Fed’s favorite inflation gauge spikes, consumer spending holds up solidly.

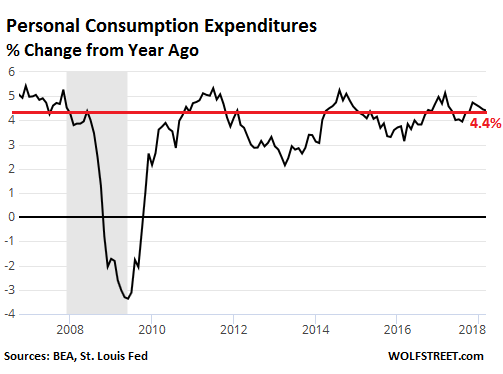

Consumer spending on goods and services – which includes anything from toys to rent and which accounts for over two-thirds of GDP – rose by 4.4% in March from a year ago, according to the Bureau of Economic Analysis this morning. This growth rate is in the upper third of the range of the past few years. Solid but not spectacular comes to mind.

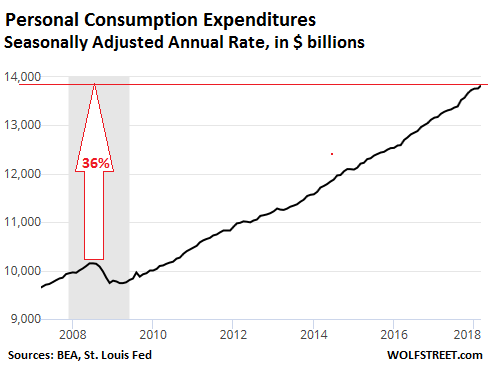

In terms of dollars, the seasonally adjusted annual rate in March (which shows what the total amount of consumer spending would be for the entire year at the rate March was going) reached a record of $13.82 trillion, and remains on the same trajectory of the past few years. The seasonally adjusted annual rate in March is 36% above the mini-peak in July 2008:

But these numbers of consumer-spending growth do not include the impact of inflation, and inflation is stirring.

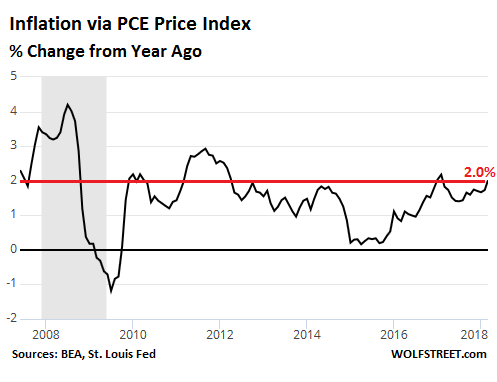

The BEA also released the PCE price index this morning – the Fed’s favorite inflation measure because it usually tracks lower than the Consumer Price Index and thus further understates the deterioration of the purchasing power of the dollar as consumers experience it. The PCE price index rose by 2.0% from a year ago, which is right smack-dab on the Fed’s target. And it’s up from 1.7% in February. Note that the Fed’s target of 2% inflation isn’t a minimum, but a target.

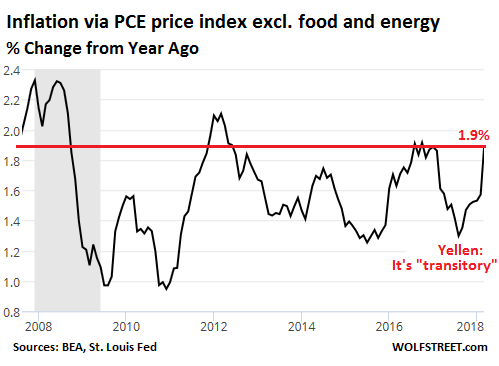

The Fed is even more focused on the PCE price index without food and energy – not because food and energy are not important to consumers, but because their prices can gyrate wildly. And this core PCE price index jumped by 1.9% from a year ago. Up from an increase of 1.6% in February. And the spike-like trend looks worrisome.

