Every housing bubble requires the connivance of the banks and regulators. Australia is no exception.

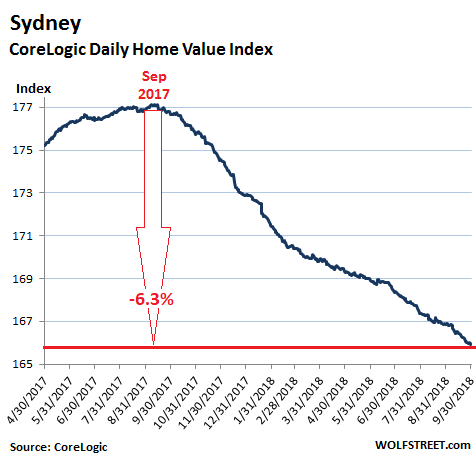

Sydney’s housing bubble, one of the most magnificent in the world, is deflating further. So far this year, home sales volume has plunged 18.5%, according to CoreLogic. And prices have followed. In September, this is what happened compared to a year earlier:

- Prices of single-family houses dropped 7.6%;

- Prices of “units” – condos in US lingo – fell 2.6%;

- Prices of all types of homes combined fell 6.1%,

- Prices at the most expensive quarter of the market dropped 8.4%;

- Prices at the least expensive quarter of the market fell “only” 3.3%.

CoreLogic’s Daily Home Value Index is now down 6.3% from its peak on September 10 last year:

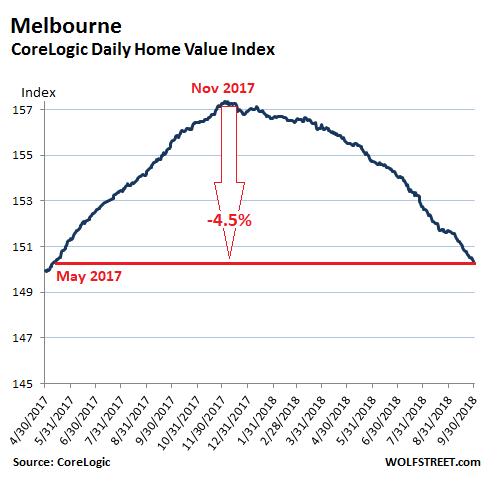

Melbourne’s housing-bubble deflation has been lagging a few months behind Sydney’s but is now catching up. So far this year, sales volume has plunged 15.8%. And prices have followed: Year-to-date, house prices fell 5.1% and unit prices are down 1.5%. Over the third quarter alone, prices fell 2.4% compared to the second quarter, making Melbourne the fastest deteriorating housing market among Australia’s eight capital cities.

At the most expensive quarter of the market, prices dropped 6.7% from a year ago. At the least expensive quarter, prices were still up 4.1%.

For all types of dwellings combined, prices declined 3.4% year-over-year, according to CoreLogic and are down 4.5% from their peak at the end of November 2017:

So how big were those bubbles?

“Despite the recent falls in Sydney and Melbourne, dwelling values remain 46% and 40% higher than they were five years ago, highlighting that most home owners in these cities continue to benefit from a substantial lift in wealth from the boom in housing,” explained CoreLogic head of research Tim Lawless in the report. So there’s a long way to go.

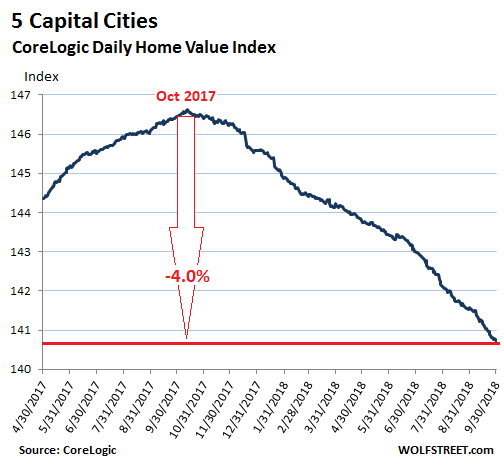

Corelogic tracks the largest five of Australia’s eight capital cities in a separate index. Sydney and Melbourne account for about 60% of the national value of housing and weigh the most in this index. Home prices in the remaining three cities in the five-capitals index weren’t hot either in September:

- Brisbane: home prices inched up 0.8% year-over-year.

