Santander, top subprime auto lender, verified income on only 8% of loans: Moody’s.

“Liar loans” were a factor in the housing bust during the Financial Crisis that brought down the banks. Bank regulators now require lenders to verify income and employment of mortgage applicants and take other steps to make sure buyers can afford the mortgage payment. But in auto loans, no such requirement exists. So here we go again…

Moody’s Investors Service analyzed $1 billion of Asset Backed Securities (ABS) backed by subprime auto loans that Santander Consumer USA Holdings, one of the largest subprime auto lenders, had issued. “Subprime” means the borrower has a credit score of 620 or below. Turns out, Santander had verified the income of the borrowers on only 8% of the subprime loans.

Moody’s found other lapses, including loans with very low or no credit scores and no co-signer.

Back in February, Moody’s had rated these subprime-auto-loan-backed securities as high as Aaa. Among the institutional investors that bought them was Massachusetts Mutual Life Insurance, according to Bloomberg.

Moody’s contrasts Santander’s lack of even basic due diligence, such as verifying income and employment, with an auto-loan based securitization issued by GM’s finance subsidiary AmeriCredit. Moody’s compared the two because they are the top issuers of subprime auto-loan ABS. Turns out, AmeriCredit had verified income on 64% of the loans in the securitization. Bloomberg:

Data tied to Santander show that it packaged riskier loans into bonds, as seen in higher loan-to-value ratios, longer maturities, more used cars, lower credit scores and a greater percentage of loans granted to borrowers whose incomes weren’t verified, Moody’s said.

The report said that the missing verification of income and employment “creates more uncertainty around whether borrowers will be able to afford their monthly payments, which becomes particularly important if they have poor credit records and risky loan terms.”

Lacking income and employment verification compounds a problem that UBS had pointed out last week: about 20% of auto-loan borrowers had admitted on a survey that their loan applications contained inaccuracies. The report suggested that loan fraud could be a bigger problem than lenders are prepared for.

The UBS report also found that borrowers are getting better at manipulating up their credit scores via tactics they learned by Googling them. As a result, credit scores have been broadly rising, though actual credit risk may not have improved in parallel. Thus credit scores have become less reliable as a predictor of default, and auto lenders may have more risk in their portfolio than they think. The report warned: “Loan terms are stretched out, interest rates are aggressive, but there may be an over-reliance on credit scores, and that’s the danger.”

Moody’s pointed out that the missing due diligence may be one reason for the higher loan losses experienced by Santander’s securitizations.

So far, investors in these bonds have been protected against losses by an extra loan-loss buffer that Santander built into the bonds, Santander treasurer Andrew Kang told Bloomberg. Up to a certain point.

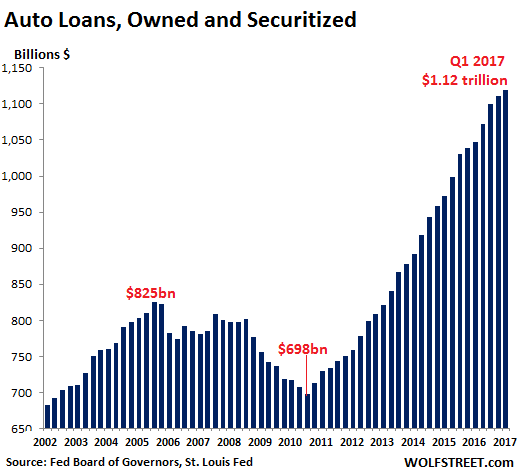

The findings by Moody’s and UBS explain to some extent the surge in auto loans in recent years. The boom in debt, made possible with easy credit and loose underwriting standards, has funded record auto sales. Auto loan balances outstanding have soared nearly 60% since 2010, to $1.12 trillion:

The risks are packaged into the $1.12 trillion in loans. Default rates on subprime auto loans are shooting up. Fitch Ratings reported earlier this year that its subprime Annualized Net Losses (ANL) index had jumped above 10% for the first time since 2009.

Santander already got into hot water for making loans to customers who couldn’t afford the payments. It settled the allegation in two states for $25 million. Bloomberg:

Around 42% of Santander Consumer’s subprime auto loans made between 2009 and 2014 by dealers identified as “high risk” in Massachusetts and Delaware have defaulted or will default, an amount that is substantially higher than the losses in the overall lending portfolio, Moody’s said in a separate report. “Information in the settlements indicate that some loans in these deals were underwritten based on inflated income and inflated value of collateral,” according to Moody’s.

