The signs and numbers are already lining up.

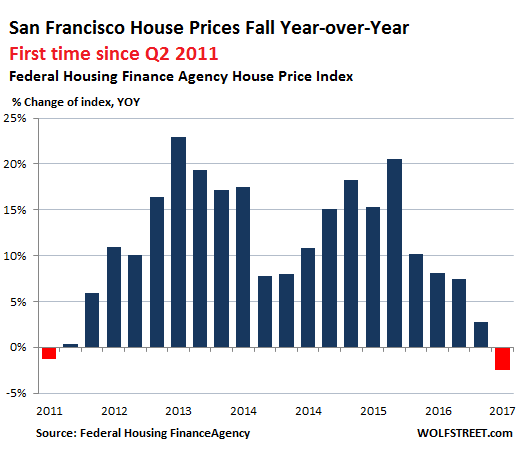

According to Federal Housing Finance Agency data on our glorious Housing Bubble 2, house prices are doing what they’ve been doing for years: they’re surging. In the first quarter, they rose 6.0% year-over-year.

“The steep, multi-year rise in U.S. home prices continued in the first quarter,” explained FHFA Deputy Chief Economist Andrew Leventis on Wednesday. So house price are going up everywhere. Well not, everywhere.

In the once hottest metropolitan statistical area where house prices have surged in the double digits for years – San Francisco, Redwood City, and the city of South San Francisco which make up the tip of the Peninsula – was the sole exception: there, house prices fell 2.5% in Q1 year-over-year.

It was the first decline since Q2 2011, when the last housing bust ended. This chart shows the year-over-year percentage change per quarter of the FHFA’s House Price Index (HPI). Note how many times prices increased between 10% and 20%-plus:

The HPI is based on data from mortgages that lenders have sold to Fannie Mae and Freddie Mac or that were guaranteed by them. These mortgages are capped – for the San Francisco area, at $636,150. In San Francisco itself, the median house price is about $1.35 million and the median condo price about $1.1 million, according to Paragon Real Estate in San Francisco. With a 20% down-payment, the home could be priced at $800,000 to qualify. I know buyers who made a much bigger down payment – given how little their money earns at the bank – to get a conforming mortgage because they wanted to benefit from the lower rates.

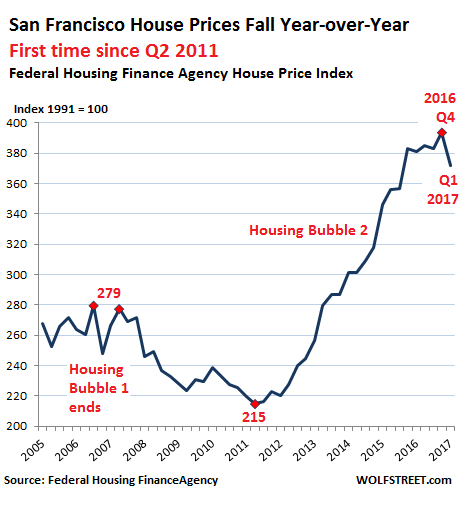

This is what the index looks like, including the ominous kink at the top, the first such sharp kink since the end of Housing Bubble 1:

In terms of price movements, how close is the HPI to the median price?

- During Housing Bubble 1, the HPI double-peaked in Q3 2006 and Q2 2007. By comparison, the median price in San Francisco (as opposed to the larger area the HPI covers) peaked in November 2007.

- The HPI plunged 23% and bottomed out in Q2 2011. The median price in San Francisco plunged 27% and bottomed out in Q1 2012.

- The HPI then soared 83% to peak in Q4 2016. The median price in San Francisco soared over 100% – and stalled in early 2016…

“Stalled” may be too optimistic a term. Paragon Real Estate notes that the three-month moving average of the February-April median price of condos was about flat year-over-year with 2016 and 2015; so two years of essentially no movement. And house prices fell from the same period in 2016.

So the turning points of the HPI were leading indicators of turning points in the median price in San Francisco, though the HPI’s movements were less steep, plunging a little less during the bust, and soaring a little less during the boom. Now San Francisco’s housing market is into the next phase.

CoreLogic’s data corroborates the lumpy nature of the San Francisco housing market; the median price in April for all types of homes dropped 4% year-over-year to $1.3 million, with sales volume dropping 12%.

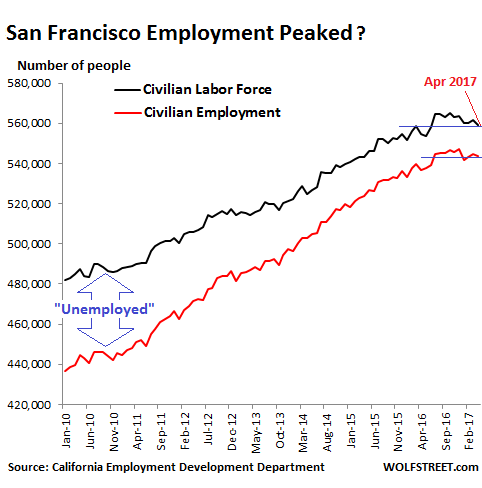

And here may be part of the reason for the lumpiness in the housing market: The construction boom has been throwing thousands of new housing units – all condos and apartments – on the market every year in recent years, and will continue to do so, just as employment growth, according to California’s Employment Development Department, has slowed down sharply:

Note that the “labor force” is based on the number of residents in San Francisco; “employment” is based on the number of jobs in San Francisco, including those jobs filled by people who commute into the city.