- Adelaide: home prices inched up 0.7% year-over-year.

- Perth: home prices fell 2.8% year-over-year and are down 13.2% from their peak in 2014 when Western Australia’s mining boom turned into a bust.

The aggregate five capital cities index fell 3.7% in September year-over-year. It was the 12th month in a row of month-to-month declines. The index is now down 4.0% from its peak in October 2017:

In the remaining three capital cities:

- Hobart: home prices surged 9.3% year-over-year, to a new record;

- Darwin: home prices fell 3.7% year-over year and are down 22.1% from their peak in 2014;

- Canberra: home prices rose 2.0% year-over-year, to a new record.

Investors still account for 41% of the value of new mortgage demand, according to CoreLogic. But they’re being hit by new regulations and higher mortgage rates designed to tamp down on investor enthusiasm.

And rental yields have been miserably low: In Sydney, “gross rental yields” – annual rental income of a property as a percentage of the property’s value, not including interest and other expenses – were 3.2% in Sydney and 2.9% in Melbourne.

Subtract interest and other expenses, and it’s a money loser. These losses are mitigated by being deductible from income taxes (“negative gearing”), but they’re still losses, and the only hope for investors under these circumstances is that the property will rise in value. But the opposite is happening now.

Every housing bubble requires the connivance of the banks and their regulators, and Australia is no exception. A banking scandal of enormous proportions has partially come to light via the Royal Commission investigation of the banks and revelations from other sources, as regulators played ball with the banks, and politicians encouraged it. There is nothing like a big housing bubble to make everyone look good and bring in the dough.

But these things can go only so far before the whole edifice – including the banks – is at risk of collapse. So now efforts are underway to get a handle on it and tighten up lending, particularly for speculators and over-stretched households.

Among other items, there is now a new focus on debt-to-income ratios, which pull many households out of the more expensive ends of the housing market, such as in Sydney and Melbourne.

“With the release of the banking commission interim report, there is a chance that already tight credit conditions could tighten even further,” CoreLogic’s report points out:

The constant theme from the report is that regulators should monitor and enforce existing policy much better, while lenders and brokers need to place client interests ahead of profits. This implies a more conservative lending approach going forward which is likely to impact further on credit availability.

The latest credit aggregates from the Reserve Bank show housing credit growth tracking at the lowest level in almost five years, and investor related credit is growing at the slowest pace on record.

If credit conditions do tighten further from here, we can expect housing market activity to follow suit.

But supply of new construction is surging:

In Greater Sydney, 77,000 condos are scheduled to be completed in 2019 and 2020, which will increase the total stock of condos by 9.3%! In Greater Melbourne, nearly 79,000 units are scheduled to be completed in 2019 and 2020, which will increase the total stock of condos by 11.5%! CoreLogic:

With such a substantial pipeline of housing stock in the wings at a time when credit has become less available, investment and foreign buying activity has fallen materially and population growth is trending lower, this could create some headwinds for the market.

This may create some challenges for absorbing newly built housing stock, especially those dwellings targeted specifically towards investors.

The US housing market is now getting hit by rising mortgage rates. The average 30-year fixed-rate mortgage already comes with a 5% rate, and 6% beckons as the next target. Read… What Will Surging Mortgage Rates Do to Housing Bubble 2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They will not allow home prices to return to the historical mean (2X median income). In 2001, you could buy a house in Melbourne for $120k. In 1985, a house in Melbourne was $50k, those days will never come back.

Governments are deadset to never allow a correction. The government recently announced to increase the population to 50 million, by increasing immigration, in order to prop up the housing bubble

Theory won’t work – ‘immigrants’ don’t buy houses that are falling in value any more than any other human being. Neither does the speculator who was buying in order to rent to those immigrants.

