But just because the contract was launched does not mean it will become dominant, or even relevant.

By Nick Cunningham, Oilprice.com:

China’s new oil futures contract is gaining some momentum as a fixture on the global oil market, although hurdles remain before it can become a key benchmark for Asia.

China launched its yuan-denominated oil benchmark in March to much fanfare, after years of planning and delays. The logic of starting up an oil futures contract in China is obvious. China is the largest crude oil importer in the world, and its growing appetite for crude has increased the urgency to establish a contract based on local supply and demand conditions. Importing such heavy volumes at dollar-denominated prices exposes Chinese refiners and consumers to currency risk. A yuan contract mitigates some of that risk.

Beyond those concerns, the yuan contract also augments the global status of the Chinese currency. China is the world’s second largest economy and shifting more global trade into yuan advances Chinese influence.

However, the new contract on the Shanghai International Exchange still has to overcome some hurdles before it can be taken seriously as a premier benchmark in the global oil market. Just because the contract was launched does not mean it will become dominant, or even relevant. Previous contracts have failed to garner sufficient liquidity and ultimately have been discontinued or have wallowed in irrelevance.

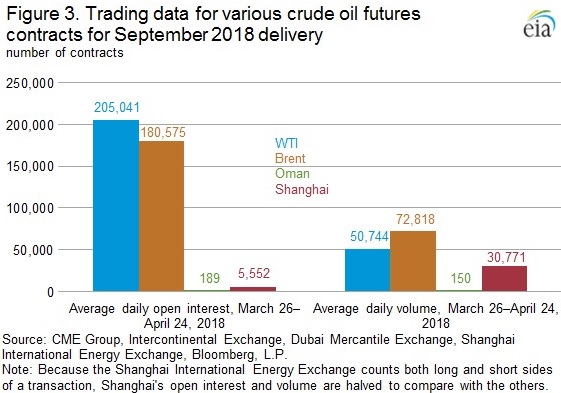

The Dubai Mercantile Exchange’s Oman futures contract has been somewhat reflective of conditions in the Asian market, incorporating medium and heavy sour blends. But “its daily traded volume and open interest (number of contracts outstanding) have remained at low levels since its inception in 2007, indicating it is not actively used among market participants,” the EIA wrote last week.

As Reuters noted in early April, there are several ingredients for success. First, the contract must serve a need for hedging. Second, it has to attract enough traders in order to build liquidity. Finally, restrictions on trading, speculation, and capital controls must not be too onerous.

Because China is already the world’s largest oil importer, the Shanghai contract can obviously meet the need for hedging. It also has a sizable pool of refiners and traders, which should allow the contract to build liquidity. An added advantage is that China imports medium and heavy sour crudes, while Brent and WTI generally reflect lighter and sweeter varieties. The need for some differentiation is there.

Reuters notes the biggest uncertainty is over intervention in the market from the Chinese government, which could deter investors. But the desire by the Chinese government itself to successfully build the Shanghai benchmark might be a strong enough incentive to allow trading to proceed largely uninhibited.

As such, the prospects look good for the Shanghai oil contract and trading volumes have picked up.

For China, the trading of oil contracts in yuan reduces currency risk for Chinese consumers, and thus, the Chinese economy. Yet, with the rest of the world buying and selling oil in U.S. dollars, for oil traders, a contract denominated in yuan creates new currency risk. That could be a big deterrent and obstacle for the growth of the Shanghai contract, an obstacle that other futures contracts did not have to overcome. For instance, the USD/CNY exchange rate has appreciated 8 percent over the past year, the EIA points out.

However, the global oil trade is gradually shifting east since that is where demand is rising the fastest. In 2017, the EIA says that Asia and Oceana accounted for 35 percent of global demand for oil and other liquid fuels, up from just 30 percent in 2008. That portion will continue to expand with China and India accounting for an outsized portion of demand growth going forward.

That puts additional weight on the importance of a benchmark that reflects supply and demand conditions in Asia. Over the longer-term, the potential peak and decline of oil demand in the OECD West makes Asia even more important as a hub for the oil market.