In the chart below, also note the low point in core inflation last summer, when Fed Chair Janet Yellen said that this was “transitory,” and she pointed at some specific factors, even as the financial media and Wall Street pooh-poohed her and clamored for the Fed to back off its rate hike path:

The PCE and core PCE inflation measures came in as widely expected. That inflation is now rising is no longer surprising anyone. It has been documented in numerous data points, including earlier this month when the Consumer Price Index for March surged 2.4% year-over-year, and the core CPI (without food and energy) rose by 2.1%.

Price pressures are building up in the pipeline to the point where companies are beginning to fret about it. Just today, the ISM Chicago Business Barometer reported ominously that the indicator for input prices paid by companies surged 22.8% compared to a year ago:

Input material prices continued to rise in April, soaring to a near-seven-year-high. Up 22.8% on the year, the Prices Paid indicator surpassed the 70-mark in April for only the third time since 2012. A wide range of inputs were reported as more expensive on the month and some firms felt uncertainty was driving prices higher.

These kinds of anecdotal and not so anecdotal tidbits on rising price pressures – including the surge in transportation costs – are now forming a steady drumbeat. This isn’t just one item, such as energy, or just a seasonal thing, or whatever: It’s broad based and ongoing and is working its way through the economy. And the Fed sees this too.

Today’s data is the kind of data the Fed will drag out to justify further rate hikes, spaced more closely together, though it will continue to use the word “gradual.”

But for now, the Fed remains on its track of only hiking rates at meetings that are followed by a press conference. There are four of those meetings a year. The FOMC’s meeting this week will not be followed by a press conference, and therefore I don’t expect a rate hike – a rate hike during that meeting or any non-press-conference meeting, would be a “monetary shock.” And this Fed is not likely to dish them out, especially not with four of the seven slots on the Fed’s Board of Governors still being vacant. But I do expect a word or two about inflation approaching its target.

The costs of salaries, wages, and benefits are a combustible fuel for the Fed’s tightening machine. Read… Employment Costs Surge Most since 2008, Fed Raises Eyebrow

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

$IRX 13-week Treasury 2 bps over FFR.

No hikey this week; check back again in June.

Correct. As explained in the article.

The yield curve wont stay negative for long? The Federal Reserve would love to feed long paper to the curve to keep it positive? Dollar bill dollar bill .

Banks get no sugar? Come on man!

There is a large, ominous, obvious triangle on the S&P 500 daily, since the February lows.

If it resolves downward, then the June hike everyone expects will likely be shelved, and we’ll look to the meeting at the end of July.

The Fed has been hiking rates during this cycle ONLY after meetings with press conferences. The Fed doesn’t follow my, your, or anyone else’s charts. It has its own plan. And it communicates that plan as it goes. The next meeting with a press conference is in June. That’s when the next rate hike takes place. The July 31/Aug 1 meeting is not followed by a press conference, so no rate hike unless the Fed wants to administer a “monetary shock,” which I doubt for the reasons stated below. The third meeting this year with a press conference is in Sept. That’ll be the third opportunity for a rate hike this year.

If the Fed does four hikes in 2018, the next three will come in June, Sept, and Dec. You can forget the charts.

Please read the last paragraph in my article above, which was totally validated by the FOMC statement today. Here it is again from my article above:

“But for now, the Fed remains on its track of only hiking rates at meetings that are followed by a press conference. There are four of those meetings a year. The FOMC’s meeting this week will not be followed by a press conference, and therefore I don’t expect a rate hike – a rate hike during that meeting or any non-press-conference meeting, would be a “monetary shock.” And this Fed is not likely to dish them out, especially not with four of the seven slots on the Fed’s Board of Governors still being vacant. But I do expect a word or two about inflation approaching its target.”

√

The FED policy on rates and the sheet is not set in concrete, just deeply set, in hard dry clay.

