What will Housing Bubble 2 do when mortgage rates hit 6%?

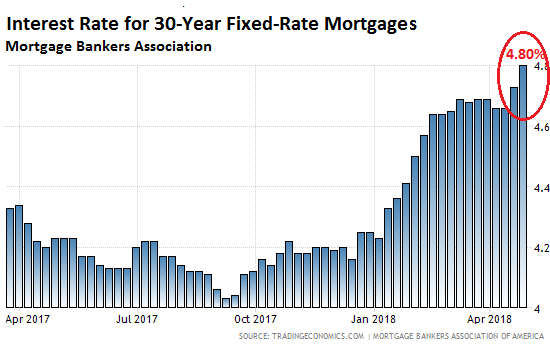

Wow, this was fast. The average interest rate for 30-year fixed-rate mortgages with conforming loan balances – $453,100 or less with 20% down) jumped to 4.80% for the week ending April 27, from 4.73% in the prior week, and from 4.66% two weeks ago, the Mortgage Bankers Association reported this morning (chart via Trading Economics):

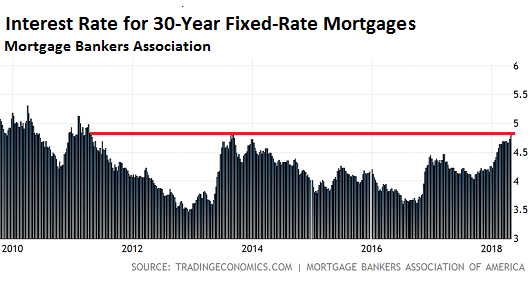

At 4.80%, the average 30-year fixed rate is now equal to the highest rate since September 2013. And the last time, the rate was higher than 4.80% was in 2011 (chart via Trading Economics):

That date with 2011 has already happened:

- The average interest rate for 30-year fixed-rate mortgages backed by the FHA jumped 10 basis points in the week, to 4.81%, the highest since July 2011.

- The average interest rate for 15-year fixed-rate mortgages jumped 8 basis points in the week, to 4.21%, the highest since February 2011.

“Points” – the upfront fees, such as origination fees, that are usually rolled into the mortgage balance – rose 4 basis points during the week to 0.53% of the mortgage balance (mortgages with 20% down), after having already risen 3 basis points to 0.49% in the prior week.

The Mortgage Bankers Association (MBA) obtains this data from weekly surveys of over 75% of all US retail residential mortgage applications handled by mortgage bankers, commercial banks, and thrifts.

The MBA’s measure of the average mortgage rate is headed for 5% in the near future and to 5.5% later in the year. The Fed is on its rate-hike path, which pushes up shorter-term yields, and longer-term yields are following with delays and in wild spasms. The Fed is also unwinding QE, which puts pressure on long-term yields. It has eased into the QE Unwind, starting last October, just like it gradually tapered QE out of existence. But the QE Unwind is picking up speed. The US Treasury yield, currently near 3%, is setting up for the next spasm higher. This will push the 30-year fixed rate to 5%.

At 5.2%, the average mortgage rate will hit the highest level since 2010; 5.5% would take it to the highest level since 2008.

The big difference between 2010 and now, and between 2008 and now, is that home prices have skyrocketed since then in many markets – by over 50% in some markets, such as Denver, Dallas, or the five-county San Francisco Bay Area, for example, according to the Case-Shiller Home Price Index. In other markets, increases have been in the 25% to 40% range. This worked because mortgage rates zigzagged lower over those years, thus keeping mortgage payments on these higher priced homes within reach for enough people. But that ride is ending.

For now, demand for mortgages continues, as homebuyers are trying to make deals before rates rise even further. The MBA’s Purchase Index, which tracks the number of mortgages taken out to purchase a home (as opposed to refis) increased 5% compared to the same week a year ago – after last week’s 11% increase.

A 5% mortgage rate will trim off some homebuyers at the margin but is unlikely to derail demand at this point. The real pain for homebuyers, and the housing market, will likely start closer to 6%. While 6% is still a historically low 30-year fixed-rate, home prices are historically high, and the equation has changed. It’s unlikely to get to 6% in 2018, but next year is a candidate.

In terms of rents, the housing market is veering off in all kinds of directions. In Chicago, asking rents have collapsed by 30%. In New York City, they’re swooning. But they’re soaring in Southern California. And the US average hides all the drama on the ground. Read… Update on the Most Splendid Rental Bubbles & Crashes in the US

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Probably more to come.

