The Fed’s new paradigm.

The three-month Treasury yield closed at 1.81% on Friday. It has been at about this level since before the Fed’s March 21 meeting, when it hiked its target range for the federal funds rate to 1.50%-1.75%. In other words, the three-month yield had been trading above the upper limit of the Fed’s range even before it was announced. So the rate hike was fully priced in, plus some, in preparation for another rate hike in June. This is up from 0% in 2015 when lots of folks said that the Fed could never raise interest rates again.

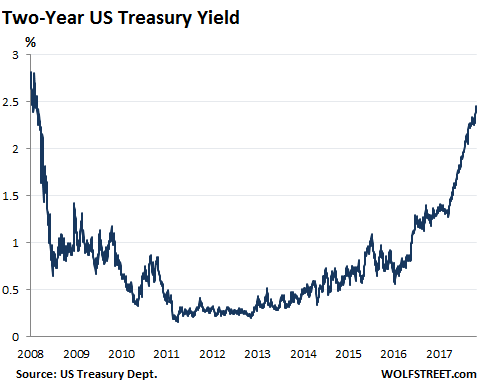

The two-year yield had no such moment of rest. It rose to 2.46% on Friday, the highest since August 11, 2008, and up from 2.31% on rate-hike day in March:

As bond yields rise, bond prices fall by definition. So a rising-yield environment can be tough on holders of bonds with longer maturities.

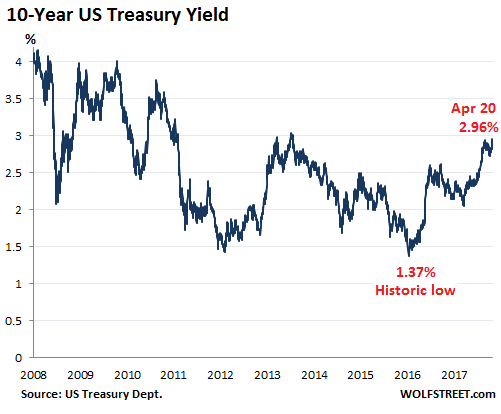

The ten-year Treasury yield moved only sporadically, wavering, or even declining as short-term yields soared, but then shot higher, before taking another break. Now it’s shooting higher again.

On Friday, the 10-year yield rose to 2.96%, the highest close since January 9, 2014. It’s tantalizingly close to 3% and appears to be setting up for a another try at breaking the 3% level. If the 10-year yield closes at 3.05% — just 9 basis points higher than Friday’s close — it will be the highest close since July 2011:

In mid-February, as the 10-year yield was soaring and threatened to take out the 3% level, I speculated that it would run into a wall over the near term, for two reasons: Enormous demand at the 3% level, and record short positions by hedge funds against the 10-year Treasury. This begged for a contrarian rally, or even a short squeeze. While the ensuing rally wasn’t exactly spectacular, it pushed the yield down to 2.73% by early April. But since then, the 10-year has sold off again. Now with the yield at 2.96%, it might try to make another run at breaking 3%.

It might not succeed this time. But it will succeed sooner rather than later. Of note, the two-year yield has not yet run into this kind of wall of resistance.

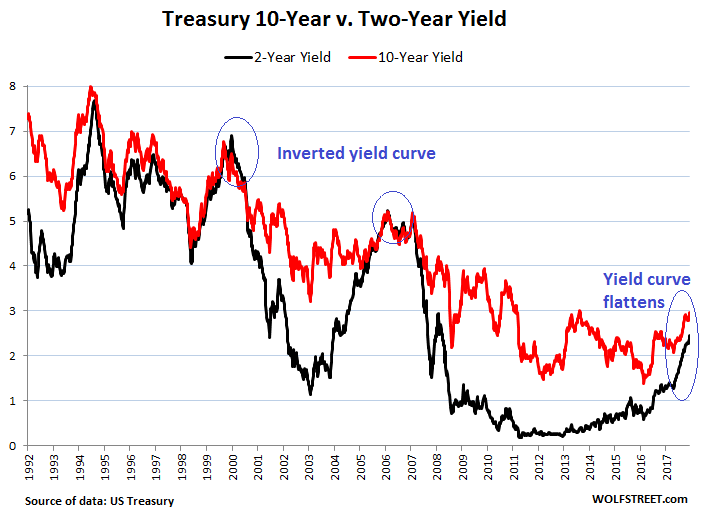

As in the prior three rate-hike cycles going back to the 1990s, the two-year yield has reacted faster to rate hikes than the 10-year yield. While the 10-year yield tends to surge later in the cycle, the two-year yield also surges and has a tendency to overshoot late in the cycle.

