During the sell-off, it ignored the whiners on Wall Street.

The fifth month of the QE-Unwind came to a completion with the release this afternoon of the Fed’s balance sheet for the week ending February 28. The QE-Unwind is progressing like clockwork. Even during the sell-off in early February, the QE-Unwind never missed a beat.

During QE, the Fed acquired Treasury securities and mortgage-backed securities (MBS) guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. During the QE-Unwind, the Fed is shedding those securities. According to its plan, announced last September, the Fed would reduce its holdings of Treasuries and MBS by no more than:

- $10 billion a month in Q3 2017.

- $20 billion a month in Q1 2018

- $30 billion a month in Q2 2018

- $40 billion a month in Q3 2018

- $50 billion a month in Q4 2018 and continue at this pace.

This would shrink the balance of Treasuries and MBS by up to $420 billion in 2018, by up to an additional $600 billion in 2019 and every year going forward until the Fed decides that the balance sheet has been “normalized” enough — or until something big breaks.

For February, the plan called for shedding up to $20 billion in securities: $12 billion in Treasuries and $8 billion in MBS.

The easy part first: Treasury Securities

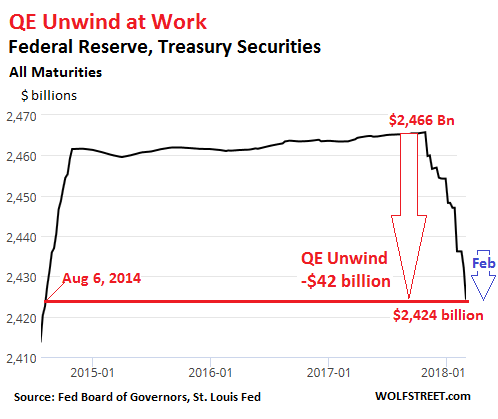

On its January 31 balance sheet, the Fed had $2,436 billion of Treasuries; on today’s balance sheet, $2,424 billion: a $12 billion drop for February. On target! In total, since the beginning of the QE Unwind, the balance of Treasuries has dropped by $42 billion, to hit the lowest level since August 6, 2014:

In the chart above, the stair-step down movement is a result of the mechanics with which the Fed sheds securities. It does not sell Treauries but allows them to “roll off” when they mature: mid-month and at the end of the month. On February 15, $16.6 billion in Treasuries on the Fed’s balance sheet matured; on February 28, $32.1 billion matured.

In total, $48.7 billion in Treasuries matured. The Fed replaced $36.7 billion of them with new Treasuries via the special arrangement it has with the Treasury Department. This cuts out the middlemen on Wall Street. So these $36.7 billion in securities were “rolled over.”

But the Fed did not replace the remaining $12 billion of Treasuries that matured. Instead, the Treasury Department redeemed them at face value (paid the Fed for them). In the jargon, these securities were allowed to “roll off.” The blue arrow in the chart above shows this February move.

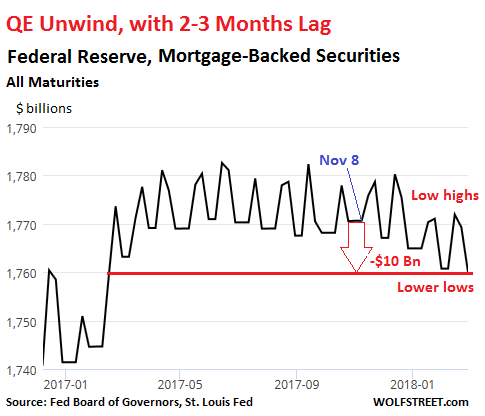

MBS are a jagged animal.

For February, the plan calls for allowing $8 billion in MBS to roll off. So how did it go?

Residential MBS differ from regular bonds. The MBS holder receives principal payments continuously as the underlying mortgages are paid down or paid off, and the principal shrinks until the maturity date, when the remainder is paid off. To keep the MBS balance steady, the New York Fed’s Open Market Operations (OMO) continually buys MBS. Settlement occurs two to three months later.

This timing difference causes large weekly fluctuations in MBS on the Fed’s balance sheet. It also delays the day when MBS that have been allowed to “roll off” actually disappear from the balance sheet [I explained this in greater detail a month ago here].

As a result, to determine if the QE Unwind is taking place with MBS, we’re looking for lower highs and lower lows on a very jagged line. Also today’s movements reflect MBS that rolled off two to three months ago, so November and December, when about $4 billion in MBS were supposed to roll off per month.

