And this is just the beginning.

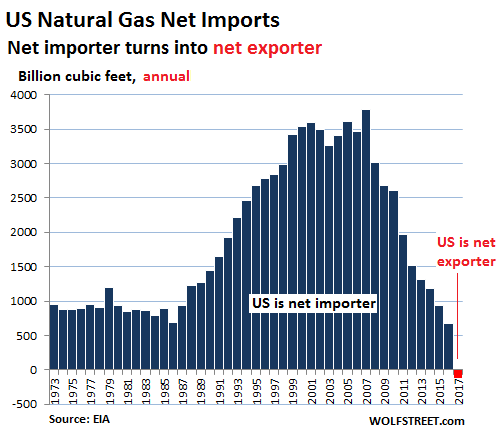

The year 2017 was when the US became a net exporter of natural gas for the first year in history. The production of natural gas has been surging since 2007, when fracking turned into a boom, whittling away at the need for importing natural gas via pipeline from Canada and via LNG from the global markets. Last year, according to the EIA’s just released data, the US exported 129 billion cubic feet (Bcf) more natural gas than it imported. And this is just the beginning:

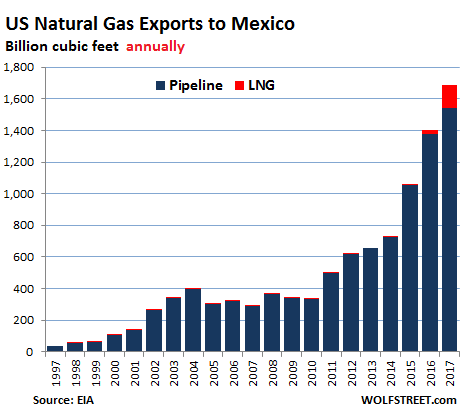

Exports to Mexico via pipeline have been rising for years as more pipelines have entered service and as Mexican power generators have switched from burning oil to burning cheap US natural gas (the US imports no natural gas from Mexico).

In 2017, natural gas pipeline exports to Mexico surged 12% year-over-year to 1,543 Bcf. But in 2016, a new trend became visible: US natural gas exports via LNG tanker to Mexico (marked in red in the chart below), which rose from negligible in prior years to 28 Bcf in 2016 and to 141 Bcf in 2017. Total exports to Mexico jumped 20% year-over year in 2017, to 1,684 Bcf:

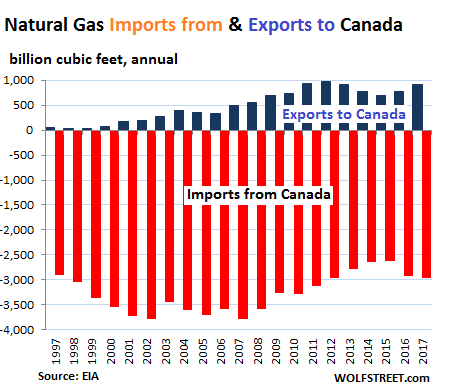

The US has a bilateral natural-gas trading relationship with Canada, both importing and exporting. Exports to Canada have surged from almost nothing in the late 1990s to a peak of 2,145 Bcf in 2016 but fell 5% in 2017 to 2,043 Bcf.

Imports from Canada, while they rose over the past two years, remain in the range established over the past two decades. But due to the surge in exports to Canada, net imports (imports minus exports) have plunged 43% from a peak of 3,600 billion cubic feet in 1999 to 2,042 Bcf:

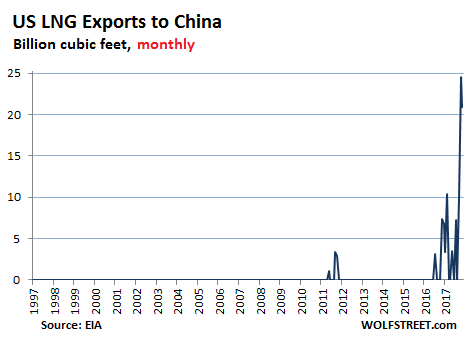

The LNG export terminals that have gone into service in 2016 and 2017 – they convert natural gas into liquefied natural gas – opened up the rest of the world to US natural gas. So for example, US LNG exports to China have surged from nothing two years ago to 103 Bcf in 2017. This chart shows monthly LNG exports to China:

What to do with all this natural gas?

