But it’s a godsend for savers.

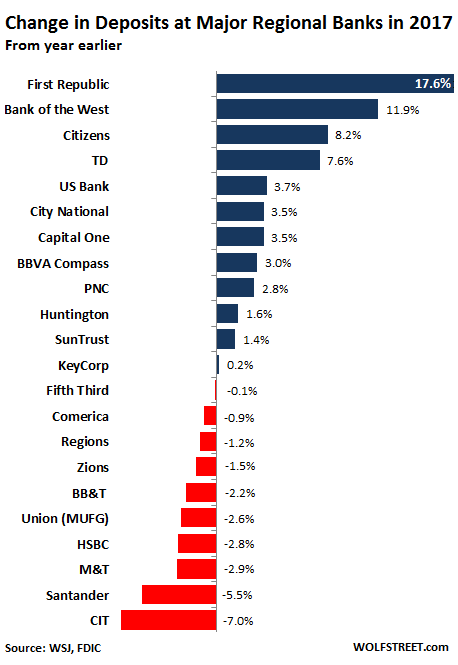

The three biggest banks combined – JPMorgan Chase, Bank of America, and Wells Fargo – increased their deposits by $118 billion in 2017 from the prior year, according to a Wall Street Journal analysis today of FDIC data. At the same time, 10 of the 22 major regional banks lost deposits. But some regional banks went all-out, and their deposits surged. This brought the tally for the 22 regional banks combined to an increase in deposits of about $55 billion.

Competition for cash has returned with a vengeance, after the Fed stifled it in 2008 to keep the cost of funding for banks to near zero so that they could maximize their profits in order to rebuild their capital after teetering on the verge of collapse. Savers paid for it.

On Friday, I described the all-out scramble to attract deposits from my boots-on-the-ground view, with Wells Fargo out-competing other banks by offering 2.25% for 13-month FDIC-insured CDs, and more for CDs with longer maturities, but only through brokers (“brokered CDs”), and not to its existing customers, with whom the bank is exceptionally stingy.

This newly aggressive approach to gaining deposits has some impact on other banks.

M&T Bank Corp, third from the bottom in the chart above, experienced a 6% drain of its deposits in Q1, after having experienced a 2.9% drop in 2017. “It’s a big concern for us and the industry,” CFO Darren King told the Wall Street Journal.

Wells Fargo, according to my own analysis of its Q1 earnings report, showed surging deposits in its “community banking” category (consumer and small business), but declining deposits in its “wholesale banking” category, and plunging deposits in its Wealth and Investment Management (WIM) category. “Average deposits” in Q1 compared to a year earlier:

- Community banking: +4.1% (+$30 billion), to $747.5 billion.

- Wholesale banking: -4.1% (-$19.3 billion), to $446 billion.

- WIM: -10% (-$19.6 billion) to $178 billion

Of these deposits, $359 billion were “non-interest bearing” altogether. And many of the $938 billion in “interest-bearing” deposits carried only minuscule interest – so minuscule that it’s essentially zero. But “brokered” CDs with which Wells Fargo is aggressively trying to recruit new money from non-customers helped push its average “deposit cost” up by 100% year-over-year, albeit from a minuscule 0.17% in Q1 2017 to a still minuscule 0.34% in Q1 2018.

Deposits are a crucial and very cheap source of funding for banks, which make money by lending to their customers at higher rates than their cost of funding. So the name of the game is to keep “deposit costs” down while attracting enough deposits to lend out. And Wells Fargo’s still near-zero average deposit cost, even after the interest rate increases in the market, shows just how well this equation is working.

While deposits in checking and savings accounts can be volatile, as people might draw their money out all at once (run on the bank), CDs provide much needed funding stability, so banks are willing to pay a little more. But if deposits dwindle at a bank, it might have to pay a lot more for funding from other sources, or it might have to curtail lending, which would crimp its profits.

The Wall Street Journal today observed in reference to the efforts by the biggest banks – such as JPMorgan Chase, Bank of America, and Wells Fargo – to attract deposits:

Welcome to the new world of Main Street banking, where deposits are starting to head out the door after years of growth. This month, major regional banks reported the increasing competition for deposits in their first-quarter earnings. Some lenders, including Dallas’s Comerica Inc. and Regions Financial Corp. of Birmingham, Ala., lost deposits compared with a year ago. Others are still adding deposits, but at a much slower pace than recent years.