The chart below shows that jagged line. Note the lower highs and lower lows over the past few months. Given the delay of two to three months, the first roll-offs would have shown up in early December at the earliest. At the low in early November, the Fed held $1,770.1 billion in MBS. On today’s balance sheet, also the low point in the chart, the Fed shows $1,759.9 billion. From low to low, the balance dropped by $10.2 billion, reflecting trades in November and December:

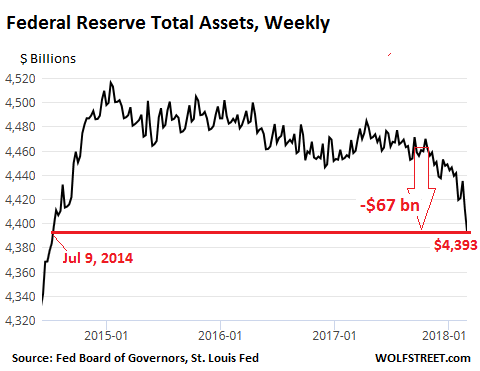

And the overall balance sheet?

Total assets on the Fed’s balance sheet dropped from $4,460 billion at the outset of the QE Unwind in early October to $4,393 billion on today’s balance sheet, the lowest since July 9, 2014. A $67-billion drop:

The balance sheet shows the effects not only of QE but also of the Fed’s other roles that impact its assets and liabilities. The most significant among these roles is that the Fed is also the official bank of the US government. And the Treasury Department’s huge and volatile cash balances are kept on deposit at the Fed. The Fed also holds “Foreign Official Deposits” by other central banks and government entities. But these activities have nothing to do with QE or the QE-Unwind.

There have been suggestions that the Fed “backed off” or “reversed” the QE-Unwind during the recent sell-off to prop up the markets. This was deducted from a single bounce in the overall balance sheet in week ending February 14. But this bounce was just part of the typical ups and downs and perfectly within range.

I have to disappoint these folks: based on what has happened in February with the Fed’s Treasury securities and MBS – the only two accounts that matter for the QE Unwind: The Fed didn’t miss a beat. The QE-Unwind proceeded as planned throughout the sell-off. And I expect this to continue.

This Fed isn’t going to try to bail out every whiner on Wall Street. It has been clear about that. It won’t take Wall-Street whining seriously until credit starts freezing up – and the credit markets are far away from that.

The housing market shudders. Could it be the new tax law and sky-high home prices? Read… I Didn’t Think it Would Go This Fast: Mortgage Rates Blamed for 3-Year Low in Pending Home Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Both the FED and GOV got one thing right. If something happens slowly, nobody is going to notice and complain, such as inflation, therefore 2%.

They also think if they slowly sell something, nobody will notice as well.

Give them some time, by the time they shrunk 1/3, people will start to notice. By the time they sell half, people will start to panick.

Now is the time for smart money to screw dumb money.

There is a Chinese saying “Cooking frog with warm water”

Amphibian sous-vide?

We’ve been getting the “Watching paint dry” discount.

It’s a whole 1.5% drop so far! In other words, a smaller percentage the Dow dropped today… This going to take some time.

Your heroes are busy with credit but rest assured the market of stocks share the same fate as everything else? The trade has blown up , long live the trade…. A week to refrain from caffeine?

Wolf,

Great job on keeping tabs on the start of the winddown. And your other articles very well researched. Thanks for your hard work!

Of course the Fed would love to get be to a “normal” lower balance sheet. Time will tell. I’m a bit on the doubting side they’ll make it all that far.

I strongly believe we’re in for another financial crisis somewhere in the next couple of years. Trillion+ fiscal deficits, 650 B trade deficits, and most importantly…severe amd worsening economic conditions for the “unprotected” 60% or so of the population and no financial gain/savings for most the rest (except the top 10%). I don’t know what’s going to give or where but something is/will.

One thing is for sure, if credit freezes up (another financial crisis), the Fed is going to go hog-wild on experimental monetary policies.

The Fed has no leeway and cannot reengage QE Infinity without losing complete credibility for the long term balance sheet normalization regime they have proposed. If the proposal goes off the rails the foreign lenders will stop buying Securities, and they will all see the writing on the wall at the same time which will freeze credit, and then the Treasuries will get dumped because the Fed Reserve can’t normalize their balance sheet.

Zero Sum end game is the rate at which the Fed has planned balance sheet normalization. Why are they normalizing at this exponential rate? The normalization is paced way too quickly, and this will blow up before they get to the half way point.

