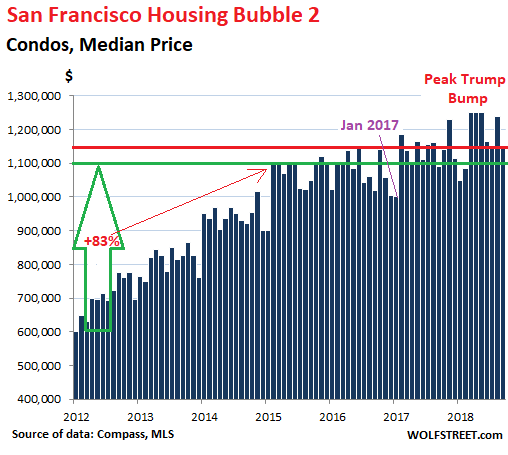

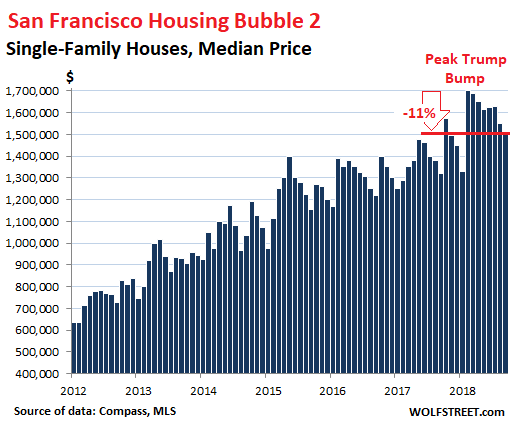

Sales volume drops to lowest for any Sept going back to 2005. Condo prices drop to Oct 2016 level. House prices drop 11% from Peak Trump Bump. It’s not fun anymore.

This is a phenomenon that is real and has cropped up in various aspects of the economy, including in asset prices, but also other data: The Trump Bump. After the election in November 2016, lofty prices that had hit a ceiling and had stalled or were declining suddenly took off again. There are many reasons, from being inspired by a Speculator-in-Chief to looking forward to big tax cuts and tax credits. The Trump Bump is a phenomenon of mass-psychology. It started before President Trump was even sworn in. But there are now the first data points suggesting that it has run its course.

San Francisco is a particular gem in the study of the Trump Bump because the city – in fact, the entire Bay Area – isn’t exactly a boiling hotbed of Trump love. Au contraire.

But vilifying someone out of one side of the mouth while adding up out of the other side of the mouth one’s suddenly inflating wealth is a fundamental part of the human existence, in a similar category as walking upright.

This theme became clear in the housing market in San Francisco.

Sales of units in condo buildings, “Tenancy in Common” (TIC) buildings, and co-op buildings – we’re going to lump them all together into “condos” – in the city of San Francisco accounted for 58% of total sales over the past 12 months. Sales of single-family houses accounted for 42% of total sales. Almost all new homes built over the past many years in San Francisco are condos or rental apartments, and practically no single-family houses have been built. So condos matter. They’re the majority of the market.

In September, the median price of condos fell $90,000 from August, to $1.15 million. The median prices and volume data here are from MLS (Multiple Listing Service), provided by Patrick Carlisle, Chief Market Analyst at Compass. “Median price” means half of the condos sold for more and half sold for less.

For example, Zillow, in its last email, pitched me 18 homes. The condos among them ranged from $549,000 for a 525 square-foot studio to something nicer and bigger, a three-bedroom two-bath unit for nearly $3 million. So yes, prices are crazy, but there is a fairly big range within that craziness.

And a median price of $1.15 million for condos is still a ridiculously huge amount of money, but here is the thing: It is the same median price as 27 months ago, in June 2016 (red line in the chart below). And it’s not far above the $1.1 million first reached in February 2015 (green line):

From January 2012 through February 2015, in just three years, median condo prices surged 83%, from $600,000 to $1.1 million, and then they began flatlining – meaning they bounced up and down but kept falling below the $1.1-million line and hit $1.0 million in January 2017.

Then the Trump Bump kicked in. In February 2017, prices surged. Note that this was the month when the deals closed and were reported to MLS as sold, but the deals were made weeks or months before then – so shortly after the election. The Trump Bump propelled condo prices up by 25% to peak at around $1.25 million in March, April, and May 2018. But this is now getting wrung out of the system.

Other aspects of the San Francisco housing bubble are, let’s say, mixed.

Sales volume of all types of homes dropped to just 318 dwellings. This is down 8% from a year ago and down 22% from September 2016. In fact, it was the worst September in the data series going back to 2005. Even during the housing bust, September sales were higher.

But it’s not for lack of inventory. Total listings reached 1,208 homes in September, which gives the city 3.8 months’ supply at the current sales rate.

