Who’s Behind China’s Wild House Price Bubble? State-Owned Property Developers, Funded by State-Owned Banks.

Beijing’s municipal government summoned representatives of state-owned property developers on Monday and told them to stop hyping the already overheated housing market, according to the portal, Chinese Real Estate Business (CREB), cited by Reuters.

State-owned property developers, funded by state-owned banks, have been a major force in inflating home prices as they bid aggressively for land to gain market share. According to CREB, state-owned developers bid for nearly half of the most expensive land in China during the first five months of 2016. And that trend has continued. But after the meeting with the municipal government of Beijing, these firms may be forced “to change their land strategy.”

Telling state-owned developers to stop hyping, as CREB put it, “operational and market activities” would be the latest effort to crack down on property speculation gone wild in China. It would come on top of the numerous other ways local and central authorities have tried to curb this speculation, without success so far.

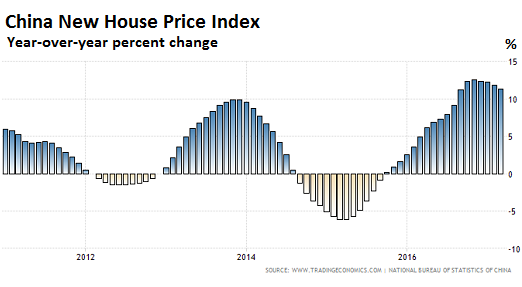

Today, the National Bureau of Statistics reported that new home prices in 70 cities surged 11.3% in March year-over-year. It was the 18th month in a row of year-over-year gains. Prices jumped 19% in Beijing and 16.8% in Shanghai (chart by Trading Economics):

On a monthly basis, new home prices rose 0.6%, the fastest in four months, up from 0.3% in February. Of the 70 cities in the index, 62 experienced a month-to-month price gain, up from 56 cities in February, once again defying expectations of a slowdown. Prices jumped the most in Haikou (2.6%), Sanya (2.5%), and Guangzhou 2.3%), followed by other second- and third-tier cities, to which the speculative fire has been spreading.

Dozens of cities have imposed ever tougher buying restrictions, more stringent down-payment requirements especially for second homes, stricter resale limits, etc. etc., and they’ve redoubled their efforts since mid-March when it became apparent that the prior redoubled efforts had not produced results, as people figured out how to get around them.

But China depends heavily on property development and property speculation for its economic growth, and no one really wants to bring it down: The National Bureau of Statistics (NBS) reported on Monday that first-quarter growth in property investment – residential, commercial, and office spaces combined – soared 9.1%.

This red-hot property sector, and the 40 other sectors that are directly affected by it, drove China’s official GDP growth in Q1 to 6.9%.

As always, analysts keep saying that it would take a few more months for the restrictions to take effect and start cooling the market. That line was once again repeated on Monday, officially:

“Because the latest round of cooling measures came out after March 17, their impact on the entire economy including home prices may show in April or later,” Mao Shengyong, a spokesman for the NBS said at a briefing, according to Reuters. Houses are for habitation, not for speculative investment, he said.

That would be a novel concept in these crazy times. But who really wants to cool the market, when state-owned developers and state-owned banks are firing it up? Yet, everyone sees the risks. Reuters:

Most analysts agree an overheating property market poses the single biggest risk to China’s economic growth, with increasingly tough government measures to cool soaring prices raising the risk of a nasty crash.

But the cooling off is not happening yet. New construction measured in floor space soared 11.6% in the first quarter, year-over-year, the NBS reported, and sales jumped 19.5%, though that growth rate was down a notch from the year 2016, when sales at soared 22.5%, the highest in seven years, as the boom in first-tier cities was spilling into second- and third-tier cities.

With state-owned developers, funded by state-owned banks, firing up much of the show, and with speculators, who assume the government has their back, running wild in a gushing celebration of ever-soaring prices and huge automatic profits, there’s little chance that this scheme that has already transcended irrational exuberance will simply “cool” to a level of “stability,” and plateau somewhere soon, as it is hoped. Phenomenal bubbles like this don’t go quietly.

