The “up to” begins to matter for the first time.

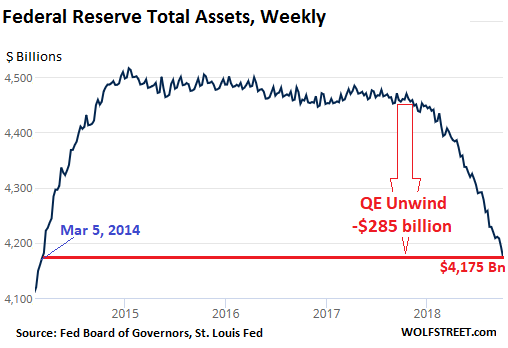

The Fed released its weekly balance sheet Thursday afternoon. Over the four-week period from September 6 through October 3, total assets on the Fed’s balance sheet dropped by $34 billion. This brought the decline since October 2017, when the QE unwind began, to $285 billion. At $4,175 billion, total assets are now at the lowest level since March 5, 2014:

During QE, the Fed bought Treasury securities and mortgage-backed securities (MBS). During the “balance sheet normalization,” the Fed is shedding those securities. But the balance sheet also reflects the Fed’s other activities, and so the amount of its total assets is higher than the combined amount of Treasury securities and MBS it holds, and the changes in total assets also reflect its other activities.

The QE unwind was still in ramp-up mode in September, according to the Fed’s plan. For September, the Fed was scheduled to shed “up to” $24 billion in Treasuries and “up to” $16 billion in MBS.

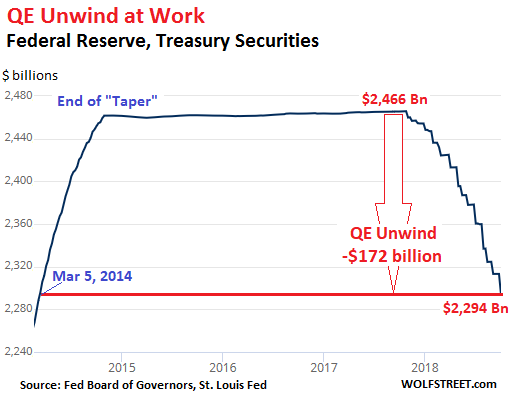

From September 6 through October 3, the Fed’s holdings of Treasury Securities fell by $19 billion to $2,294 billion, the lowest since March 5, 2014. Since the beginning of the QE-Unwind, the Fed has shed $172 billion in Treasuries:

The “up to” begins to matter

Though the plan calls for shedding “up to” $24 billion in Treasury securities in September, the Fed shed only $19 billion. Here’s what happened – and why this will happen more often going forward:

When the Fed sheds Treasury securities, it doesn’t sell them outright but allows them to “roll off” when they mature; Treasuries mature mid-month or at the end of the month. Hence, the step-pattern of the QE unwind in the chart above.

On September 15, no Treasury securities matured. On September 30, two security issues in the Fed’s holdings matured, totaling $19 billion. Those were allowed to “roll off” entirely without replacement. In other words, the Treasury Department redeemed them and paid the Fed $19 billion for them. The Fed then destroyed this money – in a reverse process of QE when it created this money with which to buy securities.

But since only $19 billion in Treasury securities matured, only $19 billion could roll off, and the “up to” $24 billion cap could not be reached.

This will happen again. For example, in October, $22.9 billion in Treasury securities will mature. In October the “up to” cap increases to the final cruising speed of $30 billion a month, but only $22.9 billion can roll off.

In November, however, $50 billion in Treasury securities will mature. The Fed will let $30 billion roll off, maxing out the “up to” cap of $30 billion, and will replace the remaining $20 billion.

Mortgage-Backed Securities (MBS)

The Fed is also shedding the MBS on its balance sheet. The Fed acquired residential MBS that were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Residential MBS differ from regular bonds; holders receive principal payments as the underlying mortgages are paid down or are paid off. At maturity, the remaining principal is paid off. To keep the balance of these ever-shrinking MBS from declining after QE ended, the New York Fed’s Open Market Operations (OMO) kept buying MBS.

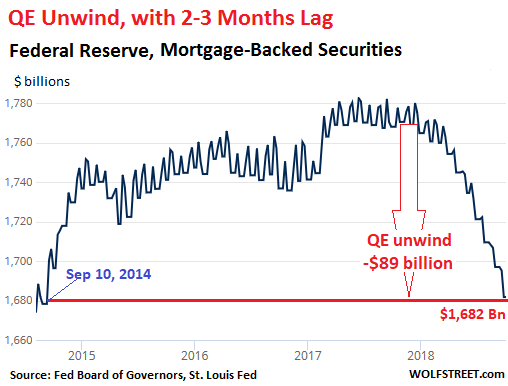

The Fed books the trades at settlement, which occurs two to three months after the trade. Due to this lag of two to three months, the Fed’s balance of MBS at the end of September reflects trades from around June, give or take a few weeks. In September, the “up to” cap for shedding MBS was $16 billion. But at the time of the trades, through June, the cap was $12 billion. In July, it increased to $16 billion. So we would expect the roll-off that was booked in September to be somewhere between the June cap of $12 billion and the July cap of $16 billion.

