Workers, bondholders, savers get sacked. So what would Yellen do?

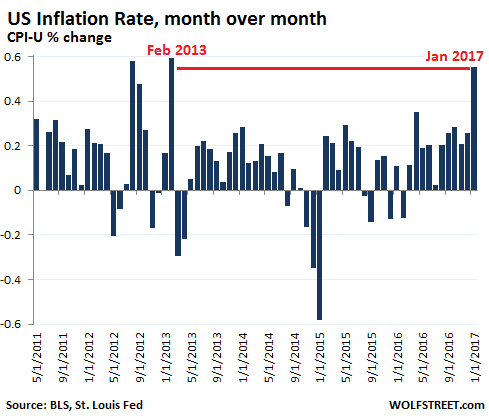

Consumer prices surged 0.6% in January from December, double the consensus forecast of a 0.3% rise. The sharpest monthly increase since February 2013, according to the Bureau of Labor Statistics.

Energy prices jumped 4% month over month, including gasoline which jumped 7.8%. Food prices edged up 0.1%. Within this group, “food at home” was unchanged, but prices for “food away from home” – restaurants, taco trucks, and the like – rose 0.4%. In just one month, the prices of apparel rose 1.4%, of new vehicles 0.9%, of auto insurance 0.8%, of airline fares 2.0%. Shelter rose “only” 0.2%, as the national numbers are now feeling the downward pressure on rents in some of the most expensive rental markets in the US.

This chart shows just how sharp that jump in monthly price increases is, compared to recent years:

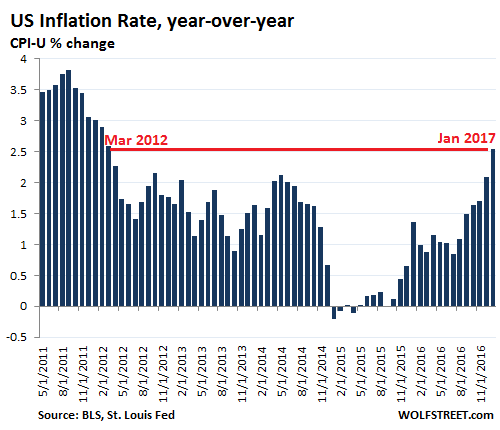

Compared to January a year ago, consumer prices as measured by CPI-U surged 2.5%, after having already jumped 2.1% in December. The rate of inflation has now accelerated for the sixth month in a row. It has surged one full percentage point over the past four months and hit the highest rate since March 2012:

So-called core inflation – which excludes food and energy – jumped 2.3% in January from a year ago. The consensus expected 2.1%. So you can’t just blame the rising costs of energy. This “core” measure of price increases has been above 2% since November 2015. Even during the Financial Crisis, when overall year-over-year CPI dipped briefly into the negative, core CPI remained in positive territory.

However much these inflation measures may understate actual increases in the costs of living that people experience in their daily lives, even those understated measures are now beginning to exude a lot of heat. And afterwards, the consensus will say that no one saw this coming.

So here is what inflation does to workers and consumers: it eats up the purchasing power of their wages. In that vein, the Bureau of Labor Statistics also reported today that real (inflation adjusted) average weekly earnings dropped 0.6% in January from a year ago, as nominal wage increases were more than wiped out by inflation.

But businesses are in denial, according to the Atlanta Fed’s survey of Business Inflation Expectations, also released today. Businesses anticipate 2.0% inflation over the coming year. That’s down from two months ago when they expected inflation over the next 12 months to increase by 2.2%.

The Fed has a special term for this phenomenon of denial: inflation expectations are “well anchored.”

Bondholders are in denial too, or they quietly accept “financial repression” as their fate. This is when yields do not compensate bondholders for the loss of purchasing power of the principal when the bond is redeemed at maturity.

The 10-year Treasury yield inched up today to 2.5%, even with January’s year-over-year inflation rate. All shorter maturities are way below the rate of inflation with the annualized 3-month yield at 0.53% and the 2-year yield at 1.25%. At these yields, inflation consumes all of the yield plus some of the purchasing power of the principal. In other words, investors end up in the hole.