The current spread between the two-year yield (2.46%) and the 10-year yield (2.96%) is 50 basis points, about the same as in December. That spread is narrow. But this is practically normal in rate-hike cycles.

The chart below compares the two-year yield (black line) and the 10-year yield (red line) going back to 1992. We’re now in the fourth rate-hike cycle over the period. Note how much jumpier the two-year yield is than the 10-year yield (click to enlarge):

The two-year yield was higher than the 10-year yield in 2000 and then again in 2006/2007. This was when the yield curve “inverted,” the unusual phenomenon when the 10-year yield is lower than shorter-term yields.

But this rate-hike cycle is different from the prior ones. The last rate-hike cycle started in June 2004 and ended in June 2006. During those two years, the Fed took its policy rate from 1% to 5.25%.

This time, the Fed is moving at a glacial pace. If it hikes rates by 25 basis points four times this year, it will be a lot. In this cycle, the Fed has engaged in policy action only at meetings that are followed by a press conference. There are four of them per year.

The Fed started in December 2015 with a 25-basis-point hike, did another one in December 2016, did three in 2017, and might do four in 2018. For now, it is set to proceed at a similar pace in 2019 and possibly into 2020. At this pace, the rate-hike cycle might last up to five years – instead of two years. The Fed’s persistent word for this has been “gradual.”

Given that the pace is so much slower, and that the duration of the cycle is already longer than the 2004-2006 cycle, the results will likely be different too. The last two rate-hike cycles ended in inverted yield curves and were followed by recessions and worse.

This pattern might not occur again – given the Fed’s new paradigm, the slow-motion approach. And we’re left guessing as to how this might turn out. If the economy adjusts to these higher rates without recession, the Fed might not cut rates again for a long time, even as asset prices – stocks, bonds, real estate, etc. – “gradually” meander lower for years in response to higher rates and tighter credit. Think about the implications.

The bond market is already talking about the next rate cuts, possibly as soon as 2019, much like it was talking about “QE Infinity” in 2012 or the permanent zero-interest-rate policy in early 2015. And given the new scenario of long slow-motion rate hikes, the bond market may be engaging in wishful thinking once again.

The two-year yield, now surging, is a leading indicator. Read… “Financial Stress” in the Credit Markets v. the 2-Year Yield

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What “investor” in their right mind is going to buy US debt that is going to be printed away by the Fed?

Good point I know I wouldn’t buy it

Interest on excess reserves recycling program! American people must learn how to stuff toothpaste back in tube?

The economy is operating at full debt issuance with debt to GDP 105% and 75% of this debt is public held? What happens if that 75% becomes 60% because after a decade of talk about higher rates they are now? The Federal Reserve has a tail risk which dwarfs the body politic and would welcome a ” authoritarian” type solution in a hearbeat? A supreme leader would be a god send ! Hank Paulson will need to be called to Gotham again to beg for a accounting miracle and a bank bailout ? Schedules must be maintained!

Those who have been buying have repeated the “Don’t fight the Fed” mantra fore years. And now that the Fed is selling I would venture to guess that those same folks will be fighting the Fed..at least at first, until they realize their policy isn’t going to reverse anytime soon.

So maybe more up/down volatility until markets finally get the message again and stop fighting the Fed; and start selling along with them?

Ten year is presently at 2.998 Closing in on that elusive three percent very rapidly folks

You can’t keep a house of cards up forever.

Can the FED delay a stock market massacre until next year?

September/October should be telling.