It will take a big big storm to loosen it and change its direction.

d,

I think the Fed isn’t going to make any big changes in trajectory until at least three of the four vacant slots on the Board of Governors are filled. Right now there are just three people on the Board. The Board is the core of the FOMC. I think they will just keep going straight until they have a full or nearly full Board.

√

“If it resolves downward, then the June hike everyone expects will likely be shelved, and”

Downward is the desired direction.

What is not desired is rapid/aggressive/sudden, downward movement.

So Unless the Downward movement is rapid/aggressive/sudden you may be disappointed with your projection.

thank you for the work you do

So by tsking inflation into account; did people expend almost the same or less than last year.

How about the “grocery index”?

And is how much the groceries you buy have risen compared to the same month last year?

The grocery index tends to be quite good I have found.

Spending rose 4.4%. PCE inflation rose 2.0%. So real spending might have risen 2.4% (that’s not exactly how the math works, but close enough).

We’re in a new labor universe these days. Boomers are smack in the middle of their mass transition into retirement. I constantly hear business owners tell me how they have to beg older workers to stay on just a little longer. What happens when they finally say “uh, sorry, I can’t stay any longer”

What if the participation rate is on a permanent downtrend? The Fed can tighten all it wants, but supply and demand will assert itself eventually.

Has the Fed accepted that the demand side of the equation is the only place to move now? But lower demand for labor = lower GDP, no? Or are they hoping for a continuation of the automate-our-way-to-productivity model?

Begging us to stay on a little longer ? On what planet … or more specifically in what industry ?

The reality is as a boomer they’re pushing you out the door as fast as they can in order to replace you with someone younger , less experienced and a helluva lot cheaper……. nine times out of ten before your full retirement kicks in .. and more often than not before you qualify for any retirement benefits at all .

And guess what … once they’ve forced you out .. try getting another job as a boomer .

Lucky me being self employed I chose early retirement at age 59 whereas I can’t tell you how many associates , neighbors friends and relatives have been forced out the door before age 60 … never mind 65 .

So how are your friends financially? Did they save like there was no tomorrow in case what could happen actually happened? Correct me if I am wrong but there will be a lot of people pushed out over the next decade that will be taken by surprise as the age of those pushed will drop and they will not have ever thought it would happen to them and as such, have not saved and as a result, several rungs down the socioeconomic ladder.

“And guess what … once they’ve forced you out .. try getting another job as a boomer .”

You probably won’t unless you have some unique or extremely specialized skill set that few other people have or be willing to work in some McJob that wrecks your mind/or body.

So you better have enough put away to survive until retirement pay kicks in as nobody is going to help you.

And here in Oz we have ‘means testing’ which limits how much you can collect from the government if you are unemployed or retired.

Both the conservative and left leaning governments have chipped away at numerous benefits for people on the lower income levels, married couples, and retirees over the recent past.

One of the biggest was the non-working spouse tax credit which was adjusted for any type of income (interest, dividends, etc) the non-working spouse had. The max tax credit was A$2500. It used to offset some of the disadvantages of not having a spouse that worked and could use the tax free income threshold here.

Another was a tax credit for medical costs over a certain threshold. That is gone as well.

“Too much” other income or assets and you’ll find those unemployment or retirement benefits whittled down to nothing. How much is “too much” has been recently changed with many people here on the old age pension losing most or all of their pension.

Do the right thing, save your money, and then find the rules changed in the middle of the game. Thank you very much.

IIRC starting in November this year another big change is coming to those who get unemployment in Oz. For those over 55 the requirement will be to put in 10 hours of ‘service’ a fortnight plus whatever the other requirement there are.

I’m not sure what all the requirements are, but I think that people can do volunteer work at an approved entity to fill that ‘service’. I wonder how in the world there are going to be enough ‘approved’ activities to fit in all those hundred of thousands or people…………

There’s no substitute for having an education and skill set that make you valuable, along with a work ethic of trying to be the absolute best at what you do. Make yourself indispensable and you’ll have a far better negotiating position with your employer. Mediocracy isn’t going to cut it in today’s labor market.