Single-family house sales dropped 18% from a year ago, to just 145 houses. The median price dropped to $1.515 million, down 11% from Peak Trump Bump in February 2018, when it was a mind-bending $1.7 million. But it’s still up $195,000 from a year ago. So easy does it:

The median price of all types of homes dropped to $1.325 million, the lowest since January this year, but remains $80,000 (or 6.4%) higher than a year ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you Wolf.

Seeing the median drop like this is even more significant because the majority of new condo’s that have come on the market the last two years have been classed as “Luxury” units.

With all the condo’s in the pipeline it looks like luxury will get a bit more affordable soon.

BTW, I sent you the September numbers for Sonoma County, I hope you find them useful.

Two market changes I have noticed

1) Buyers are taking condition issues more seriously, they seem to have realized that all the local contractors are booked at least two years out.

Turnkey homes bring more of a premium and homes with condition issues are bringing less.

Ticky tacky new subdivisions are now offering a 3% broker co-op ( Commission) rather than relying on their in house sales staff and in house marketing.

I got one from an outfit in Calaveras County that was sent to every agent in Sonoma County and probably the State.

It will be nice to see more affordable prices.

Different market but in Charlotte area, have seen a large national builder offering 7%! buyer agent commission for existing inventory if closed this year. Crazy.

This scenario has created ‘Fear of Missing Out’ propaganda by the California Board of Realtors, in order for Brokers and Agents perpetuate a ‘Bidding War’ on ‘a perceived ‘deal’ home.

Let’s sit back to observe how these current two income buyers can sustain their mortgage over the next few years, along with the rise of the hidden costs to maintain a house and a healthy household.

This scenario has created ‘Fear of Missing Out’ propaganda by the California Board of Realtors, in order for Brokers and Agents perpetuate a ‘Bidding War’ on ‘a perceived ‘deal’ home.

Fear of Missing Out (FOMO) has turned to Fear, Uncertainty, and Doubt (FUD) as the serial dissemblers of the CAR can no longer conceal the reality of a bursting housing bubble. Any knife-catcher foolish enough to buy a house before the bottom drops out – which is coming – is going to be a cautionary tale, as will be the FOMO lemmings who were foolish enough to buy into an unsustainable housing bubble created by $15 trillion in FedBux confetti lavished on the Fed’s favorite investment banks and speculators.

When I add MEX before $ it all starts to make more sense to me.

Wolf…I thought this chart on global real estate prices (San Francisco included) might be of interest…https://i1.wp.com/jugglingdynamite.com/wp-content/uploads/2018/09/UBS-global-real-estate-Bubble_index_ranking_2018_en_

The link doesn’t work.

Try this. (Previous link seems to be missing some characters at end of URL).

https://i1.wp.com/jugglingdynamite.com/wp-content/uploads/2018/09/UBS-global-real-estate-Bubble_index_ranking_2018_en_02.jpg?ssl=1

It’s hard to know what to make of the chart without knowing what factors they considered. It would be interesting from a sociological and political perspective if it was built around median incomes for example. The relative price trends would play a role there too.

From an investing perspective I’d be very wary about a chart like this. Wolf likes to point out that real estate is always a local market. In the US alone, Chicago and San Francisco have very different dynamics. Once you cross international borders, the rules and forces drastically change, so the market will behave very differently, both in terms of natural levels of affordability per unit space and in terms of length and magnitude of potential price deviations. Apples and oranges basically.

Perspective time. Using the numbers mentioned in the article a middle of the road new condo is in the ballpark of $1,000 per sq foot. I know building and the cost of construction. Materials, permits, wages, etc start the pricing at around $300 per sq foot Cdn for a stand alone single-family dwelling, (those units no longer built in SF due to their high cost per footprint). Where is the other $700 per foot riding in from? Land aquistition, zoning fees, RE marketing, development profits? Does every sub-trade pull off a skim/markup?

Something is beyond out of whack. Even if land is like gold, with condo construction the footprint cost is still divided up by the number of units. When I was in my twenties I built many condos and apartments working on a framing crew. We would be on the 4th floor still building while mechanical were installing the sprinklers and plumbers did rough in down below. The roof would be on in about three weeks and the electricians moved in staying just ahead of the drywallers. It just doesn’t take that long to knock these places up in todays specialized sub-trades with prefab finishings etc.

My theory is a huge and hidden skim is supported by low interest rates. Competition is non-existent and cost justification doesn’t exist because it is hidden by low financing and mortgage costs. Demand destroys competition with builders booked ahead far in advance.

