Some beautiful spikes too.

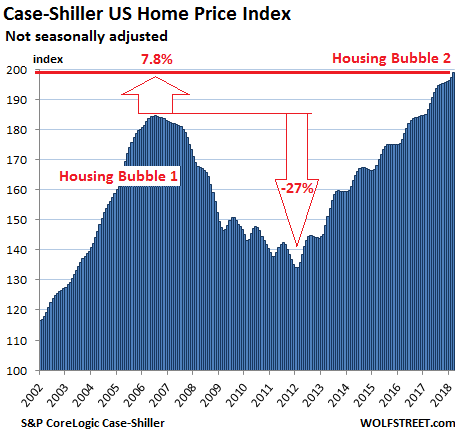

Prices of houses and condos across the US surged 6.5% from a year earlier (not seasonally-adjusted), according to the S&P CoreLogic Case-Shiller National Home Price Index for March, released today. The index is now 7.8% above the crazy peak of “Housing Bubble 1” in July 2006 just before it all came apart, and 48% above the trough of “Housing Bust 1”:

Real estate is local though prices are heavily impacted by national and global factors, including monetary policies and offshore investors who consider “housing” in the US an asset class and perhaps also escape route. These local and global factors inflate local housing bubbles. When enough local housing bubbles come together at the same time, even as some housing markets remain calm, they turn into a national housing bubble. See chart above.

That last housing bubble — “Housing Bubble 1” in this millennium — wasn’t some state of calm that the US needed to return to. It was the definitive housing bubble that then collapsed and helped bring the global financial system to the brink.

The Case-Shiller Index is based on a rolling three-month average; today’s release is for January, February, and March. The index, based on “home price sales pairs,” compares the sales price of a home in the current month to the last transaction of the same home years earlier. The index, which incorporates other factors and uses algorithms to arrive at a data point, was set at 100 for January 2000; so an index value of 200 means prices as figured by the index have doubled.

So here are the most splendid housing bubbles in major metro areas in the US:

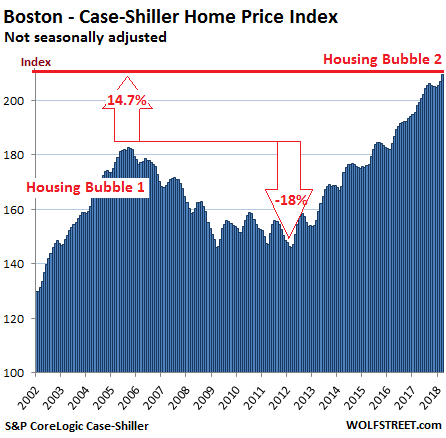

Boston:

The Case-Shiller home price index for the Boston metro jumped 1.2% from the prior month, to a new record, and is up 5.8% from a year ago. Note that little dip in the chart late last year, when prices made a feeble effort at a seasonal decline. During Housing Bubble 1, from January 2000 to October 2005, the index soared 82% before dropping. It now tops that crazy peak by 14.7%:

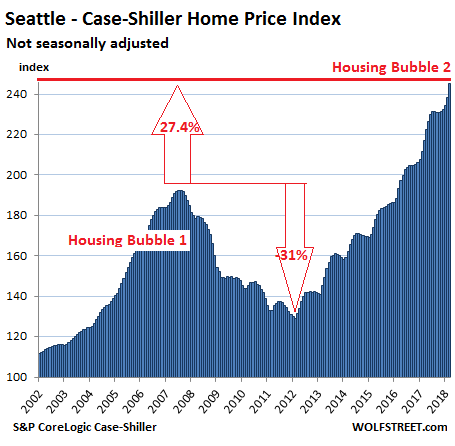

Seattle:

The Seattle metro index spiked 2.8% from the prior month to a new record. Late last year, it had experienced the first monthly declines since the end of 2014, now left behind as seasonal blips. The index soared 13.0% from a year ago and is now 27.4% above the peak of Housing Bubble 1 (July 2007). Note the historic spike over the past two months:

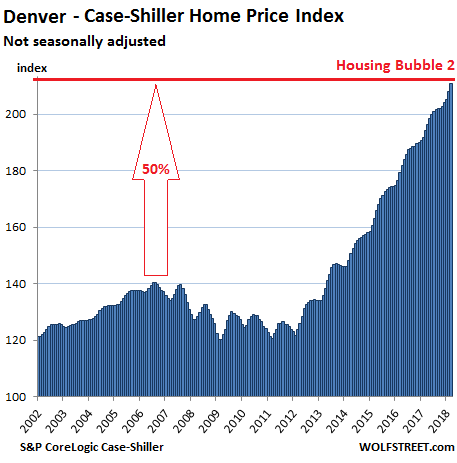

Denver:

The index for the Denver metro spiked 1.4% from prior month, the 29th relentless increase in a row. It’s up 8.6% from a year ago, and is up 53% from the crazy peak in July 2006:

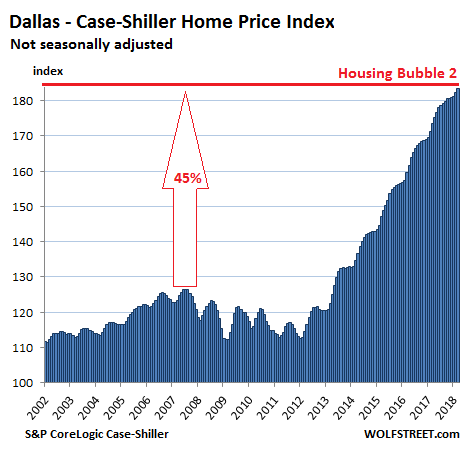

Dallas-Fort Worth:

The Dallas-Fort Worth metro index rose 0.7% from a month earlier, its 50th monthly increase in a row, and 5.8% from a year ago. Since its peak during Housing Bubble 1 in June 2007, the index has surged 45%:

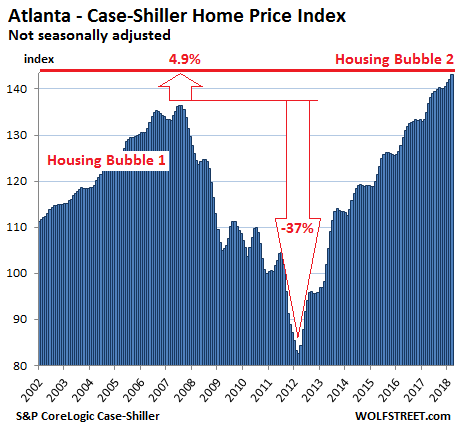

Atlanta:

The Case-Shiller index for the Atlanta metro, after a brief seasonal flat spot late last year, rose 0.8% from a month ago and 6.2% from a year earlier. It now exceeds the peak of Housing Bubble 1 in July 2007 by 4.9%:

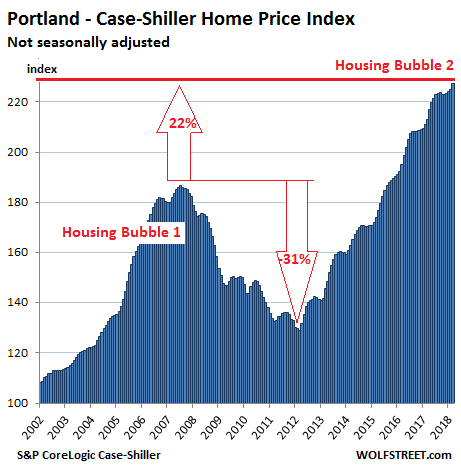

Portland:

The Portland metro index, which had been flat for five months last year, has now risen four months in a row. The index is up 1% from a month ago, 6.7% from a year earlier, and 22% from the peak of Housing Bubble 1 in July 2007. It has ballooned 127% since 2000:

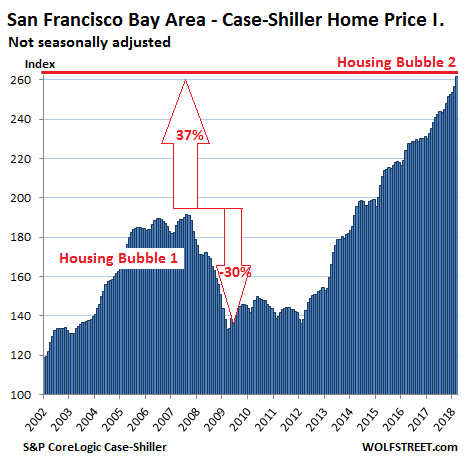

San Francisco Bay Area:

The Case-Shiller home price index for “San Francisco” includes the counties of San Francisco, Alameda, Contra Costa, Marin, and San Mateo, a large and diverse area consisting of the city of San Francisco, the northern part of Silicon Valley (San Mateo county), part of the East Bay and part of the North Bay. The index spiked 2.1% from a month earlier and 11.3% from a year ago. It’s up 37% from the totally crazy peak of Housing Bubble 1, and 162% since 2000:

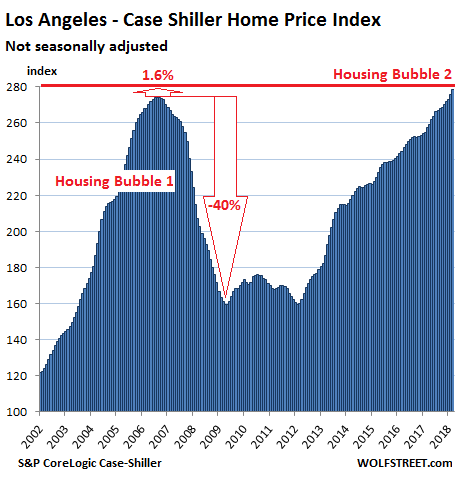

Los Angeles:

The Case-Shiller index for the Los Angeles metro rose nearly 1% for the month and 8.1% year-over-year. Between January 2000 and July 2006, the index had skyrocketed 174%. The crash was nearly as steep, as the chart below shows. The index now exceeds the peak of the housing insanity in 2006 by 1.6%. So a big round of applause. The Case-Shiller data for neighboring San Diego is very similar.

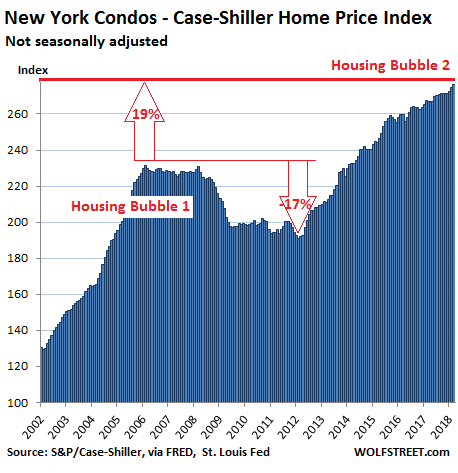

New York City Condos:

Case-Shiller’s index for condos in New York City rose nearly 0.6% from a month ago and is up 3.4% from a year ago. From 2000 to February 2006, the index had surged 131%. But even during the subsequent bust, its decline was halted when QE kicked in, and along with it the bonuses on Wall Street. Then global investors arrived again, and by 2012, it was once again party time. The index is now 19% above the peak of Housing Bubble 1, having surged 176% in 17 years:

The acceleration in many markets of this home price inflation might well be a reaction to mortgage interest rates that have surged and are scheduled to surge more, as the Fed continues to raise rates “gradually” and as it continues to unwind QE. So households may be rushing to lock in the current rates – and thereby also locking into their own budgets the current prices of Housing Bubble 2.

Here’s the impact of higher mortgage rates on home buyers in dollars and cents. Read… What Will Surging Mortgage Rates Do to Housing Bubble 2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Los Angeles and “neighboring San Diego”? They’re 120 miles apart, with 3.2 million people in Orange Co. in between. :-)))

Perhaps they’re neighbors from the perspective a commute between the two is relatively short?

I’m in Van Nuys, about 10 miles north of LAX. North Orange County starts 40 miles south, but it often takes 2 hours to make the drive (sometimes it’s only 70 min though, like late Sunday).

Carlsbad in North San Diego is 110 miles south, but the drive is over 3 hours typically.

It’s really too far to commute – many people live in one and work in another, but they either stay in hotels (like the field guys in construction) or they rent rooms to sleep in near work and head home on the weekends.

If they have their own houses, it’s typically east – like Hemet, Menifee, or sometimes Palmdale (that’s getting pricy though), and if they go south like me it’s typically to a parent’s house or a home otherwise purchased pre-bubble. It is too far to feasibly commute from LA to San Diego for a daily job though.

check out the 49th congressional district. the only thing that separates LA from SD is Camp Pendleton, otherwise it would be one continuous city.

And Orange county

As you mentioned in your previous post, RE has a more or less fixed limit up in the monthly mortgage payment. (and with decreased interest deductability, limited high income State tax deductability and increasing interest rates) that number is going down.

Sure wont’ buy anything in that environment. I’ve been waiting 3 years now. Still waiting.

does seem like a lead weight, don’t it?

as to buy vs. rent numbers, they don’t matter when the phone doesn’t ring for your rental.

buy choosy.

Strong employment numbers seem to be causing the rise of housing costs in these markets. Travel outside of the commuting radius to these cities and the housing prices are probably flat as the suburban housing demand isn’t as strong due to less job mobility.

There is actually less jobs than ten years ago thanks to bots (AI) and robots (machines) taking jobs. Is just that most companies no longer allow working from home so people prefer to live closer to their workplace.