I don’t have much sympathy for folks that didn’t work hard in school or at work, didn’t save money when times were good, but still feel entitled to a great income, job security, and unearned, unsustainably generous benefits in retirement. Sorry. It’s a dog-eat-dog world out there – Boomers are going to have to come around to what millennials have known for awhile now.

@TJ Martin: on the trades planet.

Plumbers, electricians, machinists, pavement specialists, heavy equipment operators, etc.

My anecdotal experience is that I must plan further and further ahead, and use higher inflators (I’m over 3% at the moment, whereas a year ago I was comfortable with 2.5%) for 5- to 10-year pro formas.

Most Millennials are chock full of tech and software degrees and certs, which are useless in the trades. A Milennial electrician can dictate the terms of his hire, including signing bonuses. With a few years experience, he can charge *more* than the boomers because he can still climb and crawl.

And no, I didn’t make a mistake by saying “his”. Young women are eerily absent in the trades. I see a fair number of GenX and Boomer females on sites, but not Milennials. I have no idea what’s going on, I’m just reporting what I see and hear.

“Boomer’s are smack in the middle of their mass transition into retirement”.

Not quite. Almost, but not quite.

The baby boom generation came in three waves spanning the years 1946 – 1964 an 18 year run. The first wave turned 65 in 2011 with the last to come in 2029. This event is a paradigm shift.

The funding for all pensions will suffer a shortfall and collapse.

Just do the math. It does not lie.

Real disposable income continues to shrink, as the cost of living now exceeds what incomes and debt increases can sustain.

Credit card debt hits a new record high every month now, as the average household is using debt to help make ends meet.

There have been zero times when interest rates have risen that did not eventually lead to negative economic and financial market consequences.

Hiking rates into one of the slowest growth recoveries in history, will do nothing but automatically apply the brakes. Just do the math.

– Nope. When I look at the chart(s) then it’s quite liekely that the FED will LOWER rates the next time the FOMC meets.

– Nope. (Price-)Inflation DOES NOT drive/determine interest rates. The history since say 1970is repleat with such examples.

For a year and a half, in your comments on this site, you’ve been predicting that the Fed would lower rates. You’ve been wrong about this without fail for a year and a half :-]

… and if I may Wolf … he’ll continue to be wrong assuming he continues to make the same prognostications ;-)

Simple fact is the ‘ rate train ‘ has left the station and the only way now is up . Either that or total collapse

PS; Wolf … methinks I’ve sussed out the continuing insane real estate bubble here in the Denver metro area … everyone is all in … betting the farm ( and then some ) that Amazon will pick Denver to be their next hub . Hmmm …..

I am with JM on this, the reasons for the Fed raising rates are (surreptitious?) one to defend the dollar and two to prep the skids for fiscal spending, monetization of government debt. Raising rates drives inflation, or rather lowering them caused the price of crude oil to drop in half and flooded the market with supply(DEFLATIONARY). The Fed would lower rates if the stock market crashed, or if they thought the dollar was catching a bid, and if stocks crash (which I feel is their purpose) then the proposed bond sale can go ahead without the carrot of higher premiums. A rate lowering has several rationale which the rate hike policy never made sense (unless you believe Rickards who said rate hikes were done so THEY COULD LOWER RATES when the recovery crapped out). I don’t think the market cares about credibility at this point, (they want results) so the Fed can lower.

The fed is building “powder stock”, and cleaning its balance sheet, in it what it knows, is still a shrinking, real economy.

It has to be ready for the correction, it knows must come, and when it does, the $ will be the strongest and cleanest dirty shirt, AGAIN.

I didn’t agree with JM before but like most people predicting a collapse, they are wrong until they are eventually right.