Already, the Shanghai contract has seen more trading volume for September 2018 delivery than the Oman contract. But volumes are still a tiny fraction compared to WTI and Brent. It could be a while before the Shanghai contract becomes a truly global benchmark. But it is on its way to becoming an important regional benchmark at least, reflecting medium and heavy sour conditions in Asia.

By Nick Cunningham, Oilprice.com

Is China’s latest effort to get its currency to be used globally — the “petro-yuan” — a credible challenge to the supremacy of the US dollar? And if China dumped US Treasuries, what would that accomplish? Wolf Richter on “This Week in Money”: Is the “Petro-Yuan” a Credible Challenge to Dollar Supremacy?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

‘Importing such heavy volumes at dollar-denominated prices exposes Chinese refiners and consumers to currency risk.’

What a ridiculous statement. When the Chinese government pegs the Yuan to the USD, what currency risk is there?

Let the Yuan free-float and wake me up.

But the Chinese hold trillions of dollar reserves. Who prints dollars? Not China.

As the USA prints more and more to cover baby boomer entitlements, to the tune of trillion/ year, China’s dollar reserves will just inflate away. And this printing is a mathematical certainty, given the state of USA politics, I’m sure you’ll agree. So this can contract CAN be read as a move away from USA currency risk.

Kam,

Check the exchange rate of the yuan before you make such a “ridiculous” statement.

The BOC has pegged the Yuan around 15 to 16 cents USD for more than 5 years.

Has China free-floated the Yuan, and I missed it? A peg is a hedge.

You totally and completely missed the entire concept of “currency risk” — which means the risk that the exchange rate changes. Look at the chart of the USD against the CNY. For example, over the two years between early 2014 and early 2016, the CNY lost 15% of its value against the USD. That’s “currency risk.” If the CNY then surges 15% against the dollar, that’s “currency risk” too.

When dealing with “Highly OPAQUE” ccp china.

The biggest risk are the “Hidden Risk”

As you stated. The Peg does not stop the CCP from clandestinely devaluing CNY against the $, only the speed at which it devalues.

I’m with Kam On this one. How can a currency pegged to another currency be anything other than a hedge. AND how can a currency that’s pegged to a reserve currency end up in a basket with other currencies not pegged to that reserve currency.

This makes no sense to me and I’ve had discussions with people who are convinced that the Yuan is going to take over the world but don’t know it’s pegged to the dollar……what does that peg really mean? Is that really fair when having such a massive trade imbalance?

Also, Doesn’t the quasi peg to the dollar allow China to print like mad with no risk of a massive depreciation (all though maybe they would want one as Kyle Bass has been hoping for) of the Yuan? I’ve read that the PBOC has printed more currency than the other major central banks combined…….and they are going around the world and buying it up…….

nothing makes sense anymore…….

Very interesting article, please update the charts in a few months, to see if any trends are developing.

Drip…drip…drip. Almost makes you wonder if one day we wake up after pissing off most of Planet Earth, the USD isn’t the reserve currency any more. And how dare they sanction soybeans in Trump states! Btw thx for the Wells Fargo 2.25% cd tip – got a cd maturing 5/27 and was gonna put it Synchrony at 2.15%.

Great article. and although the Yuan is “pegged” it moves, 8% as the article says. its moves in a controlled way so this also adds to the contracts being attractive AUD TO USD traded between .71 to .81 from May 5th 2017 year to date thats a 14% flux. Interesting times

*Is China’s latest effort to get its currency to be used globally — the “petro-yuan” — a credible challenge to the supremacy of the US dollar?*

My answer is “Not any time soon”. In ten years? Who know?

China is desperate to be Able to buy oil and other hard assets in a currency that it prints/ controls. The most sure fire way to get ur currency respect will be to back it with gold.

Who’s been the worlds largest buyer/producer of gold for about decade?

So China’s currency has potential to gain stength as gold back.

That Will make an interesting currency/ commodity battle: gold back to RMB verse THE nothing backed dollar for buying the worldS oil

The gold they buy on the international markets is used in production of export goods or sold on in the overpriced retail stores to the public at a profit.

The gold they produce in their uneconomic gold mines is the gold that goes into reserve. As they own it at their reduced production cost.