Question: Who is picking up the MBS, and will they continue to pick it up at this rate of normalization of the Fed balance sheet?

MOU

The US will monetize if necessary. MBS? Germans love those. Remember the 2008/2009 panic, plenty of MBSes blew up over there.

One call from the BIS, Wiedman will be loading US MBSes into the German balance sheet and back them with the repatriated “gold” (tungsten) from New York.

What can go wrong?

And what would be the probability of this credit freeze according to you. Since you mentioned it is far-off how far-off do you think it is or unlikely enough not to think of it.

I am unable to wrap my head around how is it possible to get out of the hole (debt) ALL the central banksters have dug themselves (or us I should say) into, given that they have been digging for nearly a decade. IMO, the unwind cannot be anything other than messy and could include a credit freeze and a replay of the central banksters taking over the world again. Otherwise you end up with a central banksters manipulated market for as long as they can hold it up. May be I am being irrationally fearful.

I’m not skilled enough in terms of the flow rate to nail down the timeframe of the credit freeze, but before they get through 1/3 of the dump the market will start to balk. I just read a paper that advocated for the Fed to retain the massive balance sheet [Ben Bernanke’s idea] and promote the Fed as another bank lender with a Communist sized balance sheet. Bernanke is starting to think like China here, but his idea has merit in so far as the Fed cannot reduce their balance sheet incrementally at the rate they are proposing without precipitating collapse system wide so the Bernanke proposal is essentially saying that the good old Fed Reserve USA should just be another Communist China and become an oversight lender for the Bank Holding Companies from here on out. His idea is a good idea IMO. The USA needs to redefine & re-operationalize the entire global banking system, but that must start with the absurdity of the Federal Reserve Banking System which we have outgrown due to the system incompetency in and of itself.

We know it is essentially a closed-looped cybernetic system that will rundown over time due to Entropy and the Second Law of Thermodynamics. The only decent proposal for a new global banking system would be to have an open-looped system instead of the dying closed-looped system we are all now suffering with needlessly.

Systems Theory & Information Theory should be guiding our monetary systems, but the powers that be [fill in the blank] want their grubby little hands all over the skim so they make it closed-looped and it runs down due to Entropy.

I could rebuild the entire Global Banking System in a few weeks to a few months depending on complexity required, but I could build a more equitable system with my eyes closed, and asleep, compared to the duplicitous system we now have in place. That system is just about to implode, and the grand re-set is inevitable.

Predicting the credit freeze time wise is fairly easy if one has access to the data live stream. Goldman knows when that will happen and so does the Fed. We can also assume that WW3 will start going hot if anything like a credit freeze starts to occur. Both the crash & war are timed to coincide. Thermonuclear Hot World War Three is inevitable, and so is the next crash of the stock market, and bond market.

The Fed can’t sit still, and they have no room to move either so they dance on the head of a pin until they can’t anymore.

Zero Sum end game.

MOU

To get a feeling for when credit starts freezing up, watch junk bond yields. The BB-rated index yield soared to over 16% when credit froze up in late 2008. Inflation was at zero and heading below zero. So that’s a 16% real yield. The CCC yield soared to about 25%. And the spreads to Treasuries soared. These were signs that credit was getting very tight for investment-grade and freezing up for riskier companies. But we’re very far from these conditions. It could happen, but this is not my base-case scenario.

In a credit freeze, where does one want to be?

100% cash?

PMs?

Cash flow real estate?

“In a fetal position,” to quote an infamous guy on Fast Money at the beginning of the Financial Crisis.

As a sidebar have you noticed just how much consumer protection oversight is outsourced to the funded by industry entities. This is especially true in Canada re investor “protection”. The. Save early save often mantra exposes a huge chunk of change to predatory practices by mainstreet practitioners with little consequence to those same entities. Taxpayers and voters have yet to connect the dots regarding their legal rights and protections and low priority re

So what should the new Fed head do ?

‘Unlike his predecessors, he (Powell) needs to be symmetrically fearless. Policy unorthodoxy needs to be reversed as quickly as it was deployed. After Alan Greenspan ignored the NASDAQ bubble, it crashed and led to this incredible foray into negative real rates. That created the mortgage bubble, which was initially ignored by Ben Bernanke and ultimately spawned the financial crisis, leading us to fiscal and monetary measures that were unfathomable 20 years ago.’

From a guy called Paul Tudor Jones via ZH. March 1.

He called the 87 crash,

He thinks Powell ‘should raise rates as fast as possible’

This makes a lot of sense to me.