The labor force in San Francisco fell to 559,100 in April, the lowest since June 2016 and up only 4,500 year-over-year. This is the crucial indicator for housing demand. Employment fell to 543,900 – essentially flat in 2017 and up 7000 year-over-year. So far in 2017, year-over-year employment increases ranged from 5,000 to 8,700 jobs per month. This might sound like a lot, but…

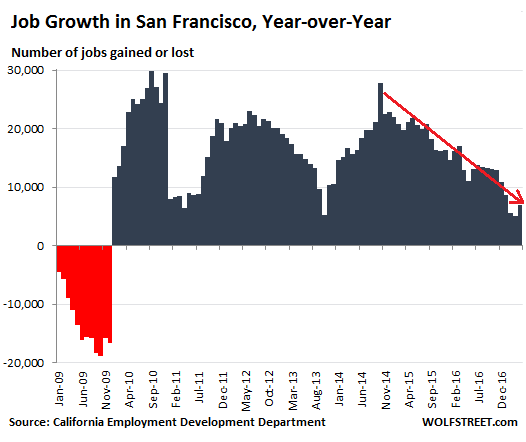

- The year-over-year increases in January-April 2016 ranged from 12,900 to 17,000 a month.

- The year-over-year increases in January-April 2015 ranged from 21,100 to 22,800 a month.

This chart shows the monthly employment gains and losses on a year-over-year basis going back to 2009. Note the sharp decline in gains that started in early 2015:

Even as employment gains are tapering off, thousands of condos and apartments have come on the market and continue to come on the market every year as a result of a historic construction boom, with new towers sprouting like mushrooms in certain parts of the City. Almost all of them are high-end. So in addition to the market facing a dose of supply-and-demand reality, it also faces a problem of affordability, with not enough people making enough money even in the tech sector to buy or rent at those dizzying levels.

Peak Rent has already happened in San Francisco and other top housing markets. Traces of relief for renters, as landlords scramble. But in some cheaper cities, rents are soaring. Read… The Great Unwind Grips the 12 Hottest US Rental Markets

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If we want AFFORDABLE housing for everyone then home lending needs to be capped at say $300,000, not $636,150

If we had a 20% minimum down payment requirement we would not have this bubble in the first place.

If we had a responsible central bank instead of Keynesian fraudsters at the Fed intent on transferring the wealth and assets of the middle class to their Wall Street accomplices through engineered pump & dump schemes every eight years or so, we would also not have such insane bubbles.

if we don’t have a central bank…..

– If the central bank is to blame for blowing all those bubbles then real estate prices in West Virginia should have gone “through the roof” (like in San Francisco) as well. Yes, real estate prices in WV moved higher but they didn’t go up by some 80% since 2011.

https://www.zillow.com/wv/home-values/

– If you want to blame someone/something for the transfer of wealth away from the middle class then blame rising productivity and blame the capitalistic system.

Hey, Gershon– The Fed ain’t Keynesians; they’re Friedmanian monetarists. The Fed are anti-Keynesian. Keynes promoted counter-cyclical fiscal and monetary policy, which essentially prevents both bubbles and deep recessions. The Fed is pro-cyclical. Keynes hated asset bubbles. The Fed banksters love asset bubbles, and they only put on the brakes with higher interest rates when it looks like the people at the very bottom of the income ladder might see a marginal increase in wages.

All of the Chinese buyers make their purchase(s) with 100% cash. No need for a loan, in fact they usually out bid all of the competition.

Do what Germany does; penalise excessive speculation on property. There’s plenty of investment choices out there. Allowing capital to spill into basic essentials like housing simply starves productive industry of needed dollars.

The “cash buyer” is a myth.

Actually, if you want developers to build affordable homes, then the cost of permits and hook up fees need to be a sliding scale based on square footage. Right now, the cost is the same whether you’re building 1000 square feet, 5000 sqft, or putting in a mobile home. If you’re a home builder, there is no incentive to build small and affordable.

These are minor expenses relative to the total price. Theyre neither disincentive or incentive.

Shut down the Fed, end fractional reserve banking and unbacked fiat currencies and housing will become affordable because money will have value.

You can have affordable housing in Utah or montana, Detroit. But that’s not what the leftists want. They want affordable at most premium locations from San Francisco to Hong Kong.

Blame Canada and our access to cheap credit.

https://betterdwelling.com/the-us-has-a-foreign-buying-problem-and-its-not-china/

Best part of the linked article:

“Last year Canadians were also busy realizing profits in the US. Citizens of Canada accounted for 23% of all sales from foreign owners in 2016, the highest of any single country. China was second, but way below at only 15%. Tied for third were residents of the UK, and Mexico with 6% of sales each. So it’s clear Canadians aren’t buying these properties to hand-down to their family, they’re buying them to make a profit.”

