Bondholders, savers, consumers to be put through inflation wringer.

Inflation will rise above target, and that’s OK, the Fed heads who’ve been talking since last week’s meeting said. The Fed will hike rates, maybe faster than expected, but they won’t catch up with inflation, keeping the Fed purposefully behind the curve, and inflation will overshoot, and real interest rates will be deeply negative, whether you like it or not. That’s the Fed’s message emerging since the last meeting.

Today, Philadelphia Fed President Patrick Harker and Chicago Fed President Charles Evans echoed Fed Chair Janet Yellen who’d suggested on Wednesday that the Fed could try to push inflation above the 2% “target.”

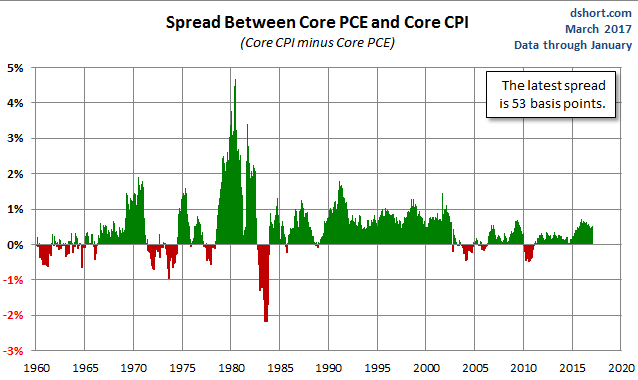

But the Fed’s measure of inflation is the Personal Consumption Expenditure index (PCE index), which is significantly below the Consumer Price Index (CPI) which already jumped 2.74% in February, year-over-year.

Harker, a voting member this year on the policy-setting committee (FOMC), told CNBC today that three interest rate hikes for 2017 make sense, and getting one of them “out of the way” in March allows the Fed to spread them out during the year.

“We don’t want to get behind the curve,” he said. But the Fed is already woefully behind the curve: The FOMC last week raised the target for the federal funds rate a quarter point to a range of 0.75% to 1.0%. The effective federal funds rate is at only 0.91%. That’s a real (after inflation) effective federal funds rate of negative -1.83%.

The Fed prefers the PCE inflation index, over CPI, because it understates actual increases in the costs of living even more than CPI. Headline PCE inflation index rose 1.9% year-over-year, as Harker pointed out, and core PCE rose 1.7%. Versus the 2.7% increase in CPI.

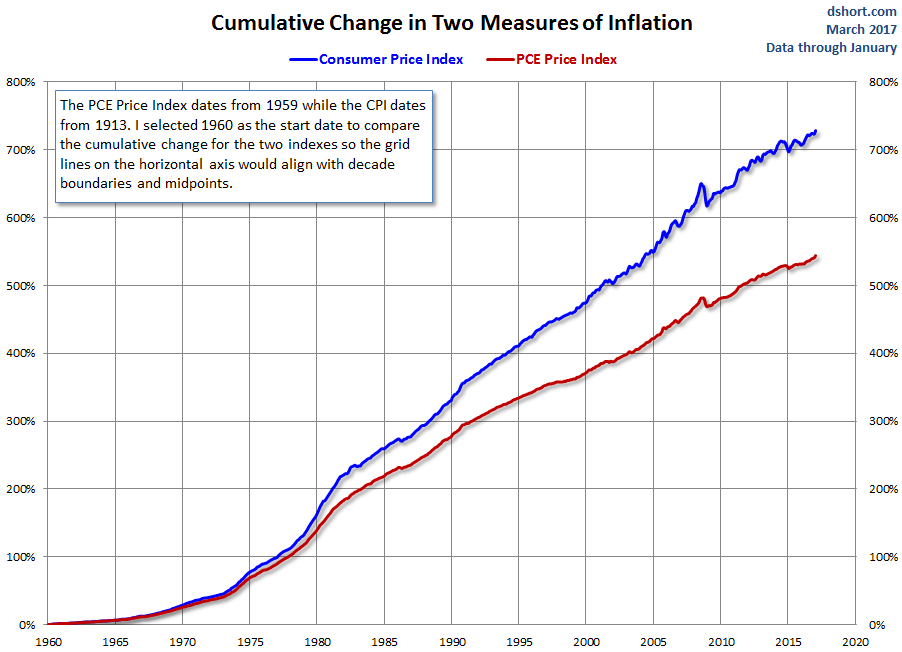

These differences are cumulative and get large over time. The two charts below, via Doug Short of Advisor Perspectives, show the differences. The first chart shows the gap between the core measures (without food and energy) of PCE and CPI every month going back to 1960. The green bars indicate by how much CPI exceeded PCE in percentage points. The occasional red bars indicate when CPI was smaller than PCE inflation:

And the chart below shows the cumulative effects of this understatement of inflation by PCE (red line) versus CPI (blue line). Click to enlarge:

So inflation as measured by PCE, is “within shooting distance of our target,” which is 2%, Harker pointed out. Hitting that PCE target would likely cause CPI to move closer to 3%. But it’s still not going to be enough for the Fed:

“I think we’re there, and we’re moving in the right direction,” Harker said. “There will be a little bit of an overshoot, and that’s OK, it’s appropriate.” The target of 2% is “not a ceiling” but “just a target.”

“You need to be concerned about is not so much the number itself but the momentum,” he said. “To me it’s more like what it feels like. Is it accelerating? Is it decelerating? We want to stay around 2%. I think we’re pretty close to that, and the momentum is in the right direction.”

Evens, also a voting member this year on the FOMC, chimed in today on Fox Business Network TV: Three rate hikes in 2017 are “entirely possible,” he said. “As I gain more confidence in the outlook I could support three total this year. If inflation began to pick up, that would certainly solidify. It could be three. It could be two. It could be four if things really pick up.”

“There’s room to get inflation up to 2%, and in fact going beyond 2% a little bit to make sure we get there, and that it’s a symmetric inflation objective, so that’s OK,” he said.

What “beyond 2%” PCE inflation will translate into might be something beyond 3% CPI.

If there are two more rate hikes this year, the effective federal funds rate will move to about 1.4%. Short-term government bond yields will be near that. After inflation, these bondholders will experience a loss of about 1.6% on an annual basis. Even 10-year Treasury notes, which currently trade at a yield of 2.48%, do not compensate holders for the loss in purchasing power due to inflation.

Prices would have to fall enough to where the yield rises to 3% or higher over the next few months just to keep up with inflation. Either way – either through falling bond prices or through below-inflation yields – government bondholders, which include already beleaguered pension funds of all kinds, are going to get screwed in this environment.

Not to speak of savers, whose lovely banks are holding $11.6 trillion in deposits but are raising deposit rates at a glacial pace, if at all. The average national deposit rate for jumbo 60-month CDs ($100,000 or over) is 0.81% as of last week, effectively unchanged since 2013, despite three rate hikes. So savers and other deposit holders are looking at losing about $300 billion or more this year to inflation. In other words, bondholders and depositors get to enjoy a long bout of financial repression.

Wage increases aren’t anywhere near these kinds of inflation numbers. However, to make consumers feel better, banks have already raised mortgage rates and credit card rates. So consumers too will be put through the inflation wringer.

It seems Wall Street will have to go look for another mirage to hype. Read… Stocks Soared on Trump’s $1-Trillion Infrastructure Boom. But that Just Evaporated. Now What?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not only are banks raising rates slowly, some are actually lowering them. It’s a single data point, but the deposit rate on my HSA (through work) dropped from 0.25% to 0.05%.

Please .. Wolf … anyone can you explain how Scott’s bank can justify / get away with this ?

And is this something we all need to be keeping our eyes on with our banks ?

Let me explain to my best knowledge.

Do you think banks still need your deposit to make loans? I am NOT a regulator so i do not know how their balance sheet work and what asset can they lend out by ratio to what capital/reserve requirement.

By the attitude they treat depositors, I do not think they need depositor’s money.

Even they need, and treat depositors badly, depositor can simply withdraw cash and no longer do business with them.

But can depositors withdraw? Can you withdraw your 401K,HSA,IRA which needs custodians?

When you withdraw your everyday money, in large quantities, you will be treated like a criminal and finCEN will be on your ass asking questions.

We used to be milk cows just paying for tax and bailouts. Now we are beef cows and getting hurdled into the slaughter house called banks and we will get slaughtered through inflation (purchasing power) and rate repression.

And there is nothing you can do about it. Those who take food stamps don not care since they have no savings. Those who uses apple pay thinks cash is useless and digital is so convenient. That convenience will give the power for banks to repress you, but would those convenience seekers care?

