But no blood in the streets. Just a rate-hike cycle at work.

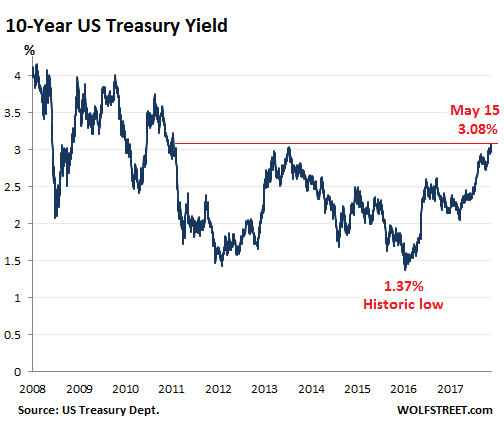

Today the US Treasury 10-year yield broke out of its recent range and surged 8 basis points to 3.08% at the close, the highest since July 2011. The price of a bond falls when its yield rises.

The odds have been stacked against the bond market for a while: the Fed’s rate-hike cycle, the Fed’s QE Unwind, a surge in government spending, the tax cuts, and the ensuing onslaught of debt issuance that is looking for buyers.

In addition, and with impeccable timing, the biggest US corporations with the most “cash” parked “overseas” are now “repatriating” this “cash” and are using it to buy back their own shares. What this really means for the bond market is this: This “cash” isn’t cash but is invested in securities, mostly US Treasury securities, corporate bonds, and the like. Companies are now selling those securities in order to use the proceeds to buy back their own shares at a record pace. So these huge bond buyers have turned into net sellers.

In other words, to entice enough new investors into the market, yields have to rise to make those bonds more attractive.

While short-term Treasury yields have been rising for a couple of years in a fairly consistent manner, longer-term yields are not so well-behaved and, despite the Fed’s efforts to push them up, are subject to messy market forces and speculative positions, including large short positions. And so the 10-year yield has moved in leaps followed by some backtracking until the next break-out and leap. Note that the most recent back-track only lasted a couple of months and barely shows up on this chart:

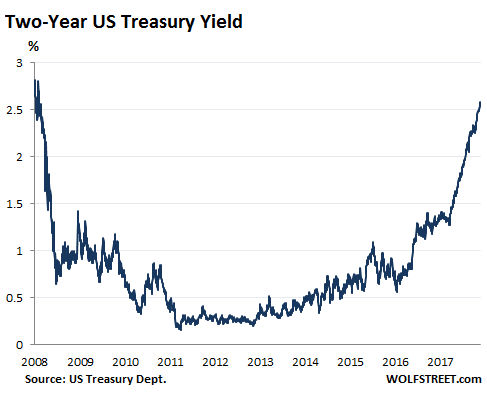

The two year yield ticked up to 2.58%, the highest since July 2008:

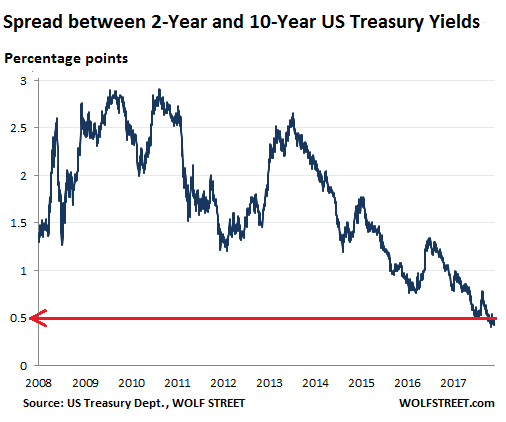

The difference (spread) between the two-year yield and the 10-year yield widened from 45 basis point to 50 basis points (0.5 percentage points), as the 10-year yield rose faster today (by 8 basis points) than the two-year yield (3 basis points).

