Bank regulators have been warning, now it’s happening.

The New York Fed, in its Household Debt and Credit Report for the fourth quarter 2016, put it this way today: “Household debt increases substantially, approaching previous peak.” It jumped by $226 billion in the quarter, or 1.8%, to the glorious level of $12.58 trillion, “only $99 billion shy of its 2008 third quarter peak.”

Yes! Almost there! Keep at it! There’s nothing like loading up consumers with debt to make central bankers outright giddy.

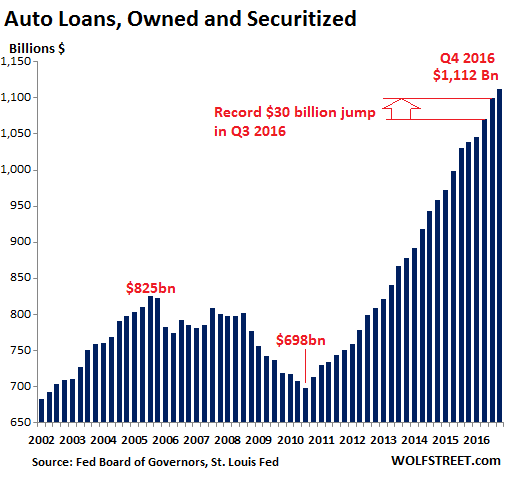

Auto loan balances in 2016 surged at the fastest pace in the 18-year history of the data series, the report said, driven by the highest originations of loans ever. Alas, what the auto industry has been dreading is now happening: Delinquencies have begun to surge.

This chart – based on data from the Federal Reserve Board of Governors, which varies slightly from the New York Fed’s data – shows how rapidly auto loan balances have ballooned since the Great Recession. At $1.112 trillion (or $1.16 trillion according to the New York Fed), they’re now 35% higher than they’d been during the crazy peak of the prior bubble. Note that during the $93 billion increase in auto loan balances in 2016, new vehicle sales were essentially flat:

No way that this is an auto loan bubble. Not this time. It’s sustainable. Or at least containable when it’s not sustainable, or whatever. These ballooning loans have made the auto sales boom possible.

But despite record low interest rates, the bane of the automakers is now taking place relentlessly:

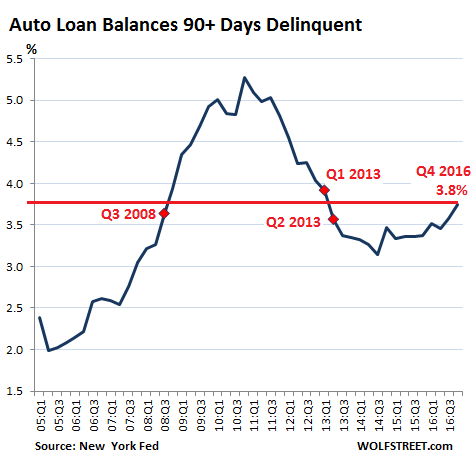

“Seriously delinquent” auto loan balances, composed of all loans that are 90+ days past due, rose in Q4 to 3.8% of total auto loan balances. That puts them right between Q1 and Q2 of 2013, as auto credit was recovering from the Financial Crisis. Last time auto loan delinquencies had surged to that level was after Q3 2008, as the Financial Crisis was tearing into the economy:

These seriously delinquent auto loans are an indication of what is next:

- Losses at auto lenders, particularly those specializing in lending to subprime borrowers, but also other lenders, including captives, such as Ford Motor Credit, which had already warned in its most recent outlook that “we continue to see credit losses increase.”

- Tightening auto credit for consumers, as those losses begin to exact their pound of flesh from the lenders.

Some specialized subprime lenders might keel over. Larger lenders with good quality loan portfolios will bleed but go on while tightening their underwriting standards in order to weather the storm. And that’s precisely what the auto industry is dreading: tightening credit.

The auto boom over the past few years was funded by historically low interest rates and loosey-goosey underwriting, with long loan terms and high loan-to-value ratios, often over 120%. They made everything possible. But they infused the $1.1 trillion in auto loans with some very big risks.

The Office of the Comptroller of the Currency (OCC), one of the federal bank regulators, has once again warned about the risk-taking by auto lenders:

Auto lending risk has been increasing for several quarters because of notable and unprecedented growth across all types of lenders.