And this is what we got. Over the period from September 6 through October 3, the balance of MBS fell by $14.2 billion, to $1,682 billion, the lowest since September 10, 2014. In total, $89 billion in MBS have been shed since the beginning of the QE unwind:

Based on various tidbits in speeches and discussions by Fed governors, it seems that a consensus is building that the Fed wants to get rid of all its MBS and only hold Treasury Securities. The Fed’s strategy of buying MBS under what Wall Street had wishful-thinkingly called “QE infinity” was designed to lower long-term interest rates, particularly mortgage rates. If the Fed decides to shed all its MBS and stay out of this market, it would further reduce the official support for – or rather, official manipulation of – the mortgage market, and by extension, the housing market.

The Fed has been raising rates to where Wall Street is starting to squeal. But Fed Chairman Jerome Powell says, “We’re a long way from neutral at this point.” Read… Powell Explains Just How Hawkish the Fed is Getting

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great article Wolf.

Can you do a chart on treasury auction sizes? The fear was that with a larger deficit kicking in in Oct, the amount of treasury bonds on auction will be much much higher than before. With so much private cash already tied up servicing other bonds, this could cause dollar liquidity to go down or even a yield spike when there are fewer private dollars chasing newer+larger treasury auctions.

But who am I to speculate!

James,

My guess is that the 10-year yield will hit 4% in the first half next year. I would consider this “normal” and “to be expected” in this rate hike cycle, not a “spike.” It would perfectly fit into my chart below from two weeks ago, which shows how the 10-year yield moves in surges, rather than in a smooth-ish line. We already started the third surge this week, it seems, with the 10-year yield at 3.2%:

The Fed’s unwind is a misnomer in my opinion. The debt is not going anywhere. It is simply being rolled over to individuals and institutions primarily in the US. There is probably a limit on how much can be rolled over to these new buyers. I guess we are going to find out.

True, the debt is not going anywhere. But the money is being destroyed, just like it was created during QE.

In September, $34 billion in money was destroyed. So far in this QE unwind $285 billion in money has been destroyed. This is the reverse of QE when this money was created. Money creation during QE helped inflate asset prices. The QE unwind is doing the opposite.

And therefore isn’t the direct effect of QT to draw down excess reserves (and backdoor subsidy) that banks hold at the Fed? There is the textbook money multiplier effect, but with $1.8T in excess still held at the Fed, we have a ways to go.

Ted,

See my reply below to Bobber about excess reserves.

This reminds of something that Dr. Frankenstein said:

“The monster was created artificially. It must be destroyed by the same means”.

It’s quite possible that due to rising interest rates, the lowered volume of new MBS’ will outweigh the Fed’s decreased purchases.

GSH: great insight. WS says “Fed-owned bonds got their face value in $$ vaporized. (money supply reduced by face value of bond). The debt was simply re-issued by Treasury to another owner (retiree bond fund, for ex).

Your expression was “debt isn’t going anywhere”. Exactly.

But money supply is being drained (a little bit) when the Fed retires those Treasuries. When the private sector buys newly-issued-by-Treasury bonds, it’s with already-issued dollars, so no new money is created.

The larger context is that the Fed financed the U.S. economy for the past 10 (OK, actually 50) years. Reduced interest rates, blew asset bubbles to create “wealth effect” spending, bought USG debt to finance the deficit (fiscal stimulus, aka Keynesian “demand of last resort”).

There are a lot of econ distortions and mis-allocation implicit in those draconian actions. Housing, bling, entertainment, etc. I’m not impressed with how we spent that money.

Is there a way out of the “induce demand by helicopter-money” dilemma? Remember, Bernanke was selected primarily because of his work on dodging depressions. They (banks, et. al) knew perfectly well this was coming; they *knew* they were gonna need helicopters.

So, we have two questions.

1. Who will buy the debt so that demand can continue to be artificially propped up (the BAU option), or

2. How can wealth (earnings) be routed through households so they’ll create (be able to pay for) stuff, and thereby provide “organic” demand (this is Magic Pixie Dust option)

The Fed is declaring that “we are exiting the artifiical stim biz”. They fervently hope someone else will step up – either buy debt, or induce econ activity that routes income flows thru mid-to-low income HH so they’ll buy more stuff (provide demand).

The Pixie Dust option has been the fervent hope of the Fed for the past 10 years.

Automation, Citizens United (captured gov’t), investment-in-consumption-industries et. al. conspire to drain income from HH and concentrate it into hands that can’t spend what they get; the effect is declining velocity of money. GDP = M x V. (money supply * turns (purch txns) using said money.

Take another look at the equation: GDP = M * V. If M (money supply) is to fall, then V has to go up, or GDP falls. Where’s that pesky V gonna come from?