Even if fuel prices are still kind of cheap no one who can avoid it likes to travel long distances to work.

My understanding is that bots and machines taking jobs is a small effect in the last couple decades, though that may change.

The major change has been the simple shipment of said jobs to low wage countries. Great for execs and investors! Bad for the U.S. Midwest, which had a big part of the manufacturing base and so the most to lose, also to the South and Texas, though mainly overseas, if you consider all industries.

Are there really strong employment numbers? I know a lot of people with 2-3 (and 4 in a couple of cases) part time jobs, just to make ends meet because no one hires full-time any more on the lower-end. These are basically double-triple counted jobs, so it artificially makes the jobs number look good.

I know a lot of people on the higher end, who hate working in the current ‘drone-hive system’ of employment in the USA [per Jim Kunstler!] so much that they prefer to stay unemployed. These folks also artificially make the unemployment numbers look good.

Except for a handful of sectors, I think it’s a pretty crappy job environment out there.

For the 90%, I think the feeling is, no matter how hard you work, you won’t get ahead, you’ll only die tired and worn out. So don’t do any more than what it necessary.

How do you measure a reasonable commute? A lot of people are commuting 3 hours 100 miles each way! Reno-SF, Bakersfield-LA, Spokane-Seattle, Pocono-NY.

You must mean Tacoma or Olympia because Spokane is 300 miles from Seattle.

Really enjoy the monthy standard aticles. Was just reading a main stream Yahoo article “The US housing market has an inventory problem” which backed it up with .. “Inventory shortages are even worse than in recent years, and home prices keep climbing..” but I still agree their is an affordabilty issue. However, I always think, who is driving cost up, if their is an affordabilty crisis.

https://www.zillow.com/homes/orange-county_rb/

zillow, almost 7,000 homes listed for sale. I think the “low inventory” meme is really code for low inventory that anyone can afford. I know I can’t afford a $600K “starter home”…….and I just noticed, there’s almost 10,000 homes for rent.

Los Angeles country is 18,000 for sale, for rent 19,000…some of this must include apartments i suspect.

Hope springs eternal!

A couple of things come to mind that are different this time. First, while Wolf is correct that the existing housing stock didn’t get any larger (though may have been remodeled by a flipper), it’s safe to say that in all these HB2 cities there is a larger population today — and thus demand — for these existing houses. New unit construction has seriously lagged behind, especially in land-constrained urban areas. Yet the people keep coming. So the prices continue to rise, enabled at least in part by still historically low mortgage rates.

The second major difference is that in the run up to HB1 pretty much anyone would could fog a mirror would qualify for the most obscene, toxic mortgage product. We all know how well that worked out. Since the collapse though it has been notoriously difficult to qualify for a mortgage. The end result being that those who hold mortgages today are on a much sounder financial footing. Barring some financial cataclysm we shouldn’t expect to see the massive wave of defaults we saw 10 – 12 years ago.

“larger population today”. How much bigger? This needs to be quantified. Also in some cases this would mean that people are leaving behind houses. So we should see the value for those houses dropping, possibly causing losses for banks.

“Since the collapse though it has been notoriously difficult to qualify for a mortgage.” I believe it’s true, but at the same time, people in areas like Silicon Valley are pledging the value of their stocks to get mortgages. Imagine what would happen when the value of those stocks were to drop.

We are in an everything bubble i.e. one bubble is inflating another bubble, etc. So if one pops, the contagion will be scary.

“The Dallas-Fort Worth-Arlington metropolitan area’s 146,000-resident jump in 2017 was the most of any metro area in the United States. And six of the top 10 fastest-growing counties in the United States were also in Texas, including Tarrant, Dallas, Denton and Collin.“

Add in the aversion to allowing new apartment complexes in most cities in the area and you are creating a lot of demand for housing.

However, you can still buy a brand new house for $200k.

As a Dallas resident I see nothing but bubble … wages are flat despite the jump in population .. my brother’s condo of a ‘whopping’ 895 sq ft sold for $189k in 3 days … … it was the cheapest property for sale in the area. I’ve seen this movie before in Portland OR and Seattle

Melbourne is growing at around 100,000+ people a year.

However, foreign purchases of RE has fallen off a cliff as a result of government policies both in Australia and China.

“The number of approvals for residential purchases fell by 67 per cent last financial year, according to the Foreign Investment Review Board Annual Report 2016-17, released on Tuesday.

The sharp turnaround in foreign real estate investment follows last year’s state and federal government reforms in which steeper charges on foreign purchases, less favourable tax treatment and a cap on new development sales were introduced.”

SEE:

https://www.domain.com.au/news/foreign-buyers-of-australian-real-estate-plummet-foreign-investment-review-board-figures-show-20180529-h10ogr/?utm_campaign=featured-masthead&utm_source=smh&utm_medium=link

However, the impact appears to be mainly in the condo/unit/apartment market and a few high priced areas that have had heavy foreign buying.

So far my little area of Oz has seen very little impact in single family homes. Several properties that are being marketed for townhouse conversion are still on the market though.

I think this is a result of several large townhouse/apartment projects in the A$1 million area that are currently under development or are being marketed.

A house went on the market last week and it is already under contract. Just unreal.

The price range was A$1.25 – $1.3 million. Another wait and see to find out the price.

I’ve been looking 2 years, starting price for a new low end home in Collin and Denton is 240k to 300k not counting the closing costs. Housing for a starter home is not affordable. And 2 bedroom apartments or 3 bedroom homes for rent are running 1900 to 2400 per month. The choice is shorter commute and higher house/rental price or long expensive commute to have an affordable home/rental.

Banks don’t lose. Taxpayers lose.

Your second point is spot on BradK. Mortgages are much harder to get today, especially for investment homes. Almost all lenders want at least 20% cash equity compared to zero equity 12 years ago. If you have skin in the game, there’s a lot more incentive to continue to pay your mortgage even if values decline a bit.

Also, 12 years ago home prices in all submarkets increased substantially between 2003 and 2006. I reside in Naples, FL. The price for homes in my neighborhood surpassed the 2006 peak levels in 2015 and have traded slightly lower since 2015. Most owners have no or minimal debt. Home prices in an adjacent neighborhood(just to the east) are still at 60% of peak prices because of the difficulty in obtaining mortgages.

How is the market in Marco Island going?

Any impact from the last big storm?

Fannie and Freddie now guarantee 97% LTV mortgage loans, house price increases are outpacing wage growth, and there is more debt in other categories competing for income than during Housing Bubble 1.0. That is in addition to all of the so-called “investors” who will try to rush the exits when prices plateau. Those are all signs to me that this bubble may be in an even more precarious position than Bubble 1.0 was in July ’06.

No Brad K . What with multiple mortgages on a single property , the proliferation of ‘ dark money ‘ loans , loans for down payments etc , loans to make up the shortfall between the appraised value and the ( much ) higher price the own is willing to sell for , shady back door private equity mortgage companies abounding handing out subprime loans like candy etc – et al – ad nauseam .