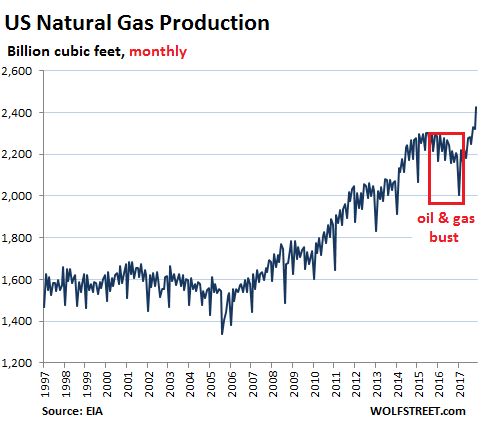

US natural gas production has been surging since the fracking boom took off in 2007. The chart below shows the monthly (not annual) production in billion cubic feet. Note the impact of the oil-and-gas bust in 2015 and 2016, when some natural gas drillers filed for bankruptcy. But since then, Wall Street opened its wallet again, and new money has flowed into the sector and production has spiked, not only from wells primarily producing natural gas but also from the renewed oil boom as many oil wells also produce natural gas — this used to be flared, but the installation of processing equipment and pipelines allows it to reach the market:

LNG exports began in earnest in early 2016 when the first liquefaction unit (“Train 1”) of Cheniere Energy’s Sabine Pass terminal in Cameron Parish, Louisiana, entered commercial service. Trains 2 and 3 followed. Train 4 is expected to enter service soon. Train 5 is under construction. Train 6 is in the planning and financing stage. All six trains combined will have a capacity of 4.2 Bcf per day.

In addition, there are five other LNG export terminals under construction, with a combined capacity of 7.5 Bcf/d, according to the Federal Energy Regulatory Commission (FERC). This would raise total LNG export capacity to nearly 12 Bcf/d over the next few years and make the US the third largest LNG exporter behind Australia and Qatar.

The LNG export trade in the US is powered by the huge price differential between natural gas in the US — where a “glut” has crushed prices since 2009 — and what large LNG importers such as Japan and Korea are paying in the global LNG markets.

Natural gas trades in the US for $2.70 per million Btu (mmBtu) at the moment. In other parts of the world, LNG fetches are massive premium. For example Japan acquired LNG in January for an average price of $11.00/mmBtu, according to the Ministry of Economy, Trade and Industry. And this is down from the range of $16-$17/mmBtu in 2013 and 2014.

Granted, liquefying natural gas and shipping it by tanker from Louisiana to Japan comes with costs, but the price differential is still alluring for US LNG exporters who’re praying that the collapsed price of natural gas in the US remains collapsed forever – even if it bankrupts producers and eats up tens of billions of Wall Street equity and debt investments on an annual basis.

And what will US natural gas producers do when this cheap money they’re drilling into the ground is no longer available as the Fed has set out to tighten financial conditions? Because the Fed is tightening precisely to turn off the cheap money spigot. Read… Fed’s QE Unwind Marches Forward Relentlessly

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wonder what the true cost of producing this gas will be….. at the end of the day.

A lot higher than the current price.

I’ve been thinking about this lately, how last time commodities saw this huge spike (which most trend with energy prices since energy is one of the most fundamental input costs) through 08 but this time commodities are so low. A common argument is that during boom times commodities are driven up by demand but the resultant rise in input costs all around is a part of what contributes to the turning over of the business cycle. When commodities subsequently crash during recession the low prices then help the economy to recover as it starts all over.

