Will Social Security Be There for You? Yes, but…

By Wolf Richter for WOLF STREET.

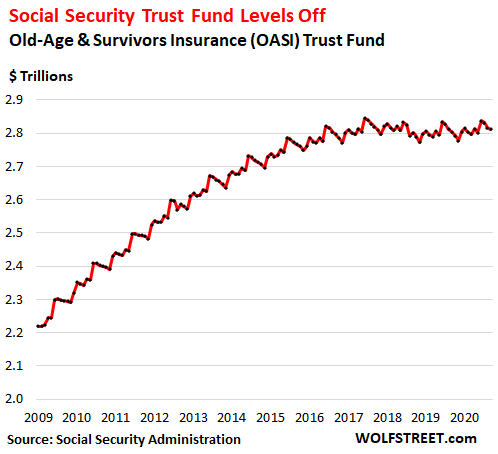

The Social Security Trust Fund – officially the Old-Age and Survivors Insurance (OASI) Trust Fund – closed the fiscal year 2020 at the end of September with a balance of $2.81 trillion, the second highest fiscal-year close, behind 2017, up by $6.8 billion from a year ago, and up by $10 billion from two years ago, according to figures released by the Social Security Administration. The Trust Fund has vacillated in the same range since 2016, after growing substantially over the past decade.

The balance is seasonal and peaks in June. The all-time peak was in June 2017, at $2.85 trillion. In June this year, the balance was $2.84 trillion. So far so good:

The Trust Fund invests exclusively in special issue Treasury securities, of two types: $2.797 trillion in interest-bearing long-term special issue Treasury securities and $14 billion in a short-term cash management security, called “certificates of indebtedness.” These securities are not publicly traded, and so their value doesn’t change from day to day with the whims of the market. The Trust Fund purchases them at face value, and the US Treasury redeems them at face value.

By contrast, a bond mutual fund that holds marketable Treasury securities must “mark to market” its Treasuries on a daily basis (producing a gain or loss).

By investing exclusively in Treasury securities that are not exposed to market whims, the Trust Fund follows the most conservative – meaning, low-risk – strategy possible.

This setup is an efficient, low-cost way of administering the Trust Fund and doesn’t allow Wall Street to extract fees and load the fund up with risks. That’s why Wall Street hates the Trust Fund and wants to “privatize” it in order to get its hands on the $2.8 trillion, extract fees out of it, and use it as dumping ground for its risks.

According to the 2020 Trustee Report, 54 million people drew Social Security retirement benefits at the end of 2019:

- 48 million retired workers and dependents of retired workers

- 6 million survivors of deceased workers.

The Disability Insurance (DI) Trust Fund is separate from the OASI Trust Fund, and is not part of this discussion here. But just to note: In 2019, it paid benefits to 10 million disabled workers and dependents of disabled workers.

During 2019, 178 million people paid into Social Security via payroll taxes. These contributions, together with interest income from the securities, generated income of $1,062 billion. Total costs of the program were $1,059 billion. A $3 billion surplus. That was for fiscal 2019.

The Trustee Report for fiscal 2020 – the 2021 Trustee Report – is not yet available, but we know already that the Trust Fund grew by $6.8 billion this year. So far so good.

Three issues: Demographics, the Fed’s interest-rate repression, and inflation.

Demographics.

For now, the Trust Fund is benefiting from millennials having entered the workforce and gaining earnings power as they move up in their jobs. But there is also the drag on the Fund of the boomers who’re now between 55 and 75 and are transitioning into retirement in ever larger numbers. For the past few years, the equation has been in balance – with millennials and boomers being both huge generations. But it will gradually change, and when it does, it will show up as a downward slope to the line in the chart above.

The Fed’s interest rate repression.

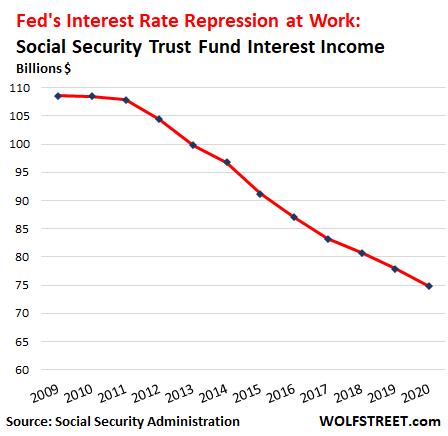

The effective interest rate earned by the securities in the Trust Fund has been declining for years, particularly after the Financial Crisis, when the Fed used QE to force down long-term interest rates. And the Fed’s current interest rate repression will show up as lower interest income in future years.

In September, the weighted average interest rate earned on the securities was 2.53%, still higher than current Treasury yields, thanks to long-term securities that carry the higher interest rates of yore. But since 2009, it has fallen by about half. And at current interest rate policies, the declines will continue.

Despite the 27% growth of the Trust Fund from $2.22 trillion in 2009 to $2.81 trillion in September 2020, interest income has dropped by 30% over the same period:

Beware of Vicious Dog: Inflation exceeding COLAs.

The monthly Social Security payments are adjusted for inflation via annual “Cost of Living Adjustments.” These annual adjustments are based on a formula that uses the “Consumer Price Index for All Urban Wage Earners and Clerical Workers” (CPI-W) in July, August, and September. The Bureau of Labor Statistics will release the CPI for September on October 13. The COLA for 2021 will be set after that. So, just guessing here, based on CPI-W in July (0.96%) and August (1.40%), and the upward trajectory it has been on in recent months, this COLA adjustment for 2021 may be in the 1.3% range.

Actual costs of living for retirees – or really for anyone – are going to increase far faster, depending on where they live, how they live, and where they spend much of their money. Even if the actual cost of living increases by only 1 percentage point faster than the annual COLA every year, after 10 years, 20 years, or 30 years, you’re talking about a serious deterioration in purchasing power of the Social Security payments. Inflation will eat more than retirees’ lunch.

Efforts to make inflation even more pernicious.

There have been discussions underway for shifting the COLAs from CPI-W to a chain-type price index because they run lower than CPI-W, and therefore in small increments every year, inflation would eat even more into the purchasing power of the Social Security payments.

Someone might be barely able to squeak by on Social Security, and use their savings – if they even have any – to supplement their budget. But each year, this gets harder, and this retiree is going to have to cut back, and cut back, and cut back year after year…. Every time this shift to a chain-type index for COLAs comes up in Congress, there should be a deafening hue and cry from everybody, young and old, because it would weaken Social Security as a safety net.

So, Social Security will be there for you, but…

You can rely on the Social Security payments. But they will lose purchasing power. The purchasing power of the payments will diminish every year, year after year, because the COLAs are not enough to cover the actual increases in the cost of living.

This is just a simple fact, and it’s not an accident, it’s purposefully built into the system. And this decline in purchasing power might shave 20% or 30% off your standard of living over the first 20 years of retirement. If it was tough to live on Social Security early on, it will be brutal after 20 years. And people need to add this into their calculations.

Hypothetical depletion of the Trust Fund.

If demographics shift in the wrong direction, and if interest rate repression continues, the Trust Fund will eventually pay out more every year than it receives from contributions and interest income, and the balance will begin to decline. And if no adjustments to contributions or payouts are made, and if demographic shifts continue, at some point, the Trust Fund will be depleted. The Trustees estimate that the Trust Fund will be depleted in 2034 unless some changes are made.

Depletion of the Trust Fund doesn’t mean that Social Security will collapse or will be “broke” or whatever. It simply means either that workers will have to pay in a little more, or benefits will get cut, or both. Social Security has been fixed before. Raising the maximum amount of earnings subject to Social Security tax would be one way of doing it, and has been done before. And there are other ways. These adjustments will be made – as they have been in the past – well before the depletion date.

The story of the man who told me that Social Security would collapse before he could ever draw on it.

