Four of the six hotels that hotel-REIT Park Hotels & Resorts owns in San Francisco are still closed as convention and business travel remains at near-zero.

By Wolf Richter for WOLF STREET.

Two Hilton hotel properties in San Francisco – the Hilton San Francisco Union Square, the Bay Area’s largest hotel with 1,921 rooms, and the Hilton Parc 55, both in the Union Square area – owned by hotel-REIT, Park Hotels & Resorts [PK], have now been added to the huge pile of hotel properties seeking relief on their mortgages that have been packaged into mortgage-backed securities (CMBS). Both hotels are still closed, though some other hotels in San Francisco have reopened.

Tourism remains a small fraction of its former glory. Leisure tourism, which has come back a smidgen from near zero, is only part of the problem for these hotels.

Convention tourism is a huge factor in San Francisco, and all in-person conventions and meetings have been cancelled or converted to virtual events, including at the vast Moscone Convention Center. People on expense accounts are not coming to the City to go to conventions. And the Hilton San Francisco Union Square is the City’s largest convention hotel, with 134,500 square feet of meeting space, ballrooms, and meeting rooms.

When mortgages that were packaged into CMBS get in some sort of trouble and borrowers ask the loan servicer for relief, they’re added to the servicing watch list, and these two properties were now added to that watch list, according to the San Francisco Business Times. The mortgage backed by the two Hilton properties is still current, but the borrower, Park Hotels & Resorts, has asked the servicer, Wells Fargo, for relief.

If the borrower and the servicer cannot work out a deal, the loan is sent to a third party, the Special Servicer, and thereby added to the Special Servicing List. If the mortgage becomes delinquent, it is then added to the Delinquency list.

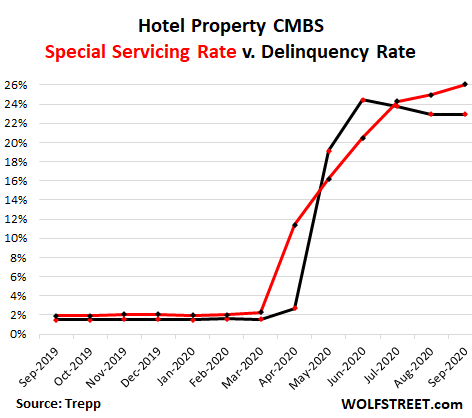

This Special Servicing rate for hotel properties spiked to a record of 26.0% at the end of September, according to Trepp, in its October report on CMBS.

But the delinquency rate of hotel properties ticked down, to a still astronomical 22.9%, as some delinquencies were “cured” because the delinquent loans were granted forbearance, and were therefore no longer considered delinquent, though no payments needed to be made. But the loans that have been granted forbearance continue to stay on the Special Servicing list, and the Special Servicing rate shows a more accurate picture of the state of the hotel property loans:

The CMBS Special Servicing rate of hotel properties has relentlessly increased every month since March, unlike the delinquency rate, which has edge down for the past three months largely due to forbearance being granted to delinquent loans.

The two Hilton properties in San Francisco that have now been added to the watch list are backing a $724 million loan, taken out by Park Hotels & Resorts Group, according to the San Francisco Business Times. Back in 2016, when the mortgage was packaged into the CMBS, the property of the Hilton San Francisco Union Square was valued at $1.02 billion and the Hilton Parc 55 at $540 million.

When the mortgage is sent to special servicing, it will be reappraised, under current conditions. According to a report by Wells Fargo, reappraisals of hotel properties have been brutal. For example, a Crowne Plaza hotel property in Houston was reappraised 46% lower than its appraisal in 2014 when the loan was packaged into a CMBS. The Holiday Inn La Mirada in Los Angeles was marked down by 27% from its 2015 appraisal. The Holiday Inn in Columbia, Tennessee, was marked down by 37%. That’s the range or current hotel markdowns: -25% to -50%.