As banks competed for market share, some banks responded with less stringent underwriting standards for direct and indirect auto loans. In addition to the eased underwriting standards, lenders also substantially layered risks (granted longer terms combined with higher advance rates resulting in higher LTV ratios).

These factors increased the credit risk in auto loan portfolios…. This embedded risk is now being reflected in lower recoveries at charge-off (higher loss severities) for both bank loans and securitized auto loans despite relative stability in used auto values.

Bank risk management practices and the ALLL [allowance for loan and lease losses] should reflect the elevated risk profile and higher probable credit loss severities.

So it’s all there – the ingredients for bigger losses among banks and investors, a few failures of smaller specialized subprime lenders, and belated credit tightening, both out of necessity and due to lower competition among lenders as some of the most aggressive ones will be busy licking their wounds.

And auto sales – not long ago the truly hot sector in the US economy – are now confronted with these tightening credit conditions as growth has already been stalling.

Despite what you might think, automakers did not “cut back” on fleet sales in January. But keep an eye on rideshare companies. Read… Car Sales Crash, But It’s Complicated

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

February 15th, 2017 This Is One Of The Big Reasons Why So Many Families Are Feeling Extreme Financial Stress

When the cost of living rises faster than paychecks do year after year, eventually that becomes a very big problem. For quite some time I have been writing about the shrinking middle class, and one of the biggest culprits is inflation. Every month, tens of millions of American families struggle to pay the bills, and most of them don’t even understand the economic forces that are putting so much pressure on them. The United States never had a persistent, ongoing problem with inflation until the debt-based Federal Reserve system was introduced in 1913.

http://theeconomiccollapseblog.com/archives/this-is-one-of-the-big-reasons-why-so-many-families-are-feeling-extreme-financial-stress

Of course prior to 1913, the United States didn’t have a middle class. You were either fairly wealthy or dirt poor. So comparisons can be difficult.

Depends on how you measure wealth. Most people in the US owned enough land to farm, along with livestock etc. People today actually “own” very little, they rent their homes, vehicles etc. (and yes I consider debt owners as renters, until you have the title in your hand you own jack sht). Just my 2cp.

We do not own our land, home or buildings. Look at the deed. We are called ” tenants”. The reason we are forced to pay property taxes. Land patents can not be taxed. Elites removed that from everyone’s titles.

“Most people in the US owned enough land to farm, along with livestock etc.”

This is not true.

By 1910, about half of Americans lived in cities. More than half of Americans were considered poor. Prior to the Great Depression, about half of white farmers (and an obviously higher percentage of black farmers) were tenant farmers / sharecroppers– generally poor, and did not own their land or livestock.

Sure, if you go back to the late 1700s or early 1800s when about 90-95% of the country lived in rural areas, farm ownership was high, but you’re also talking pre-Industrial Revolution (for the most part), and it just really bears no relevance or resemblance to America in the 20th or 21st century.

Follow-up. The US did not move from a primarily Agricultural culture until after the Great Depression. The primary movement from Rural to Urban living was absolutely facilitated by the Great Depression, only half of which was caused by economic issues. The other half was caused by climate and farming method issues.

The mortgage(e) and mortgage(r) classes.

“The United States never had a persistent, ongoing problem with inflation until the debt-based Federal Reserve system was introduced in 1913.”

Right, but the near constant banking crises and accompanying economic crashes and deflation weren’t exactly something to be desired…

Although looking at your link, I now realize you didn’t actually post anything original, and instead just to chose to copy + paste something from a website that also includes gems such as “You Are Never Going to Look at the Book of Revelation the Same Way Again.” Good stuff.

In 1881, President James Garfield stated:

“Whoever controls the volume of money in our country is absolute master of of all industry and commerce … and when you realize that the entire system is very easily controlled, one way or another by a few powerful men at the top, you will not have to be told how periods of inflation and depression originate.”

Two weeks later he was assassinated.

“and securitized auto loans despite relative stability in used auto values.”

Who is buying securitized sub-prime auto loans and how big is the market? Why not just stick with securitized sub-prime real estate loans?

At least with real estate the underlying asset ‘may’ appreciate.

According to Experian, last Summer (as the above graph shows things have got way crazier since) there were $388 billion in subprime auto loans, of which 17% were securitized: this means the market for securitized subprime auto loans was worth an amazing $65.96 billion.