By the way. All these saber destroying moves are simply this. A traditional risk averting saver will make more and consume less and save for the bad days. What they really want is to make savers so uncomfortable that savers will start to seek risk. Then savers will gamble in wealth transfer engines and we all know 10 people go to poker table and all wealth will be transferred to one person in the end.

When money is not sound, there is no honesty way of living.

I have given upon saving. It doesn’t pay. The FED and the Government are slaughtering the Golden Goose.

Another application of Gresham’s Law: Fake printed capital will push out real honest saved capital.

Well the first answer came out a bit disparate and disjunct not really addressing the issue of how Scott’s bank as interest rates rise can justify lowering the interest on any account he may hold with . As for the second reply though accurate it still does not address my specific question . But … we do have an option . Change banks , 401K IRA HSA holders etc to a Shareholder owned company . We did [ not sure if Wolf allows company names in our comments but suffice it to say they used to advertise here ] and have been watching our annual annuities and investments soar reasonably well above the market average while all but eliminating the expenses incurred by the previous entity e.g. As in our bottom line soaring . as far as our personal banking is concerned .. suffice it to say I’ll be keeping an eye on their behavior now that I’ve seen what happened to Scott .. and should they do the same with our Savings – Checking – etc we’ll walk away in a heartbeat transferring our funds to either a Credit Union or a shareholder owned local bank .

FYI ; You’ll only come on finCEN’s radar if you withdraw large amounts of cash . Do it if you must with a cashiers check instead . And with all the cash floating around Colorado even since 420 legalization even if I did withdraw a substantial amount of cash I somehow doubt finCEN will even notice with everything else they’ve got on their table .

TJ, I have never studied depositor owned banks and how they work, but if that provides good terms on interest with incurring larger risk, then go for it.

My main point is that all symptoms of absurdity in banking is because bankers have power while depositors do not.

Depositors need banks more than banks need depositors for the two reasons i pointedness out. If that situation persists, expect more weird things to happen.

It is an HSA, with an administrator/bank picked by my company, so I have little choice in the interest earned. I did choose a health program with an HSA over other options, primarily because I’m healthy and young. Any amount saved (even earning nothing) is better than a more expensive plan. Think of it like picking a fund for your 401(K), you pick the best option available to you even if you would make different selections on your own.

I think it more points to problems with HSAs than with banks. Since starting mine, I’ve done a little research into them. A large number charge a monthly fee for investment accounts and the fund selection generally appears subpar and not low-cost. I think it’s a bit of the Wild Wild West for HSAs with comparatively little attention paid to them relative to the much larger 401K business (I’m also guessing that there is less regulation). In my opinion this is one of the major reasons that Republicans in Congress like them so much (the other being that the rich can use them to eliminate taxes).

Scott, I think you answered your own question–low yields are a consequence of centralization (no competition). I propose the stinking Fed KNEW that when they bailed them out with QE and the taxpayer dollars. We will never, EVER see demand account interest rates above 25 basis points, or at least until the Fed is locked down and Jamie Demon is hung from a lamp post. This also means that the economy will have green shoots only–never a reach escape velocity (never even get off the friggin launch pad). HOWEVER, when the economy DOES finally crash and burn, the Fed and the TBTJ commercials will ban cash out of desperation. Brother, you better have your demand account emptied and in a substitute…

The bank can only get away with it AS FAR AS SCOTT IS CONCERNED, if Scott continues to keep his account(s) there.

“However, to make consumers feel better, banks have already raised mortgage rates and credit card rates.”

Here in Oz they do it because………..they can.

“Two of Australia’s Big Four banks (NAB and Westpac) have just put up interest rates out-of-cycle on owner occupier borrowers. The reasons given? Funding pressures … Donald Trump … almost “the vibe”.

SEE:

http://www.theage.com.au/money/borrowing/big-banks-hit-owneroccupiers-with-116k-extra-interest-20170321-gv2rhs.html

Actually the spread between the central bank discount rate here and the ARM rate is much, much bigger than stated in the article as the data is limited by date.

IIRC the spread is now about 2% greater than at the time of the GFC.

Showing yet again why it is at least as important for the central bank to be under civilian control as it is for the military to be under civilian control.

To be sure mistakes have and will be made with the central banks under civilian control, but we can no longer allow “loose cannon” banking or “rogue” economic management.

Just what and for whom are the central bankers working? How does the Dow at 50,000 help anyone?

