Everything spikes.

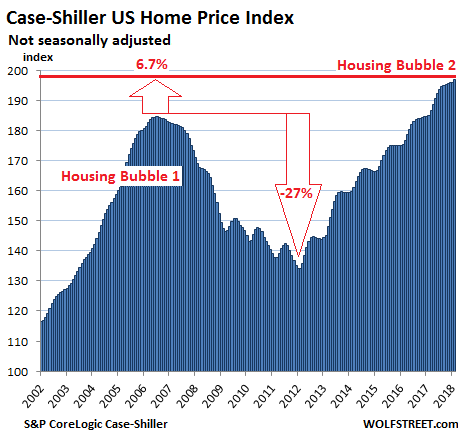

Prices of houses and condos across the US surged 6.3% from a year earlier (not seasonally-adjusted), according to the S&P CoreLogic Case-Shiller National Home Price Index for February, released this morning. The index is now 6.7% above the crazy peak of “Housing Bubble 1” in July 2006 just before the hot air hissed out, and 47% above the bottom of “Housing Bust 1”:

Real estate is local though prices are also impacted by national and global factors — such as monetary policies and offshore investors who consider US housing as an asset class and escape route — as well as by local factors. Together they create local housing bubbles. As local housing bubbles accumulate, even as some housing markets remain in the doldrums, they turn into a national housing bubble, as depicted in the chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release is for December, January, and February. The index, based on “home price sales pairs,” compares the sales price of a house in the current month to the last transaction of the same house years earlier. The index then incorporates other factors and uses algorithms to arrive at a data point. The index was set at 100 for January 2000; so an index value of 200 means prices as figured by the index have doubled.

So here are the most splendid housing bubbles in major metro areas in the US:

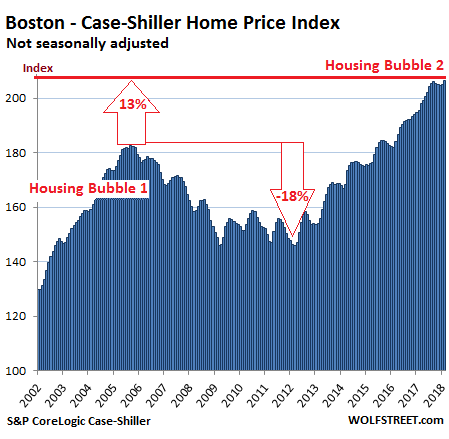

Boston:

The Case-Shiller home price index for the Boston metro jumped 0.7% on a monthly basis, to a new record, after two months of increases that followed three declines in a row, that had followed a 22-month surge during which the index defied not only gravity but also normal seasonal variations. The index is up 5.7% from a year ago. During Housing Bubble 1, from January 2000 to October 2005, the index had skyrocketed 82% before dropping. It now tops that crazy peak by 13%:

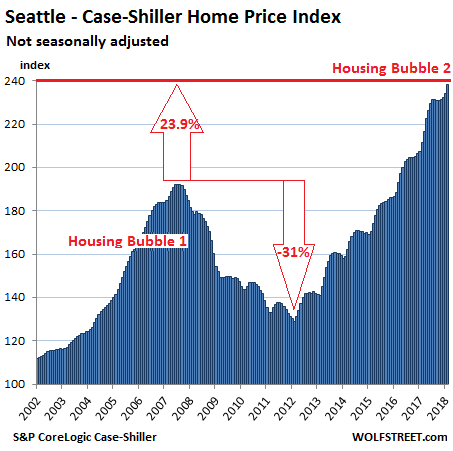

Seattle:

The Seattle metro index jumped 1.7% on a month-to-month basis to a new record. Late last year, it had experienced the first monthly declines since the end of 2014. But that was just a seasonal blip. The index soared 12.7% from a year ago and is now 23.9% above the peak of Housing Bubble 1 (July 2007):

