Millennials can go to the Fed and complain.

Home prices have been surging in many markets, mortgage rates have been rising, and incomes have plodded along with little growth, and the disconnect is getting bigger and bigger. This is not a problem for well-to-do Americans who’ve owned a lot of assets and benefited from the rampant asset price inflation over the past eight years, but it is a problem for those trying to buy a home based on their wages, especially first-time buyers, which now include more and more millennials.

Freddie Mac reported on Thursday that its weekly average 30-year fixed mortgage rate rose to 4.47%, the highest since January 2014, which is still very low historically. On Friday, the average 30-year fixed mortgage rate for top tier borrowers rose to 4.58%, according to Mortgage News Daily, on a day when the Treasury 10-year yield surged to 2.96%, the highest since 2014.

This comes to the drumbeat of ballooning home prices [Update on the Most Splendid Housing Bubbles in the US].

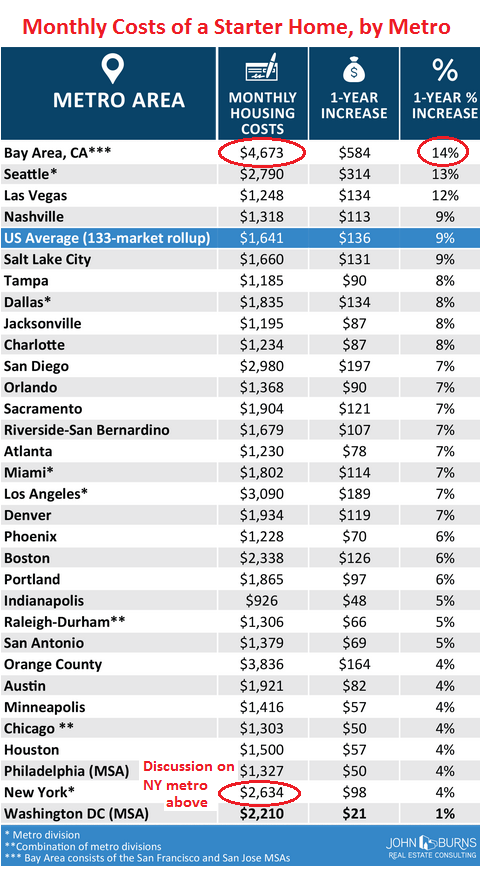

So, the monthly costs of an “entry-level home” on a nationwide basis surged 9% in March from a year ago, according to a note by John Burns Real Estate Consulting Senior Research Analyst Devyn Bachman.

The report defined “entry-level home” as one that sells for 80% of the median price (resale and new) in that particular market. It assumed a 5% down-payment and a 30-year fixed-rate mortgage for the remainder. The monthly costs include principal, interest, taxes, insurance, and private mortgage insurance. But they do not include maintenance and other costs associated with owning a home.

In the San Francisco Bay Area – a diverse area that includes San Francisco, Silicon Valley, much of the East Bay, and parts of the North Bay – the monthly costs of this entry-level home surged 14% in March compared to a year earlier, to $4,673!

This is the highest monthly cost of any major Metropolitan Statistical Area in the US. But this is based on the median price of a large and diverse area. In some cities within the Bay Area, monthly costs of the “entry-level home” are lower, in others far higher.

For example, in San Francisco, where the median home is $1.4 million, and the “entry-level home” $1.12 million, the monthly mortgage payment (interest and principal) would come to about $5,400 for an entry-level home. Property taxes would come to about $1,365 a month. Plus insurance and private mortgage insurance. So pretty soon, this “entry-level home” costs about $7,000 a month, or $84,000 a year, not including utilities, maintenance, and other expenses. If it’s a condo – and at this price, it certainly is a condo – the homeowner association fees will have to be added on top.

This is why even the median Facebook employee (not to be confused with its contract workers), making over $240,000 a year in total compensation before income taxes, is feeling the squeeze.

In the Seattle metro, the monthly costs of the entry-level home jumped 13% from a year ago to $2,790 – the second highest in the country.

The report finds that in the San Francisco Bay Area and in the Seattle metro, “home buyers have become overly exuberant.” To put it mildly.

In the vast and divers New York City metro area, the costs of an entry-level home inched up 1% to $2,634 – third highest in the country.

However, the median price in Manhattan was $1.1 million in Q1 and the average price was nearly $2 million, according to the Elliman Report. Within Manhattan, there are huge differences. In TriBeCa, the most expensive spot, the median sales price was $3.6 million, according to PropertyShark. In SoHo, it was $3.2 million, in the West Village it was $2.3 million. These are condos or coops. Talk about “overly exuberant” home buyers.

There simply are no “entry-level homes” in these neighborhoods. This is the case in many areas of Manhattan. So just forget it.

Of the largest 31 metro areas, 23 have an affordability problem that is “notably worse than the long-term norm,” the report finds.

So here’s Burns’ list of the monthly housing costs of the top 31 metros, in order of their year-over-year percentage increases. The San Francisco Bay Area is at the top with a 14% jump in costs. The New York and Washington D.C. metros are at the bottom with increases of 1% (I added the red marks):

“In conclusion, home buyers can afford less homes today than they could one year ago,” the report says. This is the effect of rampant asset price inflation. It hits real life in this way:

- The costs of housing will siphon off the new owner’s income that cannot be used for other things.

- Potential buyers are looking for housing further away, thus incurring the costs and hassles of longer commutes.

- Buyers end up with something even smaller (not as if homes in New York City or San Francisco are palatial in size to begin with).

- They’re looking for condos instead of single-family houses.

And starting in 2018, there will be additional costs due to the new tax law – on top of home-price increases and jumpy mortgage interest rates: the mortgage interest deductibility has been further reduced.

So first-time buyers, having missed out on the home-price surge of the past eight or so years – this includes most millennials – bear the brunt of the costs of this asset price inflation in the housing market. That lunch was free for some. But others are paying for it. And those folks, including the millennials, can go to the Fed and complain about it since it was the Fed that set out to “heal” the housing market after the Financial Crisis by purposefully inflating home prices – or more precisely, devalue the fruits of labor for buying assets.

Bonds, junk bonds, spreads, commercial real estate, leveraged loans, over-leveraged companies… all get named as risks to the banks. This is why “gradual” tightening will continue for a long time. Read… Now Even a Fed Dove Homes in on the “Everything Bubble”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Meanwhile many of them are moving to Nevada.

They sure are 45,000 new residents last year. Half from Cali. I’m here now and they are building literally everywhere and I see $60k trucks left and right.

Wolf,

No good deed goes unpunished. The problem though is this, if the bubble is deflated, someone is going to get hurt. That’ll largely be those people who bought in the last few years. The problem is, does that help enough of these millennials?

Worst case is we end up with a lost generation.

Not everyone who bought will get clobbered If they plan on living in the house for 30 years they should be fine

Current homeowners get clobbered as well – their houses will go underwater, so they can’t afford to move. Rents will fall, so they’ll have a negative cash flow if they rent out their home. Plus, they’ll be paying far more for their house than current market.