Over the decades, I have heard many predictions about the implosion of Social Security. But here is the one I never forgot because I was at an impressionable age. When I was a senior in high school, the dad of my sweetheart told me that Social Security was a “scam” and that it would blow up before he could ever use it. He was a CPA and had an accounting and tax firm. He passed away a few years ago, after having collected Social Security every month during his retirement. And now his wife is collecting his Social Security survivor benefits. Social security outlived him, and it’s going to outlive me too.

But Social Security was never intended to provide adequate retirement on its own. My solution is to put money aside while working, and work as long as possible – way past retirement age, especially if you have something interesting to do. Look at all these old politicians: They’re all fired up, they’re having a blast, and they’re not about to let go of that much fun, nor of the income from it, unless someone kicks them out. And I too intend to do that – keep working being fired up and having a blast at my evil WOLF STREET media mogul empire until my brain freezes over.

As after the last crisis, fueled by ultra-cheap money, they’re taking financialization of the housing market to the next level. Read… The Big Boys Are Back: Financializing Single-Family Houses

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Politicans have few term limits, great healthcare benefits paid for by the tax payers and a system where it is very hard to overthrow incumbents. They feel no obligation to ensure citizens can depend on income deducted from their earnings for their entire working lives.

They call your own deferred income through Social Security “entitlements”.

The sheeple parrot it like the gospel.

Entitlement…..absolutely…..I’m ENTITLED to what my employer and I gave the US Federal Government to hold and invest IN GOOD FAITH of our deductions. That’s a plain, simple, rational and logical statement

The idea is not that your money (or that of your generation) is saved and then paid back out to you. The idea is more that current workers support retirees, and when they retire, they are supported in turn by the workers who will come after them.

Yes. Except there is this $2.81 trillion trust fund, where workers in past years paid more than retirees in those years drew, and the accumulated surplus became the trust fund, and now those workers that are retiring, or are approaching retirement over the next few years, are the ones whose contributions fed the trust fund.

Someone needs to explain to me how it is not a retirement plan, when police, teachers, etc are allowed to skip paying for it and instead contribute to their own retirement plan.

Not to worry, Wolf, We the people, know how to deal with surpluses.

We’ve put those things down before, and by God, if we have to, we will do it again. Read my lips, No more surpluses.

MarMar is EXACTLY right. But that needs further explanation!

There is this extremely widespread illusion that the trust fund is paying out old money collected years ago, to support SS of present recipients.

Well, yes, that’s the illusion. But when that money comes out of that “trust fund,” which is money supposedly collected years ago–what actually happens is that the money deducted from the trust fund — comes from everyone’s CURRENT taxes. That is from where money from the trust fund magically appears in the present. It’s the only place it could possibly come from.

So current SS benefits are paid for by a combination of recently collected 14% payroll tax, then any difference is made up in effect by the trust fund money taken out of CURRENT income taxes, not past money. That’s the way it always has been and always will be.

Fortunately, in the past, trust money wasn’t stashed under a mattress, or in a golden “lockbox” with a key.

Ralph Hiesey,

Seems like you got yourself tangled up a little. In nearly every year going back to 2009, more money was collected via payroll deductions and earned from interest income than was paid out. Hence, there was a surplus (more taken in than paid out) in just about every year since 2009. This surplus was added to the Trust Fund. That’s why the Trust Fund grew. But money is fungible — meaning that once money is in a particular bucket it’s indistinguishable from other money in that bucket, and it’s irrelevant – and impossible to tell – if the money that was paid out was freshly added to the bucket or was old money that has been in the bucket for years. Look at your checking account. Works the same way.

Wolf

I’ll try again with a different approach- I hope not too long..

This is an issue into which which it is extraordinarily easy to become entangled. This came from my Stanford college economics course in 1962. Hopefully I remembered it right.

The main point is that during each separate month the gov’t must divert a portion the economy’s goods/services output from present workers to SS recipients in that SAME month. They cannot say we diverted that amount ten years ago, so now we can send it to you. Goods/services are perishable, so to balance the economy the value that is diverted and distributed must be done at the same time from present workers to present recipients.

The way goods are diverted is by collecting a tax in that same month in some form in combination of payroll tax and income tax. That amount is distributed by writing SS recipients checks for the that same amount each month. If the tax numbers do not match the SS distribution that month there would be either a shortage of goods, or an unsold surplus left in the economy.

Bottom line is that taxes and disbursements must balance each month. The Trust Fund just keeps track of the surplus or deficit that month–but doesn’t have any other effect except it directs a trickle of interest each month to go from general tax fund to the Trust fund.

So money collected way ahead of time can’t help. It will make the fund go up, but no matter how it’s done, tax from somewhere (payroll +/- income tax) must equal SS disbursements in each month — or the economy will get badly messed up.

The day the trust fund goes to zero, it could even go negative except for a minor point that this would be illegal. No one but the accountants would know. No taxes would change .

I much prefer the solution of raising the income level upon which payroll tax is collected above $133K. It’s a super regressive tax that income above $133K does not now touch.

It seems you’re describing my checking account. That’s how money works. Everything is just a debt or credit. We’ve gotten comfortable with that long ago, except when it relates to Social Security? Somehow when it comes to Social Security, we want to see boxes full of $100 bills with names on the boxes?

TheRealMRDyno,

It’s not considered a retirement plan, because, originally it was designed to prevent people who did successfully live a long time and could no longer work from being destitute. It wasn’t expected to make up a significant part of a person’s life.

As for the local city and sometimes state pensions, I’ll pass. Calipers (the California plan) is going to be devastated just like Detroit’s was. Those local pensions are much more risky, although, realistically the Fed might have to cover those who had failed local pensions. If that happens though, the number of failed local pension systems will skyrocket, although work from home, could cause enough people to move to destroy many as well.

As for protecting social security, they need to remove the cap from max income for social security altogether. Treat all income the same (I.e. Capital gains would just be income). Get rid of local and state systems like calipers and switch to paying retirees an amount relative to where their income used to be. So if income level wise you used to be in the 55% percentile, you would make maybe 50% of that (in then present dollars, once you’ve elderly you should have less expenses) from social security (there would be additional considerations as well). You would also automatically get food stamps and certain other benefits.

The entire healthcare system is a disaster and needs to be fixed. Food stamps rather than being a check for groceries, could be a agency that buys up for directly from farmers, pays to have it processed and delivered (possibly to your house in certain situations, otherwise you would have to pick it up at places that are managed by the city). As for the food provided it would a system that gives rations of essentials and then let’s you get choose with a point system and other mechanisms what you get. You would end up with assortment of staples like rice, bread, wheat, eggs, ready to cook mixes, and whatever fruits and vegetables the agency gets a good price on. As well as some bakery and premade items.

Most students back at my high school (late 2000’s including before 2008 recession) thought social security and other pensions won’t be there for them. Beyond how social security itself works, they thought America would be too poor in the future, because, the older generations would looot everything. And that there simply wouldn’t be any money left (both many democrats and most Republicans thought this).

enough said – but you’re not close

IT’S SUPPOSED TO BE BASED ON INCOME for lifetime + COI(which govt is screwwing us on)

Actual costs of living for retirees – or really for anyone – are going to increase far faster

ie DEVALUATION(ie buying power of almighty $dollar) are going to price out most retirees soon enough

I’ve told my wife that soon we’re gonna price out most of our retirees currently renting our units – ie thru RENT INCREASES

so sorry – but I didn’t create system – just living by it

you only have to pay for 10 years – but given you live long enough – you can collect more than you’ve paid :)

@alku you are thinking of Medicare where you can get a full benefit for 10 Years of work.

With social security unless you become disabled your benefit would be prorated down based on 10 years of work instead of 35 years which is needed for a full benefit.

Your monthly SS check would be mighty small if you only paid in for ten years.

I paid into the system from 68 till 2008 so 40 years

I hope to live awhile longer to get at least some of it back

@Dave

I was referring to 40 credits you need to become eligible: max 4 credits a year / ~ 6K yearly income.

How many government employees get automatic and elevated bumps every year?

In IL, 3% every year for pensioners. That doubles their pension in just over twenty years. Retiring at 55, and bringing in during retirement much more than you ever made working.

