The economic miracle fueled by foreign-currency debt.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

The Bank of Turkey’s decision mid-September to hike its policy rate from 17.75% to 24% may have temporarily stemmed the rout in the Turkish lira, but the hiatus is now over. This week, the pressure is back on the nation’s currency, which is down almost 40% against the US dollar year to date, as well on its beleaguered banks, 20 of which were slapped with another downgrade by Fitch Ratings.

The lenders, Fitch said, are “more likely to come under pressure as a result of the further depreciation of the Turkish lira (by about 20% against the US dollar since the last rating review), the spike in interest rates (driven by the increase in the policy rate to 24% from 17.75% on 13 September) and the weaker growth outlook.”

The banks affected include foreign-owned subsidiaries such as Turkiye Garanti Bankasi A.S. (half-owned by Spain’s BBVA), Yapi ve Kredi Bankasi A.S. (part owned by Italy’s Unicredit), ING Bank A.S. and HSBC Bank A.S., which were downgraded to BB- from BB, as well as large state-owned banks (B+ from BB-), all with negative outlooks. As Fitch warns, the recent interest rate hike is likely to hurt lira borrowers’ debt service capacity, while exposures to the construction and energy sectors and high borrower concentrations are also “significant sources of risks at many banks.”

As long as the current climate of economic and financial instability continues, these problems are not going to go away. According to data recently published by the Turkish Statistical Institute, economic confidence in Turkey has sunk to a decade-low. Last week the country’s Finance Minister (and President Erdogan’s son-in-law) desperately tried to assure investors that he would, in classic Draghi fashion, do “whatever it takes” to support local banks, but few seem to believe that he has such means at his disposal.

Indications are piling up that the 4.25 percentage-point hike in interest rates last month was too little, too late. By the end of September inflation in Turkey, instead of slowing, had surged to nearly 25% from a year earlier, its highest level in 15 years. The increase on a month-by-month basis, clocking in at an eye-watering 6.3%, was even more alarming.

Soaring prices will heap further pressure on the Bank of Turkey to deliver another hefty rate rise at its next policy meeting, in mid-October. And that is unlikely to go down well with Turkey’s president, Recep Tayyip Erdoğan, a self-professed “enemy of interest rates,” who fears that further rate hikes will bring his foreign-debt-fueled economic “miracle” to a grinding halt, plunging Turkey into a deep recession, if not depression.

By most indications, the slowdown has already begun. Fitch expects Turkey’s economy to grow by 3.8% in 2018 — down from expectations of over 7% earlier this year — and by a meager 1.2% next year.

A fresh rise in rates will also make it more difficult for struggling Turkish firms to roll over their existing debts. And that, in turn, will increase the likelihood of lenders facing a fresh wave of defaults. To avoid that happening, banks across Turkey have been restructuring the debts of some large corporate customers. They are also being forced to buttress their capital bases in response to the lira’s rapid depreciation against the dollar this year.

The scale of the task is huge given that many of the banks have spent the last few years borrowing heavily in foreign currencies despite earning most of their money in the plunging lira, with the result that they are now saddled with a severe debt mismatch. According to Nafez Zouk of Oxford Economics, the country’s lenders face a growing pile of short-term external debt and inadequate funds to pay for it.

The strains are beginning to show. In the last month or so, commercial lenders in Turkey have sold billions of dollars of gold in a desperate bid to avert a liquidity crisis. And according to allegations from Bloomberg, the Erdogan government recently raided the public unemployment fund to buy 10.9 billion lira ($1.9 billion) of bonds issued by a gaggle of state-owned banks, in contravention of its own regulations. Since the bonds were sold through a private placement, the banks didn’t need to reveal the identity of the investor(s).

But it’s not just domestic lenders that have reason to worry about Turkey’s unfolding crisis. So, too, do a number of large foreign banks that have invested heavily in the country, including Spain’s BBVA, the foreign lender most exposed to Turkey, France’s BNP Paribas, Holland’s ING, London-based HSBC and Italy’s Unicredit.