I know people with their own electrical companies. When they log on to the wholesaler their screens show prices to be about 50% of retail. These savings are never passed on to the customer unless it is a friend or relative. Multiply by this for every product and every trade and you begin to see how inflated building costs actually are.

This past year I built myself a lovely little 640 sq ft rental. Materials including electrical, plumbing etc ran me $40,000. I did all the work myself from forming to finishing including drywall, plumbing, roofing, wiring, everything. Everything. I worked approx 6 hours per day 6 days per week for 8 months and I’m in my 60s, so it wasn’t highballing. This included material runs to town and the occasional day off for fishing. If I paid myself $100,000 (damn near $100 per hour) and cost the land out at $100,000 the project would still come in under $400/sq ft for everything.

When I appraise builders, sub-trades, and RE agents I always look at what they are driving. When I see an electrical company operating a new Mercedes van I know they are gouging. Same for the builders. I look at their trucks, tools, work clothes, tires, and how fast they move at the lumber yard. When I see RE agents driving a Hummer instead of a mini-van I know they are not working for their customers. Just sayin’.

If 4% is creating a drop wait until mortgage rates approach 6-7%. Then you’ll see some belt tightening, price drops, and real competition.

Similar, I built own completely using thermal clay blocks, only high quality materials, a lot of wood and it came out around 50 per square foot. Sometimes the work seems tedious, not heavy, but if you take it in your own time it stays rewarding, you just have to commit to doing a proper job and finishing everything properly no matter that it takes a bit more time. It is a real eye opener to do this, you know your house to a detail, and you can look at near any building afterwards and appreciate (or not) how it is built, the kind of work that has gone into it.

Paulo — great story and congrats on your (truly) own house. Very inspiring. I suspect the quality of your home is far superior to the crap work that goes into most “luxury” condos!

I believe a lot of people in Scandinavia build their own “hyttas” (small cottages) as a family effort. And of course now there are lots of great prefab houses available. Sadly these opportunities aren’t typically available in cities, of course.

I used to spend time in Kuala Lumpur where there is always a lot of construction going on. I could watch from my hotel the new “luxury” apartment buildings going up. My god, that looked like cheap construction and possibly dangerous.

I’d give RE agents a break in this area. Probably 90% of what makes a sale is the RE agent’s personality, looks, and what they’re driving. If you don’t have a new car, good looks, the latest cell phone, etc well you’re going to be fighting an uphill battle.

RE sales is … sales. People will buy from you if, consciously or not, they want to *be* you. So if you’re tall, not too dark, have nice teeth, etc you know the drill, then there’s a strong pull for people to buy what you recommend.

And no one wants to ride around in a ratty old minivan looking at houses.

So you’re going to get RE agents driving their clients around in the fanciest cars they can manage. If they’re smart they’re leased, only driven for business, and the ratty old minivan is their daily driver.

For some reason you just reminded me of the book Native Tongue.

I just looked up the Wikipedia on that book – sounds pretty wild! 1984? Man, that’s when Gibson was writing his first “Cyberpunk” stuff. I remember reading his “Johnny Mnemonic” in OMNI Magazine about then.

Thanks for bringing up language, though. Because along with the right looks and social signals, yes, you’ve got to have the right kind of language. A proper accent, or non-accent. In England it’d be called “BBC English”. No unclear speaking or hillbilly accents, thank you, much less what I call the “underclass mutter” that can be really hard to understand.

I do NOT buy houses based on agents look. The more attractive they are, the more I want to lower the price. I will take lower price OVER their looks and feels EVERY time. There is a disgust in me toward the realtor agent industry and buying process. I do NOT believe a single word they say. They are my enemies.

This is why I say looks etc are 90% of sales.

I also do not state that those 90% of sales are good deals for the buyers, either.

Remember it’s based on looks, charm, the ability to schmooze.

You’re in that elusive 10% of buys who see through all that bullshit.

ironically, though it’s not related to real estate, the same thing goes on in the pharmaceutical industry. A lot of the big pharma drug companies like to hire bikini models, Maxim/Playboy models, and NFL cheerleaders to become drug representatives specifically to pitch new expensive drugs to male doctors. Apparently this works wonders, as they keep doing this.

One large per sq ft is ridiculous, in my hood $100 not that long ago, now it is mostly $200. CPI (labor costs a wage component) has not appreciated to the same degree, and while materials have gone higher (as China buys up everything in site) this kind of bubble does not make any sense. I do know muni govs have a choke hold on new construction, and my muni at least is spending money like no tomorrow, even after they abolished the state redevelopment program. I suppose these projects, (and they look like projects) are subsidized but I don’t know how or where, which would explain the (padded) costs. Maybe a lot of munis are swimming naked, who knows?

San Francisco is just the tip of the ice berg.

It’s a micro economic view. One market sector, one item.