Why is the market getting so big? because more and more players are getting suckered into it, chiefly because getting decent yields in the fixed income market, yields that can keep up with the real rate of inflation, not the imaginary numbers dreamed up in New York, Frankfurt, Bern and Tokyo, is getting tough. And the old shady practices are back.

Santander Consumer USA, a unit of Santander, has been forced by regulators twice to delay its 2015 10-K filings because it “didn’t properly account for material weaknesses” in their loan books. After the second filing regulators still have their eyes on Santander because profits literally do not add up: as an officially sanctioned “too big to fail” bank, Santander doesn’t fear being hit with a big fine by US regulators because they’d be made whole by dragooned European taxpayers, just like Deutsche Bank and VAG. Until the taxpayer will grow tired of this shenanigans.

We had a subprime loan a few years back on a used car. The note was charging us at least 24%(I’m trying not to remember.) Our credit was so bad we were lucky to get anybody to loan us the money. Anyway, the outrageous coupon is the reason you invest in subprime auto loans. Even if the debtor defaults, the lender has already recouped their investment, and they can take back the car and resell again.

Great point. Hope your finances have improved.

Just like mbs! turn it faster than you can remember the borrowers name and with 24 levels of tranches? Opportunity knocking (do you like range rover sir and/or mama) and you brought your refund FABULOUS.

So. My next question is – how the heck do I short some of the recent sub prime auto securitization bonds? There’s no CDS on ABS market to short like there was in 2007-08. Any ideas?

Good luck…..it is probably owned by the FED. LOL

Warning: this does not constitute investment advice. I will not be held responsible if you lose money, your house or get sent to debtor prison.

Try looking into Santander Consumer USA. They are listed on the NYSE and are neck deep in this fiasco. The stocks are climbing again just as regulators are probing them for having fiddled with their loan books. Not ripe for the picking yet, but given Santander is playing this game in Europe as well, they are going to get hit on the head, and hit hard.

Check out who the owners are of Santander ….

Don’t tell me Rothshilds

Well reasoned, I would say good call MC although the same warning you posted applies.

Worth noting that Blythe Masters, formerly of JPMorgan, was one of the people credited with helping to create the credit derivatives market that led to the 07-08 crash… she was hired as chairwoman of Santander Consumer in July 15 (that is Santander’s sub-prime auto loan division), and barely lasted a year, resigning in July 16.

Where that lady goes, smart as she is, bad things follow…

I just google a bit and found this

http://www.autofinancenews.net/auto-finance-performance-the-nations-top-lenders/

Santander is 12th right now for subprime auto. Ally Financial #2. Just looking at the list.

Most of the funding comes from private equity, but there are big chains of used car dealerships that deal with them.

Ask Goldman or if you ask real nice Jamie Dimon might let you in on the deal and sign his book for you! (Don’t wear a wire!)

There wasn’t really anything back in 2007 except maybe a R.E. index out of Philly. They changed the history to hide the inside job. Don’t ever watch a movie unless you read numerous books first!

I never seen the big short! I lost a bit during it and would have become Irish before the ending “credits”.

Well in 2008 the 4% delinquency rate was equal to 32 Billion.

In 2017 3.5% is equal to 38 Billion. It will get interesting if this rate gets hits 4.5%. That will mean 50 Billion is delinquent.

I feel like I have been sitting in a scrape with my kevlar hat pulled down tight and my fingers in my ears FOREVER. The stock market is beyond crazy and lets not talk about housing. And still it goes on……. and on…… and on.

I imagine people who are in war zones (mostly of the west’s making) think it must end soon, and yet the war is endless.

The financial oppression will be endless.

“The financial oppression will be endless.”

And perfectly predictable. As Kent mentions above, before 1913 the U.S. had no appreciable middle class, and its rise was the result of reforms begun FDR in the 1930s.

The very existence of a middle class is an aberration of history, and with the reversal of those reforms that aberration is undergoing correction worldwide. Advances in technology and transhumanism suggest that correction can be permanent, so that in the future humanity will revert to the historical pattern of a very small master class tyrannizing a subjugated general population.

Even without Carroll Quigley, it is all too easy to find examples of how corporatists, particularly in the Financial Industrial Complex, are directing governments to ensure this outcome:

Humanity is clearly headed for a very nasty dystopia half a dozen different ways, and soon, and there seems to be no way at all to prevent it. You’ll know you’re just about there once your overlords have confiscated Medicare and Social Security, probably in the next year or two.