But it’s not just the regional banks that have watched their deposits drain, according to the Journal:

The smallest U.S. banks, which tend be community lenders with a handful of branches, have also seen deposits decline, according to an analysis by investment bank FIG Partners.

And these declines in deposits at some banks – while other banks are aggressively pursuing and gaining deposits – “could mark the start of an important industry shift where deposits become less plentiful and Main Street banks do more to compete for them.”

That competition, however much banks may hate it, is a godsend for savers and small businesses that have placed a total of $9.1 trillion in “savings deposits” at all “depository institutions” — which includes credit unions — in the US. If rates rise across the board by one percentage point, it would amount to about $91 billion a year in extra income and thus extra spending money for these people and businesses.

For most banks, running short on deposits to lend out isn’t a huge issue just yet: At the end of 2017, about 72% of the deposits were lent out. So on average there’s some room left, though for some banks, it might be getting tight.

Banks are focused on another issue: Rising interest rates. By this time next year, short-term rates might be a full percentage point higher than today. And Wells Fargo might have to offer 3.25% on a 13-month CD to attract more deposits, or else deposits might start draining from its “community banking” category. So if it can get customers to buy its currently offered 25-months CD at 2.75%, it locks in this source of funding for two years at a lower overall rate. And the fact that banks are now fighting over deposits, and that they’re outbidding each other, shows that they take the likelihood of higher interest rates, and higher funding costs in future years very seriously, and are preparing for it.

Here’s my boots-on-the-ground report of how Wells Fargo is doing it. Read… I Asked my Wells Fargo Branch about CDs with Higher Interest Rates. This is What Happened Next

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Full online banking, no branches, no expenses: Ally

Ally’s cd’s used to be the highest rated, but now the brokered cd’s offer higher rates and are easier to sell in a pinch.

Banks are nothing more than ‘Roach Motels’ for your wealth.

Maybe but most people need a cash component to their wealth. And there is not better stash right now than online savings or some CDs. Better than money market funds.

Where do i go to get cash?

“Where do i go to get cash?”

The ATM?

(And please, don’t call it an “ATM Machine”. Please.)

Wolf has the capital ratio changed lately? FYI, you might want to use new tab/new window for embedded links so viewers don’t leave the article.

In most browsers just hold the CTRL key while you left click the link – it opens in a new tab.

A friend of mine recently received her payment from the Wells Fargo class action lawsuit with regards to lines of credit and services she didn’t request. After having her credit ruined and having to spend countless hours filing correction requests with the credit bureau’s, she received $1.47!

But the lawyers got rich :-]

Well – As the lawyer of a friend once said: “She can always throw a half-brick through their window”!

Tide is changing here in Canada too…. I have a account where my cash was getting 2.5% and until August, and they sent me a offer of 2.75% to the end of the year. I was content with 2.5% but hey sure i’ll take more

If there is a will,there is a way…

Gutta cavat lapidem, non vi, sed saepe cadendo…

In the mid 1990’s, Walmart tried to penetrate the banking space by registering to be a savings and loan institution, but was shot down by the enactment of the Gramm-Leach-Bliley Act of 1999, which closed loopholes for commercial entities to become financiers.

Undeterred, Walmart tried again in 2005 under Utah’s more lax local policies, only to be rejected this time by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.

Now both Walmart and Amazon redoubled their efforts to become full service banks.And eventually they will prevail.

Hook + uppercut = knockdown for the “too small to succeed” meaning local and regional brick-and-mortar banks.

Whoa, First Republic and Bank of the West were leaders in this field? I wonder what they were doing to get the increased amount of deposits, to be honest, I had considered any bank money to be dead money in the last eight years or so. Thanks Ben and Janet.

Check out First Republic’s CD offers on its site. Go to the “Personal” tab and click on CDs. They’re actually offering their own clients reasonable interest rates, unlike some other banks. That’s how they attract deposits.

