Happily dreaming in La-la-land till the rude awakening.

The Fed’s efforts to raise interest rates across the spectrum have borne fruit only in limited fashion. In the Treasury market, yields of longer-dated securities have not risen as sharply (prices fall when yields rise) as they have with Treasuries of shorter maturities.

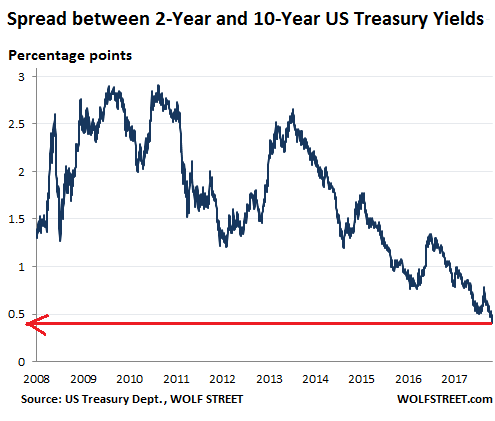

The two-year yield has surged to 2.41% on Tuesday, the highest since July 2008. But the 10-year yield, at 2.82%, while double from two years ago, is only back where it had been in 2014. So the difference (the “spread”) between the two has narrowed to just 0.41 percentage points, the narrowest since before the Financial Crisis:

This disconnect is typical during the earlier stages of the rate-hike cycle because the Fed, through its market operations, targets the federal funds rate. Short-term Treasury yields follow with some will of their own. But the long end doesn’t rise at the same pace, or doesn’t rise at all because there is a lot of demand for these securities at those yields.

Investors are “fighting the Fed”— doing the opposite of what the Fed wants them to do – and the difference between the shorter and longer maturities dwindles, and it dwindles, and it causes a lot of gray hairs, and it dwindles further, until it stops making sense to investors and they open their eyes and get out of the chase, and suddenly long-term yield surge higher, as bond prices drop sharply. That’s why short sellers have taken record positions against the 10-year Treasury recently: they’re waiting for yields to spike to the next level.

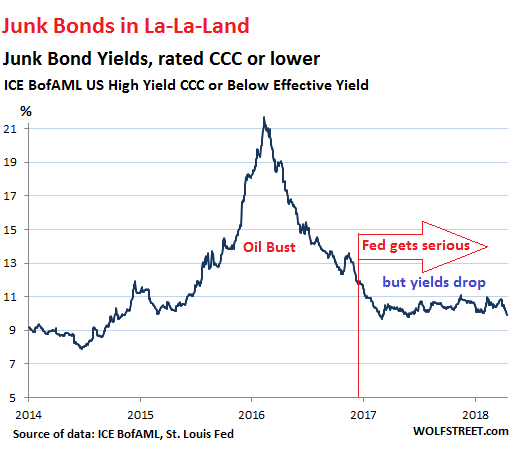

But this disconnect – this symptom of investors fighting the Fed – in the Treasury market is mild compared to the disconnect in the junk bond market. There, investors have completely blown off the Fed. At least in the Treasury market, 10-year yields have risen since the Fed started getting serious about rate increases in December 2016. In the junk bond market, yields have since fallen.

In other words, despite the Fed’s tightening, the junk bond bubble has gotten bigger. And investors are not yet showing any signs of second thoughts.

At the riskiest end, the average yield of junk bonds rated CCC or lower dropped two percentage points since the Fed got serious about tightening, from 11.9% in December 2016 to 9.9% currently (per ICE BofAML US High Yield CCC or Below Effective Yield index):

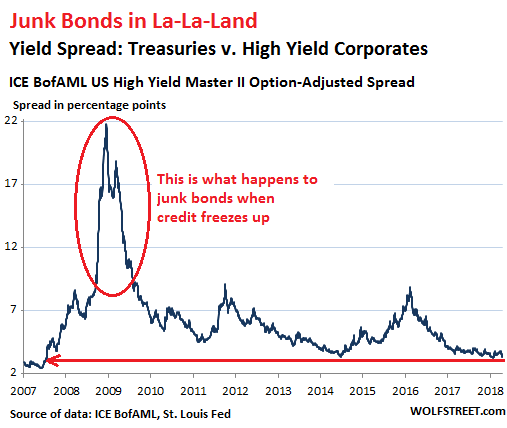

The difference in yield between junk bonds (high risk) and Treasury securities (low risk) is how much investors insist on getting paid for taking more risks. When the spread narrows – hence, when the “risk premium” shrinks – investors are chasing yield and are taking ever larger risks for ever smaller amounts in compensation.