Governments will only prop up housing markets as long as it’s a net vote winner. That point has long passed.

Buy? Landlords pack 20 people into a room who are used to overcrowding conditions back in their countries. This keeps rentals high, which keeps the housing bubble afloat. The population ponzi relies on an endless stream of immigration to prop up the housing bubble/

According to Fannie Mae’s report, as baby boomers exit their owner-occupied homes there could be a glut of new homes and steep decline in price– returning to historic, pre-globalization levels.

Government Solutions to prevent a return to home affordability includes Mass Immigration, which spurred the dramatic price surge in housing booms 1 and 2.

Adjust immigration policy to create more potential homeowners, to keep hyperinflated prices afloat.

Advocates for this tactic suggest that creating more legal households would increase the number of potential owner-occupants in the market.

https://thinkrealty.com/generational-housing-bubble-forming/

That’s right, blame the immigrants! And there’s nothing about immigrants in the link! Here’s a link with something about immigrants @ 1:30. (Be warned the last several minutes of this video are an infommercial not reflected in the title.)

https://www.youtube.com/watch?v=Hzx7TwpnVg8

I missed the immigration suggestion in the link–which still doesn’t support the claims made. My Bad.

Makes you wonder why?

Why don’t they want affordable housing prices?

Why do they want their children to become debt slaves?

Why make a basic necessity of life so expensive?

Why blow bubble after bubble all fueled by cheap and easy credit/debt and massive government deficits?

A successful bubble ponzi economy cant sustain itself without an endless stream of people, hence immigration/open borders

“Their” children aren’t like “our” children.

Theirs don’t become debt slaves; too many of ours disregard our guidance and become debt slaves.

They say the same thing here in Canada. They’re wrong here too. If governments could prevent bubbles from bursting, they’d never burst. The mighty US government could not prevent a 32% drop in national housing prices a decade ago. Yet Canada and Australia are somehow capable of doing that? I don’t think so.

California is a money laundering operation for china.

even canada relies on this formula

-old person dies or moves out

-1100 sqft crapbox on 5000sqft plot is put on the market for $1.5m

-chinese buy with an all-cash offer ~$100k over ask to take it off the market instantly

-agent does zero work and walks away with a pile of money from commission

-chinese uses home purchase to launder money out of china

-home is rented out to foreigners, h1b or whatever, 10 or 12 of em typically

-h1b is only $70k-90k, but with 10 or 12 of em, the $4000~$8000 rent is reasonable

Once the laundering/immigration/h1b is cracked down on, the $3500~$4000 rent is no longer reasonable. The $1.6m is in no way justified. $1.6m at 3% will make $48k a year, and zero hassles from renters. Also that $1.6 is now going down, the appreciation is over. It was totally worth it when you bought it at $1m and a year later you could dump it for $200k more. Or 2 years later $500k more. But now? eh. Bonds will get you a better rate and carry less risk. Time to bail.

That might have been the case in 2014-2016 but foreign investors now especially Chinese have been blocked from their gov. Capital Outflows are not what they were a few years back. There might be still a lot of money sloshing around in US banks from them, but looks like now the game might revert back to looser standards, etc etc.

My coworker just purchased a home in LA in what used to be called “Black Beverly Hills” with a mortgage rate of 3.2% this summer (2018). So some lenders are still providing that rate for people with good income and credit willing to venture in gentrifying neighborhoods.

Sure the high end will slowdown or even drop slightly, but looks like there’s a real effort into boosting the bottom end of the market. Just a feeling.

Thanks. I’m an old person and I plan to sell my house next year and now I know who to contact –China! I waited until the very bottom of the market in 2010 to pay cash for this 1200 sqft “crapbox” on 9000 sqft lot in Joshua Tree, CA, USA, paying a mere $35K. Before the global collapse in 2008, it had been listed at $168K. Now it’s back up to $160K and climbing. With one BRs in LA, 100 miles west of here, renting for $5000/mo, Angelenos are bailing, driving up prices once again in this cute little artsy town and gateway to a National Park. But this time, it’s not sub-prime mortgages. It’s Chinese buyers in L.A. and San Diego and a bloom of AirBnB speculators driving up prices. It’s not a bubble this time.