Over the last 4 years I have averaged 4% on my gold coins, and 7% last year.

The banks are going to have to offer a lot more than 2.25% if they want to compete with gold.

From July 2011 ($1495/oz) thru July 2016 ($1340/oz) gold averaged negative 10.5 percent. The banks offering zero percent on savings did far better.

If you bought gold in the mid-1990s when it was below $300/oz, your rate of return looks rather better, no? So it all depends on your chosen time window.

I bought a 12 month CD from Capital One at the beginning of April ( 2.15%). Don’t like Capital One as they fill my mail box with unsolicited junk mail but its the most interest I have been able to get since Wachovia was offering in 2006!

“At the end of 2017, about 72% of the deposits were lent out.”

Anyone know the required reserve ratio per the Fed is? I’m assuming around 10%. So having an extra 18% sitting around doing nothing seems odd. Are the banks having difficulty finding things to lend against?

Do these deposits include the “excess reserves” created by QE? Would unwinding QE effect the scramble for new deposits?

If the reserve ratio is 10% (as is the case for large US banks, but it’s a fairly complex formula with items that are included and others that are excluded), it means very roughly and super-boiled down that for each $100 in deposits, a bank has to keep $10 in cash on hand or on deposit at the Fed, and that it can lend out the remaining $90.

For a bank, deposits are a liability; cash and loans are assets. So if a bank takes in $100 in deposits, it borrows $100 in cash from its customers: It books a liability (“deposit”) of $100; and at the same time, it also books an asset (“cash”) of $100. It then has to keep 10% of this $100 on hand as cash (or deposit it at the Fed). And it can lend out $90, which moves the $90 from the asset category “cash” to the asset category “loans.”

In this case, its books show:

Deposit (liability) = $100.

Cash (asset) = $10; and loan (asset) = $90. Total assets = $100.

And thus the balance sheet balances.

Do banks really work that way? I thought commercial banks created money out of mostly thin air when they loan out money. Only 10% (US) or 3% (Europe) need be actual cash on deposit.

GSH,

“I thought commercial banks created money out of mostly thin air when they loan out money.” That’s a rumor based on a theory. In reality, banks raise the funds they lend out from various sources, and one of those sources (and usually the cheapest one) is deposits.

The fact that banks are paying higher interest on deposits to increase their deposits proves how important this source of funding is to them.

That may be the case in the US but not in the UK, where private banks conjure dosh out of thin air whenever anyone takes out a loan[1]. I’m pretty sure the UK model applies to the EU too, but cannot swear to it.

[1] http://positivemoney.org/2014/03/bank-england-money-money-creation-modern-economy/

Here’s a direct link[1] to the BoE’s bulletin referred to in my above post.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

You really need to read the whole linked article carefully — it’s not what the headline says. It’s a LOT more complicated. It includes this paragraph that essentially says that banks create DEPOSITS in a circuitous way, and that these deposits that it creates are then lent out:

“In fact, when households choose to save more money in bank accounts, those deposits come simply at the expense of deposits that would have otherwise gone to companies in payment for goods and services. Saving does not by itself increase the deposits or ‘funds available’ for banks to lend. Indeed, viewing banks simply as intermediaries ignores the fact that, in reality in the modern economy, commercial banks are the creators of deposit money . This article explains how, rather than banks lending out deposits that are placed with them, the act of lending creates deposits — the reverse of the sequence typically described in textbooks.”

This is a THEORY. It’s based on the idea that NO CONSUMER should save. That consumers should spend all their income…

Banking 101 (Video Course)

http://positivemoney.org/how-money-works/banking-101-video-course/

Bankers don’t lend out deposits. Economists teach the money multiplier theory because the bankers don’t want the public to know how lucrative banking is.

See my comment just about this theory — and how it has been misrepresented.

And just look at reality.

@GSH,

My question is related to yours and I respect Wolf’s response too. I had heard that banks create money out of thin air when they lend. So the reserve ratio becomes critical. If the RR is 10%, and my next loan will take me below that, then I desperately need to attract deposits.

However, if banks are currently sitting on 28%, then I shouldn’t be fighting for deposits just yet. But banks are. So either something different is happening, or, as Wolf noted, the actual complexities of the calculations mean 10% is effectively 28%.