Qualifying for a mortgage in todays bubble markets is as easy as pudding and pie … if you know the right doors to open and tables to crawl under

I think situations like these probably only exist if some of the lenders do not record some of liens on the property. If that’s true then these lenders are putting their business in peril. After what we went through in the late 2000s I would hope no lenders are that stupid enough to let that happen.

About the only lender is the GSEs. The banks do not want to loan money at artificially low interest rates.

Behind the $Greens$ Door ??

.. could be a movie ..

This may be a dumb question, but is this adjusted for inflation?

In some sense that is a dumb question. Housing prices rising *is* inflation.

More seriously: The *official* Case-Shiller index is *not* inflation adjusted, nor should it be. Adjusting housing prices for “inflation” is misleading. It makes not more sense than to adjust a milk price index for inflation.

Asset inflation is as bad as is consumables inflation.

True.

However, as I mentioned here a few days ago, I think it would be reasonable to adjust the index by median household income growth (which can be “gamed” a lot less than CPI). Between 2006 and 2018 median household income has grown by nearly 30%.

Adjusting with that metric we are definitely not back to the same highes as 2006.

I don’t know what you’re talking about but most incomes have gone no where since 2000. I know mine hasn’t nor has anyone I know gotten a 30% raise since 2006…..the only wage earners i can think of with a decent pay increase are min. wage drones.

https://www.advisorperspectives.com/dshort/updates/2017/09/19/u-s-household-incomes-a-50-year-perspective

2nd chart

Interesting: The chart you attached is inflation-adjusted incomes. It is not relevant in this context.

I am talking about nominal incomes, which is what you’d need to use in order to adjust against a nominal index like the Case-Shiller. Nominal median household income is up almost 30% since 2006. If it wasn’t then the line in the chart you referenced would have been sloping downwards, not flat as it is.

You could also adjust by CPI but it is more prone to various statistical “adjustments” than income measures.

Interesting: The FED and Gov have gone and redefined nominal median income in 2014, and now they are dictating to us that our nominal income have increased. I like 20 people right here comment whether their income have gone down or up since 2006, and I say at least 20 people since some people might have the incentive to post fake numbers.

Just like you, all my coworkers around me and that’s quite a high number of coworkers, tell me they are far worse than they were compared to 2000. But hey, who needs reality when you have the gov telling you that you are getting paid more. The only group that I can think of whose wage has increased are people who earned minimum wage since minimum wage has increased in many states.

Changing definitions of inflation, median income, corporate review have become normal. It’s like you are a loser in a game, and you just arbitrary change the rules of the game, and suddenly declare yourself the winner.

Oops, I mean corporate revenue.

R2D2: I am not sure what “redefinition” you speak of but even if you use actual rather than computed measures, like for example income figures from the IRS and the SSA they also show average as well as median incomes being up about 30% between 2006 and 2018 in nominal terms.

https://www.ssa.gov/oact/cola/central.html

Max Power,

I don’t care what my charts or your charts are saying all I know is nobody around me makes near enough to buy a home and the only people I know getting home inherited it.

And the final thought on incomes is, a massive increase at the very very bottom (on a % basis going for $8 to $9 to $10 in the last 3 years is huge) coupled with the people at the very very top getting massive increases as well must skew the numbers for the median higher…..cause I ain’t seeing it nor is any people I know.

I agree with ‘interesting’ 100%. I know no one that is making much more than they were 10 years ago (or more) and most are LESS economically secure than they have been in their entire lives. Ppl making $10/hr here in Dallas are NOT doing well even IF full time. Rent is too high unless one goes to a drug infested slum. I have observed the same thing in Seattle, Portland Oregon and the cities in the high desert north of LA. In Dallas I don’t see ANY medium or lower cost homes being built at all … just apartments and high end cookie cutter shit.

Those income numbers are based on actual tax revenues. There are no adjustments or hedonics or other suspect adjustments. And remember, for tax purposes, people’s incentive is to report as low as possible income and yet it’s still up 30% in 12 years. Now your own personal situation may be different is but it is incontrovertible that NOMINAL incomes are up.

Of course, inflation is up too at the same time and therefore a lot of people feel like they are stuck where they have been for many years, and rightfully so. Those are real incomes, which have definitely been flat. But again, we’re talking nominal incomes in the context of the Case Shiller, not real incomes. Every measure of median or average nominal income, be it using actual income numbers or various estimates shows it up about 30% since 2006. That is a fact. Yes, it doesn’t FEEL like it’s up becuase it is nominal but don’t confuse feelings and facts.

Max Power: We are all talking about nominal income; other than minimum wage earners very few make more just in dollar term (nominal) now compare to 2000, and back then a one bedroom apartment in Bay area was $600, and now it is $1800. Interesting already explained why the median income numbers might show a higher number. Everyone is saying they earn less, and you are the only one who keeps saying we make more. OK, we get it, you make more; good for you.

Ant Naples,

For another perspective than Justme’s, I think that housing prices should always be inflation adjusted because the official US inflation rates and housing price changes are not always in sync. Those differences have potential investment value that can be revealed in modeling. Case Shiller is not adjusted and you will need to do that yourself if you are interested.

However, it is worth stressing that Justme is correct when it comes to how purchasing a home “feels”. Inflation adjusted numbers are pointless for that metric.

@Wolf,

This may sound a bit outlandish. I was looking through the sales of some homes here in Bay Area recently and I noticed that there are offers on homes which are rejected. I was curious if there’s a front running/shilling operation afoot here. After the front running shenanigans of the likes of Goldman, one is sure to wonder.

For example, if a certain organization, say the Fed or somebody else, wanted the home prices to be high.

One way to do so is to get a fake offers into running as soon as a home comes on the market. The fake offer has to be one that is imperfect enough to be rejected. The actual customer will then have to match this new bid and this will ensure the home prices stay high even when the demand is low. We keep hearing about how these homes are not affordable, yet people are clamoring for them. I know people who are buying some of these homes and most of them report how they had competiton and how they outbid the competition. Yet, the so called competition seems very week and not interested in pursuing or countering the bids. Could these first bidders be somebody with a fixed price point in their minds? I doubt that because the first bids are also above the asking price.

I don’t think this is the case here on a large scale. I know quite a few people in real estate here, and that’s not what they’re seeing.

Friend just bought a house she was the lowest bid, but they accepted her because she had a big down payment. They don’t crunch the numbers until after the bidding and if the buyer can’t raise the money the process starts all over again. Also marginal buyers treat offers like an option to buy and ask for 90 day escrows, (sellers counter with less) in order to see if the value of the property has gone up. Then they scramble to pull the deal off. House in my area sold six months ago above asking price and no one living in it. Lots of folks playing fast and loose.