Savers have been forced into financial repression since whenever, but no one cares about them. They’re sitting ducks. They’ve been among those that were tasked by the Fed to pay for the biggest wealth transfer of all times that is now morphing into the next stage via inflation.

So what would Yellen do?

The fear of “waiting too long” to raise rates is spreading. The Fed Chair has been voicing that fear recently, as have other Fed governors. But there are some Fed governors who have been suggesting that “waiting too long” is just fine. San Francisco Fed President John Williams said last year that the Fed should consider targeting inflation in the range of 3% to 4%, which would more effectively wipe out savers, workers, and those bondholders who bought their government instruments when yields were near zero.

More Fed flip-flopping is expected. But at the current pace of acceleration of inflation, even the doves are waking up.

The Fed focuses on the core PCE inflation index, which is usually lower than the already understated CPI index and largely detached from the reality of rising costs of living that many people experience. So the Fed’s target of around 2% inflation – which it ironically calls “price stability” as part of its Fed propaganda speak – is based on core PCE. In December, the core PCE inflation index rose 1.7%. Not far off the Fed’s target. A little push in January will get it there.

The surge in consumer prices also sheds some light on retail sales for January reported today by the Census Bureau. Retail sales rose 5.6% year-over-year. But they’re not adjusted for price changes. For example, gasoline sales jumped 14.2%, based largely on the soaring prices mentioned above. Take the price increases out of the equation, and suddenly retail sales don’t look so hot anymore.

The Fed is already sitting on a powder keg, after years of QE and zero-interest-rate policy that have caused mind-boggling asset price inflation, including in housing, which is filtering into the costs of living. During this period, corporations and governments have loaded up on record amounts of debt, as have many consumers. But someone owns this debt as assets. Now add a surge of inflation to the mix, along with the Fed’s reaction to that surge, to get some possibly very toxic effects along with some new groups of losers of Fed policy, or the same groups of losers, as decided by the Fed.

Is it the fear of “waiting too long” or of “having already waited too long?” Read… Fed Frets about Commercial Real Estate Bubble & its $2 Trillion in Loans Mostly at “Smaller Banks”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

I read this article about the Weimar Republic and was wondering if this is the aim of the elites?

“First, it would be wrong to think that everyone was opposed to inflation. Many big business leaders accepted it cheerfully. It wiped out their debts. They knew how to protect themselves and even profit–by speculating in foreign exchange, by converting money into goods and fixed plant, by borrowing money from the bank and using it to buy up cheap stocks and competing companies. Their wage costs, in true value, decreased, swelling their profits.”

http://www.usagold.com/germannightmare.html

Also I cannot understand how Trump can cut taxes, increase infrastructure & military spending without revving up the printing presses. Has Trump forgotten about the $20 Trillion US debt and $105 Trillion in US unfunded liabilities or is he delusional?

Trump can’t spend a dime unless Congress is complicit. The news media along with the average American, needs a lesson in basic civics. He is not a king even with Executive Order which is a power not given to him by the Constitution.

Thanks’ John. Learning new things everyday.

So, the question is then, will Congress be complicit?

When Obama was in power the debt ceiling was ‘supposedly’ pretty firm in Congress with mandated cuts in spending to match any spending increases. Today I read on CNN that ‘earmarks’ are being reintroduced under a new name.

My question is: How will Obamacare be replaced and improved with no changes in coverage mandates…at a lower price? Plus, infrastructure spending, increased military spending, tax reduction and reform, high speed rail, and the border fence? All this while deporting illegals who perform low-cost but vital work?

No worries, Mate. Eat, drink, and be merry. The music will never stop.

Both parties always vote to increase the debt ceiling because they really don’t care. They always do it as a last minute kabuki show to add urgency and drama. The debt ceiling is 20T now and will probably go to 30T before long. If there’s one thing our new president has a lot of experience with, it’s using credit.