One could make a good argument that civilian politicians already have too much influence over Fed policy. President Nixon nominated Arthur Burns as head of the Fed in 1970 on the condition that he keep interest rates low. That policy later set off a strong burst of inflation in the mid-1970’s. The Humphrey-Hawkins bill of 1978 gave the Fed a second mandate in addition to relative price stability, namely keeping employment levels high. I doubt that the Democratic sponsors of the bill cared all that much about savers, if it meant higher unemployment among their working class supporters. Irresonsible fiscal policy by Republicans placed more of the economic policy burden on the Fed.

It only took the Germans about nine years to destroy their currency from 1914 to 1923. We have been luckier. More than 50 years after Lyndon Johnson’s guns and butter policy (the Viet nam war abroad and a growing welfare state at home), the US $ has actually performed better than the currencies of many of its trading partners (C$, pound, Italian lire, A$ and others).

Not lucky. The US is a RESERVE currency. The German currency was not. Also losing a couple of wars aside, the US still retains the full faith of the international community. The Germans lost this thing called World War I.

RE: …the US $ has actually performed better than the currencies of many of its trading partners …

—–

Less bad is not better.

The USD has performed quite well over time, actually.

Invested in risk-free treasuries, it has increased in purchasing power since WW2. Even just put into a savings account it has maintained purchasing power quite well.

The Federal Reserve was established as a division of the Treasury when originally formed in 1913. It was removed and made a separate agency in 1951. At which point it became accountable to only to the legislative branch, not the executive. And, of course, Congress reports directly to Wall Street.

The US Federal Reserve Bank is a privately owned corporation with a federal charter. All the stock is owned by the “member” banks. It has never been under direct governmental control and was never a branch of government. See:

https://en.wikipedia.org/wiki/Federal_Reserve_Bank

The FRB is a hermaphrodite organization with features of both a public corporation, i. e. stockholders, but the officers are named by the President and subject to Senate confirmation.

As a private corporation it is exempt from the FOYA laws, and unlike all other U. S. corporations, has *NEVER* been audited for finances, conflict of interest, or anything else.

As Clemenceau remarked during WWI “War is much too serious a matter to be entrusted to the military,” so too “the socioeconomy is much too serious a matter to be entrusted to the bankers.”

Here comes the middle class squeeze. Hope we all like eating hand sandwiches.

There really are ways for us “middle classers” to avoid a squeeze. See earlier postings of mine…

Wolf could’ve also discussed the sticky rate at the Atlanta Fed.

https://www.frbatlanta.org/research/inflationproject/stickyprice.aspx

Based upon the 2.6% rate of this version of the CPI this bodes more troublesome IMHO since this represents prices that historically do not change over time that much. In other words, cost/push inflation is not part of this metric but more likely demand/pull

I have said for a while that central banks around the world have been printing money and giving it to bank. This money is not invested in created new manufacturer plant and thus increasing real wealth of a countries,

This new money created goes into speculative asset such as housing, auto loans and stock market and commodities such as oil. Oil is high inflationary because it is at the core of modern society.

Some proof are starting to come out about central bank printing schemes.

http://www.cnbc.com/2017/03/20/op-ed-the-feds-stealthy-qe-267-billion-of-fresh-liquidity-injected-since-mid-january.html

The fed is now in panic mode and is afraid of hyper inflation because of this printing.

Banks do not need the federal reserve to print money for them. Banks print the money themselves. The federal reserve may print money, but they can only use it in exchange for other bank assets. So if a bank needs to make payment, and don’t have the cash, they can repo other financial assets with the Fed to get the necessary cash. This is not necessarily a good thing because they are generally exchanging interest bearing bonds for non-interest bearing cash.

However, you are absolutely correct that banks no longer use their loans (which is where new money comes from) to build new factories and productive capacity. It used to be that way prior to Reagan when the government had a number of regulatory structures which forced them to do so. It is far more profitable for banks to lend money against assets, because they know that the very act of doing so will increase the price of the assets. And this is very profitable for the folks who control the banks.

However, 99.9% of the population has absolutely no understanding of how the financial system actually works. So they will continue to vote for deregulation assuming that it will fix some problem, when actually it just makes it worse and worse.

“The fed is now in panic mode and is afraid of hyper inflation because of this printing.”

No they’re not.

The central banks never “printed” money as part of QE. QE was a glorified asset swap program. Which is why it didn’t lead to the inflation that people scaremongered about. Which is why the Fed was never worried about hyper inflation.