Transitory!

The tightening is strong in this cycle! Credit gets crushed at the top of said cycle? Wang punch in the punchbowl? Silent running in credit, we have auctions where the bids are hard to understand?

So if mortage rates are 2011 redux, what about stock prices?

Bouncing along on top of the 200 day M/A’s, while the height of each bounce is getting smaller and smaller. Like a ball, basically.

Eventually, there is a polarity reverse and stock prices are reflected off the M/A’s in the other direction, down 30-50% or so. Should be fun to watch. Could happen already on the next bounce.

Imagine if rates stay high for the next decade as baby boomers downsize and die-off and their homes flood the market as rates are tracking historical norms of 5-8%

Things are gonna get more interesting in the next decade.

I wouldn’t worry about the boomer die-off. The total US population is increasing by roughly 0.9% per year, or 10.0% per decade. At 326 million currently, it will reach 335 million in 2020, 368 million by 2030 and 400 million by 2040, barring a pandemic, meteor taking out earth, etc.

Overall, this should absorb any homes vacated by boomers and still place an upward bias on prices.

Have you been around people? So many dumb people are around; the top dumbest 5% are so dumb that you can actually sell bridges to them.

These people rushing in to buy an overpriced house because the interest rate is increasing must be nuts. They are like sheep to the slaughter.

100% agree. Quite dumb.

Mania for sure in some markets. We went to an open house in the eastern suburbs of Seattle this weekend. Not to buy… just getting a feel for the market periodically. Nice house, new McMansion in a suburban neighborhood (stacked houses, trees gone, all houses look the same.). Convenient to I-90. 3000 sq ft. 900k asking. 10+ offers and sold in five days. Took five days only because of an offer review date limitation, otherwise would have sold day of announcement.

But butbutbut… Real Estate only goes up! Just like Pogs and Beanie Babies!

An old guy I know bought his first house with a mortgage rate of 18%. Right in the middle of Paul Volcker’s successful attempt to kill manufacturing and unions. Said it was the best deal he ever made. Bought at peak interest and refi’d all the way down. The appraised value went up three times, the interest rate went from 18% to 6%.

People that bought at sky high prices and near zero interest rates have no upside. Only wage inflation can save them from the bed they’ve made. And yeah the powers that be aren’t going to let that happen.

Excellent point. Our first home in late 80s was financed at about 12% as I recall. Today it’s worth 4 times what we paid for it. Same crappy neighborhood just much more expensive house.

Brilliant observation!

If they are doing it for short term resale like flipping or with a risky arm loan I agree. However if people are coming off the fence to buy a long term home they can afford to control the future cost of living with a full 20% down then that isn’t necessarily bad.

There is always risk buying a home. And no one knows what crazy shit will happen next to prices.

I suspect stagnation and slight price decreases over a long period.

When will the higher rates increase the gubmint bill for all oir debt?

That has already started. But a lot of the debt is longer term, and the interest rate (coupons) those bonds and notes pay remains fixed until they mature and have to be replaced with new bonds and notes.

This this phases in gradually, over the years.

This forum is one of the best on the internet, Wolf. Excellent comments.

Even if rates were to reach 6.0%, they still seem inexpensive compared to even the early 2000s, and certainly the 1980s and 1990s. Buyers can also opt for a 15 year term, which has a lower rate, albeit a higher payment because of the shorter amortization. And they’ve already reached 5.5% in Canada for mortgages with a 5-year term.

My first home, in Toronto, has a 12.75% mortgage amortized over 25 years with the rate renegotiated every 5 years. And that was without the benefit of mortgage interest or property tax deductibility for income tax purposes, which Canada has never had for personal taxes.

So, rates may be rising, but they’re a bargain compared to the recent past.

HB, would be interested to see inflation adjusted incomes from the last 20 years. Rate increase don’t help but the spread on incomes may be a larger culprit than a 6% mtg.

Housing has gone up much faster than incomes the last twenty years. Historically the housing market has not been too sensitive to rising rates. There is a small impact but not as much as you would think. However, with the low supply and so many marginal buyers, I suspect this time around the housing market is much more susceptible to rising rates than in the past.

Wolf’s 6% number is not something I’ve verified independently but it sure seems like a reasonable working number for real pain.

Certainly, housing prices have risen sharply since the late 1990s. Why?