@Paulo

If the GOP actually repeals Obamacare, they will change the coverage mandates. Think how crappy some insurance plans were before Obamacare, and that is what we will probably end up getting. Most people will most likely be happy about it since it is costing them less upfront. However, if they get seriously ill or injured, they will soon realize how worthless their insurance plans are. I would expect to see bankruptcies from medical bills to soar again.

Another idea that Republicans love is Health Savings Accounts (HSA). The problem with HSA’s is that most Americans don’t even have $1,000 saved up. HSA’s are another good way for the better off to put away money for retirement tax-free. Other ideas are high-risk pools that funnel chronically ill people into. The problem with high-risk pools is that they have been tried before and failed miserably. Typically, politicians don’t fund these pools adequately so the burden ends up falling on the sickest in society. People that were in high-risk pools end up spending on average 29% of their income on health insurance, which makes it unaffordable. Another problem with high-risk pools are the long wait times due to lack of funding. Again, though, most people will benefit from funneling the sickest into high-risk pools since their (healthy people) rates will decrease.

Republicans are in a pickle since the ACA was the Republican plan. Its framework comes from the Heritage Foundation, and it was pushed by Newt Gingrich in the early 1990’s. Mitt Romney had a similar plan in Massachusettes. Republicans’ constituents are now finding out that the ACA and Obamacare are the same thing. With Republicans not backing the ACA, we will see health insurance companies dropping out of the market. I am hoping for the best since I am chronically ill, but I am expecting the worst.

Cutting the deficits would really mean taking on either the defense industry or the medical establishment. Or raising taxes.

Anyone really think this Congress is willing to do any of those things? The national debt will continue to grow unabated.

“Also I cannot understand how Trump can cut taxes, increase infrastructure & military spending without revving up the printing presses.”

He is a master negotiator. He’ll threaten other countries to pay up or he’ll take the US economy to the cleaner which will mean other countries too will blow up. In other words, other countries will pay for his programs. Witness all those foreign central banks buying up US equities as well as foreign leaders pledging to help Make America Great Again.

Thanks’ NotSoSure, that was a cool reply! I am not from the US, but I follow US politics and economy.

That’s just a pipe dream. “Master negotiator” is a six time bankrupt and other countries are on the verge of blowing up even without paying up for his brilliant plans.

Right! 45% border tax will also help. Well, maybe 45% is too steep, but it can be negotiated at, say, 15% in exchange for investment into the US infrastructure.

In truth, the problem with the US infrastructure building is too much bureaucracy. By the time all permits are received and paperwork done, the policy may change again. Another problem – runaway budgets. Everything woul cost 3 times as time, just look at F-35.

I hate to give him any credit but his insistence on NATO countries spending more to reach a 2% gdp buying on defence will increase USA sales of all kinds of military hardware that USA makes plenty of.

The gold sites sell fear. I own gold. I know why I own gold. But, reality is a complicated, fickle, and unforgiving beast. I started my journey of figuring things out back in ’07 or ’08 after financial difficulty. It is a process, sort of like the “five stages” theory of grieving/accepting loss – but you have to learn how to *think*.

The psychology is well known, we are all more or less the same critters, so marketers know how to sell to every step along the way.

My point is simple: learn to think for *yourself* and *your* circumstances – not all things are equal and simple.

If you want to *learn* something, I have a few concise recommendations, sort of the “cherry picked” list of reading over all those years (almost ten).

There is an out of print book called “The Dying of Money” by Jens O. Parsson. You can shop around for PDFs on the net (learn to use google power search features – for example, filtering a search by file type, which in this case would be PDF only results). The book is narrative at first, almost a third, but then gets into pretty basic algebra stuff, which is easy to follow along if you got three brain cells to rub together. It builds a base about how to thing about a system of money – which once understood allows you to see right through bullsh**t. In short, it was how money was viewed all the way up to about a hundred years ago (give or take).