Yes, yes it can.

But if you see Tesla, Uber and Netflix unable to sell more junk bonds or selling way less than expected, then the bubble has crashed my friend.

I am using those three zombie companies as a measuring stick to see when the market is crashing since they literally cannot live without keep taking debt.

Tesla seems to think Google or some other company will buy them, but considering their huge debt and Google and so on having their own alternatives, why would they?

All these companies carry first in class brand names so that brand may be worth absorbing a nasty financial hit for some buyers.

call it the Debt Zombie Index. Keep us posted

Care to buy a can for the other end of the string? Its a communication medium or a ball or a dog ? Time in a bottle your call? The Federal reserve is paying debt to banks to keep capital from markets which banks need less than the markets? Jump in the north sea before the iceberg? The bet is the legacy dollar debt will get paid in full?

“But if you see Tesla, Uber and Netflix unable to sell more junk bonds or selling way less than expected”

Given what Tesla’s junk bonds have been trading for, I think the debt market is closed to them.

“Tesla seems to think Google or some other company will buy them”

An Apple or Google will want to use their own software stack for any sort of car manufacturing endeavor. There’s no reason a company would want the unremarkable NUMMI factory, that boondoggle in the Nevada desert, on top of Tesla’s liabilities, at $30 a share, much less $300. If a company with too much cash on hand wants to buy a car manufacturer they may as well go with one that’s profitable and builds a magnitude more cars per year. Ford is trading at a smaller market cap than Tesla. It just goes to show how over valued Tesla is. Their Supercharger network is probably their best asset in the case of a reorg.

Tesla is still selling their bonds like hotcakes, is not how much they are worth but how long Tesla can keep selling junk bonds.

To suppose whether raising rates slowly enough can avoid tripping a recession calls into question what the true cause of a recession is. It’s apparent that cheap debt for many years helped launch an upward spiral of exuberance in many forms of asset speculation as well as business speculation. Even with the cost of this behavior increasing it’s still going strong as if nothing has changed leading me to believe it is more psychological than akin to physics. Gravity can keep tugging harder and harder, and supposing it isn’t pulling harder as fast as it has before, that the people won’t lose their balance seems possible, but what if the ones who jump first actually win the game? Well then I still think that like a flock of birds where when one apparently decides to up and leave and then the whole flock simultaneously goes with it that there will be some kind of tipping point similarly in many assets. Since some of these do actually relate back to the investments in businesses dabbling in the real economy and on down the line to jobs, incomes and ultimately aggregate demand that can also squash less speculative forms of business at the margin I really can’t see how a recession won’t happen at some point despite the slow pace of rate hikes.

Banks being greedy jerks who cannot look pass their very long noses.

That was literally the cause of the previous crisis.

And if you look how much banks still have in junk debt, will also be the cause of this incoming one.

The Fed been saying “Look man I am gonna raise the rates, get rid of that junk debt.”

And the banks are like “Uh… not feeling like it?”

“Even with the cost of this behavior increasing it’s still going strong as if nothing has changed leading me to believe it is more psychological than akin to physics.”

Agreed 100%. I have long suspected that the Fed has studied human psychology effecting the business cycle and has begun to actively factor that into their monetary policy. So far we’ve seen that through strategically timed commentary (i.e. “jawboning”) and it’s accommodative policy (e.g. a quantitative easing program that was publicly announced as indefinite, giving the financial markets no psychological incentive to try and capitalize on its inevitable end) . As game theory teaches, affecting psychology is far more effective at delivering predictable effects than traditional monetary tools and I think we are now in the era were this will be the chief mechanism by which credit will be governed.

On a different note, I suspect that the slow normalization of the nominal rate has more to do with the Fed giving themselves room to re-establish a stimulative position in the event of a downturn (i.e. raise rates slow now so you can aggressively cut them later) since inflation, by their measure, is largely the same as it was for the last few years.

We know there are three things guaranteed in life: death, taxes, and recessions.

