The Fed leads, the ECB follows.

The voices are getting clearer: The ECB will end QE likely this year and begin raising rates possibly as soon as 2019. For now, these are not official announcements, but central bankers talking — not just German central bankers anymore, who have a more hawkish bend to begin with, but now even Francois Villeroy de Galhau, the head of the Bank of France and member of the ECB’s Governing Council.

They’re preparing markets for a new reality, the era of QE Unwind and rising rates. And the end of NIRP. The key word, so effectively etched in stone by the Fed, will be “gradual.”

Villeroy was talking on Monday at a central banker conference by the Global Interdependence Center and the Banque de France in Paris. Cleveland Fed President Loretta Mester also spoke there; more on her speech in a moment. Villeroy was talking to the media too to make sure his message got out.

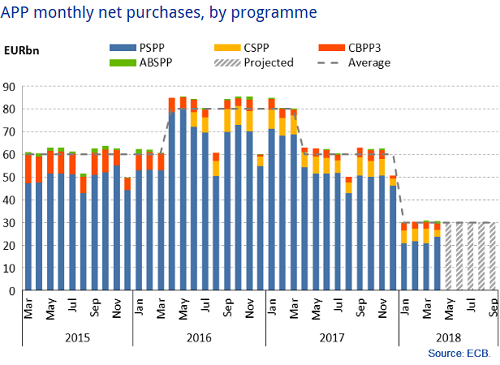

The ECB’s current QE program is scheduled to run through September. It already tapered its asset purchases from €85 billion a month at the peak in 2016 to €30 billion a month starting in January. It includes an alphabet soup of assets: government bonds (PSPP), corporate bonds (CSPP), asset-backed securities (ABSPP), and covered bonds (CBPP3):

So what everyone wants to know is what happens after September.

In his speech, Villeroy said that “the time when our net asset purchases will end is approaching,” but whether net purchases end in September or December is not “a deep existential question.” But they will end. The last time the ECB tapered, as the chart above shows, it took its purchases from about €60 billion in November 2017 and prior months to €50 billion in December and to €30 billion in January 2018. If this pattern holds, Eurozone QE will drop to zero sometime before the end of December.

And Villeroy added that, as the ECB approaches the end of QE, it will need to adjust its guidance on the “timing” of future rate hikes. These rate hikes are coming. The ECB has consistently said that rate hikes would begin “well past” the end of QE. In his speech, Villeroy defined this phrase, “well past,” as “meaning at least some quarters but not years” after the end of QE. So rate hikes in 2019?

In an interview also on Monday in Paris, Villeroy told Bloomberg that the ECB “will probably give additional guidance for the end of the year for the timing of the rate hike and the contingencies.”

He thus joined other ECB governors who think that the Q1 slowdown in inflation and possibly GDP growth, was “clearly temporary,” after “strong” GDP growth in 2017 with an “acceleration” in the fourth quarter. He said that he expects the underlying price pressures to strengthen, and the current “temporary” slowdown will not cause the ECB to delay its exit from QE.

At the moment, the ECB’s €30 billion of QE and the Fed’s $30 billion of QE Unwind nearly zero each other out. But the Fed’s QE Unwind pace accelerates to $40 billion a month in July and to $50 billion a month in October. Thus, the ECB’s QE taper to zero runs in parallel with the Fed’s ramp-up of the QE Unwind to $50 billion. By December, the net QE Unwind between the two central banks will be $50 billion a month of liquidity that just vanishes.

Interestingly, at the same conference in Paris, Cleveland Fed president Loretta Mester, in her speech, presented a blast from the past:

“Three years ago when I spoke here, … I discussed the Federal Reserve’s plans for normalizing policy and some of the challenges we would face as we transitioned from extraordinary economic and policy times back to ordinary times.”

No one believed her at the time. The Fed would never or could never “normalize” its policy, the meme went. The Fed had painted itself into a corner, they said. But after an initial hiccup, the Fed has been raising its target range for the federal funds rate “gradually” and without missing a beat since late 2016, and it has been ramping up its QE Unwind since late 2017.

Just like QE took six years to pile up $3.5 trillion in assets, and the Taper cut QE down to zero gradually over a year, the ramp-up of the QE unwind will also take a year, and the QE Unwind itself will “take several years to complete,” as Mester said. Everything is gradual.