That’s because they have unions. Something more workers might want to consider.

There is no free lunch, someone, someday will have to pay for this.

They have unions, they vote, and their employer (the government) doesn’t have to make a profit or even balance the budget.

The unions entered into retirement agreements knowing full well that the money is not there. The government officials on the other side of the table figured they will be dead when it all collapses. Both sides are criminals. So we need more criminals fleecing the taxpayers (unions)???

The problems facing SS were known long ago but the worthless politicians have chosen over and over again not to address them. America has a history of elect ing losers to manage the country. I’m speaking specifically about Congress.

‘America has a history of elect ing losers to manage the country’

Wonder Why?

If every voter, discerns clearly between the those lawmakers who vote more for PRIVATE interest over the interest of the PUBLIC and vote accordingly, we will have more sensible lawmakers in favor of what’s good for the general interest, NOT the private interest like – Military industrial complex, Medical industrial complex including Big Pharma, etc. It is all there, a public record of their voting hx, online!

Some how, most voters are easily ‘brainwashed’ by both WARFARE and WELFARE parties and distracted by political ideology ( Lib/Cons, Capitalism vs Socialism)

Below the Belt issues like abortion, birth control. This happens prior to EVERY election.The latter have NOTHING to do with solutions needed for our (& furure generations) problems like ‘meaningful’ education or jobs for now and for the future. Packing SCOTUS with judges favoring their ideology, right or wrong is now more important than the needed 2nd stimulus for the bottom 90%!

Blind ideological slavery (polarization) has triumphed over critical thinking, which is hard to graduate in, for many!

WE have found the enemy. Look in the mirror!

In 1981 then president Regan assembled a Blue Ribbon commission headed by none other than Alan Greenspan to address Social Security shortfalls. Their report and conclusions out in 1983 amounted to an entire (baby boom) generation over – paying in advance their payroll withholding taxes along with increases to age eligibility requirements. It was sold to us as a fix desperately needed because so many of us were fixing to retire all at once.

Also Regan for the first time ever, started taxing Social Security benefits which continues until today. Do you remember Al Gore’s Social Security lockbox? It was full of non marketable securities (I.O.U.’s). These were quickly used in just about every Administrations general fund as illegal as it still remains today.

And these are just a couple of the shenanigans our elected and non – elected representative’s have played regarding Social Security. So as you can see, they have tinkered with Social Security much. It original intent was far from the all inclusive club it is today. The historic origins of Social Security is a very informative read.

As with any Ponzi scheme, those taking cash out earlier will fare better than those requesting cash when contributions fall below disbursements.

This ”sheeple” doesn’t parrot that line IP,

I been saying for many years that the best way to ensure the SS and Medicare program is to make them the ONLY tax payer supported retirement and medical services delivery programs.

When every elected politician, every single one of them, PLUS every appointed or hired guv mint employee at every level of guv mint has to rely on SS and Medicare, you can bet your bottom dollar those programs will be healthy for eva…

Anything else will eventually cause the entire global wealth now delineated in digital dollars, to CONTINUE to be sucked into the criminal and corrupt crony capitalism that we now see growing all around us.

SO: 1st, Term Limits on all guv mint employees, elected and appointed; 2nd, SS and Medicare ONLY for all.

There, fixed it!

AMEN!!!

I’ve been saying the same for 30+ years.

The US is a democracy, if the demos ie ‘we the people’ vote to share out the wealth of the country fairly, then it must be shared out fairly.

Indeed. The Congress can allocate funds over and above those collected through payroll taxes, at any time and in any amount. The idea that SS will go broke is just another right wing lie. Let’s start with transferring some of that corporate welfare masquerading as “ Defense “ expenditures into SS and give everyone receiving retirement and disability benefits a substantial raise.

@ KK

‘we the people’ vote to share out the wealth of the country fairly’

Yeh. Wonderful concept!

See my comments/reply to Mario above. Thank you

No, the US is a Republic. We elect representatives that supposedly have our interests at heart. Sadly, that stopped being true rather a long time ago.

Income taxes are also “entitlements” to politicians from taxpayers, working within a VOLUNTARY income tax filing system.

“The U.S. tax code operates on a system of voluntary compliance. Some taxpayers have used the voluntary nature of the tax system to support their claims that they don’t have to pay tax at all. However, it isn’t the payment of the tax itself that is voluntary. Rather, it’s the manner in which people submit their own taxes.”

Copied from Turbotax’s website.

No endorsement of them.

Wolf describes a disgusting and pathetic system. When will pathetic, sick Americans ever outgrow their ignorant right wing ways?

The politicians make SS look like “Entitlements” because they spent the actual fund and the payments are coming directly from each current year’s tax revenue. Their promises to spend sound great at election time, especially if no one bothers to ask where the money is coming from.

I would think the nation would be in depression this year if not for Social Security payments. There would be a heck of a lot of older forgotten starving people like in the 30s.

Most people can’t manage their money through life or can get wiped out. That’s just the way it is. A monthly check for most is essential.

Given we are about to enter a Supreme Court Nominee battle it’s worthwhile to review Fleming v Nestor. We might like to think it’s

“our money” but that has not been upheld by the SC

” In this 1960 Supreme Court decision Nestor’s denial of benefits was upheld even though he had contributed to the program for 19 years and was already receiving benefits. Under a 1954 law, Social Security benefits were denied to persons deported for, among other things, having been a member of the Communist party. Accordingly, Mr. Nestor’s benefits were terminated. He appealed the termination arguing, among other claims, that promised Social Security benefits were a contract and that Congress could not renege on that contract. In its ruling, the Court rejected this argument and established the principle that entitlement to Social Security benefits is not contractual right.”

https://www.ssa.gov/history/nestor.html

That’s one of the reasons H1-B visa holders are so popular with corporations. The corporations do not need to pay the matching Social Security tax, making them 6.2% cheaper.

Do not forget someone coming here say at age 40 gets the same medicre as some starting work at age 20,

Spouses who never work get medicare and soc sec when the spouse dies

And the real inflation rate the past 30 years has been 5% points higher than the govt uses.

They are ENTITLED to it because they paid into it! :) IT. IS. OUR. OWN. $!

If it weren’t for SS, I would have ended up in a state run orphanage after my father’s death when I was 7 years old. I hold SS near and dear to my heart.

Why let the GOP rip Grandma’s $600 check from her hands? Why?

We COULD make SS even better but that would require compassionate human beings in places of power within our government.

It’s the most successful program in US history. Embrace it and make it even better. We are all brainwashed to think the USA can’t do things other western industrialized nations do, like provide free health care and college to the citizens.

It’s time for Americans to wake up and demand the society we deserve. Keep up the good work, Wolf!

You live in a van down by the river.

Why should we listen to your arguments that are used to demean ?

By the way, the argument that SS = welfare is confused

and incoherent .

Lots of Van people nowadays Look on youtube you will see that their numbers are exploding Coming to a Kroger’s parking lot near you Thanks FED

Well written, and I completely agree. We’ve mastered much of the physical world, enough to provide that and more. It’s the Capital folks that need to accept lower IRRs though. I don’t see that happening without a fight.

if social security is so good, why am I forced to participate?

Taking my income by force and putting it into a program I want no part of is Un-American.

nodecentrepublicansleft, it’s not true that the only options were Social security or state run orphanage. That’s like saying, if not for the government lording over us, we’d all be hunter/gatherers

Oh that’s why we are 27 trillion in debt, not including unfunded liabilities..

Pacifica,

No. You got this mixed up. Social Security is a LENDER to the US government. That Trust Fund is the amount of money Social Security has LENT to the US government, just like me or anyone else: when we buy Treasury securities, we lend to the US government, we don’t contribute to the US debt.

The money LENT that will be never paid back

BS. It’s paid back every single time a Treasury security matures, which is the pre-set date when the US Treasury Department redeems it by paying the holder face value. I hold some Treasury securities and that’s how it has been working from day one, every single time. Never once failed.