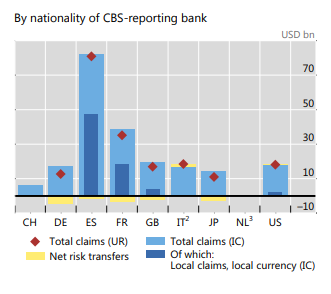

In its latest quarterly review, the Bank of International Settlements dissected just how vulnerable foreign banks are to Turkey’s fragile economic and financial situation. According to the data, which the report’s authors concede is “imperfect”, as of March this year Turkey owed roughly $223 billion to foreign banks, only a third of which was denominated in Turkish lira. The rest was due in foreign currencies, meaning every time the lira slides against the dollar, euro or other currencies, the debt burden for Turkish borrowers increases.

This chart by the BIS shows the extent to which banks in Switzerland (CH), Germany (DE), Spain (ES), France (FR), Great Britain (GB), Italy (IT), Japan (JP), Netherlands (NL) and the US are exposed to Turkey, expressed in US dollars:

Spanish banks did much of the lending, and now have total claims in Turkey of over €80 billion. Spain, more than any other foreign country, needs Turkey’s banks — in particular, Turkiye Garanti Bankasi A.S. — to stay solvent even if, as reassuringly promised, their Turkish operations are siloed from the rest of the company. By Don Quijones.

Why are Bank of Mexico executives and employees resigning in droves? Read… President-Elect of Mexico’s Bombshell: Economy in “Situation of Bankruptcy”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks. Don, for this excellent report on the Turkish economic situation.

I’m surprised there is so little comment on the connection to Erdogan’s opposition to interest rates ( not just high ones apparently) and his desire to return Turkey to Islam.

The Saudis etc. have come up with ‘work arounds” to make investments possible, but strictly speaking Islam forbids interest on loans.

It’s not easy to borrow money without paying interest (outside of the Eurozone or Japan, hahahaha). An Iranian diplomat once explained to me patiently that this Islamic system is more like equity where the source of money participates in the gains, which might be fixed (similar to a dividend, or well, interest) or variable. Listening to him, it occurred to me that the main difference is how all this is phrased — and the essence is still the same: you have got to pay the source of money to allow that source of money a reasonable profit, given the risks, no matter what you call it. However, I just nodded when he was talking.

Funny on EU + Japan :-) ….on Islamic finance:

Participation is quite different though, and so it does involve the funder differently. I am not an expert in the intricacies that arise, but for example if a house is being bought:

In Islam, funder will buy the house on behalf of the person who wishes it, then will sell it back at a fixed higher price to what would be the borrower, paid by installment. Investor has used his money, he has ownership till payment is finished. You can say that is equivalent to interest, but it is not actually pricing money by interest.

In the west, and let us say 100% gold backed lending for simplicity, the lender calculates a time value for lending, and calls that interest. He lends the money to the borrower who then spends it on a house, the lender makes sure his lending is marked as debt against the house. The view of transaction is that the lender is less involved, he is a money dealer who secures any lending against whatever he thinks would be of eventual equal value to him, in short is a speculator who is trading between two positions for profit – the price he can obtain money for and the return he can obtain from his borrower. This is not morally acceptable in Islamic finance.

You could say Islamic finance is playing for keeps, but lending by interest leads to money markets and cross pricing giving rise to a pooled monetary value disconnected from source of activity, and this has opened the way for both the flexibility, and detachment from reality, of the fiat system. With Islamic finance you are technically not allowed to convert the profits into a tradeable interest value, though obviously that could be done. It is a different way of thinking, and acting, and so cannot be called the same…because it isn’t.

So for example, I ask a friend who does business in Saudi if the system is fair… no he says, because there is still a lot of monopoly, pre-arrangement and kickback … like in the west. However the way finance is accounted is visible. This is no small matter. If you look at Islamic finance in the UK, a lot of detail has to be fulfilled to make sure it fits… so? So that is why there is disbelief over some government buildings no longer serving alcohol, other restrictions, after they use key buildings to obtain finance from Islamic sources… because in the contract the lenders become the temporary owners.

Now if you want to convert Islamic finance to an interest eq. , you will always be able to , but you will not be able to convert interest finance to Islamic standards because most of the contracts must be rewritten to do so, which they cannot be. So the two systems can exist side by side, but interaction with Islamic finance must be hand to hand, that is the contract must be fully completed in the sitting, no leverage, no open time variables on value.

Nick, Erdogan will be judged by what he does, not what he says. If he wants to go no interest he should do so…the rest is speculation… which is haram. I guess he is keeping his options open.

(disc. – anyone feel free to correct anything I have written above, I am not professing full knowledge here)

Well done.

