Fear of “waiting too long” or of “having already waited too long?”

The fear of what Fed Chair Janet Yellen on Tuesday – and other Fed governors earlier – called “waiting too long” before raising interest rates is increasingly inserting itself into Fed pronouncements. One of the aspects – and this is getting articulated with increasing intensity – is commercial real estate (CRE) and its impact on banks whose nearly $2 trillion in CRE loans are backed by collateral whose boom-prices are known to crash periodically in phenomenal busts.

Or is it the fear of “having already waited too long?”

Boom and bust: that’s the material CRE is made of. We had seven years of boom, and now the Fed is worried about the bust. Yellen didn’t mention CRE in her prepared testimony on Tuesday before the Senate Committee on Banking, Housing, and Urban Affairs. But it featured in the twice-yearly report that the Fed delivered to Congress in support of Yellen’s testimony.

And it wasn’t the first time that it was mentioned in these twice-yearly reports – but the fifth time in a row.

In its February report two years ago, the Fed first pointed at “valuation pressures” in CRE. And warnings about CRE have appeared since then in every report, twice a year, with growing sharpness, including in the report issued in June 2016, which warned that “valuations in the CRE sector appear increasingly vulnerable to negative shocks….”

Other Fed governors have also warned about the CRE boom and a potential bust, particularly Boston Fed governor Eric Rosengren, who was gazing with amazement at a stunning crane forest in his own city.

What concerns the Fed about CRE aren’t the valuations per se, but the fact that the sector is highly leveraged, and that when prices collapse, which they tend to do, the collateral value gets crushed, and banks are left to twist in the wind. That’s what happened during the Financial Crisis.

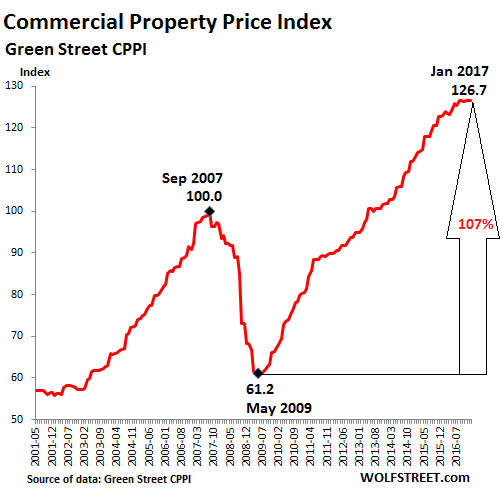

Just how badly can prices get crushed? The national averages hide the drama that happens on the ground in particular cities. But even these national averages still show enough drama, as per data from the Green Street Commercial Property Price Index. The index shows that overall prices across the major markets in the nation plunged nearly 40% during the Great Recession and have since more than doubled:

So that’s why the Fed is fretting about it. This time around, the Fed report said:

Commercial real estate (CRE) valuations, which have been an area of growing concern over the past year, rose further, with property prices continuing to climb and capitalization rates decreasing to historically low levels.

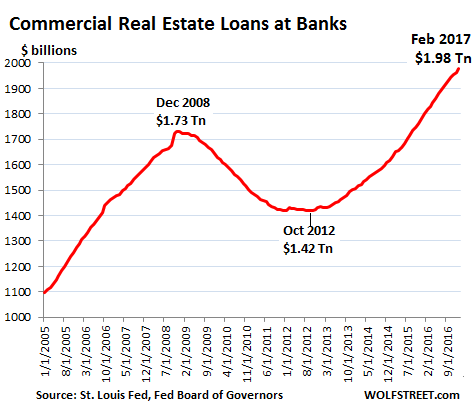

Then the report discusses the debt that nurtured this boom to these heights. This debt has ballooned to $1.98 trillion, and is now 14% higher than during the crazy peak of the prior bubble that collapsed with such spectacular results:

The Fed is careful not to sow panic among bank investors. So it couches its message in a big “while” and some other mollifying words, before getting to the meat at the very end of its long sentence, namely that a “sizeable” decline in CRE prices could take down “smaller banks”:

While CRE debt remains modest relative to the overall size of the economy and the tightening in bank lending standards for CRE loans in the second half of last year may reflect some reduction in the appetite for CRE lending, the heightening of valuation pressures may leave some smaller banks vulnerable to a sizable CRE price decline.

And “smaller banks” are precisely what’s the most on the hook: they hold about $1.22 trillion of these CRE loans.

But the national averages hide what is happening in individual cities. Some markets are still rocketing higher, but others have shot craps, particularly Houston, whose CRE market has been slithering into deep trouble for well over a year. New York City is having its moment. And San Francisco’s office leasing market has just had the worst year since 2009. They’re among the large markets where the dynamics have already flipped. Other markets will fall in line behind them.

Boom and bust – that’s the nature of the sector. Only this time, historically low interest rates for eight years and the resulting wild chase for yield among desperate investors have created the most magnificent CRE bubble ever with the most leverage ever. And I have no idea how the Fed is going to unwind its handiwork softly without pulling the rug out from under the banks and CRE investors.

