Next: higher rates or currency crisis?

By Nick Kamran – Letters from Norway:

Sweden’s welfare state supposedly allows for success while providing a safety net for those unable to keep up with the market. In principle, it is an ideal, utopian-like state. However, Sweden’s touted economic success has come at the expense of its currency, the Krone (SEK), and long-term sustainability. Riksbank, the Swedish Central Bank, like its European contemporaries, has undertaken experimental policy, driving real and nominal interest rates below zero.

Not All Growth is Equal

Since 2014, Swedish deposit rates have been negative. Not only has overall negative real interest rate policy affected housing, but it also drove Swedish consumers deeper into debt. Embarking on the dual mandate policy may have staved off recession, but it created greater problems for the future.

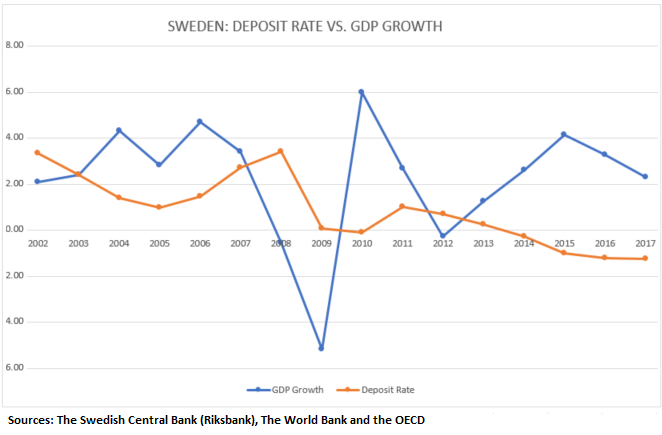

Although current deposit rates are at a record low of -1.25%, the latest GDP print came in at 2.3%, and the growth rate has been tapering since 2015. Sweden’s “hot” GDP growth – hot relative to the region – could be attributed, not to industrial growth, but rather increased government spending, funding social programs.

Additionally, with no incentive to save, consumer debt has taken off, along with the housing prices, while disposable income lagged. Swedish household debt is now at a record high. Hence, the Swedish growth story is not organic but rather a borrow-and-spend one (Source: The IMF Working Paper WP/15/276 by Rima Turk):

The Riksbank Shell Game

Swedes, like Norwegians, are victims of the “exchange rate versus housing price shell game.” The SEK received today for the sale of their inflated flats has fallen 30% against the US dollar (average USDSEK in 2014 was 6.86 vs. 8.95 on March 15, 2017). Stockholm housing rose 31% during the same period in SEK terms, negating the recent gains over the same period. The SEK fell 23% against gold in the same period.

Hence, the “Swedish Model” is under attack. The egalitarian underpinnings, unwinding with the negative rates, are driving a wedge into Swedish society, creating extremes on both sides of the economic spectrum. The rampant consumerism, encouraged by artificially low rates, continues to widen the wealth gap. Coincidentally, the middle class deteriorated the most between 2014 and 2015: the same time that deposit rates took a dive. Furthermore, the negative savings rates are driving the average person to “gamble” on speculative investments instead of saving and building a future over the long term.

No Pain No Gain

Recently, inflation has been heating up. Near zero from 2013 to 2015, it edged up to almost 1% in 2016, and printed 1.8% in February. Much of it is supply driven: rising import prices attributed to a falling SEK. The real interest rates fell to negative -2.3% (Repo Rate minus Inflation) last month. At some point, Riksbank will either have to raise rates or the government will have to intervene to avert a currency crisis.

Interestingly, Sweden is one of the most economically diverse nations in the world, ranking fourth in economic complexity. Historically, Sweden has been an industrial and innovation powerhouse with firms like ABB, SKF (ball bearings), Astra Zeneca, and H&M. An economy like Sweden’s could more easily adjust to a sustainable interest rate than almost any nation. Although there would be a short-term housing bust, the money would quickly flow into the other and diverse industries, creating new opportunities rather quickly.

Hence, instead of undertaking experimental rate policy, Riksbank and the Swedish government should be engineering a soft-landing or a “controlled crash”, adjusting taxes and policy to ensuring a smooth transition to sustainability for the general population. There is precedent from Iceland that already exists.