And now the second largest US residential brokerage is trying to capitalize on the desire among property investors in China to ride up the US housing bubble. Read… Warren Buffett’s Berkshire Hathaway Will Market US Homes in China

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So if I’m understanding this correctly … in conjunction with the Berkshire Hathaway news thing just got worse for us here in the US what with China cracking down on their housing speculation leaving the most viable option for residential real estate speculating and investment in the US housing market .

Brilliant ! And we’re screwed …. unless that is China comes to grips with how much money is about to leave their shores and heightens their regulations and restrictions for overseas investment .

Ironic aint it that between this administration and the 21st century American Robber Barons we’re becoming more dependent on China’s actions by the day .. with them leading the world and us rapidly becoming the has been / also rans .

China has a few things going on.

1) Until about 20 years ago, it was the wilderness. They joined the commercial world and supplied it with all it needed. This much money coming in so rapidly was not unlike the Beverly Hillbillies getting rich, only the Chinese decided to spend it.

2) They discovered central banking, credit creation, and money printing. In one sense it amounted to what happens when you give a monkey a gun — random shooting without understanding the consequences. They also noticed money printing matched with growing demand and growing capacity equaled wealth if you could get some.

3) Smart people grew the economy and saw no problems with the excesses of go-getters. Lots of credit … no problem. Everyone is making out well.

4) Eventually somebody noticed excess valuations and decided the best course was to keep 1 billion or more Chinese under control by not letting a credit bubble explode.

5) Now it’s keeping the plate spinning as best as it can. All manner of BS is OK as long as it works.

You are inverting history with respect to no 2: “They discovered central banking, credit creation, and money printing. In one sense it amounted to what happens when you give a monkey a gun — random shooting without understanding the consequences.”

The Chinese were the ones who founded paper money. And if you even bothered to read your history, it coincided with the decline of Chinese creativity. Prior to that Chinese civilization were doing plenty of invention, including gunpowder, but once you can print paper money, why bother doing anything else?

“it coincided with the decline of Chinese creativity”

Interesting. I did read they invented papaer money but never read about a parallel with its decline in creativity. Any good sources/books to recommend?

I think it is worthwhile to never underestimate how big a speculative bubble can get.

Being from Ireland, I try to constantly remind myself of the Celtic Tiger property bubble, circa.1996-2007.

The IMF published a report in 2000 to outline the dangers of Ireland’s overheated property market. By the time 2003 came around, even i the ever risk tolerant gambler, was shaking my head at prices.

As it turned out, the fledgling property developers were only “warming up” in the year 2000. The bubble inflated until the Spring of 2007.

The Irish Government did not try very hard to talk down prices. Although they did raise stamp duties on transactions. The market crashed only when it was ready to crash.

Similar to Japan before that, similar to China now.

And Australia in the near future!

Well we know one thing from history that bubbles dont last forever and that they always crash in the end ..once they have screwed enough people

The Fed’s engineered boom-bust cycles are the most efficient means to transfer the wealth of the middle and working classes to the Fed’s oligarch accomplices in the financial sector.

Absolutely. Those in power have no incentive to dampen the speculation. A few luckies and lemmings will get rich too – but mostly, not. I wonder if this is partly fueled by the bias that economic growth = good and sustainability is bad/boring/less profitable.

I found this little background on Wikipedia.

It’s headline is : “The Chinese property Bubble from 2005-2011”.

https://en.wikipedia.org/wiki/Chinese_property_bubble_(2005%E2%80%9311)

The gist of it seems to be that the Chinese Government tried to prick the bubble in 2011.

There was a documentary on Al Jazeera English in 2015 called “Chinese Dreamland”.

The point of it was to chart the rise and fall of the Chinese property market.

So much for that. Now the bubble is bigger than ever.

When I read a Wolfstreet column like this, I’m impressed with the information and analysis. But I’m left with the question: how would you (Wolf or commenters) begin to solve the problem of frantic speculation in residential real estate?

I can see the argument that cheap money fuels real estate bubbles, and I can hear you saying, “Bury all central bankers and the politicians who brought them to the party.” But I live in LA, home of boom/bust real estate cycles. We bought our first house in 1980 with a mortgage that carried a 13% interest rate, and high interest rates weren’t impeding the rapid upward swing of home prices.

