And these are the good times.

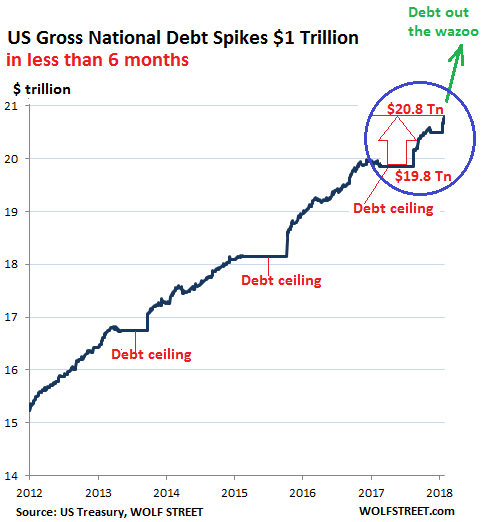

As of the latest reporting by the Treasury Department, the US gross national debt rose by $41.5 billion on Thursday, February 22, to a grand total of $20.8 trillion.

Here’s the thing: On September 7, 2017, five-and-a-half months ago, just before Congress suspended the debt ceiling, the gross national debt stood at $19.8 trillion.

At that time, I was holding my breath waiting for the gross national debt to take a huge leap in a single day – as it always does after the debt ceiling gets lifted or suspended – and jump to the next ignominious level. It sure did the next day, when it jumped $318 billion.

And it continued. Over a period of 8 weeks, the gross national debt jumped by $640 billion. Four weeks after that, it had ballooned by $723 billion, at which point Fed Chair Yellen – whose cheap-money policies had enabled Congress to do this for years – said that she was “very worried about the sustainability of the US debt trajectory.”

Then Congress served up another debt ceiling – a regular charade lawmakers undertake to extort deals from each other, beat the White House into submission, and keep the rest of the world their on their toes. It goes like this: First they pass the spending bills, directing the Administration to spend specific amounts of money on a gazillion specific things spread around specific districts. Then they block the means to pay the credit card bill.

That debt ceiling was suspended on February 8, at which point the gross national debt began to surge again, adding $1 trillion ($960.4 billion rounded to the nearest 100 million), a 5% jump in the gross national debt in just 5.5 months:

In the chart, note the somewhat technical jargon (marked in green) of what will happen going forward. The past week saw record issuance of Treasury debt, and that surge of Treasury debt issuance will continue. The Treasury department now expects that the debt will increase by $617 billion by mid-year.

The debt ceiling is like playing toss with a loaded gun: The gun will normally not go off because almost everyone is trying very hard to catch the gun without pulling the trigger. And historically speaking, it hasn’t gone off yet, and everyone hopes that it will never go off. It’s dramatic, and sound bites from those playing toss permeate the media, but what it really does is distract from the consequences of the fiscal policies that these same people are hammering out in Congress. Those consequences are best summed up over time in the gross national debt.

The trillions fly by so fast these days, we can’t even see them anymore. And afterwards we wonder: What was that? Where did it go?

The Treasury Department, in its Financial Report for fiscal 2017, which it just released, and which was silenced to death by the media, shows where that money came from and where it went. Now, just add the tax cuts and the ballooning expenditures. Read… US Treasury Posts Gigantic $1.16 Trillion Shortfall in Fiscal 2017, Hilariously Points out “Where We Are Headed”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Over indebtedness (unsustainable debt related costs) only has a few solutions. For individuals and businesses it usually leads to some form bankruptcy. For governments that have a compliant CB at their backs the most politically palatable solution will always be inflation, all the better if you can keep it understated without too many people going cross-eyed in the grocery store. Keep that in mind if you’re a saver/investor. A recession could knock down asset values in the short term but expect them back up and heavily in the long.

Very true I made the most money buying great distressed property during recessions and selling after the recovery 1980 and 1992 were two great entry points for me

Your comment just made things click. I’ve been a disbeliever all this time waiting for the “normal” free market environment to return and asset prices to drop to reality levels. But the way you put it, now I get it. It’ll be hard but I guess I’ll just have to hold my breath and start buying on the bigger pull backs instead of waiting for calamity prices. Sad how things are so artificial. But great comment. Thanks!

Well the thing is I’ve been doubtful of this economic “recovery” for a long time thinking maybe it would just suck in on itself like a sink hole and assets values, stocks, etc. would reflect what seemed like the poor second economy for us regular consumers residing on the lowlands of the income distribution hockey stick. In hindsight everything seems clearer of course and it seems the saying don’t fight the fed really was the best investment advice and I missed out due to doubt about that statement. However with the fed tightening you may very well see your calamity prices in not too long (probably within a couple years? Who can say for sure though especially about how much they’ll fall) but who knows maybe the correction in all prices will not be as deep if rates are raised so slowly.

I think certain statements by fed members about plans to come back swinging next time there’s a recession with more potent QE and maybe even negative interest rates is why this parade will continue. You might see a year or two of depressed asset prices following a big crash if it gets here but the second a recession shows up in the data hold on to anything nailed down because I don’t think CB’s will hold back next time. I had several econ profs suggest QE was nowhere near strong enough during it’s time in the past decade echoing the too weak for escape velocity argument economists like krugman were making and despite being a small sample I think it also indicates a strong feeling within the economics community that extends up into the fed that the “stimulus” last time was not enough.