So today provided some relief for those people who fear an “inverted yield curve,” a phenomenon when the 10-year yield is lower than the two-year yield. There are various theories about the cause-and-effect relationship between an inverted yield curve and the economy, but the last inversion was followed by the Financial Crisis, and prior ones had been followed by recessions, and that’s why people are nervous about this spread between the two-year yield and the 10-year yield. But so far so good, by the skin of its teeth, so to speak:

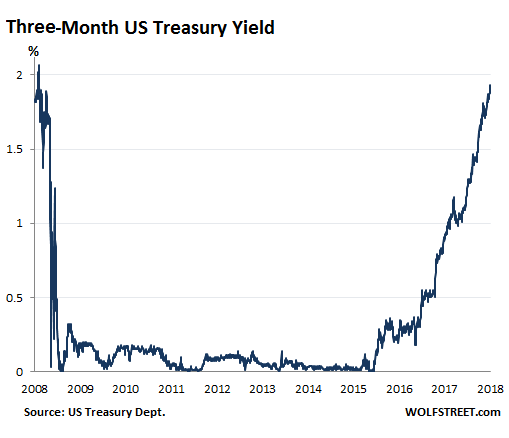

The three-month yield edged down to 1.92% from yesterday’s close at 1.93%, which had been the highest since June 18, 2008:

The 10-year yield functions as benchmark for the mortgage market, and when it moves, mortgage rates move. And today’s surge of the 10-year yield meaningfully past 3% had consequences in the mortgage markets, as Mortgage News Daily explained:

Mortgage rates spiked in a big way today, bringing some lenders to the highest levels in nearly 7 years (you’d need to go back to July 2011 to see worse). That heavy-hitting headline is largely due to the fact that rates were already fairly close to 7-year highs, although today did cover quite a bit more distance than other recent “bad days.”

The “most prevalent rates” for 30-year fixed rate mortgages today were between 4.75% and 4.875%, according to Mortgage News Daily.

The 10-year yield remains low, given what the Fed is trying to accomplish. Spreads remain narrow. Risk premiums between Treasury securities and corporate junk bonds remain extraordinarily low, still, despite everything. The Fed has been moving at a very “gradual” pace. It is two-and-a-half years into this rate-hike cycle and has raised its target range only from 0-0.25% to 1.50-1.75%. During the last rate-hike cycle, it raised rates from 1.0% to 5.25% in just two years! So this rate-hike cycle is occurring in slow motion and might last four or five years.

Markets are very slow to catch up to this already very slow pace. But they’re in the process of catching up, and today was one of those days, and there will be many more.

The Fed leads, the ECB follows. Read… Global QE Dream Ends, ECB Sees Rate Hikes, “Normalization” Becomes a Thing

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In other words, to entice enough new investors into the market, yields have to rise to make those bonds more attractive.

In other words, to lure more bagholders into buying debt the Fed is going to print away, yields have to rise. Fixed it for ya.

So, no blood in the streets because of the slow pace of the rate hike, or because of the steepening spread between short and long term yields?

The benchmark treasury bond can’t go much over 4-5% without someone’s blood in the streets.

I heard on CNBC that it’s nothing to fret about. That interest rates (yields) are simply “normalizing” (albeit gradually). Recall, yield on the 10-year benchmark was 6.5% back in 2002, they said. Well, gee, we didn’t have $21 Trillion debt back in 2002. There’s going to be at least some blood in the streets if the FED loses control of the benchmark 10-year treasury bond.

Oh don’t get me wrong. Higher yields mean lower asset prices. This is by definition the case in bonds, commercial real estate, and other asset classes. And this also tends to be the case in stocks for a number of reasons.

Two of the big reasons are: The difficulties junk-rated companies have funding themselves in an environment of rising rates and rising risk premiums; and the dividend yield is now lower than “risk-free” yields.

But “blood in the streets” is a metaphor for having hit the bottom during scary times, and therefore a buying opportunity. But that’s precisely what we don’t have. Far from it. There is still a huge amount of exuberance in the markets. But we might eventually get there, “gradually,” as the Fed likes to say :-]

Would that exuberance be irrational per chance?

The Hemingway Law of market adjustments still applies, I think:

“How did you go bankrupt?”

Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises

Like: Suddenly some hidden OTC-Derivative will have a Magnetar-Scale (Richter 42) tectonic plate adjustment.

The crufty cron-job running the position adjustment for something highly leveraged and very exotic stopped working and nobody noticed until they rebooted the server over something else and it did run – all adjustments at Once. Fragility is the Rule.