Mester has been on the forefront of these voices to “normalize” monetary policy, and the Fed kicked this normalization off in earnest in late 2016. Now the ECB is communicating that it will follow the Fed’s procedure: First, taper QE to zero; second, raise rates gradually; third, after a few rate hikes, start the QE unwind. Turns out, central banks have not painted themselves into a corner, and the markets better get used to the idea.

Been reading misleading headlines about low inflation again? Read… Consumer Price Index Rises Fastest since February 2017.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, if the central banks painted themselves into a corner, what makes you think that the central banks will be able to complete this (insincere) attempt at “normalization?” Ben Bernanke himself said that there would not be normalization in his lifetime. Sure, the central banks are making an effort, but is in sincere and, if you think it is sincere, can they complete it?

Central banks never cease to surprise. Which is part of their MO. They did with QE, ZIRP, and NIRP in the sense that in 2006, those concepts weren’t even on the horizon. And it looks like they might “surprise” again, this time in the other direction, by showing everyone that in fact, they didn’t paint themselves into a corner.

Think about it this way: a central bank needs the freedom to act or else it might as well just pack up and leave. If it cannot “normalize” its balance sheet and shed those securities it acquired, and if it cannot hike rates from those ludicrously low levels, then what CAN it do?

The Yellen Fed has proven this statement by Bernanke wrong, and later Bernanke came around to it and started talking about HOW normalization might take place.

Several Fed heads have indicated that the Fed might let the balance sheet normalization continue even into a mild recession during which the Fed will cut rates. For example, if there is a mild recession in early 2020, the Fed could cut its rate (which then might be around 3.5%) by a couple of percentage points. But it might also continue with its balance sheet normalization because this is unrelated to the economy but very much related to asset prices, which the Fed is now targeting.

I can’t help add;

FED will never normalize away a large chunk of assets since they want to keep a trillion or so in excess reserves in the system.

But w money supply diving and now growing slower than nominal GDP asset markets will run into problems sooner or later – all else is just a pipe dream My guess is that it wont take more than 12 months before so and QT stops (and might even reverse).

Balance sheet normalization is not unrelated to the economy. When the Fed sucks money out of the system, interest rates will rise. This will have an inflationary effect on prices as interest rates are a cost for companies. They can either pass it on to the consumer or profits will come down or they go out of business.

Of course as you mentioned before, mortgage rates are rising, which is a cost for consumers. The Fed is unloading MBS. Auto loans will be more expensive, which is a big part of consumption. The government deficit spending will have to rise to compensate for higher interest rates, or the government will cut spendings. So less government handouts.

Tom,

Keep in mind that the Fed is purposefully hiking rates. It wants interest rates to rise. That’s the plan. And it wants the yield curve to steepen. This means asset prices, particularly those based on leverage, will come down (bond prices will fall by definition). That has some impact on the economy — which is what the Fed wants. Adding the QE unwind to the mix has little extra impact on the real economy. It just takes some liquidity out of the system.

The same thing happened the other way around. QE had little impact on the real economy, but a huge impact on asset prices. Now just reverse that, but in slow motion.

IMO the only reason the fed is getting away with this is due to the tax cuts…Unless the EU members get their socialist heads out of their collective a### they will collapse their economies with higher rates. Their mantra like the socialists in the US is tax the rich, redistribute the wealth, and spend like drunken sailors. Chickens coming home to roost in the EU, their open border policy with unfettered immigration and PC run amok will finish them off

Gotta disagree completely…”normalization” is truly a farce, with huge ongoing issuance since QE ended but the disappearance of nearly all conventional sources of Treasury buying.

Before offering that the CB’s didn’t paint themselves into a corner, I’d suggest you offer who is buying the Treasury debt since QE ended and which maturities the Fed is dumping…and which they are feverishly buying. The publicly available data to these questions confirms there is nothing normal about this cycle and the damage that QE continues to do.

Hot off the press:

https://wolfstreet.com/2018/05/16/but-who-the-heck-bought-the-1-2-trillion-in-new-us-debt-over-the-past-12-months/

And when the price of oil skyrockets and economies tank, watch the back-pedaling. The World is addicted to debt.

This should never have gone on so long, imho. 3-5 years maybe….10? No way.

I think letting it go on for a day was too long. Can’t scare them into fighting against greed when the criminals get rewarded.