A lot of those Canadians are probably of Chinese origin. Most Canadians I know can not afford the kind of house prices we have here in SF. The impact of Chinese investors in the North American is huge. It’s difficult to come by accurate numbers because of the PC nature of the topic.

I for one have no issue with limiting foreign investment in housing property and am not afraid of letting my elected officials know it!

I’ll second the motion ! That along with a cap on residential investing . Enough is enough !

You are saying US of A has been printing 4trillion to buy Chinese goods during the past 30 years and when these hard working Chinese folks come back with the 4 trillion to buy companies and houses here in US of A, you tell them “No. you can NOT buy anything, please just hold the paper? Enough is enough!” I thought this is the true color of this country’s government, but I have never realized everyday citizens are like this too.

I think the issue addressed by SDUB here is non-resident foreign investors that treat homes as a global asset class without any intention of living there or renting it out. They buy homes to diversify their portfolio (and get some of their wealth out of the reach of their government). That’s speculative demand that can create all kinds of problems. It can appear suddenly and drive up prices to the point the local economic equations no longer make sense. And this demand can disappear without notice, causing a sudden reversal with huge impact on the local economy.

The elected officials of Vancouver and now Toronto have issue with it. If the vast majority of people in San Francisco welcome foreign investment in RE, I have no issue with that. Yet if it goes the other way, we have to respect that as well.

Sounds great!!

Yep, I think that all people who own houses in the USA should be restricted in a number of ways.

First, they should not be able to sell to a foreigner.

Second, the price of a house should be limited to around the average yearly income for an individual in the USA. If the price goes above that amount all the proceeds should be taxed at 100% and sent to the US Federal government.

Third, as those wicked investors push up prices people and companies should be limited to owning only one house/condo/unit. That should release a huge supply onto the market and make housing affordable.

Fourth, as farmers aren’t exempt from this, we can’t have them owning over priced land either. Farmers should be limited to owning one section of land as well.

Of course as I don’t own a house/condo/unit/farm in the USA these all sound great to me!!

Hit the hypocrites right in their pocket.

JZ, your assertion is morally correct, as long as US citizens have the same access to foreign markets. Its not right that US citizens can not own beachfront property in Mexico, but we allow Mexican nationals to do so. The same should hold true of the Chinese.

Wolf I agree with you that speculative behavior will wreck people’s lives.

The solution is NOT to regulate/destroy the honest price discovery market that let people speculate as well as let people eat their own consequences of speculating. That market based process is how this great country was built.

The solution is to see the root cause and address them there.

I am just trying to point out who actually fueled the speculative behavior in all asset classes including houses.

It is those $ created by central banks that encourages debt encouraged behavior. Smart money speculate on assets, dumb people use debt to consume. Big reasons domestic inflation is tamed is because all of those $ are exported to China, but those money are coming back.

Whose fault is it? Those who complain about these $ coming back should remember they have been enjoying cheap Chinese labor/goods for the past 30 years. It is time to face the consequences.

Oh, right. US of A never faces consequences. We print and buy goods/services, and when the reckoning day comes, we have the strongest military.

Wolf,

As you say- foreign investors can disappear without notice. This is exactly what is happening in Melbourne. A real estate agent told me just last week that Chinese apartment buyers have completely disappeared and those with deposits down are walking away because they can’t find a bank to give them the other 90%.

Your elected officials care deeply about what you think, prole.

No really. They do. Their oligarch donors pay them to represent you, not to be the oligarchy’s flunkies and enablers.

/sarc

The game is all relative to how deep the pockets go. Realize there are many people, worldwide, with huge incomes, and they hire people to look for investment opportunities. Whether or not that prices you out of your home they give a f*ck less.

Rather than limit what they can invest in and to what degree, it’d be much better to address how they get those income streams. And yes, I know that’d be a helluva battle. Nobody want’s to try limiting or taxing excessive incomes, as they deep down think, or should I say hope, that someday there own ship is going to come in.

Foreign speculation into our housing markets is pretty ingrained at this point. But it seems to me if our State and Federal government are really pro home ownership, then there is no place for foreign investment into homes unless those foreigners have a valid visa or green card to come live in that home.

I suspect in many ways Americans wanting to own homes would be better off in many markets if foreign buying was simply banned.

Though I have no doubt the transition may have a dramatic effect on current markets.

I have met speculators of all ages and backgrounds in Toronto.

Greed sees no colour.

It also doesn’t help that the entire industry doesn’t care where the money came from or how indebted a person is, as long as the they find a large enough down payment to reduce the balance of the mortgage to qualify for mortgage insurance on the bank loan.

Shawn – I’m in North San Jose, California, and the number of Chinese, Indians, and amazingly, Koreans, here is amazing. Good old SF Market (Shun Fat – we shun the fat so you don’t have to?) market closed which was a bummer but a Korean market is going to open there and it’s going to be great. In the old SF place I was typically the only “round eye” in the place, and the Korean place might be the same. I’m a distinct minority in my own country/state. On a day-to-day basis I can’t complain, because as a general rule, all of ’em are nice people and it’s nice being able to get a variety of foods, but it’s kind of … weird.

