A distant possibility in early 2018 is making its way to reality.

The markets no longer have any doubts whatsoever that the Fed will raise its target range for the federal funds rate by a quarter point at its September 25-26 meeting to a range between 2.0% and 2.25%. This will be the third hike in 2018. Its probability is now 100% according to CME 30-day fed fund futures prices (chart via Investing.com, red marks added):

As is always the case, the closer the rate-hike date gets, the more confident the market is that there will be a rate-hike – unless some debacle happens.

The debacle that happened in late May – as you can see by the plunge in the probability of a third rate hike from 73% to 33% — was the Italian government bond debacle where bond prices plunged and yields surged. The 2-year Italian yield skyrocketed from the negative to 2.8% in 11 days. By comparison, it took the US two-year Treasury yield five years to accomplish a similar feat, and it still hasn’t moved quite that much, but is getting closer.

As soon as Italian government bonds fell off a cliff, expectations ballooned that the Fed would stop its rate hikes to calm the waters and prop up the markets. But the Fed just shrugged, and by mid-June the target rate probability of a third rate hike in September was in the 80%-range. Now it’s at 100%.

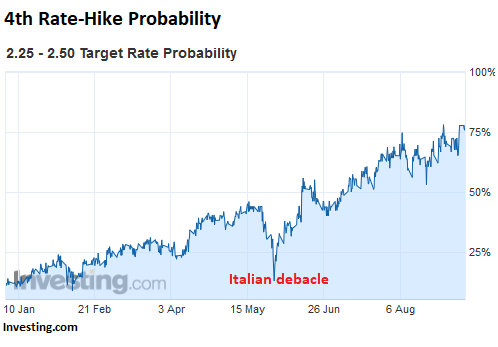

The fourth rate hike showed up on the table in February, at first as mere suggestion. A lot of observers were in the no-way camp. Some were talking about rate cuts, given the stock market declines at the time. But by now the idea of a fourth rate hike in 2018 has taken hold, and the FOMC meeting on December 18-19 is the likely occasion. This hike would raise the target to a range between 2.25% and 2.50%.

The target rate probability of the fourth rate hike rose from around 10% at the beginning of this year to 77.7% today, according to CME 30-day fed fund futures prices (chart via Investing.com):

The federal funds rate is an overnight interest rate – the rate at which banks lend reserve balances to other banks overnight on an uncollateralized basis. The Fed tries to manipulate this rate into its target range with its open market operations (OMOs) by buying or selling securities in the open market. The resulting effective federal funds rate is currently 1.92%.

And what are Treasury yields saying?

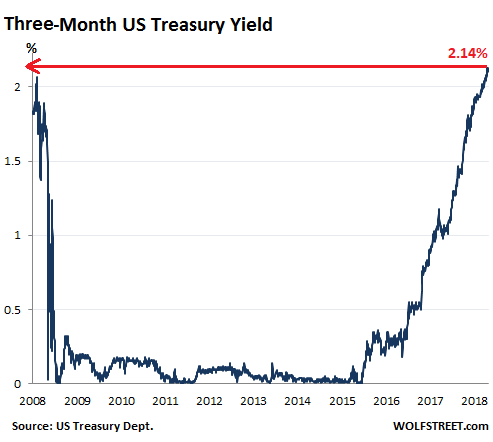

The three-month Treasury yield today (September 10) is still outside the three-month perimeter of the December 18-19 Fed meeting and is not impacted by it. But at 2.14% today, it is mostly pricing in a rate hike at the September meeting, being right in the middle of the Fed’s post-rate hike target range of 2.0% to 2.25%:

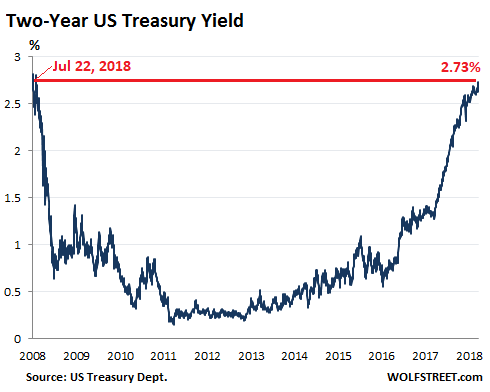

And the two-year yield which closed today at 2.73%, the highest since July 22, 2008, is gradually coming to grips with higher rates beyond 2018:

What seemed like a thin chance for the markets in early 2018 is now getting closer to becoming reality for the markets.