Think of buying a house as a sort of reverse annuity. Buy an annuity at the wrong time, and your payout is less than someone whose timing was better. Buy a house at the wrong time, and your housing costs are higher than they would be at a different time.

I am a homeowner since 1995, which has been paid off for years, but I don’t get clobbered – with the exception of property taxes.

Not having a rent or mortgage payment to make every month is fantastic!

This is all assuming that while the economy is tanking, Joe HomeMortgagePayer’s job keeps existing, there are no cut-backs on hours, no “temporary” layoffs etc.

In the last crash, a lot of people could not keep their homes because when housing crashes, a lot of the economy crashes along with it. Hence the term, “jingle mail” (mailing the keys to the bank).

Maint. $50

Cell $7

Internet 100mgb $6

Electricity +-$10

Root canal $200

Some expats enjoy life!

Not many marriages last even ten years.

“..but I don’t get clobbered – with the exception of property taxes.” How convenient for all the taxing authorities that property taxes rise in tandem with home prices. QE was a gift to bankers and bureaucrats, the nexus of which is the Federal Reserve.

That’s if they can keep a good job for those 30 years. That’ the major problem.

Mch – the problem is that the people who “have won big” have won big purely because of the Fed’s actions. In order to make them a winner, everybody else had to lose (millennials, elderly people with savings who have been robbed of interest income).

The “big winners” only became big winners because of government and Fed engineering and manipulation, and yet they don’t want to give that ill-gotten gain away. No, no, that just wouldn’t be fair (sarc)!

I’d disagree – interest rates plummeted to save the economy. This caused housing prices to skyrocket- people could afford the payments on higher dollar homes, so prices were bid way up.

The fault is the Republican “loot the pension funds to buy expensive weapons” mentality. Stop that, and many of our other problems become solveable

Interest rates didn’t “plummet”. They were pushed down by the Fed. The undeserved corrupt (at the top) were saved (and engorged like ticks). And the voiceless paid the cost.

But the starting point is corruption. Hot, dirty money bought political power to disassemble American factories and offshore jobs, wages, and value added to foreign countries, mainly China and to a lesser extent, Mexico.

To replace purchasing power that was lost from American incomes, the Fed and the Federal government went on a borrowing and printing binge. That is what inflated nominal asset pricing and destroyed the hope of millions of Americans.

Until and unless productive capacity and the attendant jobs, incomes and value-added get returned to this country, this insanity of beggaring the nation, will continue.

Economics cannot be separated from Politics. And Politics is Power.

You can look back through history and empires that engaged in continuous war often fell apart from within.

The war-making mainly drains the treasury but it also distracts from what might be desperately needed to shore up the internal situation. By the way, rough estimate of defense expenditure:

Department of Defense: $686B

Overseas Contingency (special war funds): $50B

Nuclear weapons: $18B

Veterans Affairs: $164B

That doesn’t include everything, I know. For instance, Homeland Security ($44B), DARPA ($3B), etc. Just the numbers I’ve listed get the U.S. very close to $1T in defense expenditure.

Feel free to fix up the numbers.

My point is that a smart electorate and a smart Congress could easily make a bipartisan deal to trim the defense budget, raise the social security start year, spend on infrastructure and investment, and still cut the debt significantly based on defense and soc. security changes. They certainly wouldn’t do a stand-alone tax cut for the wealthy and corporations.

RepubAnon,

I disagree with you completely. The RE market is so far away from free markets it’s almost criminal. Banks kept properties off the market for years so that the real value was never realized. I personally know a couple that lived mortgage free for 48 months all the while the bank paid their taxes.

the government IS the RE market. There is no price discovery anywhere in the financial markets including the RE market.

And then you go into a republican “expensive weapons” rant? WTF…..Obama dropped 26,171 bombs in 2016 alone. This is NOT a left right argument.

Ed

If I’m not mistaken deep cuts in defense spending would not cut the debt at all and it wouldn’t even eliminate the budget deficit for the year.

Not only can we not pay down the debt but even having a balanced budget isn’t going to happen . The huge tax increases or huge spending cuts needed would be political suicide even if military spending was drastically cut.

Meanwhile, the medical monopolies, though medicare and out of control forced “health insurance” alone takes up more than the defense budget and RE costs. Think about it. Kill the medical monopolies, and yes, you bring in a huge recession, but a short one, and then all of a sudden even RE becomes affordable to the average family at even today’s inflated costs. The average American families health insurance premium IS a mortgage payment, and in some cases a car payment combined. Then add in the huge deductible to even use it, and well, forget it. The “expensive weapon” of today is not from the Pentagon, it is at your local doctors office or hospital.

√

Is there an American MIC.

Undoubtedly.

Is it actually responsible for even a 1/3 of what it is accused of, and blamed for.

NEVER in a Million Years.

Don’t necessarily dispute this, but let’s face it, the govt picks winners and losers all the time. So, ill-gotten gains is the wrong thing to say, when student loans are forgiven, the govt is picking winners and losers. Do you see anyone really complaining about the ill-gotten gains of those students even though they made bad decisions?

What do you say to someone who bought their home last year who might suddenly see their value go down by however much should this bubble deflate. Ill-gotten seem to be a very strong word indicating some nefarious activity by the person who bought a home recently. How would they be any different from the student who have their loans forgiven by the govt.

@Mch. I wouldn’t say “ill-gotten”. But I am not wild about the trickle down methods of attacking the crisis, even if those methods have been good for my book. ;-)

Infrastructure spending back at the bottom would have been smart. Wouldn’t do it then but now it appears that we are using tax cuts and spending to prolong the bull.

Paper gains don’t build a future for the next generation but that’s where the focus seems to be in Congress (and the Fed, but that’s about all the Fed CAN do).

Here is what I will say to people who buy houses at high price and see price goes down due to “bubble burst”. If they are strong hands and their earnings can afford the house regardless of the price, I will say “congratulate on your home, you deserve it”. For those weak hands who borrowed money, and a recession for two years will kill their ability to maintain payment, and they can NOT offload the house to next sucker, I will say “Too bad you found the risk you are seeking, eat your loss and be smarter next time.”

Let’s face it, for the winners that government picked, those who got rich by sitting on a house collecting money showered from federal reserve, or students whose loan was forgiven after they partied their years away in college, they will be contributing to the moral decay fostered by the government and receive no respect from fellow citizens. They will contribute to more dividsion, more finger pointing, more hatred.

“Do you see anyone really complaining about the ill-gotten gains of those students even though they made bad decisions?”

YES.

1. All those that scrimped and didn’t spend on normal things in order to pay off their student loans.

2. Those that actually used the money from the student loans to pay school fees, books, tuition, room and board at while at school instead of blowing it on booze, drugs, trips, and cars.