1. Fed counterfeiting, er, QE1, 2, Operation Twist, etc. Add to that the help they received from their fellow criminals in China, Japan, UK, ECB, BoC, etc. All that money didn’t just wind up in bonds or equities.

2. The number of foreign real estate buyers in IOUSA has increased dramatically since the late ’90s. Many pay cash.

3. Many buyers are downsizing and/or leaving CA, NY and other expensive markets. They received bags of money after selling their coastal homes and can afford – for the area they move to – a relatively expensive home. For example, look at Boise, ID or Reno, NV, fueled by former CA residents. Or Naples, FL, fueled by NJ/NY buyers. I know many people who moved there, and all paid cash for their new homes.

My point is, rates may be on the way up, and house prices have risen, but for many buyers, it’s an inconsequential bump in the road.

“My point is, rates may be on the way up, and house prices have risen, but for many buyers, it’s an inconsequential bump in the road.”

You are correct. It all comes down to where one is selling and where one is buying. Same thing was happening in the run up to 2008. Folks whose phase in life allowed them to relocate without regard to work and such, were selling in high price areas and relocating to lower price areas: they were paying cash for a new house with money left over.

As mortgage interest rates increase, can mortgage shenanigans be far behind?

Yeah middle America tech bubble cities think their home prices are unsutainable. Yet they fail to discuss how people bailing on California and New York can fuel that fire for a long time to come baring another massive crash.

Yes, rates are inexpensive, but homes are not.

You need to look at home prices vs. income levels (and personal cash levels). You don’t want to exceed a loan amount of about 5x your gross income, and that’s on the very aggressive side. 4x is substantially safer.

So you would need to be earning 200k/year to afford a $1 million home @ 20% down, which is a bargain in a lot of SoCal and NorCal markets. The difference between a 4% and 5% rate is a car payment ($475/month). That also means if you’re maxing out your budget, you would need earn over 13k/year more just to qualify for the increase in interest.

I’ve been doing some digging in my area, San Diego, and it’s pretty staggering. People are maxing out their purchasing power by buying the most expensive home they can afford and putting down as little as possible (3-5% jumbo financing). I even found a loan that was MORE than purchase price.

With rates going up, this can only continue if prices come down (LOL) or income increases. I don’t know which is more unlikely.

The other issue is that home prices haven’t been “stress tested” in a recession since 2008-9, and I bet there are a lot of weak handed owners out there that aren’t going to be able to make payments when they or their spouse loses their job. What I see here in Seattle is that it takes two full time professionals to afford a home at these prices, and even then it’s a major stretch. They have to accept being house poor to hope to buy. I’ve been through plenty of these $1M+ homes with IKEA furniture and old Toyotas in the garage…

During the next recession, it could ugly as a lot of inventory is coughed up in foreclosure. (And I’ll be waiting with a bag of cash in hand for that day…)

Mark:

I think a lot of places have the same issues. The incomes may be lower and the homes lower priced than your area, but the money stretch is the same.

One bit of democracy left. A guy with a$200,000 income living beyond his means can be in exactly the same place as the guy making $50,000 living beyond his. When the bank takes all the stuff back, Mr. $200,000 may be left sitting on the curb in a more upscale neighborhood. But, that’s about it.

OK, I’ll take the 1980’s interest rate at 1980’s housing prices….sheesh.

Absolutely. Forget the mortgage interest rates, at 1980s home prices, I’d put 50% down or just rent and save a few more years, then buy the place outright.

Putting 5% down on a $1M house is just nuts. You have to believe home prices are going much, much higher for buying today to make financial sense…

I am not one to think these prices are a bargain even at 6%.

My mortgage interest was 12% from 1985 to 2000, but my house price was 1/5th the price it is today. Those high interest rates kept my home from appreciating in value for 9 years.

This isn’t the 80s or 90s bud Have you looked at the thirty year chart of US debt to GDP lately? Take a gander and get back to me

Much higher, for sure, but the Fed can/will engineer QE to Infinity, if need be. And the Fed also held the interest rate on long Treasuries to 2.0% from 1945-1952, in part because of the high debt to GDP ratio.

As to the chart of US debt to GDP, I presume you’re referring to gubment debt. If so, the US level is less than half of Japan’s, not that I’m advocating we follow their lead.

Finally, the Fed and Treasury have another ace-in-the-hole. The Treasury could swap outstanding US debt held by the Fed for gold, and the cancel it. It wouldn’t hurt gold prices, but anyone holding Treasuries wouldn’t like it.