I’m an immigrant. I have zero desire to pay $900,000 to purchase a tiny shack in Melbourne. NO WAY. Let me tell you that many immigrants have already gone through a million hoops to get to your country. We know how to wait for opportunity. Some of us waited years. We are happy to come work in your over priced cities, get a six figure salary, rent a nice place, gain work experience, and then leave to find a new job in a more affordable location.

I too was an immigrant to Melbourne, but left Australia after a couple of years, just as soon as I realised that I risked becoming a late entrant into the housing “Ponzi” scheme.

From personal experience I can confirm that “more immigrants” will certainly not help prop up the hugely overvalued housing market.

Not quite so, the West is transitioning towards a globalized housing system, to reach the state of housing in BRICS (Brazil, India, and China). This is the basis of creating and keeping housing bubbles.

Contrary to what naive folks might assume, the really stupendous profits aren’t made in luxury buildings–they’re generated by tightly packed slums. Here’s how it works. Let’s say a middle-class flat of 600 square feet (7.5 square meters) goes for $1 per square foot. The slum’s equivalent 600 sq. ft. has been cut up into numerous cubbyhole rooms, each housing many people who each pay a relatively high fee for the miserable lodging. The rent per square foot in the slum is thus $5/sq. ft.

According to Davis (and this book is heavily, even obsessively footnoted/sourced), densities in Third World slums are astronomical–18,000 residents per acre is not uncommon. That’s four modest-sized 10,000 sq. ft. residential lots in the U.S. suburbs–4 houses that might house 8 people, total, not 18,000.

So slums are immensely profitable–much more profitable than permanent “middle-class” housing. And will you be surprised to learn that most of the property in these mega-city slums is concentrated in a few hands?

The net result of this great urban overcrowding/high-rents/profitability is indeed pernicious.

The Western housing market is in the process of gradual slumification.

Can you tell me the name of the book?

My family were originally from Bangladesh so I know a thing or two about overcrowding haha.

“Planet of Slums” is a brilliant exploration of how globalism turned Western cities into mega-slums.

The West was the last hope, and now globalism has Brazilified our last hope.

https://www.amazon.com/gp/product/1844671607

You mean 18,000 per square kilometre?

18,000 people per acre is implausible.

…

The Australian property bubble is supported by deep economic analysis. You must understand each family analyised the situation and found that house prices are uppy-going things. Case closed. It was a bubble now it is a puddle.

You assume that governments have control over the laws of physics. Sorry, but that’s a false assumption. When the fraud, money-laundering and fiscal/monetary can kicking becomes unsustainable, the bubbles always burst. The U.S. was just one example. Appears Australia and Canada are warming up for a repeat of sorts. Sooner or later the malinvestment is exposed for what it is.

Looks like anyone who purchased a house in the last year is fooked.

Soon to be last 2 years…last 3 years…

At 10x income. With little to no downpayment.

With no more sweet equity…how long until “jingle mail mate!”

Even a flat market is a disaster for “property investors” as nothing is cash flow positive.

And the alligator must be fed every month.

I don’t think Americans understand that mortgages in Australia are for 5 year terms and owners must re-qualify. If prices are dropping while interest rates rise, as they have in the large cities, people will be forced to sell. This will be a downward spiral. Look for the mega landlords, we all know here in America, to scoop down for the kill.

Forced to sell…for less than paid…must bring money to the table… or walk away…but these are full recourse loans…banks will garnish wages and freeze bank accounts…

I see lots of “victims” news reports and reality shows in the future.