So, why do you leave your country (India/Korea/China) for a different one 1000’s of miles away with a very different culture? Obviously for the most part, it’s because there’s money to be made, and money to be kept safe – the US is far less prone, so far, to by gov’t decree, empty your bank account, seize your house, etc.

I wonder if people living in cash-havens like Monaco(?) or large Swiss cities feel the way I do? “Hm, I’m an ordinary Joe from here, and here are all these wealthy to downright rich people from all over the place, living in my town”.

Is that going to be the US’s future? To be a safe place to park your money, hide out from the dictator or dictatorial government back home?

For the working class in the US, it’s already by far the best choice to go into the military and then into the “security” industry. Is that what average Americans are going to become? The warrior class? Are we destined to become “Worf” in the new Star Trek world? Yeah, Worf gets to hang out on the bridge, but no one expects any intellectualism from him; he’s there as a necessity to do the fightin’ when fightin’s needed.

“For the working class in the US, it’s already by far the best choice to go into the military and then into the “security” industry.”

It all depends on what branch and what MOS you are trained for in the military. If you can get trained in a highly skilled area and then use it in civilian life then go for it.

As for a long term career, I don’t think it is a good ideas as the rules keep changing.

Pay is much better now than it was when I was in. IIRC people in the Peace Corp were were making more than most new officers.

Yet making $1600 a month basic pay and being shot at as a grunt 11B really doesn’t seem very appealing nowadays.

Even for Officers at around $3000 a month doesn’t seem much either.

Lee – I just had a look at the current pay charts and it’s pretty good pay. $1600 a month basic pay and getting shot at beats the hell out of $0 a month and getting shot at. And this is the choice a lot of working-class Americans are looking at. I kid you not.

What’s good is to get some sort of “tech” skill, that confers a clearance, then when you’ve done as much time in the service as you like, take your fresh clearance and work for a military contractor. But that takes tech skills many don’t have, and what’s funny is, tech really doesn’t pay more than any other humdrum field, with a very few exceptions that are magnified hugely in the media. Soldering circuits or driving a forklift both pay the same $12 an hour where I am.

I don’t think many of the “chattering class” realize how life is for a huge number of people in the US. Even with getting shot at, I’m willing to bet the “quality of life” on the front line doesn’t mean giving up any more years of life expectancy than living, yes just living, in many areas of the US.

Alex,

When I was a brand new O-1 the pay was well under US$1000 a month so the pay levels have come way up since then. Can not remember what my E-1’s and E-2’s were making back then

Compared to what the people in the military get here in Oz, the US pays peanuts. When I got out similar rank equivalents were making multiples of what I was getting at the time.

In any event I wonder how many of those ‘working class Americans’ could actually meet the various requirements and actually complete the training………..unless standards have fallen for the military as well.

It’s the same way in Seattle. In my immediate neighborhood of 6 homes there are two Chinese families, and Indian family, and two retirees that have been here for a long time. The only people buying houses here recently are immigrants. It makes me wonder if the immigrants are more willing to accept financially risks, or whether they’ll just do anything to live in the United States, or whether they just have boatloads of cash to burn. I suspect they see real estate as more opportunity than risk, perhaps mistakenly at this point in time.

I was born in India. Nobody “seizes your house” for random reasons and the democratic process is like in any other democracy – messy but substantial.

People are highly educated, follow opportunity and demand and want to buy a home around where they work. They view real estate as a long-term investment, not speculation. And most of them buying homes are American citizens.

Why are aspirations of highly qualified non-Caucasian Americans that hard to understand? They are the same as the aspirations of Caucasian Americans.

There are plenty of Bosnian Muslim refugees where I live, who are now American citizens. No one seems to have questions about them buying homes, etc. Or about their citizenship status. ‘Cos they don’t have strange looking skin or eyes, I suppose.

More like a Praetorian Guard for the Overclass, to enable their looting and pillaging, and keep the “Losers” (that would be the rest of us) a safe distance away.

From the Software world its pretty clear why you have a wealth of well educated Indian buyers. Part of the Silicon Valley labor force is green cards and the most talented Indian engineers jump at the chance to work in or with the US tech companies because they pay very well. Many come over as dual income tech workers and end up at a minimum upper middle class.

In theory if more Americans focused on obtaining a strong graduate level credentials in STEM fields there would be far less demand for foreign workers through VISA programs.

Though at this point many large companies can kind of hold visa’s hostage because it is much harder to job hop when your visa status depends on your work.

People buying homes here on visa programs don’t bother me . If there are super wealthy Chinese though living in say Hong Kong and just buying high rise condos to park their money and get a vacation home or have a rental that bothers me. Because that seems more likely to drive housing prices beyond what the local job market should bare.

To a degree this is probably unavoidable as plenty of wealthy Americans would probably happily take their place and own multiple homes on all the major metros….