I also recommend “Fiat Paper Money” by Ralph Foster – if only for the first few chapters, which are an easy to read summary of the Chinese inflations (they invited paper money one thousand years ago), French inflations (revolution about two hundred years ago), and American inflations (English revolts). You will learn why credit is necessary for growth in very easy to understand terms. Think of credit as a gun, shoot food and eat and avoid starvation or shoot your neighboor to rob them – money/credit is a tool, just like a gun and it can be applied to many problems – it is men who are good/evil in their intent.

Once you those merit badges, learn how the real, modern world works. Buy a textbook, “The Economics of Money, Banking, and Financial Markets” by Fred Mishkin.

This ain’t rocket science – they just pretend that it is.

Slog through all that and you won’t need to ask anonymous folks on the internet how to save yer butt – you will end up like me, in a small town in rural Alaska. :-D

Lastly, once you kind of get your head screwed on straight – find a copy of “The Story of Civilization” by Will Durant. It is twelve volumes, he spent his life writing the series (with great help from his spouse Ariel).

The short version is “People suck – hard times a’comin'”. Find a good gal, raise a great family, and die knowing you wouldn’t do it different.

Regards,

Cooter

Crazy Cooter,

Cool! Thanks’

Not sure I want to hear life lessons from a guy who wrote a 12 volume series. Sounds like he lived in a room, sitting at a desk, by himself. But I agree the only way to live life is your own way, not needing to prove anything to anybody.

Durant? More travel than you’ll ever manage. That was a well written series but it’s kind of a 1930’s point of view. Great man theory of history is what current historians would call it. And uninformed by PC, so all the identity groups are missing.

Precisely why it was recommended – the story of civilization is a very old one, not a new one.

Or, as I said, people suck, hard times a’comin.

Regards,

Cooter

“… you will end up like me, in a small town in rural Alaska. :-D”

I considered Haines, AK (and other locations), but settled in the mountains of WV for a number of personal reasons.

Your trek toward low population is generally applicable.

I just bought a house in Huntington, West Virginia. It is a decent city in case I am wrong.

Cooter, it is remarkable how similar our stories are concerning our economic/political educations. However I wound up in a small town in rural Florida as I really don’t care muchfor cold weather.

rx

No powder keg. Same story, muppets still can afford to wait another 4 years. By definition, there’s nothing urgent about the situation. Easiest mathematical proof ever.

After eight years of loose accommodation, M2 bottoming, hourly wage driven down, and a long term downtrend in purchasing power –

the Fed “discovers sudden” higher inflation just in time to hike in March!

I call BS and not the only one to do so.

http://www.tfmetalsreport.com/blog/8163/sudden-onset-inflation

Sorry –

Should read M2 Velocity bottoming and M2 Stock still growing.

Good post.

As I have mentioned before, I have returned to work ( for the next coupla years ) during my retirement. Where I work, many young people do not see the necessity of saving in the 401K for a variety of reasons that I won’t address here. BUT THERE IS A HEALTHY MATCH. And we all know the contributions are deductible against current income.

So I plead with the young people to put 2% in the 401k — which effectively costs less than that, AND EVEN LESS WHEN YOU CONSIDER THE VALUE OF THE MATCH. Oh, yeah, and I ask them to increase it 1% annually when they get a raise — which this Company does give. This is just advice, and I do not push hard at all.

I tell my peers this, also, in a similar vein : Insuring your financial assets with 2% PMs is really not very expensive. 2% of $100K is only $2000 — and 2% of $500K is only $10,000.

And increase it by 1% annually. IT’S INSURANCE, NOT AN INVESTMENT ! ! !

Your homeowner’s insurance expires worthless — annually — if you were not lucky enough to have a home disaster and collect against your policy. Even if you get an annual dividend, that is a scant return on the policy.

Your gold may never pay you if there is no disaster, but that is a good thing, is it not ? ( Same goes for Junk Silver and American Silver Eagles ). Over the next decade or two, absent a financial meltdown, I EXPECT GOLD TO HOLD ITS VALUE, if not grow at a rate even with inflation.

I have been doing this a long long time. The volatility is of no concern as the decades pass, I can testify to that. I have homeowners and auto and health and life insurance. I also have portfolio insurance.

GOT GOLD ?