The Fed is throwing a Hail-Mary pass. I’m not saying we can’t catch that pass and run with it, but we need to be clear among ourselves that the football is now airborne.

Two points in error above and also answers to the 2 questions:

1) “When the private sector buys newly-issued-by-Treasury bonds, it’s with already-issued dollars, so no new money is created.”

This is not true. The Fed’s Primary Dealers are able to absorb Treasuries with zero reserves required. And under hold-to-maturity accounting, they don’t need to worry about booking losses either if rates continue to rise. This answers your question 1 about how BAU continues.

Error #2) It’s quite clear the banks didn’t know how big a crisis their shenanigans would create; if they had they would have traded it much better!! I think Bernanke was selected because they knew he would be a loose-money guy; the helicopter thesis being just one example. The banks do know that crises will happen (it’s endemic to the system) so they want friendly faces in charge.

Answer to Question #2: To create organic demand by routing more income through households, the system needs workers’ income to be a higher share of GDP, as opposed to corporate profits. And, more broadly, the economy needs more income flowing to the lower end of the distribution and less to the very rich. Those with lower incomes have much greater pent-up demand, and tend to spend everything they earn every pay period. So paying them more would increase velocity of money. This would actually increase everyone’s income overall. Historically, this more equitable distribution of income was a big source of the general prosperity of the 1950s and ’60s.

WisdomSeeker:

Pt1 above: Thks for correction; most appreciated. I too seek wisdom. :)

I don’t recall seeing this point on Wolf’s recent article “who’s buying treasuries”. Wolf, if you’re listening in, pls comment.

Pt2: We agree that routing income thru mid-low income HH is surely the way toward increased velocity.

Durable re-routing of income will only happen when the capacity to generate wealth is redistributed. The war over “socialism” is about forceable, mob-directed one-time transfer. History shows this method doesn’t work all that well. The current transfer-payments regime looks creaky on several counts.

The durable solution is for the unskilled and therefore undercapitalized to get the necessary skills to stay in the game. This route requires Herculean effort and discipline, and therefore seems unlikely.

While the capital .vs. labor battle (concentration of wealth) is timeless, this go-round has a significant wrinkle.

Automation is an uncontrollable vortex. The rate of automation (which serves to replace labor with capital investment in lower-operating-cost “machines”) has already exceeded the general rate of human adaptation (Red states: “Who moved my cheese!?!”), and even 200 years in, the rate of automation is just starting its acceleration trajectory.

The reduction in the value of labor – worldwide – will continue to accelerate, and expand into the upper reaches of the skills stack.

Most people sell labor. The implication is that people must now – and rapidly – learn to acquire/build and operate automation machinery (mainly software) on their own account.

The situation seems to be rapidly evolving toward “You’re driving the steam-roller, or you’re squashed by it.”

This is a significant qualitative difference, and it’s a difference that’s not amenable to top-down adjustment.

Does that mean all theses toxic assets being reduced from balance are being buried in our 401(k)’s?

Also, the toxic treasuries and toxic bond China is selling (I assume since no one is buying the treasuries the US is taking them back) and burying those in our 401(k)’s as well. Any thoughts?

These early stages of QT might have little impact, given banks have so many excess reserves. I think I saw a chart not to long ago showing that the cash being “destroyed” through QT was simply reducing the amount of the excess reserves. Thus, the cash being destroyed was never out there inflating asset prices. The QT may have a psychological impact though.

Bobber,

There seems to be practically no correlation between excess reserves and QT, and linking them in this manner is not supported by the numbers.

Excess reserves peaked at $2.71 trillion in July 2014 (over 4 years ago), while QE Infinity was still going on but was begin tapered. Excess reserves have since plunged by $1 trillion to $1.73 trillion. Most of that plunge occurred before Dec 2016!!

So based on this, the QE unwind has nothing to do with excess reserves.

You have to keep in mind that excess reserves are customer bank deposits that have not been lent out. I read a NY Fed post a while back but can’t find it anymore where the researchers said that there were only a few banks responsible for most of the excess reserves — those few banks just didn’t have enough lending business to lend out their deposits. It’s not a broad phenomenon.

Lending (corporate and consumer credit) has grown vigorously since 2014, and that explains the drop of $1 trillion in excess reserves.

if the banks excess reserves were from customer deposits not used, then velocity of money shrank as did economic activity.

but i think there is more do it. during qe they created money and lent it to the banks. the banks deposited it back to the fed as excess reserves earning 25 basis points. this is why ive argued undoing qe will have no impact. its just offsetting journal entries.

What would have been the point of QE under that assumption then?

@Broker Dan:

QE was designed to provide liquidity to banks so that they could meet their liabilities and cut-off any thought of a run on banks. Much of that money ended up in excess reserves because with no one fearing a run, everyone didn’t need to call their loans. By providing interest on the excess reserves, it also helped to recapitalize banks.