I am thinking about this too. Can’t they just keep borrowing from Fed funds with over night rate and maintain “reserve ratios?” Why would they need to borrow from depositors? I guess FED is raising the rates for FED funds over night, and it will soon be 3%, and if they can lock the depositors at 2.X% for a year or two, they make money. I am going 3 month treasury bills. F the banks.

Yes, that’s how I understand it works, as does this guy[1]. I believe all major money systems work that way.

That is, when say Alice takes out a 200K loan to buy a house, from Bob the builder, Alice’s bank creates a 200k mortgage in its assets column and at the same time creates 200k deposit in the liability column (double entry book keeping, AIUI). Thus at the end of the day Alice’s bank’s books balance w.r.t. Alice’s loan.

Next day Alice writes out a cheque to Bob. If Bob’s bank is the same as Alice’s then its books still balance. If not then the 200k is going to end up in Bob’s bank but that bank knows the game and isn’t going to accept the cheque (for which it’ll have to write 200k in Bob’s deposit account, a liability) without something coming with it. All private banks bank with the central bank, where their accounts hold reserve currency. Bob’s bank accepts the 200k cheque as it knows it is shadowed (so to speak) by 200k of reserves that Alice’s bank will move from its account with the CB into Bob’s account with the CB.

So why are banks willing to pay more for CDs than ordinary deposits? AIUI, CDs are timed deposits (if that’s the correct term) unlike ordinary deposits, which can be withdrawn, more or less, without notice. Now, QE resulted in banks being stuffed with reserves and so they didn’t need deposits (for the reserves that shadow them) of any kind. But if QE’s being unwound then banks need to get reserves from elsewhere, hence are willing to pay for CDs that bring more stable reserves than ordinary deposits. Hope that makes sense.

Anyway, that’s how I see it. Am interested what others think.

[1] https://www.pragcap.com/where-does-money-come-from/

This is wrong. Check out my comments in this section.

This is one of those memes that is partially based on a misunderstood and very complex theory that doesn’t even hold up in practice, and this theory then gets simplified into nonsense, such as “banks create loans out of nothing.”

And this is then endlessly repeated until people start believing it.

A deposit is a liability for the bank that it owes the customer. Of course banks don’t lend out the “deposit.” Banks lend out cash (the asset) from those deposits.

A $100 deposit is booked with two entries (double entry accounting): a $100 liability called “deposit” and a $100 asset called “cash.” Banks lend out that cash and thus convert this “cash” asset to another type of asset called “loan.”

As I explained to Kent:

If a bank takes in $100 in deposits, it in essence borrows $100 in cash from its customers: It books a liability (“deposit”) of $100; and at the same time, it also books an asset (“cash”) of $100. It then can lend out $90 ($100 minus the reserve requirement), which moves the $90 from the asset category “cash” to the asset category “loans.”

In this case, its books show:

Deposit (liability) = $100.

Cash (asset) = $10; and loan (asset) = $90. Total assets = $100.

I have to add this to justify the “misconception”. Bank wants to lend to Joe to buy a house, say 100K, but the bank do NOT have deposit, what does

the bank do? The bank go federal reserve and borrow 100K and then lend to Joe. That 100K is primised to pay back tomorrow since it is overnight. But tomorrow, the bank borrow pay back 100K and borrow again promising to pay back the next day, and they keep rolling. See? as long as FED is there, the bank have no trouble funding their loans. What does the FED do? The FED just “creat” that 100K out of nothing. So, the banks can NOT create, but the central banks can.

JZ,

Good lord. The banks that are affiliated with the Federal Reserve park their reserves (cash from deposits) at the Fed. There are required reserves (the minimum cash that the banks have to deposit at the Fed) and excess reserves. Currently, in addition to the required reserves, banks put over $2 trillion (with a T) on deposit at the Fed. Why would banks borrow from the Fed if they place their excess cash at the Fed? Not happening.

Reality is this: the banks can request emergency loans from the Fed if they’re in a liquidity crisis, and the Fed acts as lender of last resort. That happened during the Financial Crisis. Not happening now.