Goodbye to all, and adieu. I’d wish you all good luck, but really, under the circumstances, that would seem gratuitous.

You make is sound like FDR’s reforms were single-handedly responsible for the middle class, which is absurd. Industrialization, technology, and unions are primarily responsible for the creation of the middle class. Oh, and WWII left the US with a highly developed industrial backbone, a shortage of available workers, and little competition from other industrial countries who were largely in ruins.

It’s interesting how technology, unions, and industrialization elsewhere is now decimating our middle class.

While default of US debt and ensuing great financial pain seems inevitable at some point, “…confiscated Medicare and Social Security… in the next year or two.” is hysterical nonsense.

Obviously untrue. Without FDRs reforms all economic gains would have accrued to the rich, and none to the general population, which is presently the case. Your alternate facts notwithstanding.

Only a cheap-labor corporatist could complain that labour unions are decimating the U.S. middle class, and with deliberate dishonesty at that. Unions are a remnant of the middle class, soon to be exterminated to more freely enable pillage by the predator class.

Plans to eradicate SS and Medicare have long been established and implementation now proceeds. As if you didn’t know.

Good comment. I just read that Kraft is trying to buy Unilever for $143 Billion. The bid is backed by Brazil’s 3G and Warren Buffet. What ever happened to stopping monopolies.

By the way I would have never thought that Budwieser, Coors, and Miller would be owned by the same company. 85% of beer sold in a liquor store is now owned by one company.

“What ever happened to stopping monopolies.”

Monopolists disliked the impediments to their avarice and took over the government.

Clearly a rent-seeking method of subjugating the population, but monopolists can rightfully claim that this is, after all, what the people have been voting for.

Another way to look at this decline might be the following :

40% of Americans have “good” (or better) credit, meaning their FICO is 750 or above. that means 60% do not have “good” (or better) credit.

In order to have good credit all one has to do is pay one’s bills on time for a few years.

Therefore in my book, at least 60% of people in the USA are either poor or on the brink of being poor. Keep in mind, a chunk of people with “good” credit may be struggling to pay their bills. At least they are doing so. It does not mean they are not 3 months of expenses away from living on the streets.

Let’s not forget Henry Ford’s contribution to the Rise of the Middle Class. Paid wages that were double and even triple the going rate; and, the massed produced Model T’s, gave mobility and greater financial opportunity to the working poor and rising Middle Class.

While, the notion of a Middle Class may be an aberration historically; it was likely squashed by Wealthy; and, not because Ordinaries, didn’t have the ability or ambition to work their way out of the Class System. Henry Ford provided that opportunity; and, was richly rewarded for it.

In the past the markets depended on confidence to keep them going, now they depend on illusion. The drugs help.

Overall auto loan delinquency rates have soared to 2009 levels, during the height of the crash. The number of lease returns are at a record high, as the loan charge rates rise. Media auto ads are at a fever pitch. There is a new high record number of underwater delinquency rates, as people owe more than what their car is worth. A large portion of trade ins were in negative equity territory, as the old loan is rolled into a new loan!

The collateral loan obligations (CLO’s) derivative sector, infested with sub-prime auto loans, is now beginning to crack.

Don’t worry. They have remote kill switches and GPS in all these cars. They can repo them and sell them to somebody else on a longer term. Used cars with a 72 month loan, anyone?

The big problem is we are swamped with used cars. And trucks. And jetliners. And combine harvesters.

The agri market is swamped with used machinery from leasing: these machines are great deals because the lease includes not only full maintenance but major repairs as well. You can have a late model John Deere 7760 (the machine which radically changed the cotton industry in Asia and Australia) with less than 900 hours, a brand new fan and fully upgraded firmware for US$490,000. The same machine brand new is well north of the million mark and at 900 hours the 7760 still has a lot to give, especially with a brand new fan.

You are not buying this machine from some auction lot, but from an official Deere dealership which partecipates in their lease program. You get full support. If you haggle hard enough you may get something off the tag price, a smaller down payment or other benefits: both the dealership and Deere need to get this machine out of the door as soon as possible… but at the same time they need to keep the 7760 assembly line going. DE shareholders need to justify those nosebleed values in face of dwindling returns.

The only difference I can see is a farmer whose lease is coming to an end won’t thrash a machine, mostly because if he does he’ll be paying a penalty he can barely afford, while people driving cars they cannot afford literally drive them like they stole them. Not their problem.

