This is how.

We have long lamented the persistent understatement of soaring US housing costs in the Consumer Price Index, and thus the understatement of overall inflation as experienced by people with a roof over the head. But now two economists from the National Bank of Canada spell out their doubts about the housing inflation component in Canada’s overall CPI.

The Consumer Price Index in Canada rose 1.6% in April year-over-year seasonally adjusted, Statistics Canada reported last week, same as in March, but down from 2.0% in February. Over the past four years, CPI inflation ranged from 0.4% to 2.4%.

For inflation lovers, it was too tame. But Canadians – like Americans who’re in a similar boat – have long complained that life overall is getting a lot more expensive a lot faster than reflected in the CPI. And a big part of that expense is housing costs for owners and renters.

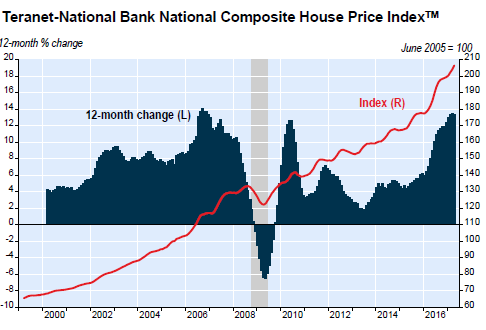

Canada’s house price bubble has become one of the hottest and longest-running in the world, having barely dipped during the housing bust in the US. The Teranet-National Bank House Price Index, which uses a similar methodology of sales pairs that the Case-Shiller index in the US uses, has surged over 100% since 2006 (red line, right scale). The year-over-year increases in much of 2016 and all of 2017 have been in the double digits (blue columns, left scale):

Everyone except the housing industry is fretting about Canada’s house price bubble – from international organizations to the Bank of Canada. The provinces of British Columbia and Ontario have undertaken drastic measures, given the limited tools they have, to put a damper on the house price bubbles in their main urban areas, Vancouver and Toronto. And just today, a Bloomberg View article proclaims, “Canada Must Deflate Its Housing Bubble,” and “The central bank needs to raise interest rates, and soon.”

That has been the obvious but ignored solution for years. Now some observers and the housing industry are saying wait… inflation is only 1.6%; why raise rates?

StatCan’s CPI report detailed that “shelter costs” rose only 2.2% in April year-over-year, same as in February and March. “The homeowners’ replacement cost index (+3.9%) was the main upward contributor to the 12-month change in the shelter index, despite slowing growth since November 2016,” it said. That’s like so benign – compared to reality.

Stéfane Marion, Chief Economist and Strategist at Economics and Strategy at National Bank of Canada, and Matthieu Arseneau, Senior Economist at the same shop, came out with a note today debunking the low rate of housing inflation and the low rate of overall inflation:

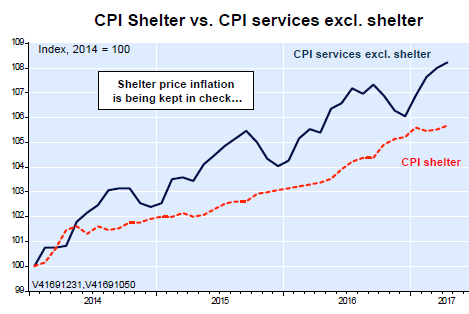

Canadian CPI inflation continues to surprise on the downside despite robust GDP growth, low unemployment, surging home prices, and a depreciating currency. What’s helping keep inflation down? Shelter costs!

This heavyweight component of the CPI (27% of the index) is currently growing an anemic 2.2% annually compared to a more robust 2.7% for all other services (a two-year high by the way).

The note points out that the price of shelter was “only up a cumulative 5.7% since 2014 compared to 8.2% for all other services (that’s a sizable difference of 44%).” In other words, the CPI shelter (red line) rose more slowly than CPI for all other services (blue line):

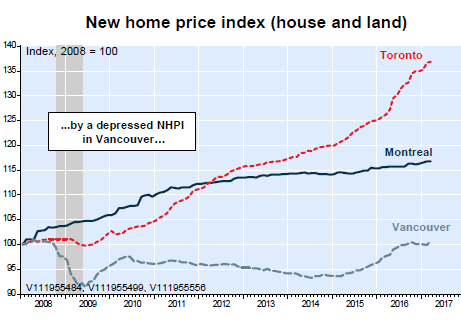

In order to understand the divergence, we dug a little deeper and found that the new home price index (NHPI) for Vancouver that is used in the CPI calculation [dotted blue line] is essentially unchanged since 2008 for both its house and land components

As a result, the Homeowner’s Replacement Cost component of the CPI (20% of shelter costs) is no higher in British Columbia than it was in… 2005!