So after years of financial repression by the Fed and its bankster partners, I welcome higher rates, hope they do cause massive dislocation, lead to a debt jubilee of some variety, and in the end, we may be forced to return to the gold standard (or a derivative thereof). None of which would be a bad thing.

The combination of higher mortgage rates and massively expensive houses is a deadly one. If you have only one of them, yeah, maybe prices will not fall. But both? No way prices will not drop.

Yes, but home prices are in a different league today. That’s the issue with rising rates.

Precisely. It’s the actual payment that matters. Low rates are not a bargain if the asset prices (debt) have ballooned to record highs.

Very telling that Freddie Mac is expanding their 3% down payment mortgage option. One would think we would have learned that lesson. Apparently not.

It isn’t. Freddie is just catching up to Fannie which has offered this program for a couple years.

Nothing new here.

“Even if rates were to reach 6.0%, they still seem inexpensive compared to even the early 2000s, and certainly the 1980s and 1990s.”

Yeah, but you’re kind of ignoring a huge part of the equation… the home price.

You’re talking about houses that cost, in some cases, seven or eight times what they cost in 1980. Housing is all regional, so I’m referring to the ‘hot’ markets here.

The increase in principal payments dwarf the decrease in interest costs in many cases. I’d take a 10% rate on a $100,000 house any day of the week over a 5% rate on the same house for $700,000.

I don’t care if mortgage rates go to 0%, most Americans (and Canadians) simply have no business buying $1,000,000 worth of house. The traditional economic fundamentals are simply not there.

People are deluded and you’re already hearing the same narratives from the mid-2000s: housing only goes up, must buy now while you still can. The situation is not the same, and I’m not claiming another 07-08 will happen, but it doesn’t look sustainable to me.

I’ve had contradicting thoughts on this recently. On one hand a higher rate should mean a lower price but it will also mean even more of a disincentive for people to move and swap house creating an even bigger lack of supply. Plus it seems as though there are plenty of people willing to sign up for 50-70% of their income to housing. Idk anymore. – Priced out millennial

People spend 50% income to buy houses for two reasons. Speculating on price increase. Fear of rent keep increasing.

Wolf publishes rent data. NOT rising too fast.

If price starts to drop, it kills speculation. People will less likely to buy and if mass lay off happens and recession hits, cash is king.

People do NOT “WANT” to sell, but those stretched leveraged weak hands will be “FORCED” to sell.

I do NOT know how strong the hands are holding these houses. When the tide retreats, we will see who are naked.

You need housing just like you need groceries, and while Greenspan thought grocery products were fungible, you would buy the cheaper protein, that option doesn’t always work in housing. I would suppose the Fed is concerned about a lack of affordable housing (yawn) and would QUIT RAISING RATES!!

Maybe. What happened in Denmark was that the banks left the most highly leveraged folks alone (some of them even lived for free as “caretakers” of their “repossessed – but not quite cause then we’d have to book the loss” 2-15 MEUR mansions.

They left lots of houses alone too. Nobody living in them, yet, not listed for sale, nor bankruptcy or anything. The banks just kinda kept them in limbo as it were. We still have those empty storefronts and houses in the less popular towns – negative interest rates doesn’t force anyone to “cover” their positions as it were.

Some middle class people will be wiped out as an example to others, especially those who are not fully leveraged and / or paid off a portion of their mortgage are at a real risk from “changing terms and conditions”.

Those situations where the bank can clear the debt and cover the repo fees are the ones to be wiped out first when stressed-out banks need to reduce exposure. Everyone else will get to cut a deal. The bigger the crater they can make in reserves, the better the deal will be.

I wonder who does the actuarial analysis for the banks that are deciding wether to hold empty houses in these less popular towns or simply sell them at a loss and cash out. Is the decision making formula different in Denmark than the US’s midwest rust-belt for example?

In the US banks did that to home owners during the great depression. They’d call in loans for homes that were almost paid off in order to seize the property and flip it for cash. While leaving owners who were underwater alone.

I know nobody believes this but there will be a day the FED will be “FORCED” to raise rate and “FORCED” to punish irresponsible debtors in order to restore some discipline in the system. That will be the day the nation faces existential threat after years of waste, decayed morality and wealth transfer.