The American rate shouldn’t stop going up yet, given there isn’t a noticeable collapse in the American system yet. The warning sign I see north of the border is that Bank of Canada halted it’s rate hike planned for March, with 1.25% being the point it can’t seem to surpass.

Wallstreet hasn’t recovered from its Jan. peak and it might be a few years before the bottom is found given the number manipulation and denial from the industry.

– Agree. But the FED is “Data Dependent” and the only thing they look at is the 3 month T-bill rate.

– I am actually quite surprised to see that investors are still so bullish and have been bidding up that one rate. So, don’t blame me that this rate has moved higher and higher. Mr. Market remember ?

– This 3 month T-bill rate gave a warning in january of this year that there was a Sell Off up ahead. It gave me one month in advance that the sell off was about to happen.

– However, when short term rates move above long term rates and short term rates keep rising then that’s the confirmation for me that the 35 year bull market in bonds has (finally) come to an end.

Throw away all the traditional economic and financial theory.

It doesn’t work anymore because it relies on such ideas as the Quantity Theory of Money, the Velocity of Money, Interest Rate Risk, and Risk-based Pricing.

In the world of QE and all those other crap monetary easing programs foisted on the markets by the BOJ, BOE, ECB, and others they have destroyed the ability of the markets to function ad to discover prices and to price risk.

A flat yield curve in this type of environment means nothing as the measures to define risk have been destroyed.

The FED will continue to increase rates until it gets to a point where the markets react in a hugely negative manner. QE unwind will also continue until the markets are able to re-price risk in a ‘normal’ manner.

Totally correct.

This is a Qe market STILL.

Until we return to a completely normal Market, and have the benefit of hindsight. We will not be able to objectively Annalise all of what has happened and deduce the rules for any future Qe market period. Even then, those rules will be only a guide, as a future administration may possibly cooperate with the FED. As opposed to the P 44 administration, which did not do so.

One of the things that made the period so difficult, was the failure of the P 44 administration to play its part. leading to the FED Speak rebuke “Monetary policy alone can not resolve the economic issues which face us” to the P 44 administration and congress.

They know they’re going to raise em up right into a recession but it’ll be worse if they don’t

Had the elections gone differently, rising rates would likely have been a wisp in the wind and low to negative rates would be the new normal today. Printed money would be a replacement for saved capital. Asset bubbles would be a replacement for income from capital. Actual saved capital would be seed corn and eaten out of necessity.

Fortunately, that’s the situation facing the rest of the world, by their choice. We are in a position to rebuild the part of the capital base that was wasted away over the previous decade. The momentum, here, now, is based more on historical economics rather than new age globalism where low rates, low income, and open borders are considered the wave to ride.

Having said that, the Fed is a tea leaves reading body. They know where their future lies and how things have changed if they don’t go along. This means rates will rise for whatever reason is easiest to sell and defend. “Inflation” is a good enough reason. Had things gone differently, it would be a good reason to ignore for “a bigger purpose”.

BTW, the rebuilt capital base will be a massive tool for international competitive advantage. Those who ‘ate the seed corn’ will take what we offer. QE only works if everyone does it equally. The one who opts out wins and eats the lunch of those who continued. That’s us.

” QE only works if everyone does it equally. The one who opts out wins and eats the lunch of those who continued. That’s us”

Untill you add a variable like P 45, who is changing all the trade rules (some of which need gently and slowly changing in a good way) in the stupidest of ways far to quickly.

Which will probably upset the balance, seriously.

Agree that changing trade rules will help the capital build. Low rates and QE are only a part of the picture. Also needed, and also on the way out, here, are open boarders and low wages.

Most people don’t understand negotiation and naively assume ALL parties are honest in all parts. Many countries have been taking advantage of the US, with US support from previous times. Great negotiation with parties who would rather die than change policies takes a strong and sometimes radical ‘sounding’ starting position. This is to get and keep the attention of the ones who would rather you go away. Along the way, which can LOOK rather messy, things spiral into something more traditional and likely successful.

