Commercial Property Bust to hit Multifamily Rentals in San Francisco & New York, the Most Expensive Markets in the World

Two reports – one on the most expensive rental markets in the world, and the other on the top multifamily “Sell Markets” in the US – have the same winners: San Francisco and New York City, where the dynamics have changed and, for landlords, are veering for the worse.

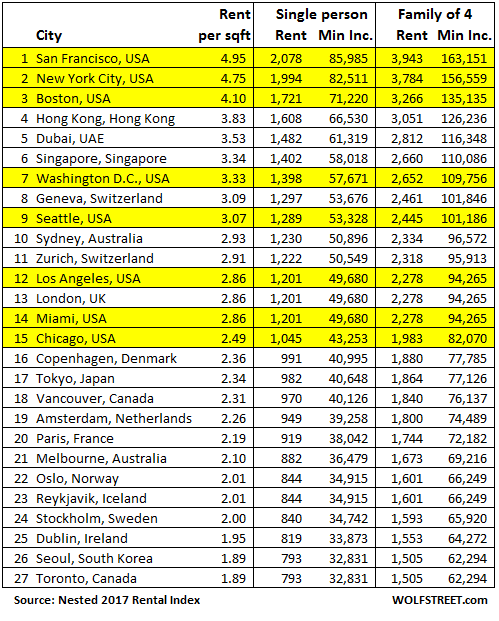

Of the 120 global cities researched by online property service Nested, the top three most expensive rental markets are San Francisco, New York City, and Boston. They easily blow away other global hot spots such as Hong Kong, London, Tokyo, Paris, Vancouver, and Toronto. After years of soaring rents in the US, eight US cities are among the 15 most expensive rental markets.

To measure affordability, Nested’s report compares the cost of rents per square foot. Based on the minimum recommended dwelling size for a single person (420 square feet or 39 square meters) and for a family of four (800 square feet or 74 square meters), the report calculates the minimum incomes required to be able to rent in these cities (with rents not to exceed 29% of gross salary).

The table below shows the top 27 cities in Nested’s 2017 Rental Index. I chose the top 27, rather than the top 25 or 20, to get Toronto on the list. We’ve covered the ballooning house price bubble in Toronto (#27 on the list) and the now deflating house price bubble in Vancouver (#18) many times, most recently with the January numbers. Both cities measure among the most expensive in the world in terms of house prices, but are way down in terms of rents. This is another indication of just how precarious their house price bubbles have become.

In San Francisco (#1 on the list), rents cost $4.95 per square foot. So a single person in a 420 square foot studio, costing $2,078 a month, would have to earn $86,000 a year in gross salary (before taxes, social security, and the like) to be able to rent and have some money left over for living expenses. For a family of four, the income requirement jumps to $163,000 a year:

Since the table is in US dollars, exchange rates influence the rankings. But it’ll do for our purposes. Within the US, these three most expensive rental markets are the same in other reports I have cited. So there’s some rare agreement in the data. And in these markets, rents have begun to drop sharply, though they’re still soaring in Mid-Tier Cities.

San Francisco and New York have gotten so ludicrously expensive, and have so much new supply coming on the market, just as their economic growth has begun to slow, that they’re now the top two SELL markets for investors, according to Ten-X Research’s report and outlook.

In the US overall, the multifamily market is “still strong but fundamentals are weakening,” and some “face worrisome market dynamics.” The report summarizes:

The Bay Area is seeing high development and is the most exposed to a change in cyclical dynamics. NYC and Boston are seeing building booms, while Northern NJ will struggle as availability in neighboring NYC rises. Miami too is seeing high development at the wrong time cyclically.

As development rises, most markets will see vacancies creep higher, slowing rent growth. It appears the apartment cycle is drawing closer and closer to the end.

In some cities, the dynamics have soured. Expected rent declines through 2020 and surging vacancy rates are turning them, for landlords, into the “top sell markets”:

#1 Sell Market: San Francisco

- Though there was still “solid annual employment growth” last year, the pace has “decelerated to the mid-2% range with major sectors losing steam.”

- Apartment vacancies “have been rising steadily” from just above 3% in 2012 to 4.4% now.