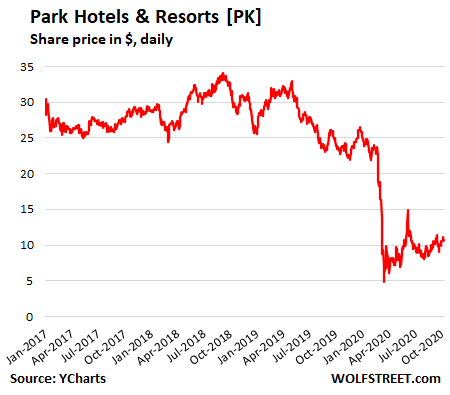

Park Hotels & Resorts was spun off by Hilton Worldwide Holdings [HLT] in early January 2017, and started trading on the NYSE. Park Hotels lists 60 hotel properties in the US, including six hotels in San Francisco (two Hiltons, a Hyatt, a JW Marriott, a Le Meridien by Marriott, and the Adagio by Marriott). Four of these six are still closed.

The REIT’s shares, which peaked in the fall of 2018, started heading seriously lower in May 2019 and by February 2020 were already down 30% from their 2018 peak. Then the Pandemic hit the lodging industry. At the moment, shares trade at $10.75:

Wells Fargo, the servicer of the mortgage backed by the two Hilton properties, has already agreed to provide relief to Park Hotels. It granted a six-month deferral of regular contributions to the fund for upgrades to furniture and equipment. This contribution typically amounts to 4% of revenues at Park Hotels, according to the Business Times. Instead, the borrower is using these funds to service the mortgage in order to keep it current. Wells Fargo also waived obligations for a debt yield test through the end of next June, according to the Business Times.

While there has been some uptick in leisure tourism in cities – and a surge in tourism near National Parks, state parks, and other wonders away from the cities – the convention tourism along with business travel in general remains in collapse mode.

These travelers on expense accounts used to be a lucrative part of the lodging business. Now they’re gone. A considerable portion may be permanent, even after the health crisis is more or less resolved. Companies have discovered over the past seven months that its employees and executives can in many instances accomplish the same thing virtually, while staying at work rather than wasting time gallivanting around the globe, and thereby saved the company a lot of money. Cost cutting is always a top priority. But one company’s costs are another company’s revenues – and hotels and airlines are catching the brunt of that shift.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hotel markdowns -25 to -50%.

Target figures for all commercial property while c19 still rages.

Commercial property owners need to be able to survive at half income for at least 2-3 years. Gonna be tough.

I bet they could fill every single room in these SF hotels at $1800/month 3-6 months lease. But , just as profitable to keep them closed and ask for a bailout.

I realize you’re thinking $1800 is better than $0, but $1800 a month likely doesn’t cover the cost of operation for those hotels – and your idea that they would easily be able to fill them at $1800 is a little silly. These are hotel rooms – they are not fungible with apartments. They lack any kitchen accessories whatsoever.

For context, the RevPAR (not ADR – which is even higher) for the Hilton and similar class hotels in San Francisco was around $275-300. $60/day is not enough to keep the lights in.

Ever heard of Extended Stay America. Hotel room plus mini fridge, plus mini cook top. Silly you.

It’s iffy if California hotels will get a bailout. Renting out hotel rooms as apartments, a reverse Airbnb, would be interesting. It would also be interesting, what the number of people that would have to be evicted out, would be. Knowing California though, the state would probably block it or in some way make them regret it.

From hotel to apartment, in 1 of the 2 most insanely overpriced rental mkts in the US, would seem to be slam dunk obvious.

But as alluded to above, vested interests…acting via gvt, proclaiming some phony baloney “public interest”, will fight it to the death.

Gvt only favors “affordable housing” when the money first gets routed through the G…otherwise, how would it get skimmed?

Might as well rent them out before the squatters get to it.

Some general comments about this.

We have one major conference that I attend each year in SF, it’s not nearly as major as something like F8 or DreamForce, or any that stuff. But it’s still a show with 10K to 15K attendees.

