Wage Growth vs. Housing Price Growth

By Nick Kamran, an American living in Oslo, Letters from Norway:

Historically, central banks throughout Europe had one mandate: price stability. They did not worry about employment or economic growth, only currency integrity. Setting interest rates to contain inflation ensured that a Krone or a Euro would purchase tomorrow what it could today. Nevertheless, since the ebbing of the 2008 financial crisis, The ECB, of which Finland is a member, officially added full employment and economic growth to their mandate. The Norwegian, Swedish, and Danish Central Bank’s followed suit, stating that they would consider “other factors” than inflation when basing an interest rate decision.

Hence, instead of remaining impartial — leaving it to lawmakers, markets, and the public to deal with the prevailing interest rate — the central banks became involved in policy making. Adding employment and economic growth to their mandate equates to the National Institute of Standards changing the definition of the meter to help an engineering firm, working on a major bridge project, meet budgetary and timeline constraints. In addition to creating a dilemma, the additional mandates made central banks appear politically biased.

The Conundrum

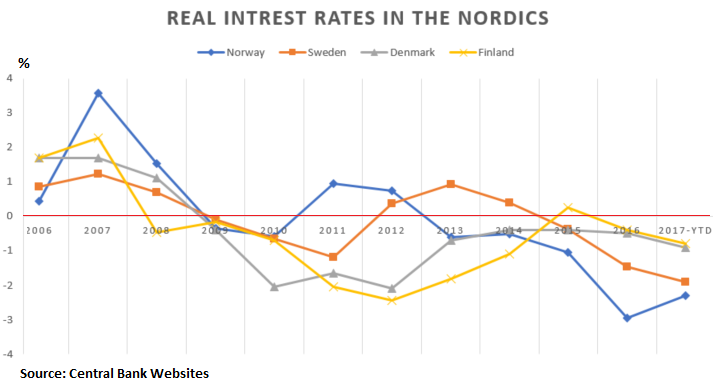

In an attempt to balance, what central bankers perceive as two opposing forces, inflation and unemployment, they chose economic stability over maintaining price stability. The other option, raising rates would have led to greater short-term unemployment. The central banks pushed benchmark rates all the way down, nearing zero in Norway (.5% – Key Policy Rate ) and Denmark (.05% – Discount Rate), hitting it in Finland (ECB at 0% – Refi Rate) and going negative in Sweden (-.5% – Repo Rate).

Note that central-bank deposit rates are even lower, and negative, to force money out of the banks and into the economy, stoking inflation. Currently, the real interest rates – key interest rates minus inflation — are deeply negative for all the Nordic countries.

Although the policy mostly kept unemployment at bay, relative to historical levels in the respective countries: currently at 4.4% in Norway, 7.3% in Sweden, 4.2% in Denmark, and 9.2% in Finland, it inflated a housing bubble. In Norway and Sweden, where real interest rates are especially negative (-2.3% and -1.9% respectively), housing prices inflated the most. In Oslo and Stockholm, the trend continues.

Wage vs. Housing Price Growth

From 2007-2016, professional wages grew, in local currency, 40% in Norway, 32% in Finland, 25% in Sweden and 24% in Denmark. During roughly the same period, apartment prices, in local currency and on a per square-meter basis, surged 107% in Stockholm, 93% in Oslo, and 38% in Helsinki. Copenhagen area, overall, only went up 8% during the same period. However, in recent years, they experienced a surge as well.

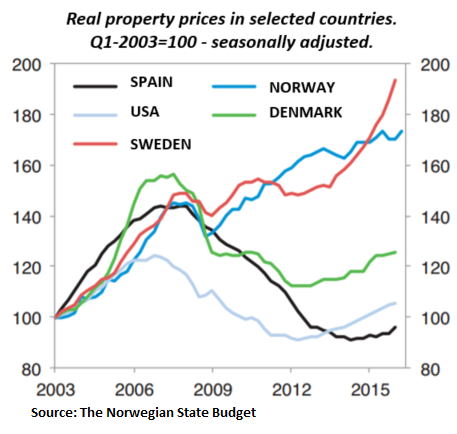

Taking the difference, housing price rise minus wage increases, discounting salary hikes, we can see that housing rose 82% in Stockholm, 53% in Norway and 6% in Finland. In Denmark, wage growth outpaced housing by 16% in the same period. The chart below, taken directly from the Norwegian State Budget, further illustrates the Nordic housing markets compared to other major western markets. Using indexes and accounting for the whole country, we clearly see that Norway is lifting-off and Sweden is going parabolic.