In New York City, a few “success stories” overshadow “very anemic activity.” Read…. The Most Expensive Office Market in the US Fizzles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Real Estate .. some house prices in Frankston Victoria went up by $50-$100.000 in one big jump. This suburb is considered a very bad area to live in & is considered underprivileged, no one wants to live there & yet prices have sky rocketed.

At the same time a 4 kilo bag of potatoes went up from $4.99 to $9.99 over night.

If interest rates go up the whole of the real estate market will be revalued down & there will be a fire sale.

Everyone will declare bankruptcy, the loans will be deemed repayable at 1 cent in the dollar .. how on earth will the banks survive such a massive loss .. the banks will have to close.

At the fire sale, it will be a game of musical chairs, previous property owners with new names will buy up cheap .. a new start.

But .. how will the banks survive the crash ?

Like they did the last time by thieving our money BUT this time they will raid your savings directly with a bail-in. Check it out.

The fed would not like to sow panic but believes there are too many loans? (Banks on every corner and no one can make any money – what would Rothschild do?)

He wouldn’t have made such highly leveraged loans in the first place.

Photo shop is such an excellent tool, something that is not there can be made to look there.

I looked at the house listings on line .. one house has a tin roof in one picture & a tiled roof in another .. in fact it is tin.

Or take you house pictures with a wide angle lens, the interior space of your tiny condo will look massive.

Can you post the link?

The solution is simple: start QE4. Japan does it now for 30 years. I do not understand why raising interests will help here. An interest cut would be here most appropriate.

Forgot the /sarc tag?

Sarcasm or not, don’t be surprised to see it happen.

Valuations my dear bean!

Oh the punch bowl is too heavy and no one trusts the liquid?

Why does Lucy always pull the football away knowing she is faster and smarter than chuck?

Chuck is way to leveraged to the game?/sarc

The focus should be on whats behind the curtain.

DERIVATIVES.

Specifically, – Commercial Mortgage Backed Securities.

This is a paper house built upon wet sand, in an area prone to occasional heavy financial rain storms, with attendant highly leveraged hurricanes.

What could go wrong? And the Fed frets!

From the peak in 2007, the CRE fell by 38% to 62% from 100% and moved up by 100% . The DOW fell by almost 62% and from 2009(L) is up above the 2007(H) by 38%, to 20K.

The $SPX with the double humps of the 2000(H) & 2007(H)

have rendered itself totally useless. The “Experts” love it.

Please draw a line between the 2000(H) & 2007(H) and extend,

in the DOW, R2k and other indices, you will see that we are

in an overbought territory , above the long term line.

It is not for the first time and maybe not the last that we have

crossed the border. You can crawl along the fence, but it’s an

unmarked mine field. We are also squeezed between this line

and the long term line connecting the 2009(L) & the 2011(L),or the 2016(L). Major hostilities can erupt with out any warning.

This area can be a war zone.

If you are a TOURIST just go home, or find a safe shelter.

The Fed new what they were doing with zero interest rate and QE policy. I have nothing but contempt for them. Personally jail term for legal theft would be to kind for them

The fed Have heiped create this mess. Yes they can kick the can down the road .but what a way to live your not free just like a thief you better have eyes in the back of your head one wrong move and bang. The price is to high I would FAR sooner be FREE .MY best bet is so would they it’s not nice having to watch your back day and night sooner or later your going to blink

Also, because the Fed is there, extremely little fiscal discipline is shown by our politicians. They should have to face war crimes in addition to theft. Every war in the last hundred years has been underwritten by the power to print. We are now facing endless spillover effects.

Do the “smaller banks” that hold about $1.2T of CRE loans keep these mortgages separately? In other words, are these debts bundled and packaged up, or are they held and serviced as a single contract between the bank and borrower?

I would assume that if a small bank has done due diligence on making a CRE loan, and holds the mortgage in-house it should be OK; with exceptions like the Houston market. Or, am I missing something in the big picture?

Commercial RE loans are divided in two: Commercial Mortgage Backed Securities, or CMBS, and portfolio loans.

Portfolio loans are originated by a lender (in both the US and Europe usually a smaller, local bank) and are held on its balance sheets to maturity. In short your standard “bank loan”.

CMBS are pretty sophisticated financial products: basically many loans of varying size and quality are transferred to a fund. In the fund these are pooled together but, here’s the twist, loans are all jumbled together inside the fund and then the fund issues “traches” of bonds, usually three but sometimes four. These tranches are usually divided according to rating and are “investment grade” (AAA to BBB-), “below investment grade” (BB+ to B-) and unrated. Some CMBS add a fourth category, rated CCC+ to C.

These bonds are all backed by the same pool of loans, the difference between them being akin to ordinary senior and junior bonds but with many more gray areas given the complexity of the product.

Hope this helped you out.

Yes. Thank you.

Unless there’s a CRE bubble collapse, which seems quite possible, portfolio loans should be just fine. CMBS could also stand for Commercial Mortgage Bull Shi#, eh?