I usually take three to four nights at one of those hotels in the city even though I live in the bay area, why? Cause, the alternative is catch a train early in the morning and back again late at night, and wandering the streets with the old normal (think homeless, etc). Or suffer through traffic and park at an overpriced garage, and then walking to Moscone. Especially considering we have meetings set up throughout the day, into the evening, as well as meeting with all the team that comes in from out of town and the usual trade show stuff.

If my conference happens again next year, I’m not sure I want to live in a hotel in the city, since I have no idea which one of those were used or are still used to house the homeless. Then there is the C19 threat, I do believe that a hotel will sanitize the property, but I have no clue about any of the hundreds to thousands of others in the same hotel. (why risk it)… my colleagues who goes to those conference see it the same way.

My company is already considering not going next year. There is still a discussion of whether to do the virtual events, which by the way, cost as much as a real event, but our experience so far is: “totally not worth it.” Because serendipity does not happen in virtual event. There is zero chance of me walking around the conference halls and bumping into old customers or colleagues…. why? Cause, there is no conference halls. I would not stop in to a random booth out of curiosity to visit because I would never walk by it.

So, there will be an impetus to go back to real conferences, but would I do it considering the new realities… not so sure any more.

I think at this point, some of these hotels are like zombie companies, and they need to be let go. But in doing so, you’ll also be hitting a good part of the labor force. So, it’s a no win situation. Conventions though are not going to go back to normal for a good while. I don’t think even a vaccine will matter unless there is a mandatory requirement for it. And I’d still be skeptical at what got produced by an operation called warp speed.

I think the problem with Covid is that what got let out of the bottle was fear. And once it became uncontained, there was no way to put the genie back in the bottle. There is no going back.

Now, it doesn’t matter what the WHO or the CDC says any more (would anyone trust anything these guys say about Covid now, given all of the missteps… sure trust the science, look where that got us trusting the science from WHO way back in January). all that’s going to matter is the images of the dead bodies in NY, and the incompetent leaders that caused the problems, and the media that exacerbated it.

Well said, MCH. Times have changed, and we’re probably not going to see a return to what might now be remembers as the Good Old Days.

Our last “Family” trip to SF was Twenty Plus years ago. From our downtown five star, we wanted to head out to find the local version of 31 Flavors for a treat. Five minutes of walking around, it was a scene the kids did not need to see, so back to the hotel for room service. Family trips now are to destinations outside of the city, with daytime runs in for wanted activities, then back to the suburbs for the evenings. No more Good Old Days.

RE

Well, this assumes that the event, your company, and your affiliation with it, will still be around next year. Uncertainty is likely to escalate short term.

Look at this from another angle: If they are marked down significantly, now could be the best opportunity for Americans to purchase them at bargain-level prices And then convert them into apartment housing. Hotels are, arguably, the easiest commercial properties to re-purpose for residential use. Re-zoning could be a headache though depending on your state laws, but with this pandemic, I’m sure the authorities will bend over backwards for you, if you can contribute to their dwindling tax revenues. :)

I have an old friend of mine who bought over a hotel in Florida some years back and I suspect he could be hurting bad now, but I shan’t ask him; ‘cos you NEVER do business with close friends or family. It hurts the relationship or it hurts your bottomline…so either way its no good.

America is full of enterprising individuals, so I’ve always wondered why a group of renters don’t use some part of their government cheques to collectively come together to setup a company and buy over a hotel to redevelop into their own homes, and then sell (or rent) the remaining units.

That way, the renters get a house of their own and then some ownership of equity in the company or be able to collectively become landlords themselves.

– A win for themselves, good for the US economy, good for America to reduce her enormous wealth gap and broaden asset ownership among the working poor (instead of having wealth concentrated in the hands of the top hedge funds), increases home ownership rates and at the same time provides more housing for those who needs it.

I mean, it will be a challenge managing a big group of renters-turned-business-owners, but it sure beats sitting on the sidewalk with no job and no house and no plan. What have Americans got to lose now, when the real economy has lost them almost everything?