It also insured low interest rates because the Fed could buy treasuries an MBSs at higher than real market prices.

I disagree with Mr. Knights assumption because with the current, strong economy the banks are going to want to lend. QT will cause a reduction in excess reserves (along with the new lending) which will reduce liquidity and cause interest rates to head up.

Kent,

You’re confusing QE with the numerous liquidity programs the Fed announced during the Financial Crisis.

QE was specifically designed to inflate asset prices.

The liquidity programs were designed to keep companies and banks afloat as credit had frozen up. The Fed came up with a veritable alphabet soup of programs such as TALF, and many others that I can’t remember.

These liquidity programs were all short-term and all have been paid off years ago, and the Fed got all its money back.

I believe that excess reserves climbed sharply during QE, and I suggest that is exactly where most of the QE money went.

Your comment that there isn’t much demand by qualified borrowers at rates that justify taking any risk with the principal is also true.

“Lending (corporate and consumer credit) has grown vigorously since 2014, and that explains the drop of $1 trillion in excess reserves.”

Growth in money supply is equivalent to (by definition) the growth in borrowing. How can we reduce the ms and expect continued credit growth?

This is an incorrect explanation. Banks do not lend deposits, never have and never will. Excess reserves can only lower the bank borrowing cost when sourcing reserves to fund loans they have created. This is the interest rate channel that stimulates the economy! Yes it’s inflationary and that was the point.

C

You’re way off, believing the nonsense-BS about deposits. Go ahead and keep believing this nonsense that banks don’t lend deposits. But don’t spread this BS here. People might actually take it seriously. An individual bank cannot create money out of nothing. It MUST get the funding for the loans it originates. Sources of funding are: deposits, equity sales, bond sales, loans from other banks, and funding from central banks. The COST Of FUNDING is a very closely watched data point in bank financial statements, and deposits (the cost of deposits) figures very heavily in this and is closely monitored as a sign of health at the bank.

That said, the banking system as a whole creates and destroys money in the ebbs and flows of the economy via a complex process.

I’m just so sick of this nonsense. It wastes my time to have to squash it.

Wolf,

A bank creates a loan which becomes a deposit which is then sourced, period. Sourced hierarchy is deposits, repo, fed funds and discount window. Agreed banks can’t create money! What in my post allude otherwise? The concept of not lending a deposit is allusive to many but essential to understand. To believe otherwise is to believe our banking system is constrained. The only thing constraining our banking system are capital ratios (which can be hedged three ways to Sunday) and qualified borrowers/collateral. I’m sorry that you feel what I’ve said is nonsense. Maybe we’re closer in agreement than might a peer.

C

C,

OK, I interpreted your comment to be about “creating money.” In fact, you didn’t mention it and didn’t even allude to it. My bad.

In terms of the rest, folks keep lumping together an individual bank and the overall banking system. And it seems you do too. A bank is constrained. The banking system as a whole is not.

Interest in excess reserves i.e. excess deposits may effect the effective federal funds rate according to John Mason. Every time the federal reserve has increased the federal funds rate it has been below the posted rate i.e. recent 2.25%. So they use a range 2.00 to 2.25%. In essence the federal reserve is putting a floor under the federal funds rate. This alludes to the phenomena that there is no market pressure to push up the “effective” federal funds rate. John Mason thinks the interest on excess reserves would need to go to zero first before there would be any real market pressure to bid up the federal funds rate for actual price discovery i.e. the real price of short term credit. Connotations of the phrase “pushing on a string”?

On another note, I remember David Stockman (in 2016) stating that banks had earned $120 billion on excess reserves held at the regional federal reserve banks.

Sadie,

Every year, the Fed reports how much it pays the banks on excess reserves. This amount is deducted from the money the Fed remits to the US Treasury. So what the Fed pays the banks comes out of tax payers’ pockets. I report on this in January every year when the Fed releases this report.

I think you’re mixing up some numbers with the $120 billion. Memory does that to me all the time :-]

In 2017, the Fed EARNED $115.5 billion in interest income mostly from its bond holdings and a smidgen from some foreign exchange events.

In 2017, the Fed PAID BANKS $25.9 billion in interest on excess reserves. And it paid banks $3.4 billion in interest on securities sold under agreement to repurchase. So the Fed paid banks a total of about $30 billion in interest – not $120 billion.

The Fed also pays for its own operating expenses and some other things. The remainder is remitted to the Treasury Department. This remittance was $80 billion in 2017.

Here are the details for 2017…

https://wolfstreet.com/2018/01/10/fed-pays-banks-30-billion-on-excess-reserves-for-2017/

Wolf, please see FRED graph below, you will be enlightened about the direct 1-to-1 link between QE and Excess Reserves.

https://fred.stlouisfed.org/graph/?g=lu4y

There WAS a huge correlation between QE and Excess Reserves from the start of QE until the peak in 2014. If you graph total Fed Assets (minus a base value of about $1T), multiply by 0.8 and compare it to Excess Reserves, there is a perfect agreement. So, there were no excess reserves to speak of before QE started, and they expanded almost in lockstep from 2008-2014, with the balance sheet growing about $10 for every $8 in Excess Reserves.