And it’s just the beginning: 30 other states are probing into its underwriting and securitization activities, according to Santander’s most recent 10-Q filing.

A broader side effect is that customers may be stuck in cars whose payments they cannot afford, or can afford only by curtailing other essential spending, which puts an additional damper on consumer spending in other areas.

While subprime auto loans are not big enough to tear up the financial system, they’re big enough to dent new and used car sales. Any pressure in used car sales may cause further erosion of used car wholesale prices, pull the rug out from under new car sales, wreak more havoc among rental car companies, hobble auto leasing companies, and spread turmoil among automakers.

The Office of the Controller of the Currency and other bank regulators have been fretting about auto loans for the past two years. Now lenders seem to be getting the drift and some have started tightening their lending standards. This pressures already falling auto sales and spreads more pain in an industry that accounts for over 20% of US retail spending. It impacts manufacturing not only by automakers but also their vast network of component suppliers. It impacts railroads, trucking, and the finance and insurance business. Since the Financial Crisis, the booming auto sector has been a hefty prop under in the wobbly US economy. But last year, the prop cracked. And this year, it’s crumbling.

The #Carmageddon data is just relentless. Read… Used Vehicle Trade-in Values Sink, Hit New Vehicle Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Back in February, Moody’s had rated these subprime-auto-loan-backed securities as high as Aaa. Among the institutional investors that bought them was Massachusetts Mutual Life Insurance, according to Bloomberg.”

WTF? So good, working-class people are buying life insurance as a conservative investment for their future from Massachusetts Mutual Life Insurance who is taking their money and buying fraudulently produced ABS fraudulently rated by Moody’s. And no one goes to jail.

Boy, this stuff wouldn’t happen if we just had a Free Market with no government regulation!/s

By starting at $650B instead of 0, your graph is very misleading.

It looks as if these loans went up ~500% but in reality it is less than 100%.

That’s the standard way of doing it. Charts have to make sense. You have to be able to see the movements. These are not “percentage change” charts, which are different but also common. Here’s the standard chart of US GDP for the past decade by the St. Louis Fed. Note that it starts at “13,000” ($13 trillion), and not zero.

https://fred.stlouisfed.org/graph/fredgraph.png?g=dPUS

There was a similar comment from someone else when this Fed chart was first presented a few months ago.

My response was, (not that Wolf’s was inadequate – I hope he doesn’t mind) :

“A bar chart beginning about zero, and representing auto credit would have to begin about the year 1900, approximately when the financing of horseless carriages began, but would not be relevant to the recent credit boom-bust-boom years under discussion.

[ … ] it would be interesting to see such a chart if the subject was the history of credit in the auto industry for the last 116 years.”

Not quite, but close. It would have to stretch through several web pages, but can start any year, i.e. it does not make sense. The alternative would be to use logarithmic scale.

Uhhh…maybe not.

I doubt people who can’t make sense of a truncated bar chart are going to be able to understand a log chart.

less than 100% is still a lot.

easy credit has led to a lot of sales, which eat into the future. credit will get tighter, which will slow sales, while used cars will depress prices.

uh, i think i am being obvious, but buying the bonds at the right price might work.

but not my area of investment.

“Santander already got into hot water for making loans to customers who couldn’t afford the payments. It settled the allegation in two states for $25 million.”

I notice many banks and lenders pay fines like this for their fraud. What I would like to know is where these fines go?

‘What I would like to know is where do these fines go?’

for the ‘regulators’ : bonuses, strippers, … and porn ! Am I missing anythng ?

for the head financials : caviar, more spacious yachts, only the best booze and drugs, …. Oh, and even MORE ASSETS & WEALTH !! What’s not to like ?

Just look at Citi Banks(ters0 most recent wrist slap …. ‘all the world a farce !’

I suppose you have never heard of Champion Mobile Homes. Why not take a look at who owns them and their ‘loan and repo’ practices. While you are at it get some donuts and coffee, and maybe a taco or pizza. How there is a story the media will never never ever print.

