the last 20 years, the S&P 500 has traded at an average valuation equal to the 1929 bubble peak. That’s 2 consecutive decades of peak bubble. And after over 10 Trillion in buybacks in order to keep that multiple from being even higher. Valuation resides in the Institutions willingness to support it. We have seen with GE what happens when they don’t.

Muppets getting slaughtered

Without the particulars I like GE here. In a few months debt will get cheaper, as the bear market in credit reaches capitulation stage. They can probably refinance their debt at that point, new QE and they have some interesting businesses, like HC.

Is GE too big to fail, or is the point in the movie where the other velociraptors smell blood and start cannibalizing it?

As for the rest, I find it kind of funny that people are still like “The party’s still going, right? We’re partying?” But what do I know. Maybe someone’s about to whip out a fresh bag of blow and keep this drawn-out, twitchy sausage party going FOOOORRRREEEEVVVVEEEERRRRRRRR!!!

“Booming economy” due to pulling demand forward by using experimental monetary policy.

What could go wrong when special interest groups decide to cash out, will they be left in the dust, who will be holding the bag?

The FED does the bidding of unregistered criminal offshore special interest groups.

https://youtu.be/9rEuLEHcFGM

Goldy just said to expect stocks to net return zero in next 12 months.

So will people pick up pennies in front of the steam roller?

If you mean GS, surely they’re trustworthy.

I guess all that Six Sigma/Black Belt nonsense at GE finally brought the company to its knees.

Since 2008 I’ve been wondering exactly how many international megacorps are fuctionally bankrupt and just haven’t bothered filing papers yet in hopes a hail Mary comes along to bail then out.

They’re called hail Mary for a reason…