China’s holdings of US Treasuries has increased, so who’s dumping US Bonds?

Or is it just the increased supply that can’t be absorbed yet?

@Lenz Link? source please

MikeB @ Fused,

China is holding on essentially to what it has, but Japan has been systematically lowering its exposure to Treasuries.

If “gradually” is the word of the day, I’d say that the above chart shows that China is gradually reducing the amount of US T-bonds it holds.

Didn’t I see headlines a few months back that Japan had passed China as the holder of US gov debt? I think I remember numbers around 1.2 billion for both nations in those stories. Did I imagine that, or is this chart showing a differnt figure?

Mellon,

that wasn’t a “few months ago” — that was during China’s peak capital flight period (2016/2017) which is in the chart where the red line (China) dips below the blue line (Japan). This period lasted 8 months. But Japan continued to unload, and China began adding again.

Japan appears to be dumping US bonds.

Why?

Who knows.

So far the bond selling hasn’t increased the value of the yen as it is now back in the 110 area.

I’d like to know the answer to “why” also.

Here’s a partial theory: Japan does a lot of foreign development projects, where it funds the construction of a high-speed rail project or a port or something, while insisting that Japanese companies do the work and provide the equipment, etc.

This is part of how the government aids Japan Inc.

If Japan funds this development project in dollars, it could recycle its exchange reserves for that purchase. The development project then pays the Japanese companies in dollars, and so the dollars end up with Japan Inc., perhaps in their offshore locations.

The economy in Japan has hit a brick wall according to the news. I think I saw it on Reuters, after 6 or 8 quarters they are now in a contraction. QE has stopped working for them.

Lenz:

Given the surge in supply from the large issuance and from the Fed’s QE unwind, there can be no dumping of bonds by anyone else. Everybody MUST buy in order to absorb that flood of debt hitting the market, or else. The Treasury will issue about $1 trillion (give or take some) in net new debt in fiscal 2018. So you need to find buyers for $1 trillion in new debt. And all existing bondholders must hold on to their bonds. No dumping allowed :-]

How do you dump into a market where there are still, 3 Buyers for every Bond available??? Unless you are intentionally trying to depress it.

The over-subscription, or lack of, at the next big T sale will be an interesting # to watch.

After China Dump 1, a young hedge fund op bought up a sizable amount of the drop in the secondary market, after grilling Bernanke personally. The Fed also “cares” who owns their paper. Going back farther, the Fed once set the stage for a showdown with China by printing a trillion in CASH, just in case. The point on the hedge fund, which would seem vulnerable, is that they hold a lot of collateral should collateral become scarce. Point two any wholesale dumping would destroy whats left of your holdings, in dollar terms. And if corporations are dumping their bonds in order to ladder up at a later date, at a better rate, that’s bond market magic. It’s not a case of owning bonds or stocks, you can do both until such time as the US credit rating slips, the currency collapses, or credit contracts (squeezes) and obviously pushing new record issuance into a slowing global economy is not according to Hoyle, but so far it always works.

Japan is dumping bonds.

https://wolfstreet.com/2018/05/16/but-who-the-heck-bought-the-1-2-trillion-in-new-us-debt-over-the-past-12-months/

If you research the issue you will find that as interest rates rise. and currency shifts regional banks in japan end up with US bonds they are taking a loss on.

The BOJ has PUBLIC stated those bank’s should sell. Book the losses NOW, and move on, instead of keeping the bonds to maturity and incurring a larger loss.

Its just part of the changing landscape in increasing yields.

Further several Forigen projects, that were financed with $ (a common Japanese occurrence) are closing, so those Bonds get liquidated back into Yen an much nicer currency for those Japanes companies to hold.

That is NOT JAPAN DUMPING $ BOND’S alarm alarm Japan is dumping $.

I’m not quibbling about what constitutes “dumping”. US interest rates are going up – PERIOD. The fed has signaled 3 or possibly 4 quarter percent rate rises this year. I’m pretty confident this is going to happen, regardless of who is “dumping” or what is considered “dumping”.