It is what it is but I wouldn’t buy any “dips” right now, but after whatever correction we get, once the fed turns around and government debt levels also require a high inflation rate to remain manageable, which is what I was getting at, asset values will probably be through the roof in the 2020s. Over the next couple years after a correction may be the only truly good buying opportunity for a long time in a variety of assets otherwise you may just be riding inflation after that. Who am I to give advice though… The future is always full of surprises.

“Economy is NOT about morality”, Paul Krigmen. Translation, “if I can make my situation better now by screwing others and my children, I will do it, all I need is my cat”.

“The greatest asset of US is its military”, Obama. Translation, “we do NOT need to be land of the free and home of the brave to lead the world, set out our carriers and you give me stuff at a price I ask using my currency”.

Borrow and spend, live a good life and leave our children with unfounded liabilities? Let’s party.

The thing is, there was occupy wall street, but there was NO occupy the FED. And if any of my coworkers hear anything about property price goes down, they all freak out because they are counting on it to pay off other spendings.

Americans overall seem to favor inflation – so clever with money. The average American is a net debtor and does not save, their debts are partially paid for with inflation and they don’t have any savings to lose purchasing power. Their paychecks may not keep pace with rising prices but that’s a small price to pay to be able to default (via inflation) on their outsized debts. Plus the central bank economists have told them inflation is good and necessary.

Inflation means the plastic junk purchased from China on credit does not need to be fully paid for – it can be defaulted on and as for the Chinese, screw them – they are the bad guys, right? So with inflation we are winning and our frenemies are losing. Win, win!

Only “wage inflation” helps consumers pay for debt. “Consumer price inflation” increases consumers’ debt burden because they have less money left over to service their debts.

But “wage inflation” is precisely what the Fed is most worried about. They like “asset price inflation” and don’t mind “consumer price inflation” (unless it gets too big). But they fear “wage inflation” because it would lower the profits of Corporate America.

People keep saying, inflation helps pay off debt. That is only true for companies; they have more revenues as the prices of their goods rise. It is not true for most Americans; they need “wage inflation” to help pay off their debts.

Also, even wage inflation only helps pay off fixed-rate debt, such as a fixed-rate mortgage. It doesn’t help at all with variable-rate debt, such as credit cards, whose interest rates follow inflation upward.

Right, and as a result, to maintain the standard of living the solution has been to increase leverage. What’s sustained that has been the precipitous fall in interest rates over the past 40 years. That, not inflation, is what’s kept folks (and govt.) above water.

Alas, this trend, having reached the zero bound, is now starting to reverse, which in turn means that yesterday’s solutions will no longer be applicable. That’s what all the talking heads on CNBS fail to understand and/or convey to the sheeple… and it’s what will bring about the next crisis.

[That is only true for companies; they have more revenues as the prices of their goods rise.]

Only true for some companies depending. Asset inflation doesn’t help most of them much. The downside is rents ratcheting upwards as leases expire.

Wage inflation? What’s that? Been two decades since I’ve seen my wages go up. They have actually gone down (thanks to illegal immigrants). And the depression has never ended. That’s right depression not recession. It’s been a depression for the working stiff. Last ten years have been the worst in my life. I’m 56 and have been on my own since I was 15. I lived better at 15 than I do now. American Dream LMAO, American Nightmare is what it is.

“American Dream LMAO, American Nightmare is what it is.”

Globalisation was supposed to raise the lowest boats and improve all live.

When it was first talked about we said rubbish it will drive the labour rates to the lowest common denominator.

What is has done has been abused by china and its American Globalised Vampire Corporate Allies, to leapfrog themselves to the top at the expense of labour and the western Economies, driving the lowest boats lower.

Globaliseation is not the problem, china and its American Globalised Vampire Corporate Allies that abuse it ARE.

The rules need to be changed so that these entities and unfair STATE AID Traders like china can not abuse and game the Glkobal trading system as they currently do.

Since 2008 Western workers have lived in Recession/Depression and still are whereas assets traders, china, and its American Globalised Vampire Corporate Allies have made huge fortunes. Wealth must flow from china and its American Globalised Vampire Corporate Allies back to western workers or there WILL BE huge problems on the planet.

If governments could just print money to solve their problems, I think that would have become standard policy centuries ago. There’s a reason why the U.S. is now doing reverse QE.

QE only redistributes wealth and income. It doesn’t increase the pie over the long-term. In fact, it ultimately decreases the pie by encouraging bad investments, wealth inequality, and political chaos.

” it ultimately decreases the pie by encouraging bad”

NO it makes you give more currency to get the same amount of pie as the “currency” has been DEBASED by QE.

Since 2008 Fed financial intervention (debt) has amounted to $33 trillion, causing $2.64 trillion of cumulative economic growth. This equates to $12.50 of interventions (debt) for every $1.00 of economic growth.

This is a classic example of the diminishing marginal productivity of debt.

I remember the disgust and anger with a Congress, that voted in favor of TARP to the tune of some $800 billion, despite widespread grass roots opposition.

I also remember when the Fed started purchasing their own debt, which caused shock that they were “monetizing” debt.

Remember back when the amount “trillion” sent ripples of horror through the population? No big deal now. More debt issuance, Fed openly buying in the market place, trillions being thrown around like it was “normal”, criminal financial behavior going unpunished, etc. etc.