But these loans could be put into Blackrocks new magical ETF so broke ass mom and pop could play the odds.

just saying….

This is the kind of thing Warren Buffett is into, predatory mobile home loans and such things. I don’t know why anyone thinks he’s a great guy when all he’s done is put a layer of yes-men between himself and the welfare mothers he preys on.

It’s because 99 percent of the public only see the Great old wise uncle Warren that shills like Becky Quick salivate over on the boob tube They don’t have any critical thinking skills whatsoever Sadly

AAA rated dog crap. Almost as bad as “the full faith of credit” in the US Dollar and US Treasury bonds.

Yup pretty good comparison there Mike

Hmmm,

With the extreme push of first, drivers by Uber, partnering with Stantander, while pushing the self driving car concept, but in the meantime, Obamas cash for clunkers while helping the automakers with sales in the short term, will put them right back in 2008 crash territory.

Now that the lease contracts are ending and and dealers are the engaging in “Channel Stuffing” what will happen to Uber and the Auto Manufacturers when the next recession hits?

Uber is completely screwed, in regards to the Waymo lawsuit and are trying to get traction to prevent being down rounded.

I guess what I’m asking Wolf and the readers is this; Are we looking @ a massive transportation and rideshare bubble?

Thanks, Gustave.

A few months ago, I was speaking to a auto Repo guy in East Oakland Ca, & he said the majority of the vehicles repossessed were Ubers, the dealers were begging him to stop because the lots were overflowing with them, I expect nothing has changed for the better…

Uber has a program where if you want to drive for them (for that $weet $10 an hour I guess) but don’t have a car, or a new enough car, that’s OK, they’ll sell you one, paid for by their loan company. Talk about being owned by the company store! I’m pretty sure this is how a guy I know, who has found Uber to be a way to finance his drinking and driving, is driving around in a new Prius.

owning the company store can backfire.

were i to cab, it’s lfyt.

I can’t believe how many new European luxury vehicles I see here in Portland with an Uber/Lyft decal (particularly Mercedes GLAs.)

– So, even Uber drivers are having trouble to make their carloan payments. OMG.

– I am not surprised to see this happen especially when knows how flimsy the driver’s “profit margin” is. The bulk of the revenues goes to Uber. And this called the “sharing economy” ?? Bolderdash. This is what predatory capitalism is like.

– And what’s the organisation that is supposed perform oversight on this kind of lending ? To enforce the laws for carloans ? The (paper tiger called) SEC ?

Nope. SEC does not regulate car loans. Essentially (by design) nobody does.

Congress (the guys you voted for) created a carve-out in Dodd-Frank that essentially leaves the auto financing business unregulated – that was the explicit point of the carve-out.

The Consumer Financial Protection Bureau (CFPB) is trying to wiggle around the carve-out to get into the business of regulating car loans.

There has been no oversight on anything is 8 years…period.

Look around, I see no bankers in jail.

We ALL know the problems, but it is fun hashing it out instead of lashing it out on some deserving backsides. Strike that, make it just backs.

The bosses of those who put people in jail are bankers; so, you can’t put your own boss in jail, can ya?

If we look up the chain high enough, we’ll find out that all the presidents, kings, and queens ultimately report to the master banker.

If you go to open secrets dot org you can see who owns “your” representatives, i.e. their main campaign contributors.

They do not work for you and me.

Barak Obama is cashing in to the tune of $400,000 per speech for being a Wall Street water carrier. Attorney General Eric Holder got set up in a nice corner office with a $2M a year salary as his reward for ensuring no bankers went to prison for causing the 2008 financial crash, and had the unfettered ability to loot and defraud the public with impunity.

If you like your crony capitalism, you can keep your crony capitalism.

Where the heck is Jon Corzine? If anyone deserves three hots and a cot in Leavenworth It’s that crook

The SEC is the most singularly worthless of all our captured, co-opted regulators and enforcers. They are completely in bed with the shysters they’re supposed to be protecting the public against.

Alta road runs north from the Otay border crossing to access Donovan Prison and San Diego County jails.

For 10 years there have been signs selling land with no takers.

In the last six months acres of gravel lots are appearing where there was once chaparral.

Filled with factory fresh Hyundais. The lots are getting bigger and bigger and the cars dustier and dustier

Wow! It seems you’re regularly driving down this road. If yes, could you take some photos of these lots and send them to me. I’d love to publish this with a comment from you.