But when it comes to recessions, the next one might be out further, and might be milder. Most run-of-the-mill recessions aren’t even officially pronounced by the NBER until after they’re over. An official recession requires more than just two quarters of GDP declines in a row. The NBER would need to see that many aspects of the economy are weakening, including a significant decline in the labor market.

So what will the Fed do if there is just a mild slowdown? For example, if unemployment ticks up to 5.2% and stays there before the labor market tightens up again? I doubt it will resort to drastic action when this occurs.

For example, if unemployment ticks up to 5.2% and stays there before the labor market tightens up again?

Does anyone out there really believe that our true unemployment rate is “only” 5.2%? Or that inflation is holding firm at 2%? Other centrally planned economies, i.e. the former USSR, faked their economic data, too.

Check out the BLS data. It’s a huge amount that is released every month. It includes 6 types of unemployment rates and all kinds of employment numbers and ratios, split up in a myriad ways, seasonally and not seasonally adjusted.

Everyone at the Fed knows the definition of “unemployment” and “employment” the way it is defined for each one of those rates and ratios. These are not absolute rates and ratios, the way you try to simplify them into oblivion. They’re measurements of well-defined conditions. This gives the discussions a common denominator. But the Fed looks at numerous other labor market indicators.

I understand that it’s just easier to fabricate your own data to confirm your own preferences rather than dealing with the complexities of measuring the conditions of an immense and complex economy.

Of course they are lying about the numbers Everyone knows this It’s VERY obvious Wolf Can rail on all he wants and I still am not convinced Everything is about deceiving the sheeple now

Hasn’t the Fed always been a trailing indicator, though to some, appearing as if it knows far more than it should. The real cards are probably being dealt under the table.

“The real cards are probably being dealt under the table.”

Yes. The invisible hand makes the big moves, but only when the workings under the table take a break. People run the financial markets, not abstract theories. The invisible hand is the only one that has any respect for abstract theories and it appears to act on them whenever possible.

People steal whatever they can, and they become especially aggressive if it’s not illegal to take what isn’t nailed down. This is human nature. It’s the simplest explanation for much. Nobody waits at the end of the line if they can make someone else wait there while they move to the head or inside the door of whatever is being waited for. Hence algos and putting your people on the inside.

I think the 3 month is more indicative of what the algos ignored. The public perception of demand for money is in the 2-10 ratio and the 10 year rate and ‘the slope of the yield curve’. Nobody writes about anything else, except for the blog post above. A flaccid 3 month would mean a flaccid market for money. Apparently, it’s more forward looking then the pundits realized.

Moral – to get real insight, look where everyone else isn’t in addition to where you are expected to look, then come up with an explanation for the difference. (kind of a herd behavior theory).

Tamara,

The fed is actually the forerunner indicator. The reason they seem underhanded is because they rely on the financial ignorance, of not just the masses, but the political class. Look at what they do and ignore what they say.

The fed says inflation is under 2% and everybody knows it’s a lie. Pushing short term rates up to where they are now attracts money to treasuries, decreasing the money supply, an anti-inflationary move. They are removing liquidity from the system because they can see the inflation. Their favorite method for soaking up liquidity and shrinking the money supply has always been the 10yr bond.

On one hand, raising rates and reducing the balance sheet decreases the money supply.

But, what about the velocity of money as rates rise and people earn income from savings and spend it, as opposed to fake wealth effect capital gains that few if any of the 99% ever spend?

People earning income that’s spent increases the velocity of money which expands the economy and might even be inflationary from a demand-pull perspective. The only people who complain are the ones who used to get free money for paper flipping purposes.

Everyone has been trained to look at the COST, and never the INCOME. Part of the herd mentality mentioned above.

People investing in 10yr treasuries aren’t spending the income, they are investing. If the fed wanted to increase the velocity of money they would not be offering $30 a year for $1000. They would be encouraging you to spend the $1000. The velocity spread between $30 and $1000 is astronomical. Look at what they are doing.

Not written in stone.

This is a new paradigm in which markets “act” not “normal”.

Consider crude oil and the dollar today. Normally when the dollar is up, crude is down and vice versa.