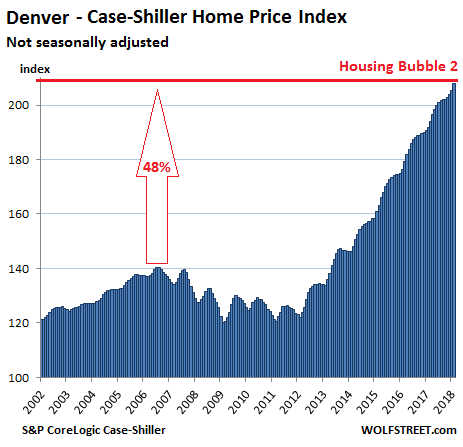

Denver:

The index for the Denver metro spiked 1.2% on a monthly basis, the 28th consecutive increase, surged 8.4% year-over-year, and is up 48% from the peak in July 2006. What a relentless ascent since 2012:

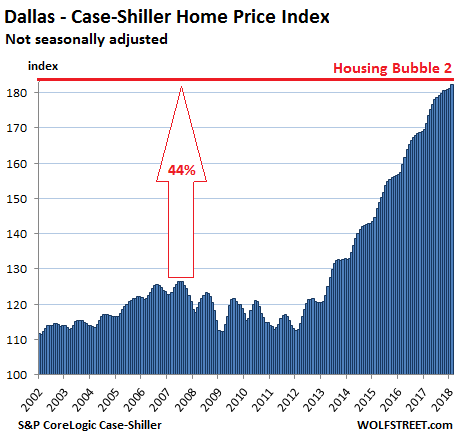

Dallas-Fort Worth:

The Dallas-Fort Worth metro index rose 0.6% on a monthly basis, its 49th consecutive increase, and 6.4% year-over-year. Since its peak during Housing Bubble 1 in June 2007, the index has surged 44%:

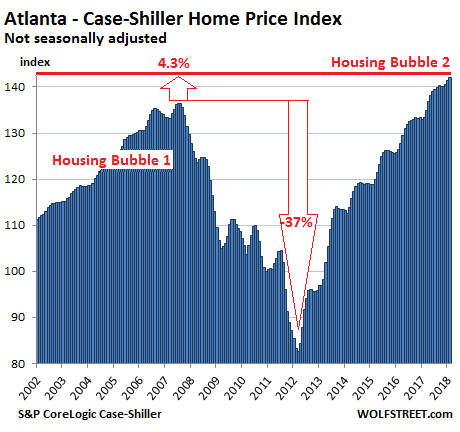

Atlanta:

The Atlanta metro index, after going through a seasonal four-month flat spot, is on the rise again. It ticked up 0.4% on a monthly basis and rose 6.5% from a year ago. It now exceeds the peak of Housing Bubble 1 in July 2007 by 4.3%, having surged 72% since the bottom of Housing Bust 1 in February 2012:

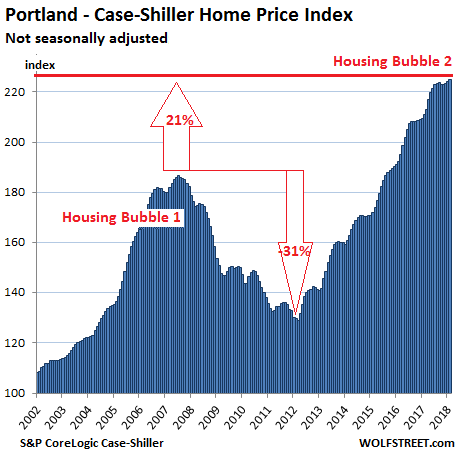

Portland:

The Portland metro index, which had been about flat for five months last year, has now risen three months in a row, to a new record. The index is up 6.7% from a year ago and is up 21% from the peak of Housing Bubble 1 in July 2007. It has ballooned 125% since 2000:

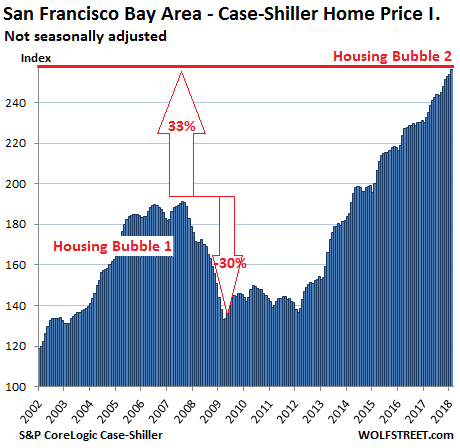

San Francisco Bay Area:

The Case-Shiller home price index for “San Francisco” covers the counties of San Francisco, Alameda, Contra Costa, Marin, and San Mateo, a large and diverse area that includes the city of San Francisco, the northern part of Silicon Valley (San Mateo county), part of the East Bay (the counties of Alameda and Contra Costa) and part of the North Bay (Marin county). The index surged 1% on a monthly basis and 10.1% year-over-year. It’s up 33.4% from the crazy peak of Housing Bubble 1, 93% from the end of Housing Bust 1, and 156% since 2000:

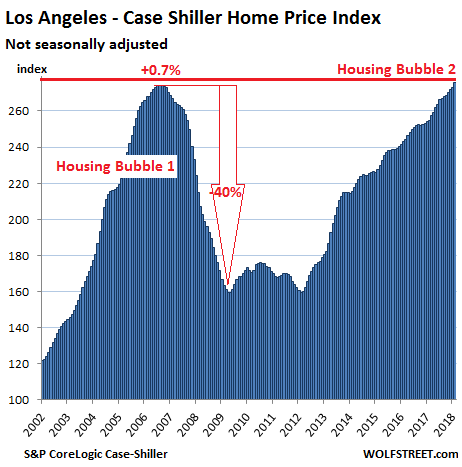

Los Angeles:

The Los Angeles metro index accomplished a major feat: it set a new record for the first time since July 2006. It jumped 1% for the month and 8.3% from a year ago. During LA’s Housing Bubble 1, home prices surged 174% between January 2000 and July 2006. The the subsequent crash was nearly as steep. The index now exceeds for the first time the peak of the housing insanity in 2006. The chart for neighboring San Diego looks nearly identical, though the absolute numbers of the index are a little lower.

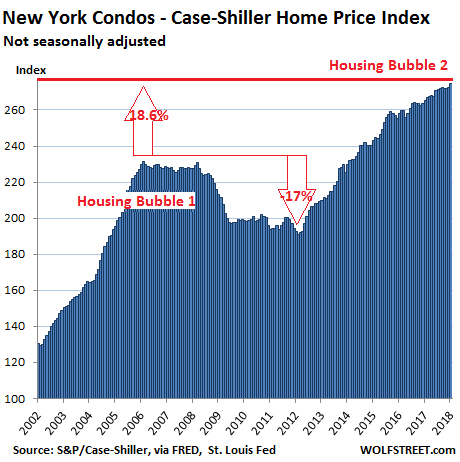

New York City Condos:

Case-Shiller’s index for condos in New York City rose nearly 1% month-to-month and is up 3% from a year ago. From 2000 to February 2006, it soared 131%, and then declined. But QE kicked in, and so did the bonuses on Wall Street, and global investors arrived too. By 2012, the condo market was rising again. The index is 19% above the prior peak, having surged 175% in 17 years:

Did the individual houses and condos underlying the charts above get bigger or nicer as their prices surged? Nope. They got older. That’s all. This type of home price inflation is a monetary phenomenon where the dollar loses its purchasing power with regards to homes, which had been the Fed’s well-communicated plan since late 2008. Since there has been little wage inflation, the value of labor, denominated in those dollars, has been crushed with regards to housing. Hence the current “affordability crisis,” or as it’s now called in many cities, “housing crisis.” Asset price inflation is a free lunch only for some. The others pay for it.

And if this doesn’t suit the millennials, who’re now entering the housing market for the first time, they can go to the Fed and complain. Read… This is How First-Time Buyers Get Squeezed by Rampant Home Price Inflation

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

Can you show what happens with the property taxes over time too. I think the property tax take does not go down ever, just up.

I am interested in see the data if you can show that aspect of the housing market

If the house price goes does, so does the property tax.

LOL. I wish it were that simple. I had 3 houses on my street that could not sell for years and at least another 3 in the neighborhood (I still have one that is two doors down and that has not sold for over 5 years despite being renovated and asking market rate per square foot). De facto evidence that we might need a re-assessment, right? I was told no – the tax assessors records don’t include houses that don’t sell or are vacant. You let me know when you get the rollback….

Not necessarily. In many markets House prices can move lower and municipal, county or township real restate taxes can and often do move higher.