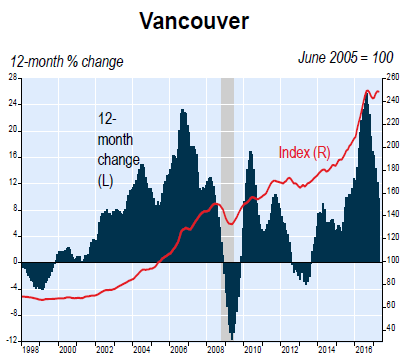

Yet home prices, according to the Teranet-National Bank index for Vancouver have surged 80% since 2008:

The National Bank’s report goes on:

Note that the NHPI is also used for the calculation of the Mortgage Interest Cost component of the CPI (12% of Shelter costs) which, incidentally, remains stuck at a decade low.

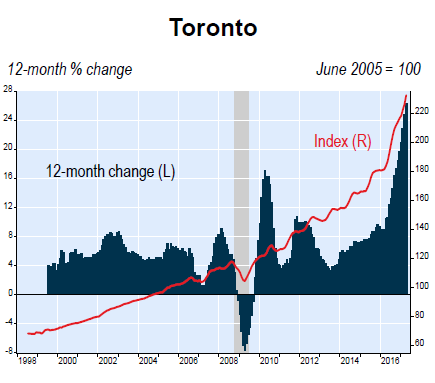

We are also baffled by the reported cumulative increase of only 37% for the Toronto NHPI since 2008 (vs. 118% according to resale market data).

This chart of the Teranet-National Bank house price index for Toronto shows that 118% surge since 2008 in resale prices in all its glory:

So the note concludes:

Also helping keep inflation in check, the Rent component of the CPI (22% of shelter costs) shows rent inflation averaging near a record low of 1% in Toronto, Montreal and Vancouver. Bottom-line: Shelter Cost inflation reported in the Canadian CPI report is eerily low.

“Eerily low” may be one of the best descriptions I’ve heard – and from the Chief Economist at the seventh largest bank in Canada – to describe the housing inflation component of CPI and overall increases in CPI. This principle of understating the increases of the actual costs of living by understating the impact of soaring housing costs is also true for the US where the housing component of inflation and therefore overall inflation as measured by CPI remain “eerily low” as well.

What are Canadian homes and mortgages actually worth when push comes to shove? Read… Chilling Thing Insiders Said about Canada’s House Price Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Meanwhile, Home Capital keeps drawing down its lifeline as depositors keep pulling out their money.

Securing lifelines at usurious interest rates while funding subprime borrowers doesn’t seem like a viable long-term strategy.

$1.35B left on the $2B loan and $1.325B bond payment due 5/24, ouch……

Actually, they drew down $1.4 billion in the first two days after the $2 billion loan from the Healthcare of Ontario Pension Fund was approved.

Now there’s only about $350 million left of the $2 billion line of credit. They drew down $250 million more the other day to make a payment on a $325 million dollar bond that was due today. So they’re paying maybe 20% interest on a loan to pay off a loan. (The interest rate drops on amounts over a billion – up to a billion it was 22.5%).

We will have deflation in real estate, stocks, bonds and in health care and education costs once this hideous bubble pops ….. and not a minute too soon.

Stealth inflation meanwhile goes no where and it continues to incrementally give you less for more money in food, fuel and other staples.

Was in Home Depot on the weekend. Electrical department.

10 half-inch lock nuts in a sealed plastic bag. I dug down to the bottom of the bin. 15 nuts in the previous bags. Price per bag the same, quantity drops by 1/3, hence 50% inflation. Inflation every where.

I have to have a skin cream from Glaxo. Used to be 500g per bottle. Now 450g and the upfront price is up also. Translation 20% bump in prices.

That low inflation rate isn’t the only eerie financial anomaly.