Thanks, that is appreciated as I am overextending myself a bit to try to wrap the theme into an understandable explanation, but hopefully it will give at least the gist of the difference, it is something few know much about, and personally I know more about the basis than how all the finer details are arranged in practice . At a deeper level you are looking at two different cultural standards, and how they interact, which is in itself fascinating.

In theory, the source of money is exposed to same risk. the source of money is not guaranteed gains.

Good point. If the lender is sharing risk it makes it different than usual Western loan, which you owe no matter how venture turns out.

It used to be that receiving interest was regarded as the normal compensation for deferred gratification, but the banks which own the Fed have rigged things so that savers receive virtually no compensation (the banks, however are, with a peep allowed to charge card-holders double-digit interest rates.[I think even the non-Moslem Bible called this “usury”]

Erdogan’s “opposition to high interest rates” is regarded as a sign of financial insanity (or illiteracy), but nothing much is said about the TBTF bank’s successful demand to pay virtually no interest on the trillions extracted from the American taxpayers through TARP and QE.

Debt and inflation are part of Turkey’s problem.

But just as much as problem is Erdogan moving Turkey away from a democratic secular state (established under Atatürk in 1923) where islam was basically banned in politics into an islamic dictatorship.

I will add my thanks to you and host.

I live near an east coast port that ships bulk sawdust and the deal is with turkish company. The pile has been growing larger than ever, and they have stopped making more.

Could this have effect on Letters of Credit to ship goods, etc?

Might I see that pile for a while?

Yawn.

So another obnoxious dictator who knows nothing about finance is going to depend on the “good will” of others (including the tooth fairy & Easter Bunny) to shore up his economy.

Then, if all his accumulated mis-management is not rewarded by financial salvation, he will claim it’s Trump’s fault.

‘scuse me while I go get a beer.

I think Erdogan is learning global finance Lesson One. You mess with the Controlling Powers, these Powers (City of London, Washington DC) will trash your country’s currency and bury you in debt overnight. Erdogan probably didn’t believe that his NATO allies would turn on him so quickly.

Just my take.

Erdogan: “I don’t need NATO allies or the Americans. I have Russian and Chinese allies. Eventually, China will need to secure its sea lanes of communications to Europe (I’m making this stuff up), and I can offer them basing rights and access to the Black Sea. That should be worth a few billion. Then there are the Russians, they need to get their ass out of the Black sea, so that access ought to buy me something too” (yeah, and the tooth fairy and the Easter bunny will help too)

Lion

Erdogan (the dictator) buried Turkey in debt (not London or WDC); Erdogan compounded the felony by borrowing in foreign currency. Other than pure stupid greed, why banks make these type loans to creditors like Turkey is a mystery.

NATO allies haven’t changed their position on recent Russian aggression in Crimea & Ukraine so much as Turkey has turned its back on NATO. Turkey may have have expected “flexibility” from NATO, but if it’s insistent on sliding back into the same hot mess as Iran, Syria, Palestine, they’ll have to go without NATO.

An excellent summary, as always, of the fallout resulting from yet another debacle precipitated by terminally venal financiers. What were missing is a description of the actions pursued by the financiers to create the debacle in the first place. Maybe I missed that article.

Financial racketeering is normally so lucrative. Where did they go wrong?

The workers who actually generate wealth have been toiling along since the dawn of history, and they themselves are obviously in no position to create such a debacle, even though they’re the ones who will inevitably be squeezed to pay to clean up the messes made by their betters. To make messes on this scale you need High Finance, and I for one would really like to know what is these guys are smoking, and maybe get them into rehab or something.

These financiers are obviously overpaid. I could have screwed up the Turkish economy half as bad for a tenth of what these guys are making, on a skeleton staff in a cheap office. For my fee, I would recommend trying to avoid the next catastrophe by not employing them at all and requiring them to seek productive employment rather than trying to make careers out of scamming the system so bad that it shatters.

Turkey has had a negative balance of trade from ’47 I think, but it widened considerably from ’87 EEC application. The current account balance went strongly negative from around 2000, around when reforms to enter EU were being pushed through…not that those are necessarily related but it shows the general direction. BBVA started buying into Garanti in 2010, which if I remember was a time Spanish banks were trying to diversify away from their own troubled economy. In 2010 Turkey was not on the political path it is now, the opposite in various ways.