3. The current taxpayers who have to pick up the tab for those that don’t pay.

The .gov controls the mass like Mafia controls prostitutes.First make sure you suck up all of their earnings through rent. Second you put them on drugs, so that they can NOT escape. They have to come back to you asking for another dose. Debt is the drugs for government. Once the mass is on debt, they FEAR the price goes down, they support all the bailouts, they support money pritnting, they support sucking the children dry without a future. This causes the divide and competition among the mass and the mass h always “return” to the government for more law, more policy, more regulation, more debt.

In 08 – 09 it was the US that led the housing market crash.

This time around Canada has had a good head start, and will be the first at the scene of the coming RE collapse.

Residential housing prices are already well on their way down in the two largest overheated RE markets of Toronto and Vancouver.

This on top of the final Q4 2017 stats, that show Canada reached $40.78 billion of residential investment. That’s an historic high for any fourth quarter and represents 7.34% of GDP. The largest ratio for a Q4 ever observed! This ratio has never passed 6.74% without a recession following. No one will be immune.

Just think how many of those mortgages, loans, and sundry debt, have been bundled up (securitized) into different derivative packages and sold on into the market, only to be snapped up by yield hungry pension funds etc. BOOM

I’ll sit, lay back, and and watch the carnage; would be fun to see stupid people pay the price of their stupidity, rather than be rewarded for their it like the last 8 years.

So you believe central banks will stop rewarding stupidity? Good luck with that – but don’t hold your breath.

The Fed has an infinite supply of Federal Reserve Notes (electronic credits) to make available to asset holders that aren’t feeling as wealthy as the Fed believes they should feel. They seem willing (maybe even eager) to allow the value of their currency to plummet.

Hold fiat monetary units at your own peril. No one will have sympathy for those who held onto to dollars (or Euros or Yen), in retrospect they will look like idiots who should have known better.

Sadly, I have to second that.

I’d say if anyone is stupid enough to buy a house at these insanely, artificially inflated prices, then by all means please let him/her buy. You need to allow the stupid to hang themselves by buying such properties; world needs such idiots.

Agreed. Let these FB “victims” be a cautionary tale for the consequences of foolishly buying into such a grotesquely distorted asset bubble, courtesy of the Keynesian lunatics at the central banks. For ten years now the prudent and responsible have been penalized by refusing to pay such insane, unsustainable prices, but they will soon have the last laugh.

Gershon: “For ten years now the prudent and responsible have been penalized by refusing to pay such insane, unsustainable prices, but they will soon have the last laugh.”

I really hope your right. I fall into this prudent camp and I am getting really frustrated and stressed. I have a young family and need to get some school district stability. However, I can’t find a house that I would consider staying in for the next 15 years that is below 1 million in Southern California. I feel like maybe I made a mistake and was too pessimistic about the markets about 5 years ago. My landlord is selling the house I have leased at below market for the last 7 years and now I have limited options and will be forced to pay a much higher rent.

It is frustrating as hell that these people are stepping up and spending a large portion of their income on sub-par homes. It seems like there is an endless supply of people willing to be house poor. I had this same feeling before the last crash. I hope I am right but starting to wonder if I have been wrong.

No one knows..Just venting. Have a wonderful day.

Man, you are not alone, well said…nobody could say it any better than you…I am getting desperate myself…at this point all I can do is keep waiting, invest in other ways hoping things will soon turn my way…I bought lots of Gold as well, not selling, in fact buying even more…but who knows if I am just throwing my money away on that as well…

You sound like me before the 2008 recession. I was on the same boat and waited 6 years to purchase a home. Best to decision I ever made purchase in 2010. 40% less than what I would have paid in 2006.

and suppose home values double in the next five years? or the stock market? do you have a crystal ball? people operate on needs linked to various considerations, the right age to marry and have a family? do you wait until you’re fifty and the economy is better? the opportunity to take a better job. do you put your life on hold because you’re afraid you might pay too much? sure these people become victims, we still have an open economy (i hesitate to call it free) and those forces, along with government intervention tend to define the sea changes in social patterns. the 1930s was the end of the family farm, (are the 2030’s going to be the end of the family home?) if you saw a truckload of Oakies heading west, did you blame the Oakies? most of the migrants in the dust bowl settled in CA, and are now third generation home owners, so for the most part the damaging effects of social displacement and economic change tend to get canceled out in the long run and their credit rating resets, and the foreclosed owner starts again. Without idiots buying houses the system would collapse.

Houses are also a good hedge against inflation.

Also a good way to launder that money you embezzled and want to get out of China or Russia.

This pretty much. There is no telling when a “good” time to buy is until years after the fact.

People buying their primary home do so as a hedge against future cost increases to lock into an affordable cost of living.

Any hope of appreciation is purely speculation. The people who got killed in the last recession were not people putting 20% down on a home to live in.

They were flippers and people gambling on a short term refi that never materialized. If you can afford to own a long term residence today and it is more lucrative than renting or you want to anchor yourself to a city then buying could still make a lot of sense. Even if prices are over the top.

Great points Ambrose Bierce.

Actually I’ve heard home values will quadruple in the next 2 years. I better run out and buy before I’m priced out. OMG, the humanity.

For house prices to double in the next 5 years, the FED must print out at least 10 trillion, and take the interest rate to -10. Daydreaming is never productive.

Yup! Exactly!!

There is just never a good time to buy a house or have children or buy stocks – or whatever one wants / needs to do.

Embrace Chaos! Some things will fail miseraby, some things will work out well, the only certainty is that if one waits for the ideal moment, nothing good will ever happen!

For my part, I am very happy that I had my children early on – they have all moved out while wife and I still have the capacity to make good money, and we have grandchildren (since they followed our example and had children early).

My daughter goes to “mothers group” with people who are almost twice her age – from her observations, it takes quite a heavy toll on people, physically and mentally, to have children in their 30’s and late 40’s.

Older, established, people basically have to rewrite their lives; whereas a younger person who isn’t established yet can sort-of walk into their new situation.

I can NOT believe people generalize the way to think about mirriage, family building to think about financial decisions like buying houses.

I agree there is NO “optimized timing” for many things in life due to randomness.

Under all uncertainties, the principle to buy a house is like the principle to spend on other consumptions. You buy it when you can afford it, and you better make sure you can afford it for the next 30 years.

R2D2,

Here’s a classic example of the Greater Fool theory of investing (it won’t last long ;-), “Charming 1 bed/1 bath home located in downtown Niagara Falls [Canada],… minutes from the ‘Falls’ ” for only C$159,000 (that’s C$ folks!): https://www.kijiji.ca/v-house-for-sale/st-catharines/4832-st-clair-avenue-niagara-falls-ontario/1345332170?enableSearchNavigationFlag=true

Just look at that bright grey sky in the background :-)

“A single-level apartment close to the beach at Mona Vale soared $326,000 above reserve at the weekend as buyers aged 50-plus dug deep to purchase lifestyle properties in prime spots.