This time it seems the extraordinarily cheap rates and apparent economic lunacy that’s taken over has presumably caused many companies (mostly referring to the energy sector in this context) to delude themselves and investors into thinking they are profiting when they are in fact losing money on a cash flow basis in a number of cases. Commodities have now oddly dropped to relative lows during the high point of the business cycle merely because of obscenely easy credit conditions that allow them to furtively produce at a loss and the future be damned. All this makes me wonder when the next recession hits with all the chaos that will bring, could we possibly observe the odd and seemingly paradoxical phenomenon of rising commodity prices?

I’m having similar thoughts. But it may not be a recession that will cause that, though it could. I think the more likely cause will be the tightening of financial conditions and a deterioration in the credit markets.

Once these more leery and prudent investors demand to see actual positive cash flows before they invest more, the money might dry up for these drillers, and production might sink, as it had started to do during the 2015/2016 energy bust. Once production backs off enough, and after we get some more bankruptcies, we’ll higher prices.

A recession could occur at the same time, but I don’t think it is necessary in order for these dynamics to play out.

Not sure I agree with how this is being stated, but do agree with the outcome more or less…

I don’t believe the companies are all losing money by drilling, they just happen to have a low cost of capital at the moment. If/when the cost of capital is higher, then it becomes a problem. If the smart ones have hedged cost of capital to match the duration of debt or capital life expectancy (i.e. been prudent financially) and/or hedged production prices, then they will be fine, even if conditions change, they will just produce out what is locked in and supply will fall off (raising prices if demand remains the same).

There seems to be an underlying implication that all of the companies are drunk with debt, behaving imprudently etc., which might be true, and is likely true for some, but I have not seen any evidence that it is necessarily widespread.

Is there evidence for this? Whom are worst offenders? I honestly do not know but would be interested to ensure I stand aside.

Good points. It is also reminiscent of the argument that China has been perpetually dumping. A nation that has loses money with every foreign trade transaction does not show an impressive, steady increase in the standard of living of its people (to the extent that the one-child restriction lifted) that China has, even as the U.S. middle class has been raped and abandoned because of the criminal greed of American corporations bankers and politicians.

The problem is figuring out the productivity/’fill rate” of these fields. Unlike liquids, gases can be generated at tremendous rates for a long time. The geo-chemistry along with the new drilling methods have increased the theoretical reserves by incredible amounts.

The subterranean earth is a giant anaerobic organic reactor: product= methane.

Kevin

Why is the country so eager to export that which we could use ourselves, rather than importing it? Why not keep it in the ground until we do?

Seems the product actually belongs to the people of the nation, no?

(I can understand trades where the geography makes it a good deal for both sides)

The country is not exporting the gas, private parties are exporting the gas that they rightfully own and control.

If I invest my hard earned money in land that holds natural gas and spend more money to extract it should be my right to sell it to the highest bidder – the government should not tell me who I can sell my product to. That is how free markets are supposed to work.

The same applies to steel. I know we now have a command economy and no longer operate under a free market system but allow me my dreams. Dreaming is free (credit goes to Debbie Harry)

None of these people are investing their hard earned money–they are investing money hypothecated into existence by the Fed and burning through it at an astonishing rate, literally losing money on what they produce so long as the Fed spigot is turned on like a fire hose.

James:

You are 100% correct. It is the Fed by printing money out of thin air that has been financing the money losing shale oil and gas boom. This is just one aspect of the US’s financial war against the rest of the world exploiting the fact the USD is the world’s reserve currency. The reason it works for the US is that about half of the issued USDs are held by foreigners so they are effectively paying half the costs whether they want to or not.

Ah, yes: children have Santa Claus and the Easter Bunny, while ostensibly adult Glibertarians have “the free market,” and self-serving echo chambers that guarantee they don’t grow up…

People of the nation? Hahahahaha good one

It costs 10% of te energy to compress and liquefy the gases too.

” The typical gas consumption for the production of LNG from feed gas in the liquefaction plant can be calculated on the basis of 10% of the feed gas used for internal fuel consumption.”

http://petrowiki.org/Liquified_natural_gas_(LNG)

b/c it’s fair trade, not free trade (code for globalism chasing labor arbitrage) and must not be allowed.