Take a look at the map tool on zillow.com and set it to show the pre-foreclosure listings, indicated by blue dots. If you have an account on Zillow, it will show the date when the owner defaulted on the loan. There are quite a few in my local area, and many in San Francisco. I am not sure what the trend is in defaulted mortgages, but there is probably a lot more shadow inventory than what is currently listed for sale. With costs of housing absorbing more income, there will be a lower hurdle to jump for a recession to cause a surge in defaults.

It’s fascinating to look at this! There’s one house valued at 5 million with a past due amount of $800,000. I guess you have a lot of folks pretending to be rich.

I wonder what percent of these homes will transition to “foreclosed”.

Also, does anyone know what this map looked like roughly one year ago? Has the pre-foreclosure rate gone up since interest rates increased?

And everyone keeps telling us that it’s different this time. This is another bubble no if ands or buts about it. Only when it pops will we see what shenanigans were going on.

The thing is, are those who shouldn’t going to get bailed out……again.

I’ve speculated for a while that there are a good many ppl living in their homes on borrowed time…I.e., overly leveraged and just moving debt around to make ends meet. When and if the hamster wheel stops without an exit plan…look out.

I don’t have a sense of whether the trend in foreclosures is going up or down but I don’t sense that many of these “pre foreclosure” houses are necessarily new problems. We have a house across the street from us that would have shown as “pre-foreclosure” for something like 7-8 years (before we moved into the neighborhood from another one in San Francisco).

You can look up a lot of historical information on the city’s web site to see some of the things that have happened.

It is very, very difficult to get someone evicted in San Francisco if the people living or owning a property are savvy and know how to use the system to their advantage.

As far as I can tell, this house hasn’t paid their mortgage in 7 years and the owner has been renting it out to 3 or more unrelated parties at a time. It was supposedly up for foreclosure auction again a few months back (for at least the 3rd time) but didn’t seem to get foreclosed.

The house has weeds for a lawn, people parking rusting cars on the weed patch and lots of safety violations according to inspectors who were called on the house, probably by tenants. (It has multiple reports for things like bare electrical wires hanging from the ceiling, abundant mold, broken pipes).

We’ve seen lots of weird events surrounding the house with a woman moving out with a large moving truck in the street at 2 AM, people playing with RC cars and flying drones around the dense neighborhood in the middle of the night and other bizarro stuff.

I feel bad for some of the tenants living there since they’re living in a craphole and seem to be living on the edge. Maybe they’re getting a better deal on rent which the owner pockets without paying the mortgage or doing maintenance. That’s what it seems like, anyway.

I don’t think this one has avoided foreclosure for lack of the bank trying or some strategy to hold the asset on the bank’s part. The payment problems started after the last financial crisis and records indicate the bank has tried foreclosure several times and it still seems owned by the same people.

This! This right here!!! Excellent observations. The government and RE organizations and big companies paying inflated wages can all scream as loud as they want that everything is fine but the quality of the system doesn’t seem to improve with more quantity.

How much is the rise if you take the dollar of 2006 being more valuable than the current dollar? Doesn’t it end actually lower than the previous bubble?

What you’re looking at with this data is asset-price inflation, mostly. The same home requires a lot more dollars to be purchased. This means that the dollar loses its purchasing power for assets such as homes. A home stays the same size and just gets older. It loses real value unless something drastic changes in the area, such as the construction of a new subway station nearby, or major gentrification.

Some of the latter has been happening in some areas. But mostly, these price increases are related to the dollar losing its purchasing power versus assets.

I have to add that scarcity & restrictions are huge factors, even more important than affordability. In cities like SF, beach cities generally, there are no empty lots available. And some cities won’t allow an increase in the house size (Del Mar, CA is an example, above ground or below!). So, with size and usage restrictions – zoning that disallows changes – and residents who want more not less exclusivity, the price can only go up. Until of course it goes down.

Hi Wolf, that was my thinking as well. If so, is it fair to call it a housing bubble at all? Is the many 1000’s percentage rise in the Venezuelan stock market a bubble? US housing and equities may yet prove to be a superior investment to cash, even if neither gives a positive return on an inflation-adjusted basis. Is this crazy thinking?

While north of the border, Canadian housing values seem to have flat lined and are now slowly rolling over lower.

Household debt hit $2.13 trillion, adding almost $3 billion in April. Total increase from last year is $99 billion, an increase of just over 4.9%.

Mortgage debt accounts for $1.528 trillion, while consumer debt is very close to a record high at $604 billion.

Even though the pace of mortgage debt growth, both short term and annual, is now the lowest it’s been since 2001.

The average consumer is consuming, just not housing. TIMBER!

Stats: BofC report.

Depends on where? Certainly over priced markets like TO are declining (for many reasons), but where I live on the west coast house prices are marching ever onward and upward. I live about 1/2 way up Vancouver Island, but it is thought of as being the north Island. Campbell River is a 45 minute drive east and home values there have increased this past year percentage-wise more than any other locality according to a local RE rag. A crap postage size building lot in CR is now over $200,000, then add on fees and permits + $300/sq ft construction costs at a minimum and you have an expensive market for new home buyers. A result is that people are surging into our area driving up prices.

Maybe an economic crash will adjust things downward but our mild climate still attracts people in droves. Today a cold front is sweeping through giving us 35 kt westerlies, clear skies, and perfect short sleeve temps. I have 40-60 humminbirds at any given time trying to nudge/budge into the feeders. Eagles and swallows are circling over the river and there are no bugs to worry about. We don’t even need window screens. The only people selling seem to be folks who have health concerns and wish to relocate closer to the hospital.

The south west coast is an anomaly.

What we have driving it is the tip of the baby boom demographic.

This population segment is down sizing while liquidating assets, then moving to their retirement dream location and buying real estate.

@Wolf Richter

Why don’t you use the seasonally-adjusted data?

Seasonally adjusted data are only as good as the seasonal adjustments. They’re one more layer of data manipulation, pure and simple.

Even Robert Shiller himself said years ago that he isn’t happy with the seasonal adjustments of the Case-Shiller data.

The ONLY TIME EVER that seasonally adjusted data should be even glanced at is for short-term month-to-month changes. And even then, they’re only as good as the seasonal adjustments. If the adjustments are off, the results are off.

But here we have a rolling three-month average. And we look mostly at year-over-year comparisons and long-term comparisons. There is no need for seasonally adjusted data if we compare the current period to the same period a year ago.

Our smart readers see from the charts that there is some seasonality in housing data, and that this seasonality disappeared over the span of 2014-2016 in some markets, and that some of it has returned in 2017. By adjusting the data, you’d never see that. But you would see other fluctuations that have to do with the adjustments, and not the data.

does Case Shiller index track property taxes too.

i would love to see what happens to property taxes tracked too.