Don’t blame Canadians. We can’t even afford housing in any of the thriving provinces. The east coast is less expensive but there unemployment is high.I’m a disabled senior and would give love to downsize but the 50 year old smallest bungalows are going for 699k and up. However we do have foreign investors buying up big time and this is enabling price hikes. On a personal level my husband and I honeymooned in S.F and returned 10 times for a holiday. I love it and would love to come back. M.Marr.

Robert Shiller came on TV yesterday and said that equity markets could rise 50% under Trump. Mister irrational exuberance usually fills the role of the resident worry wort, so that shook me a little.

It reminds me of Grantham’s very bold and bullish 2 sigma overvalued S&P 2250 (election time) call back in 2014 when it had already rallied up to the 1700’s.

If anything remotely resembling that scenario plays out (Nasdaq on steroids) i would postpone any pent up enthusiasm for a continued correction to SF home prices. It could easily reverse course violently upwards. God help us all…. well at least those of us in the bottom 95%.

On a side note, Manhattan home prices were up 1.3% February 2017

Y/Y. More affordable Brooklyn fared better with a 6% Y/Y increase. I have not yet seen more recent data.

Seattle and LA seem to be the better performing major housing markets right now.

It’s amusing when i recall watching Shiller on TV years ago candidly telling an interviewer that “forecasting is mostly guesswork”. True.

Robert Shiller? This guy isn’t even certain what he had for breakfast. They always bring him on everywhere and I haven’t been able to hear one single informative fact from this man. His response is always, it may go down, but no one knows, it might go up, or vise versa.

Even crooks like Yellen or Greenspan will give you a few piece of useful data. So, I’d trust Yellen more than Shiller, and that should tell you how low my opinion of Shiller is.

Shiller was relentlessly negative on stocks in 1999/2000, and on housing in 2007. So too was Grantham.

However, they now seem to be of the belief that markets will bubble up quite a bit more. That’s uncharacteristic of them as they know valuations are close to nose bleed levels.

I’m taking note as these guys are not exactly rank amateurs when it comes to studying boom and bust cycles.

Schiller and Grantham? Sort of like Howard Ruff back in the ’70’s. Write books and preach to high heaven how it was all going straight to hell in a handbasket, then jump on the other ship and ride it to the moon. They use your gullibility as a stepping stone.

I agree with you. What the bears refuse to see is how the market is perfectly under the control of the PPT. This country will go to hell the moment the stock market collapses.

And so it begins It couldn’t go on forever folks Same with stocks Everything reverts to fair value Even Bitcoin lol

Inflection point achieved. Its all down from here.

Don’t bet on it.

Whether or not the rentier class is able or unable to reinflate the SF bubble they’ll be blowing bubbles in other markets to continue their profiteering. Call it a business model.

In the meantime, you’d be well-advised to check your records to make sure somebody hasn’t signed you up for any liabilities, expenses, or anything else, of which you may so far be unaware. You wouldn’t want to start getting notices of fines for late payments on a property you didn’t buy, for example, or find out your bank is foreclosing on your house ten years after you paid off the mortgage.

No, I’m not exaggerating. It truly is amazing what goes on out there.

walter map – OMG this. This kind of sh!t happens all the time. Mostly to the elderly, those whose command of English is not that great, anyone who’s sniffed out as “weak”. Anyone who for any reason is not perceived to be able to fight back.

Here is a list of things that will not just cap real estate prices everywhere, but crash them as you have never seen.

1) earthquake, or unprecedented natural disaster

2) riots, wide spread civil unrest

3) EMP be from the sun or an ‘enemy’.

4) web ransom crash that takes weeks and or months to fix.

5) infrastructure attack, including financial asset records disappearing

6) radiation leaks, containment failures

7) bio plague from CRISPR experiments, Accelerated Genetics accidents by unregulated parties

8) national government crisis

9) mass migration ( ie dust bowl)

and the winner is

10) war

I guess you forgot alien invasion.

What is the agenda of posting this? That only some natural disaster will crash the housing bubble? The interest rates or oversupply is enough; we don’t need your list of natural disasters.

The “agenda” is called reality We haven’t seen much of that commodity in a very long time Long overdue

“The interest rates or oversupply is enough”

Not if the Fed keeps its ZIRP/NIRP policies, and not if bankster continue to keep supply off the market and have the government put their losses on the national credit card.

Lots of things could crash housing markets, but so far interest rates and oversupply don’t really seem to be two of them.

HAhaha, oh man, that made me laugh. Thanks for the Memorial Day funny, even though it’s kinda a bad joke to be made on Memorial Day!

I LOVE doom and gloom. The more doom and gloom the better. If everybody is a cheerleading, I’m worried as F!

Sam

I’m with you Meme, the American people are not prepared for even a minor disruption of services. There are a lot of things that could go wrong and some are clinging by a hair, like all of our nuclear power plants. We’ve got millions of people on mind bending, dehabilitating drugs, even babies. Poison water, food, air. Still we can’t see the forest for the trees. The trees are interesting though.

The tree I see everyday is the total lack of traffic on the roads, this has been going on for several years. It’s the weirdest thing to pull out on the road in the morning and there are no cars.

No traffic on the roads??? You don’t live in the Bay Area….