Well, an extraneous recession would force many on the edge to sell and downsize. This whole system seems to be building up vulnerabilities at every corner. It’s great as long no shocks happen.

Contrary to what economists would like to think, systems hate equilibrium states.

All this makes sense, but then again, the market is under no obligation to make sense.

“…it will also mean even more of a disincentive for people to move and swap house creating an even bigger lack of supply.”

True, but that is only one part of supply. People are also still building condos like crazy. https://www.forbes.com/sites/joelkotkin/2017/08/31/high-rise-glut-affordable-housing/#a02c18453e01

Even if no one sells, but all that new stuff comes online in the highest priced areas while rates are spiking, there is going to be a huge wad of supply with no demand. While it may take a while to percolate all the way over to affordable housing in full single family homes, a sufficiently gross glut of high income condos with no buyers and raising rates should eventually put downward pressure on the entire housing complex.

Good point but my real question is what is the glut of luxury apartments going to do( if anything) to housing. Where I am they aren’t doing the condo building in fact they’re only building a handful of million dollar condos. What they’re pumping out is luxury apartments to the tune of several thousand this year alone.

Pat:

Same here in mid-size southern USA town. We even had a two year moratorium on new apt building. It timed out and the developers went right back to it. There could be genius behind this building, or it could be folly. Time will tell.

They’ll be forced selling, and there’s no doubt about that. They’ll be plenty of deaths, divorces, foreclosures, layoffs, job shifts, etc. in the upcoming recession. Plus, we have more investor ownership of homes than ever before. What do you think they will do in an environment when prices are rents are set for a multi-year decline? Sell, sell, sell – and they’d be making the correct decision. Plus, there are tons of boomers waiting to downsize as soon as they see prices going against them. I know some of them. When your home equity gains are a big part of your retirement funds, and you will be retiring in a few years, it makes no sense to take the financial risk of keeping a large house you don’t really need in a shaky market. Your successful retirement depends on selling that house.

Plus, all it takes is 1% of the housing supply to sell at a lower price, and prices are lower for everybody, whether they stay in their house or not.

Bingo We have a winner

Nice to see someone who “gets it”

A good friend is in the real estate foreclosure business. She just passed her RE broker exam. Good timing, because I think her company’s about to be very busy.

Which is why a home should be a place to live. Not a bank. Not a retirement plan. Not an investment.

Real estate investment is a whole ‘nuther thing entirely.

The goal in home investing is gaining income flow, so if you are a boomer and you want to move, you rent out your old home. Should rents fall then housing values will follow, and that could happen two ways, less demand, or new home building technology. It could also happen that income will become so scarce that landlords will have to compete by lowering rents, very unlikely with rising inflation. If I was a investor with a portfolio of income properties I would be feeling pretty good right now.

the trend has been higher home prices and low yields on alternate investments. So you can accrue gains on the home value teax free while avoiding high transaction costs. And why sell if you are then stuck trying to get a decent yield on a new investment. At least you know your home, neighborhood, etc., and can always move back in if you have to… When home prices start to decline and yields increase, there will likely be a spike in for-sale inventory.

In South Bay (SF Bay Area), a year ago, you couldn’t find even a single one bedroom for under $1800 just a year ago. Now, everyone, regardless of how big their one bedroom apartment is have to price the one bedroom apartment at $1795 if they want to find a tenant. And of course even at these prices, I have seen 3-4 Indian men working in tech living in these one bedroom apartments. So much for higher rents. Despite all the numbers real estate industry want to give us, rents are going down. And right now is the best season. Between Aug-Feb they were begging for renters. Here’s a link to craigslist for one bedroom under $1800:

https://sfbay.craigslist.org/search/sby/apa?max_price=1800&min_bedrooms=1&query=-roommate+-share+-master+-private+-furnished+-cottage+-law&hasPic=1

Oh, by the way just rented a one bedroom for only $200 above the rent that I was paying for a studio that I used to live in. The apartment is twice as big. And they didn’t even do a credit check or anything. As soon as I walked in, they were so happy to give it to me since it had been sitting empty for 3 month. A year from now, the landlord’s begging for tenants will become much more pronounced as their apartments sit empty for 6 month. So much for your theory of higher rents :).