SnowieGeorgie

Yeah, push the kids into 401ks. Maybe if enough of them fall for it, it will boost your “portfolio” enough to allow you to properly leave the workforce, freeing up jobs for people that still have a future to look forward to.. Congratulations on all your hard work and financial success. You’re obviously better.

Sorry,

I neither agree with nor share your cynicism.

I am 100% in stable value ( meaning no stocks or any long bonds ) in my previous and most current 401k. It’s just a savings account replacement, and a pretty good one at that — given the 4.5% match, and the generous annual profit sharing.

You don’t know me well enough to level such a cynical and sharp criticism — my approach is a gentle and a caring approach, only concerned with helping young people save a little cash, and I am not the least bit concerned with how I exit my [ non-existent ] market positions.

As for my “hard work” and “financial success” — well, like you I have worked hard and fell into no easy money — no inheritance or trust fund.

As for my “financial success” — NOT REALLY — hence my necessity of RETURNING TO WORK a few years after RETIRING.

Sheesh

SnowieGeorgie

@Snowie,

I have a very good friend who lost his job, at age 52 and after 30 years, working at Kennedy Space Center. He saved every penny he could in various plans over those years.

He had to go home and tell his wife that he was unemployed, may never work again, and had $1.1 million being rolled over into an IRA. You’re telling the young’uns the right thing.

Really depends on the individual circumstances. Given the paltry returns on a MM and the probability of not being with a company long enough to vest in the match, professional youth would get a better return by paying down debt. Guaranteed return.

Once they are 100% out of debt then and only then contribute enough to max out the match and stick in MM. Market is valued to high to risk a 10-20% correction, even for a 20something.

But as a general rule, your suggestion is sound.

Yes I do Silver too and about 20percent of my total net worth

For the BLS to have understated inflation (and now ramp it up) to align with desired Fed policy would require the complicity and collusion of hundreds of economists and statisticians, and not one spilling the beans about the nefarious and deceptive activities… for years.

Besides, that article made one common but very wrong mistake, which takes away a big chunk of credibility it may have had: QE was -NOT- money printing.

When the Fed “creates” $100 billion, that money does not enter the economy but instead sits on the Fed balance sheet. It’s then used to buy bonds from member banks, effectively creating an asset swap, but NET no new assets entered the economy. It is exactly why we didn’t have hyperinflation.

+1. Most people have little idea how the QE actually worked or why they did it. It was simply a mechanism to provide banks the necessary capital to meet their inter-bank obligations so there wouldn’t be a Great Depression style meltdown. But the banks had to pay a price by trading their income producing assets to the government.

But it makes for great conspiracy theories

But some of the money printed ends up in circulation which does create inflation. Case in point is the student loans worth over $1 Trillion. Also, the banks would borrow the newly created money at almost zero percent and then turn around and buy government bonds. The government then spends this newly printed money, that is, it enters the economy and creates inflation. But not all of the money printed enters the economy. Some of it end up in stock and bond market to create the so called “wealth effect”.

Inflation was always there, but some students who failed the tests for engineering and science got accepted into economics, and then applied for a government job.

You mean Wall St job?

Re the govt. job: Pretty much what I did, SIXTY_TWO YEARS AGO!

Used it for sustenance while building a life of relative independence and at liberty in a remote place.

There are ways for individuals to adapt to and exploit “the system” in a microeconomic way, all the time.

Yellen will be gone by next year and she knows it. It’s now that we will see care thrown to the wind. The entire banking world has been spooked by the Trump win, and they can smell change coming all around the world. I heard Trump might get to appoint a handful of Fed governors. Who would have bet on that.

Who cares honey. He is already lame duck 45 after 1 month LOL. Do you not think the actual real powers in the world, well beyond him, have not already set up the game for their win. He is a speed bump on a continued development of Corporate monopoly and consolidation. Trump after 2 more years literally does not matter and in fact now, matters very little other than to himself. Wake up.