The reason for this being “assessed value formulas” often determine real estate taxes, and NOT market value.

With City or County payrolls continuing to increase and the responsibility to pay pensions and benefits of all those employed therein, it is likely that the ‘golden goose’ of property taxes will be used to help pay the entire municipal workforce and their benefits and pensions.

Property tax rates in Seattle are up 43% in the last few years, so even with the increase in value, the total taxes are up even more.

In south Florida the property tax is determined by the purchase price. When the market crashed it affected the tax base as homes were purchased out of foreclosure. The upside is restricted to not more than 3% a year, of the tax.

James, you must be referring to what goes on in Canada–property taxes never go down.

Property taxes are based on the assessed value of each individual home, annually. If property prices go down long enough, the assessed value should drop too. I don’t know if a two-year downturn would be long enough. I went through long-term housing bust (Tulsa, OK late 80s into 90s), and the assessed values actually went down, though you might have had to nudge the assessor’s office a little every year. This doesn’t stop the local government from raising property tax rates. And then overall property taxes might rise though assessed values dropped.

I am actually house hunting in a bubbly part of the country. Hoping to wait as long as we can to purchase to see how things play out but our lease ends this summer so we are just looking. We are using Redfin which allows you to follow homes showing you when it goes under contract, when it sells and for how much and any other changes. I randomly track some of the homes that are listed in our price point (under $300k, appeals to downsizers and first time buyers). In Feb, homes were selling in a couple of days and any time we toured the home there would be several other buyers there too. Not happening now when we tour and I have been getting several price drop notifications on some of the homes I’m following. This wasn’t happening a month or two ago. Also many of the homes are sitting longer. Not sure if just a fluke but this is the busiest buying time of the year so I’m surprised to see things appear slower, even if just a bit. Also, we are pre-approved for a mortgage and our lender reached out for the first time to us last week asking how it was going after not hearing from them at all since our pre-approval in January.

The crash is going to be even more spectacular than the bubble It always is

The tungsten filament of an incandescent light bulb burns brightest right before it goes out.

haha…i love it!

And nothing dulls faster than the cutting edge…

Full on FOMO mode here where I am, multiple offers above house list price within hours. Of course its not because the house is actually worth that much.. its all physiological fear of missing out…mixed with easy credit.

For once, we canucks are ahead of you, yanks.

FOMO is now a forgotten word in Big North.

Here in Northeast USA, where I have lived in a number of Cities and Towns — and however your initial assessment is calculated (it varies) — YOUR TAXES ARE STABLE UNTIL A REASSESSMENT EVENT OCCURS. Prices rising in the open market have no effect — except to possibly act as a trigger for City/Town leaders to try to schedule an assessment event.

Realistically, under the current regime, there is no way to measure and apply “market-based” price increases to your assessment. No way !

Think about it — if housing price appreciation could trigger a reassessment event — then the proles (me, specifically) would demand a reassessment down if home prices decreased. As if that would ever be allowed !

Robert_D

Having lived in eight states from coast to coast and all places in between ; No two states in the Union treat property taxes the same . Therefore do overgeneralize by applying your personal experiences within the state you reside in to all others .

As an example ; In Colorado property assessments are annual especially in the verging on the insane bubble we’re in .

As well as in Colorado you the homeowner can demand a reassessment if you either feel the assessment given is over estimated .. or if you can prove your property values have gone down

Good luck with that.

First Ferengi rule of acquisition “Once you have their money, you never give it back.” In other words, once you set the tax, you never reduce it; that’s the first thing politicians learn, unless they benefit from it.

Your last paragraph describes perfectly California Prop. 8 (the 1978 version, not to confuse with the 2008 model.) Property that has declined in value may be reassessed downward but then is reviewed annually. Of course that which has appreciated upward is never reassessed unless sold thanks to Prop. 13. Commercial property can avoid reassessment even when sold I believe via the mechanism of selling an interest in the shell company holding title w/o selling the shell company, sorry “LLC.”

From the more than you want to know department:

https://www.boe.ca.gov/proptaxes/faqs/prop8.htm#1

I owned a house–recently sold–in San Jose, CA for 22 years. The property was reassessed every year; always upwards IIRC. Prop. 13 merely puts a cap on the rise in assessed value–think it’s 1%/year, max–it does not stop it.