Are 100-year mortgages next?

Finland and Denmark, the Nordic countries with the least negative rates, experienced the least housing price growth. Wage growth did not keep up with housing prices, (except in Denmark), further illustrating that negative interest rate policy, in general, which intends to go all out for growth, does not properly stimulate the economy and does not promote sustainable growth across all sectors.

The Nordic case clearly illustrates that central banks should only maintain price stability which upholds currency integrity. The rates, when correctly managed, act as a regulator, ensuring the economy remains diversified. No one sector can take all the growth. The “negative (real and deposit) interest rate” experiments are failing. They’re distorting the economies which undertook them. Surging housing costs are aggravating inequality and depriving other sectors in the economy. For example, retail sales since 2007 in Norway grew only 8% despite a brisk population increase (up 11% over the same period) and expanding consumer credit (up 13%).

Sweden and Norway are already deep into the bubble; housing continues to outrun inflation and wages at an alarming rate. Helsinki outpaces the rest of Finland but remains in check due to unprecedented construction of new housing. Although Denmark appears to have escaped, recent developments suggest a bubble is on the way.

Despite the figures and bubble narrative, the Nordic central banks appear to have little appetite, to raise rates, favoring growth and full employment. Nevertheless, they will have to rein inflation in at some point, raising rates. To mitigate a potential crash, we can expect to see the introduction and more widespread availability of longer-term mortgages: 40, 50 and even 100 years. Sweden and Japan already have 100-year intergenerational mortgages. By Nick Kamran, Letters from Norway.

And America has become “Landlord Land.” Read… So Who’s Pumping Up this “New Normal” Housing Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What may be logically consistent and desirable within a closed system is frequently seen to be inane and unsupportable when viewed from outside that system.

100 year mortgages? As a thought experiment, consider what the underlying asset would be worth across the duration of the mortgage, and how much interest would be paid. This is a multi-generational obligation/commitment, and IMNSHO a grossly pernicious mis-allocation of capital. The best thing that could be said about 100 year mortgages is “it seemed like such a good idea at the time.”

The true mandate of the criminals at the Goldman Sachs Feral Reserve System has always been making the rich richer by stealing from those least able to afford and giving it to those who least deserve it.

The purchasing power of the US dollar today is only about 3 cents what it was in 1913 when the Goldman Sachs Feral Reserve System was criminally created. That’s hardly a good example of a store of value.

I think it is unfair to say that the purchasing USD power is 3 cents to what it was in 1913. You have to see that in relation to the respective income of workers then and now and other expenses. It is not that simplisitc. Regardless of the “purchasing power” you have in mind, I think a worker has a better life now then in 2013.

Meaningless considering “a worker” can’t afford anything without committing financial suicide

100 year mortgage … come on down suckers. Have we got a deal for you.

Just because you know someone who loved rehabbing the classic nightmare that needed new plumbing, wiring, and foundation repairs after the termite damage was fixed … that doesn’t mean I want to buy into a collateralized mortgage obligation that represents this type of treasure.

It may look new today, but in 75 years, will the contractor special still hold the same appeal?

100 yr vs 30 yr … maybe 25% lower payment. Practically free. Thankfully, real estate prices always rise.

A 100-year mortgage places the debtor and his/her descendants into permanent inter-generational debt slavery on houses designed with a 30-year useful lifetime. That’s like having a 45-year loan on an automobile. It’s a great deal for the debt serfs owners. Well, at least until the debt serfs rebel and kill all the owners.

“places the debtor and his/her descendants into permanent inter-generational debt slavery”

Bingo……and the Moneyed class loves the sound of that….JR. not only has student debt to contend with, now when he’s done paying for that he can inherit dads/moms 100 year mortgage. Goldman is watering at the mouth over that I’m sure.

>>Historically, central banks throughout Europe had one mandate: price stability.