I’m waiting for the small Kubota backhoe to come up at rock bottom pricing, but then I think about spending the money when I can just pay the local operator to come when I need something done for a fraction of the cost. :-)

Which brings me to my point. Petunia, who has extremely valuable replies to share with us, mentioned she had to purchase a used vehicle at a high rate of interest as she rebuilt her life after her Great Recession nightmare. The key word is ‘used’. Unspoken was that she ‘needed’ the vehicle. But when I drive the highway I usually see ‘new’ vehicles, and very nice ones at that. If they aren’t $60,000+ trucks they are $40-50,000 cars. The latest local local fad are Range Rovers with the nearest dealer 2+ hours away. $80,000? If a car isn’t a Mercedes or Audi the little hood ornament and car styling seems to emulate them. I know many people with these fancy vehicles. They have convinced themselves that they either ‘need’ those unaffordable cars, or that they deserve them.

I have a friend who cannot afford to retire. He still owes lots of money on his mortgage. He was explaining to me how he ‘needed’ a new Toyota 4X4 PU. When I asked him why?, he said that he and his girlfriend needed it to haul their kayaks and complete other off road adventures. This is a guy who lives in a condo. He does no yardwork or building that requires a truck. In fact, they have just one kayak. I told him that he could probably pick up a very good roof rack for $100 and skip the $50,000 bill. He just started to spool up on his “We need this truck”, and I felt myself tuning out. In fact, I did tune out.

For some reason, people in north America (Canada too!!!!) seem to mix up this ‘needs and wants’ mindset. I guess if you want something bad enough it might seem like a need, but why are so many people hollow inside, and why do they need to fill this hole with’stuff’? I know a few will reply that it is the fault of ‘the banks’, or ‘advertising’, whatever. I simply do not understand this situation? People need to assume responsibility for their poor decisions. Unfortunately, the results of not doing so are going to hurt many many others as this particular sinking ship sucks down other facets of our economy.

Mr Paulo-

but that’s the crux of this TRAGIC little biscuit, isn’t it? that ALL this death and destruction of the world, our water, air, and each other and insatiable hungry ghost of neeeeed and want and perpetual CRAVING is piped in through the air vents of an insatiable capitalistic society where everything is built on instant obsolescence for the Economy, which is really the west’s TRUE religion, and why any Jesus or Martin Luther King would get murdered for preaching love and fairness and brotherhood sisterhood and all that “stuff.”

once you get it, it’s astounding and horrifying to watch.

and i mean that trump’s press conference was tragic for all. even HIM. along with the smirking press that sat there trying to feign respect.

Petunia was right about him signifying the end of something big. there’s no more pretense about much of ANYTHING, but what worries me is that we have nothing solid now without all that american pretense.

and maybe Petunia was joking about all the drugs, but she’s RIGHT. i think prescribed pharmaceuticals drive a lot of this insanity. a lot more than we realize.

for example- isn’t the brutally insane world of coding and tech secretly powered by adderall?

KL,

I worked in tech and Wall St. The highest drug usage I ever saw was on Wall St. You have to stay lucid to code, but not to steal, lie, and cheat.

But those people with their self-convinced needs are the ones that drive consumerism? We need the money to change hands for things to work!

At the end of the day, money is all made up anyways. Just numbers in computers.

These people with special needs are the ones who are winning. The last time they indulged, they were bailed out with ZIRP, and look what does self restrain brought you: negative real return on savings. I am not sure if they don’t consider you a nut for your sane advice.

I was talking to a good friend who lectures in one of the Germanic countries in Europe. He was decrying the fact that he *had* to buy an Audi soon. When we pressed him further, he said that it was down to expectations. If he didn’t have the proper car commensurate with his profession then he could say bye-bye to future career opportunities and be socially shunned.

Oh come on, we said, surely it can’t be that bad?! But he was adamant that it was.

Then pay a visit to a Club Med country. We are drowning in almost new earth moving equipment from all major Asian and European brands: Komatsu, JCB, Liebherr, IHI, Doosan, Kubota etc. Starting in late 2015 prices have started to come down a long way because to shift metal manufacturers are offering crazy financial conditions to contractors and construction firms. This is of course leading to a glut in used machinery which, more often than not, is very low hour and coming from “all included” packages has been serviced by factory-trained technicians using original parts.

It’s beyond crazy.