And the spread between the broad junk-bond index and equivalent Treasury yields has narrowed to 3.33 percentage points. Beyond the brief dip on January 26 (to a spread of 3.23 points), it’s the narrowest spread since the la-la days in July 2007 before the Financial Crisis put an end to it (ICE BofAML US High Yield Master II Option-Adjusted Spread via St. Louis Fed):

These days, investors are so eager to chase yield that they’re engaging in huge risks with little extra compensation. This is precisely one of the conditions in the financial markets that the Fed is targeting with its tightening policies. It wants yield spreads to widen. It wants risk premiums to grow. It wants long-term Treasury yields to rise, and it wants junk bond yields of equivalent maturities to rise faster than Treasury yields.

All this means is that the Fed wants bond prices to head south.

Eventually, the Fed wins. And when it does, junk bond yields have a tendency to blow out as the companies that issued those bonds suddenly get caught in a credit squeeze and have trouble servicing that debt. The last two charts above show how far and how suddenly junk bond yields can blow out, as bond prices collapse: during the Financial Crisis and during the oil bust – and that was just an oil bust for crying out loud, and not even a recession.

But not yet. For now, the market is in total denial and happily chasing yield and taking on more risks. And for the Fed, it’s a sign that its tightening job has really just begun.

Short-term interest rates have surged. But are banks paying their depositors these rates? Well, they do offer higher rates, but not to their own clients. Read… Why Aren’t Big Banks Paying Higher Interest Rates on Deposits though Rates Have Surged?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The access to “cheap money” which has infused the market has allowed not only zombie companies like Netflix and Tesla (junk bond issuer) to endlessly issue debt, but also to squander opportunities for actually profitable enterprises to proliferate.

Taking this a step forward desperate pension funds continue to plow into anything that has yielded gains or appreciation. Heck, the Eurobond market doesn’t even beat inflation.

What I want to know what will be the outcome of this Junk bond insanity?

The outcome is know.

Bubble crashes and company sinkings.

The questions are not “how” and “why” but “when” and “who”.

So far it seems 2019 as the year were it will be literally impossible to ignore the FED rising rates but who knows? Could happen earlier.

The latest number on negative yielding debt globally: $8.3 trillion (mostly in euro bonds and yen bonds), according to Bloomberg.

While this is down from the peak $10+ trillion, it is still huge, and investors in those areas are scrambling for alternatives. That global interest in higher-yielding instruments in the US is part of the reason the 10-year and 30-year Treasury yields are still so low, and why junk bonds continue to rally.

So would you say the Fed is pushing on a string? HYG has started to rally back to its highs, and yield instruments only seem to rally on days when the stock market is up. As you say the size of the market (even in negative yielding bonds) is creating inertia, ROW bond market is simply too large to lay off in new US 10yrs. There might be a lesson here for those who believe in the mass reallocation of investment capital into gold through ETFs. Such a move would dilute the value of the paper relative to a finite resource.

Paper money always loses value in the middle and long term.

What the FED is doing is trying to raise the dollar value short term.

But is going slow because there is still a lot of “super low interest rates” debt circulating around.

As cheap debt gets paid and or replaced by more costly debt, the market won’t be able to keep ignoring the FED.

Do remember the FED is also raising rates at baby steps and telling everyone who cares to listen months in advance that’s is going to do so.

Why are companies like Uber, Tesla, Netflix and so on still able to sell junk debt as if it was two years ago? Because there is the expectation that those companies are still gonna last a few years more.

What people fail to realise that a slow sink, like Yahoo did, is the exception to the rule, not the norm.

Uber, Tesla and Netfix have competitors that are already eating a part of the cake and that will quickly eat more of it once these companies full of debt go under.