Because of dollar weakness recently, the action has been on the short side in a big way. While being long crude oil, which recently has been trading range bound in the mid sixties.

A short squeeze is in play with the dollar up and crude flat. You would think given these market actions, that the short end of the bond curve would begin to recede. Not so. The Fed’s intervention in the market place has wreaked all semblance normalcy. This as they attempt to “normalize” their balance sheet!

“meander lower for years…”

As in the movie MoneyBall the economy has two avenues;

Take one to the chest and slowly bleed out, or one to the head and it’s over. To me it looks like a shot in the foot and a lifelong limp, with the aid of the Fed monetary cane!

It all depends on whether tax-paying, private sector incomes grow. And there is a better than even chance.

You can’t offshore your industrial engine without consequences.

Otherwise we are back to jiggy-jigging the Monetary ethers. Until it can’t be jiggy-jigged anymore.

Sentiment seems to be that the raises will be so gradual that just stopping them may prove sufficient. It’s morphing into a very slow game of chicken. I’ve got two low-end houses on the market right now and I’m sensing a slow-down from last year. Not critical, yet, but the hype is not matching the reality.

How much money is invested in the 2 yr vs the 10 yr bond? It would certainly explain the speedy movements of the 2yr if there are ten times the number of ten year bonds over the 2 yr. (I’m making the comparison of large cap to small cap stocks, which may be incorrect.)

The two-year yield moves faster because it has a time-frame that ends after two years, and it reacts to the expected events in that time frame. What matters for it is what happens in those two years. For the 10-year, the time frame is a decade, and much can happen in that decade that can bring rates back down.

Conversely, this is why inflation, when it takes off, is such a scary beast to bonds with long maturities. If bondholders lose confidence in the Fed’s ability or willingness to keep inflation at 2%, they start calculating in higher inflation rates for future years, and suddenly, they’ll refuse to buy bonds that don’t compensate them enough for those risks, and prices of those bonds fall sharply, and yields surge.

Securities with shorter maturities, such as the two-year, are much less impacted by long-term inflation fears.

Lotta “mights” in there Wolf. I think the largest is the perceived U turn in Fed policy to QE, that they will go to the whip much sooner this time. And the big threat to that is whiplash, incremental rate hikes allow businesses to make long term decisions. Everyone is moving to the other side of the boat, institutions too big and slow to move quickly. The market seems to believe that buyers of 3% UST10 yrs are getting the deal of the decade, and sellers of that paper, and corporates? Not so much.

RE: ‘glacial’ pace of Fed tightening.

The Fed is scared spitless and given the near- death of 2008 that isn’t surprising.

I’m still convinced that most people, however much they refer to those days, don’t really grasp how unprecedented they were.

It’s really bad in Canada where Joe or Suzy six -pack often think it was just a US problem. In reality the Fed also lent Canadian banks money, but that didn’t stop Canada having its own Asset Backed Commercial Paper crisis, where money presumed to be not lent but ON DEPOSIT could not be accessed.

As other people in the world have seen, it is not a given that a cash machine contains cash. The presence of cash is a function of credit.

Vanity Fair has an archived piece: ‘The Week Goldman Almost Died’ that

MIGHT help some people understand this wasn’t about letting a few banks go under and then we all get on with our lives.

From the confidence people we hear a lot about how much better things are now. Well one thing is for sure- debt isn’t better.

As the Fed tries to tip- toe past the sleeping bear, several factors make it extra tricky: its own ugly balance sheet, a looming trade war connected at the hip with an unpredictable Executive Branch.

I think we’re reaching the end point, now that national deficits must be in the trillion-plus range to avoid a recession.

Even if the Fed restarted QE to reduce the debt buildup, it could not possibly buy a trillion debt per year without creating massive inflation.

It’s the runaway fiscal deficits (or the anticipation of them) that will trigger the collapse.

Nice chart comparing 2s and 10s back to early 90’s.

From the chart, the broad trend for the 10s is down from ~6.x% in the 90’s, down to ~4.x% in the 2000’s, and down again to ~2.x% in the 2010’s. While the 10s are on the doorstep of breaking above 3%, it may not get much higher given the amount of debt outstanding, and would have to break this longer term down trend as well.