There wont be much change and if you want hope watch a soap opera

Don’t think so. We’ll see …

Honey, I am not so naive that I see the new president as more hope and change. He is a puppet as well, but of a different variety. He represents the demise of the two party state, the demise of the conglomerate media, and eventually the deep state as well. The courtiers always think the people love them, until they find out they don’t.

Thorny You sound exactly like George Carlin and I agree completely

“Yellen will be gone by next year and she knows it. It’s now that we will see care thrown to the wind.”

These people are obsessed with their legacies. I don’t think that’s likely, although I’m not a psychic.

“The entire banking world has been spooked by the Trump win, and they can smell change coming all around the world.”

What? Goldman Sachs is up 40% since the election. JPMorgan is up 30%. Gary Cohn, nearly 30-year veteran of Goldman Sachs, is his chief economic advisor. He got $285,000,000 as part of his package to leave GS and join the Trump administration… you think bankers are spooked? Do you live in an alternate reality?

Inside the firms a high stock price means it’s cash out time. Big deal.

Trump will be reminding Cohn and Malpass how much they FU’d the financial system, if his treatment of the press, is any indicator.

People have just one solution. They will cut back on their spending. They can do this through outright reduction, or through substitution of products and services.

Good for the Planet, bad for banks and Govt.

LOL. Or they will continue to gorge on credit as long as the banks will give it out.

You forget the credit cards. Eliminate credit cards and see what happens.

It also might have slipped your mind that not far where you live is the epicentre of housing inflation. All right, that is officially called bubble.

Don’t know where Paulo lives, but where I live is, indeed, “far from the epicenter” of housing (or any other) inflation). It’s called avoidance – a viable strategy on the micro economic level of the individual.

I see that the illegal immigrants are staging a work stoppage to show us all how much we need them. If I hadn’t seen it on tv, I wouldn’t even know it was going on. So much for disrupting my limited economic activity.

shrinkflation is forcing everything to shrink at a faster rate than inflation forcing prices higher.everything is rapidly shrinking while quality is virtually nonexistent,shrinkflation/inflation one two punch,only way to make money in this dept driven economy is to cut cost everywhere while relentlessly forcing prices higher

Bond holders got wacked from the time WWII era price controls were lifted after the war and bond yields started to rise shortly thereafter. But the really big rise in interest rates (and bond price drops) took place from around 1974 to about 1982. In early 1982, bonds issued in the early 1960’s with many years remaining until maturity sold at steep discounts from their original prices.

My longest term bond comes due in 2028. I bought it during the Meridith Whitney California bond sell off in late 2010. I am being well compensated to hold my zero coupon, non callable, general obligation bond until it comes due in about 11.5 years. Of course if 10 year Treasuries spike to a 15% yield (as they did in 1982), all bets are off. At my age, it won’t much matter.

DUH!

How else did you think the U.S. would pay off 20 TRILLION DOLLARS OF DEBT ?

Plus, DON’T EVER FORGET that understating the “official” inflation numbers benefits both the Fed and the US Govmnt.

In Dallas I’ve seen 35-50% increases in material costs over the last 5 years. And as Wolf has clearly documented, rents and housing prices here are easily up 30-50% over the 2007-2008 pre-recession highs.

This too shall pass. Very quickly and messy, I’m afraid.

ANON – It will and we wont be talking about it for very long at all. This is nothing new at all. Move along and live. Life literally goes on. Its great news but very old at that. Gee debt, and housing and other items for most costing more. Shocked I tell you LOL

Inflation is up? That just means you need to cut cost more, pay less taxes, and store your wealth and not in the bank. Start your diet and cut restaurant spending to once a week. Find items on-line and not pay state sales tax. There’s multiple ways to use Sc-Amazon, to find the resellers not in your state. Gasbuddy helps you find the cheapest gas near you. Pay out less than you ever have before, its not that difficult. And the state will love you for it!

The last thing the GIANT world debt-berg needs is higher interest rates, not to mention a stronger dollar, and the strong dollars influence on the dollar denominated EM debt-berg……interesting times….in the chinese sense

Hey Wolf – off topic, but it would be interesting to know which large companies have changed their capital structure the most in the last few years, going from mostly equity to mostly debt. Stock markets up but with accounting shenanigans this change is not obvious or even noticed.