Take a macro global outlook at what is transpiring and it will scare the you-know-what out of you! This is NOT an anecdotal statement.

Australian real estate has tanked.

Canadian housing sector is rolling over.

London’s high priced market is being abandoned.

The entire Chinese debt built housing sector is wobbling.

Bear in mind, this is just the residential real estate sector. When you begin to look closely at the global commercial real estate market, it gets even scarier.

Mix in a good dose of global, crazy multi lateral politico/military tensions along with a heating up currency war and we have a recipe for some spectacular fireworks ahead!

Look at Palo Alto, Belmont, Redwood City, Menlo Park, Mountain View, Cupertino, Saratoga…That is the Gold Coast in Bay Area for working rich. Or Woodside or Atherton for the actual rich.

Only fools (Wolf is an old timer) would now buy and live in SF.

Maybe Wolf likes SF and actually wants to stay there?

I make 1/10th or 1/20th of what Wolf does, maybe 1/50th, not sure, and I like it here because this area doesn’t require a car, which would cost my current yearly gross income to own and operate. Or heavy winter clothing, winter heating (gas, electric, propane buddy heater, campfire, something) and not working for half the year.

If I live just 35 miles outside “the city” here, it’s like that. No work for half the year, a certain amount needs to be spent on heat, and much more clothing and heavy boots required.

Yeah, I only make about $15k here, but 35 miles out I make $7k. Go another 35 miles and I’d be doing well to make $3.5k. See how this goes? Go out as far as Arizona, where I was living with a friend, and my income might be $1000 or $1200 a year if I’m really enterprising (not counting food stamps at about $150 a month).

If you don’t have car expenses, winter expenses, and year-round work, so what if a studio costs you $2000 a month? There are a lot of thrift stores and such resources in SF too. I’ve found a decent Goodwill in my area; Wolf probably has 10 places as good up where he is.

Neal Woods,

Yes, we love it here. There are some big issues, but there is lots to love too.

The issues are so big that for the first time in my life I’m getting involved with our local candidates, particularly for Supervisor in my district, where I actually talk to them, let them know what I think the biggest issues are, and listen to how they want to address them. I want to make sure these issues are on top of their agenda — and that they have reasonable solutions in mind.

This process of getting involved at the local level is actually enjoyable and soothes somewhat my very cynical feelings about how our democracy in general functions.

Please report back and let us know how things develop. My own brief involvement in local politics made me more cynical than I ever imagined I could become. But hey, maybe I’m an outlier.

Buckaroo Banzai,

I was talking about this little corner of local politics. There is the corruption part in SF local politics (and elsewhere) that is really sickening. And it’s not going away. That part continues to make me more and more cynical. So I won’t be able to give you a clean answer when I report back a few years from now, but hopefully, SF will address and mostly solve the three issues I’m most worried about (along with many other residents). And I will be happy to report back if things have improved or gone to hell entirely… this will take a while though, so be patient :-]

Congratulations in getting involved in local politics. SF politics is fascinating. It is a weird combo of deep corruption and good policy, laudable do-gooders and extreme cynics, and that’s often all in the same person. My advice is take this town’s politics with a sense of humor. Humor and absurdity will check the cynicism.

I used to live near the old Gold Coast on the N. Shore of Long Island where the robber barons of yore built their mansions. Most have now been torn down, some are museums or part of the park system. I wonder what they’ll do with Silicon Valley when it’s over.

Go to Detroit and look at the mansions built 100 years ago by the “Horseless Carriage Millionaires”. Many of them are still standing, more or less.

https://www.youtube.com/watch?v=3p7G4hpvUn4&feature=youtu.be

Los Gatos will look like this in 100 years.

Hence my user name!

It will be nice seeing some of the finest agricultural land on the planet returned to agricultural use.

Been to Palo Alto, it sucks. Been to Redwood City, it sucks even more. Menlo Park, Mountain View and maybe parts of Cupertino, ew. Good indian food but terrible places to live these days if you are spending 1.5 million to buy a shack.

Saratoga, Woodside, Atherton you can only compare against Pacific, Laurel Heights or Sea Side etc., apples to apples and I would pick the latter any day if I could afford it.

Last but not least, it’s too darn hot in all the places above. Give me fog city and my Golden Gate park, beaches, bridges and headlands any day of the week.

Yeah!!!!

Someone gets it!!!

Trump is another example of the finance-dazzled ‘head in sand’ western politician – he laughably thinks that a country’s economic wealth and health is indicated by stockmarket indexes, when in reality those indexes reflect nothing apart from rampant speculation predicated on cheap credit – and employee low wages.

Hence the disconnect between main street and wall street – and more worryingly, the abject failure among the political class to not only address that issue (because that requires better pay and we don’t do that because it affects stockholder returns), but even acknowledge it exists in the first place.