Because prices haven’t come down for the retail investors at all. Hotels are listed at prices that make no sense, maybe big investors can get 50% off but forget about the small guys.

There is no price discovery out there, You have to tread carefully.

Thats why I said renters can/should collectively come together to form a company to buy into the hotels and re-develop them.

At a fundamental level, your “big investors” are basically also conglomerates consisting of many retail investors aka Shareholders, so there shouldn’t be any difference in pricing between “big investors” and so-called small guys.

All companies are essentially groupings of many “small guys” acting as one big guy just to give them more bargaining power. lol.

For many years the convention center and associated business’s had been complaining that Portland had no “Headquarters” hotel near the convention center. Finally after many years of politics and wrangling the taxpayers provided a pot of money and a big Hyatt was built next to the convention center. It was finished up just as Covid hit. There have no conventions since then and the place has been empty. Not sure there is any way forward for the Portland Hyatt, or the two big Union Square hotels in the article.

Wolf, watching for double top on Nasdaq, the infamous FANGMAANT leading the way. However small caps broke out of the range a little, so double top may be some wishful thinking here.

On another note, I only had a single fund in stocks in 401K (small cap value, many US industruals). Fidelity (what crooks) quietly replaced it couple of weeks ago with ‘mid-cap growth’ fund – top holdings Tesla, Shopify, Zoom, Veev, all else at P/S of 10+. Moved it all to money market at once.

@ Andy

Nasdaq zooming due to SHORT squeeze!

Nasdaq Explodes Higher Amid Unprecedented Gamma/Futures Double-Squeeze

ZH

Did wonders on my calls on TQQQ! But already bought puts on the same just before the end of day. Just crazy day!

This is all money disappearing.. And disappearing money is deflation…

It’s lenders and owners dealing with a mess and taking losses, and in some instances with lenders eventually foreclosing on hotel properties and reselling them at a loss. This is an investment event. If you want to call this a form of monetary deflation, fine with me. But then you have to call the stock market bubble and the general bond market bubble “inflation.” Which is bigger for now?

The fed is telling you which is bigger. For over 10 years now they’ve been printing to fill a bucket with a hole on the bottom. They keep printing faster and faster hoping to catch up.

Luckily very little of this is getting into consumer goods, or the hyperinflation people have been warning about would have happened.

This was/is well known since the beginning but got confirmed as the years went by, since ’09.

Mkts and productive Economy on the ground (save Tech sector) remain disconnected. More financialization of FIRE industries favoring top 10% and the Wall St.

This has become a CRAP-SHOOT mkts with betting more on the long than short side since Fed keeps on buying 120 Billions each month! Never seen any thing like this but lately I got adopted with swing trades.

(Been in the mkt since ’82)

Wolf,

When you say “This is an investment event,” how do you mean?

Is the fundamental assumption that things will eventually trend back to some type or normalcy, or is it more along the lines of this is going to be a real estate investment event where the real estate itself is valuable, but not necessarily how it is currently being used?

The real question is probably one of timing and the general situation around SF, but I don’t know how investable this is in the next couple of years unless it is for the purpose of more residential real estate. Cause the tourists and the conventions will not come flooding back in over the next twelve months. At least, I don’t think they will.

As opposed to a monetary event. Maybe not best choice of words.

Sold to SF for $1. :)

The stock market bubble, along with the housing bubble are definitely inflationary. I do not see how anyone could deny that. So far as the deflation from losses, we have only seen the tip of the iceberg.

We are still in the “pretend” phase of this recession. People really want to believe things are going back to where we were, but they are not.

At some point in the not too distant future, loses will have to be realized and dealt with. Loans that can no longer be serviced will have to foreclosed and the assets will have to be sold at market, which will begin the downward spiral.

Every city has a need to promote their football team, fill butts in the seats. Those fans buy hot dogs, beers and stay in hotels. If I were a city manager I would figure a way to put people in empty hotel rooms. The corporate expense account is on hold, get people with cash if you have to pay them and put the game on TV. And gambling…

The assumption is that the hotels will be closed through winter. . Can the hotels survive another 6 months?

