That would be a first, but it might be happening. Everything in slow motion, even market declines?

There is nothing like a good shot of leverage to fire up the stock market. How much leverage is out there is actually a mystery, given that there are various forms of stock-market leverage that are not tracked, including leverage at the institutional level and “securities backed loans” offered by brokers to their clients (here’s an example of how these SBLs can blow up).

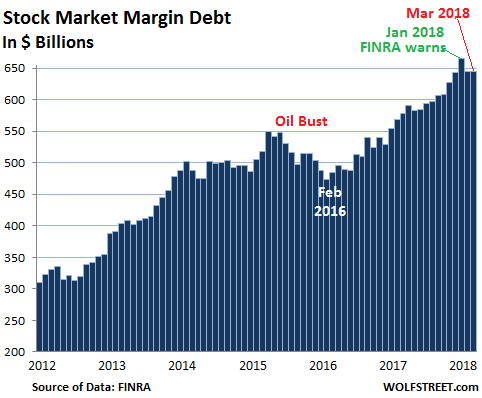

But one type of stock-market leverage is measured: “margin debt” – the amount individual and institutional investors borrow from their brokers against their portfolios. Margin debt had surged by $22.9 billion in January to a new record of $665.7 billion, the last gasp of the phenomenal Trump rally that ended January 26. But in February, as the sell-off was rattling some nerves, margin debt dropped by $20.7 billion to $645.1 billion.

By March, those worries have settled down, and margin debt ticked up a bit to $645.2 billion, but remained $20.5 billion below January, according to FINRA, which regulates member brokerage firms and exchange markets, and which has taken over margin-debt reporting from the NYSE.

In January, days before the sell-off began, FINRA warned about the levels of margin debt. It was “concerned,” it said, “that many investors may underestimate the risks of trading on margin and misunderstand the operation of, and reason for, margin calls.” Investors might not understand that their broker can liquidates much or all of their portfolio “under unfavorable market conditions,” when prices are crashing. “These liquidations can create substantial losses for investors,” FINRA warned. And when the bounce comes, these investors, with their portfolios cleaned out, cannot participate in it.

This is why leverage such as margin debt is the great accelerator for stocks on the way up as it creates new liquidity that goes into buying stocks. And this is also why margin debt is the great accelerator on the way down, when forced selling kicks in and liquidity just disappears.

But this is not the scenario the markets are in at the moment. Everything is so orderly, though it’s a lot more volatile than it was during the run-up last year. And margin debt too has declined in an orderly manner:

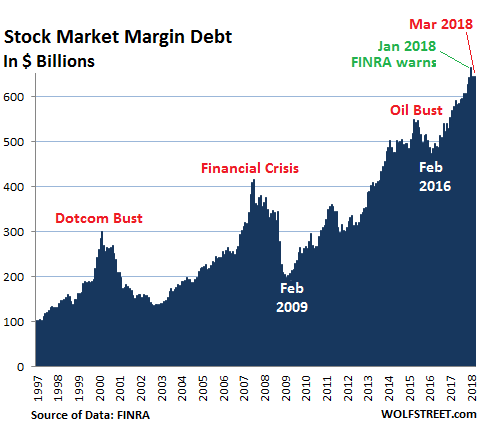

For the 12-month period through March, margin debt rose $67.6 billion, down by nearly half from the 12-month period ended in January, when margin debt had soared $112.2 billion, the fifth-largest 12-month gain in the history of the data series, behind only the 12-month periods ending in:

- December 2013 ($123 billion)

- July 2007 ($160 billion)

- March 2000 ($133.7 billion)

- November 1997 ($132 billion).

Margin debt has soared since 2009, with only a few noticeable down-periods – including during the Oil Bust when the S&P 500 index dropped 19%, and the 2011 sell-off when the S&P 500 index dropped 18%. In March, it exceeded the prior peak of July 2007 ($416 billion) by 55%. But that’s down from 60% in January.

This chart shows the longer view:

During margin debt’s peak-to-peak surge of 60%, nominal GDP (not adjusted for inflation) rose 32% and the Consumer Price Index 20%. Historically, this disconnect has had a tendency to correct via messy panicked crashes and deleveraging. The last three spikes in margin debt are indicated in the chart above. The first two were followed by market crashes. And now?