Since late 2016, when the Fed stopped flip-flopping, the Fed has studiously avoided springing surprises on the markets. Everything was telegraphed well in advance. By the time it arrived – rate hikes as well as the QE unwind – the market had already digested it. And this is likely the path forward in 2019.

But for 2019, the Fed has given itself more flexibility for more rate hikes, or differently timed rate hikes, by making all eight Fed meetings “press conference meetings,” not just four of them, as in 2018 and prior years. There has been a market expectation that this Fed would only raise rates at meetings with press conference, of which there have been four per year. But in 2019, all eight meetings will be followed by a press conference and will be “live” meetings. And this might indicate that the Fed doesn’t want the markets to be surprised by a surprise move.

Here’s my math when the Fed’s QE unwind will end. Read… The Fed’s QE Unwind Hits $250 Billion

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not sure how accurate the below site is, but it confirms two more hikes.

-the link requires you allow all cookies,and turn off add blockers! Really annoying, but perhaps useful info.

https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html/

“the link requires you allow all cookies,and turn off add blockers! Really annoying, but perhaps useful info.”

It dosent if you use the correct OS, browser, and approach it, the wright way.

Wolf I gotta ask, how were negative rates legal to start with?

Yeah, negative rates are a form of wealth transfer, similar to theft. But this is done by a central bank, so it’s all hunky-dory.

But is even illegal by a technically. If someone borrows money they owe money not the other way around! What were all the people who are supposed to defend their country from being scammed doing?

Insider trading :)

– 4 rates hikes in 2018 ? What are they smoking ? Is that stuff legal ?

– One rate hike ? Quite possible. Two rate hikes ? Yes, provided that we see a 1st rate hike first.

We already had 2 rate hikes in 2018. 3rd coming in Sep, 4th likely in Dec.

– I’ll re-write that post: If there’re going to be 4 rate hikes then we first have to see a 3rd rate hike. Only then I am willing to entertain the idea of a 4th hike.

– And of course, then the 3 month T-bill rate has to rise MORE before I believe a 4th hike is even possible.

The 3-month already prices in a 3rd rate hike (Sep). The meeting date for the 4th rate hike (Dec 18-19) is more than 3 months away. Securities with a 3-month maturity today will be redeemed before then, and will be gone by then, and are thus not impacted by a Dec rate hike. So they predict NOTHING about December.

I am still wondering at why the “markets” expected the Fed to intervene because of something they had no control over in the first place, such as a spike in Italian bond yields. What were the people at the Eccles Building supposed to do? Stop their already too merciful rate hikes because of something outside of their mandate? This is wishful thinking at best and being spoiled rotten at worst.

I have been also wondering if the Fed won’t perhaps become even more aggressive with their “QE Unwind” and rate hikes after midterm elections. The US economy is starting to show some clear signs of overheating and I think it was Dullard who openly spoke about investigating options to bring the unemployment rate in the 4.5-4.8% range to put a lid on wage inflation.

Accelerating QE unwind would probably be the lowest risk option, but I honestly think the US economy can take 50bps rate hikes with minimal issues these days.

Finally there’s an issue I think we are all painful aware these days: the chief reason why the US economy is starting to feel the heat these days is that capital is pouring back into it record pace. Foreign investors are only part of the story: it’s mostly US capitals coming back home because yields are finally discernible and risks are considerably lower than in EM’s.

The ball is now in the ECB’s camp. The ECB has announced, not exactly enthusiastically, an end to their QE program, albeit they immediately assured they’ll keep hitting interest rates on the head with the biggest mallet they can find in the shed. However the ECB is now also engaged in an arm-wrestling contest with the Italian government, whose crumbling infrastructures and fiscally irresponsible electoral promises require the ECB to keep on buying massive amounts of Italian bonds on top of the present “Stealth QE” already implemented by Italian banks with fresh ECB funding. Take that, National Team!

If monetary policies in the EMU continue the present course, expect the US economy to become an even more attractive haven for investments, thus becoming even more red hot, thus requiring the Fed to look for ways to cool it down somewhat. Nobody likes to get burnt.

If our economy is doing so well, why do we have such huge budget deficits? And why have we needed nine years of “emergency measures” from the Fed?

Maybe this economic “boom” is a sham based on $15 trillion in Fed funny money “stimulus,” a tripling of our public and private debt levels, creative accounting by corporations, and mark-to-fantasy stock and asset valuations.