Rents in DC are starting to look healthy. One can get a 1 bed with about 600sqft for about 1700 from private land lords. Large properties trying to lure people in with 2-3 months free and a lot of condos are coming online now and first half of 2021.

Its weird to see a studio renting for 1700 one website while being offered on another for sale at 400k. The math dont work.

It’s all insane and will come back to fair value eventually just like all markets do

@Frederick

But when???

Reversion to the mean is the rule, but NOT when Fed is determined to keep the bubble floating by buying 120 B each month.

Since that announcement seral (?) weeks ago, part of my investment strategy became tactical trading (compared to strategic/structural) with hedges, of course. This has resulted in positive feed back on my portfolio.

swing trades in option trading accomplishes this, most of the times.

In a way I started betting against my self ( rational decisions!) crazy!

Back in the bad old days of banks owning mortgages, 20% down and enforcement of GAAP and fraud laws…

The worth of an average rental property was about 120× monthly rent.

So, in this case, the sale price needs to be cut in half.

Imagine the property taxes.

Now imagine them cut in half…or more.

Will city spending be similarly reduced?

“the property of the Hilton San Francisco Union Square was valued at $1.02 billion and the Hilton Parc 55 at $540 million.”

“The Holiday Inn in Columbia, Tennessee, was marked down by 37%. That’s the range or current hotel markdowns: -25% to -50%.”

My estimation is there will be resistance to cut taxes. Think about the additional loss of hotel taxes including loss of tourism and business dollars.

I suspect there is going to be a big budget issue soon.

In the case of San Francisco, property taxes are set at the purchase price + an adjustment approximating COLA each year so I don’t see that requiring an adjustment. Of course commercial property owners use various loopholes to circumnavigate the actual taxes that should be due but at least there is a proposition on the ballot to try and limit this. Hopefully it passes. Hotel taxes are another issue. They’re at 18% of occupancy dollars so the city will face a hit. Over 90% of SF government expenditures are voter approved and these are locked in place.

What specific service would you like to see cut?

Locked in place! Well then, the debate must be over.

I am not quite sure you understand what a budget is and how revenue needs to match spending when you can’t print money.

Of course, SF can play the borrowing game for awhile but SF already has a staggering $16,400 in debt for every taxpayer (2016 numbers).

“Over 90% of SF government expenditures are voter approved and these are locked in place.”

Well don’t you know, that’s what federal bailouts for municipalities are for! After all, the federal government can borrow at very cheap rates forever with no negative consequences!

lol

I’m an accountant and have a pretty good understanding of budgets, etc. If you knew anything at all about the specifics of how government is run you wouldn’t weigh in with these snarky anti-government comments. Here in San Francisco (as probably many local government do) initiatives are put on the ballot that allow citizens to actually vote on where they want the City to spend money. And isn’t this what Democracy is all about?

I wouldn’t worry about San Francisco. It’s a wealthy, healthy City who’s natural beauty and residential architecture is unmatched in this country. And the good news is that you never have to come here so none of this is your problem.

Government is by its own nature corrupt. The more money you pour into government the more corrupt it gets, and the more money gets stolen without providing any benefit to taxpayers.

The money going into government is being taken out of the economy, and can no longer be productive. It is a downward spiral.

> What specific service would you like to see cut?

Local govs dont want to cut anything, nor people that rely on the myriad of services… but it will happen nonetheless with people kicking and screaming into the wind like they did in stockton and detroit…

LOL. You are seriously comparing Stockton California (and Detroit?!) with San Francisco? Get real.