The problem with the Federal Reserve is that it is essentially a Ponzi scheme, and if the benchmark Interest Rate rises too much after all that debt consumption worldwide the costs of servicing the debts rise proportionally. Government can’t service their overly leveraged debts anymore so they kick the can down the road and build deficits that can’t be serviced either. And then every year they pretend to care about debt ceilings and government shutting down so they can milk the system for a few more paychecks and bide time marking time instead of fixing the system that they don’t know how to operate.

That’s called a Hegelian Death Spiral.

MOU

What he thinks and what Powell thinks might well be different! To be considered is also whether the Fed can raise rates as fast as possible without crashing the markets (at least the market still thinks so). IMO, that is extremely unlikely given the confluence of global factors.

Yep. Raising rates faster, not slower is absolutely critical. The Fed is SO far behind the curve it isn’t funny. If they don’t raise them faster now, they will eventually have to resort to a Paul Volcker like, super rapid escalation of rates, that will then for sure, crush the economy. That approach is so much more destructive. 1/4 point increases spaced way too far apart, are just way to impotent to have any meaningful impact. Its kowtowing to WS, and the markets, to allow them have their cake and eat it too. The bubbles just get exponentially larger. They have to completely forget about what might happen to stocks, and stop worrying about keeping them propped. The propping has occurred ad nauseam now since the 2000 bubble burst. Its time to face reality. Like Buffet said, everything is too expensive to buy. When a guy like Buffet actually gets to the point of admitting that, it means every single corner of every market and asset has been bubbelized and overinflated to the nth degree. They could do 1/2 point increases, spaced closer together, and that probably would not be fast enough. The dollar is already in a secular downward trajectory, so leaving rates so low, is only going to continue that slippery slope of hope. Having a stronger dollar will keep imports down, despite any talk of ‘trade wars’ or tariffs, which will only be on a very very few items anyway. China by the way, has really been absurd about their currency devaluation, and no matter how strong our dollar is, they absolutely must be handed blow after blow, to force their hand on their currency. Theirs HAS to rise faster than ours, so there should be no worry about us raising our rates, and making the dollar stronger. Same thing with Japan. This world wide negative rate garbage has gone on far too long, and its time to pay the piper for the destructive impact it has had. It has imbued far far far too much risk into every market. Its eroded previously solid economic foundations. If it blows up all the financial leaches, and blood sucking predators, so be it. The bottom 99% has been sucked dry. The top 1% is over engorged, and deserves to implode.

This was a great article and extremely insightful, thx.

Actually the article was boring, the discussion is something else

Thanks for this interesting post. It’s nice to have a site that reports the facts and not the media ideology.

Start a trade war with the country you need to export inflation toward? I would rather export inflation than face the fool force of deflation? “Fool force”!

Wolf, I have some additional information on why the MBS portion of the FRB holdings is so jagged and sometime even rose during the first 3-5 months of QE-unwind (Oct 2017-Feb 2018). It turns out that when news reports said that FRB would QE-unwind 4B/month (initially) of MBS, it was a bit of an oversimplification.

In fact what the FRB own documents say is that they would unwind (up to) $4B/month of GSE MBS **and** FAO (Federal Agency Obligations), the latter being short term loans from FRB to GNM=GinnieMae. The GSE MBS are shown in the FRED data series called MBST, and the FAO are shown **separately** in the FRED data series called FEDDT. Looking at FEDDT, one can see that most of the early so-called “MBS” QE-unwind actually did not come from MBST but from FEDDT. Lately, FEDDT has flattened out at a low level, and I expect MBST will therefore drop more markedly from now on.

For completeness, here is the exact wording from FRB on the “MBS” portion of the QE-unwind, From the Dec 2017 statement release:

QUOTE: The Committee directs the Desk to continue rolling over at auction the amount of principal payments from the Federal Reserve’s holdings of Treasury securities maturing during December that **exceeds** $6 billion, and to continue reinvesting in agency mortgage-backed securities the amount of principal payments from the Federal Reserve’s holdings of **agency debt** and **agency mortgage-backed securities** received during December that exceeds $4 billion.

NOTE1: What is meant by “agency debt” is FEDDT, and what is meant by “agency mortgage-backed securitie” is MBST.

NOTE2: I hope everyone would be able to follow along by graphing MBST and FEDDT via the FRED website. I don’t want to trigger moderation so I will not post explicit links.

Yes. And I put “up to” or “no more than” into my descriptions too.