I’m still laughing hard about “I am still wondering at why the “markets” expected the Fed to intervene because of something they had no control over in the first place, such as a spike in Italian bond yields”.

I thought doing something about “something over which they had no control” was what the Fed did.

Please explain how the US Federal Reserve can influence the yield of euro-denominated bonds issued by the Italian government.

Short of buying said bonds outright (and I know before I go into the grave somebody will start suggesting the Fed buys Mexican securities or the ECB buys Indian bonds; the scary thing is too many people will listen), absolutely nothing.

According to the link below, the 2y yield is 2.73% and the 10y is 2.94%. Both of them near 0% or slightly negative after adjusting for inflation. In what world does this makes any sense? The 10y ought to be around 5%. Is the demand *that* strong?

https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield

Yeah but is not really negative like they did in Europe and other countries. And is actually POSITIVE if you expend those dollars outside the US in place were the value of the US dolar has risen.

So that’s why these rate hikes caused trouble in Argentina and in other countries, because the hikes make dollars too expensive there. Not to mention the fact Argentina has the nasty habit to borrow a lot of money.

So yeah 2018 is the year of green… as long as you use said green outside the US.

Old dog, yes demand is that strong for two reasons: 1) absurd levels of money creation by Central Banks and 2) no real productivity gains in this new world economy….just the opposite…negative productivity. So all this money sloshing around has to find some yield.

The Fed will continue to inch up rates however, all the long rates will stay flat. We’ll have a very flat or slightly inverted yield curve. Don’t let the pundits scare you into some sort of crash sign with this. Not this go around because this is NOT the same economy that those signs/rules were baked under.

So, if I’m understanding, THIS TIME REALLY IS DIFFERENT.

I get the idea behind your comment about ” NOT the same economy that those signs/rules were baked under”, but an inverted yield curve is still an inverted yield curve.

It’s kinda like saying your fluffy cute little lion cub absolutely won’t grow up to eat you.

The inflation rate is around 3% now, but the market believes it will reduce soon. People are betting the U.S. will apply the same playbook as Japan. We’ll see years and years of QE and low inflation. A fixed income investment paying 3% in that environment doesn’t look too bad.

People in LT bonds could lose money if the long rate rises, but they see only a nominal chance of that. The economy has clear limits to growth, especially now that the government fiscal situation has turned dire and must be addressed in the next few years, which will hurt GDP growth.

Plus, more risky investments such as stock have high potential downside, which adds to the attractiveness of treasuries.

Lacy Hunt offers good explanations for the low long-term rates in his quarterly newsletters.

Japanese citizens had deep personal savings accounts that they could draw from to offset the inflation caused by their central bank. This allowed the QE to continue for decades. Most Americans are one or two paychecks away from the street. They will mot be able to stay afloat through decades of Central Bank easing. Noticed a lot of homelessness lately?

I wish I knew what the game plan is. I hope it’s raise interest rates then implode the stock market 80 to 90 percent (which is fair market value) then cut interest rates into the negative category for good. That looks like the game plan to me. The central bankers need some sort of an excuse for not being at the end of a hangman’s noose when they pull the plug on the stock market. I guess their excuse will be crippling interest rates.

I think the game plan is to carefully balance maintaining a small negative real interest rate against the risks of a catastrophic collapse of all the bubbles that have formed due to those negative rates. Let real rates become too negative and the bubbles go exponential. Let real rates go positive and you get another GFC as they all implode.

They’ll probably succeed. However in my opinion, the easy monetary policies and failure to control the financial sector have basically destroyed the incentive system at the heart of capitalism. This is causing a steady decline of the real economy and that is why the cost of living is continuing to climb and even the manipulated inflation figures are now edging up. Force enough doctors out of med school and into finance and you get a whole lot more GDP, but probably not of the type that is actually useful to society.

This has always been the central bankers downfall: They think they have found the leak and become so obsessed with dealing with it, that they don’t realize the boat is on fire and all the passengers are jumping overboard.

“They’ll probably succeed”

They say there’s a first time for everything!

Leader of the Pack.

The Fed is ALWAYS either too late or too early.

They are now tightening and raising rates going into a downturn.

Outside the US the global economy is in a tailspin, that will end in a deflationary depression. One look at global fundamentals will tell you this.

Higher rates have seriously impacted the EM economies and as a result the FX currency credit markets. This is now spreading from the periphery to the core. The current trade shipment bulge in the US system, is sending false signals to the North American markets. While outside the US, global trade has collapsed.