No it doesn’t. But that would be a good one.

Subprime borrowers with shoddy credit get most of the blame for blowing up Housing Bubble 1.0, but research by the NBER shows that it was caused primarily by middle and upper-income prime borrowers used for “flipping” houses. Subprime borrowers did indeed have “skin in the game” in that they were borrowing for homes to live in, not speculate on.

http://www.nber.org/digest/aug15/w21261.html

There was an article in the Denver Post not too long ago about how more people may be considering leaving Denver than relocating there and cited housing prices as “a reason.”

A more accurate assessment would be that the cost of living is a major reason, if not THE reason, for the Denver-Boulder area being on the verge of a net outflow of people.

Yes it’s true that Denver has a remarkably low unemployment rate; however, the cheerleaders conveniently omit the fact that most of the jobs do not pay enough to keep up with the ever increasing prices of housing and rents.

The official line is that Denver is going through “growing pains”, as if this is something that will pass. I’ll believe it’s “growing pains when the gap between income and cost of living balances out, or at least improves from what it is right now. Unless that happens, and there is no guarantee that it will, the “growing pains” line is complete nonsense, if not an outright lie.

There was another article recently suggesting that Denver housing prices will stay on the same trajectory thru 2018 and 2019. If that’s the case, I can almost guarantee you that net in-migration will reach zero by 2020. More and more, Denver simply isn’t a good value for many people trying to make a living here.

Watch for a shift in Denver’s rental market as the rent-slaves bail, and the property owners have a harder time finding tenants at their asking price. At that point, I think we’ll see lots of lower-tier properties come on the market as it will be more tempting for landlords to cash out.

Desirable single-family homes purchased by well-heeled out-of-staters will probably retain their value, but condos and townhouses will likely be another story.

Regarding your point about housing prices continuing to rise for at least another couple of years, I’ve heard something similar. It could be true–anything is possible at this point.

As for your point about the rental market, I think there are number of variables in determining whether a landlord continues to rent or sells. A key one is probably whether they bought in cash versus took out a mortgage. For fairly obvious reasons, a landlord who bought their rental property in cash is a lot better positioned to take a hit than one who is paying a mortgage–I suspect those paying mortgages will be more likely to sell than those who paid in cash.

If there is a correction, I don’t think it will be because people suddenly stop buying homes. The more likely scenario is that it will be precipitated by a recession.

While Denver is not as bad as San Francisco–at least not yet–I suspect there are more than a few people in the Denver area who own homes but leveraged themselves to the hilt to be able to do so. Thus if they lose their job or end up underwater on a mortgage they will likely sell.

We received an e-mail a couple weeks ago from a local real estate agent entitled “4 Reasons Why Today’s Housing Market is NOT 2006 All Over Again.” It was complete with data from sources such as the National Association of Realtors and the Fed.

Surest sign of a bubble to me.

Did it say “Whatever it takes” in small print at the bottom of page?

I have a friend in the foreclosed RE business. She’s one busy lady, what with the housing market being in its current state. Think the laws of physics — what goes up must come down — and you have the idea.

On a related note, I arrived at the coworking space this morn, only to find a business card tucked under my keyboard. It was a well worn card (not a good look) and the owner of said card is a CRE guy specializing in SoCal properties. Not the sort of thing I’d be interested in investing in, but I take this as a sign of a market peak.

If they’re saying “there has never been a better time to buy” … run for your life! Lol

Here is a TRUE story, my parents former house in Miami, FL got flipped 2 in less than 2 years – Originally sold $191K on Oct 2014 (Short Sale) then flipped in June 2015 $329K, then not satisfied sold again in June 2017 for $360K that is 3 sales in less than 3 years.

For sure this plays into the rhetoric of a HOT market but I think it is just flippers generation 1/2 the actual volume, once the TOP is IN the flipping will stop and the volume should decline

Miami without doubt has the bubbuliest housing market in the Southeast.

Here in Calif, Toll Bros is offering buyers of their new homes 3 year fixed rate loans at very attractive rates like 2.75% to 3.25%. Generally these are $1Mil + size loans. when the loans reset to market in a few years, they will have a massive payment shock. Could even cause some to default. These are not subprime loans just subreal interest rates.

A family friend worked for the Toll Brothers in eastern PA. While he was in their employ, he coined this slogan:

Toll Brothers Homes: Guaranteed for Five Years. Then They Fall Apart.

My mother still gets a big kick out of that one.

One or two commentators said that the job situation in the San Francisco Bay Area has a lot to do with the upward march of house prices. But the reality is that at these prices, tech workers can not afford a house in the Bay Area. So where is the demand coming from?

There is a very large number of vacant condos here in San Francisco. Nearly all high-end (many of them over $1.2 million). And they’re not exactly selling like hotcakes either, with many of them getting prices reduced after a while, or getting pulled off the market for a while.

Not surprised at the condos, I think there is something to be said about owning the land. Let’s face it, if you tear down the condo, you really don’t have much rights after that. Look at the Millennium Tower, if that building goes away today, each of those occupant might literally own a couple of square feet of that lot. Which is worth a whole heck of a lot less than the fixture that got put on top of the land. That would be true for condos everywhere.

There seems to be a lot of mystery regarding who is actually buying these houses. One possibility is that we’ve started to see a great transfer of wealth between the Boomer generation (or even the Boomers’ parents) and younger generations. I was recently at an open house in the affluent North Berkeley area, and I overheard a woman saying she was buying a house for her kids and needed a cottage for her and her husband to stay at. I think there’s a fair amount of successful older parents giving early inheritances to their grown children. So that tech person with a decent salary may be able to get 70% of the way, but the generous parents allow them to seal the deal.

Thank you for the insight. I believe that is a part of the puzzle. But I would like to see some hard numbers. Even paragon’s news and analysis doesn’t really say,

https://www.paragon-re.com/trend/san-francisco-home-prices-market-trends-news

San Francisco’s home sales seem to be in decline, fewer properties are selling but the prices continue to climb. AKA, the housing crisis, in the bay area (source: SF Chronicle). So, who is buying? Is it the Bommers, the tech workers, a combination of the two, the Chinese, the Canadians, Warren Buffet?

A relative sold their house on mercer island a suburb of Seattle , iin 2014 for 1.4 million. Then in less than a year resold off market for 1.8 million

Last asssesment one year later 2.4 million

So In less than four years a one million bump….. nice

A friends house sold in late 2016 for 1.6 million and is now at 2.2 million in a bit more than 18 months

Who has the dough??

Here on the Olympic peninsula houses are being snatched up in 2to 5 days

Nuts…. must be all the cash outs fleeing

Ca and Seattle

Wow! That is a juice bubble! Are those new and used home prices? But look at the housing builders they all topped out in January along with the building suppliers. The bubble is already deflating ..the markets way ahead of these maniacs bidding up housing prices. The whole market is rotting. A crash or a decay appears all the same when Santa Claus comes down the chimney!