So how, exactly, is he different from any politician? Politicians are either colossally ignorant about economics (most of them), or are knowledgeable about it but don’t dare speak the truth about it because it will spook the herd (a few of them).

Trump is most likely in the second category, but even if he’s in the first, it doesn’t much matter. This system is headed for collapse either way. Trump’s practical hands-on knowledge of business might help him make some good decisions behind the scenes to lessen the impact if the collapse happens on his watch. Or, maybe not, who knows. Looking at the current national political landscape, this country is hopelessly and thoroughly F*cked (or “FFFFFFF*cked” as our newest SCOTUS judge might say).

The politicians themselves are stupid but their appointees are self centered selfish looters.

Wilbur Ross, US Secretary of Commerce, the biggest proponent of Steel Tariffs. He says it’ll bring steel manufacturing back and help US industry while completely laughing off how it will impact companies using steel (like car companies, truck companies, construction companies).

Is he just an old fool?

Just look at where his investments are. Just look at his career experience. He’s making tremendous profits RIGHT NOW.

He doesn’t care if many US companies go down because of higher input prices because his own investments go super high

The Americans are being suckered into believing random nonsense which is picked up by American media (most of it who has a vested interest in people believing that nonsense).

It’s too sad. I really really feel bad for people who believe in American politicians. I hope the younger generation survives this.

This phenomenon is not unique to SF. I can attest that most regions in Florida also experienced a price surge sometime between Spring ‘17 and Spring ‘18.

Prices are definitely coming down now though. Although price cuts are rather modest at this point, they indicate a change in trend. Also, time on the market appears to be rising. And this is at a time when the economy is otherwise quite robust.

I suspect the price decline will be a multi-year process which may exacerbate as overall economic conditions will likely begin deteriorating starting in the second half of next year.

As Iv’e mentioned before, I think national average house prices are likely to decline somewhere in the range of 15-25% over the next 2-3 years. In real terms this would be an almost 40% decline from the 2006 high, which will likely prove to be a multi-generational high.

Also, ZH linked to an article today which shows that the housing ship in Denver, one of the biggest price gainers over the past few years appears to be tuning around as well:

https://www.denverpost.com/2018/10/03/denver-housing-market-goes-cold

Sales volumes have fallen substantially and although YoY prices are still up, it’s only time before rising inventory and mortgage rates start weighing on prices as well.

I’m getting reports and articles from people in Seattle that document similar conditions: falling sales, rising inventories, and prices that started to decline a few months ago though they’re still above, if barely, where they had been a year ago.

The Case-Shiller index (which we track here on a monthly basis) lags about four months behind. But it should pick up the declines pretty soon. So far it has just shown slowing price growth, rather than outright declines in Seattle.

Just a heads up… I am not sure if you use it or not but Zillow has an outstanding statistical section which can be used to analyze the housing market using hundreds of measures and variety of geographical breakdowns:

https://www.zillow.com/research/data

The President has NO impact on the economy of the country. Bush or Obama did NOT create the recession. Nor the congress, republicans, democrats, independents have any impact on the economy. Trump’s policies including tax reforms have ZERO impact on the short term. It can only have an effect on the medium/long term. The economy, San Francisco housing and the stock market would have surged whether a republican or a democrat occupied the White House. Only the policies of the Federal Reserve has an impact on the economy and market has reacted according to Fed interest rate policies. In terms of the employment situation, more jobs are created in almost all countries of the World led by America. Unemployment rate has declined even in Canada. Housing prices has increased in several countries around the world Did Trump cause an increase in employment or an increase in home prices in Canada or other countries around the world?

Agree mostly. But I think you misread what the Trump Bump is. It’s a psychological phenomenon. It started even before Trump’s inauguration. Mass-psychology is a driver in asset-price inflation as well as in market crashes. This mass-psychology can be impacted by many factors, including the Fed, presidents, the media, Musk, etc.

Honestly Wolf it has little or nothing at all to do with Trump outside of tech stock valuations.

One thing FAANG has done is make middle management in corporations RICH, with salary and stock packages in pro-athlete territory.

These people have to live with-in a commute to the City/S Bay, so while they were single they bought Condos to live the urban lifestyle.

Now they are rising families and moving to the suburbs to have a yard and a dog for the kiddies, with literally no limit on what they can and will spend on traditional single family homes.

At this point a market correction will only accelerate the whole process as the cost basis is zero and the benefits of diversification become obvious.

the point is that compared to the “judgements” that “analysts” have made on the valuations of “equities” under “capitalism” a single family home in driving distance of the office still has an almost unlimited upside.