California resident here. State income taxes, property taxes, sales taxes, toll taxes, taxes up the wazoo! whoo!!!

Socal best weather in country though.

Sure is tempting to sell everything right now and sit…. Of course, Murphy would surely raise his hand and spank my @#$&, so I’ll just play it safe, and try to be ready when the next one hits….Maybe I’ll finally be rewarded for saving!!..

Hopefully there’s at least a correction by the time my kids are ready for there first home. Makes me nervous just watching other people fork out the mortgages that it takes to buy ….

So Wolf .. re; the header ” Everything spikes ” … though in essence that is true … we on the Front Range / Denver – Colo. Springs – Ft Collins metro area keeping asking the question … when the hell is our ludicrous verging on the insane bubble going to finally spike … and then burst ?

Because in all honesty every time someone predicts the tipping point has finally been reached … the damned market despite all logic and the facts on the ground keeps going up … and up … and up

Any thoughts ?

You summed it up well.

I’ve been a bear for the longest time. And I am thinking it will be a while before it bursts. Just look at Google’s result. Muppets have so much money now, they are clicking ads at a pace that indicates that everything is going great.

I know it seems to defy logic because the absolute numbers are so large in SF, SV, Seattle, LA, etc, but based on pure inflation-adjusted affordability regressions we’ve only recently gone from “above normal” to “damn high”. We are still quite a distance from the unaffordability metrics reached during the 2006 bubble. Couple that with the lack of supply and I suspect this summer will be the peak frenzy.

However, it is an extremely thin market. If we get a surprise downturn in the economy I think the market will flatten (not collapse) in real terms in a hurry.

“Affordability” metrics always include mortgage interest rates to arrive at a monthly payment, and these rates were historically. But they are now rising, and are far from done.

But if interest rates go up, won’t that discourage short term flipping and thus help push down home prices? But not rentals as more rent is sucked out to pay purchase interest?

You know there is an interesting dynamic in tech places like the Bay Area, and beyond, between house prices, mortgage affordability and job-hopping. Question, how likely is one to hop jobs in Tech, to say, save your career, if one has a 1.2 or 1.5 million dollars of debt hanging over ones head?

Wow, I remember when “job hopping” was considered a bad thing.

Job-hopping is a way of life in tech. I don’t think you’re supposed to stay with any one company longer than 3 years, and 3 years is kind of stretching it.

hahah @ 3 years. I’ve worked in entertainment/tech for the past decade. Broke my 2.5 years last year.. that was a first. The average is closer to 6-12 months, emphasis on the 6.

The positives are tied to variety and wage increases and possibly travel if you think its a plus. The negatives, forfeit starting a family, and buying the traditional “home”. Would stick with investment property instead, because of the nomad work/life.

That is the reality of “older millennial” such as myself. Probably a real reason why people in their mid 30s are postponing having kids.

Btw, Wolf, thanks for the update. Looks like LA has a little more room to grow unfortunately. In a long enough timeline, you will be vindicated on your bearish views. Lets hope its sooner rather then later.

We learn nothing from history apart from the fact we learn nothing from history…however I’m sure there are plenty [invested, natch] who could offer up many reasons why it’s “different this time”.

What a weird world where the greedy, reckless, downright foolhardy and the basically financially illiterate are in fact rewarded with easy profits, because lots of people like them have cheap and easy credit thrown at them.

Those who are ‘sensible’ it seems are not required at the party and can only sit on the sidelines and wonder at the insanity of it all. And just maybe buy some precious metals as an insurance policy..!

Surreal is one word that sums it up for me.

Take comfort in the thought that 50% of today’s stock market and bond wealth (i.e., ill-gotten wealth) will never be spent on anything. It will simply evaporate in the next crash.

“POOF” .. Like a windy Uranusian fart, this gaseous, flatuently fake economy needs to pass !

I know I’LL feel better, the FANGs however ..

“We learn nothing from history”

Well what I learned from history was that if the RE market crashes the bailouts will come and will make many of those whole who bought into the bubble.