Actually the link that I added was a filtered one; this is the real link to see how many one bedroom apartments on on the market for under $1800. Note that many of these are buildings which have 4-5 vacant one bedroom, but they have only one posting: https://sfbay.craigslist.org/search/sby/apa?hasPic=1&max_price=1800&min_bedrooms=1&availabilityMode=0&sale_date=all+dates

Pat, it is all dependent on each individual’s situation of course, but my analysis (based on Seattle area and WA taxes) is that renting is actually a better deal than buying right now with the following assumptions:

1. Decent savings (at least a 10% downpayment)

2. Decent income above median

3. That the housing market is at a ten year peak right now

4. That your investment returns will be about 6% a year

You buy real estate because it might appreciate.You rent real estate because it might go lower. Casino never closes

(except 2008).

When the everything bubble bursts, it will be glorious. No debt, and not invested in any market.

Ready Player One.

It’s sure been long in the tooth but it sure feels like it’s getting close Charles Nenner on Greg Hunters site is calling for DOW 5k

Charles Nenner has been known to be wrong before. We’ll see Dow 300K before 5K.

Got popcorn?

>When the everything bubble bursts, it will be glorious.

While a correction is long overdue it will be painful for the average families on main street who are over-stretched. This is probably half of the people where I work, and I am not in bubble territory.

I would like to see, at a minimum, 7% (which used to be considered a bargain back in my mortgage days). Then, people might actually have to evaluate debt and the rampant consumerism passed off as an economy in this out-of-touch era.

Next….tax factory robots the same rate that people have to pay income tax. Use the money for education and real infrastructure financing.

regards

Sounds fair to me.

In most of Seattle, I can accurately state that it no longer makes sense to buy a home to rent it out. With the increases in interest cost and real estate tax, and the stagnation in rental income, the rents will not offset the costs. Throw in the costs of attracting renters, maintenance and property damage, etc., and it’s a clear losing proposition unless there is decent appreciation, which is nothing you can bank on.

I assume we’ll see less investor demand for single family housing going forward, and that’s been a big part of it. Better to simply put your money into a treasury or CD if you want steady income.

I found that most investment properties are sold to cash buyers (I’m relating to single family / duplexes). The properties I invested in were bought for cash. So the rising interest rates where I have invested would not have much impact on rentals purchases. The competition was always against another cash buyer. In California it was brutal, so much cash bidding for a single property. So many buyers willing to accept 4% returns. I wasn’t one of them so I moved investments out of CA.

But the rising rates may in fact fuel rent increases in the future.

Investors borrow at the institutional level. Large investors issue bonds or get large bank loans secured at the institutional level. Then they use the proceeds to buy a property. So yes, there is leverage and debt associated with the property, but it’s just not an individual purchase mortgage, and the deal looks like a cash deal.

When Blackstone bought 45,000 single-family homes out of foreclose to rent them out, it raised funds at the institutional level to do this. It also securitized the rent payments for more funds. Then it sold the whole thing to the public (REIT IPO), and that REIT is now going through Wall Street for its capital requirements.

Purchase mortgages are only for individual homebuyers or mom-and-pop investors.

Always wondered what happen to all the new housing that was built durring crisis 1, then sat empty. This good example where some of the supply went and more notably, how its funded/leveraged. Insightful comment. Thanks.

Blackstones’, “Invitation Homes INVH, -0.17% is the leader in the single-family rental space, with about 82,000 homes of the roughly 200,000 held by institutional investors. The stock has a buy rating among FactSet analysts and a target price of $25.86, 14% higher than its Wednesday trading levels.”

https://www.marketwatch.com/story/is-the-reit-bloodbath-finally-a-buying-opportunity-2018-03-28

In other words “cash” buyers aren’t special because of anything having to do with cash.

“Cash buyers” are special because their source of funds doesn’t add a third party whose approval is required to complete the transaction. This could be because the source of funds is the buyer themselves. Or it could be, as Wolf described, because of some large scale multi-transaction funding scheme.

“Cash buyer” sounds nifty, but “no-lender-contingencies buyer” does a better job of describing the important distinction.

CDs for the win. Or treasuries. Because they don’t call you to report that the toilets are stopped up. And it’s 3 am on a Sunday morning.

If you can’t write a check to pay for it, you can’t afford it.

https://www.esquire.com/lifestyle/money/a19181300/nassim-nicholas-taleb-money-advice/

Debt free,

That was a great article and thanks for sharing! I’ve always enjoyed reading Taleb’s books and speaking engagements, although somewhat arrogant.