This is not important at the moment. But it will be important in Q4 when the cap rises to $50 billion a month — $40 billion in Treasuries and $10 billion in MBS. MBS won’t be a problem, but in terms of Treasuries, there are only about $30 billion to $50 billion maturing in most months. So when only $30 billion mature in a particular month, the Fed can allow all of them to roll off, but it would be less than the cap of $40 billion. And the total would be consistently below the cap.

I’m not sure how the Fed will handle this. In September, when they announced this, it was very clear: it was a “cap.” But I get the feeling that the new Fed might be considering an alternative, such as outright selling of some small amounts of securities to turn the “cap” into a fixed quota to make sure they get to $600 billion a year for enough years to normalize their balance sheet before some other S hits the fan.

Some Republicans in Congress were somewhat impatient with Powell concerning the slowness of the QE Unwind, and Trump gets to fill four more slots on the Board of Governors. So this will be interesting.

https://www.mcoscillator.com/learning_center/weekly_chart/its_the_fed_yanking_the_punchbowl/

Tom McClellan is associating the jagged course of the rolloff with stock market selling. To argue with that is to take the position that the correlation is a matter of degree. The MSM relates the selling to “Tariff” talk, which is a real stretch. If you could somehow get that information “sooner”, we would all be indebted to you, Wolf…

There was also a large amount of debt issuance in February by the federal government. It was around 350 billion dollars.

By the H4.1, the Fed is still 24 billion dollars short of the cumulative decline in assets per T-notes & bonds, agency securities, and MBS stipulated by the unwind order. They’re actually 26 billion dollars short since agency securities weren’t formally part of the order.

What does debt issuance by the Treasury in February have to do with the Fed’s QE unwind? I don’t get the connection.

And read the article to find out why MBS roll-offs are lagging the target (the short answer: MBS trades take 2-3 month to settle and the Fed accounts for them on a settlement basis).

… they get to $600 billion a year for enough years …

“Enough years” … uhhh … with hindsight, thats the margin what they had in like 2012 or thereabout.

In 2018 every security it is possible to buy has been priced into even peaky-er perfection than back then and every market is more connected with less friction and more AI’s on the trigger.

The FED can’t unwind QE without some stuff hitting the fan, the longer they wait, the more fodder there is for that fan.

For example – In the province towns in Denmark there are empty shops everywhere because a business cannot afford the rent, but, the rent is never adjusted because at 1-2 % interest it is trivial for the owner (an investment company) of the buildings. There is no pressure to liquidate poor investments or turn them around.

Rates really need to go up!

—

Unless the FED has decided that *now* they don’t care about the stock market dropping perhaps 30% and interest rates ending in the region of 7-8 percent (which IMO they shouldn’t care about, but …. fear of pain held them back before)

I read that in early February the Fed’s balance sheet actually went up by $14 billion… presumably to help stem the sharp weekly decline in the markets. Is this true and can anyone shed any light on it ?

Please read the article!! And all the way. Your question is answered in the text.

The Fed wears many hats, they use the same policy they use on rate hikes (RRPO) to backstop M2 or Money Market accounts. For a time you could count on interest rate hikes around the first of the month, when the Fed added reserves. BOJ used to do this also and seems like we are more like them all the time. To withdraw liquidity is anathema to them.

Hi Wolf, reference credit freezing-tightening, at this moment in time a lot of heavily indebted companies are failing and presumably the banks are taking hits. With that occurring more and more surely the banks are going to get tighter and tighter- bemore careful on lending anyway?, we’ve seen that in Italy. What’s everyone’s thoughts?

The Fed wants to tighten “financial conditions.” Your scenario is part of tightening financial condition. This means that a zombie company that suddenly cannot refinance its debt (see iHeartRadio) goes bankrupt. Usually creditors take over and become the new owners to either restructure the company or sell it in pieces. This has a cleansing effect on the economy and is needed from time to time. That’s part of tightening condition and part of the plan.

But when IBM suddenly cannot meet payroll because the short-term credit market, where it borrows the funds for daily operations, has frozen, that’s a different story. If that type of scenario spread around the economy (as it does during a financial crisis), a credit-dependent economy shuts down. So the Fed will respond to that.

Wolf,

The problem with the central banksters’ credibility on QE and rates is this.

First this…

“Right now, the members of the policy board and I think that prices will move to reach 2 percent in around fiscal 2019. So it’s logical that we would be thinking about and debating exit at that time too,” he said. “I’m not saying that the negative rate of 0.1 percent and the around 0 percent aim for 10-year bond yields will never change, but it is possible. We will be discussing that at each policy meeting.”