We sure haven’t felt the glut of natural gas delivered by the monopoly Atmos in Texas. The prices have surged to to alarming levels. Meanwhile my electric bill (which is mainly generated by natural gas power plants) has dropped tremendously. What gives?

TheDona

You’re seeing the monthly service connection charges going up. The gas companies can do that, raise those rates. The gas itself is really cheap and by state law they cannot profit off you from what they pay for the gas from their suppliers. So local gas companies make almost all their money from the monthly connection charges.

The big gas powered plants use massive quantities of gas and only have one or a few connections per plant.

We also had this problem, it is cured by getting industrial size propane cylinders, and connecting them to the Facility, then having the gas company disconnect and remove their meter, No more line charges. And no monthly bill as when you fill the Cylinder, you pay.

Thanks d. I am writing my city now to see what their code is for that.

“Thanks d. I am writing my city now to see what their code is for that.”

In the Corporate Oligopoly US, it would not surprise Me, if there were regulations against it.

If there are. Look at the Regulations/Insurance regarding use of “Indoor Barbecues”

An Indoor gas stove is easily converted to an “Indoor Barbecue”. Nothing says that the Gas Cylinder for the Barbecue “must be” in the same immediate area as the Barbecue. Or can not be connected to it, with a Metal Tube.

Freestanding gas heaters have Individual small cylinders, like the small Aluminum/Steel ones used in Motor Homes and Boats. A little Lateral thinking, can alleviate many Corporate Vampire Fees.

Gas Fridges and freezers are Available, Again with Freestanding Cylinder Hookups Califonts, the same. Califont Hot water does have upsides as a large amount of the Energy consumed by Hot water Cylinders, Is wasted. Simply keeping and unused cylinder full of water at 60/80 Degrees C 247.

MY Boat and Motor home have everything a house has, yet neither, are Permanently connected, to any utilities.

Gas fridges aren’t worth while but gas A/C (ammonia type) might be, depending on circumstances. Gas heat and A/C most likely will convince your propane dealer into offering a contract. Not sure how large that tank will be but tanks can be installed underground.

I think a propane dealer has info you’ll need.

Well at least it helps reduce the trade deficit by a tiny amount (if only by a sliver).

If only you guys would cut your petroleum consumption by 40% we would no longer have an energy trade deficit. This could easily be achieved by driving smaller, fuel efficient vehicles and driving less. I know, I know you guys won’t do it because you like wasting fuel – but allow me my dreams. Dreaming is free (credit goes to Debbie Harry).

I spent almost $10 on fuel for the old Dodge Caravan last year so even I’m guilty of contributing $4 to the energy trade deficit in 2017 – makes me a hypocrite I guess.

My math is bad whats the weak dollar do for all this and particularly NG prices? Some of the gas going to Mexico is probably for US built power plants. Should America have an energy policy, it would be to provide some economic benefit to Japan,and some geopolitical security to Europe, and make the US energy independent. I expect prices will rise when cheap money dries up, how far who can say? Right now on a BTU basis NG is half as expensive as gasoline. Of course you can use NG to make electricity and charge your car, or just put the NG in your car. Trump promotes coal, why is he allowing China to import LNG? Does he suddenly believe in global warming (and gun control) Maybe he should reverse tariff those exports.

Not so easy to NG your car, LPG yes.

The US is once again an energy superpower, with combined production of oil/gas surpassing Saudi and Russia. Exporting to EU is of vital strategic importance, as it keeps the pressure on Russia. All of this in spite of Trumpism (as the export terminals began construction during Obama’s era).

@Nicko2: Not really. It has been estimated that up to half the fracking oil is shipped to Europe because it is a low grade oil and Europe uses the oil as a distillate. Many of the US refineries can’t refine the low grade oil. As a result we still have to use imported oil to make up the demand difference.

I believe it’s completely the other way around. US tight oil is extremely high quality crude. That’s a problem actually becuase most existing US refineries were built to handle much heavier crude. The US has been having to buy tar sands oil from Canada (very heavy fuel) in order to mix it with shale oil so that it can be refined in US facilities.