To MC & Paulo,

Most city folks have no idea how much capital it takes to be a farmer or a seedsman. Having been in the wheat seed genetics business from 1993 to a few years ago, I have great respect for those in the business of growing food. A couple combines, a planter, a sprayer, a truck to haul grain, storage for equipment, and storage for grain adds up to millions of dollars.

Having owned a dozen or so cars and trucks over the years, but always paying cash to buy them, probably puts me in the minority, but I can’t wrap my mind around making car payments. Before 2008 (and again today), I would see nice suburban homes with a Lexus and Mercedes in the driveway. I wondered how much it took to make a mortgage payment and two car payments every freaking month. Now the car companies want to sell at seven years with little down payments, and people go for it instead of being wise like Paulo describes.

What the heck, I’m living large and being frugal at the same time here in south Minneapolis.

When god created bar charts, she naiavly assummed the these intelligent creatures she invented would always base a bar graph at zero so as to get a realistic view without having to mentally expand the bars down to zero to see the actual differences.

And that they would learn how to spell.

What spelling error are you referring to?

Sorry, should have noted mine ….naiavly,,,,,checking ms google, it’s supposed to be naively but that’s another thing to disrupt my morning, words should be spelled somewhere near how they are pronounced.

Truncated bar charts are nearly universal. Not always intended to distort the significance of the variations I suppose, but they should be against the law anyway. Lets resist!

While you’re at it, take a look at ‘assummed’.

A bar chart beginning about zero, and representing auto credit would have to begin about the year 1900, approximately when the financing of horseless carriages began, but would not be relevant to the recent credit boom-bust-boom years under discussion.

Better to resist extraneous and irrelevant data, though it would be interesting to see such a chart if the subject was the history of credit in the auto industry for the last 116 years.

fuck occasional charming spelling errors when you report all you do on your own as we go up in flames. we’re so far beyond spelling errors meaning anything at all right now.

Probably the ones in his own trollish comment.

Why is it that commentors that point out non-existent spelling errors most often make spelling errors, sometimes many, in the space of a few words? In any case, it’s better to focus on the forest, not the trees.

Maybe ‘god’ (sic) is British and believes that ‘Securitized’ should be ‘Securitised’, forgetting that different parts of the world have forms of spelling and grammar that differ.

Also, the chart has its basis in the year 2002, thus the data is relevant and relative to the years 2002 to the end of 2016, the period of interest.

Another such chart may study the years from 1930 to the present day, a different analysis, and not relevant to the discussion.

Financial Times has an article on Car Loan deliquency rates.

https://www.ft.com/content/0f17d002-f3c1-11e6-8758-6876151821a6

Still, regulators have been raising concerns for months about weakening underwriting standards in the car loans sector as Americans borrow larger sums to buy bigger and better vehicles, and take longer to pay off the debt.

The average borrower has about $18,400 in debt on their car loan — up about a tenth from three years ago.

Nancy Bush, an analyst at NAB Research, said: “Auto lending was so hot for a while. It’s almost inevitable the credit quality would be stretched.

“Investors have tended to worry less than they should about banks going out on a limb with credit quality, just because we haven’t seen the evidence up until the last few quarters.”

Signs exist that lenders are stepping back from the riskiest parts of the market.

Santander Consumer USA, the subprime car-loans division of Spain’s biggest bank, reduced originations by a quarter in the final three months of last year in the face of “heated” competition.

Whats driving some of these subprime auto leases?

“In a deal led by Goldman Sachs, Xchange received a $1 billion credit facility to fund new car leases, according to a person familiar with the matter. The deal will help Uber grow its U.S. subprime auto leasing business and it will give many of the world’s biggest financial institutions exposure to the company’s auto leases. The credit facility is basically a line of credit that Xchange can use to lease out cars to Uber drivers…..Xchange caters to people who have been rejected by other lenders. The program is run by Andrew Chapin, who pitched it to Uber Chief Executive Officer Travis Kalanick in 2012. Before joining Uber, Chapin was a Goldman Sachs commodities trader. He oversees all of Uber’s auto-financing efforts, including a partnership with Enterprise Rent-A-Car and vehicle-purchase discounts.”

https://www.bloomberg.com/news/articles/2016-05-31/inside-uber-s-auto-lease-machine-where-almost-anyone-can-get-a-car

From the time the bad stuff started coming out in2007 it was still over a year before a real domino started falling?

There is plenty of fraud to come as the fed and its discount window picnic loan programs have jumped the shark again!