Same old, same old. Just a different day.

If Japan is any guide to our future, I dont see any debt crisis in the US for the foreseable future, by which I mean in the next 50 years.

Comparing Japan with the US is a lousy comparison

Since the real estate crash of 2007 we have been following the Japanese scenario almost identically, why is it a lousy comparison?

Here are are a few reasons: big trade surplus, good condition infra-structure, a very stable political system with virtually no ethnic or religious fault lines. No evangelicals of any religion having any say in government ( aka., separation of church and state.)

Almost crime free. You can leave your wallet on the seat at a KFC etc, and an hour later it will still be there. Violent attacks on strangers almost unheard of, very safe for women.

Gun murders usually under 10 per year. One year recently there were none.

This place can take a lot of stress without snapping. By comparison some US states seem on the brink of secession.

Can you blame them?

Because the Japanese own the majority of their own debt whereas that is NOT the case with ours The two societies could not be more different in nearly every way imaginable actually

I forgot to mention a biggee as you say: debt held internally.

There is one more important thing – Japan manufactures almost every imaginable thing and do it perfectly. They certainly have a problem with resources and their trade goes into deficit, when those rise in price, but otherwise they have enough capacity to accomodate any imaginable increase in demand both domestically

and abroad.

And Japanese debt has emerged not just because of fiscal latitude, but to a significant degree as a consequence of the major natural disasters that hit the country.

You could use Japan as your example but with nearly 1/3 of all working age Americans on sabbatical we’re probably more akin to the Soviet Union.

Thanks for this perspective, Wolf. The climbing debt rates for so many countries is absolutely mind boggling. I listened to an interview with Hazlett? during a WH briefing the other day. They are now talking about what a change in forecasted growth this debt trend has produced…from the anemic 2.2% to a whopping 3%. (What happened to the 4-5…even 6% growth talking points?)

I guess the problems are simply baked into the political process. No one will get elected promising austerity and belt tightening, aka reality.

It just seems like there is absolutely no country on earth that is living within their means these days. None. And while the news cycle seems frantic, consequences and change is always in slow-motion. I just read the other day that Devos is making changes that might allow student loan defaults? I suppose this means default, then tax-payer bailouts for the institutions further adding to the debt with emergency legislation covering losses.

I still believe the careful individual who pays down debt will be better able to withstand the forces of reckoning that are looming. When I look back at old Depression era photos I don’t imagine any of the people thought they would be standing in soup lines with just the clothes on their backs. It was a pretty normal sight for the times and not that long ago. The only work my Dad and Grampa could find was working in a slaughterhouse in the Twin Cities. My Grampa told me that his job was to ‘stick pigs’, and said he could hear them screaming for the rest of his life. That was after he lost his fuel business to bankruptcy. (no one had money to pay their bill). He just delivered his oil to folks who needed it until it was gone. The times were great until it all stopped.

And then came WW2.

I don’t think they can get any more inflation than they already have, and Japan is a bad comparison. The bond market (globally) has gotten so large it does not move efficiently, which is to say whichever way to want to manipulate rates, it’s not likely to follow easily, or quickly. To wit the problem then is not OLD debt but new debt. I am not sure the old debt cannot be orphaned, depending on how much of it is held as collateral through forex, or pension funds, honor the principle, cap the interest. If I was Trump I would try this trick, nothing to lose really.

Interest rate differentials allow America to export ANY excess printing?

Trump, debt, tricks?

Like he did for the Taj casino?

The Majority of US debt is also held by Americans.

If you have a dollar bill in your hand you have a liability, as for debt debt or treasury debt there’s the distinction. 45 feels like he can haircut those treasuries held in forex accts without hurting US widows and orphans. Better yet trash the dollar and those holding bonds domestically are okay, while the offshore bond holders scream. Looks like that is his plan.

Two words come to mind that sums up Wall Street Banks and the Federal Reserve – Control Fraud. So what are the characteristics of Control Fraud? Control fraud consists of ease of obtaining control, weak regulation, ample accounting abuses, and the ability to grow rapidly.

Correct me if I am wrong but is not this national debt counterbalanced by an equal amount of money in circulation here in the U.S. and globally?

Does this debt necessarily cause a problem related to solvency? I am not seeing that as much as risk of inflation.

Every financial debt is ALWAYS someone else’s asset. So yes, every debt is “counterbalanced” by definition – but that is totally meaningless. The debt is owed (by the debtor) and must be paid to those that hold it in their portfolios (the creditors). If not, there is a default. And in such an event, these assets held by pension funds, investors, etc. get wiped out. The global damage would be unthinkable if you tried to do this with Treasury securities.

“The global damage would be unthinkable if you tried to do this with Treasury securities.”

And yet, some people do think about such things, particularly about how best to make it happen. Sufficient damage could render some governments so helpless they could be drowned in a bathtub, which is an explicit goal of certain anarcho-capitalist circles.

Connecting the dots is frequently bad for my blood pressure.

How does that square with QE? Allowing bonds to roll off the balance sheet? With bond buyers who use margin? Impaired collateral? Fractional Reserve banking? In Argentina 2006 there was no global bailout of the bond market, but there was a white knight who bought stocks, and it might be that this is the public/private difference in approach. At some point as you allude to, the public solution will fail.