Actually, as someone who dies this for a living, the crude us light and sweet.

So light in fact, that we can’t make gasoline or diesel from it. The refineries dint want anymore of it.

US refineries handle very heavy crude from Venezuela, they have no problem refining shale oil, which is very light. Shale oil is so light it must be handled with care to keep from blowing up during transport (as has happened a few times in the last decade).

I wouldn’t call any country that need to imports 7 million barrels of oil per day an energy superpower. We may produce a lot (at the moment) but we consume much more, 40% of our petroleum consumption is imported oil.

van_down_by_river,

Timthetiny and Max Power have it right. Light sweet shale oil is mostly composed of short chains of hydrocarbons, the stuff that goes into gasoline and lighter easily vaporized aromatics. Kerosene and diesel are long chain hydrocarbons and so shale oil cannot produce much of that.

In the 1950s, the problem was in reverse – there was a gasoline shortage and they figured out how to “crack” heavy crude with the long chain hydrocarbons into short chains and turn it into gasoline. Reversing that process to produce more diesel from ultra light crude is not something that anybody has figured out how to do cheaply and on a commercial scale yet.

And so, refineries set up to handle heavy crude cannot easily refine the very light and sweet crude that comes out of fracked shale. The refinery owners would have to physically redesign and rebuild the refinery. It’s a different process.

These days, running refineries is all about squeezing out maximum profits since this is not a high margin business – that’s why hardly any new refineries have been built since the 1970s, and why so many of them got sold off from the once vertically integrated major oil companies. So, rebuilding a refinery set up to refine very heavy crude is the last thing these refinery owners want to do.

Citgo, which is majority owned by Venezuela’s PDVSA, would be one of the refinery operations in the US set up for that very heavy crude. And they are not getting enough Venezuelan crude now, and they don’t want to spend money on rebuilding their refineries to refine light sweet shale oil which they could easily get through the crude oil pipelines. So they keep importing heavy crude from wherever they can get it.

That’s part of the answer as to why we keep importing foreign oil, while exporting that excess light sweet shale oil. The other big reason is that the refineries along the East and West coast regions are not connected by crude oil pipelines to the major shale oil field regions, which are mostly in the central regions of the U.S. This shale oil can be piped down to the oil terminals along the Gulf of Mexico and shipped as exports to other countries now, but the Jones Act forces shipping BETWEEN U.S. ports to be on U.S. flagged ships only (the same law that delayed hurricane relief aide to Puerto Rico), which increases the expense, etc. It’s cheaper for these coastal refineries to just buy oil from whatever foreign country they can get it from than to have it shipped on a US flagged oil tanker out of one of the Gulf area oil terminals. Plus, they too are probably not all set up to handle the ultra light sweet shale oil.

Generally speaking, the blessing of abundant natural gas in the U.S. is not shared very much by the the average citizen.

Case in point; The West Virginia legislature just killed a bill in committee which would have imposed a severance tax on gas extracted and, for the most part, exported. It also recently massively increased vehicle licensing and titling taxes.

These two tax policy decisions, taken together, mean West Virginia will remain, to some extent, like a third world country of the last century: Her raw materials exported for the use of just about everyone else in the U.S. and the world, while regressive taxation of it’s citizens pays for domestic governmental services.

“…the blessing of abundant natural gas in the U.S. is not shared very much by the the average citizen.” What? Much reduced pollution and far cheaper energy costs generally due to substitution of gas for coal and oil in both energy generation and manufacturing somehow don’t count? WV counts for 0.5% of total U.S. population. Where do you come up with this stuff?

And the still-ongoing teachers strike in West Virginia is proof of what you say, as some W. Va. residents decide to fight back, God bless them.

West Virginia has been a colony of outside capital since the coalfields first started being developed in the mid-nineteenth century…

Seems the U.K. is having the opposite problem:

“UK running short of gas as National Grid issues deficit warning”

https://www.mirror.co.uk/news/uk-news/uk-set-run-short-gas-12107673

The UK is a net importer of both oil and natural gas, their own production has been declining for years.