- “Persistent heavy supply will boost vacancies north of 6% by 2018, and even higher in our 2019-2020 recession scenario.”

#2 Sell Market: New York City

- The city’s pace of employment gains has “decelerated to the mid-1% range with slowdowns in most of the metro’s major sectors.”

- Vacancies have risen nearly 2 percentage points from recent lows to 4% in Q3.

- “Heavy supply additions in Brooklyn and Queens will boost vacancies north of 10% by 2018.”

- Expect rents to decline “by more than 5% through 2018 as vacancies mount. Rents will fall even further as our 2019-2020 scenario takes shape.”

#3 Sell Market: San Jose

- Another city subject to Bay Area dynamics. While metro employment is up nearly 3.4% year-over-year, job growth is now decelerating.

- Apartment vacancies rose 0.5 percentage points from a year ago to 4.1% and are “forecast to continue rising past their highest recorded levels as demand falls off amid a robust pipeline, reaching 6.5% by 2018 and climbing to the mid-8% range under our recession scenario.”

- Rent growth has been cooling rapidly to 1.5% from a year ago, with no more than “tepid growth” next year. Rents will “begin declining by 2018, ahead of our 2019-2020 stress test scenario.”

#4 Sell Market: Miami

- The number of jobs rose 1.6% “but the pace of growth has slowed over the last year.”

- Apartment vacancies rose 0.7 percentage points to 4.7% in Q3. And a lot of new supply is in the pipeline, “boosting vacancies to a historic high above 8% by 2018 and past 10% in our 2019-2020 recessionary scenario.”

- Effective rents are at an all-time peak, “but growth has already decelerated and will continue to slide as vacancies rise.

These multifamily properties are part of the vast commercial real estate bubble that the Fed is now confronting, with an eye on the banks that have made it possible. Various Fed governors and even Fed Chair Yellen have been voicing their fear of “waiting too long” to raise rates to cool it all down. Or of “having already waited too long?” Read… Fed Frets about Commercial Real Estate Bubble & its $2 Trillion in Loans Mostly at “Smaller Banks”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Most major landlords in Manhattan require income of 40 to 50 times the rent.

when I went shopping I was told 50 to 60x. So a $4K per month apartment needs a min $200K income. All in at that level NYC residents will pay north of 40% in taxes. So $120K after tax and $48K in rent.

Amazing amount of wealth coughed up for an average dwelling. Kinda like sending your kid to college. Same price, same value.

Get your employer to cover your rent. Should be part of any decent compensation package. Winning. ;)

Yeah. I know. Fuck’em.

The most overpriced and demanding landlord I encountered, was Equity Residential in Florida. They asked us for income of 5X the rent because of our bad credit(foreclosure). If we had that kind of income we would never rent from them, crazy.

@Petunia That was their way of excluding anyone with a mark on their credit history without running afoul of any fair housing laws.

What’s not fair or logical or reasonable about that?

This is really about the elite, isn’t it ?

I live near enough to Boston, rents in my neighborhood are up YOY, but nowhere near obscene.

I see writeups in the Boston Globe all the time celebrating what you can get for $1.2M or $2.6M or even $4.7M, and wonder who they thing their target audience is ? Elitist rag . . . . .

This is 1929 redux, I am sure of that.

SnowieGeorgie

Jimmy rogers come back home?

I love the way libertarians (Jim Rogers, Sovereign Man, etc.) are touting Singapore as the best country to move to. Sure, go to one of the most politically repressive countries in s-e Asia and express your personal freedom! (I lived there for several years.) I suppose they can blind themselves with all the money they think they’re going to make.

/sarc

They broke up the homeless camp behind the kohls yesterday!

The people moving south got escorts, the ones from Denver push up rental costs?

The elite did a good job on us the sheeple. They purchased all the assets which would rise in value in a high inflation scenario by free money courtesy of us the sheeple and our overlords, the feds. Good job.

They are already planning the next phase of transferring of wealth. After the next phase, 10 chosen billionaires will own 99% of the worlds wealth. You gotta love it when they actually call it capitalism. If Adam Smith comes back to life, he’d be laughing his ass off if he heard this as being considered capitalism.