The early morning Saturday auction of the five-year-old property at 9/25-31 Darley Street East sparked frenetic bidding. The apartment finally sold for $2.226 million, which was well ahead of its reserve of around $1.9 million.”

SEE:

https://www.domain.com.au/news/cashedup-downsizers-hiking-up-prices-of-lowmaintenance-sydney-properties-20180422-h0z3f6/?utm_campaign=strap-masthead&utm_source=smh&utm_medium=link&ref=pos1

House prices are only inflated in comparison to wages of working people – by any other measure houses are not inflated. There is still trillions of dollars sloshing around the world looking for a home (pun intended).

Those wage earners who do not yet own a house are SOL. Several years ago Bernanke had a message for these people – the world (the Fed) does not owe anyone affordable housing. It’s their own fault for being born too late. Start shopping for a nice used van to sleep in and get a gym membership to shower every morning. Changing times mean changing expectations.

Those trillions are being sponged off fast by the FED; this is a game to enrich the rich; and I suspect all the big boys have already dumped all the assets they could onto the public, and will do more dumping as the asset prices fall.

A bunch of Idiots got lucky sharing a ride along with the FED and think it was their genius that doubled their asset prices. Now, the FED will break all the alleged geniuses. Only the big boys will get out much richer, not the Joe plumbers who bought a house for twice the price on a 40 years mortgage.

“This is why even the median Facebook employee (not to be confused with its contract workers), making over $240,000 a year, before income taxes is feeling the squeeze.”

I doubt very much if a median Facebook employee would make $240,000 a year. Only a manager at Facebook, and even then now the low level managers, makes that much.

I like to see some comments from others who are in tech in this regard.

Agreed. I heard that 180k was the upper limit in Amazon and the salaries for people with 15 year experience seems to be 180-190k at best, including start ups. The more established companies pay even less. The start ups throw in options that are worthless today while companies like Netflix and Amazon throw in stock options that can be sold on the market soon. The Facebook employee making 240k must be after stock options. They are better off in this situation than with 240k base salary since they will be taxed at capital gains rates, a number far lower than income tax.

There are people who believe rumors that developers are beingpaid something like 300k+ in behemoth companies. Like you, I wonder how much of it is inflated.

You are incorrect about Netflix. Total compensation at Netflix is straight cash, rather than the typical tech company “some cash, some bonus, some RSUs/option”.

Here are some of the sites which provide salary stats for programmers in the Bay area. I chose Java developer since this is the most prevalent technology in the Bay Area:

https://www.payscale.com/research/US/Job=Java_Programmer/Salary/cc7d7110/San-Jose-CA

And this one provides the salary of Java developers within each company with this description “The average salary for a Java Developer is $102,382 per year in the United States. Salary estimates are based on 86,564 salaries submitted anonymously to Indeed by Java Developer employees, users, and collected from past and present job advertisements on Indeed in the past 36 months. The typical tenure for a Java Developer is less than 1 year.”

https://www.indeed.com/salaries/Java-Developer-Salaries

Salaries are hardly above $110K.

I’ve always maintained that big software companies spread these rumors about $400K salaries for developers so that more idiots can be sucked into the industry so that they can keep the wages as low as possible. It is all made up. I’ve been in this industry for a long time; it is a difficult industry where you have to accumulate huge amount of knowledge to just be able to pass the interview; and once you pass the interview, then expect to work at least 10-11 hours per day for the 8 hours workday. There are absolutely no overtimes no matter how many hours you had to put into finish the project.

I went back to electrical engineering because the CISCO-certified networking consultants were driving ever shittier cars on each visit. I figured (correctly) that it was now just a question of time before my gig would be up too :)

The last time I did a phone interview with Amazon, $140K salary was the number floating around, and they said there was a $20K yearly bonus for keeping active government top secret clearance. Also the stock grants. This was Northern Va.

I have had friends work for companies in the Bay Area and clear $400K and $600K in stock after a few years. It does happen, but it’s basically nerd lotto. It doesn’t happen to everyone and it’s hard to tell what will pay off.

I work for one of the few failing tech companies, so when it comes to house down payment basically went down toilet heh.

The need for the Top Secret clearance indicates that you’d be working for some section in AWS that deals with government contracts and not the retail areas of Amazon.

Completely different employment characteristics and requirements.

The fact that you need that clearance in order to work sort of makes the idea of getting a bonus for maintaining one ridiculous: no clearance – no job – no bonus.

The value of the Top Secret clearance, one granted and then maintained, is that it would make you instantly employable at numerous other entities that require one. Depending on the type of information needed access to you might need a polygraph update though.

Of course, for those of us that have traveled, worked, or lived outside of the USA for any length of time (And not on US government business) or heaven forbid married to a FOREIGNER are relegated to second class status to never again be able to get one of those holy, anointed perks again.

And just because you’ve had one for well over 10 years doesn’t mean squat once its gone – everything you learned/know from having that access to TS/SCI/TK and other code word programs remains in your brain, but locked away never, ever to be divulged or discussed.

When I went into the hospital while on active duty there was discussion around putting a person in the operating room in case I said something I shouldn’t!!

PS: My SF 86 would make Jared Kushner’s look like a short story!!!

Note Mr Richter’s usual deliciously ironic touch: “Median FaceBook Employee”.

In statistics “median” is defined as the value separating the higher half of a data sample (or population, probability distribution etc) from the lower half. It’s often confused with mean (technically arithmetic mean) but it’s not the same thing.

To put things in layman terms it means that exactly half the FB employees makes more than $240,000/year while the other half makes less than $240,000/year.

Everybody got that?

I assume FB is a typical “top heavy” hi-tech conglomerate, meaning the people they have on payroll are disproportionately management, senior accountants and heads of projects/R&D/whatever term FB uses.

There aren’t a whole lot of people with the skills required to fill these positions in the world, so they command a huge premium.

Like many other hi-tech conglomerates, however, FB needs legions of workers to fill the lower positions, from the junior programmers (forgive my outdated and unappropriate language) to the janitorial staff.

The trend worldwide these days is towards outsourcing these positions, either to external contracting firms or by using “temporary” contracts or whatever they are called in California these days.

These workers are not considered FB employees and as such they do not enter considerations for the median or mean wage at FB.

How FB pays their employees is another matter however. I am sure there are a whole lot of stock options, especially the higher one goes on the gerarchical ladder.

While FB took a beating during the recent selloff (I think it was the worst FANGMAN stock), it has since bounced back thanks to dip buyers and savers from all over the world being sacrificed to allow people with more credit than common sense to buy a 30 grands SUV that will start literally falling to pieces in a couple of years.

These people had better hope and pray financial repression will continue driving us savers crazy because the moment investment grade paper yields over 3.5% it’s game over for equities.

I studied median and mean in the 6th grade; I’m quite familiar with statistical terms. Actually, in this case, if it was average, it would have made more sense since I’m sure there are more than a few whose salaries are in the millions.

