The magnificent house price bubble wheezes.

By Steve Saretsky, Vancouver, Canada, Vancity Condo Guide:

With 2017 mortgage pre-approvals having now expired, the first wave of buyers facing OSFI’s ground breaking mortgage regulations are being put to the test. The regulations, also known as B-20, require all borrowers to pass a stress test at an interest rate 2% higher than the qualifying rate.

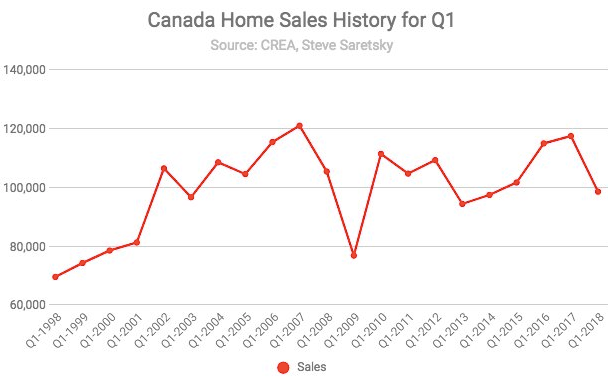

Early symptoms appear rather obvious. National home sales slid for the month of March, falling 23% year over year, and pushing the average sales price down 10%. Overall, it was a bearish quarter for Canadian housing, first quarter sales fell 16% year over year.

Much of the declines were felt in the single family housing market in Vancouver & Toronto, with many buyers unable to qualify at the recently inflated prices. The average sales price of a single family home in Greater Vancouver now sits at C$1.6 million and C$1 million in the Greater Toronto Area (GTA).

Chief economist of the Canadian Real Estate Association, Gregory Klump, noted the squeeze as “tighter mortgage lending rules, which make it harder for home buyers to qualify for uninsured mortgages, are also shrinking the pool of qualified buyers for higher-priced homes.”

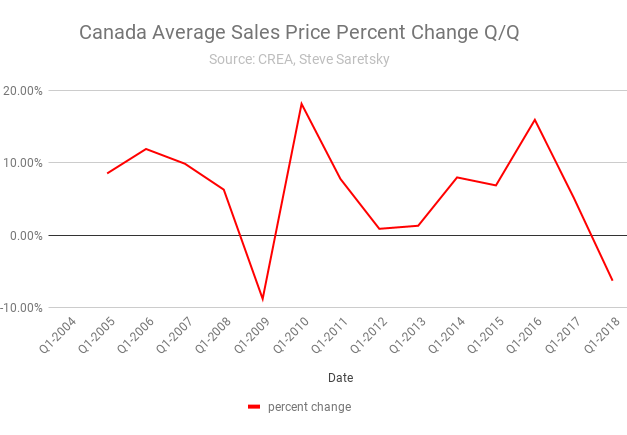

To little surprise this reflected in the national home prices across Canada. The Q1 2018 average sales price declined by 6.27% from Q1 2017. It was the first year-over-year percentage decline since Q1 2009.

The impact of the mortgage stress could become more apparent moving forward, particularly if borrowing rates continue to rise. As of today, a homebuyer hoping to purchase the typical home in Greater Vancouver (as per the MLS benchmark price of C$1.084M) would require a minimum down-payment of C$216,800 and a verified income of C$175,000, assuming a 5-year mortgage at a generous 2.99% interest rate.

Is it any wonder prices of one bedroom condos continue to rise? The median price in Greater Vancouver hit a record high of $540,000 in March.

“Given their limited supply, the shift of demand into lower price segments is causing those sale prices to climb,” said CREA’s Gregory Klump. “As a result, ‘affordably priced’ homes are becoming less affordable while mortgage financing for higher priced homes remains out of reach of many aspiring move-up home buyers.” By Steve Saretsky, Vancity Condo Guide

Big Six Banks’ out-of-control “Mobile Mortgage Specialists” on commission. Read… Government of Canada Just Pointed Out Mortgage Market Might Be a Cesspool

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am sure some Canadian RE agents are now trotting out the following lines:

1. It’s now a bargain guys.

2. Buy the dip.

The only question is how big of a loss will it need to be for the banks to take notice?

Loses so far seem to be from private lenders.

Larger banks can either foreclose on your home or use government mortgage insurance to cover their loses.

We haven’t hit the point where the bank needs to foreclose on a home, but can’t easily sell the property for the price they need to make themselves whole again.

Another ‘line’ I heard was ‘buy now before prices collapse’.

Haha what does that even mean?

It means you are going to miss out on the fantastic opportunity to lose a crapton of money! Aren’t you worried about that?

Do you mean sell before prices collapse?

Borrowing money for anything sucks. We saved our beaver nickels and paid cash, took years but I’ll die in my own bed. Less the gov’t rent of course.

Housing and government (deficit) spending are the only things keeping the Canadian economy afloat outside of commodities. The powers that be are going to do what they can to water down federal and provincial regulation designed to deflate the housing bubble.

Housing is a commodity

Want the real scoop on prices go to zolo.ca West Vancouver with the highest priced real estate in Canada and highest per capita income. Detached homes sales down 60% and prices down almost 25%. Real estate boards, agents, and local news are not giving anyone the real info here as it’s the only economy we have in Vancouver.