@Smingles — Re Earlier post ( No reply button )

“The USD has performed quite well over time, actually:”

Ha Ha ha – – what a load of absolute BS ! In 1915, a person with only $4.26 could buy the same amount of food, clothing, and other necessities as $100 would buy today. Or to use the BS “Official” USA Inflation rate you’d need $1903 in 2017 to = $100 in 1917 !

In case maths is beyond you that’s a $ loss in value of just on 95%!

http://www.coinnews.net/tools/cpi-inflation-calculator/

http://146.142.4.24/cgi-bin/cpicalc.pl? — (Govt Calculator)

Remember my friends…. Nothing accelerates the economy and creates jobs like falling prices to dramatically lower and more affordable levels.

Until these massively inflated prices fall, there is no economy.

Doing my taxes this week. An Atlanta super regional bank paid me a whopping $120 this year on an average daily balance of just under the FDIC limit of $250,000. Of course I must pay income tax on this interest income so I will not even net my $120.

The Fed is doing Congresses dirty work. The biggest beneficiary of Financial Repression is government. It allows the programs and benefits that sustain the parasites and underclass to be funded through issuing more ( low cost) debt and avoiding a tax increase on those with a job. Should the US government have to pay 4 or 5% on its debt mountain its game over for the clowns in Congress.

Why is it game over? The US prints its own currency. The US by technical definition can not go bankrupt. Now if you are talking about the loss of value, that’s a separate story, hence Wolf’s story about inflation.

RE: Should the US government have to pay 4 or 5% on its debt mountain its game over for the clowns in Congress.

—–

Indeed!

The fiscal situation may be even more unstable than most people realize due to the change in the term of the average bond shrinking. As short term debt is generally lower interest than longer term debt, as part of the debt management/rollover process short term bonds were used to replace long term bonds as these came due. Therefore any return of normal/historical interest rates will have a very quick effect on the debt management process.

FWIW — the UK gilts are 50 year bonds so the impact of a return to normal interest rates will be much more gradual.

My sister wanted to withdraw a large sum in cash, what a routine she went thru they tried to tell her she needed a guard to the front door after that the bank was not responsible.They told her that they had to report the transaction to the I.R.S. this was in new jersey .

Bank secrecy / anti-money laundering act. Fun stuff.

I entered the workforce two years ago after spending the entirety of my 20s in school or in training (medicine). Now I’ve been saving maybe 60% of my income every month but find nothing with attractive to invest in. I either buy into the S&P500 index (at ridiculous valuations) or the local housing market (at ridiculous valuations), or keep sitting on my cash, renting, and losing 3-4%/year through inflation. I’m just frustrated to no end here waiting for the correction I doubt the Fed will ever allow to occur.

Wow. You can save 60% of your income? After taxes and living expenses? I was never able to do that… After I got through paying taxes, SS, and the like, and then for housing expenses, a car, food, dates, etc. I was able to save, but dude, not 60%. I envy you.

Or was that a typo ;-)

Yeah, about 60% of my post-tax income is saved. I’m pretty frugal after living on maybe $25k/year for most of my 20s, but I’m also lucky to not be sitting on hundreds of thousands of dollars of debt either like many of my residency classmates.

The other issue driving the savings is that I may want to transition into something non-clinical or outside medicine in the future. The medical environment is rapidly changing for many physicians: we’re transitioning from a system of solo and small group private practitioners to employees of national mega-groups and hospital chains. Once a group sells out to a national group or hospital chain, conditions nearly universally get worse for the younger docs that stay behind as they’re now just turn-and-burn employees working a lot longer/harder for less. The trend has really accelerated the last 5 years or so, and with interest rates so low financing M&A activity, I don’t see it abating. Best to work hard now, save a nice nest egg and leave all options open.

OK, 60% of after-tax income is more plausible … good for you!!

The situation you describe for young doctors today is quite like the situation of junior partners in law firms, when I made the choices (I have written about here, earlier) sixty years ago: among them, forgo law school.

Your transition should, in my opinion, take you out of densely populated areas – you will quite naturally enjoy a much less “other people control my life” situation.

I my case I used a little savings and a lot of leverage to buy a big old mountain boundary and it has been my private domain (and Eden) ever since. For you, it could be comparatively easier – you would be able to purchase for cash.