From Taleb’s article:

“There’s nothing wrong with being wrong, so long as you pay the price. A used-car salesman speaks well, they’re convincing, but ultimately, they are benefiting even if someone else is harmed by their advice. A bullshitter is not someone who’s wrong, it’s someone who’s insulated from their mistakes.”

Sounds like he’s describing real estate agents and mortgage brokers. ;-)

I’m sure there are some out there, but I’ve never met a RE agent or broker who states that housing is in a bubble. Only one has said a “little frothy.” Here on the Front Range, prices have skyrocketed. I guess I need to drink the kool-aid and put my head back under the mattress!

> If you can’t write a check to pay for it, you can’t afford it.

Oh I can write a quadrillion dollar check — just watch.

Now, whether it bounces or not, that’s something else entirely… :)

Although “I” can NOT afford it, somebody else could still PAY it for me.

This is the mentality behind the wealth transfer, the mentality of speculate on borrowing to take position and off load later at higher price for the next sucker.

This way, “affordability” no longer matters,

what matters is the “trend” of prices, and the the psychology of next sucker.

The best part, with low down payment and securitized loans, both lender and the borrower has NO SKIN in the game. If they win, they make money, if they lose, borrower walks away without much penalty and lender is fine since they just make loans and they do NOT carry loans. Fanny and Freddy and who else hold those securities eat the loss.

I know in this cycle, the W2 borrowers paid more money down so there is some skin in the game. This week, Freddy said 3% down without income verifications. For wall street land lords, I am sure they have many more ways to diffuse the “skin” in the game to somebody else through IPOs and securitizations, insurance and derivatives.

Well looks like the Fed is pausing. They are leaving rates unchanged. Going to reverse direction soon?

This is not a pause. There will be 4 * 0.25% rate increases in 2018. Learn that the FRB now only raises rates at those FOMC meetings that have press conferences scheduled afterwards: Mar, Jun, Sep, Dec.

CalculatedRisk blog is speculating today that FOMC will start adding press conferences to all 8 yearly meetings. If they do, I think the motivation is to scare Wall St into understanding that FOMC is serious about rate increases, and will be open to raising rates at ANY meeting.

Rates,

Nope. The Fed did exactly what I said it would do. and what everyone said it would do. In this cycle, the Fed has been hiking only in meetings followed by a press conference. There are only 4 of those meetings a year: March, Jul/Aug, Sept, and Dec. Next rate will come at the Jul/Aug meeting.

I explained this in my article on Friday. Here is the relevant paragraph from my article, which the FOMC statement validated today:

“But for now, the Fed remains on its track of only hiking rates at meetings that are followed by a press conference. There are four of those meetings a year. The FOMC’s meeting this week will not be followed by a press conference, and therefore I don’t expect a rate hike – a rate hike during that meeting or any non-press-conference meeting, would be a “monetary shock.” And this Fed is not likely to dish them out, especially not with four of the seven slots on the Fed’s Board of Governors still being vacant. But I do expect a word or two about inflation approaching its target.”

https://wolfstreet.com/2018/04/30/consumer-spending-holds-up-fed-favorite-inflation-gauge-spikes/

Thanks Wolf. Maybe we’ll see more fireworks this June then.

But the QE wind-down continues without waiting for a press conference…

Yes. I’ll post my monthly update later today as soon as the numbers are out.

Meanwhile, the usual corporate media touts and shills are trying to convince the last of the retail investor muppets to place their bets in Wall Street’s rigged casino.

The media can be counted on to cheer on two things: the economy and war. On those two issues bipartisanship reigns in the MSM. They may hate Trump but they are not talking down the economy. And the only criticism the guy gets when he bombs someplace is why he didn’t bomb it more. Most other issues are fair game. War and capitalism, not so much.

Many “homeowners” are going to learn how ephemeral home equity is during the next downturn. They will discover the canonical equation of accounting the hard way: assets = liabilities + equity. Asset prices are flexible while liabilities (loans) are not.

Shouldn’t the equation read this way:

Equity = Assets – Liabilities

I think that Debt Free is trying to tell us that many people will soon have negative equity.

This is such an important point that home buyers don’t get. They chase interest rates because when they buy a home they are buying a monthly payment without thinking critically about the future. They think of it like rent.

If rising rates bring a decline in home prices, many many will be underwater. Whereas last housing crash we were in a declining rate environment. Interesting time ahead…

Or buy shelter for family for the next 30yrs.

You people make it all too complicated.

Which is better: rent or buy?