– If you can do price ROC prior to the year 2000, including the

negative spikes, you might see that 2000 to 2002 bottom set a certain

trading range. I think that 2006 would be a “peak”, 2013 & 2015

are lower highs and now it’s the last time to sell your house, in SF area,

for the next decade or two.

– If you put 5% down payment and the market bust, you win.

If you put 30-40%, the bank win.

The bank is protected from a down market of 30-40%.

Your down payment cover them.

That’s one of the big issues I see now. In the ’08 bust, many people in the Bay Area had 85-15-5 loans where they only put 5% down. If things went bad and you needed to walk away, the sting wasn’t that bad. In fact if you stopped paying and waited for eviction, you’d probably live 9+ months rent free (many people did). I know people that did that and took their rent money and invested while the stock market was bottomed out. They did well.

When I sold last year in the Bay Area, the person that bought put down 30%, I assume to get a conforming loan. A crash for them would sting unless they stay employed and can ride out the crash for a number of years. It could also hamper their mobility if they want to move elsewhere. If they didn’t want to eat the loss, they would need to rent out the place while they wait for the market to recover and who knows if the rent would cover their mortgage payment or not.

What were some of your reasons for selling last year 2016? I thought the slowdown would continue into 2017, and it has for condos. But for single family homes in the north side of SF and the west side (Golden Gate Heights, Inner Sunset, Richmond), demand is off the charts b/c everybody is looking to buy SFHs.

So many people are putting 20% – 100% down now and since 2010 b/c they have to. That is a huge buffer for the next correction.

Sam

Median price of single-family houses is down year-over-year in SF. Demand is not “off the chart” for anything in SF.

In the Marina, median house sale price in 2016 was below that of 2015 AND 2014 (yes, below 2014!). In Cow Hollow, median house sale price in 2016 fell below the level of 2013! And so on. Other areas are also down YOY, some areas are essentially flat YOY (i.e.Central Sunset), and some areas are up YOY (i.e. Inner Sunset). Data via Paragon RE.

Oh, BTW, if you’re waiting for the Uber IPO miracle to drive up home prices in SF… you should know that Uber will move its headquarters to Oakland into the old (and beautiful) Sears Building as soon as the remodeling work is finished.

I assume you mean they’ll have a buffer because they have so much cash (equity) in the property.

The high down payments / all cash offers can be a bit misleading. Some of these buyers use delayed financing or even get informal loans from family members. At the end of the day, this still translates into a liability and isn’t as much of a buffer as you might think. If the buyer loses their job and can’t replace it, for example, they might have to foreclose. (The informal lender – e.g. family member – may be understanding in hard times, but I wonder how many people fall into this category.)

Check out the latest median home price figure for me. Paragon reported it and we are at $1.5 million for a single family home.

This is an all time high by $100,000. I’m in the weeds right now and got a great offer for my Home in the marina and three homes in Golden Gate Heights around me went into contract offer 20% to 25% over asking to new record highs.

Sam

Did you miss this one?

https://wolfstreet.com/2017/06/06/san-francisco-house-condo-prices-spike-home-price-bubble/

Does everybody here suffer from terminal cynicism? I know I do.

I sometimes see myself as someday living in a squalid Hong Kong tenement, banging out unpaid articles on an IBM Selectric for stodgy British economics journals that nobody reads, rejected by a moon-faced oriental beauty who ran off with a street vendor, and ending up hanging myself with a typewriter ribbon.

I must know ten guys this has happened to, all because some mortgage broker said “sign this”.

Michael Hudson and Steve Keen are the experts on bubbles and overlending, anything they write will clue you in to the current situation.

Experts my lily white posterior . Like anything Keen and his group of theoretically addled post Keynesian MTT grifter/con artists have said or predicted has been proven or come to past . Suffice it to say they talk a good talk [ though in reality the majority are in dire need of public speaking skills ] the fact is their walk is lacking in substance or reality .

Nice rant TJ.

If common Sense hasn’t told you we’ve reached the ceiling on home prices Keene and Hudson tell you exactly why.

Toronto is only the first Domino to fall. Capitalism has run out of gas because they’ve run out of resources and fraudulent Financial promises.

Now what?

Ha, you truly think they’ve ran out of fraudulent financial promises? I do believe there’s many more where the last came from.

For those with serious money San Francisco’s trophy homes make sense. Since the first mansions went up on Nob Hill, San Francisco has been the home of the wealthiest Americans ( and now foreigners) and always will be.

OTOH not all of San Francisco is choice real estate. They didn’t build mansions out in the fog belt or along 101. They built middle class and working class housing in those neighborhoods so pretending they are now million dollar properties and will remain million dollar properties requires a lot of faith and zirp.

There seems to be housing bubbles in every western countries right now: Canada, Sweden, Australia, USA, Spain.

It means there is a lot of money being printed to get that kind of bubble that can lift housing prices in such a large scale. I am starting to think that this bubble can go on for another 10 years with all this money printing going on.