Wolf is correct, it will be paid back but the value of what you get back will be greatly diminished, even Wolf would have to concede that fact.

libertarian57,

In terms of semantics: I wouldn’t call it “value” because that’s expressed as “face value.” Your $1,000 bond will be paid back with $1,000. But you’re talking about “purchasing power.” And purchasing power of anything gets crushed by inflation. A big theme here.

And that’s OK-ish if the yield more than compensates you for the loss of purchasing power. But that’s NOT happening. We are in a period of “financial repression,” as it’s called.

Yes and I certainly don’t trust the government, or at least the one we have

By buying Treasuries you make it possible for the government to go into debt. If you make something possible, you contribute to it.

Just my logic.

Precisely, Wolf. But this argument, that the Trust Fund money is not there, is made by supposedly reputable blogs. The counter argument would be – well, that must come as a shock to all the US Treasury holders, then.

Thanks, Wolf for clearing this misperception, repeated again & again!

Part of that ‘why we are 27 trillion in debt’ is due to USA trying to global policeman and maintaining hegemony over the rest of the world lime maintaining over 600 bases, world wide.

Spending 2-3 Trillions in meaningless wars in ME since 2003, creating millions refugees and over 6000 US soldiers dead! For what? Where is the public outrage? THINK!

Except that the number wasted (i.e. transferred from the Treasury to war profiteers) is currently estimated at $5.2T. I wonder how many posters raging at government waste, spending & deficits actually supported these invasions?

You forgot to mention a big contributor to potential Social Security insolvency.

The upper income thresh hold subject to tax has not been raised for a long time by deliberate policy choice by or governing elites, so as to accomplish their objective to undermine and eventually destroy Social Security.

This – never raising the upper income thresh hold – was never intended by the founders of Social Security. The founders of Social Security intended the upper income subject to tax be raised at least at the same rate as inflation. And by inflation, not the fake inflation the Fed and government uses. But instead, the real inflation rate as shown by stocks, investments, housing, assets, etc.

Real, actual, inflation that affects the cost of living.

If the upper income was raised based as always intended, by the rate real actual inflation, you might be able to find a Social Security funding short fall maybe in the next 200 or 300 or 400 years. Good luck with that.

Remember…the ratio of Social Security beneficiaries to payees is and always has been about 1-1. Contrary to anything else anyone claims.

time is YESTERDAY TO ELIMINATE THIS

pay 100% ssi taxes on 100% income

then MEANS TEST(based on today) SSI benefits

if you make over $150,000 in retirement do you REALLY NEED SSI-NOOOOO

You definitely do NOT need it

Then SS becomes a welfare program, don’t we have enough forced wealth transfer?

Most of the “forced wealth transfer” is upwards. Interesting how the huge suite of tax cuts targeted at the wealthy and owners of assets (the corporate tax structure, capital gains, real estate, etc) are not called “welfare programs”. A bailout of the airline industry or the banks is called a “bailout”.

When there is an attempt to restructure healthcare costs through Medicare for all or make Social Security contributions more equitable, suddently it is “welfare program” and a “forced wealth transfer”.

Social Security taxes have been eliminated this year by fiat. If this continues next year, it will become a welfare program.

Apple,

Not eliminated. DEFERRED. Another deferral program, like forbearance and all the others. They’ll have to be paid back next year. That’s why most companies said forget it, we’re not following this crap policy.

Deferring the payroll taxes helps how?

The people that need the help are unemployed! Those are the people who can’t pay their rent or utilities.

I think that deferral is two things: first, a symbolic bit of “help” that has little effect but can be touted and, second, another attack on social security and medicare.

SS sooner or later will become one of the these unsavory things:

1. Turn into a welfare program.

2. Number of people who contribute keeps magically increasing to keep up with number of retirees who draw from the program.

Base of the pyramid needs to keep ever expanding to keep the scheme going. There is a famous term for such a setup.

3. Real value of benefits keeps shrinking. BLS is on it with its bogus inflation numbers and Fed is on it with its active devaluation of currency.

4. One or more of the above.

Joe Saba

I agree with your premise, but when my Dad was forced to take SSDI (Parkinsons Disease) from age 58 until 65, he protested, said he didn’t need the $$$ (he was a doctor and had decent savings). We kids told him to take it because his private disability insurance required it AND we joked we (kids) would not get our SS except through his inheritance.

Well after reading Wolf’s excellent article, we kids WILL get SS, but looks like it will be beaten up by inflation, so I am glad my Pa took his benefit.

My Pa ended up needing most of his savings for a hospice-like private living facility toward the end of his life. What he collected in SSDI was a drop in the bucket of those expenses….BUT…..as others have stated – you paid it in, so you should get it out, regardless of your income level. It is not meant to be wealth re-distribution, it is meant to be a forced savings account of sorts.

Since people are forced to contribute, they are entitled to a benefit. It’s not about need, it’s about a level playing field, fairness counts. People who don’t need it can donate it to their favorite causes.

I do agree the SS tax should be on every dollar earned. That way they can lower the tax rate for everybody.

I’ve contributed into SS rom 1959 (yes, since then) to 2019 (last year I had wages from consulting. That’s a long time…..and I have now been collecting from my DEPOSITS since 2012.

It is not an entitlement for us guys, it’s getting back what we put into the system. If we collect more than what we put in, good for us.

> “real inflation rate as shown by stocks, investments, housing, assets, etc.”

Is there an indicator for that? Would love to know.

All we have is skewed numbers from BLS and Fed.

You left out the number one indicator Precious Metals Funny how that happens Do you work for the FED?

One must specify the ‘TIME FRAME’ ( 10yr-20yr-30yr++) re REAL ‘Inflation rate’ for each asset class including CASH, Bonds, Stocks and PMetals in the past. Otherwise it is meaningless!

Remember No one lives for ever!

The upper income limit does go up by the same amount average wages go up.

that sounds fair. who do i vote for to ensure this policy remains in place?

Ummm… no. The wage threshold does get adjusted annually for inflation.

Perhaps you are confusing the Social Security income threshold with the threshold of when social security disbursements start being subject to income tax. That threshold has indeed not been raised in decades, thus causing more and more people’s Social Security payments to to subject to IRS income tax as time goes by. But this has nothing to do with undermining the viability of Social Security. It’s just a way to shaft more and more Social Secure recipients every year.

Just refill the HP cartridges and print some more money. Am I missing something here?!?!

they don’t use outdated HP Printers

just computers and iPhones

Yes. It is another industry that we are destroying here with the Internet. Think of all those poor money printers, in the printing presses, and the people who work at them.

Not to mention the entire supply chain supporting them. Those are people too, you know. what’s next? Going after the insurance industry. Is an AI going to replace the telephone workers that tells you your insurance is denying benefits, and that’s putting that cooperator out of a job. How cruel.

Have you no compassion.

Why print when you can just type it in? Less dead trees.

Not a good idea. Have you seen how much those cartridges cost? ;-) The govt would go even more bankruptier than it already is.

I think they should switch to Epson ecoTank :-)

The incoherent rage in America is money in the bank for plutocrats. Say what you will about America, you can absolutely count on the fact that 95% of Americans will never catch on to the class war that they have so decisively lost.

soon to be 99.9%

Got that right. Living in trailer parks in Mississippi complaining about socialism. Never underestimate the stupidity of the American people. Dumber than dirt.

Yes, and privatizing education will keep it that way.

Dan, you forgot the sarcasm tag.

Actually the cost to educate a kid in public school here in BC Canada, has hit about 12K a year for about 160 days a year teaching or attendance anyway.

My brother was in the returns line at Costco

with a teenager in front. The clerk said, “OK sign here for refund”

No could do. The teachers have opted out of ‘cursive’, aka ‘writing’ and after spending at least a hundred grand on educating this kid he can’t sign his name. So I guess it’s back to ‘his mark’ (here gov docs for pensions still have that option) like the days before public ed.

Don’t even ask about history or geography.

Here in this city of over 100K a kid has to be bussed to take physics. It’s like he wanted to take Mandarin or something.