I disagree They should NEVER have gone down the QE road to begin with Should have let the crooks go broke and disbanded the FED

QE1, back in late 2008 and early 2009, should’ve been done at a penalty rate (i.e.; selective bond buying) rather than unlimited free money. QE2 and QE3 should never have happened.

The central bankers’ swindles against the 99% are, unsurprisingly, finally waking up more and more former sheeple who are rejecting the corrupt, crony capitalist status quo in favor of populists and nationalists. Italy appears to be the latest EU country where populist candidates appear to be on the verge of achieving a political breakthrough. This suggests that the ECB’s ability to keep playing extend and pretend may finally face its first serious check.

This is all fine and dandy but I sense that a recession coming on in the next year to year and a half or so. Assuming they start clearing out the giant pile of bonds sometime early next year, by the time a recession hits they would have only cleared a teensy-weensy part of their overall balance sheet. That’s a problem. Heck , even the Fed by then would have only cleared off a quarter to a third of what they probably mean to by then (assuming their plan is to normalize down to around 2T).

So, assuming we do have a recession starting around the second half of next year, it’s pretty frightening to see where we might be compared to the monetary and fiscal situation would expect to be in right before a recession. This time around the FFR would be at about half what it was before the last recession, the Fed balance sheet would be three times as large (and let’s not even talk about the ECB’s balance sheet), total US debt to GDP would be almost twice as high and the budget deficit almost three times as large… and remember this is right BEFORE a recession when all these metrics should be their mirror opposites. If this is not a recipe for disaster I don’t know what is.

well will the Bank of Japan follow suit ?

I can’t pretend to know a lot about this stuff but Japan is REALLY different.

We always hear about the two decades of ‘depression’ or ongoing deflation but Japan has done pretty well all that time.

Unlike the US it has a big trade surplus. Also its debt is huge but is held internally.

Re: the trade surplus. Japan needs this to eat and the high yen has been its biggest problem. Don’t be surprised if it is content to keep its rates at zero while others raise.

A rising interest rate by the US and EU would help to sooth PM Abe’s announced intention of a lower yen.

He could accomplish something by doing nothing.

I think the Fed is sincere and really, really doesn’t want to back track. It will take a serious crisis, I think, for them to reverse their gradual rate hikes. I can see them pausing but reversing?

It’s not just that they want higher rates for their own peace of mind but also they don’t want to lose what credibility they still have.

Way too early to draw any conclusions as to how QE will unwind. They have barely started with baby steps to be meaningful.

By the time we hit a tiny recession, financial media will be in such “end of the world “ panic mode to scare off every living thing, including the fed and the Congress, remember how Paulson bailed them out last time. The question won’t be about unwinding QE as that will be anathema, but why can’t the Fed keep a 4trillon balance sheet forever, or add more, who is to say what the right balance sheet is anyway, why not 10trillons, the magic of fiat currency in action, they really own the world with the click of a mouse, and I keep commuting every day for a pittance , honest money is no more.

Shut it down WE know or you could just say “ pull it “

In my view, the big boys, the insiders have dumped all they could onto the so called investors big and small. Now, it is time to crash the market, and in few years, the big boys will buy back everything they sold at pennies on the dollar. Rinse and repeat till .0001 percent own 99.9999 percent of the world; owning 98% of the world is not enough.

These damn peasants can still eat; we’ll have to make sure that they can’t afford even a loaf of bread; so they would beg of like a dog even for a loaf of bread.

Bingo. Engineered boom-bust cycles by the Wall Street-Federal Reserve Looting Syndicate are the most efficacious means to transfer the wealth and assets of the middle and working classes to the Fed’s oligarch accomplices. Notice the gusto with which the corporate media talking heads are trying to lure the sheeple into Wall Street’s rigged casino so the Great Muppet Massacre of 2018 can commence. It’s a matter of time before Goldman and its ilk go massively short, then orders its Fed creatures to hike sharply enough to crash these rigged, broken, manipulated “markets.” It’s happened like clockwork every 8-9 years since 2001 – wash, rinse, repeat.

Unless mortgage rates plummet, it looks like the total QE unwind will max out at about $40 billion per month, not $50 billion. See page Chart 2 on page 9 (pdf page 10) at the following link:

https://www.newyorkfed.org/medialibrary/media/markets/omo/SOMAPortfolioandIncomeProjections_July2017Update.pdf

That’s Chart 2, not page Chart 2.