I think most people passed over your “mega landlord” reference and it a very important point. Back in the day a home was a home. Governments around the world have monetized the home, incentivized prchasing one by printing money, lowering interest rates and in effect massively inflating the value of homes. In this next downturn the mega landlords will swoop in again and purchase more homesvthereby making it difficult for people to buy a home. We as a country are on the decline, greed has taken over. I know I didn’t express myself fully and i don’t have all the answers. If you have a home good for you, if you don’t tough luck. I know I’m being negative, I just don’t see a way out of this.

Since they know what’s coming, legislating against mega landlords would be a wise step. If they don’t, the winds of populism or worse will blow there as well.

Greed is not a new phenomenon. It is an innate human feature. Even very smart people, e.g. Sir Isaac Newton, get sucked in. Newton went broke after “investing” in the South Seas company/bubble. He actually made some profit on a small investment first but when he saw other people making a fortune, he went all in and lost it.

So cheer up, greed has been with us a long time. You can count on it. With information readily available, you might even be able to profit from it. Just don’t let emotions carry you away.

Not true.

You are talking about special ‘interest only’ loans which may have a 5 year or 10 year term at the end of which the loan becomes due.

Other loans are similar to loans in the USA and have no re-qualification.

One type of loan which you will not find is the common US 30 year fixed loan.

Commonwealth Bank used to offer 15 year fixed loans, but the rate was something like 7.5% when the equivalent ARM was around 4%.

Not True ,Not true

Incorrect on the 5 year loans in Aus, most are 30yr on variable rate.

If you choose to go the Interest only Loan, they are generally from 3 to 5 yrs and REVERT back to then a 30yr type loan, no re applying or reappraisal. 10yrs? never seen one

Virtually no bank will offer a fixed loan at anything over 3-5yrs, THAT is when you will need to renegotiate for an extension-continuation.

My most recent loan was for small investment industrial property ($200k) which I use for myself, was initially investment only and reverted to variable.

Happy that its all paid off now and I have NO desire to get back in, its getting ugly

“There is nothing like a big housing bubble to make everyone look good and bring in the dough.”

You forgot to add and bail them out with tax-payers’ money and skin the savers, prudent people and retirees to the bone or worse (ZIRP/NIRP take your pick) and then crow to the world you have saved the world.

When we start punishing the perpetrators instead of giving them a get-out-of-jail card is when things will change. For that people have to go for the perpetrators and make them pay for their sins.

For how long are the sitting ducks going to remain silent and allow them to milked while the perpetrators get away with murder?

What happens to the ‘interest only’ borrowers?

Wouldn’t you walk away if you could then rent for less than your payment? This would accelerate the decline.

I just did a quick search and 25% of owner occupied homes are interest only and 66% of investor financed homes are interest only. This is a freaking time bomb.

https://www.moneysmart.gov.au/borrowing-and-credit/home-loans/interest-only-mortgages/australias-interest-only-mortgages

I tried to find this out for Canadian mortgages and couldn’t as a percentage. They are mentioned only as an additional but scarcely used product for actual homebuyers (by mortgage brokers), but nowadays usually represented as a ‘secured LOC’ on an existing home already owned. I thought about this and realized I once did this. I bought my current home for cash after securing a $95,000 LOC on my main residence. I then paid off the new property and subsequently sold the main residence. I did this after completing the renovation on new purchase and realized I did not want to rent out either and couldn’t live in two houses at the same time.

The money I made from the house sale was locked into a term deposit so I wouldn’t do anything stupid with it (like buying toys, cars, trips, stocks, etc), and then I used it for collateral to buy some raw land. When the term deposit came due I paid off the interim financing on the property. I lost maybe 1% for the year that needed carrying, but we lose this amount to inflation anyway on savings and meanwhile the land has appreciated quite a bit since buying it.

If we hit a big downturn I would do this again in a heartbeat for the right deal. It is all situational and depends on one’s equity, age, country of residence, etc as to whether it is wise. I guess. :-)

http://www.abc.net.au/news/2018-08-01/interest-only-mortgage-borrowers-flock-to-principal-and-interest/10059960

Sort of explains how they are trying to get out of that interest only corner.