Administration of your boundary will be entirely up to you (my boundary has provide surprising opportunities to generate income – not all of it cash, over the years).

Most importantly to me, I have not invested in somebody else’s enterprise – it’s my own.

Silver dimes

My situation exactly Mark. In trying to plan/build a future, it seems that the CBs of the world have purposely put up barriers to facilitate that end….essentially insisting that we all go “all in” now and forget about the future. Mr. Yellen even said that she would consider negative interest rates in the future “to encourage investment in risk assets”. All aboard the ponzi to keep the bubble going.

And you said they’d never bring NIRP here…

Not that you actually said that, but according to the above, it’s here. And nothing fancy about it like Europe or Japan. Just old school inflation.

Take it out if the bank. Leave it in the bank. Who cares?

As far as saving 60% of one’s income, it’s easy. But teetotalism is not a solution; it becomes the problem

“As far as saving 60% of one’s income, it’s easy. But teetotalism is not a solution; it becomes the problem.”

Not always true – it can be a temporary means to build capital for a less stringent life later.

When I was in the Army during the Korean war years I did not spend any of my “salary” at all, except to send some Noritake china home to my fiance. The savings were used to make a down payment on our first house.

What happens it seems is that many “savers”, like myself, calculate roughly what true market rates of interest on capital would be, and in the absence of any meaningful rates of return, have no choice but to save the difference plus an extra 2-3% to account for inflation. Problem is that as that nominal stash gets bigger, more and more savings is required to fill the gap. At a large enough level all additional savings is negated by inflation.

I sympathize with mark. I’m trying to save up for a house in socal. I wanna pay cash or mostly cash so I’m sitting on sizeable funds as I continue to save.

How can they’re be inflation when there is so much debt and interest rates are moving up. I thought new debt or money supply had to enter the system at a geometric rate. How will all this existing debt be serviced without ever expanding debt and lower interest rates? Somebody please explain this madness to me!!!!!

Why but a house when you can rent it for half the monthly cost?

Buy later after prices crater for 65% less.

Good advice HB

Any chance you could expand your target, away from So Cal?

Avoidance is a valid strategy, sometimes.

Let me try with my limited knowledge.

Currently, Goldman Sachs go to fed window and borrow 0.75% overnight on monday, promising to pay back on tuesday. This is the overnight fed funds market. Yellen’s rate rise is here.

Goldman Sachs then use the borrowed money go to buy 10year treasury at 2.75%. Tuesday comes, Goldman go to fed window again and borrow the same amount promising to pay back on wednesday, and then use the money to pay back the loan they take out on monday. This is rolling. Goldman makes 2% guaranteed. Since this is so guaranteed, they can leverage this operation by 10X and get 20% return on their capital that runs this operation.

The rate rise in 0.75% may kill this operation but it does not mean 2.75% 10 year will move. If goldman does not buy any more because of the rate rise of 0.75% then who is willing to buy 10 year at 2.75%? You are. Remember Obama’s myRA? Treasury will also call all the big funds, pensions, endowments, foreign sovereigns and say ” you guys have to buy at 2.75%” other wise …

This force buying is called “financial repression” as the title of this post.

Big chucks of interest rate increases with banks leading louder cheers each time the cost of money raises ?

Derivatives written when rates never went north and deals never went south?

Everyone is sitting on their hands waiting for some future date to ” go all in” risk free? ( in fear?)

Inflation is transitory! The number has been reached now we start backing our economy down to save the banks and force some moral hazard back into the world?

cagney

Inflation is the result of near zero interest loans chasing any thing that looks like it has a return on investment. Interest rates are only going up for the little guy.

Regarding existing debt….it will not be serviced just like it was in 2008

Rising rates will cause more inflation, it’s a virtuous circle. Low rates caused overproduction in energy (Chesapeake) and crashing energy prices. In a negative rate environment it might be difficult to sell enough bonds for the Trump stimulus plan, except of course bonds can be collateralized and put to work in the equity market, as long as rates don’t rise too quickly it works like the old discount window. Raise rates AND provide liquidity. All the pieces are in place for a stock market rally, Fed mandate number one. So Trump gets his stimulus and the market rockets higher, it’s all good of course. until you pull up to the gas pump. As wages pressure rises, immigration restrictions cut off wage competition, SS raises the retirement age, and a lot of 50 and 60 somethings who voted for Trump have to go back to work. That’s what I call poetic justice.