These are “sales pairs,” so the same property sold twice over time. By definition, these are existing homes, and new homes are not included.

Jobs report looks pretty rosey. More rate hikes are now assured.

From my neck of the woods, Sillycon Valley, this was on local news last night:

https://www.mercurynews.com/2018/05/28/sunnyvales-most-expensive-single-parcel-home-sale-yet-guess-how-much/amp/

“The record-breaking sale comes less than three months after a smaller home in Sunnyvale’s Cherry Chase neighborhood sold for the highest price per square foot recorded in the city — a whopping $2,358 — in a $2 million sale. Local real estate agents say both sales are further evidence that the city, traditionally lacking the prestige of neighbors like Menlo Park or Palo Alto, is becoming more desirable — and more expensive.

…

The city, nestled between Mountain View and Santa Clara and within easy commuting distance of Google, Apple and other tech companies, has seen the average sale price for a single-family home increase by nearly 50 percent since 2015 — rising to more than $2 million this year, according to MLSListings. The city itself also is becoming a hot spot for tech, with Facebook and Fortinet recently securing leases in Sunnyvale.

Even so, Sunnyvale remains more affordable than neighboring cities including Mountain View, where the average home sells for $2.4 million, Palo Alto, where the average home sells for $4 million and Menlo Park, where the average home sells for $3 million, according to MLSListings.

…

The $3.15 million sale closed May 16 for about 25 percent above the home’s asking price after spending eight days on the market, Moran said. The buyers, a husband and wife who both work in tech and have two high school-aged children, had been searching for a home in the Sunnyvale area for more than two years, Moran said. The family, who declined to be interviewed, previously lived in Santa Clara and wanted a bigger house in a better school district.

…

The home fetched such a high price partly because it includes an enormous, 12,800-square-foot lot, Moran said. The big backyard was part of what sold her clients on the property.”

Re. that last bit, my sister and brother-in-law (since divorced and moved away) bought a similar-sized lot and home in higly desirable Los Altos circa 2000 for around $1 million – I’m sure it would easily fetch more than triple that now. My rent (shared 2br/2ba ~900 ft^20) has nearly doubled since the downturn during the GFC, it will likely hit $4000/mo when we get our next annual rent-jacking, erm I mean lease renewal notice next month. Being semi-retired w/no kids (i.e. ‘great schools’ means diddly to me) I’m getting the hell out of here – looking to move to the North Bay at end of August, hope to find something less-egregiously priced in San Rafael, Novato or Petaluma or thereabouts. Any tips from Marin countyers reading this appreciated!

Just used Zillow to check my sis and her ex’s ex-lot size, it’s ~10,000 ft^2, and Zillow estimates $4M current valuation.

I thought you were supposed to move all the way north to Oregon. So the us locals can then complain about being overrun by Californians… :)

“….because it includes an enormous, 12,800-square-foot lot,”

Must be an old fart – that is just over 1/4 acre – not enormous to me at all!!

“Large” in a city is well over 1 acre…………………

Enormous ???

If you’re talking acres around the valley, you better be one of the eighty plus Billionaires that live around here, or at least centa-millionaire. Especially in the neighborhoods that are being mentioned.

I’m surprised though that no thought was given to moving out to places like San Rafael, or Livermore, or such, those should be still reasonably priced for rent.

As for the schools around Sunnyvale and Cupertino, in reality, they are no better than the schools in other parts of the bay area. The biggest difference is the Asian parents that are pushing their kids, this is one of the reason why Kumon and their counterparts does such great business in and around the Asian communities. This in turn drives the test scores and a whole host of other things, including desirability for those neighborhoods. It’s interesting also because the pressure cooker these schools have become generally means that non-Asian kids are gradually forced out. Just take a look at the top performing schools in Cupertino (Lynbrook and Monta Vista), their demographics look even more skewed than schools in Hawaii where the predominant ethnicity are Asian.

EWMayer, drop me a line.

I’m a Broker Associate who works out of Santa Rosa, you can find me via the CA DRE ( I don’t want to post my contact info here).

Briefly, we’re seeing lots more inventory above $1MM and prices just beginning to soften across the board.

More price reductions, more days on market and more inventory…it won’t show in the numbers for a few more months, but it’s clear to those who follow the market daily.

You’ll save a nice dollar by waiting until next spring.

Take a look at the number of apartments for rent in South Bay on Craigslist (https://sfbay.craigslist.org/search/sby/apa); 5000 just in South Bay; and multiply this by at least 4 since each building has multiple apartments vacant, but they advertise only one apartment. I say 4 since some of the postings might be repeated posting, and some maybe ordinary houses for rent; otherwise, I would have said multiply by 5. There are so many vacant apartments; there is no shortage; they just make it look like shortage. I recently moved to Sunnyvale, and the rental company didn’t even do a credit check on me. They were just happy that someone would take one of their vacant apartments.

So, the real estate prices are not justified at all and sooner or later will crash hard.

In my experience, price to rent ratio is a critical data point. It won’t ever stay skewed in either direction indefinitely. Right now in many cities, monthly cost to own is still less than renting. I suspect this is a strong driver of purchase decisions, especially for young people with decent jobs. As irrational as humans can be, most of us, most of the time, don’t make personally disadvantageous decisions for very long.

Also in the suburban area I live in, houses in fairly good condition in top school zones are “hot” with big price gains probably driving up metro averages. Less premium areas are only showing moderate appreciation. Undesirable houses (needing tons of work, bad layout, etc. ) sit on the market with price cuts. All of that is just like you would expect in a balanced market. This was not true during the 2006 peak, when every standing structure sold like a winning lottery ticket.

Over time, rent tends to be much more stable than house prices. That’s probably one of the reasons the BLS uses rent as a measure of housing inflation (rather than house values) in the computation of the CPI.

It should all work out just fine till it doesn’t.

Just like Italian bonds that is the subject of Wolf’s next article: https://wolfstreet.com/2018/05/29/nirps-revenge-italian-bonds-plunge-worst-day-in-decades/

It should all work out just fine till it doesn’t.

Lots of foreign Chinese buyers still. It could be a visa holder in the US or even a citizen that is Chinese, and LLC’s can be used, but a lot of money coming from China. There are no really good stats to understand how many properties are being bought by Chinese out there because it can be hidden. My guess it is substantial.

Seattle, and CA cities heavily affected by Chinese buyers.

Unfortunate that the local people who just want to buy a home they can afford to raise their families have to compete with so many foreign buyers.

Saw a no down payment adveristement in the swamp metro area today.

I just got an email of a report from Zillow on market conditions for a zip code I have been following. I’m in Plano, which is just north of Dallas. Plano has cheaper houses than Dallas, but it has been exploding lately due to Toyota and a bunch of other companies moving here.