The spread between the 2 y Treasury and Bund is at all time highs @2.98

Since the Feds actions both on raising rates and letting maturing bonds run off is exclusively focused on the front end,foreign buying will dominate the longer term Treasuries.If the foreign central banks ever stop supporting the long end ,the convexity of longer term bonds in all countries will result in massive losses throughout the world.That will in turn be the catylst for the worst junk bond route in history and one of the worst stock market routes

Why? At least their money is,safe

Wolf,

I disagree with your premise: “It (the Fed) wants yield spreads to widen. It wants risk premiums to grow. It wants long-term Treasury yields to rise, and it wants junk bond yields of equivalent maturities to rise faster than Treasury yields.”

All of that is the old model of how things worked. We are in a new, peverted economic system. And surely the Fed knows this. Essentially, there is way too much “money” chasing way too little gains.

The money level is high in part becasue of QE but also because the Fed had been inflating the money system for years as productivity stalled; however, inflation stayed benign because of wage suppression, so they kept inflating.

Gains are non-existent because productivity no longer exists. Tech productivity has hit the wall and probably reversed. And since the US economy is now somewhere around 60% government related, and the rest largely monopolized by private equity and other buyouts, productivity there is non-existent.

If the Fed doesn’t see this, they are blind. My thinking is that most of this rate hiking is for optics. As I’ve said before, the 10 yr much above 3% will probably stall the economy. Of course that is with all other factors staying equal (1 trillion + deficit, no major trade wars, etc.).

I’m not saying there isn’t risk in these cockeyed yields. Of course there is. But most of this is backed by the moral hazard of 2009. The Fed will do whatever to keep the economy from crashing. Right now, they are trying to talk/walk a careful game of normalizing to SOME SLIGHT DEGREE. Only that.

IMHO

Interesting and perhaps correct. But I believe the bias among the central bankers and at least some of the Power Elite is to return to “normal” (i.e. “great moderation” norms) if at all possible. The current system is politically and economically unsustainable, and they know that. Average people, especially workers who remember the 90s and a rising middle class standard of living, demand real wage increases. Politicians have promised them this. Political operatives, especially on the Right (the Left still being too weak to intervene effectively) are waiting in the wings to exploit continued stagnation or decline among the group in the roughly 40-85% income bracket who feel the squeeze. Deflation means loss of jobs for these people. Inflation means loss of purchasing power. Governments and central banks need to give these people a boost without too much inflation while keeping employment high. It’s going to be one hell of a trick if they can. But that is the unspoken backdrop for every decision made at the top going forward.

Nobody knows what the FED is thinking. They may want to crash the US domestic economy to bring down China, Russia harder. They may want to crash it so that war could start. or they crash it so that nobody pay attention to Stormy Daniels or James Comey. Or they may do what you suggest, talk walk carefully and babysit the economy. Or they do what Wolf suggested, crash it slowly to clean up the rot and wrong unproductive investment. Nobody know what they are thinking and what their intention is. But we all know what their situation is. and that is, by easing, they will creat companies like telsla and snapchat, money losing business competing with sound business for labor, and raise salary. if they tighten, the rot will be cleaned but the economy will crash. For high yield funds, their position is simple. Keep buying and get yield. if they are right, they get bonus. If they are wrong by fighting the fed, invested will lose money and they will say “hey, it is NOT me, index is down, everybody lose money, it is he economy”. That keeps them stay long for ever until it pops.

Very good analysis. The high tech part of NJ economy was pharma research (rapidly being outsourced to India) and Bell Labs (a few small fragments survive), RCA (gone). I don’t know what our economy is actually based on. The cities are largely wastelands of abandoned factories from the 1950’s. Most middle class people seem to work for the government which has unsupportable pension burdens even though we already pay almost the highest taxes in the country. The rest mainly commute to Manhattan to move pieces of confusing paper around. We sill have tourism. Believe it or not, the NJ shore is a big tourist attraction. Jail, divorce, welfare industries are doing well. On the plus side, we may have legal weed soon if enough politicians can figure out how to make money of it. I figure real productivity has gone down about 80% during my lifetime. Whatever we got from computers has been more then canceled out by people using them for facebook,etc all day. The “education” system costs 8 times more and the college part produces a lot of people that actually know less then before they started. The health care industry has made a lot of progress in charging a lot more for mostly the same thing. Weapons industry has figured out how to make planes that cost a billion instead of a million for bombing old buildings in a desert in countries that usually don’t have an air force. Average IQ must have been dropping since Athens and it’s still going down fast. Idiocracy on the way.