Clearly, this will correct again. It always does. But the manner in which it corrects may well be very different, more orderly rather than panicky, taking its goodly time, given the glacial pace of the Fed’s tightening and the large amounts of liquidity still in the market looking for a place to go. And this type of gradual unwinding of stock-market leverage would be a first, but it might be happening before our very eyes.

The Fed’s new paradigm: everything in slow-motion. Read… What’s Going On in the Treasury Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Orderly, or less disorderly once that one extra grain of sand makes its mark? But, but, but what about the ECB and Eurozone later on? Will their claim of orderly removal of QE be any more than BS and more BS with another layer of BS just for fun?

This is what makes markets.

As yields begun to increase in the debt sector of the economy purchasing such securities becomes more attractive. However, the shift from equity to debt will cause a deflation of the stock market that will gradually weaken nonprofitable cash burning machines like Tesla, however, is unlikely to completely kill them off. Thankfully we will not see a massive sell of like the kind that caused the Great Depression. I think.

The global economy is actually doing OK…as long as a major war doesn’t break out.

Funny you should say that.

I don’t know. I have a feeling we are (including the Fed) maybe fighting the last wars and trying to draw too many parallels between what caused the last recession/crisis and what may cause the next.

And while we are having our eyes fixed on the usual suspect metrics (housing, fed rates, inverted yield curve,,,), a black swan comes in crashing from behind us. What that might be. I don’t know.

I understand what you are trying to say, however markets are extremely efficient. Whatever your black swan event is, it’s going to have to be big.

I too enjoy the ‘markets are efficient’ axiom.

The fate of the stock market is now hinged on the fiscal deficit. The deficit is now exploding at a trillion dollar pace per year. This is very destabilising and may cause a crisis at some point. Thus, I’m not in the gradual adjustment camp. I don’t see how there can be a gradual slowdown when deficits are putting pedal to the metal. I only see a 100 mph crash ahead.

A slowly simmering economy, suffering years of stagnation and low to no growth. Or a catastrophic blow up and general economic collapse, that occurs fairly quickly.

These seem to be the only avenues ahead for the global economy. There appears to be no middle road. The idea of a new worldwide economic boom happening anytime soon, has slowly died.

The general consensus being that a global financial reset is required, for the economic system at present to continue with any semblance of normality.

Whether this reset occurs slowly or quickly, depends on the very undependable human emotive factor. For now most have a wait and see attitude, while scrambling around searching for wealth protection, where there is scant any to be found.

Hasn’t Japan been sort of stagnant since 1990 or so? I’ve seen it mentioned more than one place/time that what we’re looking at is what Japan’s been going through.

Japan has only been stagnant in terms of inflation. In other words, Japan is one of the few places with true price stability for two decades. On a per-capita GDP basis, Japan’s economy has grown nicely, faster than most. And on a per-working-age person basis, which is what matters the most for individuals, Japan has grown by far faster than any other developed country over the past 20 years.

The “stagnation” label is a New York Times and Wall Street Journal invention. At these papers, inflation is always good, as is relentless population growth (more readers paying higher rates?). But population growth just cuts the economic pie into smaller slices. What matters for individuals is per-capita: the slice of the economy that each person gets.

The big problem Japan has is of fiscal nature, not of economic nature. Its deficits and debt are a gigantic mess.

Thanks for this comment about Japan. This kind of description is what I have heard anecdotes about for many years: the average Japanese feels better off than during the “bubble economy” of the ’80’s. There are lots of unfortunate exceptions, but this is generally what I have heard.

Also, the per-capita GDP is what is important, in my opinion, as you say. The main-stream media and economists fret about the GDP stagnating, but if your population is shrinking, that might not be a very meaningful indicator (‘total GDP’).

It will be an interesting change to the economic models when they try to deal with the math of shrinking total population. Compound growth of certain things doesn’t work out too well with that…

Ah yes, the pundits that talk about the terrible woes of Japan and how it hasn’t gone anywhere for years.

They missed everything that was going wrong in Japan during the bubble and the reasons for it and they have missed the action there over the past 20 years as well.

Mostly likely many of them have never been to Japan.