In any case, if median FB employee makes that much, then there must be thousands making above that much. That’s just not the case. I’ve worked for these big companies, and I still do. That’s just a myth. I provided links above to real salary surveys; take a look.

I suspect the number is indeed the median.

But I strongly suspect they are including stock options or restricted stock payouts in the number.

If Facebook’s stock weren’t going up like a balloon, the median wouldn’t be very near $240k. It would be down in the neighborhood of $150k. And only that high because Facebook is a tip top high-paying firm in Silicon Valley.

Let me also add that it’s important to keep in mind that most of H.R., custodial, Admin, etc. may be contract or very thin with most of the work done by outside contract workers.

So every single one (almost) of Facebook’s direct employees is a high-end white collar employee.

(I think someone said this above but it’s critical to understanding how the median pay can be so high)

Ed,

I have provided links to salary stats in a post above. Salaries are around $110K. With stock options, if you are lucky, it might get to $150K; but it will never be $240K. Googles, and Facebooks of the world love to say they are paying that much to their employees; but it is all a lie. As a programmer, only those with skills so difficult that no one can master, can dream of $240K income. So, don’t be duped by these rumors.

I have a few friends in their mid 30’s that are basically in their peak of Silicon Valley desirability. Successful work xperience and advanced degrees. They’re all making around $200K to $250k. They’re the cream of the crop. If their pay is median, then I would like to see the data set.

True. Stock and/or bonuses are surely included in that $240k number.

FB and GOOGL do not account for a majority of The valley’s employees. They do have an outsized effect because of the shortage of inventory. The price appreciation in the Bay Area is a double edged sword, you have a much larger tax bill now when you exceed the gain of $500k in the Bay Area if you sold. And you can’t switch homes because the cost nearby is just as bad. Makes less people want to move and constricting inventory.

On the other hand, we have thousands of new condos springing up across the Bay Area, the so called starter home is now the only affordable home in this region for most.

WSJ says FB median pay = $240k:

https://www.wsj.com/articles/at-facebook-median-pay-tops-240-000-1523924535

That’s good, so what, nothing I said contradicts the WSJ. FB median pay is a bit of an aberration in the bay area, and FB does not employ half the population in the bay area. I would guess it employs at maximum 0.01% of the population (probably less) in the greater bay area.

I would note that most of the companies in bay area do NOT offer a median salary at $240K. The other ones that might are all software companies like GOOGL.

The point was that the only reason those people at FB or similar companies have such an impact is because of the low inventory of housing. My guess though is that this will be turning shortly for a variety of reasons.

$240k to pay programmers to write code that allows boring people to post pictures of the food they ate last night?

Seems like another good reason to sell FB stock.

Jeff,

And here the links from indeed.com that provides estimate of salaries at different companies: https://www.indeed.com/salaries/Java-Developer-Salaries. WSJ can write whatever they want. I only care about the reality on the ground not what some paid out reporter writes.

This second-guessing is getting silly. Here is what Facebook itself said in its proxy filing, verbatim:

“For the year ended December 31, 2017: the median of the annual total compensation of all employees of our company (other than our CEO) was $240,430; and…”

https://www.sec.gov/Archives/edgar/data/1326801/000132680118000022/facebook2018definitiveprox.htm#sBCD8DE604AFF5931877A1DBB737D7A6C

Wolf,

I took a look again around for FB. Their pay rate seems to be an anomaly. Google pays much less, and Amazon pays even less. I don’t know what is going on, but my question would be, not from you, but in general why would FB pay far above market rate? Companies don’t live to just hand out money. They will try to pay as little as possible.

FB disclosed the median value of total compensation packages, including bonus and stock-based compensation. All companies are now required to report median compensation, but they differ on how they report it. So it’s not always easy to compare.

Amazon, which is largely a warehouse and distribution company in terms of its employees, reported a median compensation of about $28,000 globally. This includes many employees in “cheap” countries. Yet engineers at Amazon get paid well.

When shares surge, such as they have, stock-based compensation is a big part at a place like FB or Google. When shares decline for a long time, stock-based compensation shrinks as a factor. So salary offers alone cannot describe the total compensation packages.

Add to that that your time at Google or FB is limited. If you haven’t made it to a project manager by the time you’re 30-ish, your time is up. Would be well advised to look around for other job, or be phased out, but your costs of living will not decrease.

“That lunch was free for some. But others are paying for it.”

This is what has been happening since 2008! This is what is bound to happen when fraud is the corporate business model and it goes unpunished (not only that – it is aided and abetted by regulators and government). Bad guys go unpunished (not only that, get rewarded too – think banksters, accounting agencies, rating agencies), regulators go unpunished (think central banksters, government agencies) and good guys get punished (think savers, retirees, prudent people, tax-payers)

Where do you think this road is leading us?

“Where do you think this road is leading us?”

To a demographic steamroller, so resist that urge to grab that last penny !

Millennials overwhelmingly voted for “hope and change Goldman Sachs can believe in” instead of Ron Paul, who was our last best hope to end the Fed and its swindles against the 99%. They made their bed; now let them lie in it.

Is not our current Secretary of Treasury Mnunchin a Goldman Sachs alumni?

Trump has already fired a lot of his Goldman Sachs appointees already:

Steve Bannon

Gary Cohn

Jay Clayton

Anthony Scaramuci

Did I forget any?

As a millennial, I have this thought about my peers all the time – I truly don’t understand the hyper liberal socialist utopia many my age seem to yearn for. Free college for everyone, who will pay for that? Healthcare for all, who will pay for that? What’s next, free housing for all? God help us.

I think this not understanding the value of money it is a consequence of relying on parents’ money for too long. I can’t think of a single friend who put themselves through college or bought a house on their own. Many can’t even buy cars on their own. And also the very liberal environment of colleges – as Libertarian, I felt not just out of place, but was often afraid to express my opinions even to professors.

So yup, an entire generation that’s pretty screwed financially, and yet we keep voting for more of the same.

They don’t call our multi-millionaire rulers in Washington “The War Party Of The Rich” for nothing….

Free markets were long ago extinguished, (thanks Fed)….. and all the oligarchs have spent their pocket change on spreads purchased in New Zealand, etc. to flee to when they’re done with us.

Complete vulture capitalism

“Complete Vulture Capitalism”

Should read

Complete Vulture Cronyism.

Which is the system you have currently in, America, russia, ccp china, and a few other places

Vulture Cronyism (AKA Crony Capitalism) is not Capitalism (Capitalism is a sustainable Economic System (Crony or Vulture Crony, Capitalism, is not.

“You better get into real estate while you still can, it’s only going to go up from this point on!”

I remember that line back in 2005, 2006 and so on and so forth… Someone I know has been trying to sell their very nice and expensive home (about $400,000 originally) in a very nice town just south of Tampa Bay along the very scenic Gulf Coast, for over a year now. Over the last 12 months, they’ve dropped their asking price by near 8 percent, and as of today, it’s still not sold.