There’s other types of negotiation strategies for those who can’t be trusted. The above is only one, but is the one being used most regularly for foreign policy.

Open boarders and low wages need to gone for the capital build. Unclear in my post above. It looked like I was for them, not against them.

‘The last two times this ‘classic late cycle activity’ emerged, a recession soon followed:

4:40 PM ET Fri, 27 April 2018 | 01:36

A disconnect between the best- and worst-performing sectors this year is raising a note of caution to some market watchers.

Recently, the degree to which the 2018 market-leading consumer discretionary sector is outperforming the biggest laggard, consumer staples, has reached extremes, said Larry McDonald, editor of the Bear Traps Report. ‘

This is from CNBC’s Trading Nation

Does anyone know WHY this is the case?

I would have thought the opposite: that households cutting back on discretionaries to buy staples (I’m assuming this includes food) was a bearish sign of belt tightening.

Conversely, I would have thought that increased spending on stuff the consumer does not need was a bullish sign.

More discretionary spending should be bullish, people eat out instead of buying groceries. go to the movie (Avengers set a new record) rather than watch TV. The psychology of consumer spending moves in nebulous ways, and right up until housing collapsed in 2008. Bob Prechter believes investors sell stocks when their collective psychology turns negative. I believe the opposite, people gamble and spend when they feel desperate.

“and spend when they feel desperate”.

And what do they have to spend with? CHARGE!

Yes, they max out their credit cards.

There are people who budget their grocery bills, and when there is nothing to eat in the house they go out.

50bp?

No way. Not this Fed. No rate hike this week. 25 basis points in June. 50 basis points would be a “monetary shock.” I don’t think this Board of Governors, being down to just three folks, out of seven, would have the guts to do this.

Yes but the possibility of getting a majority vote with 3 people is much better than with 7.

I wish Powell would just start “normalizing” interest rates right now and stop pussy-footing around. Savers and pensions have held the bag for long enough. We’ve turned credit from a resource into a drug for far too long. They say we can’t raise rates much because companies are leveraged up to their eyeballs from stock buybacks, acquisitions, etc., zombie companies just holding on need cheap credit, or we can’t destroy the “wealth effect” this has built. Tough. We’ve been drunk on low rates and we might as well get on and start to face the hangover that’s coming. You can have a smaller fire now that burns the duff off the forest floor or you can let it build up and have a massive fire that burns down the forest. PS, I see car companies have again gotten “hooked” on the high mark-ups from SUV’s and pick ups again like ten years ago. That worked out well. Welcome to reality, enjoy your stay.

I’m in the camp that thinks the Fed will back off rate increases if there is any hint of a recession.

One problem with the Fed’s thinking is they see no purpose to a recession. They will admit that growth after a recession is stronger, but in their mind, the growth would bring you back to where you started. In the Fed’s mind, why do something that brings you back to where you started. You might as well stay where you are and avoid all the dislocations.

The flaw in this thinking is that it avoids any consideration of systematic risks. Staying where we are means that the debt will keep rising. A depression would come eventually, and it would be a doozy.

If the Fed appreciates systematic risks, it will continue the tightening until we are in a recession, and then it would only delay further rate increases, not reverse course.

However, I see no evidence that the Fed thinks about the long-term health of the country. If they did think long-term, we wouldn’t be where we are today.

The Fed can change its mind though. I’m open to that. But until I see evidence of a real change, I’m assuming the Fed is a spineless can kicker when it matters.

I hope they surprise me.

Maybe…

However, I think that even Neel Kashkari who has been quite vocal about not raising rates for the past 6 months wants to “Wait and See” in June…

https://www.cnbc.com/neel-kashkari/

How can the Fed continue to raise rates when other major CB’s

aren’t ? Does the Fed think other CB’s will be forced to follow ?

ECB will follow. BOJ may not.