I’m going to start deleting these misleading comments. I don’t have time to whack them all down individually.

Long overdue anti BS action PLEASE.

You’ve deleted, what you consider are, misleading comments, which is fair enough, if only because they’re going off topic. But it would be useful to agree on some basics.

One important basic is, “Where does the majority of the money, circulating in the real economy, come from?” Ignoring cash (notes and coins), which is circa 3% (in the UK), the other 97% (stored as ones and zeros in computers of private banks) is loaned into existence by private banks when they make loans, right? Or do you disagree? If so, where do you claim the majority of the money comes from?

Thanks for your time and patience.

L Lavery,

“Loaned into existence” by a bank, to use your phrase, is just one side of the equation. By this measure, deposits take the money out of “existence,” to re-use your phrase, which is one of the other sides. They go together. That’s why the linked article said that banks “create deposits” in a circuitous way — because the money they lend out eventually comes back as deposits (guys takes out a loan to buy a house, the cash from the mortgage to buy the house goes to the seller, his bank, the brokers, other service providers, the taxman, etc. and “circulates” until it ends back up as deposits to be lent out again.

Why do you think banks sell loans (mortgages, auto loans, consumer loans) to investors via MBS or other asset backed securities? Among other reasons, because they want the cash to lend out again. If they could just create money out of nothing to make loans, they could just make an infinite amount of loans. But that’s not how it works.

When money is credit, credit creates money, but that happens in a vast and complex system – and to say that a bank “create money out of nothing” to make loans (as it has been said here) is wrong. Monetary theory tries to describe some of those aspects. These are complex issues. They cannot be dealt with in a soundbite. And they mystify people, and people hear stuff, cherry-pick one aspect out of it, simplify it, distort it, generalize it, and turn it into sheer nonsense that they then spread and more people read it and start believing it. And in the process, they misunderstand how an individual bank has to operate and what kinds of constraints it faces (such as having to pay interest in order to raise the cash via deposits, bonds, or other loans) to lend out.

Wolf, the situation I described IS the financial crisis. During the financial crisis, money IS created from thin air to fund the liquidity. Everybody knows the FED is tightening NOW and money is destroyed INTO void. Deposits as well as FED are both source of liquidity. There IS certain truth that without liquidity the banks can still find their operation through FED. FED IS supposed to be the “LAST RESORT”, but during the past 10 years, they have been the “MARKET ACTIVIST”. I am NOT trying to mislead anybody. This is my understanding of the FED after what I have observed what they did in the past, and I still think there is certain truth that banks DO NOT need depositors as long as they have FED, therefore FED can shove what ever rates to any credit market including deposits.

The use of RRPO to push up interest rates tends to throw a blanket over all banking, not only the Feds charter banks, and the Fed is by design a “regulatory agency.” And of course if mortgages and origination had been better regulated in 2007 that trouble might have been avoided. The outcome being that housing is a national market (something it wasn’t ten years ago?) and so the Fed seqways to enforcing more uniform banking rules, and rates. If the Fed dropped it’s rate hike program, where would the market be setting rates? My feeling is lower, so why do regionals have to pay more interest to depositors, and charge borrowers more? To make them more profitable and by that reasoning safer to own and invest in, as well as giving the FDIC some cushion? Why is the Fed so nervous about banks, they keep repeating the mantra banks are safe and going to extraordinary lengths (normalization, please) to prop up the banking industry all the while credit is contracting. Or are we headed for a giant S&L event, banks locked into rates on deposits their loan portfolio cannot possible cover? This credit contraction is leading to real outsized efforts on their part, after then years of holding up the banks now they jack them up (and they’re pushing on a string). Somebody is worried.

“Fight for Deposits Erupts among Banks, with Winners & Losers”

Besides Wells Fargo, who may need cash because people are fleeing them like the plague (and MT I hear is also a terrible bank), I don’t see any evidence from my own studies that banks are fighting for my cash.

What are yields on savings? Virtually nil. That they’re hiding their better rate offers in brokered CDs also suggests they’re not too hungry.