A “solution” would be to cut down on gas imports but that would still lead to a loss anyway.

Honesty the current situation were the US both imports and exports gas is insane. If there is enough local production, why import? If there is deficit, why export?

But Green, from dollars, is good and any regulation to control how and who to sell gas is communism, right?

Any country that has no local gas production must think Americans are crazy by the way they are dealing with gas.

“If there is enough local production, why import? If there is deficit, why export?”

I’ll give this a shot.

The US and Canadian NG markets integrated via pipelines regionally. So in some regions, Canadians buy US NG because they need the supply and they have a pipeline connection to the US. In other regions, it’s the other way around.

New England is notoriously isolated from the US NG pipeline infrastructure. The closest producing region is the Marcellus, but the Marcellus didn’t produce much gas before fracking game along. So all this is new, and there was no takeaway capacity at first. Since then, they’ve been building pipelines (and reversing the flow of some) to be able to get the NG out of the Marcellus. But this takes time.

During peak winter months, some utilities in New England don’t have enough supply of NG and they use oil (which is easier to store than gas) and when push comes to shove they import LNG to make up for the shortage. And NG spot prices in the local markets spike to extraordinary levels when these shortages crop up. There has been some discussion of how a pipeline from Quebec could solve their problems.

In other words, it comes down to proximity to producing regions and to pipelines.

I work for a nat gas pipeline company not too far from the Marcellus, have for almost 20 years. We used to take gas from Canada (Dawn hub), usually 300-400 MMcf/day through the location I mainly work at and send it South. About 7 or so years ago, it reversed direction one day. normal volumes now are 500-600 MMcf/day. I would say a lot of it is Marcellus gas.

You are absolutely right. Without knowing the US nat gas grid in detail, I can confirm that in the European gas markets I have traded in fro 15 years now, regional supply/demand balances and various grid bottlenecks result in commercial decisions exactly as you describe them. Between pipeline supplies fro Russia, Norway and Algeria, LNG can act as a balancing mechanism. And let me add that many Europeans are incredibly thankful that the US LNG exports act as a counter balance to our enormous dependence on Russian gas.

“There has been some discussion of how a pipeline from Quebec could solve their problems.” AND the Marcellus – but NIMBY won out. Kinder-Morgan tried to build a pipeline from Albany to Dracut, MA just north of Boston several years ago (Northeast Energy Direct). This would’ve moved some of the cheapest gas in the world to where it is currently most expensive at retail, but the ant-growth crowd shouted it down.

And Canada imports oil to the East Coast and exports it from Alberta. But natural gas flows from West to East through the Trans Canada Pipeline.

It’s not crazy, it’s a function of economics, and transport costs.

In the States, the last time the government got involved in telling the industry how and where to sell fuel, and for how much during the ’70s, the lineups at the gas stations were a mile long and there was no end to the excuses and the blame game by bureaucrats.

Whether it’s nat gas, oil, or gasoline, or really anything, the market handles pricing and distribution well, and allocation and pricing discovery is measured in microseconds, not by the number of votes you can buy by pretending the market is wrong.

Wonderful article…..Wolf. The economics are the fascinating part of the political mess we are in.

Oil has taken a back seat to NG geopolitically,as the number one destabiliser. War in Ukraine? Syria? Tension with Russia? As the US (pulls out its old covert Oil playbook) to screw the Russians/Quatarian/Iranians out of a pipeline through Syria/Ukraine supplying NG to Europe cheaply….

The Europeans don’t want cheap gas via a pipeline…..they want American gas a premium…and can tank the US for it!

How about millions refugees in Europe as a direct consequence of American interferiance in the blocking a pipeline through Syria? Libya a little different….(just read HRC’s email, which Assange gave the world).

If we can block their pipelines, our export terminals should be up and running (if local state governments don’t try to de-rail them first).

Exporting cheap US natural gas probably has more to do with international coercion than anything else. Supply Japan and Japan stays happy with us and all of our sordid demands.