Several auto auction businesses in the Alta rd area. So there are always alot of cars in lots.

I looked at the photos. The cars are brand new with the white protective foil from the factory still on the hood and roof – a sign that they haven’t been prepped by the dealer yet. These are not auction cars. They’re headed for new car dealers that apparently don’t have room for them.

I was reading how auto insurers are going to raise rates on older cars that do not have the collision avoidance systems that are built into the new ones. While that might help new car sales to the extent insurance premiums are a factor, it certainly will make buying a used car less attractive.

A $10 or $20/month premium difference adds up over a 72 month payment plan.

i would hope the insurers would offer discounts for accident avoidance systems rather than increase rates for cars without.

I have a10 year old car with 35k miles (I am a senior) mint condition, –my risk level is low,

but then again let the government into home and auto insurance next so it can screw up risk ratings and premiums on that.

Next, why do I have to pay uninsured motorists premiums when the laws state you can only drive if you have insurance.

most government elected officials are either corruprt of inept of both and employees, frankly , do not get pushed for optimized performance like they woudl get pushed in many companies.No accountability either.

BTW–St Louis Fed Fred graphs allow changining the time frame-rectangle box at bottom of chart

the best analysis there is to overlay GDP vs Debt growth from 1947–visually you can see how coincidently things got out of hand August 1971, but really blew up starting 1981, then 1993, then 2001, then 2009-blew up means debt growth is running around 10% while nominal GDP running at 2-3%-bad karma folks–

lord knows whats coming

Hello. No worries, I can do that if you would like. Yep, I have worked connected to California Corrections ( oxymoron) for over a decade.

Maybe a trade if you’re feeling like a bit of research. A correctional officer I work with recently said Cali passed a law to release nonviolent offenders to reduce inmate populations. Ok, sure… one small detail though. A drive by shooting is no longer classified as a violent crime here. Unless a bullet hits someone. Then it’s a violent crime. I haven’t looked into the A.B. but the recent 40% drop in detainees makes me think it’s true

Great. Thanks.

Here is the deal on the inmate release program:

Based on the approval of Proposition 57 at the last election in November (remember?), the Legislature passed a law that would cut prison population by 9,500 inmates after four years (or by about 7%). Releases have lots of limits.

http://www.latimes.com/local/california/la-me-california-inmates-20170324-story.html

The prison system is trying to make room for the executives at Wells Fargo … just kidding :-)

Not a single banker went to jail for causing the 2008 financial crash, despite massive, systemic fraud and criminality.

Eric Holder said we couldn’t go after the TBTF banks because it could cause systemic damage to the financial system.

Eric Holder now occupies a corner office on Wall Street and is pulling down a $2 million salary that looks a lot like payola for services rendered while a “public servant.”

The .1% are literally above the law in our crony capitalist wonderland, and they know it.

@Gershon,

Decades of propaganda to worship private sector CEOs has left us here.

Notice the regulators dont notice this stuff until the bubble is popping, despite having years to do so.

That’s because all these companies are part of the system, as are the regulators, all one happy family.

They all know the plan, and play their role. Work the bubble to the last drop, then pretend they just found out there’s a problem only after all the money has been made and the damage done.

Media plays its part by couching their actions with terms like “dumb” or “out of touch” so people think this is all one big accident by incompetent bankers and lenders.

Nothing could be further from the truth.

Works every time.

I suppose, Santander securitized these loans, sold them to yield starved investors who do not have any choice, e.g. pension funds, who bought CDS from a trusted party. Just like the last time?

Now for a higher level of insanity! If that’s possible.

Blackrock has just announced their intention to form an ETF;

“iShares Consumer Asset – Backed Securities ETF”

Exactly what assets you ask?

Consumer Loans

Credit Card Debt

Student Loan Debt

Just when you thought things could not get anymore Bizzarro!