I don’t want to bust anybody’s hopes, but the big €360 billion pile of NPL’s on Italian bank sheets include a large number of CRE portfolio loans: part of the reason that banking system is such a big mess is that collaterals aren’t as good as originally envisioned.

This is not merely a case of values collapsing due to a burst, but of book values being inflated in the first place to extend bigger loans and/or keep interest rates depressed.

Part of the reason the NPL disaster has been behaving like an avalanche (by June 2017 the €360 billion will probably be €380 billion: read on) is Italian banks have been keeping collaterals at original book value for as long as possible, helped by “frozen” prices which effectively killed the Italian housing market between 2010 and 2015, when market forces finally defeated the high price fiction.

Leaving aside the “Korean loans” Italian banks have long extended for purely political reasons and then stuffed in every nook and cranny, collateral values realigning with reality is what is causing the avalanche to grow in size: if collaterals go down in quality, loans need to be renegotiated. Even with the ECB machinations, a warehouse posted as a collateral with a book value of €2 million being suddenly valued at €250,000 can cause a creditor to take advantage of the new (introduced in 2013) debt/business restructuring procedures even if he has a good cash flow.

And this is just the beginning.

Lets just call CMBS for what they are –

DERIVATIVES

Since they “derive” their value from the underlying mortgages.

The AAA tranch pays low return for low risk and is paid first. The second BBB pays a little higher for a little higher risk, but must wait for the first tranch to paid before they receive payment. At the bottom of the derivative pile, exists the highest risk and the highest returns and are the first tranch to “dry up” on a financial crisis.

As for in house portfolio CRE loans, (usually the size of the loan is predicated on the size of collateral valuation), when a financial crash occurs these valuations go out the window and the small bank is left holding the loan with no equity. Broke.

I would argue that both are a problem. The portfolio loans are an immediate problem for the banks in case of a bust. The CMBS is probably more delayed as they would be sold to “investors” which would include pension funds.

Big CRE loans, like those extended to big developers of casinos or huge skyscrapers, are often syndicated among banks. The builder approaches a bank or brokerage and they agree to raise the money in syndication. These syndicated loans are usually held in house or traded among the syndicate. The purpose of syndication is to minimize risk and also to expand the scale of the lending.

Syndication

The problem arrives when these individual syndicate members enter into a hedge by generating a derivative position, utilizing the “collateral” of their holdings within the syndicate as the underlying “value”.

What could go wrong? A paper house built on wet sand.

They hedge everything now. This is what creates the complexity that prevents unwinding the assets in any orderly way.

i was reeling from MC’s breakdown and jumped too fast to Petunia’s comment and now i have an ice pick headache of “YOU’RE FUCKING KIDDING ME” existential incomprehension again. oh my god… this website, along with Petunia et al, is always like overdosing on hollywood-size handfuls of red pills of Reality all at once and being forced to even see in slow motion not only your parents having sex, but your grandparents.

KL,

Have a cookie. It’ll make you feel better.

Hey kitten, what about if you designed some attractive women’s hazmat suits? Submit them in a deal to Melania. I bet about now Melania Trump would add them to her fashions lineups, after being around Steve Bannon and Bibbi Netanyahu this long…

If the smaller regional banks start stressing out over bad CRE collateral, im sure the TBTF national banks will be happy to use the FED’s QE whatever once again to help bail them out and thus absorb them into the collective so we can start the process all over again.

That said, I’m not convinced there will be anymore QE or that would be effective this time around. That ship has probably sailed.

At the end of this decade we’ll probably only have 4 banks in the US. They’ll all be part of JP, Citi, Goldman, Morgan Stanley.

“CRE loans are backed by collateral whose boom-prices are known to crash periodically in phenomenal busts.”

Sounds like these smaller banks just need to be introduced to non-standard GAAP valuations*. You know, no more “Mark to Market” when you can simply “Mark To Maturation” and assume that once the market “adjusts” the valuations (if held on the books) will revert to the assumed collateral value.

Also known as “Mark To Fantasy” and “Bony Pony Loaners Value”.

The government can be stuck on stupid longer than you can stay solvent!

… as can Wall Street . Brilliant comment by the way .

I think the FED should fret about the founders of this country got reborn and clean up everything with FED being the first to get prosecuted and put the country back to some sound principle. Well that is just my dream. I know before that happens, the corruption has to go a lot worse until the destroyed sheeple don’t even have food stamps and TVs to watch.

Wolf you say “boom and bust” like this is an ordinary cycle. I suggest otherwise. The Chaos Monkeys of Silicon Valley have pooped on the pardigm of old fashioned retail stores with ever increasing piles. This has occurred ever since Amazon booked its first buck online. The trends are entertainingly explained by Galloway / L2inc – for many 2 minute long chuckle sessions see the youtube channel (link below). But it is also scary in that the advertising business is also getting destroyed by Facebook / Google, as well as traditional bricks and mortar. Galloway insists it will only be the hybrids who survive. Can you paradigm?

https://www.youtube.com/channel/UCBcRF18a7Qf58cCRy5xuWwQ