And I just had a discussion with a person that was the exact same discussion I had 10 years ago…….and that was……”just buy and if the price drops just walk away”. This was the lesson learned. Also if the crash is big enough and lasts long enough you just might be able to live mortgage free for years, that’s the other lesson many were taught in the last crash.

So I think people do learn from history, just maybe not the lesson they should be learning from.

I think you’re correct. I hate to admit it but I’ve been tempted to do this myself. However, what stops me (besides a sense of morality) is the fact that if everyone tries this approach this time it won’t work!

They require 20% down payment now.

I am selling into this absurdity.

20% DOWN is Not Required.

Buyers only need 3.5% down with FHA.

As low as 3% with conventional FANNIE MAE, FREDDIE MAC).

0% Down with VA and some teacher/first responder loan programs.

Seller can pay UP TO 6% of Buyer’s fees, prepaid items (2 months of taxes, 14 months of insurance), appraisal, survey, etc., etc.

Illegal immigrants can get loans again with no SSN as lonf as they have 10% down and are willing to pay 8-12%.

No liar loans yet, But wait…

Also 0% down on USDA rural loans, available in many close-in suburban areas near major metros.

Sold a house in 2013 in central Mass, and another in Greenville, SC in September 2017, both with 0% USDA financing.

So US government backed loans are the principal ones at 0% with no risk to the bank lenders…yet, it is a big risk to buyers as they have no equity if a crash occurs.

While I personally would like to see an end to this insanity it will not be any too soon in coming. If one assumes SF bubble symmetry and that we are at the top you can assume we will reach the bottom again in 6 years or 2024. That assumes that its not different this time.

You forget about the QE unwinding. I recently spotted a bike that was green in color for renting. Apparently by a company named limebike. The was moved a couple of blocks in the last 2 days since it was obstructing the walkway. They’ve recently closed series B funding at 225M. This in short is a summary of what passes for innovation now. I think the fed can keep pumping but there not many ideas to match the money. IMO, they’re now scratching the bottom of the barrel.

This means employment will not rise but probably fall. Notice the pump and dump in progress in companies like Zuora— they went ipo last week. There are a bunch of companies raring to get out. Their investors want to see returns, so the rush to the gates. I think the top brass will take the money and run. The employees will be thrown out when stock buyers demand cost cutting.

Now add the h1b fiasco. H1b is allotted through a lottery. Doesn’t matter how good the candidate is. Students are having a tough time from going to h1b from OPT/CPT. Those who want to change jobs need to go through premium processing to get a chance to change jobs, which everybody’s doing which in turn means the line is backed up. Back in Obama’s days, spouses could come to US with zero technical education, join a body shop and get the work visa. That’s now gone, afaik. Most people in the market I see in the market for new homes and new rentals are usually from india now. Trump is suggesting tightening the normal h1b as well to stop body shoppers. The point is that even if jobs are there, the inflow will be severely curtailed. Throw in the green card application process and people will stay with an employer for a while. During Obama’s days, these same people were jumping jobs in the hunt for riches. Now they’re in lockdown mode, at least more than before. Staying with the same employer means no hikes and getting locked out of the home buying.

Then there are the baby boomers who own most property in the peninsula. I am guessing the 2024 number you mentioned includes that factor.

If the economy tanks on top of these, you’ll probably see an opportunity sooner.

I wish Trump would listen to be because my plan would really resonate with his base (and a lot of his non-base). Here it is:

For every H1B you hire, you also have to hire an American at the same wage, even if they have no tech skills at all and just play Oregon Trail all day.

If that damned H1B is so talented and valuable, you’ll happily pay. This also encourages hiring Americans, and training Americans.

you can swipe one with a 20 buck bolt cutter. just sayin’.

but you can’t call it home.

Or, you can strip it of needed parts like wheels, hub and tires.

I think many rational people are fueling this bubble thinking there is safety in numbers. If enough people get burned by the bubble popping, the government will be required to bail them out. They are probably right.

Many rational people are also thinking that central banks have created a problem they cannot recover from. The only solution is to inflate the currency for many years to come (and seek to hide it in reported figures). In that environment, you have to own assets such as RE and stocks, not fixed income.