It feels good to see rates go up. I wouldn’t mind picking up some GE at $5 and some AT&T at $15. In the meantime the best investment looks like a 2 year CD at 2.6% which about covers inflation.

Where is this magical kingdom you abide in where real-world inflation is only 2.6%?

The strangest things are happening. One of the markets I frequently check since i recently sold some properties there is Clearwater / St Petersburg in Florida. The prime real estate is now edging closer to 2006 highs. Odd considering rates are arguable much higher now for a 30 year fixed. I can understand prices reaching peaks in CA/NY since they have retained jobs during this last economic “expansion”, but Florida too?

Is the job market growing there? Is RE demand higher then supply?

Are we seeing the shift into low tax havens or the dispersion of the wealth effect into those lingering markets?

Some teenage kid made a video recently sarcastically listing “the top most boring cities in Florida to party” and the champion taking the trophy was a city 80 miles south where 80% of the population was over 80 y/o.

(80 over 80) that could spell a dead end to the supply glut.

Wonder how stranger things will get as rates edge higher.

Northerners are fleeing NY, NJ, and CT. Florida is considered NY with palm trees.

Funny you say that because I have an old girlfriend who from Long Island Who is now enjoying a waterfront condo in Palm Beach Knew I should of kept her

My Millenial daughter (27) lives there. We are visiting this weekend. Downtown St. Pete is booming with new high rise construction. We are staying at a recently opened Hyatt Place with a rooftop pool overlooking the bay. Lots of new museums. It is also a big foodie and craft brewery town. They have s beautiful waterfront and are not far from clearwater beaches. There are lots of high tech startups. I live on the east coast of Florida and St. Pete has become highly dedirable location and not just for millenials. Lot’s of low cost starter homes and the Millenials are buying.

Wish I had a feel for the relative magnitudes of the Japan selling vs the corporate-overseas-cash-repatriation selling vs the fed-QE-unwinding additional supply vs the due-to-deficits additional supply. Without numbers it’s not clear to me which of these matter and which are just edge noise.

Eastwind

Over the first 3 months this year, Japan cut its stash of Treasuries by $18 billion. This includes March (today’s TIC data) when it cut its exposure by $16 billion.

So in the overall scheme of things ($ trillions), these numbers are not huge.

Wolf,

you are my now favorite blogger! Not that I always agree to what you say (write) but you have the ability to connect top down understanding w bottom up knowledge, and that is something I respect and appreciate a lot!!

Cheers,

Frederik

Thanks!!!

This is great news. When money has a price, real physical capital (natural resources) is less likely to get squandered for marginal or wasteful purposes. Environmentalists should love higher interest rates. Frackers and land developers, not so much.

It will be interesting to see how yields on UST will develop during FY 2019 when the borrowing need of the US government will reach new highs at the same time as the FED will reach full speed of QT. And what will the ECB and BoE do if yields on UST is considerably higher than Euroland and UK paper, thus luring money away to the US market ?

Nothing to see here guys, just don’t look at South America.

It’s interesting to watch the yields pop on the 15th and the end of each month.

Personally, I think the inverted yield crowd is way premature. The Fed for sure has distorted the price of the 10-year, and they can manipulate it higher lower with a mere announcement.

The one question that I have is: To what degree has the Fed masked the effects of the Trump tax cut, and Federal deficit spending in the 10-year? I guess (wildly, I know) the spreads between the 2- and the 10-year will start widening even further, as sales continue, both for the Fed held securities, and the new issues from the US government.

Agree with you on the yield curve: The Fed now has a tool to keep it from inverting that it never had before: its balance sheet.

It can threaten to outright sell those securities, and just that threat will make long-term yields pop. And if that’s not enough, it can sell, say, $500 billion of its longer-dated Treasuries into the market at opportune moments and with enough rhetoric to support the effect, and watch long-term yields spike.

I doubt it will do that, but it can.

More realistically: In the past, toward the end of the rate-hike cycle, the 2-year tended to overshoot since the end of the rate hikes wasn’t clear enough six months in advance. Those rate hikes came quickly, often one a month. So it made a difference.

Now the rate-hike cycle is very slow (“gradual”) and predictable, and I doubt that the two-year yield will overshoot. So there is less chance of inversion.