Another is that households with investable assets under 100 K are least likely to use advisors. So why does oversight ignore it’s duties in protecting retail investors using discount brokerages including large bank owned entities. Clearly the less in your wallet to pick the less of a priority for industry oversight entities

Gee. Two economists got hit in the eye by a flying object, and noticed it?!

The Canadian CPI is a pure joke with or without the housing inflation. For example, when the oil price crashed, so did the Canadian dollar. So you would expect that the manufacturing imports dependent country would be heavily hit, but the CPI kept it’s cool, between 1 and 2 percent. And not that you wouldn’t notice the inflation on the shelves, usually it jumps by 10-25%.

I’m been wondering a lot recently about Hyundai.

Wolf I emailed some examples of the limitations of quick smartphone photography in “no stopping” “no parking” “no standing zones” :-D

Got them. Thanks. I replied via email.

I assume you’ll be researching and writing on this? I’d like to read and see.

You bet.

i go to the supermarket in new brunswick and it seems…..more expensive……..

Groceries for sure are more expensive due to the Cdn dollar used for US sourced products, but also due to the crappy California winter for fresh vegetables.

However, the inflation skew due to property values in Vancouver and Toronto does not apply across the country. I live on the BC west coast and have been debt free for the last 20 years. How did this happen? Frugality and staying away from buying things when I did not have the money. What a concept. :-) No, I cannot afford to see a Maple Leafs or Canucks game, or at least that was my mantra which set us up financially.

Granted, it is expensive to live on the treadmill. Folks should spend some honest time for planning and reflection on how to get off it. Looking for a relocation spot well away from the large cities might be a good first step. If that is impossible for some folks, or they simply want to live in the city, then suck it up and appreciate being behind the eight ball for the rest of your life. A fixer upper in Vancouver is over a million dollars. I paid $100,000 for mine which included 141 feet of riverfront. No brainer. It is now finished and new….with no debt used to get it done.

The sad thing is that even if people get their city houses paid for, as they age they are most likely unable to stay there unless they defer property taxes on the eventual estate.

Inflation: The Ugly Truth that would crash the system

First…the bullshit:

JPM Cuts 10Y Yield Forecasts “Significantly Lower” Due To Weaker Inflation Outlook

RBC: inflation expectations remain D.O.A.

The ugly truth

Devonshire: True Inflation Is Three Times Higher Than Officially Reported

May 9, 2017 – In a fascinating, new report by the Devonshire Research Group, the research team focuses on what may be the most controversial …

Shadow Stats: CPI using the methodologies in place in 1980 show inflation running at 10%

Michael Hudson puts the FIRE sector into place in his video-ed talk here.

He defines the parasites behind the wealth grab they, very successfully, make.

https://www.youtube.com/watch?v=6PgilZn7eZU&feature=em-hot-b-vrecs

H’em…need anyone be reminded that the Central Bank of Canada as well as numerous other institutions (some top to bottom) are run by

ex-Goldman partners, just like in the USA, and the UK, and the EU, and Oceania. How does one become an ex partner when it is so difficult to become one to begin with? Do they just quit? Do they call each other once in awhile and chat about old times, see how the old gang is going ?

Odd, isn’t it. Just a conscience I am sure, so I will run along now.

Odder yet .. albeit more ironic in light of his campaign promises to ” drain the swamp ” that the majority of the Chaos in Chief’s cabinet and advisor picks are ‘ex’ Goldman Sachs as well

And yeah … where do all these ‘ ex ‘ Goldman’s come from ? Damn Goldman’s must be an awfully deep … errr … swamp .

The time with Golden Sacks is just a summer boot camp. Then they spread out like a mosquito infestation.

Correct answer.

Double Bubble Toil and Trouble … inflation rampant yet no one’s troubled … Scales of Rand … tooth of Greed … like a hell broth bubbling .. with none taking heed .. when and how this all ends … no one knows .. but when it all does …. it’ll be one hell of a blow .

Unfortunately I am not sure how interest rates can be raised without a severe contraction in economic activity. The provinces have been borrowing heavily as have households and the federal government since the liberals come in. Many provincial budgets would be severely constrained with higher rates and households facing higher interest rates and a decline in the value of their highly leveraged assets would be retrenching as well. This would be exacerbated by a weaker job market. The facade that actual inflation is reflected in the CPI must therefore be maintained.