One high school here where a friend is a TA told me the staff has quietly, verbally. been told to stop recording ‘lates’

So the teens aren’t learning about punctuality either.

There are lot of dedicated teachers in the system but the system works against them.

There is no accountability for results because the deadwood is protected by the union.

I say give industry a chance to see what it can do for that amount. I don’t see how they do worse.

BTW: ‘the dumber than dirt’ are products of public education, unless they weren’t educated at all.

When I read “I intend to do that too” I was hoping it meant you were going to “kick them out”.

I sincerely believe every gov’t employee (from the President on down, to include judges, Senators, etc.) should have a mandatory retirement date, and it should not exceed 70 years of age. I cannot believe the best and brightest, most capable people to lead this nation are 20+ years older than me when I’m planning on retiring in the near future.

In the 1970’s it was all about not trusting anyone over 30. Funny how that changed when they got into office.

The most disgusting thing I ever saw in congress was wheeling in almost dead senators to vote. It reminded me of the old Soviet Politburo, but worse.

You mean like John McCain

You see, when you name names, is when commentary goes from being general to being overtly politicized.

And Ted Kennedy, and Robert Byrd….

At least they are not digging up the graves of dead politicians and dragging in coffins, although I wouldn’t put it past them to do that.

Great analysis of a problem many people only have a vague understanding of. Its obvious the Fed has repressed interest rates for some time and plans to continue to do so into the future. This has fueled a huge inflation in stock and bond prices but not helped the Social Security recipients. I think it would only be fair if the Fed transferred at least one of the trillions of dollars of treasury bonds backed up on their balance sheet to the Social Security Administration to offset the damage they’ve done.

Your brain freezes over, wolf? Are you planning to go into cryo sleep so you have a chance to be reanimated as the ultimate debt slave in our cyberpunk future?

From Propublica in 2018:

If You’re Over 50, Chances Are the Decision to Leave a Job Won’t be Yours

“ProPublica and the Urban Institute, a Washington think tank, analyzed data from the Health and Retirement Study, or HRS, the premier source of quantitative information about aging in America. Since 1992, the study has followed a nationally representative sample of about 20,000 people from the time they turn 50 through the rest of their lives.

Through 2016, our analysis found that between the time older workers enter the study and when they leave paid employment, 56 percent are laid off at least once or leave jobs under such financially damaging circumstances that it’s likely they were pushed out rather than choosing to go voluntarily.

Only one in 10 of these workers ever again earns as much as they did before their employment setbacks, our analysis showed. Even years afterward, the household incomes of over half of those who experience such work disruptions remain substantially below those of workers who don’t.”

Yes, ageism is a huge problem, especially in tech, and elsewhere too.

But people can start their own thing and stay active and make some money — even if it’s less money than they made at their peak earnings period. This could be consulting, or starting their own business, or learning a trade and using it, or turning a hobby into a business or whatever…. Even a part-time job somewhere is helpful in keeping retirees active and supplementing income. not everyone can pull it off, but it’s worth a try, and it’s very rewarding if it works out.

Wolf

Great article pulling back some of the myths of Social Security and also great comments RE reinventing yourself after 50. I retired (pushed out) from the desk job at 50 and became a FT musician. Not so much a hobbybtgat pays well, but sooo much better for the mind and soul. ;-)

With respect, these are all great personal virtues but when only 1 in 10 is regaining their previous earning power it’s a serious policy failure.

Advice about this would make a great article too!

One of the following must occur:

1. Social Security benefits rise with

the pace of actual, true inflation.

2. Urban rents drop dramatically.

3. More tents get pitched on the sidewalk,

so grandma has a place to stay.

Society has chosen #3, apparently.

Instead of working forever, you can also choose to quit and do the things you want to do while you are still relatively young and healthy. Enjoy life while you still can. What is the point of throwing your life away just to be financially secure at age 95? (which you will probably never reach anyway).

Your healthy years are worth much more than your old age years in a carehome (if you are lucky – many will have to live on the streets the way things are heading now).

There is a point to be made to just set your life end-date at (say) 75 and make sure you enjoy the present to the full. If there is still money left after that, great, that gives you a few bonus years. After that, just exit happy on your own terms after a life lived in full.

However, if you cut all unnecessary crap (the stuff that doesn’t really make you happy) out of your life, you will save tons of money and feel more freedom. Reject consumerism, live minimalist. In that case you may even sit it out till your natural expiry date.

YuShan

Yes, most people live there lives backwards

re: “However, if you cut all unnecessary crap (the stuff that doesn’t really make you happy) out of your life, you will save tons of money and feel more freedom.”

Yep, was thinking similarly just this morning: life is (at least) as much about shedding the unimportant as acquiring more stuff. Or, as a famous philosopher once said “Life is what happens when you are busy making other plans.”

That was John Lennon, a musician. Unfortunately he never got close to his use-by date. A lesson for us all.

From my collection:

“Sometimes life hits you in the head with a brick. Don’t lose faith.” – Steve Jobs

“Open your eyes, look within. Are you satisfied with the life you’re living?” – Bob Marley

“Life is a lively process of becoming.” – Douglas MacArthur

“We are here to add what we can to life, not to get what we can from life.” – William Osler

Let me add one:

“Everyone has a plan, until they get punched in the mouth.” -Philosopher Mike Tyson

YuShan:

I agree completely and have lived that way. I retired several times when I was in my 20’s. I lived in Omaha and used to quit whatever job I had and cruise around the country on my Triumph. I would head back to Omaha when I started to run low on money or the weather got crappy – which ever came first.

People forget that when you get old, there are many things that are much more difficult to do. Just getting from gate to gate in an airport is not much fun in your 70’s.

Social Security IS a pyramid scheme, BUT if we ever run out of working contributors at the base of that pyramid we will have much bigger problems than how to fund retirement. Like the extinction of humanity or the end of American sovereignty.

No, the problem is that Congress plundered money from the trust fund long ago to fund war and general purpose outlays – and I fear that if this half-assed M.M.T. experiment we are currently conducting goes sideways, the United States government will selectively default on its obligation to make it whole again.

Harvey Cotton,

“…the problem is that Congress plundered money from the trust fund long ago..”

You need to quit mindlessly regurgitating this ignorant BS. The Trust Fund invested in Treasury securities just like bond mutual funds invest in Treasury securities or as I invest in Treasury securities. It’s the most conservative investment there is. No one plundered anything. But if the fund is privatized, Wall Street will certainly plunder it with fees and as dumping ground for its toxic crap.

“My solution is to put money aside while working, and work as long as possible – way past retirement age, especially if you have something interesting to do.”

Great advice and which I echo. Retirement is a great time to try out interesting things, many of which provide a financial return. And it can be fun! My wife and I opened a jam business (which failed) and now are in a book business (which does okay). But we’re doing it together, which is best of all.

My wife and I are building a resort on the Med coast in SW Turkey It’s a good thing my income stream presently is in Dollars and Euros since the Lira has lost a lot of value recently My Precious Metals stack hasn’t been looking a lot better lately

Resident Gold bug

A few years ago my wife and I drove from Izmer to Marmaris. Leaving Izmer, we had to pick between the big interior highway and the little 1.5 lane road carved into the coastline. We picked the little road, and that was the best drive ever. It was a few days before summer season, and there is a hard line on that it seems, because there was almost zero people around. Somewhere on that trip is a big power plant, and near that a pretty big beach, which had folding chairs out, 3-4 deep, as far as you could see in both directions – with exactly zero people. I took a video of that, it is like a science fiction movie. Anyway, that is one of the very few places I would ever visit a second time, seems like a great place for your venture.

We do that drive all the time as we live near Marmaris and my wife’s mother lives just north of Izmir Their are a lot of geothermal plants along that route and a couple soft coal ones as well Glad you enjoyed it We love living here after the outrageous cost of living where we were before in East Hampton , New York

The U.S. Government has the final say on the printing of dollars.