The debt dwarfs the cash in circulation. The cash in circulation is only about 1.6 trillion.

The debt is often held by pension funds, who have been having a rough

time since 2008 because of the low returns on it.

The frequent calls for debt liquidation either through inflation or actual repudiation (or reneging) is fundamentally a desire to loot the cash paid into pensions during the workers’ employment.

If gov. would enact a 10% sales tax and 10% transfer tax on crypto’s they could spend to they’re hearts content. Then they will support crypto prices to the moon.

I wish I could figure out how do do this with my personal finances. I could live high on the hog. Until, that is, it blew up in my face.

It’s certainly true that debt is a problem but not the largest one. Americans have approximately $100T of net wealth. Taking that into account and setting aside the unfunded liabilities (SS and Medicare), the American balance sheet doesn’t look so dire. The real issue is the distribution of wealth. The top 0.1% owns as much wealth (roughly $22T) as the bottom 90%. How in the heck did that happen?

In a democracy, what is to prevent 51% of the population organizing and voting to confiscate the wealth (or prospects of obtaining wealth) of the other 49%? In a way, that is what is happening via the mechanism of Central Bank manipulation of the financial markets. Quantitative easing was little more than a global banking-cabal counterfeiting $trillions and laundering that money through the asset sales of well-connected insiders.

Holding interest rates this low for this long is very bad policy. QE wasn’t only bad policy, it was a heist. Reverse robinhood on steroids. The single largest theft since the founding of early Sumerian civilization and an epic wealth-transfer upward. We would have a far healthier economy (and society) if asset prices rose in tandem with middle-class wages instead of being manipulated higher by printing-press fiat and interest-rate manipulation.

And although the 51% didn’t actually vote for these Central Bank policies, their elected representatives certainly allowed it to occur. What’s to stop it? Roughly 50% of the US population owns stocks in some form. While the vast majority of the value is held by the top 10%, there are enough people participating in the market that they’re not going to complain about a “whatever it takes” policy to keep asset prices elevated. In a slight twist of the Upton Sinclair saying, It’s hard to get a man to understand something when the value of his 401k plan depends upon his not understanding it.

All this is not without a downside, however. Too many are being left behind as their purchasing power evaporates over time. The social fabric of the country is being rapidly and permanently altered. The next generation of young kids (who aren’t being financially helped by their parents) are going to have a difficult time achieving economic mobility.

Perhaps the only fair way out of this is to heavily tax the estates of the top 0.1% and use those funds to pay down the debt. But as ever more wealth flows to the top, the corporations and oligarchs will be able to purchase even more political power to prevent this from occurring.

Is the system beyond repair at this point?

The problem is that there isn’t much cash flow behind that $100T when the S&P CAPE ratio is at 34. When it mean-reverts, as it eventually will, those 100 big ones will come down, a lot.

Max, I would agree with you if we could get the Central Banks out of manipulating and pegging the markets higher. Unfortunately, that ship has sailed. Rising stock prices have become one of the more important political barometers for measuring economic success with the President bragging about it constantly. They may want to slow the rise a little for fear of letting the bubble get away from them. Not to mention they’ve created a wealth divide within the country that would embarrass a banana-republic dictator. But it seems unlikely that they would allow a significant sell-off to occur without pulling out all the stops.

https://www.reuters.com/article/us-usa-fed-yellen-purchases/yellen-says-fed-purchases-of-stocks-corporate-bonds-could-help-in-a-downturn-idUSKCN11Z2WI

You are assuming CBs can always maintain control. I am not so sure.

Trust me, there WILL come a day when valuations will suddenly matter and a crash will ensue, with CBs being limited in their ability to placate the situation (unless you count Zimbabwe-type solutions as acceptable).

Speculation can run rampant in the markets for a very, very long time but make no mistake, eventually actual cash earned by companies per unit of ownership (share) will affect valuations. It’s not a matter of “if”, but “when”.

I reckon they could always raise taxes instead of cutting them.

NOW that’s a novel idea Imagine a man with common sense But seriously I very much doubt it would make much difference unless they get serious and tax the very rich heavily

Raising revenue is not the only reason to maximize taxes on the very rich. Judging from policy documents from the 1930s, it is also to prevent them from having the easy means to corrupt the government to its own destruction, thereby leaving the general population to their tender mercies. Not that this could actually happen, of course.

Our current situation is “Representation without Taxation.” It denies accountability. If revenues were in line with spending, then the constituents will have a stake in the budget outcome. Right now budget items are at the bottom of the list of concerns. You don’t how much magic helicopter money they spend.

Why is this an issue? Reagan proved deficits don’t matter (as Dick Cheney famously made clear).

There is no shortage of dollars in the world so if the government can spend them to do so many wonderful things why shouldn’t they/we? For example, we need more aircraft carriers (we only have 10), sure they are sitting ducks in the event of a shooting war but they bring us prestige and that’s worth more then anything, we Americans value our prestige and power above all – we should have what we want.

We don’t even have a wall to protect us against Mexico – they could invade and conquer us any moment – we are wide open down there. Ditto for the Canadian wall. Obviously we need to ramp up spending not cut spending and Americans work hard for their money they should not be asked to pay taxes when the money can just be borrowed or printed. At last we have someone in the white house who can lead us to prosperity and safety (and all you can eat free lunches).

Nick, Can you say “sitting duck”?