Additionally, I strongly believe, but obviously can’t prove that US fracking is a top level strategic (as in military and economic) imperative that will be supported financially and behind the scenes, if necessary. It wouldn’t be the first market controlled by the US government.

When France and Libya were not so covertly fighting each other over Chad in that series of little known conflicts which became known as the Toyota Wars (1979-1988), Muhammar Gaddafi was happily selling France all the oil and natural gas she wanted, exactly the same he did when in 1986 he fired missiles at the Italian island of Lampedusa in retaliation for that country’s support of Operation El Dorado Canyon.

Morale: when it comes to selling natural gas and oil, politics do not matter.

As an old oilman, I feel compelled to comment. One fact I would submit that may come into play as to our future as a natural gas exporter is that there is still a lot of conventional natural gas to be discovered on the globe.

I have a few prospects for conventional gas in my filing cabinet that I could dust off if the market evolves in that direction.

√

The last estimates I can remember from pre-fracking days are that the US alone is sufficient in natural gas for something like 400 years, and that was based on estimated resources at the time.

Running more autos on NG would surely be one of the prospects you mention should the economics justify it. A lot of vehicles in the world already do run on NG and propane. Probably better than running cars on resource-hungry high tonnage batteries with limited lifespan, though they will always have a place in many applications (historically primarily industrial), and in niche consumer and low distance applications – as justified economically.

Not correct. Adding in something called ‘unproved reserves’ increases the very optimistic supply to 86 years. However, the following must be highlighted ahead of the quote.

(The vast majority of natural gas left in the ground is “unproved.” This means that we cannot readily access it because the infrastructure is not in place, or it doesn’t make financial sense, or the presence of natural gas is assumed but not confirmed.)

Quote:

“The U.S. Energy Information Administration estimates that as of January 1, 2015, there were about 2,355 trillion cubic feet (Tcf) of technically recoverable resources of dry natural gas in the United States. At the rate of U.S. dry natural gas consumption in 2015 of about 27.3 Tcf per year, the United States has enough natural gas to last about 86 years. The actual number of years will depend on the amount of natural gas consumed each year, natural gas imports and exports, and additions to natural gas reserves.

Technically recoverable reserves consist of proved reserves and unproved resources. Proved reserves of crude oil and natural gas are the estimated volumes expected to be produced, with reasonable certainty, under existing economic and operating conditions. Unproved resources of crude oil and natural gas are additional volumes estimated to be technically recoverable without consideration of economics or operating conditions, based on the application of current technology.”

https://www.americangeosciences.org/critical-issues/faq/how-much-natural-gas-does-united-states-have-and-how-long-will-it-last

My opinion that without cheap credit and stock hype offering yield, that is to say if companies actually had to turn a profit to remain in the nat gas business, I doubt the Industry would survive very long.

It will be interesting to see how the looming Trade War will affect the energy industry. I guess we’ll find out pretty soon. :-)

The estimates change every year depending on who makes them and when they’re made. Consumption goes up, what counts as resources etc varies. Lately, resources went up almost 500 trillion in 1 or 2 years. In my example it was a guess made, I think, in the ’90s. Someone else at the same time would have thought different, i.e what counts as a resource.

After all, in the late ’70s according to the MSM, quoting experts, we were supposed to run out of oil by 1987 … they took proven reserves and divided by consumption :)

We ran vehicle nationally on both gasses for a while PROPANE IS GOOD, it simply needs some faults with regulator freezing sorted in many applications.

NG power vehicles are not so good. BTU values vary between fields and suppliers, which raises issue of where you fill and what you are tuned for. There are much bigger regulator and starting problems.

The National Vehicle NG Infrastructure has been removed. Propane is still readily Available for Vehicles, Nationally.

\\\

Natural gas will hopefully now, without significant political obstruction, become a popular vehicle fuel. It’s cheaper then gas and pollutes significantly less then diesel or classical fuel. Given these systems could be manufactured in the USA, it should be a win-win-win situation.

\\\

A good example is Turkey with roughly 25% of cars converted to CNG consumption.