It is clear that the negative rate experiment is neither sustainable nor helpful to economic growth. It only inflates bubbles while widening the wealth gap in Swedish society. A once prudent and financially conservative people are now getting drunk on debt, wrecking their future. The very premise of Swedish society is under attack. Nevertheless, it does not appear that this policy will abate anytime soon. There seems to be one lever in the Central Banker’s control room: interest rates. If anything, they may get more aggressive with it. By Nick Kamran, Letters from Norway.

Lagging wage growth vs. house price bubble. Read… Are 100-Year Mortgages Next? Effects of Negative Real Interest Rates on Nordic Housing Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Although current deposit rates are at a record low of -1.25%, the latest GDP print came in at 2.3%, and the growth rate has been tapering since 2015.”

Does Sweden use the same methodology as the USA to calculate GDP? For example with regard to government spending?

I guess I want to know if GDP is arrived at by a universally accepted ‘equation’.

Thanks

GDP calculations are reasonably standardized across the developed countries. So they’re comparable. That doesn’t mean that GDP accurately reflects what’s going on in the economy.

The Swedish population is currently growing at a pace not seen since the mid 19th century. GDP growth in Sweden is largely driven by construction due to the enormous housing shortage caused by this population growth, along with the middle classes desperation not to live near this new population (2/3 population growth consists of asylum seekers + family re-unification).

I you look at Swedish GDP/capita you’ll find a rather less impressive growth number of less than 1% and you’ll find the same to be true for the average of the last decade. At the same time, helped by low interest rates, debt has been rising at a rate of about 7% per year for quite some time. While the population has been expanding, this expansion in debt is rather larger than population growth + salary growth, and most of this debt is taken on by native population as few immigrants would qualify for a mortgage as a large majority does not support themselves even a decade after arriving and indeed never will.

Every country on this Planet uses imaginary numbers to calculate everything, EVERYTHING.

You see, imaginary numbers never lie and are never wrong.

Frankly, it is all governments has left. Yet, people still buy it.

Can the world be any more lost that it is right now? Yep…wait.

The most appropriate term to describe this phenomenon regarding both countries , banking and business in general is ;

Potemkin Village

Or alternatively ;

” Emperors New Cloths

Central Banks push debt…..The foolish and leveraged laugh from their towers as the prudent save and strive. Winter is coming.

Is winter coming for both parties ?………. both “the foolish and leveraged” and “the prudent that save and strive” ? …….or just one party ?

Please explain your analysis.

Personally I’m in the “prudent that save and strive” category.

I think you will find it’s both. When the Titanic sinks, only those who can get to the lifeboats have any chance. This means the very rich.

The Swedish and Norwegian model are doomed to failure, leveraging on low interest rates to encourage consumer spending creates the high demand due to too easily accessible credit, which consequently jacks up prices across the board. So inflation is artificially high.

What comes up goes down and when they go down, sucks to be them holding the bag. At least Norway has oil and salmon.

Ikea n meatballs can’t go that long a away to prop the economy.

The sad reality being despite the US’s Ayn Rand addled hyper capitalism – our ongoing Greed is God zeitgeist – and an RNC shoveling money into the hands of the wealthiest while stealing from the poor congress and senate for the past 6 years …. don’t kid yourself [ or buy into the Alt Right NeoCon propaganda machine ]

We ( US ) are in the very same position if not worse . Fact is all the ‘isms .. capitalism , socialism , communism etc have exceeded sustainability across the globe … with the chickens are on the verge of coming home to roost .. and the ‘ Piper ‘ now demanding his due

You are completely off the mark – only one ism creates all of the wealth and standard of living increases while co-existing with individual liberty. It is the only system where the seller must serve the buyer to survive. Only the govt can create a situation where that is not true, and then only through coercion and threats. Capitalism is what the world needs. The unequal sharing of wealth is much better than the equal sharing of misery.

How about the Lingonberry sauce?

Well at least last year they cut the maximum mortgage term to 105 years.

Not good, from the point of view of a householder who wants to sell.

“They” should have DOUBLED the maximum mortgage term.