So there is surely some wider story with EU playing out, not to mention US involvement in the country. An Italian bank BBVA was looking to merge with also has fair amount of Turkish investment also, that didn’t go through…but sort of says there is quite some dealing going on here.

Who knows where it is all headed there though, Turkey is not going to be joining EU anytime soon I think… though they keep pushing for visa free travel and Erdogan likes his visits to Germany, which are well received by the current leader, if not always the population.

Though EU is not much in headlines recently, that isn’t because it is all hunky dory.

Boggles the mind, selling collateral (gold) for liquidity which can be lose its value overnight. Does go to highlight how central bank gold transactions have nothing to do with retail gold prices (check the charts for Sept). Gives more weight to conspiracy theorists.

Then Chancellor of the Exchequer (Minister of Finance) Brown sold most of the UK’s for about $250.

Canada sold most of its for about 400.

So the Turks could be doing worse.

Recall that the article stated one third of their bank debt was denominated in lira- that means selling some of their gold, which has not lost much dollar-denominated value the past 5 years, enables them to cover the lira debt cheaply. The same is true for Russia, which, we are told, has liquidated its entire U.S. Treasury holdings (and just in time, by the looks of it: rates have skyrocketed the past two months, tanking the value of those bonds) to buy gold, which allows them to pay debt denominated in rubles, also under attack, relatively painlessly.

So, it turns out that gold, derided by Lenin as useful only for lining urinals, not so useless after all.

Erdogan is finished.There are 2 methode to destroye state or person one is To kill other is to much debt banksters love debt and traders are here To hellp. Messenger of gros.

“Last week the country’s Finance Minister (and President Erdogan’s son-in-law)…”

The problem begins right there.

Erdogan is doing everything a self-respecting dictator would do: he placed incompetent donors and incompetent family members in positions of responsibility, installed a personality cult, used the country’s Treasury as his personal ATM, surrounded himself with proven loyalists, went after dissidents… you know the drill.

Erdogan, like all dictators, is paranoid about the next coup. Crushing potential plotters is more important than saving the economy. If I were a Spanish bank who lent them money I’d be cutting my losses and quit praying for a recovery. A default is more likely.

Lesson for all dictators.Don’t buy unless they accept

your currency for payment.This gets tricky when you

need to buy weapons for your survival. Ve only take gold

okay poppy

As to my earlier inquiry, I’ve done some checking and figured it out.

Fraudulent loans. In the billions. Made by borrowers in the full knowledge that they could not – or would not – ever be repaid, often in collusion with fraudulent lenders. Many prominent Turks are involved.

Motorola got scammed by a wealthy Turkish family years ago and won a $4 bn judgment. Unknown whether they got their money back.

You knew it had to be something like that. Loan fraud is the oldest finance scam in the book. Any gambit you could dream up has probably been done with any number of variations, including the always popular Take the Money and Run scenario. Points to a need for honest and stringent controls, so on and so forth.

Banksters: “We don’t need no stinkin’ regulations!”

Lenders, especially foreign ones, still haven’t learned their lessons from the 1997 Asian crisis.

The situation you speak about, not having any intention of paying loans made by foreign investors back in full, was very common in The Philippines under Marcos and in Indonesia under Suharto.

Foreign investors, mostly from Hong Kong and Japan, who sued after Suharto had been ousted, found the local legal system to be fully arranged against them, as Jakarta courts usually ruled in the borrower’s favor, when they allowed the case to move forward at all. To add insult to injury, the lenders were usually billed for legal expenses incurred.

The Indonesian godfathers had been very careful not to have any sizable asset abroad (apart from their favorite “hideout” where they are always safe, Singapore) that could be seized by creditors and those who did usually relied on the time-honored “Matrioska doll” or “boite-a-secret” mechanism.

The whole system had been carefully set up from the beginning.

I have no problems believing Turkey has set up a similar system. Erdogan may not be another Marcos or Suharto, but as usual history is rhyming with herself. Popular strongman relying on a overheating economy built on very shaky foundations, foreign investors looking for double digit “risk-free” returns, consumer product companies in the West looking for cheap labor… it only remains to be seen how long it will last this time.

Agreed.