The 2s to 10s may compress further and possibly invert, but the 10s may not get much higher from here.

I’m on the bandwagon that says that the incredible 30-year bull market in Treasuries has ended, that the trend has turned, that it was great while it lasted, but that longer-term yields will continue to wander higher and not return to the lows of 2016, though I doubt they will go back to the highs we saw three decades ago.

Oh my, what it must be like to have the job of deciding the price of money….a fundamental consideration in every rational economic decision.

Some here believe the FED saved us during the crisis a decade ago… without examining how effective they were at setting the price of money prior to the crisis. Yes, it was a scary time when a share of Citi wouldn’t even buy a hamburger from the dollar menu. By the way, how many times has Citi been saved? (..and why??) Allowing failures to happen enables improvements/progress because poor decisions made by executives results in pain. The FED has continuously arrested the natural process of making economic progress because the disincentives of making poor decisions have been replaced with incentives. As an aside, if you become frustrated when bad news leads to a rise in equity markets, smile, you are a part of the solution. Everything is now upside down.

There are people who possess a condition that prevents them from experiencing pain. This sounds wonderful, i.e. touch a hot stove and it is no big deal …unless you are allowed to leave your hand on the stove. The FED policies of recent years have actually encouraged just that, and to an extent that was previously unfathomable. Was it politically motivated? That is a subject for another site.

The FED now seems intent on making changes. If this is a genuine effort, the risks for the FED (& the political risks) are obviously quite high. Hopefully, they will not be punished for trying.

The Fed is in charge of monetary policy. Arguably it could do a better job than it has done. However the fundamental problems of the US economy are fiscal. The government spends more and more than it takes in and any hope of correcting this seems more and more distant.

The disconnect begins when Nixon disconnected the dollar from gold. He did this because the government did not want to raise taxes to pay for the war in Vietnam. With gold gone as a limit on limit on money and credit creation all that was left was will power, i.e., politics.

As David Stockman told us in ‘The Triumph of Politics’ it was under Reagan that the deficit really took off.

The accumulated debt of the US since 1790, after WWI , WWII, Korea and Vietnam was one trillion.

Reagan ran on a platform of lower taxes and lower govt. spending. Problem was, he lowered taxes BEFORE shrinking govt.

First part easy. Second part hard.

In vain Stockman prepared spread sheets showing choices between menu items.

So after running up one trillion since 1790, four years into Reagan the debt has doubled to Two Trillion.

Today as we head for ANNUAL deficits of a trillion and a debt of 25-30 T or…those numbers seem like a long lost Eden. The new mantra is ‘deficits don’t matter’.

The last Trump tax cut was the death knell of whatever fiscal conservatism still lingered in US conservatives.

The Fed’s fevers and chills and apparent delirium are symptoms but not the underlying problem.

A good lawyer with a bad brief can seem like an idiot as he tries to make his client seem reasonable.

Even a good business manager of a spend- thrift rock star will be blamed when bills come due. (See Johnny Depp)

Maybe the problem is partly ourselves. We vote for whoever promises the most goodies. If the unborn have to pick up our tab, that’s a problem for them.

But at the rate we are going, when we start trying to mortgage the kids of the unborn, the lenders may balk within our lifetimes.

Agreed on most points, though I think it is hard to separate fiscal matters from monetary policy. Congress likes to buy votes with poor fiscal policy and the Fed enables it.

Hard to see how anyway gets an opportunity to serve on the Fed without being a political hack.

I’ve followed Michael Pento’s commentary on the bond market and he has been saying for some time that the bond market will collapse and that the continued issuance of debt (bonds) has been unsustainable because the debt situation since 2008 was never resolved.

Issuing more and more debt to repay legacy debt. Madness.

+1000

I increasingly wonder if the FED is more-than-in-the-past spooked by its asset book, which is much larger than ever before. Perhaps they really do care about taking a bath on all those bonds. I wonder if QT might accelerate as other players offload USTs.