In regards to any inflation measure it really depends on the person’s unique circumstances.

Inflation in Japan measured at the economy level is supposedly negative. At the personal level there are certain areas where the price increases have been quite large.

These are health, pension, and medical costs. Combined with low wage growth these increases have really squeezed people’s ability to spend. That is one reason why the amount of the salary man’s monthly ‘pocket money’ allowance from mamasan has been going down for years.

Mamasan doesn’t have as much as before leftover from the household budget to dole out to papasan for drinks and after work entertainment.

(When we lived in Japan we did things the ‘Japanese way’ and mamasan would give papasan his spending money every month. I balked when she told me the amount as I thought it was way too high and never spent even half of the reduced amount that we agreed on.)

On a corporate level things are doing very, very well.

The fall in the value of the yen and the huge fall in oil prices (and now somewhat being corrected) has had a huge impact on the corporate sector, but not on increasing wages. Many Japanese companies have huge hoards of cash, but still refuse to increase wages by any meaningful amount.

The other area where there has been a huge change for people and not companies is in the area of inheritance taxes which is going to slam many families as old people die off. More tax to the government and less to the people that were supposed to get the money.

Japan has been printing like crazy for years attempting to create inflation in their own economy, and ABE is now/still going for the elusive 2% target. Problem with that thinking is all that money goes everywhere but into Japan. What Japan IS doing in spades however is exporting RISK. Their RISK flows where their money flows. Some day people holding US stocks and US Bonds will understand what that means.

A few problems concerning Japan. It has NO natural resources (other than perhaps oysters). It processes but no longer the cheap labor pool as it was in the 1960’s. Japan is innovative in terms of robotics, which ultimately reduces the “people” component of anything it’s applied to. Secondly it has an aging demographic. A thrifty gray population. From what I’ve read, it’s Japan’s central bank that buys ETF’s comprised of Japanese stocks. Synthetic. Furthermore, Abe, at present, won’t win any popularlity contests. I haven’t recently followed the Yen vs the Dollar. DOES it matter?

Efficiency,

As I pointed out, I agree on the fiscal issues (debt and deficits). They’re a huge mess. The BOJ is just trying to keep it from blowing up. Ironically, these problems are hardly every pointed out in the NY Times and other clueless media that constantly invoke Japan’s “stagnation” or “lost decade” or similar BS.

As to our other points:

1. Japan NEVER had a lot of natural resources. That’s a strength. It figured out how to have high-value manufacturing, etc. It buys the commodities, turns them into high-value products, and sells them for a lot of money in the global markets. That’s one of the reasons Japan has a large trade surplus.

2. Thank god it’s not a cheap-labor country like Bangladesh. It’s more like Germany, with a large manufacturing base and a highly trained workforce and lots of automation, and it’s doing just fine without cheap labor.

3. Yes, Japan has been a leader in robotics and automation for a long time.

4. In country like Japan, whose urban areas are huge and immensely crowded, a declining population is good for the individuals. Quality of life improves as it gets slightly less crowded (homes get bigger, commuter trains are less packed, etc.). The population is declining in tiny increments, so the economy can adjust perfectly well. It also means full employment for the declining number of working-age people. And they’ll make more babies when they fell like having more babies. So don’t worry.

5. Japan has an eating culture that imho ranks at the top in this world. And they spend a lot of money on it.

Correction: Japan HAD no Natural Resources. Now they have enormous amounts of one that everyone covets the most. Granted this is something they won’t be able to fully tap anytime soon but once the ball gets rolling, this will be the “shot in the arm” the Japanese economy may just need.

https://www.sciencealert.com/japan-just-found-a-semi-infinite-deposit-of-rare-earth-minerals?perpetual=yes&limitstart=1

Japan √

Article

Since 1997 we see higher highs and higher lows, only. NO True correction.

Even with real inflation, and currency debasement, this is way out of line. IMHO.

Am I wrong in thinking a big correction event, is out there.

1929 didnt really recover, until post 1946, and later.

A pretty sad time is coming. People might have to work for their earnings instead of riding on the Fed’s choking out private savers and enterprising income earners.

Growing an economy by inflating assets and stealing (silently) from your neighbors is rightfully ending.

In the meantime our UberRich still beat the dead drum of “free markets”.