Your last phrase, “…has an almost unlimited upside” is a dead-giveaway that the market has peaked. I’ve heard this phrase every time after the market has peaked while promoters were still trying to whip it even higher. It’s a scary phrase, even scarier than “this time will be different.”

Nothing has an “almost unlimited upside.”

“Nothing has an unlimited upside”

Sure it does. For example, I believe the price of a loaf of bread in Zimbabwe went to 100 trillion Zimbabwe dollars a few years back.

;-)

They are rich with a cost basis of zero…. just like all my tech friends south of Market in 2000, and in the nationwide retry in 2006.

BTW, in your analysis above, what does this supposed mass exodus from condos to SFH do to the condo prices? If this unlimited upside is true, why did the market not jump to that equilibrium immediately?

Spoiler: The answer is that SV/SF is a boom town and all boom towns are cyclical. Also, most residents of boom towns become a boiled frog and don’t see the issues.

Wolf – does the Trump Bumb impact all matkets or just some markets? Is there something else going on in the markets that are softening? What about the new tax law – it could be argued that it negatively impacted states like Cailfornia with the cap on state taxes. Could it be that certain markets finally overeated after years of strong ecnomic growth and low interest rates – regardless of the president? I’m not convinced of the Trump Bump.

The way I’ve always looked at it as soon as it appeared: The Trump bump is a temporary phenomenon, based on mass-psychology, that will eventually vanish. According to this scenario, it will look like a true bump: its goes up and it goes down.

After the bump, the economy and asset prices will seek to find their own ways (wherever that will be).

Lots of things have changed over the past two years, including fiscal policies, rising interests rates, and majestic asset price inflation. These are all fundamentals that will impact the economy and asset prices over many years, long after the Trump Bump has vanished.

Keynes used to call it “Animal Spirits”.

Of course, Trump has very limited impact on this bubblicious cycle. Acting Man had a chart with rising stock market, next to a picture of haplessly looking Trump shrugging his shoulders, with the title: The Donald just cannot help it.

The central driver is the FED, with its special status among central banks, and other central banks follow competitive interest rate policies.

People in places with rampant housing bubbles were bemused (and some not very amused) by the rising housing prices. Who believed that they have anything to do with reality? So now, like a herd are heading for the exit.

Will the stock market follow?

You can be sure the right-wing media will blame the slowdown on whatever gains the Democrats make in the midterms.

Nobody in the rest of America wants to move to California, including me. That’s the elephant in the room. We chose red state, middle of nowhere, fly over country, over CA and don’t regret it at all.

Bottom line is you couldn’t afford it anyway, right?

No we can’t and neither can the people living there. When people live in trucks while holding a good paying job, it’s crazy town.

Volkswagen just put out a version of its old camper and they named it California. I wonder why.

Volkswagen just put out a version of its old camper and they named it California. I wonder why.

Because the F**ked Borrowers (FBs) who bought insanely overpriced housing in California are going to end up living in campers and tents after the implosion of Housing Bubble 2.0 wipes them out financially.

I think you answered your own question, Petunia

the “california” is not sold in the usa. somehow, that seems fitting. to your point, old vw camper vans have become shockingly expensive. ask me how i know :)

Ha. The VW California is a practical joke from Wolfsburg (who knew they were in joking spirit). Not available in NA.

…thought you just needed to wear some flowers in your hair and that was ok ?

You should see the flowers in my yard.

IN THE WINTER.

Here in south Spain/Portugal we are roughly similar climate, rarely freezes. Inland is dry dry over summer, but west of Gibraltar there is more precipitation and cooler summer so it stays a bit greener. The seasons are very different from northern climate, the winter is when everything greens up, flowering is often very early, some plants in mid winter … a lot of plants will just not go dormant. Great to be able to grow mango, litchi, avocado, even papaya . The last time I visited SF was going on three decades ago, still remember the Japanese gardens there… blues festival….and just ambling around all over as I tend to.

Keep on spreading the word, AZ is nice. NV has gambling. Or has lots of trees, We have nothing really. It’s sad.

Pet, dear, I’ll stand by my dictum: There are two kinds of Americans; those who live in California and those who wish they did.

I used to live in CA and don’t miss it at all. I live in flyover red state, not my political cup of tea, but this place and the Bay Area are a wash when it comes to amenities, natural beauty, etc. Ten minutes commute to anywhere and plenty of trails near the river and mountains a short bike ride from home.

I think the sweet spot is somewhere on the East Coast – Raleigh?

Or maybe contentment is just a state of mind. Where you live and how much money you have is secondary.

Why waste energy hating where other people live? I live in California and love it. You may live in Nebraska and love it. Is this a reason to sneer at each other?