Then this…

“In testimony that lasted about three hours, Kuroda seemed to try mitigating the negative market impact”

(source: https://www.zerohedge.com/news/2018-03-02/kuroda-shocks-markets-hinting-qe-end-nikkei-usdjpy-tumble)

The moment you get a small impact on the market, they come running with soothing comments.

Similarly in the US market, if Dudley had not indicated that 4 rate hikes are ok, the markets would have recovered yesterday. So at this moment it looks the Fed WILL HIKE. The true test is when the market falls significantly, which IT WILL if they stick to doing what they are doing.

How do you expect the world to believe you when you do not believe in what you are doing and you are playing by the ear (market moves)?

Good points. Your last sentence is key. This is part of the problem the Fed faces after spending years flip-flopping. I used to call it the flip-flop Fed for a reason. But now the Fed is trying to rebuild its credibility. If it fails in getting its credibility back, it can just pack up and leave. And it knows that. So I think it will tighten until markets become believers. It will tighten until it has its credibility back. That’s what my tea leaves say.

“But now the Fed is trying to rebuild its credibility.”

I watched Powell yesterday for a few minutes. The most striking thing was his ability and interest in replying with declarative sentences that were easy to understand. I didn’t watch for long so I can’t say for sure that was the whole show, but it stood in stark contrast to his predecessors.

Yellen used to babble incoherently. To me it looked like a cross between running down the clock and incompetence, highlighted with sheer stupidity. Bernanke seemed a little better, but used a lot of econ-babble and seat of the pants nonsense. Greenspan at least took pride in the confusion he created.

Yellen and Bernanke can be accused of many unpleasant things but one thing is certain. Both are highly intelligent individuals.

If it happens, then there will be blood on the streets!

Worse. The buyer of last resort will have left the market (if Wolf is reading the tea leaves correctly). No PPT? Return trip to SPX 666 and below….

Credibility cannot be restored to the Federal Reserve Banking System, Wolf. QE is coming back soon.

MOU

My Tea leaves (actually my friends that I borrow) say WATCH JUNK.

When it goes bang. YES WHEN.

We will see what Powell and the new FED, is made of.

If they run, they might as well never stop. As they will not be able to rebuild credibility from that, for decades.

Everybody is worried that the markets will fall. The pgoing to problem is, will the markets continue to stay open?

Look at the market for JNK and HYG. In selloffs, these things have serious liquidity problems. The same is true for mutual funds.

The FED is find out that printing is a lot easier than retracting.

@Paul,

“The FED is find out that printing is a lot easier than retracting.”

Yup! Especially when it is coordinated printing (on an unprecedented scale) !! One stop other starts, essentially running a relay between them.

That is the point. Only the Fed is gamely going about it for now. For how long is a big question.

How do ALL THE CENTRAL BANKSTERS get out without blowing up the stock market is beyond me. Because when it comes to either the bond market or the stock market they cannot but go with the bond market.

Was it like this when the market blew up during the Great Depression?

The depression was the end of a free trade cycle. Don’t you think we’re going through that now?

Can’t have a seller without a buyer

The bubbles are unsustainable. To blame declines in bubbly prices on this relatively insignificant Fed unwind is to be in denial of that simple truth. More likely, the bubbles are reliant on QE forever and forever bigger. Easy carry-trade and corporate buy-back credit forever.

…..unsustainable, as I said.

Ridiculously slow…………. Too slow to matter………. Only the “chatter” has any affect and it is too minor to be separated from market “noise”……

Great body of work Mr. Richter! So much better than the click bait Zerohedge.

+1

yes, gets the grey matter working, thank you Mr. Richter

Agreed.

This site and wolfs writing is much more interesting, on point and factually based than the site you have referenced.

Really like this analysis

I am a graduate of Zerohedge U. Professor Tyler(s) is an excellent professor, and the ZH riffraff are a great bunch of sparing partners, but I got booted for angering the POTUS supporters which are not a great bunch when it comes to free speech.

I did learn quite a bit from the Tyler(s) and the commenters. It’s not always click bait unless it’s Friday and then the Doom Porn articles come out for mosh pit analysis on the fly. Paul Craig Roberts is the best read on ZH for Doom Porn on a Friday IMHO.

MOU

Wolf Richter,thanks a lot for the article post.Much thanks again. Fantastic.

So in a QE unwind World AKA QT where do you want to position yourself? If you already own a hard-asset such as real estate is the next best thing cash? Is cash is king in the near future?