The FED, the great (last) Defender-oF-Central-Planning, could regulate Margin Debt as a way to decelerate the inflation of the Stock bubble.

BUT THE DAMNED FED CANNOT SEE BUBBLES AT ALL !

And as the Central Planner of all Central Planners, the FED declines to “control” [“control” is execution of a “plan”– is it not ?] Margin Debt. EVER, at least not in recent decades !

https://www.investopedia.com/ask/answers/032615/why-does-federal-reserve-board-regulate-which-stocks-can-be-bought-margin.asp

Why is that I wonder ? There is a story there, and it is an ugly one for sure.

The last page of that story tells us whom the FED truly serves — after all is said and done. And it is not us proles at all.

The balance sheets of corporate US in 1929 were pristine compared to today. Junk bonds hadn’t been invented yet.

Consumer debt scarcely existed. There were no credit cards.

There were no HELOCS (home equity line of credit)

Hardly anyone financed a car. Most people drove second- hand cars, many of them still Model T Fords.

There were no computers trading billions of dollars in millionths of a second. There weren’t trillions of dollars of derivatives trading on top of those mere billions.

This why 2008 threatened to do in a week what it took years to do after October 1929. The first bank failures in the Depression took a while after the stock market crash. In fact many people believed the underlying economy might be OK.

I forget exactly which week was the ‘The Week Goldman Almost Died’ (Vanity Fair) but it was shortly after Lehman went broke.

There is every reason to think that a credit crisis today could happen much faster and be much more violent than in 1929.

Agree with your comment N Kelly. Plus, everything is simply more intense and volatile these days, not just because of the debt levels in all sectors, but through social media stoking the fires of fear, reactions, rumours, etc.

When the exit rush begins it will be like lemmings off a cliff. Those who are debt free will be standing aside, watching them pass.

Not only that but computers are designed to prevent a massive selloff.

There is a computer program under development designed to stabilize markets. In downturns it buys stock on its own account and recoups from the recovery it automatically creates.

A product of IBM’s Cloud Division, it will be marketed to government as ‘The Bag Holder’

I have to disagree about “computers are designed to prevent a massive selloff” because of the rapid progression of AI, and quant funds that will actually exponentially create massive selloffs that “buy on dip” computers, and even market circuit breakers won’t be able to subside, and will occur over several weeks.

Simply stated – When the dam breaks it will wash away everything to all-time lows with the speed of a light.

I have been in computers since the 60’s, and when the S*Storm happens and it will, these funds will use their maximum leverage to the downside, like we have never seen in our life’s.

Margin calls, bankruptcies, foreclosures, etc galore will transpire, and the destruction caused will be catastrophic, and the Fed and US Gov are out of chips to cover, this time, totally helpless.

The calm before the storm… (:-(

“We will never see another financial crisis in our life time” – Janet Yellon.

“2008 style financial crisis in the future is certainty” -Bill Gates.

People keep asking why should any one holds dollar when it can be printed. Reason is simple, because they have guns and they will ban/kill anyone or any form of competition. To hold treasury and USD is to surrender to those guns, the law and order.

If there is a crisis, at violent levels more than 1929, I guarantee you they will pull out printers. If printers do NOT work, they will pull out guns to make it work.

To go against them is to go against unlimited guns, lawyers, jails. Pick your fight wisely.

I do NOT think any trading bots of “market” manipulators would be able to overwhelm central banks. Central banks own the markets and markets will do their biddings. To say market “force” will finally win is to say revolution will in the end happen. True, but NOT likely in our life time.

How ever, it is another matter if central banks decide to kill each other. Citizens and markets is NOT capable of fighting central banks, but different nations do have enough power to fight each other’s central banks.

The age of central bankers

work together seemed to have passed.

The FED may gradually attempt to unwind. However, at some point the participants are going to rush for the exits. The FED cannot erase herd mentality.

I don’t know Wolf … with the global eCONomy being one humoungous, and rickety, Rube Goldberg Machine, I think I’ll go with the Hemingway Derivative … ‘;0

I’ll change my mind when I see signs that point that way. These things don’t happen without plenty of warning ahead of time. The only thing that surprised me last time was how long it took from the moment I clearly saw the signs and started preparing for it until it actually happened :-]

I agree despite the volatility of the market caused by computers trading in milliseconds, things like this take a long time to propagate. Still, I’m hopeful of whats to come. I think.