I just took a look at the area on Zillow and WHOA!!! There are a lot of houses for sale all along the coast south of Tampa Bay. Blew my mind at how many. So I took a look at the local realtor publications and everything sounds peachy-keen according to them. Always does most of the time with those kind, after all they live off commissions. Their comments were generally that everyone is moving to Florida so you better buy now while you still can. The only complaint was there were not enough affordable homes for first-time buyers being built. I guess the developers want the big bucks, and the realtors want the big commissions, and the neighborhood doesn’t want the cheaper homes built anywhere near theirs. But I seem to remember that Florida has had its share of real estate booms and busts throughout the years.

As a side note, when I do “due diligence”, I place very little significance on sales people. I guess they sometimes call that being “street smart.”

On top of all that, I just read that the Zillow Group, owners of “Zillow.com,” are going to add “house flipping” to their portfolio because Zillow has never actually made a profit (think Amazon & Tesla), so their hope springs eternal as well —- until it doesn’t anymore. I think that they’re hoping that “house flipping” will finally help them to finally make a profit is a very alarming sign. Then add to the mix: 78 percent of workers in the United States are living paycheck-to-paycheck (Harris Poll 2017), rising interest rates and many of the millennials not wanting to live in McMansions (much less can afford to) and I think something very dark this way eventually comes. Bumpy, bumpy, bumpy and then a big fat loss in the old pocket book of net worth.

Ride em’ cowboy!!!

Here in Oz we finally have a few ‘discount’ RE Agencies popping up.

They’ll handle the entire process for a flat fee of between A$5000 to $6000. Less than 1% of the cost of the median house price in Melbourne.

Much cheaper that the standard RE commission, lawyers, and other related costs.

Even seen a few houses in the area being marketed by them.

market disruption that couldn’t happen to better bunch of people!!!

After the bust, 2007-2008, my wife and I spent a week or so on the gulf coast.There were thousands of ” no offer refused” type signs. Lists of hundreds of foreclosed properties. That was a time where 25K cash could buy a lot of house. I picked up one for 8K. No typo.Those times will come again. Save your money. Be patient. Strike when everyone else is full of fear.

Yeah, even concrete bubble houses or “concrete igloos” are ridiculously expensive in this economy. And wrh working from home disappearing because companies don’t want to have empty buildings anymore, buying in a cheaper place is not an option unless your company exists there.

If you buy a car make sure is comfortable to live in and has good heating. It you can get a van? Even better!

Winter is almost here guys!

Relevant:

https://www.theguardian.com/news/2018/apr/17/get-rich-quick-silicon-valley-startup-billionaire-techie

So we basically have the “current generation” wasting away in a very badly paying gig economy and tech jobs, renting shared space, how can this people ever afford a home? Even a concrete igloo i sbeyond them.

Great article!

In short: Be a huckster!

No question housing will slow up as interst rates climb. I would expect the Fed understands this too. They will be watching housing markets closely.

I don’t expect any form of collapse in housing prices. More like bleeding off some pressure. As real estate is fully much local/regional anymore, the bleed-off will vary.

The Fed has absolutely no interest in crashing the housing and housing related economy. It is one of the main drivers of the overall US economy. So in spite of their jawboning for further increases, do not be surprised if increases get put on hold sometime this summer/early fall.

Low 3% for the 10 year is what I believe the economy can withstand. That rate will likely not pressure the 30 year rate all that much more. Mortage rates will have increased some and prices will have to adjust down some (and will).

Don’t get me wrong. I do not at all like the current economic situation in the US. We are headed for a crisis; but I just don’t think this will be it. I personally believe the government will do whatever is necessary to keep things going (huge deficits, more QE if necessary, etc.) The long run effect on society/social cohesion/suffering/crime, etc. is where I think we’ll see the break. I’m not smart enough to predict what it will look like but suspect it will be something sudden and violent like a massive riot that will spread. Certainly the US has enough “firepower” within its citizenry to cause some major carnage.

I hope I’m wrong.

You have been proven wrong many times in the history if you look at the historical prices unless this time is truly different

It’s a bubble and it would burst then only question is when and how

I do not see marginally higher interest rates substantially decreasing home prices soon.

Prices of homes are driven by a combination of multiple factors. Here in Seattle, the local economy remains very strong, NIMBYism restricts developers from increasing density in central neighborhoods, transportation has been woefully underfunded for decades making commuting from the suburbs increasingly time consuming and painful, and buyers have an expectation that prices in central neighborhoods will only go up in the future.

In my neighborhood, a new 1500 sq ft townhouse now lists for $1-1.2M and would take an offer of at least $100k more to actually buy. I think even a two tech worker family, no kids, are starting to be pinched by these prices. But, as long as they believe it’ll be worth more 5 years from now, they’ll stretch to buy the place. When that faith is tested in the next recession, I think we’ll see some declines.

Yes, the sales volume is so low here in Seattle that the median is being set by very few (relative to history) well off buyers. We went to open houses today to gauge the foot traffic and it was quite heavy and the realtors were all getting ten offers a home, if not more. I bet this is peak frenzy right now. I expect we’ll see a leveling in real home prices this fall. It will take a heavy recession to get inventory back, however, because everyone is priced out of moving. Trapped by their own appreciation!

We looked around at townhouses this time last year and had a similar impression. My wife and I are early 30s, both work in healthcare, our combined median pre-tax income is 4-5x the median income in Seattle, and we aren’t interested in buying into this.

We certainly could lever up big time to buy that $1.5M home, but it’s just not worth it. We can make an equivalent income working almost anywhere where patients have decent insurance. We’d rather keep putting $15k/month into our portfolio of index funds called “early retirement” than be house poor in an increasingly expensive, congested, dirty city. Hood River looks better and better to me each year.

Wolf has already answered this question in his article: https://wolfstreet.com/2018/04/20/financial-stress-in-the-credit-markets-v-the-2-year-treasury-yield/

The FED will have to keep increasing the rates, and the 10 years yield is already almost 3%.

The FED didn’t have any intention to “collapse” the housing market in 2007-08 and even made many spiels about how strong that market was but was back-slapped when it didn’t pay enough attention to the banks and financial institutions under it’s charge that were creating and selling bundles of bad hotdogs wrapped in used toilet paper!! So I wouldn’t trust the FED for absolutely no judgement whatsoever this time around. I am glad that they have decided to try to influence a push up in interest rates but as another commenter said above that (para) a push to at least 3.5% (an up) will overturn this rotten apple cart in a Silicon Valley minute. Our whole economy (social and money wise) is unsustainable. Too many lost good paying jobs; crushing of organized labor that built the middle class; corrupt politicians; continuous failed foreign policies (Remember PNAC? Project For a New American Century? that spelled out just what the US foreign policy objectives were going to be; Paper written in mid 1990’s; easily researched, 81 pages etc.); continuing greedy environmental destruction; trashing of our public school systems; different levels of justice; banks publicly declared “to big to fail” by our own legal system, and on and on. What chance does the “little guy/gal” have? Endless debt?? Is that the new norm. That is slavery. This will not end well. And, as a late octogenarian I thought it might be quite a few years before a real collapse I think now it will be sooner rather than later.