Every company buying back their own stock is on that list. It’s all borrowed money.

Is Peter Schiff here? lol

He must be. I remember him reflecting relevant Wolf’s posts revently

Road trip cause the buyers are eating the diff!

Oil was very cheap last year. So, 2.5% is in my view not yet troublesome. However, this could escalate as worlwide Central Banks have to sell their Treasury holdings due to shrinking current account surpluses. Imports and exports are soaring worldwide.Brazil, Peru, Indonesia….show 30% more exports than last year.We have finally some reflation. However, this is probably more than the FED wanted, as this endangers the property, car and consumer loans.

From the article

“So-called core inflation – which excludes food and energy – jumped 2.3% in January from a year ago”

More importantly, Cocoa Krispies, Cap’n Crunch, and most of your favorite cereals are still relatively cheap. Thru genetic engineering boxes of these vitamin fortified goodies can be had for $2 (and under) when on sale. Just sayin.

You EAT that stuff?

“CHARLESTON (WV) — The Senate Agriculture and Rural Development Committee Senate Wednesday took up bills dealing with establishing a farm-to-food bank tax credit and setting up a process for vendors to sell home-based foods at farmers markets.”

There is a strong movement afoot to move food production and marketing back to localities. Suits me!

One of my local supermarkets has a large buy local section.

I saw a few minutes on PBS the other day about urban gardening, they showed a super market where almost the entire roof was a mini-farm– supplying much of the produce that the supermarket sells.

I thought it was pretty cool. I think it was a Whole Foods in New England, nonetheless I don’t see why the idea couldn’t be copied around the country.

Best health insurance is a good diet. Cheaper too. Process foods suck compared to home grown and cooked foods. We rediscovered home cooking about 2 years ago and won’t go back.

2 years without a soda. Where is my 2 year pin? :)

Love this site. Finally comments with intelligence and substance. Mostly.

I’m of the opinion that these inflation numbers and the associated ‘scare’ press are meant to support the Fed to raise rates. I don’t think inflation is going to escalate; certainly NOT in the broader cost structure. Yes it has in the big three of medical, housing and college costs.

That said, why is the Fed setting up to raise rates in such a tepid economy? And one that is ready to roll over into recession if not there already? The Fed now realizes that they are out of bullets and that fiscal stimulus is what is needed. So they will raise rates 2 or 3 times this year and watch with Trump as the economy starts to implode. They are using the inflation scare as cover for this move. Trump and Congress will see how bad things are getting and unleash massive infrastructure spending (most largely wasted btw). The Fed wants to wash its hands of ‘being in charge of the US economy” and but the burden back on Congress and the President.

As long as all those winning stock market investors drop us some crumbs then the Fed has been a smashing success. Cold fusion!

Well, if one must search for the silver lining in this dark, bleak, thundering cloud of bad news – it is the fact that rising energy prices have led to improved conditions in the oil patch. The last two weekends I had the (mis) fortune of being in Odessa to help some friends move to their lake home in Coleman. The restaurants and retail businesses seemed to be doing booming volumes over the weekend!

“The Fed is already sitting on a powder keg, after years of QE and zero-interest-rate policy that have caused mind-boggling asset price inflation, including in housing, which is filtering into the costs of living.”

That CRE price chart from the Wolf’s linked article, tells a lot of the story. The CRE has to be paid for, CRE price/carrying charges pass through. ‘The customer pays for everything.’ Impossible to stop the inflation pass through.

Transitory!

Looking at that chart of the inflation rate year over year with inflation at 3.5% in 2011 and on avaerage 1.5 to 2% thereafter, one can clearely see the theft that the FED has perpetrated on the unsuspecting american saver with interest rates at 0% for the last 10 years.

Feb 16, 2017 Inflation Finally Rears Its Head

https://youtu.be/cKhtrNvC5mM

The latest Get it? Got it! presentation by Grant Williams on youtube is a good watch after reading this post.