What Adam Smith never thought of is the industry of hiring one half of the poor to kill the other half.

isn’t there a wolf article that says 8 people own half the world’s wealth. I’m pretty sure we are past 10 chosen billionaires with the world’s wealth.

http://wolfstreet.com/2017/01/16/8-men-own-as-much-as-poorest-half-of-world-oxfam-reports-global-elite-in-davos/

Yes Erica; but the next phase will be only 10 billionaires and they will own 99% of the world’s wealth. Then our slavery will be complete.

I have a bunch of savings, wanting to buy a house but I’m thinking I should wait until this bubble bursts. I’ll keep renting.

Smart move for sure because it’s a comin and it’s gonna be a doozie

Any idea when? 2018? 2020?

Ideally I’d like to buy something priced like it was back in 2011/2012 (the bottom). But of course no one can predict the future.

The cost of transferring ownership of a house is very expensive: Down payment, inspections, real estate commissions (paid for by seller, so is thus built into their ask price), moving, painting, furniture, etc. You should only buy a house if you’re willing to stay at least 3-4 years minimum.

(Disclaimer: if you live in NYC, San Fran, Vancouver, or some other hot market, my advice below does not apply. For those markets I don’t see any good answer to your dilemma other than moving to an area that isn’t overheated).

But if you plan on staying in your current area for this long, and could find other employment if you lost your current job, then I see no reason not to buy. Even in Bubble 1.0 prices didn’t drop all that much, and it was only for a short period of time before they started to rebound. If you plan on staying in your house for at least 10 years then you’ll be in it long enough to ride out a drop and still end up with appreciation. In the meantime you’ll be building equity.

If you sit around waiting for a major shock to occur before buying you’ll probably be too scared to buy when the time comes, thinking that the “other shoe is about to drop.” It’s hard enough to time the stock market, and you want to try to time the purchase of the most emotional of all purchases? You’re going to fail at this. Having bought and sold two different houses in my life I know how much regret and angst can occur, and I consider myself to be a very stoic, reasonable person. Don’t try to play this game with houses. Speculate with something else.

Put 20% down, mortgage payment no more than 25% of income, buy in a good school district neighbored by other good school districts (in other words, not on the border of a neighborhood that may go south), and don’t pour money into any major renovations. You follow that advice and stay in the house for at least 10 years you really can’t go wrong.

If you think we’re headed for great depression 2.0 or worse then buy a small house on a large piece of land in the middle of nowhere with access to fresh water, get your solar/wind off the grid thing going, farm your own food, and live like a wacko.

Mid cycle Real Estate Pause arrives in 2019. Top of cycle is 2026.

The Secrets of Real Estate and Banking by Philip J Anderson.

Wolf,

In your opinion are mid tier cities rents increasing due to property speculation? I hear numerous radio programs talking about rental investment out of state. Coincidence?

Lots of speculation going on, for sure. But each city has its own dynamics.

The main theme is, I think, that the most expensive markets have hit that pin, and so the bubble burst even though the local economies are still pretty decent. So what happens in those cities when the local economy is no longer pretty decent?

There is also some flight going on from expensive markets to cheaper markets. Detroit is a big beneficiary of that. Downtown has been revitalized and has been drawing in people for years. Charles Schwab, which is headquartered in SF, has been sending jobs to cheaper areas for years while cutting its footprint in SF. Other companies do that too. It means people move and dynamics change.

The expensive city’s will eventually die, unless they can keep enough high paying job’s there to keep themselves alive.

When Hillary Clinton called Trump supporters the Deplorables that’s when she lost the election because her own supporters identified with that. She was calling them stupid. Sometimes the truth hurts

Just a reminder: she won the popular vote by about 3 million voters.

The Hillary won the popular vote by 3 million . . . .

OK, I’ll concede that arithmetic.

But when you look at a county map of the USA for both Obama elections, and one of the Donald’s, something is very much out of whack.

What if you put up the popular vote totals for JUST CALIFORNIA, and then for the remaining 49 states of NORMAL AMERICA ?

http://www.jsmineset.com/2017/02/12/the-coyote-principle/

What would you have then, a sweeping win for Hillary in the popular vote ? I think not.