Actually, Jersey produces about 46 billion in manufactured good per year, and exports roughly 1/3 of it overseas. One of the weird things about modern manufacturing is the lack of smoke stacks and huge plants. Much of what is made uses electric power, even for smelting. Even steel mills are much smaller physically than they used to be and have vastly smaller work forces. The lack of huge concentrations of industry, and a concomitant industrial proletariat, does not mean that there is no longer industry about making lots of goods. It just does it much differently than it did 50 years ago.

I think the exports are mainly refined oil and pharmaceuticals. Not many jobs and lots of pollution from both. We do export some software at the remnant of Bell Labs I work at.

Mikey,

Your comment is one of the best I have read in a long time.

I am bewildered these days. I thought an economy actually required a meaningful product to be made, or a necessary service offered for purchase. I guess I was wrong.

I looked up the lyrics to the Beatles, All You Need Is Love. Just substitute the word debt for love and it’s bang on. Here is a snippet. (sorry for the mind worm…but something to hum today :-)

Nothing you can make that can’t be made

No one you can save that can’t be saved

Nothing you can do, but you can learn how to be you in time

It’s easy

All you need is DEBT, all you need is Debt

All you need is debt, debt, debt, is all you need

regards

Nice explanation. I have wondered about the spread during normal times because it has been too long since normal times for me to clearly remember. My MM fund appears to circle the 3 month treasury rate, with no capital loss risk – like a passbook savings account. Its 7 day average today is 1.78%. When rates normalize it could rise to the 3.5% – 4% range with practically no capital gains/loss risk.

After rates normalize in a couple of years: Moving to safe corporate bond funds or the like, perhaps a couple of percent could be added to that, but share price risk would also be added. Add a couple of percent on top of that for a high yield fund that pays interest monthly.

Add Social Security to risk free or nearly risk free interest income and life will be nice … for me and for lots of others who did not see all of their savings eviscerated over the past decade.

As people spend, business will expand and jobs will be created.

Business will borrow because it has a need to expand the business, not because funds cost next to nothing. This was always the stupidity of QE – the assumption that business borrows only because the cost of funds is low. Even paper flippers borrow because they have a use for the money … to flip paper assets to greater fools. Since little of that cash makes it to Main Street, QE paper flippers do not expand the economy by borrowing.

Old people spending interest income actually does expand the economy.

Perhaps this time someone other than me will notice that QE and managed low rates are highly deflationary since low rates removes income, and thus, spending, from the economy. Normalized interest rates expands the economy because income is being generated where it will be spent.

Thus raising interest rates from where the are today will grow the economy and the only people hurt will be the paper flippers and those who own bonds priced with current rates. And those parts of the world who still embrace QE and negative rates.

I’ll buy in after the bond correction to come.

Or, to put it differently, rates may look sticky now in the corporate and high yield areas, but just wait. At some point, nobody knows exactly when but it will be within the next 9 to 18 months I suspect, the risk free rate will rise so high that bond prices will fall so the the correct rate differential is maintained.

Since lots of paper flippers exist today so that it’s a highly competitive market now, raising the cost of funds should cause a liquidity crisis among paper flippers. Kaboom and freefall, creating a market wide liquidity crisis for a short while. In a liquidity crisis, all prices fall a lot and fast because people sell what they have for whatever they can get to raise needed cash. A fire sale.

That’s when rates will normalize with a bonus for those who move fast and buy the excess part of the dip.

“Business will borrow because it has a need to expand the business, not because funds cost next to nothing. This was always the stupidity of QE – the assumption that business borrows only because the cost of funds is low.“

Not really that stupid…

They’ll definitely borrow just becuase the cost of funds is low – they’ll use the proceeds to buy back shares to raise the stock price and make management’s stock options viable.

I call those people paper flippers, stock buyback part of the family. They only do it because management profits using other people’s money (the corporation’s). The managers make gains. The firm gets stuck with the bill … very legal.