Since 2014, there has been some reduction in Excess Reserves, because other factors on the balance sheet (H.4.1 reports) have evolved. Comparing the H.4.1 reports from 10/2/2014 and 10/4/2018 is very informative here. Currency in Circulation has risen by $400B, the Treasury General Account is up about $250B, and there are some minor changes. So the system has very gradually absorbed about 1/3 of the Excess Reserves.

The Fed under Powell may see the current level of excess reserves still at the Fed as dynamite waiting to blow asset prices even higher. It would be catastrophic (and embarrassing) to allow the S&P 500 to blow up to 4000 and housing up another 50% for no reason other than cheap and copious money.

When the Fed originally purchased these assets weren’t many of them impaired? Are they still?

In other words, are they going out the door for the same amount (regardless of face value) they came in? I’m wondering if it’s possible that the Fed won’t mop up as much as it emitted during QE.

MF,

Under QE, the Fed bought only pristine US Treasuries, Agency-guaranteed MBS (by Fannie Mae, Freddie Mac), or Ginnie Mae guaranteed MBS (= government). When they roll off, the Fed receives face value for them. There is zero problem with them.

However, under the BAILOUT actions the Fed undertook, it bought all kinds of stuff — including $30 billion in Bear Stearns stuff. At the time, the market had frozen up for these things. But since the great wealth effect has set in, these became good investments. The other day, the Fed disclosed that it had gotten rid of the last batch of Bear Stearns stuff and in total had earned something like $2 billion on it.

Super interesting, thx Wolf.

Are the CUSIP numbers that the Fed holds public information?

Yes. On the linked page, wait till it loads fully, go down to the table, click on “T-Notes and T-Bonds” where most of them are. You can also check the CUSIPs of FRNs, TIPS, Bills, etc.

https://www.newyorkfed.org/markets/soma/sysopen_accholdings.html

“…the Treasury Department redeemed them and paid the Fed $19 billion for them. The Fed then destroyed this money”

Wow. All that money destroyed in an instant. For a moment I thought you were talking about my wife.

All joking aside, excellent article Wolf!

” In other words, the Treasury Department redeemed them and paid the Fed $19 billion for them. The Fed then destroyed this money – in a reverse process of QE when it created this money with which to buy securities. ”

Is that paper money then burnt in an incinerator or is it wiped off the records electronically ?

Electronic.

They are still creating some $150 billion of currency per year, and that should not be forgotten when discussing “QT”.

They go into the computer room with sledgehammers, then set fire to the room using all the bank notes they can find, then demolish the building on top of it all and then pour concete over iron grid to cap it . Afterwards a small monument is erected on top as warning, with the simple inscription “Here we once made lots of money, but no-one found it very funny”.

When a word such as “destroyed” is used you would be thinking physically. So if something disappears electronically a better word to use would be “wiped”.

Hey Wolf How about a discussion of why the Fed will not allow US citizens a full and meaningful audit of Fed accountings and holdings? …… What are they afraid would be disclosed in any truthful audit ?

The Fed’s holdings are audited every year, and they’re publicly disclosed. These audited annual reports are posted on the Fed’s website.

What’s not audited is what the Fed is doing behind closed doors, the deals it’s making, insider trading, etc. That’s what Ron Paul wanted to have audited. This is not a financial audit (which we get every year), but a much deeper audit into the obscure world of central bank communications and deal making.

Upon Congressional action, the GAO did two of those audits after the Financial Crisis. Though they were only partial, they revealed a lot of muck. I reported on the second one back in the day (2011). GAO found things like:

“The GAO identified 18 former and current members of the Federal Reserve’s board affiliated with banks and companies that received emergency loans from the Federal Reserve during the financial crisis….”

https://wolfstreet.com/2011/10/21/the-gao-audit-of-the-fed-doesnt-call-it-corruption/

My article also links to the GAO’s reports. I downloaded them to my server in case they disappear from the internet.

Wolf, AIG (Hank Greenberg) eventually received $181 billion in funding from the government /Fed to cover the CDS since AIG did not retain enough reserves to cover losses, therefore the bailout. Hank Paulsen was the US treasury secretary at the time and was also the former Goldman Sachs CEO. Guess who had heavy exposure to AIG’s CDS and was also loaned money in the the form of preferred stock from Warren Buffet… you guessed it Goldman Sachs.

So, if that happens future FED meetings will be a bunch of bankers walking around the streets, mumbling, and talking with their hands over their mouths?

Goodfellas, all around.

Great article and comments.

What? Somebody’s scrubbin the servers? Hmm, why would anyone do that?

Well, since nearly every major bank received emergency overnight liquidity in 2009, and since all the members of the Fed board come from major banks, this is not terribly surprising.