We paid our mortgage with weekly payments (same as bi-weekly). Our 20 year mortgage was gone in 13 years, and we did not make any yearly “contributions” that we were allowed to do if we could.

Question: Is this way of paying mortgages applicable is the U.S., and if so, why might it not be used?

I once had a 15-year mortgage on a condo and made extra principal payments from my bonus money (the rate was 8%). It took me less than 10 years to pay it off. But I’m actually not sure this was a smart move for a variety of reasons (taxes, inflation, etc.)

In the US, You can always make extra principal payments. Each extra principal payment changes the proportion of interest and principal of each payment for the remaining term (lowers the interest and increases the principal portion). So it can save a lot of interest expense.

re: “We paid our mortgage with weekly payments (same as bi-weekly). Our 20 year mortgage was gone in 13 years, and we did not make any yearly “contributions” that we were allowed to do if we could.

Question: Is this way of paying mortgages applicable is the U.S., and if so, why might it not be used?”

Yes. When I owned, my lender would try to tempt me with this offer. Since you paid every two weeks, you made 26 ‘half-payments’ instead of 12 whole-month payments. I never took the offer because I could always throw some extra at the principle if I felt flush (which I never did).

BTW, I sold my ‘bungalow’ in San Jose in March; for once I think I timed something right.

Are mortgages in Australia of the “recourse” or “non-recourse” type? I gotta believe that much of the home price declines in the US were due to the non-recourse type mortgages available in many states, although I could be very wrong on that.

Non-recourse mortgages are available only in 12 states in the US. The remaining 38 states and DC have full recourse mortgages, just like Australia

Here’s the nitty-gritty:

https://wolfstreet.com/2018/06/20/us-style-housing-bust-mortgage-crisis-in-canada-australia-recourse-non-recourse/

1/ Australia doesn’t have jingle mail…..so borrowers are unlikely to leave banks on the hook for anything.

2/ Australia has 2 big cities and 5 country towns…..so borrows tend not to sell because they move interstate for a better job.

3/ Australia only has 2 “high cost cities” eg imagine trying to work out cost of living in the USA if 60% of people lived in LA and NY……

4/ Unless you bought in the last 6 months of the peak…..you are still in the money. eg 15% up in 2017 means down 5% you are still ahead.

5/ We don’t have strippers buying 5 properties (well not as many as the USA) so you wont have a Las Vegas style contagion happening in Australia.

Instead what will happen is as banks increase mortgage rates due to RBA and out of cycle mortgage increases….hard working people will pay down their debt and reduce leverage.

Oh and people wanting a 40% crash so they can “get in to the market” are still going to be whining in 5 years everything is too expensive…..

Dean Collins,

About your first point: “1/ Australia doesn’t have jingle mail…..so borrowers are unlikely to leave banks on the hook for anything.”

See my comment and link above (in reply to Jackk).

There is a big misconception that the mortgage crisis in the US happened because the US has non-recourse loans. But only 12 states have them. Florida is among the 38 states that doesn’t have them, and it was hit harder than most states by defaulting mortgages and foreclosures.

Another misconception was that the lower classes caused the crisis when they defaulted on loans. I recently read a study that shined a light on the real culprits, and it was the flippers and investors class.

As soon as the market turned they defaulted en masse, and thus triggered the crisis.

The study also indicated that the lower classes actually strived to save their homes from being lost.

Anyone with a foreign passport is non recourse. Anyone with morgage lenders insurance (high LTV) is non recourse as they purchased 100% cover for their bank. Anyone with a legal claim due to irresponsible lending practices may also turn out to be non recourse. Anyone who declares bankruptcy is non recourse, which isn’t that bad in aus since we have public health services.

‘Investors still account for 41% of the value of new mortgage demand, according to CoreLogic. ‘

Incredible. Any market that has dug itself in this deep is in for a more violent correction than we usually associate with RE.