If the “data” keeps coming out so positive, the Fed will keep raising. Then there will be a recession. All systems look to be on Go mode for this.

At the rate we are going we should invert that yield curve by ? Any guesses here?

Probably half again longer than most people, those who are paying attention to these things, believe logically possible.

When I think about cash as a commodity it makes sense to me. So many

people I know all have an abundance of cash hanging around

waiting for rates to skyrocket like the 80’s.(The parties were better then.)

In the meantime, they are all competing for lousy yields.If

the Fed gets serious about removing money supply then the

savers will get paid.

I belong to the category of savers sitting on “an excessively liquid position” myself. And I am about to get even more liquid as I use this latest rebound to unload even more financial products to people who seem to have more need of them than I do.

However I have lost all hope yields will normalize, let alone shoot upwards, at least during the lifetime of anybody over 30 today.

Europe and Japan are committed to eternal financial repression and in my opinion financial markets (and a lot of commenters here) are right in blowing off the Fed: the first mini-tantrum will see them retreat all along the “normalization” front faster than James Stuart at the Battle of the Boyne.

Mercifully statistics and ill health are on my side but I do not envy those who’ll stay behind and will have to contend with increasing financial disconnect just to get a scrap of yield without having to resort to the equity casino.

The yield spread may be low because people believe the economy will go into recession if the Fed raises much more. In other words, they believe the economy can’t handle the rate increases and the Fed will back off. That may be correct. Nobody knows what the natural rate is these days.

We’ll know what happens shortly. When the Fed raises rates a couple more times over the next six months, the yield spread will rise or there will be a recession – one or the other.

Fed not likely to back off, would lose face. Maybe with major market crash, but typically takes 18 months to bottom.

Those shorting treasuries think fed wins, and no recession.

Those buying them like myself think economy too weak and private sector debt too high, will buckle under higher rates… this is, of course, exactly when fed always raises rates.

Bankruptcies galore, there is a reason it used to be illegal for corps to borrow to buy back stock, it’s not just bad for corps but destabilizing to system. And record margin debt fuels the crash.

My guess is 10-yr goes sub 1, the 30 sub 2. When nobody trusts corporates they’ll want the sovereign stuff.

And the euro… last recession really tough on the south. Unemployment much higher now than 2007, imagine next recession, maybe juiced with trade war and Brexit…

I agree with your assessment that the fed doesn’t know what the natural rate is any longer. In this last decade the economy and the country have changed and the old models no longer hold. The future is full of financial relationships which are only just beginning to emerge and the fed is fighting the last war.

yes I guess never.. why? because the junk bond investers know that the fed doesn’t really mean it with their normalisation plans.. no chance.. more QE and the other sick stuff plus more can kicking to come.. they will never want the so called market not to be controlled. it may get out of hand… basically everything is now junk whether called that or not..

The Fed can put the QE pedal back on, but it won’t create inflation. The fiscal deficits and growing debt load are too much for the Fed to do anything about. The Fed went off the marked trail and wandered into a cave, where it had no business, and the bear will be attacking soon. The Fed’s little arm waves won’t matter when the bear gets on top and crunches the Fed’s skull. The Fed can’t run because the bear is faster. Just like 2000 and 2007, only this time the Fed is fatter and slower, and it has no gun.

“Investors are “fighting the Fed”— doing the opposite of what the Fed wants them to do – and the difference between the shorter and longer maturities dwindles, and it dwindles, and it causes a lot of gray hairs, and it dwindles further, until it stops making sense to investors and they open their eyes and get out of the chase, and suddenly long-term yield surge higher, as bond prices drop sharply.”

That’s not really true as a rule of thumb.

Look at the last rate hike cycle.

In 2003, the 2 year treasury was yielding about 1.3%, while the 10 year treasury was yielding about 4%.

Three years later, in 2006, after aggressive rate hikes the 2 year treasury was yielding about 4.4%, over 3% higher… the 10 year? 4.5%… a whopping 0.50% higher, with the spread virtually non-existent by that point, dropping from almost 300 bps in 2003 to 10 bps by 2006. By early 2007, the Fed hiked the short end higher, inverting the curve.