“I believe there are 13 carrier battle groups (a carrier plus attending vessels) Indeed they are toast in real war, not gun- boat police actions where the opponent doesn’t have an air force.

The aircraft of today fly 4 times as fast as WWII. The carrier still goes 30-32 knots. Bombs and missiles no longer miss. ”

So Modern surface fleets, do not have missile defense system’s??

The English had 1 Proper carrier in action in the Falklands. They should have had 3 for an operation like that.

They also did not have missile defense for Exocet.

Argentina was not supposed to have Exocet .

However the french an English NATO Allie (ALLEGEDLY). Wanted to live test the Exocet on English Sailors and Ships, so they supplied them to Argentina, to use on their NATO Allie.

The loss of the Sheffield in Particular changed for ever the way modern combat ships were being built at the time.

The Chinese have anti-shipping missiles that launch to low earth orbit before screaming in at mach 6 – ships have no defense and are sitting ducks against these systems. The U.S. and Russia have similar systems and the technology is improving. The missiles can be armed with tactical nukes – so yes surface ships are antiquated, sitting ducks. Aircraft carriers are a colossal boondoggle that an overextended empire can ill afford.

This time is different. This printing and massive creation of free money. What is not different is moral hazard never ends well. What can I do? I can only follow the path of the 1930’s. Have no debt. Own hard assets. Be as self sufficient as possible. Have a trade to barter. The biggest difference will be, I doubt anyone will stand patiently in bread lines. We are all armed now ….. win

And dont trust any bank. My father told me of stories back in the thirties. How a bank will close one night and open as another the next morning. Poof went your money.

Most Americans do not know that they are

Unsecured creditors for banks in which their money is deposited. Things can easily go poof again

Ah yes the bank of terra firma may arise again

Bet

We probably will get our money back but we will be paid in debased worthless dollars as money printing goes nuts . Ironically just what happened to the pensions funds after the Soviet Union collapsed .

No one lost a dime in a Canadian bank during the Depression. Last loss for depositors was Home Bank 1926.

I find it mind boggling that the US has over 4000 FDIC insured deposit taking institutions or at least 20 times Canada’s per person.

When Clinton buddy McDougal bought a bank in Arkansas he did it with (roughly) today’s cost of a McDonald’s franchise.

On the plus side, temporarily, his bank soon acquired a major new real estate client.

Deposits are now unsecured loans to the banks by depositors.

If banks collapsed, the FDIC could cover 50 cents of each $100.

If, if, if… If every car in the US got into a fatal accident at the same time, all insurers would be instantly bankrupt, and payouts would be nearly nothing. But the chances of that are essentially nil. That’s how insurance works.

FDIC is insurance. The chance of all banks collapsing simultaneously is essentially nil. And if too many TBTF banks are teetering on collapse, the Fed steps in as lender of last resort, as we have seen in the past.

And if a bank collapses, the FDIC takes possession of it. Stockholders get wiped out. The FDIC gets all the assets and takes care of the liabilities in accordance with their place in the capital structure. So far, over the hundreds of bank failures the FDIC has handled, after secured creditors were taken care of, there were always assets left to cover at least some if not all of the insured deposits.

Not all deposits are FDIC insured (see FDIC rules, including the $250,000 limit). Insured deposits get paid in full. If there are any assets left after that, which there often are, uninsured deposits get covered pro-rata based on what is left.

I have been through 3 bank collapses including what was then the second largest one ever (MBank in Texas) and later Washington Mutual, and I have never lost a dime. Actually, I didn’t even know the difference, except that the bank name on the deposit changed.

This fearmongering about the FDIC is not based in fact and has no place on this site.

“This fearmongering about the FDIC is not based in fact and has no place on this site.”

You said it much nicer and gentler, than I thought about doing several hours earlier.’

I was confident you would correct the poster.

Wolf, your articles are always informative and thorough, which is why I have been reading them for years. Your policies prohibit political discourse here, and my comment was verging on such, for which I apologize.

The information, as far as i can recall, is from one of your previous articles. I never considered it fearmongering. Being aware or perhaps even cautious does not equal fear.

Anyway, inflation will wipe out more wealth that too-big-to-fail banks ever will.

Commoners cannot do much about these things, anyway, so there is not much point to worry.

When all hell breaks loose, and it will, asset prices, that have been inflated, will crash and all the debt that has been accumulated in preparation for an inflationary environment will grow like a mountain before those that hold it. Cash, once more, and maybe for a short time, will be king. JMO

To me, the US debt is like Yellowstone … eventually it will blow up big but please, wait for me to go onto my celestial reward first.

There is an old Alberta bumper sticker that has been updated with the addition of one word.

It now reads: ‘Please God send another boom and this time I won’t piss it away. Again.’

I believe that was a Houston bumper sticker first. I used to have a sign in my office that said “Please don’t tell mama that I’m working in the oilpatch. She still thinks I’m playing piano in the hoor house.”

When the US treasury load long range ordnance, corp debt

will pay the price.

Many symbols have chart looking like “shoot the stats”, but their ratio of ==> equity / equity + current & LT debt + liabilities is 45% and now have reached the highest high.

The length of this trading range is 1991 to 2018 = almost 30 years.

Is this length important : trust me it is !!

What this debt accomplished : mostly dividends and share buy back.