The necessity for a high level of financial repression is dictated by the overall debt levels of households and the various levels of government. There is also the preference to keep the Canadian dollar low in the face of oil price challenges and what could unfold in the trade arena with the new administration in Washington.

Unfortunately it is a rather hazardous relying on balance sheet expansion to keep the party going and to much of it for to long risks an unavoidable tipping point being reached. I therefore anticipate a very gentle tapping on the brakes with households and governments facing increasing constraints in their addiction to debt. The increasing risk of a severe retrenchment with increasing debt levels suggests much more prudence and restraint. No policy maker however wants to trigger a self reinforcing economic downturn where the options narrow significantly.

They are trying at all costs not to raise interest rates in Canada.

Especially as a new report came out showing that 14% of homeowners with household incomes of $50,000 or more, can’t afford a single increase in mortgage payments, and 38% can’t afford even a 1% to 5% increase in their mortgage payments.

http://thecanadianpress-a.akamaihd.net/graphics/2017/static/cp-mortgage-debt-survey.png

Our mortgages are different from the US, most people have mortgages that are renewed every 5 years or less and many mortgages are variable, meaning they would increase as soon as the Bank of Canada rates started to increase.

http://www.cbc.ca/news/business/manulife-housing-debt-1.4127243

Our economy relies too heavily on the real estate and mortgage lending industry, the Bank of Canada does not want to be responsible for pushing the industries or homeowners over the edge.

This reminds me of my cousin who got hooked up with drugs. My poor uncle tried to take him to rehab many times, but as you guessed he went back to crack! He’s lost his family, himself and put a huge whole into my uncle’s heart when he finally died of Aids from all that crap injections. There’s an uncanny resemblance between the insatiable addiction of us Canadians to loans & mortgage and it seems we can’t really stop it. And our beloved governments and BOC are just waiting for a miracle.

But I’m afraid that’s not coming except doom.

It’s very easy to mistake need for greed, that’s Canada’s status quo from my POV.

With respect and thanks for your comment.

At a guess, I would assume that virtually ALL major Governments tell copious lies about their economic data. Up or down, depending on the needs of the popularity polls.

When their lackeys in the Central Bank or Public service announce a policy on inflation they often refer to a 2% goal as preferable.

What they REALLY want and in fact need, is 22% rate and then a 222% rate in order to inflate away this horrendous and in fact totally out of control debt burden. Add to the debt you can add the drain on the budget of so many sucking desperately on the public teat, easily solved by telling further lies about the inflation rate, and its COLA effects.

The debt burden that has NIL hope of ever being repaid or even serviced otherwise.

Consumer price indexes have historically been fraudulent, usually only for political reasons, to comfort the masses. More recently, it’s been used to defraud pension recipients, and by the engineering-down of interest rates ostensibly justified by ‘low’ inflation, to rob people of their income from savings.

The idea of a CPI is absurd anyway, because a collective model applied to individuals’ expenses cannot apply – everyone has a personal ‘inflation’ profile, and anyway, referring to the CPI as an ‘inflation rate’ is incorrect, though people have been brainwashed into thinking it is.

Canadian government is far more talented than US government in pumping out fake numbers as real numbers. It’s not only their CPI that is fake; their official unemployment rate is 6.6; but the real unemployment rate is probably 20%-25% specially amongst people younger than 30.

I think we should send US officials to Canad to be trained to be a better liar.

Is it just a coincidence that real wage growth in IOUSA has been stunted for many years, and that the CPI has been “re-weighted” several times during the same period?

I’m familiar with ShadowStats methodology and it seems reasonable to assume that the “revisions” have not only understated inflation, but likely contributed to wage suppression, as well.

Add in illegal immigration and the impact of H-1B visa holders on the labor market, and maybe the real culprit behind declining real wages is… the US Gubment.

i have a feeling the same business folk that cook the books for private industry have moved over to the public side. i think what they are saying in 1-2% but reality is10-20% simple rounding error. misplaced decimals. when something that use to cost a dollar last year now cost 1.25, thats a 2.5% increase instead of 25%. years from now they will say, oh we made a mistake in our calculations. oops, sorry about that, our bad.