There’s no reason to believe longer term bond yields will surge higher so long as there’s no reason to believe inflation and growth are going much higher, and there’s not at this point. I don’t know where the idea comes from that investors will all of a sudden push long term yields higher. The 5-year breakeven inflation rate is about 2%. That is what the market is expecting… in other words, more of the same.

Greenspan was convinced longer term rates would move higher in response to Fed rate hikes, and it never materialized. The Fed is fighting the market, not the other way around.

“….and they open their eyes and get out of the chase, and suddenly long-term yield surge higher, as bond prices drop sharply.”

In the chart below (click to enlarge), you can see how the 10-year yield surged toward the end of each prior rate hike cycle (and bond prices fell). This doesn’t mean that the 2-year yield didn’t briefly overshoot as the market expects more rate hikes late in the cycle – it’s well-known to overshoot. But the 10-year yield surged… and that was the theme here. Sure it moves less up and less down than short-term yields. What do you expect from a 10-year bond? But its yield nevertheless surges late in the cycle:

Aren’t interest rates in the Old School suppose to represent three basic things, ROI plus a reasonable Rate of Return, RISK, and Inflation..

Inflation isn’t the only thing that can cause rates to rise…

Under Minsky’s Instability hypotheses.. when risk is extremely under priced the pendulum can swing rather quickly.. The other side of Minsky’s hypotheses is where Risk is over priced as in very high interest rates.. So don’t depend upon inflation to be your guide or sign.. It is only one piece of the picture.

Jeez, it’s strange that no one mentions that Central Planning is among the failures of the old USSR.

Central Planning may have been the first and the worst cause of the demise of the USSR !

Why does no one question the profound wisdom of the Fed Central Planners — who relentlessly choose to do the undo-able ?

I remember reading long ago that Milton Friedman had a plan for monetary management something like this, “. . . react to the business cycle as necessary, but restrict money supply growth to between 3% and 5% as conditions warrant. And change things slowly too.”

Something like that. It is still central planning, but perhaps money supply growth does need some kind of a control ? Not so much interest rates, IMO.

Keeping interest rates and money supply, on a shorter leash — with slow, deliberate changes, over a long(er) period of time — may be the perfect antidote for the volatile machinations of our supremely ignorant FED.

People want protection from everything. They don’t want Risk to touch them so we expect our Central Planners to do away with it.. It is our own fault. We want a perfect world yet few wants it to be them that has to pay for it or even make their own plan to get there. So we borrow instead of invest or save.. Just the nature of humans who have not evolved much beyond more primitive times. It is so much easier to just believe that the Central Planners know best. To believe in Inflation to bail you out rather than make the cost of money as irrelevant to you as possible.

Unfortunately the Central Planners are just humans with human desires and frailties. They make mistakes just like you and I have. Humans do that, they make mistakes, a short lapse of attention or a faulty theory.. inevitable!

In my life I have seen the cycles.. There will come a time when Risk is over priced again.. I don’t know about getting rid of Central Planners though.. We can just hope they learn from their mistakes next time.

If I had to guess, I would bet the FED continues it’s march to the sea.

The Fed not only wants to normalize rates but to build a buffer for

the next down turn. With unemployment low they can raise rates

for awhile. I wonder what MONIAC calculates .

https://en.m.wikipedia.org/wiki/MONIAC

\\\\

Let’s not forget that unemployment does not include people not pursuing employment…statistics at it’s best. The statistics greatly reminds me of the Indian cast system: there are 4 casts in general, and the untouchables. People invisible to the system, that are forced out of the labor force by chance or circumstance.

\\\\

Let’s also not forget that working for Walmart qualifies you for food stamps (subsidized economy), people with loans and lives to live.

\\\\

And the subprime loan default rate Wolf pointed out recently is showing that parts of the system is very fragile, and that there are “working poor” people in the US.

\\\\

My point being that each FED hike will take away a little bit more from the people who need it most. And yet it is painfully obvious that it needs doing to recover a broken situation.

\\\\

It amazes me that a half- time job counts as one job.

How would you like to order two pizzas and get two boxes with half a pizza in each one.

The only fair way to calculate official employment (i.e. not under the table) is to multiply hours by hourly rate.