OutLookingIn :you chimed in before i did on this. Securitization bundles these loans up via a “special purpose entity” into a tradeable instrument. These SPV’s reside on the income/revenue side. The liability is removed from the balance sheet of the creator and administrator which make money on the net interest spread. In the above narrative these would be santander and GMC . they are now “off balance sheet” and transfer risk to the security purchaser (i.e insurance companies). A remarkable bit of financial engineering. Enron was notorious for using ‘off balance sheet’ accounting . here is a link to GM explanation: i wondering what “hot potato” loans blackrock wants to remove from their balance sheet ?

https://www.gmfinancial.com/Docs/About-Us/understanding-securitizations.pdf

“..Enron was notorious for using ‘off balance sheet’ accounting .”

Please show me one company on any exchange that does not do this. Now show me one company that did not get away with doing it. and has been prosecuted by the SEC or DOJ. A joke all..

If you invest in deception, you end up with fantasy.

Blackrock is taking the securitization process for consumer loans one step further. from what i can glean their newly proposed etf could purchase SALLIE MAE asset backed securities (i.e student loans) . this etf would be traded on an exchange . I suppose the etf could also purchase subprime auto loan ABS’s. could it be someone wants these securities off their balance sheet. ? it seems that credit risk keeps shifting to the stock market in today’s brave new world .

Lenders know the Fed and middle class taxpayers have their backs. They can lend and speculate with reckless abandon, while lavishing obscene salaries and bonuses on their CEOs and corporate officers.

Isn’t crony capitalism grand?

Seeing Santander up to their necks in this pile of poo is somewhat refreshing. Until recently, if you smelled something this possibly-not-quite-legal (i.e. crooked), Citibank would be wallowing in the middle of it, generally accompanied by BofA.

Hard to tell if the US banks are now better behaved. However, a good way to evaluating investor sentiment regarding bank financials (essentially quality of internal risk models & management’s judgement regarding loss reserve estimates) is market value divided by book value”: a ratio >1.0 is favorable; a ratio <1.0 means investors don't believe the financial statements.

U.S. Bancorp leads the pack at 2.07; as expected, Citi Bank (about 0.95), BofA (about 0.65) and Wells Fargo (about 0.55) are way behind in investor confidence.

Lest we forget Santander is far from the worst when it comes to subprime auto loans . That honor falls firmly on the shoulders of the one at the forefront of sublime auto loans … Ally Bank … formerly GMAC Financial . Yet ironically despite both Ally and GM’s overwhelming activity in the world of subprime auto loans .. nether has yet to be called on the carpet … by anyone . Now why is that ?

I worked for GMAC (back when there was a GMAC and when they knew what they were doing, for the most part anyway ) in the early 1980’s. I worked for a couple of years in the field doing delinquent auto loan collections, workouts and when necessary, repossessions. I also did GM dealership inventory audits.

Then I got moved into the office where I ‘dialed for dollars’ most of the day every day and at least two nights a week, often three and sometimes four, usually until 8 pm local time, making 100+ collections calls per day, every day. I did that for about a year and half then I left and went to work for a regional bank where I did their consumer dept. collections for about a half a year before I moved into a consumer lending position where I did the bulk of their indirect (auto dealer) loans with local dealers. I still did the bank’s auto loan collections part time, usually dialing for dollars one evening a week and making the occasional personal collection visit as needed.

This lasted until the early 90’s when I got out of banking and moved on to other things because banks had lost their way. They moved from a customer service business model to a sales model and I refused to be a part of that so I walked away.

In my opinion it is also when lenders lost touch with their customers and thereby lost the ability to work out of difficult financial situations when they arose. There was no relationship there and therefore no basis for salvaging those situations. Banks/auto finance companies said ‘screw them, just repo it, sell it and write off the loss’ and customers said ‘screw them, just come and get the car and I’ll go buy another one”.

My point is I have a lot of collections and workout experience in the auto finance and banking world so every time I see a story like this, I wonder how many of these fraudulent lending decisions could be prevented (and how much money saved) if they actually had experienced lenders making these decisions instead of commission-incentivized people who only look at a credit score (credit scores are a joke, imho) and likely just ‘approve’ the computer-generated ‘recommended approval’ while not having the slightest clue about consumer lending, nor do they care.

Then there is the apparent lack of human-contact collections and workouts being done by anyone. Again, how much money could be saved/salvaged here? I guess nobody does that any more except the friendly local independent bank and they are presumably smart enough to have not made many of those types of loans in the first place.