BETTER YET, take out the 3 to 5 largest LEFT COAST Population Centers, you know the coastal elites — who — like Hollywood, do not represent mainstream American values.

Take out the two left coast elite populations, and then ask who won the popular vote in the rest of Normal America ?

DISCLAIMER : I am a massive social liberal, very pro all of the “correct” things, like abortion on demand, and gay marriage to name just two. But I am a fiscal conservative, and thus have no home here — anywhere — in America.

One last thing, Reagan was no Republican hero, he was a traitor to fiscal conservatism, as has been every Republican President since Nixon.

SnowieGeorgie

Check out my reply to John Doyle. This matches some of the points you’re making.

“BETTER YET, take out the 3 to 5 largest LEFT COAST Population Centers, you know the coastal elites — who — like Hollywood, do not represent mainstream American values.”

What are “mainstream American values” and why are some Americans — by your diktat — excluded from determining them? Why would, by definition, a minority of Americans determine what the “mainstream” is? If 90% of the country were “coastal elites” wouldn’t they be the “mainstream”? This isn’t 1776, it’s 2017.

“Take out the two left coast elite populations, and then ask who won the popular vote in the rest of Normal America?”

But… why would you do this? America is America, a hugely diverse, in every sense of the word, nation. There is no “normal” America. Selectively excluding certain groups of people because they don’t agree with your politics is decidedly un-American, and makes no sense to boot.

Hi Smingles

There was a lot of sarcasm and cynicism in my post, and with sarcasm, it is much less effective if you strongly label it up front

NORMAL AMERICA in my post is the same as what the analysts were calling “flyover America” in their many post-election post-mortems

As for the coastal elites — the big-city and big-money people who live in a rarefied world where income is extremely high, and a million dollar property is only a bungalow, I stand by my disdain for them all — Hollywood being the archetype here. ( See Wolf’s many posts on the big city property bubbles. )

The fact that the big money elites control the republican party — and now, sadly — the democratic party — means that “mainstream American values” have been abandoned for mammon.

Only as a single, and perhaps the worst example, the ongoing carnage in Chicago got nary a mention from the big O during the eight long years of his presidency.

Worldwide family trips on Air Force one; annual winter vacations in Hawaii; annual summer vacations in Martha’s Vineyard — and aside from calling out the occasional single Chicago murder victim of high personal interest — NOTHING FROM THE OBAMA PRESIDENCY FOR CHICAGO. NOTHING ! ! ! !

Our first President of color ignored a seething hot war zone in Chicago for eight long years — he lived high and vacationed even higher — and then left for a fine future for himself and his family.

Every black family in Chicago has the same worth as Obama’s family, do they not ?

You bet I have high disdain for the big money coastal elites — they have captured the USA government, and the hell with everyone else.

Obama’s Imperial lifestyle, and his ignoring the carnage in Chicago, are merely symptoms . . . . .

SnowieGeorgie

Wasn’t it all in California? 3 mil there I read at the time.

Here are the results for the Big Three states. You’re not far off the mark in California where Clinton won by 4.2 million votes…

http://www.nytimes.com/elections/results/california

and here’s New York, where Clinton won by 1.8 million votes…

http://www.nytimes.com/elections/results/new-york

Here’s Texas where Trump won by 800,000 (note that Clinton won in Dallas, Austin, and the entire Texas Gulf Coast, including Houston and surrounding counties)…

http://www.nytimes.com/elections/results/texas

Throw out CA and trump wins pop vote.

Throw out TX and she wins EV.

She won more small states than he did.

EV exists because that was the deal the big states of the day had to give the little ones to get them all to hang together against England.

He won the election not because of small states but because he narrowly carried states that had voted dem for half a century. Or, 10 million that voted for a black man in 2008 stayed home in2016. Deplorable maybe, but not racist.

I believe she was referring to people who rooted for (or turned a blind eye to) the terrible behavior of a potential leader, because they selfishly thought invisible manufacturing jobs were coming back.

It reminds me a bit of when Henry Ford was forced to increase pay by quite a bit, because people were disenchanted with monotonous factory jobs after working on farms, so he had a hard time with retention. Now people are having a hard time accepting that they need to transition from the factory to service jobs like in the fast food industry.