Unfortunately, the Fed and other central banks have created moral hazard through their perverse interventions. Reckless behavior is rewarded, good behavior is penalized. And for what – avoidance of a short-term healing recession?

The Fed’s actions are nothing short of irresponsible.

Bobber,

excellent summary. There aren’t any holes in your argument and it’s spot on. Here is the very best part of the entire missive.

“Reckless behavior is rewarded, good behavior is penalized”

those 8 words are all that one needs to remember.

“Economy is NOT about morality”. Paul Krugmen.

Because we are smarter than the mass, you should listen to our decisions about money and who should do what and buy what, it is the best for everybody.

“Americans should fear the 2% rich and intellect because they have NO skin in the game. If you want to decide to invade Iraq, your children should be in the army”. Nassim Taleb

I like your thinking Bobber. However, I think the key to the Fed’s thinking is different than – “And for what – avoidance of a short-term healing recession?”

They are scared to death of all the debt, coupled with the scary first world demographics. Deflation isn’t just a textbook depression-era phrase for them any longer. They see that the US baseline future growth is less than 2.5% based on population trends (mostly locked in place) and their timidity takes over. Now, I’d argue that adding more debt to a debt problem is not the correct solution, but then I’m not a central banker!

While bubble 1.0 imploded due to subprime mortgages, bubble 2.0 deflation will be characterized by non end user unit sales. This relatively new asset class (non primary single family residential homes) must take up a considerable portion of total inventory .

wait till 2023.

Here in Sonoma County “Days on Market” are lengthening and prices appear to have flattened.

Inventory is picking up, particularly on the high end ( $1.25MM and above).

About where we were last August, before the fires.

Tom,

I mentioned in a prior article on March median prices in San Francisco, that in February, the median condo price was down 7% year-over-year, under pressure from a lot of high-end supply from new construction. And the median price has been flat-ish (with noisy ups and downs) for two years. But then March blows the doors off all the numbers, even condos. You didn’t see this sort of March blow-out in Sonoma?

Days on market here really vary according to the price of the property. Some properties take forever to sell (What is wrong with them?) and others are gone in a couple of days. Average is 33 days which hasn’t changed for a long time.

$1 million to 2 Million dollar plus properties for living in and not the subject of any future land division potential on good streets go in a week or less. Those in the $800,000 – 950,000 area seem to take a little longer.

Those properties looking for developers in the $2 million range are not selling, but there has been a bunch of large, new developments that have take some of the demand out of the market. Prices in those are around the $1 million to $1.5 million area for townhouses/condos.

Three lots with 50’s era houses on them next to each other finally sold. It seemed that they took well over a year to flog. Price was A$1 million each for 750 square meters of land. Zoning changed and you can now put up 3 story buildings (or higher?) on them. Ten years ago you could picked them up for around $125,000 each or less.

Our vacancy rate in the area is a whopping 1.2% and there was a house that was put up for lease on our street at the end of last week. It lasted 5 days before being rented.

Prices in the entire suburb are up about 12% YOY.

Lee,

Please provide source, and links to the “Three lots with 50’s era houses on them next to each other finally sold.” That suggests they were recently sold properties.

https://www.realestate.com.au/sold/property-house-vic-berwick-125624910

https://www.realestate.com.au/sold/property-house-vic-berwick-125191002

https://www.realestate.com.au/sold/property-house-vic-berwick-125624906

“Situated in the Heart of Berwick area is about to be rezoned to RGZ2 (suitable for apartments) as part of the Berwick Health & Education Comprehensive Development Plan/ Berwick Village Structure Plan.”

These three were initially marketed and to be sold as a group at auction. They didn’t sell and were taken off the market for a while. Then they were put up for sale again as individual properties. They failed to sell and the signs came down.

They were sold on 16 March for A$1 million each.

Lee, just an off-topic question if you don’t mind: do you guys get snow down there in Melbourne during your winter season?

Lee,

These are Australian properties. The whole Article is on US real estate, and the particular discussion was about San Francisco Bay Area real estate; so, what is the connection? The properties that you have posted are not only Australian, and have been up for rent at $330/week for rent for years, and now all 3 have been sold together. Not such a good deal to buy a property at one million when all you can get out of it is $330/week. That gives you an ROI of 1.7 per year, not considering mortgage, repair, tax, etc.