Back in the early 80’s there were a lot of GM dealers on the ropes – bad economy, sky-high interest rates (remember the old 0.9%, 1.9%, 2.9% factory incentive lending programs via GMAC, FMC and Chrysler Credit?) and also because GM was building a lot of crap back then – and as collectors, whether in the field or in the office, we were workout specialists as much as we were collectors.

I repo’d a lot of cars but could have repo’d a lot more. Instead, we would actually talk to our customers and if possible, work something out. GMAC had an extensive, nationwide collections network so sooner or later we would find somebody if they decided to skip but for the most part the problem accounts involved unemployment, reduced income or some sort of family hardship.

Those were in the days before people were identified as ‘sub-prime’ but if that classification had existed, many of the people I contacted, especially in the field, would have been ‘sub-prime’. We used to shake our heads at the ’30 x 30 Club’ members – those customers who were 30 or more times over 30 days past due on the same loan, often a 48 month loan – quite a feat! But, they weren’t going anywhere so we worked out of those deals one month at a time as long as the customer played it straight and made a genuine effort to keep paying. On the other hand, those with no interest in paying and who thought it was all a game were introduced to pedestrianhood as necessary.

Also remember that in those days auto loans were recourse deals which meant that when a vehicle was repossessed and returned to the selling dealer while it was less than 90 days past due, the dealer had to pay off the GMAC loan and eat the inevitable loss. Since many dealers were already in tough shape financially, a month where they got back even two or three repos could put them on the brink of going out of business.

Recourse deals actually went by the wayside during that time, about ’83 or ’84 as I recall so collections practices tightened up after that. After that, we would drag the repo into the dealership, they would recondition them and sell them for GMAC (or the bank) and the bank would write off the loss and attempt to collect it as a deficit balance.

When these auto finance companies or banks have no skin in the game because they can dump these loans into investment products and sell them to somebody desperate for a higher than average rate of return, of course they are going to make poor decisions, including fraud in some cases. What do they care – they don’t take the loss and nobody ever gets prosecuted for that behavior so what the hell, why not! When I was in banking I had to sign fiduciary responsibility documents that essentially said if I committed lending fraud I was going to jail. It wasn’t difficult to understand!

Make the original lenders keep this crap on their books for at least two years, collect it, work out of it and repo and resell it at a loss and their lending practices will improve, assuming they can find qualified people who know how to actually make a credit-worthy loan and people who know how to collect and workout of problems. Apparently that is a lost art.

Yes, I know many loans are unworkable and need to be concluded by repo but it is hard for me to believe that a significant portion of them couldn’t be salvaged. And with new car dealerships lots flooded with inventory they can’t sell and used car lots overflowing as well, I would think the manufacturer’s finance companies (e.g. whatever GM is calling their GMAC equivalent these days) would be looking at every way possible to keep vehicles in buyers hands once they finally sell them. I guess that is not a realistic option in today’s world.

Instead, the manufacturers just do what Ford did and fire the CEO – make him the fall guy and act like everything will now be fine because there is a new guy in charge.

It is getting harder and harder for me to make any sense of this country and how things are done anymore, not just in the world of finance but things as a whole. I must really be getting old!

Stepping down from soapbox now …

Thanks for sharing. Interesting insight/history.

“Santander already got into hot water for making loans to customers who couldn’t afford the payments. It settled the allegation in two states for $25 million.”

The Financial Industrial Complex is of course exempt from fraud and racketeering laws, but they can still be required to pay dues.

Even the shadiest loan practices carry no risk because when the worst happens the lenders can simply have their government subsidiaries bill their victims.

Many countries do not have an actual government per se, and are instead run by organized crime syndicates.

Why should we tolerate impure and harmful “ingredients” in our financial products such as CLOs/CDOs, any more than we tolerate impure and harmful ingredients in our food supply?

It seems entirely feasible to require that all loans or other obligations bundled into CLOs/CDOs or other “sausage” products, sold interstate or internationally, must have 100% of the underlying loans/obligations income and “plausible repayment capacity” verified.

By addressing first one “bundling” abuse and then another, all we are doing is playing “whack-a-mole,” when a complete solution is required.

This in no way would limit the ability of an individual to lend or borrow money on what ever terms they wish, but such loans could be “bundled” and sold interstate only if every borrower’s income, plausible capacity to repay, and value/existence of collateral was verified when the loan was issued.