Check out some of the banks in the linked article that I wrote Friday…

https://wolfstreet.com/2018/04/27/i-asked-my-wells-fargo-branch-about-cds-with-higher-interest-rates-this-is-what-happened-next/

…. and two weeks ago: Citi, Morgan Stanley, Goldman’s Marcus, American Express Bank, and on and on. They’re all offering similarly high interest rates on brokered deposits.

And check out some of the comments on this article where some readers share the rates they’re now getting at other banks:

https://wolfstreet.com/2018/04/27/i-asked-my-wells-fargo-branch-about-cds-with-higher-interest-rates-this-is-what-happened-next/

Bankaholic is a nice site to see a variety of CD rates as well as MMA rates.

>>The use of RRPO to push up interest rates tends to throw a blanket over all banking,

There are no reverse repo operations going on, so why bring it up? Are you intentionally trying to mislead in order to obscure and obfuscate?

Wolf, asuming the Powell Fed sticks to its planned 4-hikes-in-2018 rate-hike schedule, can we expect brokered CDs yielding (say) 3.5% for a 2-year lock-in by EOY? Last I checked Fidelity showed 2.75% for a 2-year brokered CD from Morgan Stanley, and as you helpfully clarified when I posted about that, while these (as opposed to conventional CDs) are useful in that one can sell them on the open market before they mature, in the midst of a rising-rate environment this will likely incur a capital loss. So if we can expect 3 more quarter-point hikes this year it would seem to make sense to stick to short-term CDs yielding around 2% now and then look for a longer-term one at around 3.5% at EOY, especially if one – I am in this camp – thinks that by EOY the odds of recession will have risen enough that further rate hikes in 2019 will be looking doubtful.

Yes, seems likely that a bank offering 2.75% on a 2-yr brokered CD might offer 3.5% by year-end, assuming we get three more rate hikes. This really depends on the competitive environment.

Keep an eye Treasuries. CDs compete with them (similar risk category). The 2-year yield is currently at around 2.5%. So a 2-yr CD offering 2.75% is very aggressive (this is awfully close to the UST 10-year yield = 2.95%). It shows just how competitive this market is getting. But I don’t know if this level of aggressive competition for deposits will continue among banks.

In an environment of rising rates, I would be VERY leery buying any fixed-income instrument, including CDs, if I know that I cannot hold it to maturity. As you said, if you have to sell, you’re going to take a capital loss (and you pay fees). The longer the remaining maturity, the bigger the capital loss. The income from those CDs is small, and even a small capital loss and fees will more than wipe out the interest income.

In terms of a recession: See all the excited savers that are starting to spend the money that they’re suddenly getting again? Some of them are commenting here. Higher rates might generate $90 billion in interest income for them this year and more next year. For them, the 8-year belt-tightening is ending :-]

And as the FED continues to normalise, the compounded effect of these two features (Normilisation and deposit Competition).

On junk bonds and unicorns, will be????

I guess one way to clarify your points on banking competition for cash deposits would be to show the change in M1/M2 and the *relative* velocity of money. As banks try to lure more into savings, they initially slow the velocity until demand for loans picks up and then (as a following indicator) velocity picks up. Of course this would then be shown by the change in M1/M2 levels.

It might also be useful to show how the “loans money into existence” mantra can be disproved.

Big wow…..

With 10% annual inflation, parking your money in a commercial banks interest bearing account, is as bad as claiming zero deductions on your income withholding…….

Interest free loans to banks and the government…..

Of course the banks now want 30% interest on their credit cards…….

Well, this is an extraordinary article/expose! I checked Wells Fargo’s CD rates online just now and of course Wolf is meticulously accurate, as usual.

So Wells is paying their own retail customers almost nothing on CDs but if they’re brokered (and probably in much larger dollar amounts), they pay close to what Treasury Bills pay.

This is just one more rip-off of their customers, even while Wells Fargo has almost $2 trillion in assets….

Obviously the customers who are staying with this bank, do so in part because of the great western (stagecoach) images they have in their consumer minds. Funny thing is that Wells (back then) had to deal with robbers of their stages, while now the Wells Fargo stages are themselves the ones doing the robbing…

See the classic book by William Black – The Best Way to Rob a Bank is to Own One….