Of course, you can just wait for the bubble to burst. But I’m witness to a city I love losing a whole generation of young creative people who cannot afford to build a life here. So I’m interested in solutions a bit less drastic.

Any thoughts?

But I’m left with the question: how would you (Wolf or commenters) begin to solve the problem of frantic speculation in residential real estate?

The banks that recklessly enable such rampant speculation know that the Fed and middle class taxpayers will cover any and all loses. So the first thing that needs to happen is that banks who recklessly lend money to enable unsustainable speculation should be allowed to go bust when the F***ed Borrowers can’t repay those loans. The second thing is that fraud and lawbreaking needs to be ruthlessly investigated and countered with criminal prosecutions, which will never happen as long as regulators, enforcers, the judiciary, and lawmakers are all captured by the oligarchy. Finally, and most important, the criminal private banking cartel called the Federal Reserve needs to be audited, then shut down, and replaced with a responsible central bank that will ensure we have honest markets and sound money. Unfortunately, none of the above is going to happen until we have a systemic financial collapse due to the swindles of the Wall Street-Federal Reserve Fraud Syndicate.

As the old adage has it “to have less of something tax it, to have more of something subsidize it.”

One of the largest subsidies is the tax deductability of mortgage interest, closely followed by “depreciation” on an appreciating asset, which converts a large fraction of profit into capital gains and lower tax rates.

Elimination of the mortgage interest tax deduction would reduce the price inflation, and minimize the [indirect] subsidy renters pay to the home owners with mortgages.

Other ideas include:

* Imposition of a substantial and steeply progressive transfer tax on the profit generated by sales in excess of the inflation adjusted original purchase price.

[ This ignores wear and tear on the house, which should also be considered.]

* Require the identification of the actual beneficial owners (no straw-man owners or shell corporations) and the source of the money used to purchase real estate.

* Require individuals and corporations owning more than 2 residential units, or selling more than three residential units per year to purchase a “real estate investor’s license” at a substantial fee, possibly progressive based on number of units beneficially owned, and annual turn-over. This is specifically to reduce “flipping.”

* To minimize market manipulation and shortages due to hoarding, impose a steeply progressive tax on vacant housing units/property depending on how long these have been vacant, and their valuation.

* Revise the minimum residential mortgage credit requirements by limiting mortgage amounts to no more than 2.5X annual income, and no more than 25% of annual income, with at least 10% down. Other debt such as vehicle loans, credit card balances, and student loans should also be considered. Set maximum mortgage term to 20 years, and require a level pay amortizing [no interest only or balloon] mortgages, with APR rates between 5% and 7%.

* Implement a requirement that the only person/entity which can institute mortgage foreclosure actions are the named lien holders as shown on the records of County Registrar of Deeds and that all transfer taxes have been paid, e. g. if a mortgage has been sold and resold 5 times, 5 transfer fees must have been paid.

Canada and other countries do not have a mortgage interest deduction, and it doesn’t change a thing.

To other replies, I’d add, change NIMBY zoning laws to allow more, and denser development. Regardless of financial engineering, LA is growing, which means new housing needs to be built. If the only houses that are allowed to be built are a 100 miles away in the desert, then everything closer in will continue to appreciate in price.

LA is not landlocked like SF. There’s plenty of land. And there’s no reason why LA shouldn’t have a dense downtown at least as big as Chicago’s. To it’s credit, I think this is happening, with big investments in rapid transit which will hopefully be followed by a loosening of zoning around mass transit. But it’ll take some time.

Wolf posted here some time ago about how Tokyo has more housing starts per year than the entire state of California (by a huge margin) despite having a far smaller population. Not coincidentally, they have stable housing prices.

Keep in mind housing demand in CA is at 30 year lows…… And falling.

There is no shortage of housing. There is a massive excess supply here.

BTW, yes San Francisco is surrounded by water on three sides and borders other urban areas in the South. BUT there are huge tracts of land, including the Naval Shipyards and Treasure Island, that the Federal Government, after contaminating them during the Cold War, has handed over to SF. They’re now scheduled for redevelopment, with plans for tens of thousands of housing units, right in SF. There are a lot of other areas that have been going through that process, including SOMA where warehouses have been replaced by high-rises and Mission Bay, similar story.