I find these arguments pointless because few people truly “choose” where they live. Most of us get planted where job or family dictate.

All I know is that I live in Marin County, where all the newly fertile city dwellers are now moving because the kids need schools, and on my street there was a for-sale sign that pretty much said it all:

It said “coming soon” on the bottom and “sold” on the top.

Nothing says “trust me” like an anecdotal sample size of one that is at odds with the aggregate market statistics.

Not trying to forecast past my own yard. Wolf brought up San Francisco, not me.

Tens of billions of dollars get materialized out of nothing every day, and it is all rushing into a handful of geographical venues in the planet. The Bay Area is one of those venues. Unless that river of money dries up, or it starts getting directed someplace else, real estate prices must keep going up.

Based on how our economy is structured, and the political stranglehold that the FAANG tyrants have on the left side of the political spectrum, that river of money is headed no place different for the foreseeable future. I will allow that there is a decent chance that Trump will use antitrust laws and/or the Communications Act of 1934 to smash the power of the technocratic oligarchs–that might change the fortunes of the SF real estate market. Or it might not. The only thing that is going to change it for sure is, if the out-of-control dollar creation spigot gets brought under control, or if the whole system blows up.

There was a definite Trump bump out here

On the Olympic peninsula. A few months into the 2016 election things were picking up ,After ,red hot hot. Peaked about

Six months ago. My Zillow updates are now about 70% price reductions and now the “motivated sellers “ are cropping up.

As for the stock market indexes. They have been undergoing distribution all year. Last I read stock buy backs up. Insider selling up

2019 going to be an interesting year

The most commonly heard phrases I hear at cocktail parties around the Bay

– “everyone is fleeing SF”

– “SF is too expensive”

– “SF population is declining”

– “uHuals are all booked up – heading to Vegas”

– “SF has terrible schools”

– “Jobs don’t support rents “

– “no one can afford a house”

– “condos are over priced”

– “too much building will cause a crash”

Meanwhile SF is still the most expensive city in the US. So many of those catch phrases seem specious at best. SF is growing every year. More and more people live there and move there every year. Spillover impacted neighboring cities and suburbs.

The only phenomenon worth watching will be the baby boomer retirement and mass migration or plain old dying off. Perhaps that’s the devil lurking beneath all this craziness.

San Francisco has always lived with boom-and-bust cycles — ever since the gold-rush days. I see nothing that took SF off the boom-and-bust cycles. We’ve had seven years of boom, and now the people who’ve been here for a few decades are waiting for the bust to set in. It will just be normal San Francisco.

Two things: To appreciate the beauty (make-up) of SF, on a cool clear winter day go to the north side parking lot of the Golden Gate bridge and look at a picture perfect “photo” of a world class cosmopolitan city.

#2….get to the same place on May 1 of each year and see the more than 5,000 sailboats on the bay inaugurating the annual sailing season.

Born and raised in SF; left in my mid-twenties….but still feel that SF is one of the most outstanding cities in the US. It will always be desirable to live in despite all the political hullabaloo!

“No one goes there anymore because the line is always out the door.”

-Yogi Berra

I suspect the SF real estate market is directly correlated to the amt of venture capital flowing to tech/social media start ups. If/when that dries up, so do the overpaying jobs and poof.. a glut of overpriced homes and office space flood the market. Dotcom bust 2

Meanwhile, in Seattle, we have a record increase in inventory:

https://www.seattletimes.com/business/real-estate/as-sales-plunge-king-county-home-inventory-has-biggest-jump-on-record/

IMO it’s just as likely for Bay Area real estate to double from here, than to get cut in half. More likely, actually, to double.

One thing’s for sure. The further up the prices go, the worse it’s going to end for everybody.

Had you told a resident of Haight-Ashbury c. 1927 in forty years his street would sport property so cheap to buy and to rent it would become one of the cornerstones of the hippie movement, he would have probably noticed the nearest policeman a raving lunatic had escaped from the asylum.

As Wolf always says, San Francisco real estate has always gone through cycles. The main difference is since the 90’s these cycles have become shorter and more intense: Haight-Ashbury was an expensive upper class neighborhood with increasing property prices from its birth around 1887 until the Great Depression, over forty years later. WWII, with the need to house workers contributing to the war effort (think Hunters Point) brefly stopped the following decline, but housing generally remained cheap in Haight-Ashbury well into the 70’s.

These days the pendulum swings much faster.

Also remember that valuations in San Francisco are so extreme that a 10% drop, which is a very mild correction in any overheated market, means losing a whole lot of money: if the median house is one and a half million, it means $150,000 in median home equity goes “up in smoke”, to stay in character. Unless banks still have an appetite for 2005-style shenanigans, that alone would suffice to put an end to a lot of excesses.