The data is all in the system, you’d just be running a different program.

The results might look pretty ugly however.

One of the measures the BLS issues accounts for that: U-6. It counts those as “underemployed” that have a part-time job but want a full-time job. U-6 a key metric.

A student that is part-time employed and happy with it should count neither as “unemployed” nor as “underemployed.”

\\\

Well, I think your question is on spot, and that is: do we need a comparative parameter that we could call “effective salary”. Lets assume the median regional salary is 40k, and you get 20k, so you would have 20/40=0.5. Hence one could track not just employment but it’s actual impact on life quality that is more or less derived from the income potency.

\\\

I also think there should be a normalized “salary to real-estate” coefficient, where one should normalize the salary with the average yearly mortgage rate for a 4 person family home, given a 20% down payment, given one buys it that specific year. If you make 100k and a home is 1M, it’s 10. The less the better. I made the assumption that real-estate is the dominant expenditure for the middle class and everyone below.

\\\

I would also like to see the salary normalized to the local healthcare cost…like that is ever going to happen… :)

\\\

For a government not to have data in the “Age of Data” is just a bad excuse.

\\\

“Eventually, the Fed wins. And when it does, junk bond yields have a tendency to blow out as the companies that issued those bonds suddenly get caught in a credit squeeze and have trouble servicing that debt. ”

This junk bond apocalypse will happen by the end of 2018? As everyone sees it, we have two more rate hikes before the Fed starts cutting again and the market party resumes.

I assume the Japanese and Europeans will also have to stop buying risk assets for the US apocalypse to really kick into gear.

Sorry, none of this will happen and the Fed CANNOT raise much more for the simple reason most of its debt is less than 5 years in duration.

http://www.themacrotourist.com/posts/2018/04/11/jamie/

At first, it was said that the Fed could never raise rates again and that it could never unwind its balance sheet. Then the Fed began doing both. So now the same people say that the Fed can never raise rates much further and can never sell much more of its holdings, etc. etc. People who haven’t been through these rate-hike cycles always end up surprised that the Fed can raise rates until it gets tired of raising rates. “Monetary transmission” means that markets have to react and have to go where the Fed wants them to go before the Fed stops raising rates. But markets have been fighting the Fed on this. The longer they continue to fight the Fed, the more the Fed will raise. And it won’t stop until long-term yields are high enough, and until the search for yield has stopped. It wants to “tighten financial conditions,” as it says, and that’s what that means.

And the Fed does not care one iota about your or my portfolio.

“Eventually, the Fed wins.”

My theory is this might have been true pre-2008. This time it remains to be seen. If there is a credit freeze again, I will bet the house that the Fed will develop cold feet.

For the Fed to keep raising rates, ECB, BOJ have to raise rates and stop QE. IMHO, Not going to happen.

Japan is talking about an exit from their easy money policies for the first in ages.

The ECB is already exiting: it started to taper its QE a year ago and will likely end it altogether this year. And it will start to hike rates no later than next year. That has been well-telegraphed.

It’s like watching grass grow, but it’s happening.

And the Fed doesn’t follow my advice or your advice. It does what it wants to do. Just don’t be surprised by it.

We live in a new normal where there is no longer any free market price discovery mechanism due to central banks manipulating all markets.

Without free market pricing, there is now also no reference point or horizon.

How long central planning of the economy can go on, is uncharted territory.

Russia’s experiment with central planning lasted about 70 years or 3-1/2 generations before they exhausted their country’s wealth.

Central banks current experiment with central economic planning probably started sometime between 1930 and 1970 depending upon your view.

70 years seems about the right length of time before central bank planning fails because by then they will have had enough time to destroy their countries wealth.

WHERE IS THE OUTRAGE ?

I barely detect even any anger — in the comments following this post or any other — that an un-elected, insular (and ignorant) cabal of self-selected Central-Planning Bankers — is busy destroying our economy.

Seeds planted by FAILED CENTRAL-PLANNING BANKING led to each of the last few decades’ worth of financial breakdowns : the 1987 event, the DOT.com stock mania, the 2005-ish real-estate bubble . . .

And, most recently, what some are calling the “everything bubble”. Soon to burst !