I don’t think that is true at all. It may be more true for Germany than others. I think historically, after WW2, the goal was exchange rate stability with USD, so that neither exports nor imports would become too expensive. Exports were always important for Scandinavia.

Hence, Scandinavian countries basically followed the FRB. Whenever the Fed changed interest rates, Scandinavian countries would follow suit to keep exchange rates relatively stable. For sure there were some hickups and deviations in the 1970s after USD went off the gold standard and inflation ensued, but overall following was the methodology used.

Hence, most European central banks have been riding the asset inflation train for as long as the US has. I think a 1960s house in Scandinavia has compounded at 7% average, roughly, from 1960 to to 2016. That is hardly price stability. Europe learned asset inflation from their US masters, and now they seem addicted to it.

I’d like to find out if those 100 year mortgages are still around in Japan.

Maybe in the big cities for those really expensive condos, but out in what the Japanese call ‘the country’, I doubt if you would even need one (or get one for that matter).

The longest mortgage I’ve seen is for a fixed rate is for a 35 year loan.

Even Rakuten, the big online retail shop, has housing loans and their rate is around 1.12% for the that period with 10% down.

(Yeah, you have to add on all those nifty fees and charges as well to get the real rate of the loan……….).

What we would do in Australia for cheap loans like that……………….

I’m a mortgage broker since 2001.

They should bring back the 40 year mortgage and the interest only mortgages….only available with HELOC’s. The default rate would decrease if it was available as an option instead of paying P&I.

Wanna know why cities like Brooklyn are hot? Cause it’s too damn expensive in NYC.

Wanna know when principal starts coming off the balance on a 30 year fixed loan? About the 6th year. I’m on my 5th house in 16 years here in Florida. 30 year mortgages are garbage. Extend them or make the client choose his financial strategy.

Watch what Mnuchin does. I bet he extends the bonds creating 40-50 year mortgages.

I asked people from Japan about the 100 year mortgage. It’s a myth. Or extremely rare.

I think toward the end of the bubble (which blew up in 1989), they weren’t that rare for new mortgages. But as Lee pointed out, they’re not really needed anymore since housing costs have come down, even in more central locations. In the suburbs, housing costs are not unreasonable anymore. And out in the country, they’re outright low. (Just get ready for one heck of a commute to the office.)

Yep, you can buy a nice house on a 1/4 acre block within an 1 – 1 1/4 hour commute of Tokyo for around $250,000………….

Even cheaper if you go into the ‘real country’ or on a smaller lot…………

Unreal, but true!!!

“I think toward the end of the bubble (which blew up in 1989), they weren’t that rare for new mortgages.”

Correct.

Doctors might do this so they can start their clinic. This then becomes a family business that is handed down from one generation to the next. In general though, I think it is rare.

A 100 year mortgage lowers your monthly cash burn drastically, how many people live in the same house for life???

How about an example showing the monthly payments for a level pay amortizing mortgage for 100k$ at 3% for 20, 30, 50 and 100 years to see how the monthly payments differ?

I understand that in the UK they have really long (e.g. up to 99 year) real estate leases (often hugely expensive property which is owned by the aristocracy, who rarely want or need to sell their real estate holdings, and which they pass on within the family, largely tax free, for generations. How would this system compare with buying an equally expensive house on a 40+ year mortgage?

What’s the use of the Norway sovereign wealth fund? http://www.zerohedge.com/news/2017-02-28/norway-wealth-fund-gains-53-billion-2016-trump-rally

Best hedge fund in the world last year probably?

When ( not if ) the Swedish housing bubbles does burst, Finland will take a hard hit, because the largest bank in Finland, Nordea, is indeed exposed to the Swedish housing market, being the biggest player there. In addition, Handelsbanken ( another Swedish bank ) and Danske Bank ( Danish ) are present on the Finnish market, both of which are exposed to the Swedish bubble. Add to this the housing market in the capital area of Helsinki, the inredigents for the situation in Finland to become quite interesting are all there.