Big Canadians banks have come up with another round of good earning.

http://business.financialpost.com/news/fp-street/rbc-cibc-and-td-all-beat-market-forecasts-in-big-day-for-bank-earnings

As long as central banks are printing money exponentially, there is a potential for this to keep going on for a while.

I am starting to feel like a loser for not buying banks stocks.

Doesn’t Pelosi live there? That’s reason enough to sell

A couple of Colorado Public Radio headlines this week related to our escalating ‘ Bubble ‘ troubles ;

1) Denver and Boulder metro area public schools are having a difficult time filling teaching positions * … because the cost of housing [ rent or own ] now exceeds the capabilities of a teachers salary even in the well heeled [ such as Cherry Creek Schools ] districts

2) The last remaining trailer parks in the Denver metro area are scheduled to be plowed under to be replaced by middle and upper middle income housing developments

Which begs the question … what kind of a future can any city have when teachers – labors – tradesmen – restaurant and hospitality workers – hospital and nursing home aids etc etc – et al can no longer afford to live within commuting distance ?

*We personally know of a young teacher from NJ that had accepted a position in one of the better school districts here only to turn it down after looking into the cost of housing etc in comparison to NJ

If inflation keeps going up like it is how; the real inflation between 10% to 20% a year; not government reported lies eventually working will become an expense not a revenue stream.

Eventually the only way to make money will be to give up on the system and voluntary simplicity and detach yourself from the system as much as possible.

We are reaching a point now with all this inflation that working does not bring enough revenues to covert fast raising inflation.

I think Charles Huge Smith pointed out in the past few weeks that the only way to keep your head above water economically is to be part of the rentier class – to own assets from which you can derive a significant income. An earned wage is more often than not insufficient to stay in the middle class in many parts of the US. One could argue the spiraling costs of education make it even more difficult so I can see where your detachment thesis makes sense, especially for the younger generations. I think you also see this mirrored in corporate America, where those who seek to retire are having difficulty finding people willing to replace them – the lure of social security, much less a pension, are unlikely to exist when it comes time to collect. Younger people are not willing to slave at a job whose total compensation will come no where near their what their predecessor enjoyed.

The reset button is going to get hit and hard.

“1) Denver and Boulder metro area public schools are having a difficult time filling teaching positions * … because the cost of housing [ rent or own ] now exceeds the capabilities of a teachers salary even in the well heeled [ such as Cherry Creek Schools ] districts”

This has been going on for a while in San Francisco, with the city trying various incentives but with no solution in sight.

I was picking up supplies at a warehouse in Carpenteria, CA–a very expensive area near Santa Barbara. I asked the owner where his workers live. –Bakersfield–two and half hour drive away. They sleep in their cars during the week and go home on the weekend.

2nd graph is quite telling as looks like housing price went down in 2006 only to bounce back in 2007 (lower high) before 4 yr slow decline to its low in 2011…

I live in east SF bay area and sold my house in July 2016 I bought in Nov 2011. Of course prices crept up by another 5% and heck there are dearth of inventories in my hood where houses are sold in couple of weeks. I think the market is simply running out of suckers as the Greater Fool Theory will prevail cos peak investor and Chinese buyer came and went leaving lemmings to learn a lesson or 2.

All of this is the result of globalization. Yes the market – any market – will crash and yes it will again recover. We act as though these cycles have never happened before and when things turn down it will last forever. Come on people. Get real. Scary to read that some want controls. Well who or what provides these controls??? Yep, it’s that horrifying thing we call government. Get that creature involved in anything and true disaster ensues every single time. Free the markets and let the markets go where they will. Some win while some lose.

I would shoot myself if I have to live in San Francisco.

Look at San Mateo; by no means San Mateo comes even close to even good old San Jose, let alone Mountain View or Sunnyvale; yet the wealthy live in San Mateo; why? Cause someone told them San Mateo is where the wealthy live. San Mateo is dirty, old, and most people are ugly like hell; I want to puke each time I go to San Mateo, yet, prices are through the roof. A lot of idiots even amongst the rich which begs the question how the hell they got rich in the first place.

Demographics and no property taxes due to prop. 13.

The aging population in SF and the bay area are trapped.

They can’t move and afford the new taxes, much less the new home, so they stay until they die and there is no inventory

I live in an upscale bay area community with the top schools and in the six houses surrounding me the avg. age is 67 and I am the only one who works.

Pretty much. Camp out in your home till you die and pass on your unrealistic property tax to one of your kids thus locking that home off the market.

In meantime make it a poor choice to down size because the carrying cost on the smaller home will be higher due to a tax reassessment….

Taken from DailyMail (they cited WSJ):

“Around 80 per cent of millennials have saves less than $1,000 towards buying a home, while around forty per cent of 24-35-year-olds save nothing at all.

Inflated house prices and stagnant wages – millennials earn 20 percent less than boomers did at the same ages in 1989 after inflation – mean that home ownership is moving further out of the grasp of every day Americans.”

https://www.wsj.com/articles/millennials-want-to-buy-homes-but-arent-saving-for-down-payments-1495731583?mod=pls_whats_news_us_business_f

The US has been exporting inflation ever since the end of Breton Woods. Remember Nixon’s treasury secretary? that guy who said it’s our currency and your problem?, now the world is exporting inflation here……well, karma’s a bitch ain’t it?