No comments on the laggard parts of Core PCE bouncing in Jan Wolf? Core PCE could easily shoot over 2% any month.

https://strategicmacro.blogspot.co.uk/2018/03/core-pce-has-been-held-back-in-last.html

IMO, One thing that’s going tpo really hit the QE unwind is junk bonds. HYG announced a sharply lower March first dividend Junk bond yields have been falling for 7 years and not just because of asset price rises. The refi activity to to QE is killing them. IMO, HYG would have to fall 50% for me to even think of buying.

If the ten year goes to 4% at year end, whose going to buy HYG at 4.8?

Have you looked at whats in HYG?

https://strategicmacro.blogspot.co.uk/2018/02/hygs-biggest-position-sfr-2026s.html

Biggest position is a money-losing French employment project/ cable TV firm which is only solvent as most of the balance sheet ‘assets’ are good will and intangibles.

We are raising rates to keep capital flowing in, but LIBOR is on FIRE, which maintains or maybe even reverses the flow. The free market system is collapsing, (well documented here, UK private/public partnerships fail on the PRIVATE side). Brits are ground zero, first Brexit, now they will go full Socialist, with government offering incentives for investment something they could never do with those onerous EU regs. The stock market has a deep floor beneath it, you can peel four or five years of gains out of there without doing any damage. Powell knows that. Psychologically a lot of nuevo rich public pensioners will cry big tears when their benefit package drops back to what their base salary was. Sacrifices will be made.

The humanity You mean the pensioners will have to cut back on their Starbucks That’s brutal and inhumane treatment you know

“…you can peel four or fives years of gains out of there without doing any damage.”

What!? Ever since the 80’s, the stock market has become the modern America’s central focal point. It is the commonweal. I’m not saying its immutable, but if/when it is wrecked, there will be a LOT of DAMAGE.

… you can peel four or five years of gains out of there without doing any damage …

– Assuming that nobody bought stock on margin or were writing naked puts or doing trixy things with OTC derivatives – a.k.a. everyone learned their lessons back in the 00’ies :)

Very good article. I got tripped up by a video on youtube, they said the uptick in the Fed’s balance sheet in mid-February was to help halt the stock price decline. At the time I watched, it seemed reasonable but your article puts things into the proper perspective. I wonder if the central bankers will actually let a correction occur, I’m still not convinced but hope they do. Time to clear out the dead wood.

Yes, the US needs a stronger Dollar.

Yes; this is part on how the US gets a stronger Dollar.

No, your crocodile tears aren’t working, please stop.

Yes the US dollar needs to regain some value . Or does it ? Seeing as how both a strong and weak dollar come with consequences . Hmmm ….

No .. from what is a Potemkin Village economy to imposing ludicrous tariffs , creating trade wars , pulling the rug out from underneath the middle and lower class , playing endless games with interest rates and proving ourselves to be unstable , unreliable and in a state of perpetual chaos … this is NOT how we get a stronger dollar

Pardon me but there does not seem to be crocodile or any other type of tears evident anywhere within AB’s comment . I don’t agree with him mind you . But nary a tear to be found .

So do .. read twice … comment once … and stop reading into others comments … please

Crocodile tears refers to people who is still whining after being told several months in advance that yes this was still gonna happen.

A crocodile cries not due to sadness but simply to wet their eyes, hence they are “fake tears”.

And yes there are negatives of having a strong dollar but is what the FED wants.

Plus many companies got into debt due to the zero interest rates then “forgot” to start paying back, just getting more debt.

Basically such low interest rates created debt parasites and now they are dying.

Back to 2014 levels! Only 6 years of QE left to unwind!

Well, as you said, it took six years to pile up this stuff. Do you want them to dump it all in one month? Just get it over with?

:-]

The 12 billion in Treasuries that matured, that the Treasury Department then paid the Fed for, was originally bought by the Fed with money created out of thin air. What happens to this 12 billion that now goes to the Fed?

It disappears back into “thin air.” It’s the reverse of QE. That’s why some people call it “QT” … quantitative tightening. That’s why the QE Unwind is so important. The QE Unwind will unwind some of the things that QE has accomplished (asset price inflation).

In other words money made out from thin air goes back to the wind.

Hence it is unwind!

Nope, not sorry for the lame pun.

thanks for including factoid of timing of roll offs being at mid and end of month

The fed hold onto their credibility… hilarious.

They will start QE4 as soon as market conditions need it.

The US Govern (Treasury) pays the Fed interest on borrowed paper money the Fed created from nothing. And they use QE and QT to manipulate the “free market” from which they also collect data from all the financial transactions. Their meeting minutes are published weeks later and transcripts years later. But please, do not allow yourself to become distracted about some year long media blitz about meddling with our elections.