They only buy gold into reserve, when people like Gordon Brown who hates England. is giving it away (Browns Bottom).

To back their currency with gold they would have to open a gold window like the old Treasury/FED gold window, and allow at least other nations to redeem chinese paper for chinese gold. So they would not be a gold back currency for long, as there are many others like the french simply waiting to exploit gold windows in a Qe world just as china has abused Qe to buy up swathes of America.

The other way is to fix X many CNY/RMB to an OZ. Which is the same as a fully floating CNY/RMB as chinas can not control the global gold price. Somthing china refuses to do as they would loose control of their currency to speculators.

This talk of gold backed/Pegged CNY/RMB is even more ridiculous than the talk that CNY/RMB will replace the $ in the near future.

The only thing worse that BS, is deliberate, baseless, Anti American/Western Pro chinese Propaganda BS.

Every time some creature posts more of it. the wedge in the growing chasm between the west and china is driven a little deeper.

Well

I’m a cretin who is spouting what I heard from macrovoices podcast featuring Luke Gromen.

His charts, data and thoughtful analysis seem lot more convincing than ur little tantrum flame.

So the idea that China could ever be playing a long game of gold backed currency stability is utterly ridiculous?

“So the idea that China could ever be playing a long game of gold backed currency stability is utterly ridiculous?”

Yes.

china is doing what it has done before with commodities (PM’S are simply Hard commodities) Extr5acting wealth from the west (by paying for it with high priced exports or worthless chinese fiat) and hoarding it in them. the results are playing out the same as teh last time.

They will not back a convertible currency with them.

If facts are considered by Propagandists, those whom talk their book’s to eat, their crony’s, and their supporters, as flame, so be it.

I have bee correct so many times in the past, (Human accelerated global warning, globalisatoion, iran, P 43 (will go to war (predicted before he announced he would run0) Sub prime (As it was growing), P 44 (No good for American middle class/workers( will make teh world a more dangerous place (before he was elected))) +++ from the beginning, and told by supporters of book talkers every time, I am wrong, it is boring.

Its not clairvoyance, or even high intelligence, just history, plus basic cynical and realistic analysis.

You dont like reality, prefering the pro china, pie in the sky, of your book talker, that’s your problem, your dislike of reality, and your book talker, wont change it.

@ Wolf,

Then too what end is China hoarding/loading up on gold, as many believe they are?

The purposes of “hoarding” gold are the same everywhere, including that it’s an asset worth “hoarding.” And it’s somewhat counter-cyclical, which helps balance things out.

China has expanded its money supply and credit more than any other country in history. If it even were possible for China to back its currency with gold, it would wipe out the credit-growth-based economy, and their economy would totally collapse. The Chinese government would be suicidal morons to try to back their currency with gold. They don’t even waste time thinking about it. They’re focused on credit growth (which is the opposite of backing a currency with gold.) Credit growth has been the engine of their economic growth model.

‘Credit growth has been the engine of their economic growth model.”

Credit growth or unsustainable monetary expansion.

they are tightening private credit at the same time the state is increasing its assets by/through direct monetary expansion. The state is effectively printing itself money to buy what it wishes.

If I recall correctly, Luke Gromen was saying the Chinese would tie the oil contract to gold, so that it would essentially be a gold for oil contract. And that the gold would not come from official Chinese coffers, but from market players. Thus undermining the fiat USD petro dollar, while at the same time not depleting the Chinese of their gold reserves. Would an oil exporter rather sell for fiat USD or gold exchangable RMB?

These stories are an internet joke. Don’t take them seriously.

What happens to any oil exporter who insists on receiving gold for their product? Is it a joke or fact to say that US warships quickly end up on their shores?

If in a soon to be much more inflationary world, is “what am I going to use to buy my oil/hard assets with?”, not an urgent and pressing question. And isn’t getting oneself squared away with gold the answer?

I agree with your view of China’s current money printing bubble, and thier need to inflate, etc. But they also have a strategic battle against the USA. And they don’t want / can’t be at the mercy of their adversaries currency which their adversay alone gets to print. These are. perhaps, diametrically opposed truisms.