Would you articulate the events, highlights & processes of the “The only thing that surprised me last time was how long it took from the moment I clearly saw the signs and started preparing for it until it actually happened “?

There were all kinds of signs. Here are a few, off the top of my head that are easy to explain without having to write a treatise, ranging form anecdotal to technical:

— A clerical worker in her 20s that I watched at an airport who said on the phone that she couldn’t get off work to look at a condo, and then proceeded to buy that condo sight-unseen in order to flip it, and it seems she was getting money from a bank to do so

— Home prices. We moved from Tokyo to San Francisco in 2006. It was totally nuts in SF — though not nearly as nuts as today. Seasoned RE people tell me that today, is like 1999, maybe worse. So that would be a data point to be concerned about. But RE moves slowly, and changes in trend are measured in years.

— “Merger Monday” on CNBC … all the LBOs and how easy it was to get these huge bridge loans and other funding from the banks, and how much insane market enthusiasm there was for this stuff – even the craziest buyouts. We’re getting some of it now, so this bears watching. But it’s not at the same level yet.

— Stock market valuations. They’re there now.

— CEOs were starting to say strange things during earnings calls. Cisco’s Chambers for example talked about “lumpy” corporate demand. That was huge. Everyone got that.

— The bond fund I had quite a bit of money in and that I was watching like a hawk because I knew it had MBS in it. It had been advertised as a “money-market like fund” but yielded 5.5%. When signs of problems became clearer, people started selling the fund. It had a good yield and markets were still calm, so I held out. As people were selling, the fund was liquidating its most liquid positions (Treasuries, high-grade corporates) that had filled the top ten positions (which you can see in the fund’s publications). When the first MBS cropped up in the top ten, I sold. This was before Bear Stearns. It meant that the fund had sold all the liquid high-quality bonds (as had likely other bond funds … so this was likely systemic), and that all heck would break loose once it would be trying to sell illiquid MBS and junk bonds. So for me, the fund had turned out to be a good investment because I got out in time, but not too early. I got out of the stock market too early though.

Eventually, the bond fund collapsed and those staying in it lost a fortune. It ended in many class-action lawsuits and individual law suits that the broker (whose fund this was) settled.

Watching this fund closely gave me good insights into just a risky (dangerous, even) open-end mutual bond funds are. When there is a run on the fund, they collapse. The early mover wins at the expense of the late mover. I now consider a portfolio of individual bonds safer and more profitable than an open-end bond mutual fund. Unless the individual bond defaults, you can hold it to maturity and get your money back, plus you collect the interest. And even if the bond defaults, you often get some money back (depending on what type of bond it is).

If I start thinking about it, I could drag out many more examples from the depth of my memory.

How does one prepare once they see the signs?

By paying a lot of money to a financial advisor who will tell you not to prepare :-]

If you are prepared to ignore fictive earnings that haven’t happened yet, you can go with a mix of cash, CD’s at various maturity points, gold and silver, plus a nice stock of food, water, medical supplies, and the other things you should have stashed away for a natural catastrophe. This is not anything economists with their maximization fixation could stand, but they’re not going to be fairing well if their universities close down and they have to fend for themselves in a post-crash reality.

Naked short-selling should be banned. If an investor believes a stock is over valued they can place their bets in the options market.

Allowing raiders to “borrow” someone else’s stock to drive down the price is wrong. If you don’t own it, you can’t sell it.

This market will trend lower, in a slow motioned decline, until the institutions start the rout through massive short selling. That’s when the margin calls go out and the forced selling begins.

The retail investor, always seemingly unaware of the risks, continues to participate in a casino-style market. They are about to be fleeced again with a massive transfer of wealth going from themselves to the pros.

Compare naked short selling with what one might call “naked long buying”, that is, buying stock without having the money to pay for it. By your own logic, that should be illegal, too. To paraphrase

“Allowing raiders to borrow someone else’s money to drive up the price is wrong. If you can’t pay for it, you can’t buy it.”