I am in the camp that believes that ECB and BOJ cannot and will not raise rates!

I wouldnt put money on that.

Most of the north wants the rug pulled from under the over-leveraged club med Banks’s, as they are holding up banking reforms needed to further deepen Economic union.

Just as they want the ECB balance sheet reduced particularly its club med State bond holdings.

The chances of teh next ECB head shielding Club Med as draggi has, are below average.

Not to do with Club Med but Italy. Without free money, EU may come a cropper. How else can you explain the yields in the EU?

I could be wrong, as I often am.

An example of inflation for you. The last three years; 2016, 2017, 2018; in February / March of each year I have purchased lumber from Menards (closest home improvement store) to build a raised garden bed. Each 4′ x 24′ bed has exactly the same materials, same SKU numbers and I saved the receipts. Materials are 1 – 2×12 – 8′; 4 – 2×12 – 12′; 5 – 4×4 – 8’/ all AC2 Green Treated Ground Contact lumber. I used my 1999 Ford Ranger that I have purchased used in 2000 to haul materials and topsoil / mushroom compost for filling the beds.

Total pre-tax cost on the receipts is:

2016 = $130.75

2017 = $143.45

2018 = $154.29

Luckily I have enough gardens at this point that I don’t have to see how much it will increase next year. Tell the fed it is 8-10% inflation in lumber.

Yew cherry-picked those numbers fir convincing even a larch enemy, but I cedar your point.

$IRX will warn us in advance of any Fed hikes. The Fed will follow.

Chris…………

Your opening comment is a peach. I wood like to say that I pine for good wit. Have to go now. I need to spruce up the place.

I think you may have gone out on a limb on this comment.

At least going “out on a limb”, you can open a branch office, unless of course you’re barking up the wrong tree. In which case I’ll leaf you alone. Some may get stumped on this one!

My new laptop cost $800. It’s ten times as much laptop (processing power, memory, etc.) as my laptop seven years ago that I bought on sale for $1,200.

The point is this: When you cherry-pick just one example — lumber whose prices have surged in part due to Trump’s lumber tariffs against Canada — you get funny results.

Good examples that show how inflation differs for each person.

So for Wolf the question is: is the fall of $400 in the price of the laptop over 7 years combined with any real improvements (those that lead to productivity increases – you know watching movies from Netflix without buffering!!!) enough to offset other costs in those seven years?

For Insta will the increase in output from the additional garden bed offset the increase in cost of the materials?

Here in Oz the cost of booze and tobacco increased quite a bit in the last quarter as did education. I don’t smoke so the number is meaningless. I have a cider once in a while, but never buy some unless it is on sale so again not really material to me. Education?

Nope, not in the basket and never will be again. Gasoline was another item that increased in cost (Transport) so yes, I got hit there, but as I don’t travel to work anymore the amount I now purchase has decreased so again not as much in the basket.

Vegetables decreased in price, but my garden this summer wasn’t very good as a result of the weather. Fruit – a total disaster except for cherries so we’ll be buying apples and mandarins this year. Higher costs there………….

The result……….who knows!!!

The Federal Reserve Board are a bunch of idiots! No inflation? Look at the cost of housing, insurance of all kinds, utilities of all kinds. They have created the largest asset bubbles of all time with unnaturally low interest rates for 9 years. Total corp debt was $2.9 trillion in 2008, now it is $6.2 trillion. I sold most of my stocks and paid my house off. Now buying gold and silver which are the only non inflated assets left on earth.

Is it a bubble or is the currency devalued? I suppose that depends on whether the current devaluation reverses due to a crash. And in any case, they’re not idiots – they pulled off the biggest transfer (theft) of wealth in history! Evil but brilliant.

It isn’t often that I say this…. but Yellen made a superb call in the face of very heavy pressure when she made her “transitory” remarks. Excellent analysis by her and her staff. Of course, she also said there would be no financial crises “in our lifetime”, which is true so far and I expect for not much longer.