The Fed will lose what little credibility it has left, when it must drastically cut rates and bring on a massive QE program to combat whats coming.

As usual they will be too little, too late. It’s getting close.

Here is the game plan. FED will reduce balance sheet and raise rates without causing a market upset. How? By jaw boning into the crowd that they are doing this because the economy is strong and inflation is where they want it. This is the rape plan of a virgin. Telling her/him this will be good and you will be nice while you are doing it without causing her to upset. When things are are done, guess what? Fed has a balance sheet and higher level rates to cut. Now the market CAN go upset and cry and put on a fight, but the FED has ammos now to neutralize it. They will cut again and they will QE and they will jaw boning.

During this entire process, the FED is in control and the market is a b****.

Got it?

I remember when rate hikes were not announced in advance so basically everyone knows what is going to happen.

Were those the good old days?

I think so because these are not.

Remember when we had honest markets, sound money, and vigilant regulators, enforcers, and policymakers looking out for the public interest?

Neither do I.

Your post made me take the “thousand yard stare into the past”……and I came up with: It was a bit better before the Savings and Loan part of the market got crushed. After that it became a free for all and the “common” person could never trust another banker or their equivalent, the politicians.

LIBOR has also awakened from its slumber, which brings up the issue, if their day to day measure of the cost to borrow has been handcuffed to Fed expectations, what’s driving the global economy and is this rate hike really necessary. Being contrarian if Fed raises will the EU drop their end of the year QE taper?

The EU seems to follow the Fed but who knows.

I see asset bubbles and misallocation of capital in the US, huge debt related to low interest rates, Fed balance sheet of $4 trillion plus and tax cuts for the rich.

Does the Fed see this? Do you?

Does this seem familiar? History rhymes but does not repeat.

The EU seems to follow the Fed but who knows.

I thought LIBOR has lost it’s luster and use. Am I wrong?

Maybe the Fed under Powell sees asset bubbles in almost everything, misallocation of capital, casinoing, debt everywhere in the real world and the true difficulties most Americans have with the eroding of the middle class. After all Powell is not an economist and did not go to the Chicago School of Economics, Harvard and get “fed” the same information.

History rhymes but does not repeat. I wonder if we will have a financial issue again.

Sorry I did mean to post twice. It did not seem to go thru.

The government largely determines its own borrowing cost by dictating the cost of money. The government controls the strength of the dollar and risk on sentiment on Wall Street. The government manipulates the bond market from Treasuries all the way down to the chase for yield in Tesla bonds. But we cannot have universal health care because this is a capitalist country…

They have no choice. They have to load ammo in the magazine before they have to shot again.

Usually the Fed has lowered interest rates by about 500 basis points to fight a recession. This time the’ll probably be lucky to have 300 points to work with.

Life in the Land of Denial.

The NFIB small business optimism index for August just hit an all time high! Everything is just going gangbusters!

The BLS job openings report has hit an all time high! Jobs for everybody! Jobs galore!

The BLS also reports there are 660,000 more job openings, than there are unemployed American’s! Labor market is HOT!

The population must believe all is roses because the BLS also reports, that the job “quit rate” just hit the highest level since the 2001 recession!

Can you say “BLOW OFF TOP”? I knew you could.

BLOW OFF TOP

These stats don’t lie.

http://www.gainspainscapital.com/2018/09/11/9466/

Looks like our billionaire overlords are getting worried that the millions of screwed-over proles who lose their houses, retirement funds, and jobs in the next financial crisis won’t be bending over for the Wall Street-Federal Reserve Looting Syndicate with the same docility they displayed in 2008.

https://www.marketwatch.com/story/the-next-financial-crisis-will-be-more-difficult-to-handle-says-billionaire-investor-dalio-2018-09-11

Gold is trading at multi-month lows. When I checked earlier this morning it was down more than $7 to around $1193 an oz. It has since recovered and is now up $1.60 an oz. I suspect it would be lower if more people believed the Fed was going to follow through on its (supposed) tightening plans, but after so many years of the “Lucy and the football” routine of punting on hikes by Bernanke and Yellen, the Fed’s credibility is still in tatters. Will Powell act like a responsible central banker instead of an adjunct of Goldman Sachs like his predecessors? That remains to be seen.

FED credibility – a poisonous viper commands respect in the same manner.

Greatest economy in the history of mankind according to Trump and the MSM.

6 Rate hikes would seem to be in order