Detroit was a boom town before SF, as were many other cities in various other places in the world before they fell from grace…

Voters deciding on spending money that their municipality have saved is one thing… voters deciding on spending money that’s predicated on money they need to constantly borrow is another…

“But there will always be enough lenders”… said every city ever throughout the ages…

There are all kinds of municipal revenue losses due to the government pandemic response, this will be one. The municipalities and the states are whistling past the graveyard waiting for Crazy Nancy to come through with the $1.5T bailout for them. She is holding all pandemic payments hostage but I think she will eventually have to fold.

pandemic debt funded disbursements will have increasingly smaller effects if they happen, and essentially are hospice care for the terminally ill economy.

Said another way, the ship continues to sink in the mid atlantic, comms are down, and people are arguing over which mineut to play on the few leaky lifeboats available…

Lifeboats is right. I started reading all this financial crap after the Lehman bust to figure out how to prosper in the coming bigger crash. It has not helped. Turns out luck and timing is still everything.

Fortune favors the bold – about 10% of the time.

But the meek lose everything.

SF will borrow rather than cut spending.

To SFMarkin, there are many great cities that eventually borrow more than they can pay back. Chicago (now) and NYC (in the 1970s) come immediately to mind. NYC was rescued by a miraculous revival, but is now back on the long term insolvency track. If you think SF is exempt and can borrow forever because “beautiful wealthy city”, history suggests otherwise.

The Hilton Union Square was worth $1Bn now worth 25-50% less say $350,000,000 has gone. Where does the money go?

The money lost in a write down such as this leaves the system. Those that believe we will have a deflationary future argue that an increasing number of write downs and defaults such as the one facing these hotels will destroy money faster than it can be created ,leading to deflation.

Wolf,

Per Seneca’s comment,

“argue that an increasing number of write downs and defaults such as the one facing these hotels will destroy money faster than it can be created”

and my comment…the point I am trying to highlight is that downward collateral revaluations (in a RE environment where leverage is heavily stacked…hotel A serving as collateral on hotel B loan, which in turn serves as collateral on hotel c loan, etc ad infinitum) can sorta be viewed as analogous to the withdrawal of Fed “high powered money” (writ small) – because CRE tends to be a system heavily built by leverage upon leverage (pyramided loans).

So, that once enough collateral gets written down, it can trigger a much, much larger domino effect of write downs/defaults…which have the effect of “withdrawing “money” from the system”

It is a dark side multiplier effect within the CRE world, cratering near term use of “debt” (which CRE empire builders and Keynesians tend to define as “money”).

Therefore falling collateral valuations withdraw “money” from the CRE universe because of a collapsing multiplier effect upon the stacked leverage.

The same place where all the good men went.

Down memory lane.

It’s just numbers on paper, or digits on a computer screen. It’s not money.

Correct it’s fiat currency Only Gold is money

Of course it is money. The vast majority of the money in our system is digital, but that does not make it less real. All money is simply a representation of production.

It does not matter if you are using gold, paper, or digital accounting it is all the same. In our system, most money is created out of thin air every time a credit purchase takes place. What gives the money value is your commitment to repay that debt by way of your future production.

By that same token, if you default on your debt, the money disappears.

When money is being created faster than the production of goods and services, it is inflationary, and when it is being destroyed faster than the production of goods and services it is deflationary.

kk,

That’s just a valuation denominated in dollars. There is no money involved in what you’re saying. You could also denominate the same thing in euros or yen. Money doesn’t get involved until there is some kind of transaction, such as a sale, a mortgage payment, a mortgage payoff, etc. After these transactions, someone might have a loss (got less money back than what they paid for). But that hasn’t happened yet.

Wolf,

Well…one thing about mere “revaluations” downward is that they tend to blow the hell out of the CRE equivalent of cash out refi’s…and…a lot of RE “fortunes” are predicated upon the pyramiding of properties/leverage which in turn relies upon assumed collateral values.

Once those collateral valuations get revised downward, a whole succession of pyramided loans can go into default unless offsetting new money is put in.

And none of this requires an actual sale. It all simply turns upon collateral valuations falling.

What say you?

Yes, it’s a mess.

The question was about the write-down: “Where does the money go?”