Wolf, could you please report on the property tax level increases in yo in Canadaur next article. It seems the government is a passive actor in the property scam

I can offer a couple of observations.

The biggest scams are several: the Land Transfer Tax, which used to be a nominal amount, a few thousand at most. Now it can run to 40 – 50K. And permits and levies can run the same amount or more. On new construction, add 13% of the selling price for Federal and Provincial harmonized sales tax (but not on resales). Add it up for a Metro Toronto new house and it’s approaching 200K. So what used to be the price of a house not that long ago is just the price of taxes.

Municipal taxes are less onerous, maybe 0.4% of valuation is a guideline, for Toronto based on market value assessment, and the increase is spread over 5 years in Ontario. So for a million dollar property in downtown Toronto, 4000 a year.

Similar to the lower rent categories in SF as written in a previous article. When the high end becomes unaffordable, people move into the lower end, pushing up prices, (pun intended). This is a good news and bad news article. The good news is that prices are falling in Vancouver and Toronto. The bad news is a scared buying public still thinks they have to jump in.

Of course these two huge markets affect/skew averages which is very misleading when applied across the country. It is masking reality when conclusions are made by using broad/averaged stats to explain too many categories. Canada is the 2nd largest country in the world. Its various RE markets are unrelated and disconnected from each other other than attracting RE refugees. Take my area of residence as an example, northern Vancouver Island. Lately, houses have been selling here within a few days. Just 5 years ago a house in our valley could be on the market for a few years before a buyer might venture an offer. Prices have also climbed by 20-30% just this past year. Of course one can buy a view home for 20% of what it would cost in Vancouver. :-) It’s all driven by affordability, spilling forth from the unaffordable markets of Victoria and Vancouver.

re: Canada is the 2nd largest country in the world.

Is Siberia the 1st?

It’s amazing the Canadian government even have taken these steps. You would expect them to be like the rest of the world and let the bubble grow bigger and bigger. I guess the bubble was so huge that it scared them; not like the brave government in US who is still pumping the bubble to become larger and larger.

Governments always fight the last war, and make laws for the last crime.

The market was at the exhaustion point anyway.

The numbers in Canada seem small if compared to USA, EU or Japan but you have to remember the size of the population. In Canada the numbers are growing beyond what the population can afford to recover from. The fear is that the 2 largest populations in the country are about to collapse. With close to 36 million people in the country, having the GVA and GTA put 8 million people at risk of a housing crisis is dangerous. 1/4 of the population is in the middle of the bubble, while Paulo(sorry bud) is out in La La Land saying it doesn’t exist if he doesn’t see it.

I am not sure what will happen when it becomes obvious that the housing bubble was propping up the economy, and the air has just left the balloon.

Three things to remember about CANADA and Bankers:

1. Canadian banks already have TARP built in

2. Canada is a recourse loan nation

3. Most Canadian loans are adjustable and most can be adjusted in the next three years

2-scary!

I’m all for more coverage of the Canadian housing market, and glad to see Steve posting here, but can we please leave reporting on ‘average’ prices to the financially illiterate mainstream media?

This is a metric that conflates two different things: mix of sales by property type and house prices (on like for like basis). Better to report the two separately.

I’d expect that some of the gains in the condo/townhouse market will create equity for move up buyers, but the bigger question is interest rates. I don’t think we’ve fully seen the impact yet from the rate increases that have already happened, we’ll see if there are any more rate increases to come.

There is no perfect measure for housing prices. For example, the median price is heavily impacted by a shift in mix. So more people switching to cheaper homes (such as condos) lowers the median price even though the actual price of each unit may not change (this is not a problem with average price).

The shift in mix was a big problem in expensive cities in the US during the housing bust. For example, here in San Francisco, the wealthy refused to sell their homes if they couldn’t get the price they wanted and just hung on to them. But at the lower end, there was forced selling. So as overall sales volume dropped, the homes that did sell were at the lower end of the market which pushed down the median price a lot more than actual prices for individual homes.

To get around this, Canada has “benchmark” prices and the Teranet prices (sales pairs) in addition to average prices. In the US, we use mostly median prices and the Case-Shiller index (sales pairs and algos). But none of them are perfect. And it’s good to know the weaknesses of each.

Some Guy,

BTW, I just ran across the chart linked below that shows the median price, the average price, and the spread between them for Miami. This is a fairly typical way of looking at a housing market, from both a median and an average perspective, because each shows different elements. The spread is important because it shows how sales might be skewed.

This is for Miami, as an example. But the same applies to all housing markets:

http://www.millersamuel.com/charts/miami-percent-spread-between-medianaverage-sales-price/?goal=0_69c077008e-732f136292-120757181

So don’t disparage “average” prices. They have their place!

Not convinced (I think we should just use benchmark or repeat sales indices), but appreciate the detailed response.

“But…but…it’s different here!” (Variant: “It’s different this time!”)

The refrain (soon to be lament) of every Canadian FB (F***ed Borrower) who took out massive loans to buy into yet another central bank-blown housing bubble.

It’s gonna be epic Keep your powder dry folks