U can blame the Fed for producing guns for the financial captains, but corp CFOs hands control the trigger.

Since the recovery in 2002, shares o/ s fell by almost 10%.

The leaders of the pack had a more drastic shrinkage.

The owners of those co, who adore dividends, own nothing but skeletons.

Let me correct my comment : there is nothing to worry about gov debt,

especially about corp debt. Don’t worry, March 2018 will be great !!

Word.

https://realinvestmentadvice.com/how-corporate-debt-confirms-the-everything-bubble/

I can hear u laughing.

A trillion here, a trillion there, and pretty soon you’re talking about real money. (With apologies to Everett Dirksen).

Wolf were can you get information on what did the US government expend money in 2017?

I know the military budget was a huge part of it, but what about the rest?

For 2017, you can look here:

https://wolfstreet.com/2018/02/19/us-treasury-posts-gigantic-1-16-trillion-shortfall-in-fiscal-2017-hilariously-points-out-where-we-are-headed/

My article has the link to the Treasury Department’s “2017 Financial Report” that gives you the details and charts.

And this is how the $4.5 trillion in costs were divvied up:

24% Department of Health and Human Services

22% Social Security

15% Department of Defense

11% Department of Veterans Affairs

22% All other

6% Interest on Treasury Securities held by the public

To get total Defense and Intelligence spending:

— 15% of DOD plus 11% of VA = 26%.

— DOE handles the nuclear weapons programs = $30 billion.

https://energy.gov/fy-2017-department-energy-budget-request-fact-sheet

— The 17 US intelligence agencies are spread all over, including DOD, Homeland Security, DEA, etc. Some of the budgets are black.

If you add it all up, you’re looking at around 30% for the total defense and intelligence complex. They split it up for a reason. It’s a scary big number.

Social Security is entirely funded by SS payroll deductions (plus some). Its funding comes from contributors and not general tax revenues – for that reason, many people say it shouldn’t even be on this list.

The nuclear weapons budget is really way bigger that it should be considering how much cheaper than 30$ billion is to actually build nuclear weapons and that’s taking in account inflation.

One wonders what the heck they use all that money for.

Paperclips? Paper? Expensive vacations?

Trying to stop other countries from having it’s own nuclear weapons?

One would have to look how much France wastes on their nuclear weapons budget and compare.

Because this looks like some people got into “creative accounting”.

Or they are paying for every vehicle that can just “carry” nuclear weapons.

“A self driving military tank?”

“It can carry a mini nuke if you remove one of the seats.”

“Approved.”

Yes, Social Security is funded entirely by payroll deductions from taxpayers. Not one penny comes from the federal general fund. The money listed in the chart is money borrowed by the federal govt. being PAID BACK to the S.S Trust Fund. The federal govt. has been using the S.S Trust Fund as a loan piggy bank, but the Trust Fund must be paid back. The borrowed money is held in U.S. Treasury bonds. It is real money, in spite of the lies spread by Republican pols. Most of the federal debt is from military spending, where the federal govt. has borrowed money to fund absurdly high defense budgets, which enrich military contractors. Ike was right – the military-industrial complex is a treat to democracy.

Typo: that should read “threat to democracy”

Raxadan wants to know what government spent money on in 2017…

Google 2017 federal budget pie chart for a quick picture,,,, you will find about 70% of spending is entitlements (all UnConstitutional BTW) , social security, Medicare, etc,, 15% defense (which is specifically authorized in the Constitution) and 15% other Discretionary,,

More than $700B is spent on the military every year, they really can’t nail it down but that’s Jolly Green Giant budgeting.

So you suggest entitlements people were specifically taxed extra for should be cut in order to continue that huge waste of military spending or pay down debt?

Mean Chicken

I agree we do not need to spend more on the military but we just need to spend the money more effectively. Like Rome we are overextended with over 1,000 bases in over 100 countries . We should get the Generals together and shut down the ones we do not need . People could get redeployed in other bases and the money saved could be used on other military hardware . We also need to ask the generals what military hardware that they do not need ,cancel those contracts and spend the money on what they do need .

Empire is not optional for the United States, but essential – until it is prepared to hand over control of the high seas and trade routes to China.

Whether that transition will be peaceful. or via war…….

The message from Washington is the entitlements are driving 70% of our spending, meaning they are 4.5 X larger than defense. But how can our nation can fund wars in the Middle East for over 10 years and keep our defense budget at 15% of spending. The 9 year Vietnam War upset our spending in the 70’s. We added The Homeland Security Department since 9/11 and more intelligence apparatus. We have over 700 military bases and 200 embassies we maintain. And in Iraq we built the largest (10 times bigger than any other- consists of 20 buildings) embassy at a cost of over $700 billion and an annual operating budget of $1.5 billion. Social Security at present is paid for by the payroll tax – 6.5% from each worker and 6.5% from our employer plus the money the US government borrowed over the years from the SS Trust Fund. Maybe only 50% of Americans pay income tax, but all workers pay the payroll tax which generates as much revenue as the income tax and almost 3X more revenue than corporation taxes,. The payroll tax has been used as a piggy bank for Washington to fund the general budget instead of saving it as Greenspan claimed in 1983 when they doubled the payroll tax because he knew the Baby Boomers would “tax” the system. Medicare is a problem as our healthcare system is to say the least a mess. Medicare is an entitlement but for those of us who have paid the payroll tax for 35 years SS is not an entitlement because if I would have not paid that tax and simply saved it in a bank it would be worth about $2 million today. Washington wants only those making below a set cap of income to pay the payroll tax allowing the higher incomes and the capital interest gang to avoid paying, but now than deficits are becoming an issue they want to tap into a program that only the workers contributed to for decades. But they can give tax cuts to corps and the rich now and in the past with Bush II.