This un-elected banker cabal answers very specifically to its own constituents, NOT to the people, as Wolf said just above. WORST OF ALL, the are never called on any of their mistakes. Ever. Not by anyone in power.

Mr. Greenspan’s and Mr. Bernanke’s fingerprints were all over the most recent meltdowns, yet they fete themselves for a job well-done, annually at their Jackson Hole bash. The have more lavish than Kings soirees at the BIS Basel celebration also. And then, after “retirement” — eternal speaking tours that pay $100K per hour, or much more, for speaking of their successes (NOT !) and prescribing even more of such success to their captive audience.

WHO ARE THESE PEOPLE ? Why are then never held accountable ? Why are they not FIRED FOR FAILURE just like the rest of us risk doing what we do ?

Where is the outrage ?

“I barely detect even any anger — in the comments following this post or any other — that an un-elected, insular (and ignorant) cabal of self-selected Central-Planning Bankers — is busy destroying our economy.”

You won’t, due to propaganda. Fraud is the business model. No jail term for the culprits. It works till it does not. Like the “Emperor has no clothes” moment. It will come. Now or a decade or two later? I dunno.

The central banksters, created the problem, did not even know what is happening (Bernanke’s quotes are proof enough), and then solved the problem by changing accounting rules (mark to fantasy), throwing acronym money and buying up anything and everything. Above all, the gall to tell us that but for them we would have been in a worse place. Without adding that without them we would not have been in that position. Then you have the statement of Bush (‘I’ve Abandoned Free Market Principles To Save The Free Market System’) which never fails to amuse me as I try to figure out what he is trying to say.

That the asset prices have gone up helped a lot. That was their idea too. Needed to pull wool over people’s eyes! Looks like everybody likes a party and the central banksters know how to ensure it! Just goose asset prices!

As long as things are kept afloat there will be no anger. IMO, anger is the ending on the road we are walking on. The present monetary system is ripe indeed for a reset and there is no stopping it. When is anybody’s guess.

you must be new here.

there’s plenty of outrage voiced on this site or you haven’t read comments authored by gershon (who reads suspiciously like david stockman) or walter map, et al.

per his role as eyeball delivery meister our host allows readers their 5 msec of internet fame, an experience which might further be enhanced by garish background colours or additional articles by ms. hersh. it’s an up-turned soap box and you’re preaching to the choir.

alternative no. 1, the audience participation version of kabuki (voting), has yielded unsatisfactory results for decades. you can also write to your congressman, or something.

few – i would guess none – have any experience with the third box.

If you value free and fair trade, end the FED manipulators. Else, prepare.position for more of the same.

We could end all this but that won’t happen till a full crash. Too many globalist elites are making a killing by gaming the system (selling high priced military gear to the armed forces for example) it’s full of worm holes.

The real winning sector has been the MIC yet this lunacy is rarely ever mentioned????? Hmm………

wait.

i once thought “La-La Land” bore some discrete relationship to I5 but what you’re describing here is far more extensive than a simple geographic reference, amirite?

“A euphemism for a state of being out of touch with reality, having a fantasy prone personality.”

Not just LA :-]

The yield on longer dated treasuries should be pressured up by a combination of excess supply due to the fiscal deficits, and the QE unwind. This is admittedly difficult when the Euro bonds and the Yen bonds have such low yields. The increased risk in stocks and HY may also lead to a suppression of LT treasury yields due to rotation. Not withstanding all this the Fed can influence these long rates through the QE unwind. By doing so they potentially have room to raise short rates without a yield curve inversion which could impact credit availability.

My bet is they will attempt to pull this off with the current fiscial stimulus providing more maneuvering room for them to tighten. They will want to avoid a recession because the backdrop for all this is that there is very little stimulative capacity left in the system. Therefore a very glacial tightening with time left to allow all the lags to materialize. They may also be tolerant of a little more inflationary pressure without overreacting.

As far as priorities are concerned I would rank avoiding a recession first, containing inflation second, normalizing credit markets third, creating stimulative room for the next downturn fourth and very low on the list limiting risk off events.

Given these priorities they may be a surprising tolerant of periodic risk off events impacting equities and HY. This view might be tempered if there are systemic risks built into the current HY positions established domestically and off shore.