I think that is realistic, except that it falls too easily into the trap of blaming borrowers, which is easily taken. It is easily taken because the failure to repay is looked at as outright proof of poor faith. I don’t say what you mention has not occurred, but in international affairs it can be understood as an aggressive bet by lenders to break into a new market and build influence and leverage. Sometimes this position fails, or is even used to attempt to control a country, or even make it fail if it does not follow through with wanted reforms that are not directly atteched to the investment, or if it does not tow an acceptable political line. We are talking sovereign countries, and in practice they can write their own rules completely – no large international investors are not aware of this. They cooperate and mesh in ways that sometimes defy common understanding, out of sometimes temporary common interests where the positive accounting or its failure is only the veneer over which public discussion takes place. The wider objectives may be very different and inherently or potentially corrupt or hostile. So if you look at the chapters open that are stalled for Turkey’s EU accession ( e.g. at wiki) you find market reform, liberalisation, and politics are the three which are severely stalled. They clearly go together because they represent power and influence in or over a country. So those investing for a transition that did not happen are going to blame Turkey, but the equation works both ways. I am not defending Turkey, just saying you cannot blame it beyond a certain point, or else are into hypocrisy. If you look at the timeline of western involvement in Syria for example, there is little doubt that political demands followed the initial cooperation. So to my view Turkey, or rather Erdogan, is having to/choosing to wheel and deal his position as one set of circumstance after another plays out, and clearly he is doing that with his own position/that of his country foremost, which will not suit all, and especially anyone outside looking to profit from it in a specific way. How the whole region’s politics work are actually subtle and complex, often contrary to first impression, even if not to what we believe our own standards to be, or even our liking

Anyway, here are two links, and without mentioning a hundred other events

https://www.al-monitor.com/pulse/originals/2018/10/turkey-why-eu-interested-in-wellbeing-of-turkish-economy.html

Which looks at how Turkey/EU is balanced, and

https://m.aawsat.com/english/home/article/1418261/erdogan-orders-his-ministers-against-using-services-us-firm

Which is interesting in terms of sidelining McKinsey and therefore maybe US. Obviously it is in west’s and Turkey’s combined interest to resolve some kind of common direction from here, but it does not at all mean that will happen, or that it is even possible anymore. Too much going on at once.

The solution to Turkey’s problem is simple: It must completely de-dollarize. Only them can it completely solve its (non existent) currency problem.

In fact, this is what Europe, Russia, China, Brazil, South America, Venezuela, Iran, Africa, Asia, should do too to solve their problems: Completely de-dollarize.

The issuance of a sovereign national currency is rudimentary to all national governments.

It is a bit late for that.

They need the foreign currencies to repay loans.

When a country has huge foreign loans denominated in foreign currency and then says “Well, we will pay only in our own currency.” then you see crashes in the exchange rates like Venezuela, and the Weimar Republic.

Timbers

Turkey does have a sovereign currency (called the lira). Have you ever actually been to Turkey to see (daily) inflation devaluing the currency?

A sovereign currency means little without the skills & political will to manage it.

Yes, the biggie being “political will.”

1 Turkish Lira = 1.12 Chinese Yuan.

The Turkish Lira has appreciated over the last 2 months against the Yuan in fact.

https://www.xe.com/currencyconverter/convert/?Amount=1&From=TRY&To=CNY

Hi DQ, thanks for the article. Have you been following the Greek bank shares falling massively over the last week?

BTW this might be how it is done (de-dollarization to reclaim national sovereignty). IMO the key part it make it cheaper for non U.S. citizens to use the local national currency that the USD. That IMO is the biggest mistake nations like Turkey, Russia, etc make – to make it cheaper to borrow USD than their own currency:

“The Russian Finance Ministry has announced a plan to wean the country of dollar dependence. It is expected to be a long and painful process. RT has asked analysts to explain how this could be done.

According to the plan published this week, Russia seeks to de-dollarize the economy by 2024. The program is long and complicated, but its key point is that Russian exporters who use rubles instead of dollars would get huge taxation benefits including quicker VAT returns and other stimulus to ditch the greenback.”

Local currencies experience high inflation, so it makes sense to borrow in USD, the dollar being the home of “too low” inflation ideology.

Kudos to the Turkish stat office for being able to calculate GDP growth and forecast in the condition of fluctuating inflation. They must have some tricks up their sleeve. I wonder where they learned it?

Rep of Georgia is de- dollarising well, perhaps an example for Russia and others?

Thx, DQ, Wolf, et al., for this informative post.