Too bad that most people here don’t understand or haven’t heard of the Electoral College. Time to amend the Constitution – good luck with that.

Hillary lost my vote when she was first lady(she managed to tarnish that title and yes, I know it should be capitalized, but she doesn’t deserve the emphasis).

No she certainly doesn’t Petunia I loath that woman and her so-called “husband” The word psychopath comes to mind

Feb 15, 2017 Janet Yellen Just Revealed Something Huge But No One Is Listening – Episode 1205a

Mortgage delinquencies are on the rise. Corporate media reporting that retail are incredible in January, gas prices increased and inflation moved higher. Consumer prices surge at the fastest pace in 5 years. Industrial production declines and is at 10 month lows. GDP has been recalculated and is now down to 2.2%. The US is not in the top 10 for economic freedom. The markets are whispering something very important about inflation. Janet Yellen comes out and admits the economy is weak and don’t blame the Fed.

https://youtu.be/m6Q0kqNCUpU

Toll Brothers to Pay Manhattan-Condo Taxes to Attract Buyers

https://www.bloomberg.com/news/articles/2017-02-15/toll-brothers-to-pay-taxes-on-manhattan-condos-to-lure-in-buyers

San Francisco is also very car unfriendly. If you don’t have off street parking you can expect to pay parking fines regularly. I used to warn people to check the street cleaning schedule before they rented a place if they had a car. Nothing like having to get up Saturday morning to move your car only there was no place to move it to. You either went and bought breakfast or drove around for an hour.

At least in some of the other expensive cities, apartments might come with a parking space.

I see that ‘super expensive’ Tokyo is only number 17 on the list and ‘property is going to crash’ Melbourne is number 21 on the list. Osaka and Nagoya aren’t even on that list.

And ‘super bubble’ Sydney is number 10 on the list. Shows the difference between housing in the two cities and one reason why people are moving to Melbourne.

All you have to do to get cheaper rent is move from the CBD/near CBD suburbs.

Even in Japan it is cheaper to buy in many places than rent.

You can buy a nice house on a 1000 square meter block of land within one hour of Tokyo for around $250,000……………

You can’t do that here in Melbourne and you probably can’t do that in many places in the USA.

These are RENTS, not purchase prices. HUGE difference. Lower rents in areas with high property prices throw the whole equation out of balance and turn property booms into bubbles that will sooner or later pop because rents are among the supports for property prices.

I pointed this out in the article using Vancouver and Toronto as an example.

If anything, those numbers for Vancouver seem a little on the high side. Renting in Vancouver isn’t cheap, but more expensive than Paris or Amsterdam or Stockholm? I’m skeptical. But your general point holds, for sure.

How can employment be up when corporations in Silicon Valley have been laying off thousands of workers for years? Which companies are doing the hiring? The housing market in CA should go down by are least 50%. I enjoy your site!

Let’s be real about Silicon Valley employment i.e. there’s been enough start ups to absorb all those job losses. This is borne by SF Bay Area employment statistics. Don’t be bitter.

People are still lining up for 5 dollar coffees here.

Really? Please name these startups that are allegedly absorbing the job losses. I’m not being bitter, I’m being realistic. Everyone says the economy is doing great, but no one can name the companies that are hiring Americans. Oh, and the statistics in the Bay Area and nationwide are fabrications, and have been since the 90s. The government uses seasonal adjustments and the birth/death model to overestimate job gains.

About 2 years ago I drove up on US1 in Florida, from Hollywood at the Miami Dade border up north to Boca Raton. It was wall to wall apartment complexes newly built in the previous year or two. I wondered who was going to be renting all those small expensive apts. There are literally thousands of apts, all built in the last few years. This is all north of Miami.

The jobs to support this are just not there or anywhere in south Florida.

Oh…. people need jobs to support paying rent? Details, details …

Your sarcasm is not far off base. My general feeling, at the time, was that I was looking at the “projects” of the future. My understanding is that the vacancy rates at these places are still high, in a tight rental market. When you drive by these new developments they look semi deserted.

I would guess that these apartment complexes will be for East Coast retirees. Decades ago, my maternal grandparents retired, and moved from New Jersey to Deerfield Beach. Half of their neighbors were of similar demographics. Florida’s Gulf coast has much more retirees from the Midwest.