Enjoy your site Mr. Richter. It is just about at the decent level (including the commenters) as NC (Naked Capitalism).

Doesn’t seem like housing is going to tip off the next recession. Maybe the stock market or the tech bubble. Here in So California, there are still affordable properties within commuting distance, people just don’t know how to look for them so a lot of this is hyperventilating based on low supply and a media-generated focus on the most high end properties/neighborhoods. Also left out of the conversation is the increase in the educated & professional class who make a lot more money than the average worker. The fastest growing renter households in the LA-Long Beach-Anaheim metro area are with people making $100,000/yr or more. So, yeah, it’s rough if you’re a minimum wage employee, but housing costs are high here, at least partially, because there are a lot more people making six figures and up. http://www.jchs.harvard.edu/ARH_2017_change_in_renter_households

Every expensive city on the list is a place with exploding homelessness. The housing markets are broken in America. The mirror to this article is the rise in tent cities along with million dollar homes.

LA’s downtown is a disgrace, as is downtown Miami, and you can add Austin, TX too. While driving on scenic interstate 10 into New Orleans, you are sure to miss the miles of homeless people under it. It is a national disgrace.

It was rough winter and in cold country cities they routinely give the homeless bus fare to a warmer climate to get rid of them. The city of SD had to add an extra tent shelter, which cost them millions to build and operate, and so they raised the hotel tax. Visitors from “back east” now pay some of the fee to take care of THEIR homeless. And local government is actually doing a pretty good job of finding housing for those homeless who are cognitively able to handle it. The homeless problem is a mantra which has become the Liberals equivalent of the socially conservative agenda; abortion, gun control. The economics of the matter come to down to this, we’re all getting a lot poorer which is no way to run an economy.

I think there is more to high home prices and homelessness. Society celebrates growth. Yet as the population grows, so does the demand on all resources.. The world is a finite place and most easily accessible resources are use up. Thus all additional extraction cost a lot more in energy and time than they did even 30 years ago.

I am not diminishing the job that the FED did in transferring the wealth from the producers to the asset holders and those with first access to the cheap money.

It is my contention that the homeless problem is partially due to the growth in the world’s and this nation’s population with the inability to continue to have cheap enough resources and space to provide for all. In other words, a living wage has become more and more of a problem as the cost of living has continued to increase due to demand and scarcity..

I 100% disagree. With the technology humans have invented, if the wealth is “distributed well”, everybody in US can only work 2 days per week and there is no problem of food, shelter and medicare. It is he distribution towards 1%, wasting all the wealth on war and global dominance and waste wealth on mal-investments through bubble blowing that makes people without shelter and food in US of A

Just for the sake of discussion, technology so far hasn’t created copper from iron ore or timber or rare earth metals or more oil or… It can’t make more snow and keep the rivers flowing and clean or the farms growing production..

It has made it so I can read and post from the Petrified Forest State Park in Utah but it doesn’t create more space or fix the out of date undersized and in many cases overwhelmed sewer or drainage systems.

You may be close to the truth about dividing up the money but then at what quality of life? The US is far behind in being able to provide the basic infrastructure it needs just to maintain the standard of living we all desire. The quality of your life may not be degrading yet but the trash is piling up and so is the shit..

literally..

What we have is a society that worships money and not a quality of life.. And we all know that money won’t buy you love or your health or make you so you can enjoy your existence.

Petunia – it’s capitalism working as designed. You have to have a “reserve army of the unemployed” to keep wages down, and they have to be kept miserable to keep the employed from having any ideas about getting off of their treadmills. This is Marx 101, stuff even I can understand.

it’s funny, because in college, I had a teacher who was a raving Marxist, and the stuff he said pissed me off at the time. But he’s proven to be 100% right. Smart guy.

Marxism is great as description; much less so as prescription.

But as for describing the real-world nature of Capitalism, no one did it better.

It’s a hella lot easier to

1. know something is wrong

2. than what is wrong.

3. Let alone fix it.

“It’s a hella lot easier to

1. know something is wrong

2. than what is wrong.

3. Let alone fix it.”

Should read

It’s a hella lot easier to

1. know something is wrong

2. than what is wrong.

3. Than what is making it go wrong.

4 Let alone fixing what is MAKING IT go wrong.

To many peopel focus on fixing what is broken, instead of first fixing, what is causing the breakages.

AKA dont fix the problem, without out first fixing the root cause of it.

Marx both knew that something was wrong (and right, too: he also granted Capitalism props for its advances over Feudalism) and how it was wrong.

Most people fail at the latter.

There is also a need to maintain an army of semi-serfs that are still better off than the true serfs. Those would be living in some third world hellhole anxious to get to the “developed” world. This dynamic has to be maintained through open immigration. Marxism should be amended for the 21st century.

Last week I went to dinner with a friend, walking back from the restaurant I counted 6 campers, vans, and cars people were obviously living in.

Nother friend is living in his shop in the industrial area near the Oakland Airport. You drive around and every business has a camper or RV parked in front.

Petunia, you are spot on. California has seen a 15% increase in homelessness statewide from 2015 through 2017. (https://www.sfchronicle.com/news/article/California-s-homelessness-crisis-moves-to-the-12182026.php)

As someone who rents in Oakland, I cannot see my way to home ownership. The prices in Oakland have increased to an absurd level.

Considering over 60% of the population “own” their home, the wealth effect has done its job. New cars and xpensive eateries are all over the southwest. Even New Mexico real estate is selling quickly. But the top looks to be in. Unlike 2008, I don’t think we will see a flood of homes come on the market when the masses figure this out as mortgage underwriting has been pretty conservative. It will take a recession and even then , people will probably stay in the home as long as possible as there aren’t better alternatives.

And once forced to leave their house…..RV sales volume has been huge the last 5 years. This is quickly becoming the new way to live without renting a home. Watch for an explosion of this in the coming years.

DK,

RV living would be good if you’re single but with a family; i.e., with a kid having to go to school someplace, that’d be a recipe for alimony.

A majority of households are now single people. If they all moved into their cars the housing crisis would be solved.

I takes some getting used to but humans adapt and move on.

Get a van man.

https://www.wsj.com/articles/big-banks-find-a-back-door-to-finance-subprime-loans-1523352601

Yeah, they are more conservative indeed. They issue loans to firms that turn around and issue subprime loans. Amazing.

The question is where the next rent seeking opportunity will be – food, water, air? As the CEO of Nestle said:

“Water is, of course, the most important raw material we have today in the world. It’s a question of whether we should privatize the normal water supply for the population.”

How much of your paycheck goes to clean water? I know that the PUC is allowing my water bill to increase 42% by 2020. This will squeeze the working poor and middle class even further.

The rentier capitalists know no bounds and will squeeze until it breaks.