100 year mortgages are a de facto reality in Sweden, because people over there generally don’t pay off their loans, only the interest. And the Swedes are indebted over their ears, housing, cars, you name it, is usually financed with such debt in Sweden. The impression of a well to do society is more like a Potemkin village … Sweden is an accident waiting to happen …. No wonder that Sweden is one of the countries that has advanced farthest on the road to remove cash from use, they will need cash to be totally removed before the bubble will burst …

100 year mortgages are really just another form of rent, driven by rental shortages, thanks to rent controls.

Waiting lists for rentals in Sweden run 20 to 30 years unless you do sub-lets and key money, and there are strong rules about sub-lets too, requiring reasons to be given, etc.

One hundred year mortgages are worse than renting, at least then you can always move. I know some people in Florida that got stuck with refi’s from going thru the mortgage modification program. They now have an even bigger mortgage with a 40 year term. They would have been better off walking away. Now they are basically renting and keeping up the property as well, great deal.

I think Sweden is screwed no matter what, and that is why they have to rely on artificial growth so badly. In my view having balanced men and women in society is so important.

I do a special type of research where I look at how male and females behave in different counties, and wherever male or female are overbearing, that society will never live up to it’s potentials. My research is new so I don’t have data on all countries.

Sweden is one of the countries where women are overbearing, and thus have and will have huge problems. That is why Sweden have to rely on artificial ways of economic growth. Other countries where I see extremely overbearing women are Philippines, Greece, Egypt, Iran, Armenia; all countries with huge problems that will never be able to amount to anything.

On the other side, you have countries where women generally are great (I am speaking relatively so don’t bite my head off) like Japan, South Korea, United States. And these countries have advanced and will advance in future as long as there is a balance in the society.

I hope taxpayers don’t pay for this “research.”

I have received a grant for it, but it is not from the government; so tax payers are safe. But you’d be surprised at the number of institutes and companies who are interested in the result since it is one of the important factors which allow you to estimate future potentials of different societies.

Just to add, tension in societies will waste energy that is supposed to go to productive use. A well oiled engine always runs better and last longer than a dry running engine which heats up within 10 minutes.

https://www.youtube.com/watch?v=UxpVwBzFAkw

Why Women DESTROY NATIONS * / CIVILIZATIONS – and other UNCOMFORTABLE TRUTHS

Honestly, I don’t agree with the video at all. I believe balance between men and women is important, and it has nothing to do with Western women. Actually Western women are far better than women in almost all Muslim countries, and that is one reason West has thrived in the recent centuries. Men and women have responsibilities in society, and when one sex for whatever reason does not, or can not fulfill that obligation, you will have problem.

It’s the tension that one sex or both sexes create that is the root of the problem.

I watched the video full and more carefully. I was wrong, I do agree with probably 60%-70% of what the video says.

Probably if it weren’t for women, we’d still be living in caves, with no doors.

First they want a door, then they want furniture, then they want to decorate, then you have to invent stuff to make life easier, etc etc.

I wish I could say I have never heard bullshit like this before, but I have, the climate change bullshit. Wall Street funds crazy shit like this to push agendas and they can buy any “research” they want these days.

Welcome to the world of fake everything.

A wise man once said, “If you have to borrow for 15 or 30 years, you can’t afford it nor is it affordable.”

Amen.

If you buy within your means it is very easy to pay your house off within 10 years. If you can’t do this, you are in the wrong market.

The problems of finance always come down to two things. You either do not make enough money, or you spend more than you should. :-)

regards

Or you are unlucky. But that probably belongs in the first category.

Just making weekly instead of monthly payments and reducing the amortization after each 5 year term to the max you can afford (assuming you’ve made some improvement in your income) means a 20-year mortgage can be paid off in 13 years with a little sweat.

If you have to start off with anything more than a 20-year, you can’t afford the house.

…… and you’d still pay too much in that case.

Why pay in excess of construction cost ($55/sqft for lot, labor, materials and profit) for a used up 20+ year old house?

Absolutely correct property market in Sweden is insane. Amortization requirements regulator started 1 of June last year didnt do much to stop the circus.

Next tool (not yet installed) is a debt ratio limit that hopefully will slow down the madness.

Politicians moving slowly and property market bubble could be a reality before next regulator is installed.

House prices are in fact flattening out….but for how long?

Got some spare change…wondering when that bubble hit Sweden I just might buy a few….in case I want one.