If the economy isn’t resource-constrained, the government can always pay for Social Security or anything else, and to everyone’s collective benefit as long as it’s keen on stopping what inflation may result with the arsenal of tools like taxes and higher interest rates at its disposal.

It’s a matter of choice whether Social Security gets funded, not “availability of tax revenue” or your uncle’s doubts about “where the money’s going to come from.”

Taxes don’t pay for government spending the way a business pays for its operations out of sales. If spending cuts are off the table then taxes reduce the consumption spending by the people we tax and raise it by the people tax is redirected to.

1) Suppose the gov click 1,200 check financing it by taxing the rich. Wall street liberal speculators are going to like it.

2) Suppose US gov 1,200 check will be financed by taxing the rich & the middle class, taxing 50M out of 160M in the civilian labor force . Most American will vote for it.

3) Suppose the 1,200 check will be financed with the inflation tax.

The top Pareto snake, the owners of the 80% and the poor, who vote for free money, but will be robbed by inflation, will like it today, but not tomorrow.

4) US gov debt can be financed by the shrinking 160M civilian labor force and 100Y bonds paying higher interest rate.

5) Those who are born today, entering the labor force in 2040 – 2050,

will replace the aging baby boomers and industrial jobs coming back from China. There will be a lot of demand for their hands & brains. They will

be able to buy plenty of cannibalized assets & RE coming from the dying boomers.

6) During 2019 178M out of 160M civilian labor force paid SS payroll taxes.

Don’t plan on many jobs coming back from China. The US dollar buys 5X as much in lifestyle there. Any company coming back to the US will be buried by labor and regulatory costs, and will have to charge a lot more for the products. People won’t buy them. The company will be bankrupt in 90 days. A manufacturing process that is totally automated might survive, but will provide damn few jobs. Globalization is the great equalizer. Poor countries with low labor costs benefit the most in the increase in standard of living. Countries at the other end of the spectrum pay the price of low cost goods with loss of jobs. It’s an averaging process.

You did NOT pay into Social Security. It’s a pay as you go program. Always has been. Same as Medicare.

Capthank,

Sorry to hear. Where is your health insurance going to come from when you’re 75 or 85? Good luck finding private insurance and paying the premiums. And good luck paying for healthcare out of your own pocket when you get older. I wish you a totally healthy illness-free life in old age, because that’s what you will need.

It’s possible, though. My paternal grandmother had such a life. Never got sick, never went to the hospital, and died in her sleep at age 93. But not many people can pull this off.

No not many can I had nearly perfect health until around age 60 when I got Lyme disease and now auto immune disease which may be related Had a routine colonoscopy and ended up in the hospital with Acute kidney injury Getting old is rough let me tell you Your grandma was very lucky

I reached 65 this year….and for the first time I am starting to really feel my age…getting up with some aches and pains in my back, etc. On the other hand, I still exercise regularly, including high intensity interval training three times a week and steady state cardio other days. The intensity training has me panting on the floor after twenty minutes but I aced my echo cardio stress test the other week and my only medication is a statin as a preventative more than anything else. Its tough growing old but you can slow down the aging process. I am putting off getting my SS until 70 and already to help make ends meet I am learning to sell covered calls for extra case, and will continue practicing my profession on a part time basis to keep me going. No golf for me…not interested.

en.wikipedia.org/wiki/Flemming_v._Nestor

Flemming v. Nestor, 363 U.S. 603 (1960), was a United States Supreme Court case in which the Court upheld the constitutionality of Section 1104 of the 1935 Social Security Act.In this Section, Congress reserved to itself the power to amend and revise the schedule of benefits.

I’ve been looking into SS for the last couple of years. It is an extremely complicated system. I thought you just decide whether to retire early at 62 or wait until full retirement, wrong. I can’t believe all the strategies involved in making the decision, I had no idea, I don’t think the average person does either.

The cpi calculation for the system is a complete ripoff and so is the taxation of benefits. Benefits are taxed for a couple with as little as $44K of income, disgusting.

If the govt was serious about creating inflation the SS system is the perfect vehicle, just give more money to those who will definitely spend it. Instead they will get deflation because the retired population is growing and getting poorer.

You pay into social security with “pre tax dollars” so you get taxed on those dollars when you take them back out. And your tax rate is the same as everyone else’s, which for a married couple making 44K per year, are pretty low.

Is the above not true? I could be wrong, I am no expert, but that’s how I thought it worked.

If it is true, it seems pretty fair to me and not something to complain about.

You’re thinking of a 401(K) distribution.

Social Security payments are just regular income – which some states tax as well.

The amount you contribute is taxed before getting deducted, so your portion is taxed twice. The employer portion is tax free to them, a deduction, but it is your deferred compensation. They are taxing your portion twice and the employer portion once. So it’s a double tax scam.

Thanks to Pres.Clinton for the tax on SS, which the base has not been adjusted for inflation since enacted.

That is not correct.

Petunia – I stand corrected. THIS IS UNBELIEVABLE BUT TRUE!!! Thank you for outing this out. I am now disgusted.

And if some entity enacts a wealth tax you will be taxed a third time on the same income. At least with a Ponzi you get a quoted rate of return. The US government just moves the goalpost around.

I am 64.5 and single. Did a lot of research on when to take benefit. Mathematically it’s a very complicated decision that only a person good at math or a computer can solve if you have additional income and start running into different tax rates.

There is also the issue of how you frame the problem. For example if you defer to 70 and live to 69 then you left money on the table and that can be taken into account value wise. So if you frame the problem one way taking the benefit at 62 the break even is 78 if I remember correctly and framing the problem another way the breakeven was about 90.

For me I took it at 62 mainly because I wanted to spend socialized money, before spending down personal assets. A long enough period of financial repression might mean I goofed up. I still don’t think I would be comfortable spending down most of my financial assets so I would have a bigger check at 70 based on a government promise.

I like using the free ORP (optimal retirement planning) on-line program which will figure draw down amounts for you and even determine at what age you should take social security to get maximum tax minimized income and which bucket spending should come from to minimize taxes.

Galbreath, the younger, has for years been advocating lowering the retirement age to reduce the supply of excess labor thereby increasing wages.

That has been done in Europe decades ago. Turns out, in practice, it’s a terrible idea for many reasons. And it is getting reversed bit by bit.

After Greece got into the EU and went on a monumental spending and very popular spending spree, they decreed about 140 occupations ‘arduous’ enabling retirement at 55. Examples: hair dresser, disc jockey.

For anyone who thinks Greek problems are the result of being beat up by Big Bad Germany, see ‘Boomerang’ by Michael Lewis.

Another factor on social security is it pays out differently percentage-wise on different income levels. If you are lower income, it is a good deal. It has been a few years since I did the calculations, but if I remember correctly) the factors are .85 at low income, .32 middle, and .15 upper income. Also, withholding is 6.45% but if you are self-employed, it doubles to 12.9%. So for an upper-income self employed person, S.S. is a poor choice. Lower-income it is a good deal.

Yeah, most people don’t understand (or even know about) the concept of Social Security’s “Bend Points”. Once you hit that second bend point it becomes a pretty lousy deal.

Ron of Ohio,

Payouts are also capped. This system wasn’t designed to provide Warren Buffett extra beer money. He hasn’t even retired yet. These two guys that run the empire are in their 90s and still at it… See what I mean? The system was designed to prevent people from sinking into abject poverty as they get old.

But there’s this weird dichotomy where on the one hand “it’s just money I paid into a forced savings program so I should get it all back with interest” and on the other hand “it’s not meant to help rich retirees, it was mean to prevent poverty in the elderly, so the returns are reduced for the wealthy”.

These two ideas are both invoked frequently and yet they are at odds.

Zantetsu,

It’s not a “forced savings program.” It’s a forced pension program. Huge difference.

All pension plans work on the same actuarial basis: that a lot of people die before or shortly after retirement, like my father, at 65.5 years, along with my mother, at the same time, along with their corporate pension. The pension plan saved a huge amount of money. Actuaries calculate these probabilities and base future payouts on the math that many people pay into the system but will die either before retirement or shortly thereafter, hence never getting “their money” back, while others live to be 108, and get double their money back.