Last time I checked there were about 65,000 housing units in the planning pipeline.

It’s impossible to take a measuring stick to the length of bubbles but the IMF did write this piece to to highlight signs of a the China bubble in December 2010….. 6 years and 4 months ago.

http://www.imf.org/external/pubs/ft/survey/so/2010/INT121010A.htm

As i mentioned earlier, the IMF wrote a report in August 2000 about Ireland’s property bubble. the bubble peaked 6 years and 9 months later.

https://en.wikipedia.org/wiki/Irish_property_bubble

So it looks like property bubbles can grow in some cases for at least another 6 or 7 more years after the IMF lets us know there is one.

Let the bubble burst…

Living in Toronto and seeing first-hand how home prices have risen $50k-$150K per year over the past few years, I feel that the best course would be to allow the market to crash. A lot of economic pain will come from this, but in my opinion, is needed to re-teach consumers, investors, financiers and speculators the risks and rewards that seem to have been lost over the years. Our governments have become complicit in the flagrant money-laundering of foreign investors and banks blinded by ever increasing profits of securitizing mortgages. Blinded by money, our morals have decayed. And a good old fashioned lesson is sorely needed.

Governments and groups are concerned about excess speculation in many places. The odd thing thing about this one is it pits one government against government controlled banks, or one level of government against another.

In North America or Europe this would be a so- what, but in China…?

Most homes in China are purchased with cash, so all this chatter about down payments and limits on mortgages is irrelevant. Also, in most 2nd and 3rd tier cities, the Chinese Joe Sixpak and Larry Lunchbox can and buy affordable homes every day. If you travel around China and read the prices/sq, meter (which is how homes are priced), you will see that there is still a good supply of new housing that ordinary people can buy.

“Most homes in China are purchased with cash,…”

Check out the stats on mortgages … SOARING.

People believe what they want to believe Wolf!

And when it comes to tulip bulbs and Chinese real estate, they want to believe that it’s ‘different this time’ [for no other reason than I want it to be, and I have to believe it is, because I’m vested].

All houses are bought with cash. Borrowed cash.

…are they..?

Provide evidence.

This ‘most homes in China are bought for cash’ meme has been around a long time now; it may have been true when the housing bubble there had yet to start.

However the Chinese populace has been loading up on debt at a rate unseen in human history for about a decade now.

A speculative bubble is a speculative bubble, however much someone may want to wish that it’s ‘different this time’.

However if you choose to believe that all talk about Chinese mortgages is ‘irrelevant’ then I suggest you get in on the party and flip to your heart’s content. As long as there’s a bigger fool, you’ll be fine [as it is with all speculative bubbles].

May be they are trying to keep property prices low to advantage the US investor ?

Won’t you step into my parlor said the spider to the fly.

If the Chinese are the main investors, it makes sense to bring in an outsider to share & bare some of the burden & liability when the pimple pops,

Q: Is Buffet the unwary chump .. soon to be the meat in the sandwich ?

This will end in tears, since Chinese workers live in poor housing while ghost cities and high-rises sit empty.

To engineer a soft landing, the People’s bank can simply order banks they supervise to curtail mortgage lending on a fixed schedule and impose restrictions noted by others. The People’s Bank can also begin ordering foreclosure on delinquent mortgage loans and convert structures to social housing. Increasing domestic demand and building out the Silk Road can absorb the shrinkage when the real estate bubble contracts.

But as Wolf writes, the Party Oligarchy won’t do that… but eventually the bubble will pop and and this reckless cupidity will explode into social revolution.

This is why China will not inherit the Earth as the West collapses. They’re not worthy.

The chinese STATE is attempting to reign in the STATE entitys involved in the bubble. As they know they can not prevent the bubble going bang.

When it does, they want the non state entitys, and lenders to take the fall, before they bail out the state lenders and entitys they need. To keep the system afloat.

In china, the State is going to makje a Massive amount of debt and printed money, evaporate. At the expense of the capatalists, who are not part of the CCP clan system. If they can get away with it.

As law in china is how the CCP clans want it, on any given day, that should not be a problem for the CCP Mafia State.