I like to say this about Florida, “The further north you go, the more in the south you are.”

Petunia,

I lived in FL in the mid ’80s (Tampa Bay) and remember when Reagan did something to the tax laws that caused my employer to have a change of heart (i.e., quit), and caused out-of-state and local property owners to want to sell their rental units. Whatever that tax law change was, it caused an overnight reassessment of everything financial. There were lots of rental units being built back then, too, in the Gulf Coast counties. The expectation was that rich Yankees would buy them up (until they didn’t of course).

Aaaaaahhhhh, Wolf! Now THIS is porn. good, down home, wholesome, corn-on-the-cob porn. not the creepy kind where you feel shame, disgust, and hate yourself for ingesting and soiling your soul and any shreds of innocence you might be lucky enough to have left after making it past the ’80s and ’90s with any sense of romance left.

i know that falling rents surely means us po’ folks will be making soup out of our own feet by then, but oh my god we need some RELIEF from all this brutal money and death death death…

i knew i was hanging around these hear parts and gulping my hollywood starlet size handfuls of red pills for a REASON. i’ve been duly rewarded with today’s post.

cheers, salud, thank you for a flicker of a sunrise beyond the perpetual moon in a sun-setting america.

x

sorry i meant to write “here” instead of “hear.” i used to make fun of people who couldn’t get homonyms right. but that’s when i was 8 years old and only had to remember my home address and phone number.

Wolf, the fundamental flaw in this is using usd. London was theoretically more expensive than HK (dollar peg) then cheaper after brexit? Salaries do not go up and down with currency and are pretty stuck in most countries. This is not a good way at looking at affordability…..

Agree, as I pointed out in the article. But you’ve got to have a common denominator when you compare. Dollars is one of them. Percent of disposable income might be a better one. But that’s always tricky too.

Also the focus of the article isn’t on affordability – though that’s always interesting to look at. It’s the top sell markets in the US.

Hey Wolf, how exactly are rent prices related to home prices? I’d like to purchase property but it seems like almost everyone agrees the housing market is in a bubble. If home prices come down, will rent come down as well?

Thanks

In many rental markets, this happens the other way around. Rents decline first, making those rental properties less attractive, and prices follow.

“Rents coming down driving retail prices down.”

In the world before Wall-street hedge fund’s, moved into the stand alone family home market.

They can afford a larger vacancy rate, for longer.

Hence then Local rental price can be held up, in areas they own, as they tend to own zones, and in some cases suburb’s.

Which can hold up the rates in an entire city sector.

The US Property Market, just like it’s stock Market, is still severely disconnected from reality, by QE.

With coming downsizing and proposed decentralizing of the federal workforce in Washington, DC – dare I say ‘Winter is coming’ or does that phrase need to be retired? – a drop in 2018 tax revenues (income, sales and property) for the city and adjacent states (Maryland and Virginia) will most likely occur. If it does then I’d expect local rents and especially property values will take a leg down.

“– a drop in 2018 tax revenues (income, sales and property) for the city and adjacent states (Maryland and Virginia) will most likely occur. If it does then I’d expect local rents and especially property values will take a leg down.”

Followed by a rise in tax rates, Service cuts, or new taxes, when was the last time an administration, ever absorbed a reduction in revenues????

I should have elaborated: the loss of DC federal jobs with the accompanying drop in city & state tax revenues will trigger municipal & state job losses. Eventually the hit to the local economy will lead to private sector losses as well.

“the loss of DC federal jobs with the accompanying drop in city & state tax revenues will trigger municipal & state job losses.”

Job losses? or much more likely a reduction in new hire’s until the equilibrium is returned by retirements.

By the time muni’s and states, accept they have to cut staff, then actually get around to doing it, they usually have large numbers of low level staff, repeatedly polish the same window’s.

I currently live in the Washington DC area and I don’t quite understand how Nested’s 2017 Rental Index came up with $57,671 for the DC area. Unless you live in the most crime infested area of DC, you can hardly live with that salary. I currently live in the DC area and you need a minimum of $90,000 due to the high cost of living and all the taxes I need to pay for practically everything. This analysis underestimates a lot….