\\\

Dear Wolf, from what I understand, the QE unwind process is more or less an internal US mechanism (article from Sept 18th “Who Bought the $1.47 Trillion of New US National Debt over the Past 12 Months?”). To correct myself, as of recent it has become an internal mechanism, and time will tell is that good or not.

Q1: Could this process in any way be affected by the impending QE unwind in Europe? I am making the assumption that the EU securities will have a higher long term yield.

Q2: (If this question is too speculative and leaves the intended scope of this article or the discussion, please feel free not to reply)

Since the process has internalised itself, the US is buying back it’s debt and absorbing the QE unwind, could the US engage in Treasury trade restrictions? Let’s assume the trade war with China escalates and the US decides that their Treasuries, held by the opposing nation, are not any more valid and will not be honored. Is this even possible?

\\\

Without getting into speculation of what might happen, one thing we know: The Fed’s QE unwind is still outdone by QE in Europe (€30 billion in Sep), QQE in Japan, and stealth or other QE in other countries (China, etc.) But the ECB’s QE program tapers to €15 billion in Oct and goes to zero at the end of Dec. Japan is cutting back too. So up to this point, the global net was still QE. But going forward, the global net will be QE unwind. We have not yet experienced a global net QE unwind, but we will later this year and more seriously next year.

Assuming mortgage origination remains the same does this mean the GSEs are now holding their own paper? What is the state of mortgage paper in the aggregate and how much of it is subprime.?

Define sub-prime

The US equity markets have been supported by low interest rates (fixed directly by the Fed) and low US bond yields (achieved via QE). We can argue if the Fed or was trying to influence economic growth believing a rise in financial asset prices assisted growth or if this was a side effect. I can also accept that higher Fed rates and Treasury bond yields may have a limited impact on US growth now that this has developed strong positive momentum. I find it more difficult to believe that the higher opportunity cost for holding equities (i.e bond yields) will not impact equity markets. I suspect higher growth is priced in but not the full extent of higher Treasury yields.

Moreover, there may be a further side effect. I live in London where we face GBP real bond yields and Euro real bond yields firmly in negative territory. It may be that rising US bond yields are not fully discounted and will lead to a rise in the dollar.

Comments please.

I’m about to fully bare my ignorance here, but just to be clear, does “the Fed bought Treasury securities and mortgage-backed securities” mean that it was THE FED who was DIRECTLY (as well as indirectly) driving up housing speculation, in which they were heavily invested? Am I interpreting (what is probably a very clear, simple fact to others) correctly?

You nailed it :-]

In general you are correct but I am not sure if “housing speculation” is the best term to use in the context of “directly” drove up speculation. Housing “speculators”, i.e., folks who buy houses for a quick capital gain are generally not funded by GSE backed paper. As such, the Fed did not directly drive up speculation but their actions certainly provided substantial support to the housing market, which indirectly supported speculation in it (although not nearly to the extend that housing speculation was prevalent before the 2007 crisis).

It says in WolfStreet episode ‘Here Comes the 2nd Wave of Big Money in the “Buy-to-Rent” Scheme’ (https://wolfstreet.com/2018/08/23/second-wave-buy-to-rent-single-family-homes-scheme/):

“…shortly before the Invitation Homes IPO, it obtained Fannie Mae guarantees for $1 billion in rental-home mortgage-backed securities.” So, GSE paper, no? Perhaps the exception rather than the rule?

Thanks for the feedback regardless. I appreciate people’s patience with explaining these things.

I would absolutely agree with this. Hard to speculate using GSE paper after Dodd-Frank.

->What’s not audited is what the Fed is doing behind closed doors, the deals it’s making, insider trading, etc.

Gangster capitalism rules the world. And to think that people wonder where all those trillions disappeared to.

QT is a sham. A bit of light cost recovery from criminal officialdom and everybody would be running surpluses by COB.

I think people have to get out of the 10-year bond because the Fed is on a clear path to raise rates. Who knows how long the Fed can continue on that path before something blows up. In the meantime, there is no sense holding the 10-year. That’s why people are selling it right now.

Even if there is a 20% stock and RE correction, there is no clear sign that the Fed will lower rates. After a 20% correction, the Fed would likely just stop raising rates for a spell. There have been a lot of paper gains racked up in stocks, bonds, and RE over the past 10 years. A correction would wipe out some paper gains, but it’s not likely that the economy would be severely impacted. Note, we didn’t see huge increases in economic activity when paper asset prices were growing 20% per year, so why would reversal of those paper gains have any impact?

I think Powell’s plan is a good one. Raise rates until asset prices fall. Re-evaluate if and when the economy enters a moderate to severe recession. If a mild recession occurs, consider pausing the rate increases, but do not reduce rates. Put some speculators out of business to keep things orderly.

The Fed has a tiny hair on the elephant’s ass, ten year rates are rising now because of imploding EM debt. This gives the Fed some cover to raise rates at the short end. You should be right, asset deflation will not affect the economy any more than asset inflation boosted the same but sometimes these things are asymmetric.