‘many people pay into the system but will die either before retirement or shortly thereafter, hence never getting “their money”

I know lot of professionals who died before collecting their SS but some their heirs did, but NOT all.

With Covid 19 raging, it will ‘nip out’ many elderly, premarely in the years to come, I am afraid. I belong to that risk group but not worry excessively. Hope for the best and prepare for the worst!

There is a cap on paying in so it makes sense for there to be a cap on paying out.

Right, the max yearly SS tax liability is like $6k on the first $150k and you’re tax free after that so if you’re making 5m-25m you basically pay nothing. The income tax rate varies only from 12 to 35%. Workers pay for SS and medicare, millionaires and billionaires don’t.

@lenert

From 5m-25m you basically pay nothing

Yeah, but you also get nothing.

@ lenert:

You are somewhat incorrect with respect to Medicare. There is no cap on wages subject to Medicare.

Max – you don’t get not nothing – you get the max check like $3k a month. Sure it’s not material but even Milton Friedman cashed his checks.

Correct on medicare – too complicated for my simple brain – plus high income earners pay the supplemental ACA/medicaid expansion tax.

The number one source of income for most Americans in retirement is Social Security. The creation of the 401k destroyed pensions as a reliable retirement supplement for many. I propose eliminating 401ks and doubling Social Security benefits.

Then wall street locks you into these vehicles with their special 10% early withdrawal penalty.

Something to ponder. The money placed into SS was gold backed prior and worth more prior to 1971

Worth MUCH more indeed Back when gasoline was 25 cents a gallon and I earned over 3 dollars an hour as a high school kid Let that sink in a minute and you will understand how far our standard of living has collapsed Without all the debt we would be in big trouble

Comparing the price of gas to income is like the WORST possible metric you can think of. Can you please start choosing some other cost of living other than gasoline to focus on? Gas was relatively inexpensive back then because we were completely externalizing the costs of destroying the environment.

(and we still are).

OK whatever makes yo happy A slice of pizza was 10 cents and two and a half dollars today Even more extreme inflation than oil and no oil was cheap because we still had a gold backed dollar

Oil was cheap because it gushed way, way up in the air when a pool was struck, until you put a valve on it. Now we’re sucking it out of rocks or steaming it from sand goo. We used up the cheap oil.

The price of oil in 1970 was 3 to 4 $ a barrel.

By far the largest factor in breaking the buyers’ cartel was the Arab- Israeli wars, and the Arab embargo on oil to the US.

BY the time it was lifted, pricing power had transferred to the suppliers from the junkies.

Frederick, yes that’s better thank you. So you’re basically saying that minimum wage bought 30 slices of pizza back then. Today I’d say it’s more like 3 or 4. That *is* a big difference …

And by the way, the standard of living has ABSOLUTELY NOT collapsed. Life is so different now to the 1960s that it’s hard to even compare.

The phone in your pocket now would have cost billions of dollars in the 1960s. So compared to your 1960s self, you’re already a billionaire. Not to mention the vast improvement to so many consumer products that even the most meager income now buys a standard of living – purely from a material point of view – much better than in the 1960s.

Food is probably overall better now because we have tremendously more choices, organic became much more widespread, and people have learned to be alot more discriminating than they were back then.

Social interactions are probably much worse though, because of social media and the way people have shut off from the kinds of community contact that used to be commonplace (kids playing in the street, etc).

I’m not even talking about COVID, which is a special and temporary problem.

When I was a newly minted mechanical engineer in 1984 I got a job as an engineer at a portland aerospace supplier for $45,000 per year. I purchased a house for $70,000 and a brand new VW Gti for $7000. My sons friend graduated with the Same degree in 2014 and went to work in the same company in the same job in 2014, for which he was paid $60,000 The same house will now cost him $525,000 and the same car will cost him $27,000. Plus he has student loans to pay and I did not.

I don’t own a phone so that is irrelevant to me and yes, life sure was a lot better back then but you seem to have everything figured out so have a good day Saying that our food is superior today just shows how little you know

My experience was similar but a little different.

I was paid 30K in 1985 as a new BSEE in S. CA. My future wife also worked and was paid about 20K. We were able to squeeze into a small house in S.CA for 200K. 4X income. No student debt since I could work half-time at a $4.25 minimum wage job and pay the entire $1400/year UC tuition bill with an extra 3K for food/books/used car/bike maintenance ($300 used car). I was lucky enough to live at home for 3 years. I wouldn’t have been able to afford the $200/month to share a rental room on minimum wage. I moved out when I got an $8/hour engineering internship.

The new BSEE’s today are paid 80K and the exact same house is now 800K. Humanities entry-level jobs are starting at about 50K (BSRN Nurses, etc). 6X income to buy a house. A student cannot work a minimum wage job and pay the current 20K/year UC tuition bill so there is also student loan payments.

At $12/hour, a half-time job would earn about $12k/year

Due to housing/rent and college inflation, new grads today have a much tougher time surviving.

Unlike in the 70’s or 80’s, nobody can pay their entire college tuition with a minimum wage job anymore.

Seneca’s Cliff you’re an outlier. I highly doubt many people fresh out of school made that much in 1984.

Fredrick, it’s easy to bitch and moan about it, but if you really liked the lifestyle of the 1960’s so much, it’s still available to you now. Just don’t take advantage of any of our more modern conveniences. It will be hard since so many of our products have increased so much in value compared to then, but I’m sure that if you just bought the worst and least reliable of any item available today, you could approximate your 1960’s standard of living. You might start with denying yourself all medical treatments invented since the 1960’s. Follow it off by buying a car that gets 15 miles to the gallon and is virtually guaranteed to die before 100,000 miles. And stick to vinyl records, radio, a 19 inch TV, and don’t watch any streaming media.

And stop using Wolfstreet and all other internet.

3 bucks an hour for a high school kid? By my rough calc of when I was paying that .25 a gal (35 in Calgary) 3 bucks would be triple minimum in places that had one. Were you a teen welder or something?

Nope just a lumber yard worker in NYC suburb 2.95 was minimum wage in 68 and if I scrambled I could earn 5 to 10 dollars a day in tips

$2.95 was 2x’s minimum wage in 1968. Unless it was a union job.

I was paid $3.35/hr in 1988.

Excellent article. Thank you.

The Trust Fund will survive but with inflation, it probably won’t matter unless the payroll tax goes up.

The payroll tax is a percent of earnings (rather than a flat amount). As such, it automatically “adjusts” to income changes.

I knew that. Should have been clearer. I meant, the percentage could be raised.

Draw at age 62 don’t be foolish and buy lots of gold and silver and you won’t have to worry about it anyway

I own some gold, but I think the most important point is to stay diversified. Any hard asset will help you counter inflation. If the asset generates an income stream, all the better.

My opinion is that people would be wise to keep their precious metal holdings below 10% of assets.

You are entitled to your opinion however in this environment I would think a higher allocation than 10% would be more prudent I own real estate as well but I believe metals will outperform in the next few years by a lot I have a rather substantial cash hoard and am waiting for a pullback in metals or real estate before I go all in Patience is required

That’s OK I love them so much that I planted some Avocado trees Guacamole here I come

1) Dr. Faust : 400,000 senior citizens might perish from CV19, within

a week of being infected, instead of normal life expectancy of 15Y – 20Y.

2) There are 48M retired workers and their dependents on SS.

3) Many of CV19 victims lived in expensive salt water cities.

4) A large portion of them lived in nursing homes supported by expensive city & state pyramid financing them.

5) The baby boomers are surfing on the big retirement wave.

6) 400K CV19 victims out of 48M retirees will save SS for two decades.

7) WFH will keep the elderly on co payroll. High income workers benefits are limited beyond a certain threshold. At beyond 70Y the taxmen get both. Inflation will fade decades of SS assets.

8) SS initial booster for the poor will fade by inflation.

9) High income should stay in the labor force as long as they can,because SS will not support their life styles.