The Bush family owns a 200K+ acre plantation in Paraguay. It is suppose to sit on the largest aquifer in the world. I’m sure it’s a coincidence.

So where are you that your water bill schedule is that steep?

Out here in CA there are multitudes of “Community Services Districts” (water/sewer/parks for small communities) that are forced planning by deteriorating infrastructure and some have old fashioned “open canals” systems that have to be “piped”. They face large increases in their water bills. It is another of the infrastructure disasters that we face and our legislators refuse to fund. It’s not very glamorous to talk “water/sewer” rates. Even new prisons fare better. Somebody has to pay these bills and it’s the users. Some are screaming bloody murder. But they will have to pay or get out. Those increases will further constrict “discretionary spending”.

The cost for 1000 litres of water in Melbourne has gone from $A1.00 in 2007 to $A2.58 today.

The initial Tell will be when the airlines start charging an extra fee for the pressurrized air in the cabins. Guaranteed to happen.

Wolf should start a betting pool, with an over/under for when they’ll do it.

Interest rates are still too low compared to what they were in the ’80s. A half-percent spike in interest rates in the next round and later would be nice for some, bad for others, but overall, it’s exactly what’s needed.

I feel very bad for folks just starting out. Bamboozled for a dubious degree and in debt, then they have to move to an unaffordable location to make use of it. Along the way they cannot afford to buy, rents are astonomical; living on a hamster wheel. Welcome to the new version of tenant farming/sharecropping, only with clean hands and pale necks and a latte to-go.

Truly, this is a time for critical planning and evaluation at 18 years old? 16 years old? There is a new paradigm and please don’t believe the usual suspects. They are wrong. Have been wrong. Will be wrong.

I am a firm believer in having mobile skills that can’t be duplicated by visa workers. Of course for that to happen the Govt actually has to work for their citizens and not the large corporations. I don’t see much of that in any country.

Oh well, tea is steeped and the thermos needs filling. I am doing 2 hours of taping and some final tiling in the entrance of my rental. Tenant is moving in within the next week or two. No day of rest for me….good thing work is fun.

There is a new paradigm and please don’t believe the usual suspects. They are wrong. Have been wrong. Will be wrong.

The Usual Suspects aren’t just wrong, they’re willfully duplicitous and are cravenly propagating a Narrative they know to be false on behalf of their corporatist masters.

What’s to stop millennial from repudiating the national debt? They had nothing to do with the buildup of it.

The old debtors that have always planned to force the next sucker take on more debt. The army of older debtors will always put vote the innocents. Yes, it has been corrupted down to this.

Start with global financial Ostracism. A complete implosion of the US economy as the $ becomes worthless in seconds, and war, as more than 1 somebody would decide, if you wont pay, we are coming to take.

This is one of teh most foolish and dangerous proposals, Trump made, early in the election process.

“It assumed a 5% down-payment”

When did this happen, at 5% you are underwater immediately due to brokerage commissions selling out.

And why wouldn’t every (foreign) buyer (read, phony Chinese or corrupt overseas cash) who had access to credit buy at 5% down, prices go up 7.5%, and you ROI is 150% annualized. Default and go back home if prices drop

Leverage is a beautiful thing on the way up, and kills on the way down….

“When did this happen, at 5% you are underwater immediately due to brokerage commissions selling out.” Yep, strategic default is the risk mitigation play here.

“one that sells for 80% of the median price (resale and new) in that particular market. It assumed a 5% down-payment and a 30-year fixed-rate mortgage for the remainder”

So in other words the report is based on fantasy not reality? I’m in socal and owning a home is so far out of touch for everyone I know it’s laughable. If you don’t have a home now you never will unless it’s inherited …..or if prices drop …..well for me anyway…….70%

It’s not inflation driving homes prices, it’s invasion and environmental restrictions on new housing for all but the connected.

Wolf,

Housing inflation affects everyone not just new home buyers. The watershed is an acceleration in taxes and a lower share of the budget for consumption.

There are still lots of entry level houses available in the US for millenials, just not in the SF Bay area and several other metro areas. Try Dearborn, MI home of Ford Motor Company. For under $200,000, you will find lots of choices, but you might not like the neighborhood.

Not a lot of people want to rush into the auto industry with the stories we can hear on this site. Little niche blog post…

https://wolfstreet.com/2018/04/13/carmageddon-gm-cuts-shift-in-ohio-1500-layoffs-as-cruze-sales-plunge-production-in-mexico-started-in-2015/

The picture of tents reminded me of a recent story out of Vancouver, tents aren’t sufficient for a Canadian winter so they improvised.

http://www.macleans.ca/economy/realestateeconomy/vancouver-real-estate-is-so-crazy-construction-workers-have-to-live-under-skytrain-tracks/

Wolf,

Last I checked RE Taxes in the Bay Area were 1.25% of the sales price.

Your statement “Property taxes would come to about $633 a month” is not even close.

0.0125 x 1,120,000 = $14K per Year or $1166.67 per Month !

Murf

Ok, the was pretty sloppy on my part. I just looked up San Francisco FY2017-2018 Property Tax Rate which is 1.1723%.

I find it odd that millennials simply accept the status quo as something they have to live with. They have the votes and the power, yet they seem to accept the financial slavery that has been forced on them.

House prices are out of reach only because the Fed made them that way. The high housing prices are NOT the result of market dynamics. In this case, the millennial generation should be using their political muscle to fight it. Where is the outrage? The older generations are stealing the millennial’s future. It’s only going to get worse as we head into $1-2 trillion dollar deficits and QE to address future recessions.

Good jobs are out of reach only because globalists have moved them offshore, as corrupt or incompetent legislators stood by and watched.

Where are the millennial movements to correct these wrongdoings? If you are’t at the table, you are the one getting pounded.

Oh Pleez cry me a river LA/SF/NYC/NE/etc. folks.

If you are unhappy with the insane housing prices then vote with your feet and MOVE…

Plenty of affordable, decent cities with a good quality of life in the list… Nashville, Charlotte, Raleigh, Jacksonville, Orlando, Tampa. All have 1.5 million pops or greater (or as I like call to them… “big-enough-for-an-IKEA city” :) [although of this list Raleigh and Nashville don’t have one yet but should be getting one by 2020]

Florida also has no income tax and Tampa and Jacksonville are on the coast (if you are into the beach thing).

In other words, there are options out there folks. Don’t perpetuate the bubble!

“Florida also has no income tax and Tampa and Jacksonville are on the coast (if you are into the beach thing).”

There is a really good chance Tampa and Jacksonville will be literally under water in 50 years time.

Not a place to be advising people to move to. Unless you have personal ulterior motives.

In plain language, dollar currency devaluation money printing as government policy to pay the bills, is the culprit for all these bubbles…….

A fiat currency story as old as the Roman empire, and which of course will have the same result…..

Oh, for an Einstein in economics to one day appear, and write a new story……I`m not holding my breath…….