The Fed created $3.7 trillion in extra fiat money supply to purchase MBS and US Treasuries. Alasdair Macleod says the GDP was 30% of the fiat money supply in 2007, but now it is 80%, meaning we do not need this extra fiat, because it is not needed on Main Street, only within the canyons of financial transactions to boost financial sector profits. Financial transactions are 4 times the underlying true global trading of products. The banks get more play money for their derivative trades, which by the way are unregulated and, in my opinion, the true cause of the 2008 crash. They simply trashed Lehman so they had a cover story to never allow anyone to regulate their big cash cow- derivatives. Those with Real Estate may benefit with this extra fiat until the rates get too high and those with savings are forced, or should I say enticed to invest with the Wall Street boys for their retirement until the banks start paying an accurate interest rate.

The idea we only have 2-3% inflation is bogus. The Fed with me has no credibility as to what they say. They need to manipulate inflation rates to have the ability of keeping the low interest rates. These guys are Ivy League graduates and the reason they look like they do not know what they are doing is because what they say is just a cover story to hide the truth. If the fiat money supply has increased 50% as per Macleod then claiming a 2-3% inflation rate shows they manipulate rates to hide the truth. John Williams and he says inflation is 9-10%, if you use the old CPI index of the 70’s. Also gold was about $100 per ounce in 1973 and today it is $1200, an increase of 450% over 45 years averaging about 10% per year.

Anyone who controls the interest rate controls the prices of everything and the Fed also controls the money supply. Claiming we want a free market economy is a joke as long as the Fed is in control. Are you free to choose between savings today at a decent interest rate reflecting “true inflation” or are you forced or enticed to investing in riskier papet assets? We are again in a giantic wealth transfer from the poor to the rich

The Fed wants to insure they never get blamed for any crisis, but they are in control and use the old chairman’s doublespeak (Greenspan) to have a cover story or simply BS.

Greenspan was the King of BS when he was the Fed Chairman and he knew what was coming, as his first book out of office was “ The Age of Turbulence”.

All the Fed has done since 2008 is create a bigger bubble and pushed the can further down the road so they can find another reason for the next crash or a cover story to hide the truth. And they are doing a fine job to crash it with increasing interest rates and removing liquidity by trying to reduce their balance sheet.

The Fed by me is classified under a category of The Most Transparent BS Legally Allowed.

Sorry Wolf for the rant, but I have read almost 100 books on our economy and the Fed since 2008.

->I have read almost 100 books on our economy and the Fed since 2008.

Me too. It’s taken years to get the vomiting under control so I could post comments here.

I used to care, but I take a pill for that now.

Unamused. Love that comment.

Unamused, keep going deeper in your analysis and then you can stop buying the pill. And by deeper, here’s a couple examples. A coin is often analyzed according to its obverse and reverse. More astute analysts realize that it’s the content of the coin that matters. The most astute analysts realize that the content of the coin is less important that their own contents.

The steeping curve this week is more important than the overall move up. To me its a very good sign about continued growth in the economy. Money never should have been free to begin with.

->To me its a very good sign about continued growth in the economy.

Debt is growing faster than GDP. Borrowing and spending is not economic growth, but on the plus side, it is starting to make the loan sharks nervous.

“up to”

Has there been any verbage on whether the “X billion/month” means the maximum amount in any given month, or the maximum rate, averaged per month, that the unwind will happen (ie, if they can’t hit their goals in Sept, or Oct, would they consider “catching up” in Nov as there are ample USTs reaching maturity in Nov)?

It was my impression that the rate of roll-off that will be ultimately reached was likely chosen because this was all of the USTs that would be maturing per month anyway..

Agreed balance sheet is being reduced but who is buying it?

Is it being buried in our 401(k)’s?

No one just agrees to take back toxic assets, right?

David,

1. Under QE, the Fed acquired pristine US Treasury securities and mortgage-backed securities of high quality that are guaranteed by the GSEs (Fannie Mae, Freddie Mac) and by the US government itself (Ginnie Mae). The Fed does not carry any credit risk here. There is nothing toxic about these securities.

2. No one is buying them. The Fed simply allows them to mature. When these securities mature, the Fed gets paid face value for them by the issuer — for Treasuries, it’s the US government, for MBS it’s the GSEs and Ginnie Mae). The Fed just gets the money (and “destroys” it just like it “created” the money during QE).

3. However, because the Fed has exited as buyer, when the government sells new securities to raise the cash to pay off the ones that matured and to fund its deficits, and when the GSEs sell new MBS, they now need to find lots of new buyers for them to buy what the Fed used to buy. So this puts pressure on the market, which has to absorb these securities. To get more investors to come out of the woodwork and buy them, the securities need to be more appealing, that is they need to offer a higher yield. And that has been happening. Hence, the rising yields in the government bond market.