This article gives way too much credit to Don Dump. Interest rates are going up. Don’t fight the Fed. Sure, Don Dump 10k cap tax ‘reform’ has an impact, but this is just the end of the cycle. It would happen no matter who is in the Idiot House.

Prop 13 is killing CA. Stifles new entrants and locks people in. Limited new entrants means limited move ups all the way up the chain.

Also, a large part of real estate ‘appreciation’ over the past 40 years is really just dollar destruction. It’s just hard to see when you live inside the ecosystem…

You guys are kidding, right? Trying to ascribe arbitrary value and a terminal upside to an asset you can LIVE in, enjoy PERECT weather, unbelievable nature, and deduct (some of) for tax purposes?

Meanwhile, AMZN trades for 45X EV/EBITDA and Banksy paintings are worth 1 1/2M$ and double AFTER they self shred?

Maybe it is the way we keep score ($’s) that should be suspect?

This is a key point: No one has to live in stocks. Shares can go totally bonkers for a long time because they’re not impacted by economic fundamentals. They’re impacted by mass-psychology.

Housing, however, sooner or later requires that someone can afford to live in it, or else it’s just an expense without use or revenues. So the housing market, while also driven by mass-psychology, hits some real-world limits, which is when you run out of people at the margin who can afford it, or people who are willing to spend a big part of their income on housing.

Once you lose those buyers at the margin, the market turns. Once the down-trend sets in, people realize that owning a home is an expense, and when you overpay, that expense is too big, and when you wait and let prices settle, you can benefit for decades from a few years of patience. This isn’t new. Been there, done that.

All I am trying to say is that San Francisco IS DIFFERENT, because housing prices correlate with the those stock same stock prices that you admit can be “bonkers for a long time” because so much of the concentration of that wealth is in fact here in the Bay Area.

Throw in natural restrictions on build able land (85% of Marin is park-land) and you have a mark that will not lose buyers–at the margin–until the tech market turns, and maybe not even then (at least for a long while).

You live here, right?

Yes, I live in SF, three blocks from the Bay, where I just got through swimming a couple of miles. Gorgeous!! SF has always been boom and bust. Nothing has changed. Everyone who has lived here long enough knows this. It’s just a question of when.

I understand that Marin is different from San Francisco. There has been a lot of new construction in SF, but essentially none in Marin. In many places, Marin is a bedroom community for San Francisco. Real estate is local, so things change differently. For example, the housing market in Sonoma County (just to the north of Marin County, for our non-Bay Area readers), is already experiencing an inflection point.

my view is from the same downtown nyc neighborhood fo 30 years. in my1400 unit complex, i now only see 2 kinds of renters:

1) international financial workers

2) 20 something singles tripling up in shared one bedrooms.

manhattan island has been completely taken over by wall street. when this ends, it’s going to get ugly.

The town I like in the SF area is Sausalito, the little town on the bay below the big hill road winding down to it.

Oh wow! Now you’re talking! My place if I could come around once more! Wanted to move there in the late 1970’s but no way even then……..beautiful area; contained………there’s also Tiburon but that is/was very “classy” even back then.

I’ve been living near the “back door” to Yosemite Nt’l Park for the last 20 years; escaped Silicon Valley……..live great on modest pension/SS with also modest savings.

“The Trump Bump is a phenomenon of mass-psychology”

Wow, and I thought trucking going bonkers and those 4% GDP prints were real! Not to mention the record low unemployment and rising wages.

It’s all in my head, OK, I can deal with that Doc. My wife’s been saying that for years.

Have a look:

https://wolfstreet.com/2018/10/04/signs-trucking-boom-has-peaked/

“Housing, however, sooner or later requires that someone can afford to live in it, or else it’s just an expense without use or revenues. ” states the author.

While I agree with the sentiment of this article, I cannot allow the above comment to stand unchallenged. Housing has become the new gold for wealthy investors and funds. Like gold, housing may go up or down but in the end you still have something (mainly the land as in many cases the homes fall into disrepair).

While, historically housing has been viewed as a proper asset (series of cash flows), there now exists an enormous glut of global ‘free money’ capital that has been printed by the banks.

This excess money has a found a home in residential real estate. This money is not seeking growth, just the ability to exist.

The below links are just the tip of the iceberg for information on the ‘mis-allocation of homes as a store of capital’ topic. I hope they lend credence to my comments.

https://gritpost.com/vacant-properties-homelessness/

https://vancouver.ca/home-property-development/empty-homes-tax.aspx

http://uk.businessinsider.com/property-partner-20000-ghost-homes-sitting-empty-in-london-2017-4

Well… not really. Not at all.

Housing prices fell 40% during the last minor correction. An 80% decline is just getting underway.