So, yes, by all means we should ban buying on margin, and that should include banning corporate stock buybacks that use borrowed money. Corporate stock buybacks should be illegal unless they can be funded by net profits.

One thing I would agree with: Brokers and Banks and so-called should not be able to sell short for their own accounts, unless the sales are backed by capital and margin rules that must be equal to the rules that apply to retail customers. And short positions should be reported in real time, not twice per month as is done now.

It should say “so-called market makers” in the above, feel free to edit and then delete this corrective post.

The stock market should be structured as a commodity market, one buyer one seller, and the commodity, financial paper assets which pays dividends. Naked shorts are no different than naked LONGS or buying on margin. The stock market is rigged to go higher and facilitate government inflation policy. When it ends, and I suspect that the Fed chief and the president, have this in mind, because stocks do not fund government spending, and 45 is a bond man, businesses live and die on bonds not stocks, there will be a lot of remorse.

Naked shorting means the speculator doesn’t even borrow the stock. Its an electronic scam.

Naked short selling is illegal.

“Specialists” and “Market Makers” are necessarily short as part of their “market making” function — as they (are required to) take the other side of trades that occur in their domain.

THAT MEANS SELLING TO A WILLING BUYER WHAT THEY DO NOT YET HAVE. And there is a risk in that, but Market Makers know the game and the risks well. They suffer losses rarely.

When naked short-selling is discovered the SEC can and will prosecute.

https://www.sec.gov/news/press/2008/2008-204.htm

Look up Market Makers and Specialists to see an explanation of their being able to naked short sell.

https://www.sec.gov/investor/pubs/regsho.htm

Ha – how many naked short sellers have actually been prosecuted?

*Looks at chart… 2011?

The August 2011 stock markets fall, and

Standard & Poor’s did downgraded America’s credit rating from AAA to AA+ on 6 August 2011.

Ah that…

I don’t think the US will be hit by a credit downgrade this year since making the dollar stronger does make US debt more valuable.

But note that I said this year.

The did the US stock market get so high in 1929?

Margin lending.

Of course, it’s different this time.

An “orderly unwind” might be expected in a market experiencing irreversible upward pressure. One is naturally less inclined to borrow with a fortune at one’s disposal. Multi-trillion dollar bank holding vaults begin to leak, then trickle, soon erupt into the economy sending assets to the Moon and the dollar to the Fiat Mortuary.

That chart is correlation, and margin debt will contract while stocks go lower, although technically all shorts are done on margin. With the advent of ETFs a lot of this has been done with swaps and derivatives, if you are retail and you want a straight up short you need margin. (This is one way the market makers can squeeze the players) However now there are so many workarounds, they may not be able to squeeze the shorts and increasingly I feel there is a mercenary aspect to big institutions who would not hesitate to go all in on the short side. For the moment the players who want to take the market down, are a) going to let the buy the dip crowd set them up b) respect the market circuit breakers and avoid tripping them c) have to have somewhere else to move the money. The defenders of the stock market (Fed, etc) know they are overwhelmed, and may capitulate. Short sharp drops are preferable to a long bear market and at some point the Fed may actually rationalize selling the market to provide stability.

Something I’ve alluded to and asked about here seems key to me: the absolute quantity of capital running around compared to the debts it is theoretically back-stopping. That markets are being influenced (manipulated?) by central banks is unquestionable. That the number of players who matter in these markets is not only finite, but quite small, seems also to be true. My question is: do they have enough ammo (capital) to keep these markets in stocks, bonds, and derivatives afloat if they hit choppy water? I just don’t know the answer. I would guess that up to a certain level of buffeting, they can. But at what point does the storm sink the ship? I would love to know the answer.

Always the question, can they get the liquidity where it is needed? The stock answer has been to recapitalize from the top down, but rank and file GOP members are not adverse to funding consumers directly. I once started the Free Gasoline for Everybody Party. My idea was to take the trillions we were spending on the war in Iraq, to protect oil reserves, and pay directly for US consumers energy needs, which would have freed up a lot of consumer spending. Government deficits are like giving to charity, you end up losing half your donation (revenues) to administrative costs, lavish parties, and corruption.

Inflection Points don’t happen slowly. And you cannot predict them. Although the rate rises may be slow, the impact on balance sheets is harsh.