Not going going to happen. For one this will strengthen the yuan regardless of the peg which would eventually break as all pegs do, (remember EUR/CHF) collapsing exports and their economy. Two China has over $22 trillion in liquidity which would have to be all backed and with the total amount of gold ever mined at today’s prices only $7 trillion with most not available. Where are they going to get the gold? Three this requires a country to constantly buy gold to back the new liquidity an economy needs to grow and to restock what went out the gold window. No major country can afford this even at today’s prices so forget about higher prices.

This is what Bernanke meant in Congress when he said gold is a “relic” when it comes to today’s international financial system as it is no longer used in the world’s monetary system as a medium of exchange for goods and services.

It’s the COMMUNIST PARTY GOVERNMENT that imports the oil who have their grip on THE CENTRAL BANK note printing machine. What do they care about HEDGING? (This subject matter of this article is one of those obligatory journalism jokes where everyone (reuters, and financial press) pays obeisance making the predictable clucking noises).

imho This is to be read as China trying to become more of a financial hub, (they announced foreign banking licenses with majority stakes just a month ago too) for the future than specific immediate concern about OIL per se.

china NEEDS to have forigen cash, pored into its grossly NPL and Worthless State equity laden. Over-leveraged banking system. to help keep it alive.

Thats why it is opening these “Investment opportunity’s” to foreigners now. It what is a “mature” as opposed to growing Market. In which china holds the dominant position, and will keep it.

Any market sector china opens now, is already DEVELOPED. The money has been made, by ccp Cronys. Now the process is to Strip more wealth, and high technology from the west, the second win for china in another 2 wins for china deal..

This is other propaganda, and china wins twice, move, for china.

Not a profit making investment opportunity for foreigners.

One would be safer “investing” in NPL laden, small italian Bank’s.

“obeisance”

LOL……I had to look that one up……and now I’ll probably see that word everywhere….why does that happen like that?

Reuters, especially on topics related to Russia and China publishes a lot of propganda, and I wouldn’t believe Reuters if they said the sun was going to set in the west without independent confirmation.

The US and EU countries regularly brag about the hundreds of millions that they spend on their propaganda that they call ‘countering Russian propaganda’. As soon as these programs were announced, Reuters started running a lot of those sorts of propaganda pieces, thus to me its been very obvious that they are cashing in on this government funding source. As such, they’ve lost all credibility with me, and the same goes for articles that rely in paragraph after paragraph on quoting Reuters.

Oil futures in yuan should, more importantly, be seen as a stealth float of the yuan, excepting for the basis risk between medium-sour chinese crude imports vs brent, or WTI.

Kiers

Yes, a backdoor (stealth) float makes the most sense, domestic Chinese market needs notwithstanding.

K

Several Commentators are not getting the Big Picture:

It’s not about Currency Hedging unto the USD. It’s about having the CHY and the CHN Economy separated from the USD and the PetroDollar System.

CHN’s PetroCHY to Au Scheme intersects with several Petroleum for Au and “Barter for other Goods” Schemes.

These Schemes allow for ANYONE who wants to buy Petroleum do so without the need to have USDs on hand. CHN will be free from the PetroDollar due to its Central Planning. IND and Europe will soon follow.

The IMF-SDR, Au, and Currencies of the G8(I include RUS) should take on greater roles in Global Trade moving forward.

If the Rbl is allowed into the SDR like the CNY/RMB has been .

|

THE SDR IS DEAD

You can not have, unstable, not fully convertible, not fully floating, opaque, currencies in the SDR that can be devalued at a seconds notice, on the whim of an Aggressive /Mercantilist Administration.

Show me a better quality and cleaner shirt than the US $ and I will consider it. CNY/RMB and RBL will not be that shirt for centuries, if ever. As both have a common trait, massive covert money printing by the state, combine with opaque, and blatantly false economic statistics.

The chinese and anti US groups bullied CNY/RMB into the sdr during the GFC period one of the tactics used by china was that they would not support easing actions in the west aiding the global economy and themselves unless they were included in the SDR. CNY/RMB does not truly belong in the SDR, its inclusion may still be the undoing of the SDR system.