That is why I have this rant. Sorry Wolf.

In the last year, corporations contributed only 9% of federal revenues. And this is before the recent tax cuts. Don’t tell me that corporations are over-taxed!

You may have made some good points LE but I couldn’t find them in the wall of text…paragraphs with spaces between them would be helpful

If the US had a VAT like all the other industrial countries the proportion of taxes coming from corporate economic activity would be much higher. At the same time it would eliminate the incentives for tax havens, offshoring and inversions which is why that number is so small.

“If the US had a VAT like all the other industrial countries the proportion of taxes coming from corporate economic activity would be much higher. At the same time it would eliminate the incentives for tax havens, offshoring and inversions which is why that number is so small.”

Rubbish.

Corporates dont pay GST/VAT consumers do.

Corporates that are making money don’t pay tax either, (In the current stupid system)they make a Profit, and the Consumer pays their taxes for them, on top of their profit margin.

Every cent in VAT/GST I pay to the State, I COLLECT from a Customer..

It’s ridiculous to tax corporations,,, taxes are part of their operating costs that they pass on to consumers..so if you want to see who will pay if we raise corporate taxes go LQQk in a mirror. ..

Imagine after all these decades the Corp world realized they should not pay taxes. This is the message they want to spin. But taxes are part of their costs and thus their price of product or service. Means they must stay competitive to sell .

The corps only generate 10% of tax revenue and that is with their financial schemes and hiding profits offshore.

We help pay the taxes for the plumber, the hairdresser, the barber, the tax accountant, etc. Why should the Corp world get a pass?

If you put in the “bank” the max possible SS contributions for 35 years then assuming an average deposit interest rate of say 3% you’d end up with about $750K future value. To make it to 2 million you’d need an average compounding rate of about 7.5%, which is way more than any bank has ever paid on a long term basis.

Correction to the numbers above… at 3% you’d get just under $1 mil after 35 years. To get to $2 mil you’d need a deposit rate of 6.5%.

Just for comparison… Thanks to our wonderful Federal Reserve, the highest FDIC insured deposit rate you can get now is about 1.6% (which is “great” given that for years you couldn’t even get 1%).

Each time the Debt Spikes after the Debt Ceiling is lifted is because the government is paying back the money they borrowed from the Pension Funds so they could run the government until the Debt Ceiling was raised .

The USA prints its own currency and could easily pay off its debts in the snap of the finger. So, what pristine country are we comparing the USA to?

This false notion, that in a world where most people are impoverished there’s some intangible nanny figure waving its finger at us over a few trillion is preposterous.

There are no bond vigilantes coming to get us, the USA is not Zimbawe. It is a large diversified economy and the world reserve currency to boot. The only reason China and other can run trade surpluses is because of US deficit policy.

Everyone knows what the implicit US economic policy is and hence there will be no consequences. Government demand for dollars is still demand, and this is helpful not harmful to economic growth.

David Stockman spends alot of time writing doom and gloom articles(very well written) on the deficit day after day with copious charts and detailed correlations, but the truth is deficits don’t matter because everyone knows they won’t be paid back.

Ballooning government debt doesn’t matter only in some people’s minds.

√

This ballooning is what is causing the world to seek another Cleanest dirty shirt.

Every-time the world starts doing this, the printing presses in Tokyo Go into OVERTIME mode.

What’s the big deal? If there is no debt there is no US currency. The more the merrier. Every federal reserve dollar created is a dollar owed.

One day all of this debt will come back to haunt the US and the US$ will lose its reserve currency status. It will be a bad day for the average American.

Very true Anon70 Got Gold?

That is why we spend trillions on defense……you’ll never collect from the biggest boy on the block…..will not even try.

Historically speaking, public debt has always been more a problem of perception than anything else.

For example in November 1449 the commons were horrified to discover King Henry VI was £372,000 in debt, a truly impossible figure for the times. The ensuing political storm helped precipitating the highly complex series of events we now call War of the Roses which reached its apex in wholesale slaughter at Towton and Tewkesbury.

Yet King Henry’s father and namesake, the scourge of the French, died in debt to the dizzying tune of £310,000. Did those 62,000 extra pounds somehow cross some political and fiscal Rubicon? Hardly. The English Crown was just as broke as before.

What had changed was the king himself.

In the Middle Ages public debt was usually tolerated by the parliaments and magnates voting grants of money to pay for the interests on said debt if the rule of the king was perceived as successful.

By all standards Henry V was a wildly successful king, and hence his enormous debts were tolerated and grants of money voted without too much fuss to cover the growing mass of interest.

His son, while personally a gentle soul with a laudable interest in popular education, was a terrible king. Hence debt became a problem because the kingdom at large, from the wealthiest magnates to the humblest peasants, perceived their money was being thrown down the well of an ineffective government ruled over by a limp king.

While what we expect today from our governments has changed somehow (we expect a few more sewers in working order and few less slaughtered English and French knights), it’s beyond doubt the perception we have of our public debts is closely tied to that of the governments.