10) low income should squeeze the system as much as they can, before the booster fade. Since they are the majority, the retirees nation is a growing.

Well put!

Your postings are informative. Thank you.

Thanks for writing this post Mr. Richter. Everyone should know how social security works. There’s just to much misinformation in the media. The U.S. Treasury definitely has a perennial buyer of their paper and at some point, J. Powell and the FOMC may have to increase interest rates to accommodate social security. As for federal taxes, my wife and I are probably going to have pay taxes on 50-85% of our social security.

According to the tax guidelines if you are single you can have an AGI up to $34,000 and not pay federal tax on your social security.

I told my wife that if we were to get a “legal” divorce (revoke our marriage license) and still stay married we could increase our AGI to $68,000 and not have to pay any Federal taxes on our social security. LOL

But you didn’t pay taxes on the money you put into social security to begin with (you pay your social security tax with ‘pre-tax’ dollars), so why shouldn’t you pay taxes on the appreciated amount you withdraw later?

That’s not true.

From Investopedia:

Because Social Security is a government program aimed at providing a safety net for working citizens, it is funded through a simple withholding tax that deducts a set percentage of pretax income from each paycheck. Workers who contribute for a minimum of 10 years are eligible to collect benefits based on their earnings history once they retire or suffer a disability.5

Paulo,

.

When the federal govt taxes income they tax the gross amount less itemized deductions. The SS tax is not an itemized deduction.

.

Example: You make 1000 a week, less SS 6%, less fed tax 10%. You bring home 1000-60-100=840, but you pay the fed tax on 1000.

Paulo

Petunia is correct. I would have bet 1000 dollars that this was not the case, but I looked it up just now. Shocking. Unbelievable. Thanks Perinia for setting us straight.

And this is especially painful when you are a sole proprietor or single owner of a sub-S and must pay non-deductible taxes for both sides. 12.4% for SS and 2.9% for Medicare. 15.3% on the net after allowed expenses. Then there’s income taxes on the net with SS and Medicare not deductible. But you all knew that.

Lisa_Hooker,

For sole proprietors, contractors, etc., half is deductible.

Lisa_,

One of the pleasant surprises I discovered when my family seed genetics company sold our first wheat varieties, was that royalty income paid to us by our producers/dealers was not subject to FICA with holding.

The company was my dad and myself, so we would have had the 12.4% rate.

Wolf, I checked and you’re right. I forgot that. For the last years my sub-S was paying me no salary and I lived on quarterly dividends the sub-S paid me, not subject to SocSec. They closed that loophole some years ago.

Semantics – the taxes don’t “pay for” anything. They just shift spending from one out-group to another preferred group.

Got it you guys. Thanks.

In Canada, our CPP is a pre tax deduction. Mind you, CPP pays out a fraction of what SS pays. At 65 retirees then can collect Old Age |Security, another $630 on top of CPP and/or private pensions or private investments.

CPP is supposed/designed to be 1/3 of pre retirement income, not replace working income. Plus, neither SS or CPP was designed for 15-30 years of retirement collection. They were thinking 5 years, then death. :-)

CPP is being revised with higher contributions for higher payouts down the line, and longer payouts.

CPP contributions are deductible, but retirement income is taxable as income depending on what rate you are in. SS seems very confusing to me.

regards

Not correct. For your normal, salaried person, FICA deductions are not pre-tax, i.e., they do not reduce your taxable income.

Exactly, taxes are paid on the way in and when you collect, they are paid again (thanks Clinton) after you reach an income threshold.

We have been paying tax on SS for over 10 years now. (Me,77, wife, 75)

Using the logic of the Wall Street 401k retirement scheme this point is valid. But the entire point of the Social Security system is to eradicate, or at least minimize, poverty and misery for our elderly upon retirement. Taxing these benefits is a move in the opposite direction. SSI benefits were not taxable until 1984 in lockstep with other significant economic moves birthed from that period that shifted the burden of supporting government more and more on the backs of workers and away from unearned income.

Please delete, sorry for the duplicate.

“And I too intend to do that – keep working being fired up and having a blast at my evil WOLF STREET media mogul empire until my brain freezes over.”

I was very relieved to read that. Thanks for your excellent blog, Wolf and thanks for this promise to continue.

In favor of a positive outcome (for the fund), more people are taking early retirement, which caps the benefits. More people are dying (even before Covid). Remember in twenty years the baby boom generation will be gone. Social Security has a lot of entitlements outside retiree benefits which are redundant with state and local services. If as some speculate the Fed goes to negative interest rates the par value of those bonds will jump, while only an accounting gimmick, it will provide the catalyst for more spending. Not sure why we don’t have medicare for all, and simply clawback the clients future SSN payments. If you are really bad off and need those medical benefits the actuarial chances that will ever see what you paid in is much lower. A lot of people paying into the system will never see a dime.

Ambrose Bierce,

“Remember in twenty years the baby boom generation will be gone.”

Ha, wishful thinking? In 20 years, the youngest baby boomers will be 75. At that age, they’ll have a remaining life expectancy of 11.1 years for men and nearly 13 years for women. Mid-boomers will be 85 in 20 years. Those that are still around will have a remaining life expectancy of nearly 6 years for men and nearly 7 years for women. It might take over 50 years from now on for the last boomer to have checked out.

In other words, the boomer generation will still be here in 20 years, but it will be a lot smaller. By that time, the millennials will be the hugest biggest bulge bracket ever.

And it will be the millennials’ children (Generation Z or what have you) that will be complaining about the millennials screwing them over.

Uh…no, not all of us, thank you.

Safety nets are a real threat to that small group at the top who want to be king. As long as they are distributed in a “must be a client” fashion (ie drug/alchohol addiction, select chronic health issues, etc.) they can be limited and controlled so as not to threaten the wealth pile. Social Security is not a real safety net…it is a program of maintaining stratifications beyond the working years to ensure a status quo where the participants will fight with each other and never focus on the real problems that screw everybody in the long run. I’m afraid I can’t agree with Wolf on the you can do something else part. From what I see, with all the small improvements that came with technological advances since the microprocessor game started, the end result always ends up heading toward reduced asset values, higher taxation on everything, more spying on everybody, more rules designed to lock out those without access while protecting the controllers of rules, and wholesale destruction of entire enterprises or sectors. It never gies where you might hope. The ocean bottoms are littered with the assets of long gone empires. Probably not a good time to think of a career as merchant mariner based out of any nation…you’ll never collect those retirement benefits. And what young person needs housing, cars, or any savings when your future might be a bunk in an attack submarine as the finger pointing escalates.

You made me reflect upon all that good DeLorean tooling at the bottom off the coast of Ireland. Bankruptcy does not always redeploy assets.

What a bunch of funny comments.

So many people going to get their money back.

And yet they whine like someone might just get more.

All this for a basic income program doing what it is supposed to do for millions of seniors.

The loss of value due to inflation has been manageable for decades, yet the fear of the 1970s is so strong. If you are worried about the 70s show returning with a vengeance, then get some inflation protection.

I don’t think we will see anything other than higher taxes, and that will have some effect on future economic growth. However, the covid crisis is going to end up being far larger in terms of economic damage.

On August 8 Trump ruled payroll taxes are supposed to be deferred from September 1 until the end of the year.

Trump talked about wanting to end payroll taxes a time or two.

Congress would need to change the law.

“My solution is to put money aside while working …”

… and ‘sell’ lots of beer mugs!

My advice to my children :

You work HARD for the money in the 1st half of your life. That hard earned ‘money has to work for you’ in 2nf half. So save and invest. one check at the office and the another in the mail box!

Don’t buy anything unless you have cash (even if you have CC). Don’t be DEBT slave for life.

Between NEED & WANT, there is ENOUGH!

Either you can play now and pay later or otherway if one smart!

California Bob,

They’re gone. No more mugs for sale. The company that did that has run out. But I still have some at my global HQ, to send out as thank-you gift to folks who donate $100 or more :-]

“WOLF STREET media mogul empire”