\\\

There is some good literature on this topic online.

\\\

Gas plants are taking over from decommissioned coal plants – off-set by increasing investment in wind/solar; altogether assisting the transition toward EV adoption.

Of course there has been an opportunity window, but what is it at all, if not unfair competition?

…said the horse and buggy makers about the automobile industy

US oil and natural gas production increases will probably remain extremely until they are not needed due to ekectric cars come along.

When we talk about production increases, we talk about tight oil, and fracked gas, but the people I know drilling the Permians basin (Chevon and a couple small producers) tell me that can make a living on $45 oil and $3 natural gas.

Also, virtually all tight oil and tight gas depletion estimates have been literally blown out of the water in the last three years. Few industries adapt faster than oil. Keep in mind, oil is $60 a barrel with Venezuela almost totally shut down.

As to debt, there will be a river of future money going to the oil patch because it’s the only place where a person can get a 10% ROI. I worked in the oil industry in the 80-81 tecession and believe me, finding invetors was not a problem.

So when do our natural gas bills go down if there is such an oversupply?

Are you listening PG&E?

Lots of reasons. Unfortunately, I’m not running a natty school for people to lazy to read.

i was completely surprised by that December spike in natural gas output…i’m on record in at least a few places forecasting that 2017 gas output would be lower than 2016, contra EIA forecasts…so i’ve been very wrong on that front…which makes what is happening here all the more perplexing:

https://rjsigmund.files.wordpress.com/2018/03/march32018naturalgasinstorageasoffebruary23rd.jpg

despite that record production, US natural gas stocks are second lowest on record for late February, albeit a short record…and that’s in the face of a winter that’s turning out to be warmer than normal, albeit not as warm as the last two:

https://rjsigmund.files.wordpress.com/2018/03/march32018seasonalheatingdemanduptilfebruary23rd.jpg

Wolf, I dunno about this one. I think you have it right in that the attractiveness of US LNG hinges on the cost curve of the producers. I.e. if they go bankrupt and stop producing (a distinct likelihood considering the cheap credit/borrowed time they’ve been living on), aggregate supply comes down, Henry-Hub prices go up, and the price of LNG goes up, and US-sourced LNG loses its attractiveness in the global market relative to Qatar-sourced LNG or Russian-sourced/subsidized LNG.

However, consider these developments:

1. The global price of LNG is predominately based on the Japanese Crude Cocktail formula, which has a coefficient/slope multiplied by the current Brent price plus a constant. The spot LNG price is “oil-linked” meaning that as long as oil prices and Henry Hub have large spreads, there is arbitrage opportunity for US terminal operators, i.e. Cheniere. Basically, the oil linkage I think magnifies the opportunity for US producers of LNG to profit more than simply pointing to current gas prices and saying – if this comes up, they’re screwed.

2. The Australian domestic gas market is really screwed up. While on a capacity level, they have the largest ability to export LNG after Qatar but their domestic prices are through the roof. It’s a political disaster. There’s some question as to whether they will actually export their gas to Asia or whether they will force the project sponsors to simply re-export (is it exporting if you’re just sending it back to the same country?) to major Australian population centers. So assuming that development occurs, that’s a lot of supply that does not get absorbed by the rest of the global gas market. In other words, there’s no net increase in supply from Australia because they’ve created the same amount of demand that has to be satisfied. Or at least that’s my guess.

3. Incremental LNG demand has defied predictions so far – most analysts focus only on Japan and South Korea. Look at China in 2017 – most of that demand for LNG comes from shuttering coal-fire plants within city limits to improve air quality – part of its “Blue Sky” strategy. They did this because of the presence of a cheap alternative – LNG. What’s to say that additional developing countries won’t utilize the alternative to coal fired plants by taking LNG cargoes in the interim while overland pipelines are debated and renewable initiatives falter? If that’s the case, the price of US-sourced LNG can rise quite a bit higher and not suffer in competitiveness, even if Qatar expands capacity.

Anyway, just a few thoughts. It’s an interesting market.