This discussion has really helped my understanding of what’s going on with this. I’ve been trying to decided if more QE will be required to fund US deficit spending. I know its simplified to the extreme but could you comment on the following…

if

new lending = B

deficit spending = C

banking reserves = R

plus or minus net affect of global QE or QT = A

(B + C) = (R A). There is balance, no more QE is required, and funding from global governments not required. In view of the money that has fled emerging markets to the US and funds that have flowed to the US from US corps abroad, is this possible?

but, if (B + C) > (R A) global governments are required to fund the short fall. What interest rate would be required on, say, the 10 year treasury to accomplish this feat?

If the answer to the last question is approaching historic norms, would the resulting economic slowdown, reduction in asset values, and systemic risks result in more QE?

My algebra is not good so the formula is for illustrative purposes.

First time commenter; been reading for awhile. Love your site, but the Bank of England disagrees with you on modern banking and money creation. Banks are capital constrained; they are not deposit or reserve constrained. Quite a few papers out there (e.g., SSRN) agree with BOE.

https://www.google.com/search?source=hp&ei=4_e6W63rJYX2swWW24eACw&q=bank+of+england+paper+on+money+creation&oq=bank+of+england+paper&gs_l=psy-ab.1.0.0l8.2087.19810..21616…0.0..0.118.2508.25j3……0….1..gws-wiz…….0i131j0i10j0i22i30.msRKc6AHjIU

We have been through this silly argument MANY times here, and I’m sick of it because people keep citing the same BOE article without ever reading the 14 pages of text. The theory by these BOE bloggers is that the BANKING SYSTEM AS A WHOLE (all banks combined, interacting with each other) creates money via DEPOSITS, and NO INDIVIDUAL BANK can create money. Read the frigging thing :-]

And quit conflating an individual bank with the banking system as a whole!!!!

This concept is somewhat like the physics principle of *superposition*:

“The general principle of superposition of quantum mechanics applies to the states [that are theoretically possible without mutual interference or contradiction] … of any one dynamical system…”that every quantum state can be represented as a sum of two or more other distinct states.”

The capacity of a single bank to create credit as a consequence of a given primary deposit is identical to a financial intermediary. L = S (1-s). The superposition is that all primary deposits are actually derivative deposits from a system’s context.

Money creation is a system process. No bank, or minority group of banks, can expand credit, significantly faster than the system, or they’d lose IBDDs (clearing balances).

It is a myth that DFIs are capital constrained. The DFIs could buy gov’ts.

But Catch 22: QE = “crowding in”. QT = “crowding out” ^ 2

The Federal Government will default on its debt.

Just to rephrase my question slightly (Oct 7th 10.32AM). I am a first time poster but this seems like a great blog, what I’ve read so far.

With reference to Wolf’s post, Oct 4, 2018 at 9:29 pm.

Assuming some off that money that has flowed back to the USA from USA corp abroad, hot money, and general inflows due to safe heaven status, ends up being used to buy US treasuries: If 10 year yields hit 4% which you perceive as being normal could the balance of deficit spending be funded by issuing treasuries to governments ex USA?

Or would more QE be required, in the opinion of Mr Wolf or anyone else?

Deficit Spending is unsustainable regardless.

And Trumps’ tax cuts can’t pay for themselves.

The U.S. will probably follow Japan’s lead. And that will make things ever worse.

There is essentially only one error in economics. DFIs, deposit taking, money creating, financial institutions do not loan out existing deposits, saved or otherwise. Thus, all bank-held savings are frozen, lost to both consumption and investment, indeed to any type of payment or expenditure. This universal error produces both stagflation and secular strangulation.

All that is required to correct this error is to drive the commercial banks out of the savings business.

Thanks for sharing your thoughts on that. If commercial banks are driven out of the savings business don’t you think we would get a deflationary depression worse than the one that’s happened. To use a phrase coined by Bridgewater associates wouldn’t we end up with an ugly deleveraging?

In view of that fact that we really live in a world of abundance and that this is all just part of a longer term cycle don’t you think that they are taking the least painful path?

Personally I have benefited from copious money creation, and, I’d hasten to add that human beings in general have done pretty well out of it as well….

How do you see the funding of deficit spending panning out, Spencer or anyone else who wants to chime in…

Man can be a very stupid creature. Driving the DFIs out of the savings business does not reduce the size of the commercial banking system. There is just a transfer in the title of existing bank-held deposits within the payment’s system, a transactions velocity relationship. This increases AD. So the Fed would have to simultaneously tighten monetary policy.

But there would also be an increase in the supply of loan-funds, but not the supply of money. Thus this will tend to reduce long-term interest rates which would feed back to short term rates to some extent.

Everything one knows about economics is exactly backwards. It was promulgated by the most dominant economic predator, the American Bankers Association.

Driving the DFIs out of the savings business would make the DFIs and NBFIs more profitable. It would increase the real rate of interest for saver-holders outside of the payment’s system. It would increase R-gDp relative to inflation.