That way, the householder could sell his house for a million kronor instead of a mere five hundred thousand…

Its true it might be another bubble, but don’t forget that Sweden’s Debt/GDP is around 43 percent. At the top of that Sweden has faced large immigration that has helped the house prices and at the same time construction has not been sufficient. Household debt is high but obviously there is room on the fiscal side if the shit hits the fan. Most typically thou is that the SEK will just fall and Sweden’s export companies will benefit, just like 2008. The USD/SEK example in the article is quite silly. I suggest you take up a longer graph to see how the SEK (devaluation and depreciation) has been used in the past.

Keep in mind a couple of things regarding the indebtness of the Swedish government, all isn’t as nice as the official numbers do claim.

– The former Premier, Persson, did in fact confiscate a large percentage of private pension funds and used these funds to pay off government debt held by foreign entities, thus the state’s debts are low, but the pension system is in deep trouble due to this siphoning off of funds.

– The current government has forced state controlled companies ( for example the Swedish eqvivalent to Amtrak ) to pay out huge extra dividends and these dividends are completely financed through loans taken by those companies. The government got the money, but the debt isn’t found in government ledgers …

Just a few minor details on cooked books …

Forgot to mention that Sweden is in proud posession of:

– an education system with failing schools

– a health care system coming apart at the seams

– a police that is both understaffed and has retreated from large areas of the country

– a defence that is a bad joke, according to the C-in-C, Seden is able to defend a single location at most for a week …

And Seden has got parliamentary elections in 2018 …

Massive borrowing and speculation just to stand still…

Cheap money and low standards to borrow …

A super generous welfare state and unlimited immigration of 3rd world criminals who will take as much as they can and contribute nothing …

How do you think this will end?

In misery, bankruptcy, ruin and war.

No one knows how to stop the ball rolling. Not in Sweden, Europe or America. Government leaders tend to take the easy way out hoping they will get out with their heads and a retirement check before all hell breaks loose.

Just look at what the US media has done to Trump when he brought the Swedish mess into the light.

No free lunch has real meaning. Just wait, there is still war in the air from last year, and the non-elected have not stopped their march toward it. As soon as this summer there will be a break out somewhere and when that happens, it will spread like an ‘all clear’ signal around the world to go mad, completely utterly mad.

The idea of pulling demand forward seemed like such a great idea at the time. End game is eventually it’ll be time to pay the piper so then what?

Does NIRP apply to credit cards there as well? And if it does, how do I get one?

That was a good one :)

“A once prudent and financially conservative people are now getting drunk on debt, wrecking their future.”

Prudent should only be used in the past tense; it is now a race to the bottom. It is a game of catchup as the bottom is moving still lower. Globalists have scored a success.

Debt, in this instance, is purely a function of housing prices. And housing prices are purely a function of bank regulation. The race to the bottom is the great bank deregulation race.

Mr. Trump is doing his best by getting rid of the Consumer Financial Protection Bureau and gutting Dodd-Frank. But it is a world-wide effort.

The Consumer Protection Bureau is one of the biggest frauds ever committed on an unsuspecting public. The CFPB is funded by the Federal Reserve, the banks, and is not protecting the public, it is protecting the banks. Every time they hail Senator Warren for supporting it, it makes me want to puke.

I think, you heap to much scorn on senator Warren. If I recall, it was the FEDsters who would only agree to it if it was under the FED. Quite a sneaky fraud as the consumer protection runs counter bank protection. Blame the commander-in-chief for being a complete Wall Street puppet.

If you don’t know about the Planet Money podcasts, I highly recommend them. They do a good job diving into different financial and economic subjects with a good balance between detail and light humor. They did an excellent piece on Iceland’s Debt Jubilee, following up on a piece they did about Iceland not long after everything hit the fan.

Like most things in life, the results from the Jubilee are mixed at best.

Listen to the podcast at:

http://www.npr.org/sections/money/2014/12/05/368723679/episode-587-jubilee

Iceland is a country of 300,000 people, i.e all are related, or know someone who is related to someone.

Debt jubilee, like NIRP, is telling the prudent that they are a bunch of yesterday losers, and poke them in the eye for a good measure: it is a central banking crime.