You buy when the total cost of buying a property is less than the cost to rent. Plus if you get lucky when you buy and have some capital appreciation then the cost goes down.

Here in Oz the interest on your principal place of residence (PPR) is not deductible from your income, but there is no capital gains tax on the sale if you have lived there for over a year. You can, of course, only have one PPR.

Interest and other costs on an investment property are deductible from your regular income. If the costs are greater than the rental income from the property then you have a loss and can deduct that from your income – any and all types. They call that ‘negative gearing’.

As with other areas the government has also changed the rules for depreciation and other costs associated with these types of properties recently.

With house prices soaring here and in some part as a result of that ability to negative gear, the capital gains has more than offset any losses from renting the property out.

Lastly, we suffer from that dreaded transaction tax called stamp duty which adds a huge cost to the buyer.

On a A$750,000 house with no exemptions that stamp duty adds a cost of about $40,000 to the price of the house. On a A$1 million property it is A$55,000.

To sell and then buy a A$1 million property here the transaction costs will probably be around $100,000!!!

“when mortgage rates hit 6%?”

I lol’d…….the FED will never lat that happen.

We live in fakesville……there is no price discovery in anything!!

The Fed wants it to happen.

“For now, demand for mortgages continues, as homebuyers are trying to make deals before rates rise even further.”

Insanity in the real estate market continues. An owner-occupied house is a zero-coupon bond of unknown maturity and unknown par value, that for many buyers requires borrowing on margin, and has steep transaction and carrying costs. There must be a heavy emotional component involved, i.e. FOMO=fear of missing out.

Inevitably, sanity will reign and the margin calls will come.

Or a place to live.

Not quite zero coupon, the difference between monthly costs of ownership (include RE tax, interest, repairs etc) and rent on an equivalent property is the coupon. Definitely agree maturity and par are unknown.

It’s also has a high geographic risk, a major earthquake/hurricane your city could destroy your investment in your house. Even a single large-cap stock is relatively immune to this. Accordingly, this housing “Bond” should sell with a pretty large coupon!

If you look at Seattle on Zillow you see 852 homes for sale.

There are 4 foreclosures, 21 foreclosed, 189 pre foreclosures, and 5683 for rent units.

This is after 10 years of abysmally low interest rates. What direction do you think is next?

IMHO I think that the 2008 RE crash is still winding down, and isn’t over yet.

I live in the Philadelphia area, and know a number of people who “traded up” in 2006 and 2007 who are still underwater after the 2008 crash. Two or three are still unable to refinance their original mortgages (yes plural, a second to get around PMI,) since they are still underwater with current mortgage amount vs appraised value. Several others are unable to consider selling due to purchase price + improvements (usually financed with a HELOC,) that would amount to a high 5 or 6 figure loss.

And a quiet but constant number of foreclosures are keeping prices depressed. IMO this is the big banks slowly releasing the foreclosures that have been on the books for almost a decade that would have crushed the them if released all at once.

I can’t imagine how anyone who can do arithmetic would consider buying a 600K to 700K house with less than 10% down or make improvements that were more than 15% of purchase price within 2 years of the purchase.

I commented similarly a few days ago. I know quite a few families – you would think upper class by their lifestyle – who cannot sell due to tax liens, poor credit so they can’t buy if they sell, or their home is heloc’d to the point they have no equity. They cannot sell because they have no better or equal place to go. Another reason I theorize as to such low housing inventory.

Wolf,

Just of out of curiosity, what drives the ‘points’? Just some spread function over rates (i.e. as rates go up, points will also increase)?

““Points” – the upfront fees, such as origination fees, that are usually rolled into the mortgage balance – rose 4 basis points during the week to 0.53% of the mortgage balance (mortgages with 20% down), after having already risen 3 basis points to 0.49% in the prior week.”

“Points” are additional fees that are attached by lenders and others to originate and process the mortgage. In a very competitive market, you might get the points waived. In other markets, points might be 1% or higher. Hence the current average of about 0.5%. They’re part of the profit model of the mortgage industry.

It’s like a new car dealer charging you a “documentation fee” or “doc fee” of, say, $600. It just shows up on the buyer’s order. And they didn’t tell you about it in advance when you negotiated the price. It’s just additional dealer profit. You can often negotiate it away.

Points of 0.5% doesn’t sound like much, but on a $1 million mortgage, it’s $5,000.

At least the rates aren’t like Argentinas at 40%.