The growing worries around the developed world about public debt are tied to a slowly and steadily disintegrating trust in governments, which are increasingly seen in negative light as they fail to fulfill more and more of the tasks they arrogated for themselves.

Our forefathers would have shared our worries about the inability, or unwillingness, to exact accountability from great (financial) criminals and Henry VI’s contemporaries would have found present day persecution of basically harmless fringe elements depressingly familiar.

Like in those times the public at large is generally (and willingly) kept in the dark about the size of the public debt. When the 1449 Parliament adjourned for Christmas, members of the commons returned to their homes and spread the news, which shocked the realm. “So poor a king has never been seen” went a number of contemporary popular songs, albeit Henry VI’s household cost the kingdom £24,000 per year, all covered by a generous tax on wool Parliament had (foolishly) voted while the king was still a minor while the kingdom was still high on military victories in France.

They say history doesn’t repeat itself, and it’s true. But it rhymes an awful lot of times.

Moving closer to now, but still in the 18th century one of the first UK PMs, spelled roughly ‘Castlereigh’ said: ‘It’s a good thing war is so expensive, it tends to keep us out of them’

This was before the era of unlimited deficits.

PS: On this site you get a fair few of the ‘debt doesn’t matter because we can just print’ etc.

But you find even more on the Guardian: ‘we can just print pounds forever ‘

The UK has by far the smallest economy backing a reserve currency in the exclusive SDR club.

It pound has already been rescued once by the IMF (mid 70’s) and will get a frosty reception if it comes calling again.

Both US and UK currencies will collapse eventually if they just keep borrowing but the UK is a lot closer.

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

The Sun Also Rises Ernest Hemingway

Two competing historical Quotes .

” Give me control of a Nations money supply and I care not who makes the Laws . ” Rothschild

” If the American people ever allow Private Banks to control the issue of there currency first by inflation than by deflation, the banks and corporations that will grow up around them will deprive the people of all property until there children wake up homeless on the continent that there fathers conquered . ” Thomas Jefferson

My father, who was a depression child, was adamant about staying out of debt…especially after seeing his millionaire father wiped out in the Depression. “Sooner or later you have to pay the Piper” has been around for a long time. When I read about the continued growth of margin today i see the remnants of the dot com era only this time it is the normal folks who “missed out” on Bitcoin.

The ZIRP folks at the Fed have all gone off into the sunset while the seniors who lived frugally and lived by “preservation of principal” all got screwed as the ZIRP folks exacerbated the Division of Wealth.

Today’s social media has magnified the “knowledge effect” of all news, both real and fake, to the detriment of modern history. As mentioned in a post above all you have to do is go grocery shopping or see the price of gas to understand inflation…not all the Wall Street ratios. The average American lives by self preservation and can only bear witness to the inevitable day of reckoning when we will have to Pay the Piper.

USA-Land of the free and brave.Havin tried to internalize allwhat is written above,2questions:

1.Can the US economy be considered as a war economy;

2.Can de current government be considered as a semi-militairy junta.As an european citizen I think the number of medals& uniforms walkin around as well as the uttered opinions rather frightening,at least when it comes to democracy,whatever tht means these days

Why isn’t it clear military contractor stocks are outperforming the FANG gang? It’s pretty obvious what’s been happening for over three decades but the narrative is controlled to put the focus on FANG, etc., and keep it off the wasted giant pile of money handed to the MIC.

Try driving around the beltway, that’s all MIC money. A huge influence of unimaginable proportion that once it goes flop will change the dynamics greatly. Wait and see, remember I told you so.

What is preventing central banks from issuing themselves electronic ‘money’ out of thin air and purchasing everything in sight, every listed stock on the planet, every bond and as much real estate as they desire? It costs them absolutely nothing to create infinite sums of ‘money’, so they could own the world for zero cost. Our money is not real, it isn’t hardly even printed anymore. It is digital, conjured up on their computers. Our FED has been monetizing most of our Federal debt for some time now, or interest rates would have soared long ago. We the people owe the banks principal and interest on what cost the bankers absolutely nothing to create. Central banks are worthless, dangerous parasites. They are eating us alive! What is there out there to stop this?

How can the stock markets of the world ever decline if central banks can manufacture infinite currency to buy anything and everything? Conversely, how can gold and silver prices ever rise if central banks (through their bullion bank agents) can drown the futures markets with unlimited ‘paper’ gold and ‘paper’ silver anytime precious metals prices threaten to explode upwards? Unfortunately, precious metals prices are set in the futures markets where the ‘supply’ is virtually unlimited. There are no position limits on naked shorting gold and silver in the futures markets.

We are screwed! There is no place to safely redeploy our limited investment funds. Collectively our resources are limited, while central bank resources are unlimited. I’ve tried to explain this to my family, friends and church associates, but they look at me cross-eyed and just shrug. They are clueless and assume that I have no idea what I’m talking about.

Ah, well, I’m in my mid 70s, have a bad heart (two stents and chronic arrhythmia), so it’s most likely not my problem, as I won’t be around much longer. Either a stroke or a heart attack could take me out at any time. But it is my kids problem … and my grandchildren’s problem. God help them, ’cause I won’t be around to rescue them. They don’t want my advice anyway. Good luck to them! They are going to need it.