I’m surprised that the author didn’t mention the effect of Treasury bond sales to fund the US deficit. This fiscal year alone about $1,200 billion worth of bonds must be sold which is twice as much as the $600 billion the Fed wants to unload.

The interesting thing is this may address the “need” or desire to raise interest rates more quickly than the Fed seems to intend, and if the markets balk then the Fed may retrench (and thus be unable to reduce its balance sheet) because the Treasury HAS to borrow.

Each topic on its own. Or else each article would be a 10,000-page book. This article was about the Fed’s QE unwind and nothing else.

I (the “author”) have written numerous times about the deficit, the national debt, and debt issuance. Here are some recent ones…

https://wolfstreet.com/2018/02/24/us-gross-national-debt-spikes-1-trillion-in-less-than-6-months/

https://wolfstreet.com/2018/02/19/us-treasury-posts-gigantic-1-16-trillion-shortfall-in-fiscal-2017-hilariously-points-out-where-we-are-headed/

Or this on projected debt issuance in H1 2018:

https://wolfstreet.com/2018/01/30/us-national-debt-will-jump-by-617-billion-in-5-months/

“I’m surprised that the author didn’t mention the effect of Treasury bond sales to fund the US deficit. This fiscal year alone about $1,200 billion worth of bonds must be sold which is twice as much as the $600 billion the Fed wants to unload.”

FED IS NOT unloading any Notes .

What FED is doing, is not renewing all of the Notes it holds, as they Mature.

SO of your 1.2 T probably around .8 T < is looking for a buyer, allegedly.

As currently there are still and average of 3 buyers for ever new T note available. I personally dont see any problem arising in Treasury Disposing of them.

Should the Interest Rate/Yield rise on them a little I would expect demand to increase as the T/Bond Market. Is still starved of Quality offerings with any Reasonable Yield. china and Europe are still Covertly and Overtly, printing like crazy. The SNB is still Overtly printing, as to some extent is the BOJ.

This is still fueling the QE Cash Glut, that is driving US Stocks and the Demand for US T Notes.

To some extent this is a matter of semantics. Allowing a bond (note, bill, etc.) mature is essentially the same as selling it because money is reabsorbed by the Fed. The money that the Fed created to buy the bonds originally is literally returned to the Fed.

Therefore, I disagree with your math. The 1.2T deficit is funded by the sale of USTs and whatever the Fed allows to mature also absorbs investor dollars. The only difference is the money spent by the sale of USTs remains in the economy (e.g., pays for medicare) whereas the money the Fed absorbs “disappears.”

“Therefore, I disagree with your math. The 1.2T deficit is funded by the sale of USTs and whatever the Fed allows to mature also absorbs investor dollars.”

Whatever amount the fed does not roll has already absorbed $.

It does not absorb any more when it matures.

The .8 T is relatively accurate, as that is rough how much the Global market will be offered this year after the FED has rolled what it intends to to keep with in its normalisation program.

“Whatever amount the fed does not roll has already absorbed $.”

Not true.

Look at it this way – a concrete example: When the Fed was conducting it’s debt monetization “quantitative easing” program it bought up Treasuries and MBSs from the market using newly created money. The previous bond holders exchanged their bonds for new cash.

Now, let’s say a bond has a coupon rate of 2% and sells for $800 so the Fed pays $800 to the bond holder (the Treasury itself or an individual, institution, etc.). Over the subsequent years – say 10 to make it simple – the Fed “receives” $20 per year or $200 from the Treasury as interest. However, the Fed doesn’t really get this money because it reimburses the Treasury at the end of each fiscal year so it makes no money in interest by holding the bond. (Not a lot of people know that but it’s true.) So, after holding the bond to maturity (in this example 10 years) the bond issuer (the Treasury) must pay the Fed the full face value of $1,000.

Now, where does the Treasury get that $1,000? By borrowing it, which is to say by issuing another bond thus effectively rolling over the Fed’s matured bond. The difference is the new bond holder won’t be the Fed.

Here’s our possible sticking point: I don’t know if the $1.2T in new US deficit spending accounts for the replacement of the Fed’s maturing bonds. If it does then $1.2T is the amount. However, if it does not (and I don’t recall if the Fed’s QT program was accounted for when all the deficit projections came out) then whatever rate at which the Fed wants to unload its stash must be added to the US deficit.

It’s like the US Treasury is getting double-whammed.