A maxim of RE is that it is ‘price sticky’ on the way down, that it declines much slower than the stock market. This is because it usually has a way higher number of owner- occupiers, who can just live there.

With prices falling, and 40 % of the market being investors, we are about to find out how many want to get on an elevator going down.

Isn’t this the saner way to handle a decline in values as opposed to the US bailout before? House prices dropping back to “normal” sounds perfectly “normal” to me. What was abnormal was the unprecedented rise in house values in preceding 5 years.

Are people going to get burned? Yes. Are lenders going to get burned? Yes. But that is exactly what lending is. A game of risk assessment for the creditor and debtor.

It’s all in the stars, a transfer of wealth from the soon-to-be have nots to the haves. Whether it be real estate, stocks or precious metals the end result is always the same. If you are on the side of the haves, you’ve done your homework and are prepared to profit from the careless and naive. Greed, not so much. Opportunists, you bet your sweet a$$.

“being deductible from income tax / negative gearing”

Means that we the common worker / the average Joe on an average income & hard pressed to keep up his mortgage payments – is also paying the negative gearing factor for the property investor.

Australia is in debt.

Australia has borrowed & in the past has repaid borrowed monies with – its natural & other resources.

i.e., iron ore – timber – oil reserves – natural gas reserves – our manufacturing sector, millions of jobs were given over to China in lieu of debt & the pantomime goes on.

Alas – Australia has run out of all these goodies – today our public hospitals ( which have been run into the ground by inept cronie mismanagement ) are being offered up – gas & electricity also.

And I suspect, auditors & overseers are overhauling Australia’s general management of the nations assets to gauge what little Australia can borrow in the near future – i anything at all.

Please know I warmly welcome a correction in atitudes.

The data used PANIC PANIC forgets over , 50 % of Australian houses are owned outright ,prices go up or down does not matter if your mind set is that a house is for shelter, not a get rich method of financial greed.

Bill its closer to 1/3 that are owned outright. Half of owner occupied are outright.

It’s the ones that are mortgaged to 90% with interest only repayments that will decide the future.

Yeah, well, in the US, the mortgage crisis was caused because 10% of homeowners and investors with mortgages defaulted. No one worries about the two-thirds of the homeowners that own their homes outright or have paid down their mortgage to a large extent. They pose near-zero risk. It’s the most vulnerable 10% that caused the financial mayhem in the US.

In 1978 the first ever property in Sydney sold for above $1million. 40 years later the first property has sold for above $100million, and there are over 1 million dwellings valued at over $1million.

Money for nothing.

Tim,

Mike Cannon-Brookes buying the Fairfax estate for $100m in cash is a very very big outlier.

Would have respected you more if you used $20m+ numbers.

This said……to quote Jesse in Breaking Bad “its inflation bitchez” a 7 fold increase from $1m to $32m 40 years later is just normal inflationary returns while Australia insists in living in 2 big cities and 5 country towns.

We need more #Tier2Cities and we need them now.

Until we do we will always be overpaying for property (be it rental or purchase).

There is no chance that RBA will watch from the sidelines if the home prices decline becomes severe and impacts the economy. They will get down to the task of saving Australia and they have a model to follow in the form of Bernanke.

Bailing out is the norm everywhere (e.g. AIG in the US, IL&FS in India ec.). The politicians and central bankers have made “Privatizing profits and Socializing losses” as a way of life. That is till people go for them!

The RBA is a toothless tiger when it comes to setting monetary rates as the banks simply ignore it when it suits them.

If the RBA raises base rates, banks are all in favour and will lift rates in the blink of an eye (if not more) and will simply point the finger as an out

IF the base rate is reduced, banks squell and squirm citing “Cost of overseas borrowing” and never pass on the full rate reduction.

We recently had an announcement from the RBA that they will keep rates on hold for this quarter, but it wouldnt surprise me in the least if bank rates increase tommorow, cause you know “cost of borrowing” or the new gem they use- “Market Volatility”

Its happened too many times in the past.