My answer was that no “money” (what you have in the bank) is involved until there is a “transaction” of some type, meaning something gets sold, paid off, borrowed against, etc., and this would likely involve actual losses (not paper losses) for one or the other party. A write-down itself doesn’t involve “money.” The transactions that eventually follow involve money.

Well one thing is for sure:

Holders of 7.5 PK US70052LAA17 (2025), 5.875 PK US70052LAB99 (2028) and various derivatives writers on said debt wont care much about the sophistry of collateral write downs… still m2m losses on the books EOD and collateral calls front bank of new york mellon going out for that re up… lol

When a large part of the economy depends on lubrication of financing, based on the perception of ever increasing values, it seizes up pretty quick when that perception ends.

The HELOC fiasco was a miniature example. People could borrow on the inflated perceived values of their property, and then spend that money which drove the economy…

Until the perceived values collapsed, and the homeowners no longer wanted to pay the huge loans. Then the economy collapsed.

Today, it is everything, not just home values which have been grossly overvalued, and over leveraged.

As everyone said below, it’s just a change in what people were willing to pay. That’s the same mistake that people make with stocks. They think that if a market cap of a company goes from $500 billion to $700 billion that someone “gained” $200 billion in cash. But that’s not the way it works. It just means that the current crop of buyers is willing to pay more, and the current crop of sellers is not willing to sell for less.

Thus, you can have massive changes in valuations with very little volume.

Into the magic never-never land of mark-to-market. In other words value is ephemeral; it would only be worth $1B if it sold at that price. I’ve decided to value my modest home at $150 million. Now I just need to find some folks to agree (for an appropriate fee). BTW, it’s not for sale.

Don’t let the county appraisal district know your new value…

It always amazes me that,

1) People don’t see property taxes as wealth taxes and,

2) Equity in home isn’t taxed…but rather the *total* value of the home…much of which is made up of debt.

“Long usage” tends to blind the public to what is really going on.

There is probably a lending company that will accommodate you. Especially if you agree to invest some of the money you borrow in their company. I do think that the country owes Neil Bush (Silverado) a huge apology. He never really meant to turn that toxic waste dump into a residential neighborhood.

Lisa Hooker:

I would contact Angelo Mozilo…I’m sure he has a “package” for u…………

Property tax bills getting printed now. I’d imagine every landlord, hotelier, etc is asking for reductions.

The Roosevelt Hotel in NYC just closed.

Strangely, it was owned by Pakistan International Airlines.

Trump Tower in Vancouver closed about a month ago. Looking for a new owner. You could hear the cheering all across the city.

From a CTV article: Then-mayor Gregor Robertson wrote to Holborn in 2015 on behalf of citizens asking the developer to “quickly” remove the branding from the project. Robertson also asked the city manager to explore whether the city could have forced the developer to remove the name.

I have never understood how the infamy of the Hilton name did not have the same effect? Or, did it? :-)

If it’s vacant, homeless people should break in and use it as a crack house.

Got FAANGS?

While we are talking about taxes, lets imagine the reduction in hotel (tourism) tax that is being collected now in San Fran and elsewhere. In most cities with a significant tourist trade this is a big chunk of money that won’t be flowing in to city and state coffers. Like the falling dominos, this leads to another set of job losses that are only barely being accounted for now.

Seneca’s Cliff:

Let there be no illusions. All of the country’s locales are going to take huge hits in tax revenue.

And, as always the most vulnerable parts of those budgets will be libraries (arts), education, emergency services etc. These are the bread an butter issues confronting all of us, our legislators and local governments. I’m not sure they will have the wherewithal to address this incredible very near future shortfall.

It just might tip this country into the abyss.

My own CA county in the foothills of the Sierras is already confronting this problem. I can’t imagine what would (will) happen in big cities like SF etc., when so many “social” services will be cut.

To me it appears sheer madness to believe that “things will return to ‘normal'” anytime in the next years.

This is a compounding catastrophe!