How does San Fran compare to Vancouver in terms of year over year home price appreciation over the last 20 years?

I’ll bet SFC is only just starting and that even as tech wanes, they’ll open their arms to the near UNLIMITED, UNREGULATED flows of billions of dollars from China. The Canadians have dropped the ball and that money is likely flowing south.

You don’t need Facebook or google to make SFC great. It was great long before tech grew there.

Yeah, with all the new condos being completed, job market turning south, and Chinese government putting all the stops on capital flight, it makes sense in investing in San Fran housing and lose a few hundred thousand or a couple of millions depending on what you want to buy.

“UNLIMITED, UNREGULATED flows of billions?” That stream is drying up fast.

SF has always been expensive since the gold rush days. It will always be expensive. All we discussing is by what magnitude at any point in time. Once you get past the geography and weather there is a non ending demand curve of people from all over the globe tht want to live here. The Summer of Love, silicon valley etc didn’t happen by accident. If we go into a depression, at some point we will, SF will still maintain its price premium. I have been listening to SF been absurdly over priced for more than 45 years now.

I guess you were on vacation in 2010. 27% drop wasn’t as fun and funny as it sounds when you have a 2 million dollar house in San Fran; that translates to $540,000.

By the way, if government had not intervened with free money for all rich people to buy up homes in San Fran, that 27% drop could have very well been 54% drop. But thanks to Obama, the likes of Blackrock got free money to buy up properties they can now sell at 2-3 times the price. Once the crash comes this time, it will be 50% drop since money printing won’t be one of the available tools this time.

@R2D2 Agree that San Mateo is nothing to write home about. A 50% drop would be awesome…unfortunately, there are just too many Billionaires, too much VC money, and endless job openings in SV for the housing market to return to normal in San Mateo County imho.

27% drop so what, it proves my point. The rest of the US, even parts of the East Bay dropped 50% or more. Then when the recovery started SF immediately, compared to other locales, went to new highs.

SF saw about a 15% price drop MAX. I was hunting aggressively and there weren’t that many deals. People just held.

Sam

That’s false. Median price fell 36% in SF. The house I bought here in 2011 was 42% less than it sold for in 2003.

There may come a day when Millennials in San Fran or around the country band together and quit paying taxes. People shouldn’t be forced to repay debts others, or be forced to fund financial windfalls of the already wealthy, period. Any system that supports this is completely broken and deserves to go.

Hi Wolf,

Thanks for your analysis. May I ask how long you’ve been bearish on SF property and when was the last time you were bullish, if ever? It helps to gain some context given I think you’ve been bearish for the past several years now.

I think SF is one of the cheapest international cities in the world.

Thanks,

Sam

I turned bearish on the San Francisco housing market in February 2016, based on the housing units in the pipeline and the slow-down in employment growth, combined with prices that far exceed what most households can afford.

https://wolfstreet.com/2016/02/25/bust-royale-for-insane-san-francisco-silicon-valley-housing-markets/

In about 2013/4, I started pointing out how the SF market was turning into a bubble (which is VERY bullish because prices soar). So clearly, you haven’t read my articles for “the past several years.”

Thanks for clarifying. I must have recalled some different bearish article from several years ago that just stuck in my mind then. You’ve got to admit that you have a pretty bearish theme dominating your site, which i like and need since it allows me to see the other side.

Does this mean you have sold your properties?What is your property ownership history if any? Helps provide context. I own three properties in SF currently for your reference.

I’m thinking about selling my marina single-family home this month actually, but I keep thinking I’ll regret the sale 10-20 years later. The house has performed well since purchase in 2005, and it still seems relatively inexpensive compared to New York City, Hong Kong, Singapore, Paris, etc. based on the amount of job growth and international demand there is. But I’m older and less patient dealing with tenants and the city taxes and stuff now.

Within three years, we know that Airbnb or Uber or both will go public, creating a multibillion dollar windfall into the San Francisco Bay area. Plenty of that money will go into buying real estate, as we saw in 2012 after Facebook went public. Given less than 1% of the housing stock trades, I see a shift up in demand and prices post IPOs.

Thoughts on this upcoming catalyst? Ii’m really, really torn and have a decision to make regarding the counter offer by midnight tonight on whether to accept and sell or just hold on and pass the property to my children and suck it up.

Thanks,

Sam

I don’t give financial advise as a matter of principle. I don’t get paid for it :-)

As you know, each property investment decision has be to made in its own context. If you owned the property for 30 years and didn’t refinance, that’s one context. If you bought it in 2014 and have a huge mortgage on it, that’s another context. But you bought it in 2005, so you’re kind of in between the extremes, and in a more nuanced situation. I can understand why this will not be an easy decision to make.

Certainly now is a good time to sell (prices are very high). But as you said, 10 years from now, it may even be a better time to sell; or any number of other things could happen that will make it a terrible time to sell.

As you know, if you buy a property at the right price (not near the peak of the bubble) and take care of it, you can get through many ups and downs without major problems.