A large section of the local mall parking lot has been rented by the nearby Honda dealership which has hundreds and hundreds of new cars almost literally abandoned there. Almost 4 feet of snow in the last few weeks and these cars are just buried and not moving-since late summer. I notice the same thing on a bit smaller scale at most of the dealers in my area. Parking cars in adjacent lots and other properties and not seeming to be moving

You’ll know you’re just about there once your overlords have confiscated Medicare and Social Security, probably in the next year or two.

130% LTV auto loans are available. So ??? I needed a little spending $ so I bought a Lexus. How does this not end badly?

A friend that dwells in the auction lots says volume is increasing at a pretty good clip. Sure its nothing though.

“The New York Fed, in its Household Debt and Credit Report for the fourth quarter 2016, put it this way today: “Household debt increases substantially, approaching previous peak.” It jumped by $226 billion in the quarter, or 1.8%, to the glorious level of $12.58 trillion, “only $99 billion shy of its 2008 third quarter peak.””

So, per capita what is that?

The population of the USA was about 300 million in 2008.

2008 peak was approximately $12.7 trillion.

So per capita that is about $42,300.

Now the population is about 325 million. So per capita now is at $38,700 – so still about 10% less per capita.

If it keeps jumping at $200 billion per quarter, by the 4th quarter 2017 the figures will be. Total debt of $13.38 trillion and a per capita figure of $41,200.

At that rate it’ll take until the second quarter of 2018 to find a comparable per capita figure to third quarter 2008.

Total debt of $13.78 trillion equating to a per capita figure of $42,400.

So given that, I see no reason why there should be a financial crisis this year, or perhaps even next year. Could be 2019 that these things really start reaching their limits.

>> “I see no reason why there should be a financial crisis this year, or perhaps even next year.”

I don’t either. I’m not sure what made you think it was even a topic.

I see auto loan delinquencies rise, which will cause auto lenders to tighten credit, which will hit auto sales, which is the largest sector of retail sales (at 21% of total retail sales), which will be a problem for the economy, but it won’t cause a financial crisis.

>><So given that, I see no reason why there should be a financial crisis this year, or perhaps even next year<

There are so many dynamics in a macro scale economy, that I wonder how we could ever predict a boom or a bust.

Let's take for instance your data on how the population has grown, thus diluting the overall automotive debt. That is a good start, but how do we factor in actual employment participation rates of those 25 million new "capitas"? How about job quality for those gainfully employed? Will they continue to be able to service their debt in the face of stagnant wages and stealth inflation? Finally, I have noticed that attitudes towards debt repayment have changed – to some it's just another video game. You "die" (get foreclosed on or vehicle repossessed" and then are allowed to "respawn" (get credit offers) after waiting a predetermined time span.

I work across the street from an asset recovery company. The tow trucks bringing vehicles IN looks like an ant parade at a picnic. Tow trucks in, car haulers loaded for the auction heading out. Oh yeah, then there’s the police over there on a daily basis to calm the repo-ee or take a report on some sort of problem. It’s a bustling business. Asset recovery wasn’t this hot BEFORE the Cash For Clunkers program was it?

Neoliberalism uses debt based consumption, it works until it doesn’t.

Greece used debt based consumption, it worked until it didn’t.

Max. debt lies down this road.

Has there been any research on %age of delinquent loans due to uber/lyft drivers finally realizing the cost of ownership of their vehicles?

The last new pickup I bought was a 2008 with all the bells and whistles. It was $28,000. The same truck is now $60,000. with 7 year financing. I am a cash buyer so I have bought my last new vehicle.

In figuring per capita, keep in mind that only about half of the population earns income. Children, retirees, students, handicapped, and the poor should not be used in creating averages regarding income. The important people are those who earn enough to be double or triple the poverty line. Another way in some situations is to know the number of property taxpayers. I say this in regard to the national debt, since retiring the ND depends on persons who make enough surplus to be a factor. We are in DEEP debt and we are happy grasshoppers who cannot think further out than about two months and who have memories that only go back to the last tax return. Look out for yourself and make sure that you have a stash of food for trading/bartering. Good luck!

What a scam. The government has given the auto manufactures and dealers a licence to steal by keeping rates so low. 75 month loans, 0% interest rates, bad credit, who the hell cares. I hope the hole car deal collapses. You would have to be a idiot to pay 60k for a pick up.