If the Fed on the monetary side aided by Congress on the fiscal cannot print their way out of this hole a battle extradinare is on the horizon. The battle ground will be bloated government budgets needing more money to fund their heroic positions while the hapless non-heroic chumps scrounge to keep paying the taxes for the heroes to keep their heroic positions. Poor chance this will not be fodder for the modded.

Nearly every single Fireman that retired in NYC in 2020 had a $100,000/year plus pension.

10% of those had $200,000/year plus pensions.

Source. New York Post, October 11, 2020

It’s going to take $20 trillion and quickly. That’s a pretty fair estimate. Hope the fed has that much ink laying around.

I heard that Larry Summers said the economic hit is $16 trillion. That must be about 10% of countries wealth. We see who the winners and losers will be over time

There is one school of thought that there is a natural healing process that happens once you have a recession and all money printing and government policy doesn’t really help the time to get back to full recovery. We know politicians use a crisis to get legislation through that could not pass in normal times. Election is going to determine who eats the $16 trillion.

I do not know how anyone would be able to calculate the economic loss at this point. This has just begun, and no one knows how bad or how long this is going to be. You are talking 50 years of asset inflation based on ever increasing debt.

Basically the entire country has acted like a teenager with a $250K credit card limit who found out they could make the payments with cash advances…

“Two Hilton hotel properties in San Francisco – the Hilton San Francisco Union Square, the Bay Area’s largest hotel with 1,921 rooms, and the Hilton Parc 55, both in the Union Square area – owned by hotel-REIT,”

Wolf, you mean the REIT type that gets free Fed money?

I don’t think they got “free” Fed money. Park Hotels had to pay something like 7.5% in May when they issued secured bonds, and 5.5% in September when they issued more secured bonds. But yes, it was still low-cost, considering the risks.

I had in mind your article, during the REPO madness, that stated REITs and Hedge funds were indirectly tapping into those Fed accommodations. Am I incorrect to do so?

I see. Those REITS are “mortgage REITS.” They don’t own real estate. They just own mortgage-backed securities in highly leveraged positions, and they borrow in the repo market to fund those MBS positions. Those leveraged MBS bets then blew up. Park Hotels, on the other hand, actually owns the hotel real estate (the land and buildings). It’s a property-REIT, not a mortgage-REIT.

“Park Hotels, on the other hand, actually owns the hotel real estate (the land and buildings)” and then they float the mortgage, no? Connection?

Park Hotels borrows the money from a bank (gets the mortgage). The bank sells the mortgage or packages it into a CMBS and sells the CMBS to investors, such as pensions funds. Park Hotels has nothing to do with that. They’re just the borrower.

A recent STR (data provider for the hospitality industry), survey indicated urban hotels are at 38% capacity and all hotels are at an average 48%, so less than half full and operating at staggering loses, and the forecast for a meaningful rebound is grim. Subsequently, the AHLA is seeking an industry-wide, congressional bailout per CEO Chip Rogers beg-a-thon from. This has great potential to destabilize CMBS as CMBS is already forced into a repricing event due to mall REITs.

Did the airlines get their industry-wide, congressional bail out yet?

The hotels want a bail out, the airlines want a bail out, the States want a bail out, the Cities want a bail out, the citizens want a bail out, and the list goes on and on.

The problem is, the Federal Government does not print money. It borrows it, at interest, and that interest must be paid, and it must collect taxes to pay the interest.

As asset prices fall, and government at all levels, Federal, State, and local scramble to borrow money, much of the cash now sitting idle in Treasuries will begin to seek better returns, which is going to make Treasury auctions much harder to complete without paying higher interest.

We are about to see what happens when the laws of supply and demand come face to face with a monumental need for cash from every segment of the economy and every government entity at the same time….

We are headed for more concentration of wealth as great assets are picked up for pennies on the dollar. There will LBOs of divvy paying companies as paying the debt service will be cheaper than paying the divvys. Not just talking about hotels either. The big boys will arrange financing; the smaller guys will be shutout and default.

Alot of whats going on is deflationary