Also to be more precise, it looks like the paydown will hit $45 billion by October of this year, and then gradually drop to $40 billion.

The rubber hits the road when the rate hikes start biting (given the debt levels). It is also wishful thinking to imagine there will no impact on Southern Europe bond yields IF ECB raises rates!). We will have to wait to see what the CBs do then. Even they are not sure what will happen is the reason for the gingerly way they are going about it – both the way in which they communicate to the markets of their intention (in the form of trail balloons) and the rates being increased ever so “gradually”.

If you look at the chart provided, in April the ECB (or to be more precise the member banks) had to reduce purchases of corporate securities to step up purchases of sovereign bonds while sticking to the €30 billion/month expansion.

This was chiefly done to keep yields on 10-year Italian bonds under the “psychological” 2% threshold, but success was very limited. Not even the rumors (planted no doubt by the usual suspects) of a technical government headed by one of the usual Goldman-Sachs alumni were enough to stop this “rout”.

To get back to the issue of rates, yields on euro-denominated bonds have been seesawing higher since last November and now even banks are starting to offer depositors something akin to a yield.

The reasons are several: a spate of high-profile bankruptcies (led by Air Berlin and Areva), inflation biting more than statistics indicate, dollar-denominated bonds being an attractive deal again, junk-rated companies engaging in more of their usual cash-burning shenanigans etc.

This “pressure towards normalization” is surely going to cause some problems, especially to the usual suspects, such as small Italian banks which have grown to depend on risky business such as real estate speculation which can only work in a repressed financial environment and even then only for so long.

Normalization means poor calls and sundry financial shenanigans have to be liquidated.

This doesn’t need to be a chaotic affair: the Air Berlin bankruptcy is a good example of how to behave like responsible adults when liquidating bad investments.

But sadly politicians and other assorted megalomaniacs see this as an opportunity to stroke their own egos and gain votes from the gullible who forgot how things went last time around…

In Spain at least, and I believe Italy and Portugal, the owners have got labour just where they want them – with wages screwed way down to insulting levels, and still high (although descending) unemployment, so this will compensate for any minor rate rises.

$104 Billion since October 2017 is a drop in the bucket. It appears the FED still stands in that painted corner, but the paint is ~3% less wet- it has a ways to go and anything could happen.

My theory is that the FED is raising rates now, albeit gradually, in order have some room to reinstate QE 4, and ZIRP before it’s forced into a negative interest rate policy situation.

As for the ECB, who actually believes it isn’t still buying up Italian bonds? Or that it will ever stop buying Italian bonds? Italian banks are insolvent. Italy is insolvent. If Italy defaults the € collapses. Wake me up when there is a meaningful shift in ECB policy wrt PSPP and CSPP purchases Italian.

They have to pedal forward a bit now so as to be able to back-peddle furiously when the recession hits – and it is building now.

The first big difference is that the EU might fall apart if Draghi screws it up raising rates, whereas the USA will hang together through the next financial crisis. The second big difference is that there is no EU wide account depositor insurance, and likely never will be. Thus banking panics are baked into the crisis. The solution is likely that countries will leave the Eurozone and debase their new currencies by printing to recap their banks and default on their sovereign debt in the time “honored” fashion. Given this enormous downside, the prospects for courageous action by Draghi are minimal. This will likely blow up during the reign of his successor.

They will raise rates and crash the economy in Q1 2019.

The question is why? Is there anything happening in Q1 2019 that has a big impact on Europe?

Well, there is Brexit on March 31 – so there is that.

One could suppose a country leaving the EU would obviously cause a crash and recession for the rest of the EU countries. Maybe so much of a crash/recession that other countries will in future be banned from making such a move.

Well, I guess we’ll just have to see what happens.

If Brexit causes a crash/recession it would seem a fair compromise to ban countries from leaving the EU.

Handy too, as that will stop Five Star or League from getting any ideas in Italy!

Timing in these matters is everything of course…

Pity doing this will lead to a political revolt at the European elections in May 2019…..

H1 2019 is shaping up to be very interesting indeed.

After Argentina crisis Brazil will probably follow, they really blew a lot of money and it shows.

If teh ECB follows the announced schedule.

Things will get a little more interesting, in french and Club-med banking.

The Nasty little Mafiosis gifts of time and much free money, have been wasted by italian and spanish bank’s, in particular.