RSD2,

Lee keeps us updated on Australian real estate — has for a long time. And occasionally on RE and other things in Japan.

I been house shopping in San Antonio and Atlanta cause I’m not sure where I want to go next with my job. I been surprised at the number of EMPTY McMansions I have gone into. Some have furniture, but it’s all a decorative. Many also require anywhere from 100-200k in repairs and upgrades…Prices super high, more so in Atlanta. I am super scared to buy!

Wolf, curious, what happened to Santa Clara county. How come the SF bay area index has excluded this? Curious to see how that is shaking out these days.

Case-Shiller doesn’t do an index for every metro. There are a lot of metros that would be interesting to look at on this scale, but that data is not available, at least not to me. This also includes current housing-bubble-metro Nashville…

Obviously that box nailed from 2x4s within two weeks worth $1.2 mil due to its proximity to the gold mine (FANG).

Last year my mother was going to buy a new townhouse in Independence, Mo . , a suburb of Kansas City and there were 5 new townhomes for sale and one had been on the market for over a year . This year she was able to purchase a new townhome from the same builder for 6 % more , and on her block there were 5 new townhouses for sale that sold within a month of moving in. Today I talked to the builder and he has to do a parade of homes show for 2 weeks in a house that is already sold and he won’t have any product built for 3 months .I have never seen so much building and construction in Kanasa City in my life as now and prices are following suit .What used to be the ghetto 15 years ago, now homes are being sold for 500k to 600k .I’m sure it’s nothing !!!

Say,you waited patiently for the RE bubble to burst.Then you bought a home sweet home for $120K.The only problem is that your home is surrounded by houses assessed at $250K.

You finish your paperwork and after 2-3 month you receive a letter from the local government stating that it was a distress sale and the ACTUAL value of your property is $250K.

I am not making this up.It happened more than once in 2008 in many Atlanta,GA suburbs.I read about in in a local newspaper.

And BTW folks-DJIA will soar tomorrow.

Not soaring yet. Dow down 128 points. That said, it could still soar later :-]

“We are not retreating.We are preparing to attack !”

“We are not surrounded,we are attacking in every direction !”

LTG Lewis “Chesty” Puller,USMC

This is by no means a criticism of Wolf; I know he lives by the numbers, and he has to get his numbers from available sources. But I don’t trust any of these numbers provided by real estate related sources (such as S&P CoreLogic Case-Shiller National Home Price, etc.). They say that YoY San Jose rent has gone up by 13%. I have news for all of you; landlords and property managers are starting to beg now for tenants.

In the apartment that I currently live, so many people are leaving; the way that is going, they will have at least half of the whole apartment complex empty by the middle of the summer. 2 of my close neighbors are moving out of States.

I was leaving in any case due to some noisy neighbor, but most others are leaving in droves because the stupid owner tried to raise the rent by just $100. I have a feeling she is gonna hang herself ???. How stupid can you be to try to raise rents in this environment.

Now someone tells me please how is it that the numbers from these real estates related sites says San Jose rent has gone up by 13% YoY? The numbers for house prices come from the same scums. Never trust them. Always go and see the reality on the ground for yourself.

This article was about home prices. About a week from today, I’ll post an update on rents, and San Jose will figure in this article. Rents have declined in most of the top rental markets in the US but have surged in a bunch of less expensive markets.

Wolf,

My point is that real estate numbers are exaggerated by these sources for good reason, whether it is rent or property prices and sales. They scare people that they will be priced out, and people run out and buy because they are afraid of missing out. Thus by providing inflated numbers, they guarantee the prices to go up for the next cycle, and they keep doing that till the bit crash comes.

It is called a self-fulfilling prophecy; they are masters of making up numbers and making public believe it.

My town in Iowa has been artificially inflating housing values over the last 5 years for property tax hikes. On house we were looking at was listed for $145k. Currently valued for taxes at $150k, 2016 was valued at $130k, and two years prior to that $116k. The wife and I are waiting to buy after the next crash like we did in Phoneix are after the last one. I managed to score my first house just before I met her in 2009 2800 sq ft 4 bed 3 bath for $120k. It was originally purchased new build for $306k.