In spite of that, they say that the Plano market is cooling off, and it is a buyer’s market.

https://www.zillow.com/Plano-TX-75024/home-values/

You cannot buy a house in Far North Dallas for less than $400K. I sold mine in 2009 for $300K, it would now be $400. Dallas rentals are way overpriced right now.

$414k is the average value. That means all those new job must be in the 70k to 120k range?

Rule of thumb is to not spend more than 3x salary for a house. Lol

The 3x metric is not as applicable for the high end areas or with super low mortgage rates. Not saying things aren’t overpriced… just that 3x is really more like 4x or 5x once salary gets high enough.

I had heard from long time Dallas residents that all those McMansions in frisco is because of the toyota plant … so if Plano is / was bustling because of Toyota and frisco has gone beserk from all this so called Toyota influx … how many really are because I just don’t believe the hype. I heard the exact same crap when I lived in Oregon in 2000 and housing prices were escalating to the stratosphere

JD been here for 30 years, the Far-north (Plano, Frisco, Prosper, Denton) area is going insane. Ranch land that had herds on them just six months to a year ago are exploding in houses. I drive by these new divisions every morning and the signs Start at the UPPER 290’s or 400’s (Hollyhock) on 380. It not just Toyota, in the years between 2012 and 2015 friends of mine in Little Elm and Frisco were turning away foreign investors that were going through their neighborhoods knocking on doors and offering cash for their houses. Then these investors would either leave the homes vacant or turn them into rentals. They rarely would live in them. It’s crazy here…. the locals can’t afford a home and those that do have a home, know if they sold, they won’t be able to qualify for a newer inflated home cost.

So true…

Comment sections of articles on real estate should be read with a pinch of salt since articles on real estate generally attract many real estate agents; and obviously it is the nature of real estate agents to sell you property and justify the high prices.

Friend is selling her house. Lots of offers…but the all want her to carry the deed. Hmmmm.

They probably do not have enough for a down payment to aualify even though I do see some 3.5% down promotion s.

I have heard that RE agents are asking sellers whether they will carry the deed.

I suppose with prices in the stratosphere, people can’t afford a down payment or qualify for a loan?

Why would someone carry a deed? A better price?

Lots of reasons:

1. Maybe a tax angle from the seller

2. The seller gets a better return on their money than they can get if they accept cash.

3. If the buyer defaults they still have the property, the down payment, and any payments to date.

4. Cheaper for the buyer than going through a bank – less fees and maybe a cheaper interest rate.

5. Timing considerations for both the buyer and seller.

I was considering buying another condo in Hawaii at one time and the seller was a Canadian couple that was willing to go that route.

I didn’t buy the property and that was one of the biggest mistakes I ever made.

Lee, You make an excellent point.

Hi Wolf,

Great articles BTW.

I live in Folsom CA and wanted to share my perspective on the housing bubble. I grew up in the bay area, owned a home and moved to Folsom over 10 years ago. I had to sell my house in Folsom in Jan 2017 due to a Divorce ( Possibly the worst time to sell a home but hey my wife left me and wanted her share LOL) and as such I am now 55 years old and looking to get back into the local housing market.

I keep hearing that ” The current economy is strong and Jobs are up” but practically I don’t see it. I think the claims substantiating increasing the interest rate is a house of cards. There must be a spin happening.

What I mean is I am an engineer living in Folsom.

The max mortgage I can afford is 3K$ per month, but at my age, given my post-divorce rape financial situation, if I do buy a house I would like it to appreciate some. But in the current market everything is at max price so why buy other than helping with taxes but even that benefit is comparable to maxing out my 401K. So there is really little to no investment incentive.

Don’t get me wrong I make good money but I am aware of the local job market because my company has had a few layoffs over the past couple of years and as a result I am aware of the struggle of former colleges had seeking work in the greater Sacramento area. Bottom line, from what I see locally there are few companies, if any in Sacramento county that pay enough to afford a 500K home at 5% interest. But yet houses priced at 550-650K are currently selling like hotcakes.

That said, let me compare to the bay area. In the bay one can quit their job, walk across the street and get another job making similar pay within a week. Even contractor jobs pay well and are so plentiful you could still reliably make payments on the same 500K home at 5% interest. Even though its expensive, it is somewhat sustainable because of the local pay. This is most likely true in NYC, LA & Seattle as well but I also bet there are outlying communities like Sac in the same situation.

Now back the to the economy, as you know better that I the last boom ( Bubble 1 LMAO ) was caused by shady loans. So people ended up with loans they could not pay and bam foreclosure etc.

In contrast, the current situation ( Bubble 2) the loans are solid but because the high interest rates payment are extremely high.

So based on my backyard financial analysis, let’s compare both situations, the reason people lost their homes in Bubble1 is because they could not afford to pay the monthly loan amounts. So I do not see how the same won’t happen in Bubble2 as people are paying extreme amounts!! In both scenarios, excessive payments are the bottom line for the payer, regardless of how the loan originated.

For example, I know I make decent money and paying 3K per month is tough but possible for me. But when I see homes selling fast for 600-650 more, I envision 3500 – 4Kper month payments. That is crazy even for us “overpaid, liberal” Californians especially in Sacramento. Then I think what would happen if someone get sick or lost a job?

So I expect to see some loan defaults along the way. I agree this is not 2008 again but either way it seems when people are spending their entire take home from one paycheck for pay their mortgage something has got to give.

Am I wrong?! Cuz I’m just a 5%’er looking at the feasibility and it does not even feel right. Would you do it?

I thought I’d to add to the fodder as housing has been on my mind ever since I qualified for a home loan a month ago. I look forward to any feedback.

Those who stand to gain are like “yeah jump in now cuz its going to get worse…” but it still doesn’t feel right to me.

Like I said something has got to give, it’s a gut feeling.

I say we take a chapter out of Spinal Tap, raise the interest rate to “11” and see what happens.

Best regards,

Bruce

Real estate agent last month in Sammamish, a hot selling eastside suburb of Seattle said that the Chinese buyers are not showing up. My brother sold his house there in five days but said he felt lucky it didn’t take longer due to the lack of foreign buyers. I live in the outer Seattle area and have been reading that the Chinese have moved on to less expensive markets such as Arizona and Texas

The Texas angle has been confirmed by several people I know in Texas and by quite a few commenters here.

It’s not just in major cities either.. I was in Portland, Maine, (grew up there as a kid), for 2 weeks in May and was shocked to see prices approaching what I had left behind in Seattle. Munjoy Hill was a lower income area that was affordable back in the day is now being completely made over into yuppie havens for those who have yuppie jobs. The lament from the locals was exactly what I heard from Seattle working class. Just who is paying these prices and where is the money coming from?. I have no idea.